But there is no Financial Crisis. These are the boom times.

Given Americans’ ceaseless urge to borrow and spend, household debt in the third quarter surged by $610 billion, or 5%, from the third quarter last year, to a new record of $13 trillion, according to the New York Fed. If the word “surged” appears a lot, it’s because that’s the kind of debt environment we now have:

- Mortgage debt surged 4.2% year-over-year, to $9.19 trillion, still shy of the all-time record of $10 trillion in 2008 before it all collapsed.

- Student loans surged by 6.25% year-over-year to a record of $1.36 trillion.

- Credit card debt surged 8% to $810 billion.

- “Other” surged 5.4% to $390 billion.

- And auto loans surged 6.1% to a record $1.21 trillion.

And given how the US economy depends on consumer borrowing for life support, that’s all good.

However, there are some big ugly flies in that ointment: Delinquencies – not everywhere, but in credit cards, and particularly in subprime auto loans, where serious delinquencies have reached Lehman Moment proportions.

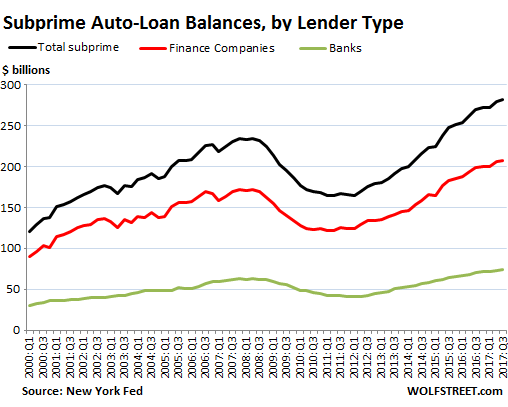

Of the $1.2 trillion in auto loans outstanding, $282 billion (24%) were granted to borrowers with a subprime credit score (below 620).

Of all auto loans outstanding, 2.4% were 90+ days (“seriously”) delinquent, up from 2.3% in the prior quarter. But delinquencies are concentrated in the subprime segment – that $282 billion – and all hell is breaking lose there.

Subprime auto lending has attracted specialty lenders, such as Santander Consumer USA. They feel they can handle the risks, and they off-loaded some of the risks to investors via subprime auto-loan-backed securities. They want to cash in on the fat profits often obtained in subprime lending via extraordinarily high interest rates.

Subprime borrowers are perceived as sitting ducks. They’ve been turned down, and they’re aware of their bad credit, and they often think they have no other options. And so they often end up with ludicrously high interest rates on their loans, which these borrowers, because of the ludicrously high interest rates, have trouble servicing.

Of the $282 billion in subprime auto loans outstanding, finance companies originated 74%, according to today’s data from the New York Fed. Banks and credit unions granted the remaining 26%.

This chart shows the dominant share of subprime lending by finance companies: total subprime auto loans (black line), subprime auto loans originated by finance companies (red line), and subprime auto loans originated by banks (green lines).

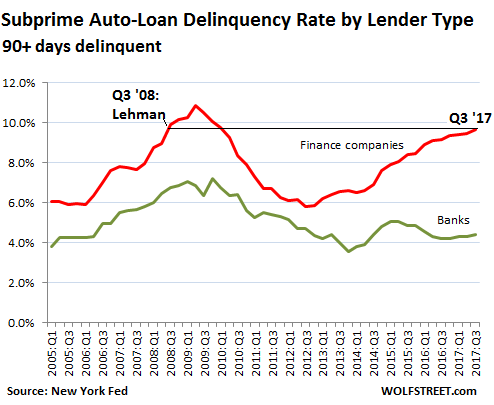

But not all subprime loans are cut from the same cloth. The 90+ day delinquency rate for subprime auto loans originated by banks dropped after the Financial Crisis and has since remained fairly steady. In Q3, it was 4.4%, down from 7.1% at the peak of the Financial Crisis. So the subprime auto-loan fiasco is not going to topple the banks.

In contrast, the 90+ day delinquency rate for loans originated by auto finance companies has been soaring since 2013. In Q3 2017, it hit 9.7%.

This 9.7% is the highest delinquency rate since Q1 of 2010. And it first hit that rate on the way up during the Great Recession in Q3 2008, during the Lehman moment. A year later, it peaked at 10.9%:

The chart above illustrates how banks have kept their subprime delinquencies under control. But not auto finance companies. The New York Fed explains, putting it mildly: “This suggests that bank auto loans may have some additional layers of underwriting – credit score alone does not explain the gap and divergence in the delinquency rates.”

The other way of explaining this phenomenon is that auto finance companies, after years of near-zero interest rates and excess liquidity, and thus an easy way to offload these loans by securitizing them, had practiced loosey-goosey underwriting standards, if any at all.

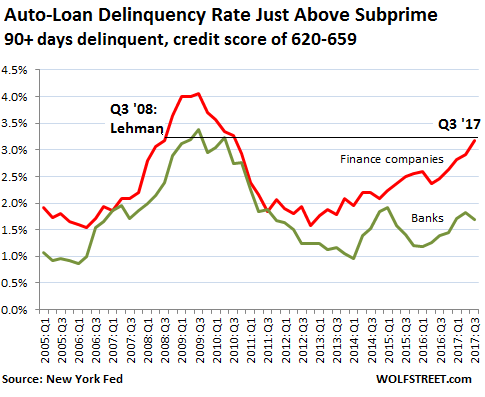

The next chart shows 90+ day delinquencies of borrowers with a credit score that is just above subprime (620-659). And they too have been deteriorating at finance companies since 2013. This impacts $155 billion in loans – $84 billion originated by finance companies and $71 billion by banks. The delinquency rate at auto finance companies of these loans has reached 3.2%, the highest since Q3 2010. And it first hit that rate on the way up in Q3 2008, the Lehman Moment:

But here’s the thing: We compare these delinquency rates to those during the Financial Crisis and the Lehman Moment. But there is no crisis these days, just record stock markets, ultra-low interest rates, a booming bond market, and a growing economy.

Auto-loan delinquencies spiraled higher during the Financial Crisis because millions of people lost their jobs and couldn’t make their payments. Now employment has been rising for years. The unemployment rate has dropped to 4.1%, the lowest since December 2000. These are the boom times. And yet subprime auto loans at finance companies are blowing up like it was Q3 2008 all over again.

And this is not a good indication of what might happen when the economy turns south even a little.

Banks have gotten leery of auto loans. They have started to tighten lending standards for prime and subprime borrowers, and it shows. Read… Next Phase of Carmageddon: the Banks.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Voted!! Worst reply ever.

Nominated!! Post to be deleted ASAP.

Fuck off Tom.

Just send all those extra cars to Australia as we don’t make them anymore. Also send us some specialists to write all sorts of new loans as we are now the second wealthiest adults in the world just behind Switzerland. Asset rich – cash poor.

(“Australia’s wealth per adult in 2017 remains the second highest in the world after Switzerland, having increased by 9.5 per cent to $US402,603,” the 2017 edition finds.)

And we did it all by having some of the lowest wage increases in the past upteen years. Wage growth YoY came in at 2.0% today. Inflation is at 1.8% in the official stats.

Yes but easy to understand – such cheap credit – take it and make autoloan which pays plenty – 4, good loans will cover 1 bad loan give it a go

When investment groups solicit potential qualified investors they ask you to list your assets excluding primary residence, as the inclusion of it can be substantially meaningless, especially in an inflated property market.

While good for government feel-good statistics, ‘wealth’ net of primary residence would be a better guideline. After the last property bubble in the States a lot of people went from millionaire to underwater to out in the street in about 6 months flat.

Yep if you owned a house in this area you were by definition a millionaire. But, tons and tons and tons of people lost those houses, and they literally did just that; went from millionaire to “underwater” to homeless in, yes indeed, 6 months.

Tons of people changed what they do (programmer to guy who makes and sells soap, engineer to VTA bus driver, RE agent who now works at a helpdesk at Ebay etc.) For almost all, it was a big step down – they had to adjust to living on half or maybe a quarter of their pre-crash income.

One silver lining though was that a lot of debt vanished. When you’ve gone from making 6 grand a month to 60 dollars a month – in a good month – well, you can’t even make offers in compromise on your debts. Anything backed by anything, like a house or a car, went when the house or car was repossessed. But there’s tons of unsecured debt, and that just went poof. This even included back taxes, depending on the state the statute of limitations is 5 years to something like 30. California’s got one of the shorter ones.

Almost fun being able to tell the Credit card companies, etc. “Aaaannnnd it’s gone”.

“some of the lowest wage increases”

I haven’t seen a wage increase in decades and that’s nominal dollars, using inflation numbers it’s a bloodbath.

+1 The unemployment rate might be low, but wages have been flat for 10-years now.

Au has one of the highest debt to GDP ratios and the SNB is off the map, printing money to buy US stocks to keep their currency cheap and improve exports. The US and GB have the lowest debt to GDP ratios, probably because the US Fed is not a true Central Bank, and the UK has Brexit. The farther you stay away from the center in the next implosion the better off you will be, and that is these two stodgy old economic powers.

I would differentiate between countries that can feed themselves, and those that cannot. Global trade, and globalization, will be gone in a jiffy, as almost happened in 2009. This time it will be worse.

Been to swissland very recenty and apart from a heap of rock I’ve seen no assets worth any real value with the exception of their amazing railroads and skilifts. BUT TRY buying these?, so as an asset “not for sale “their value is zero! Still, perhaps they have valued all their snow (water) as a commodity asset for sale?

I do some volunteer work helping low-income individuals with tax matters. One client was telling me how guilty she felt because she couldn’t pay her car note, and the car had been repossessed. Her main source of income is public assistance and a bit of income as a caregiver, and she has filed bankruptcy three times. A lender gave her a 7k loan on a car that booked at 2k at 21% interest. How could anyone think that loan would be repaid?

Tote the Note places make money by selling those $2k cars for $7k and repossessing them and selling them again and again.

There’s a 1978 Supreme Court ruling that declared state usury laws didn’t apply to businesses or banks that were “national” and headquartered in other states.

It used to be you would never see 30 or 50 or 100% annual interest rates . . . because Minnesota or California or you-name-it-state protected you by usury laws. Usury laws had been around for a long, long time before the Supreme Court knee-capped them in the U.S.

I wonder at the increasing deference to business on the Supreme Court. I suppose one has to blame it on Congress, which nominates the people who please the donors, not who is best at protecting the rights of the citizens.

‘Protection’ by usury laws simply encourages more attempts to borrow by those who shouldn’t. Lending money regardless of risk leads to disaster for the lender, unless of course they refuse to lend. Presumably the next solution would be to make legislation to force lenders to lend money to bad risks, then bail out the lenders.

Interest rates are a market, not something to be defined in absolute terms by legislation or regulation. Nobody with good credit history has a problem borrowing at market, and bad risks pay more, as they should.

The ability to borrow money is not a right, it is earned.

Don’t worry, after they pass the tax cuts next week everything will be great. You won’t believe how great it will be.

I heard I’ll be getting loads of trickle down benefits, on top of the trickle down benefits from earlier tax cuts several decades ago. Life is good. It’s nice to know politicians are working hard on my behalf.

Kind of gives you a warm fuzzy feeling doesn’t it?

There is nothing wrong with tax cuts. If you don’t want yours, make sure you send in your “fair share” with next year’s filing.

In the United States, the social contract comprising of the various government founding documents and the market-oriented climate of the founding compels citizens to pay for the bare basics and not much more. I’m speaking of the Federal Government. States have more discretion under the federalist system to enact various spending measures according the values of its constituents as long as the process doesn’t devolve into the tyranny of the majority where people vote theft as a reasonable way to secure funding.

It’s not “trickle down” when you receive money back you should not have paid in the first place. It’s called a market-oriented economy. And before there is any rumors of the rich getting tax breaks, last I read the top tier retains the same rate. It actually increases to over 40% for approximately the first $200,000 thereafter before leveling out.

Whether tax bills are good or not is the kind of question on which it’s hard to get agreement. It’s hard to exaggerate how much people’s priorities differ.

However . . . I don’t think it’s a rumor that the wealthy do well with the current bills.

The headline rate you mention is just that, a “headline” obscuring who benefits from the reduction in the corporate rate, the end of the estate tax, the non-taxation of any capital gains accrued to the estate before death (think Amazon stock. You’d never sell, if you didn’t need the money yourself, meaning neither you nor your beneficiaries would pay tax on the gains!), and lower pass through taxes, which will benefit anyone who can afford a few lawyers and who doesn’t work at all for their income.

The cost basis reset of inherited money is a new one and a big one. Previous plans to get rid of the estate tax didn’t have it.

Raymond: “It’s not “trickle down” when you receive money back you should not have paid in the first place.”

Raymond, the proposed tax cuts are paid for by increasing the national debt. This in not money that anybody paid into the system.

It’s time to understand that adding to the debt is not OK.

The national debt is the result of SPENDING. The citizenry are responsible for the basics and that’s it

You forgot to mention the huge 43% tax cut (35% to 20%) in the corporate tax rate that goes to passive stockholders. Given 90% of stocks are owned by the top 10%, I wouldn’t call that tax cut a middle class tax cut.

The only way to reduce taxes for every hard worker is through reductions to the payroll tax rate, and only when it doesn’t add to the deficit.

If you had a push mower would you be envious that your neighbor had a riding mower. A business is a tool to make money. People that make money using this tool have to pay income taxes. Some have to pay this on top of their business taxes. Most millionaires are first generation by the way.

One of the more ignorant comments I have read on this site. The rich remain rich by rigging the,system–and taking advantage of the ignorance of stupid flunkeys like this guy. Whose butler are you?

It’s called ethics. If the world was run by people like you and 95% on this board the United States would look like Venezuela. I’m against the government driving the economy and picking winners and losers. But I’m against people like you who look at others with more and think you have a right to take their private property.

Private property is a right. Healthcare, education, and handouts are not.

If corporations are not people why do they pay any taxes? Rather than blather about a corporate tax that the multinational robber barons don’t even pay due to offshoring and havens, eliminate it and also kill off the qualifying dividend exclusion. Then the income would be taxed at 100% of the shareholders rate. (They should throw in money spent on buybacks onto the 1099s also.)

Every other industrialized country has a VAT because they know that it is too easy to game the system with just an income tax. Americans are too stupid for a VAT because they have the illusion that everybody but themselves should pay for the government.

Problem is that the share for 99% of us is not “fair.”

Remember ‘trickle down’ means the 0.01% pissing on everyone else hence the name of the theory.

It has worked quite well.

Now you know the source of the ‘warm feeling’…………………

I can only translate this as you’re stating that you think Congress/government are better at spending your money as you see FIT than you are. I think this might be an oxymoron, but you are the one who made the comment, so is yours to explain.

No, I’m assuming that he thinks that Congress/government would probably be better at spending the money usefully than the extremely rich. You’re performing the standard Republican trick of saying “Keep your* own money!”

* only applies to richest 1%.

Neither do you know what an oxymoron is.

Ragnar,

You have a bad presumption. The tax cuts do not represent money that was paid into the system because the cuts are simply are adding to the national debt.

It’s a raid on the next generations wealth, plain and simple.

Nobody deserves a tax cut when it adds to the deficit. If you don’t like the spending, cut the spending.

The people who are proposing these tax cuts have no spine. They say they don’t like the spending but they don’t have the spine to propose cuts to spending. Instead, they are proposing debt financed tax cuts. That tells me they don’t care about the debt or the health of the country. They care only about printing money for themselves, as a form of welfare benefit. They want the welfare benefits before others get them. That’s not responsible.

There you go. This is the explanation you asked for. I think we agree in a lot of ways. Hopefully you don’t agree with debt financed tax cuts.

@Bobber

Yes, I think we do mostly agree. I’d just prefer to keep my money in the here and now, controlling what I can, letting the system, which I have only the most infinitesimal way of impacting, collapse as it will. Rather than having it take even more of my money to keep up the facade of solvency.

@Nick

My comment was to Bobber – see the link flow.

Oxymoron: Well, looks like it is two contradictory ideas in one term. So I guess you are correct. Correction: It is a paradox.

The more the debt the quicker the American Empire (800+ military bases world-wide) will collapse and the world will be better off.

I am planning my retirement abroad.

As I’ve posted before Bobber, I’m still waiting on my little bit of trickle!!!

Corporations are very very special people.

Last week Rep. Suzan DelBene (D-Wash.) quizzed a tax expert on this corporate exceptionalism:

“Will a teacher in my district who buys pens, pencils and paper for his students be able to deduct these costs from his tax returns under this plan?” He will not.

“Will a corporation that buys pens, pencils and papers for its workers be able to deduct those costs from its tax returns?” It will.

“Will a firefighter in my district be able to deduct the state and local sales taxes that she pays from her tax return?” She will not.

“Will a corporation be able to deduct sales taxes on business purchases?” It will.

“If a worker in my district had to move because his employer was forcing him to relocate . . . can he deduct his moving expenses under this plan?” He cannot.

“Can a corporation under this plan deduct outsourcing expenses incurred in relocating a U.S. business outside the United States?” It can.

Strawman argument. Any business, corporate or your corner store down the street, can take deductions. Individuals, firemen or billionaire coupon clippers cannot. Some of the changes many complain about like the limitation on property tax deductions and mortgages affect upper income earners the most. Working class earners are not affect because only upper earners pay significant income taxes at all.

People make these ridiculous comparisons to justify a status quo that incentivizes imports over domestic production.

Opponents in California and New York, two states with astronomical real estate values (taxable value) would disagree. In addition, pass through corporations (LLC and S-Corps) will be disadvantaged by the elimination of some current deductions. C-Corps, however (Exxon, Eli Lilly, etc) are insulated.

And with used car values falling due to excess lease returns = sour milk

Here in Canada auto sales have been strong up until Sept… and Oct 20% down… Nov looking to be 40%, at least at the dealers I follow in vancouver

Many years ago, I worked at a home appliances rent-to-own outfit in Atlanta.

They’d rotate employees to every department so we could get a feel for the entire operation; the showroom, delivery, etc.

In Collections, I got disturbed at the number of people that I was calling who were in arrears.

And I asked the manager how that was possible.

“Oh Steve,” he said in the drawl I cherish to this day. “They pay $25 per month for 30 months to get a TV that costs us $200 (1986 dollars – when good times were easy!)

Then he showed me the charts. Defaults were priced in. They could still make some money at a 33% default rate.

“It’s like hounding the physically or mentally challenged, except they’re the ‘financially’ challenged,” I said. “I feel terrible. How do you sleep nights?”

“You feel terrible, I feel terrible,” the manager said with a smile. “We’re in Atlanta. That’s why there’s all these churches!”

Nice post! :)

“They could still make some money at a 33% default rate”

And right there is the rub. I’ve heard that many apartment complexes are so flush with cash because of high rental rates that 30% of the units can be unoccupied and they can still turn a profit. IF…..and that is a big IF, rents really do fall in a big way this fact will crater rental prices.

AND the experts will say “no one could have seen this coming”

My experience with used cars in North Carolina…..the owner did better than the new car dealer…..he had four lots.

Wolf, we are in the market for a new car. Went to several dealers including the local VW dealer. Yesterday I told you about our experience with the Lexus dealer who wanted me to pay the “freight” of $1K because the car we liked came from California to SC.

At the VW dealer the vehicle we liked had the MSRP sticker on the window as per usual. Next to it was an additional sticker with a $3995.00″Market Adjustment” price. Then they wanted to charge an additional $449.00 “processing fee.”

Is this the way things are done now that the car market is on tenterhooks? Charge more? This is a VW dealership. Not the only one in town. Maybe I am getting old.

My brother had a similar experience at a VAG dealership: they tried to charge him ridiculous fees while their lot was overflowing with cars. To add insult to injury the “additional warranty” offered for sale was one extra year only over the two years they are forced to give you by law, and with several restrictions as well.

I’ve heard of VAG and LRJ dealerships elsewhere trying similar tricks to increase the originally tempting discounted price yet I see a lot of their SUV’s around so it means those of us paying attention to these extra fees are a minority.

When a dealer tacks on additional “fees,” “market adjustment price,” or whatever to the MSRP, just let them know that you don’t do business that way and walk out. Don’t waste your time.

That is exactly what I did. Stunning. The salesman thought I was crazy to walk away. Meantime the lot was brimming with vehicles.

He didn’t think you were crazy, its just part of the act. If he doesn’t act that way, the scam becomes too obvious.

I’m kind shocked they let you hit the door.

The car I have now (and the last one too) were certified used cars BUT were rentals……but who cares, the last one is still treating my kid great with ZERO problems…..who, I pretty much gave it to, for what I owed on it……but i did the same negotiation buying each.

And that is, I know what the car is worth, I have a 5 figure down payment and I want a 4 year loan…..they made me sit in the dealer for 3 hours but I didn’t care. As i told them “this is a fair deal, write up the paper work.

paid my car off in August with less than 30K miles so it should last me for the next 5 years easy.

Won’t Touch! VW is in the hole for millions over “Dieselgate”, they will claw all of that back by hook & crook.

This being before entering the deal, the time where all good salespeople are being really nice, generous even, people to be around, then …

Just imagine what happens if you bought the car and they have to service it (or there is a warranty replacement). You will have to sell a kidney to pay for it and they take it out right in the shop too!

You mean like replacing the power steering fluid in a car with electronic steering?

That is one of the scams the Assistant Service Manager tried to pull on a customer where I used to work………..

Or doing a wheel alignment on a car that needs new tires?

Such a wonderful place to work that was – listening to the customers bitch and the managers trying to rip off customers and being caught in the middle.

Dealers and their sales reps and finance people are all actors. They have scripts. They pretend, and typically do not believe their own lines beyond what it takes to sell you a car. (Your Mileage May Vary, there are some more honest people out there.)

One of my favorite sales guy lines is the following, in response to a counter-offer:

“We want to earn your business, we can’t buy your business.”

They are so earnest when they mouth those phrases. Sometimes they reverse the order, and may throw in some gratuitous indignation to try to guilt you into, well, anything. If they sense a willing buyer they also trot out the manager, and then the finance guy, each one with those silly numbers circled on that yellow pad. It is all an act.

When buying a car, remember that you do that once in a blue moon and they sell cars every day. They see people coming and going, they are up on all the tricks, they are not above stretching the truth, manipulating or otherwise doing pretty much anything to meet their sales quotas.

It is easy to forget that dealers are selling commodities. You can buy (or lease) a car anywhere else, often with slightly better responsiveness. In larger metro areas, you may find the same make and model for a different price. At that point, choice of dealer might devolve into a matter of convenience or personal preference regarding any post-sale service needs (a whole other topic!).

One way to arm yourself to do battle with auto dealers is to research beforehand. Find out the tricks and tips. Look into what items are hidden from you, when there are factory marketing funds that dealers may use to supplement purchases, which days of the month might be best to buy, how to see the different prices. A dealer may have a handy printout of its “Invoice”, to counter any offer made by some wheeler-dealer buyer of X dollars over invoice. Of course, that so-called Invoice price could hide myriad details, or just be phony. Caveat Emptor.

Another approach is to work with the dealer’s Internet or Wholesale or Fleet person. Those guys, and they’re virtually all guys, may have more latitude in pricing or may get compensated on units moved in addition to, or in place of, net sales prices or unit profitability. Be sure to ask about any special marketing funds, rebates, supplements, special financing arrangements (say, 1/4 point lower due to You Are Sitting Right In Front of The Guy At That Very Moment) or similar items.

One key take-away is that you will not get what you do not request.

Do not give in to silence. They wait for you to get antsy as you eyeball that shiny new depreciating asset and smell that new-car smell and feel that rich Corinthian leather or synthetic facsimile.

Get a burner email account with a cryptic address and your name not visible, and email several dealers for prices and load terms on specific vehicles on their websites, letting them know you are shopping around. Don’t set foot in the dealership or even give them your name (never your phone number) until you have a deal finalized and are doing the paperwork to take the car home.

“One way to arm yourself to do battle with auto dealers is to research beforehand.”

That is a key issue – knowledge. Make sure that you have researched the vehicle you are interested in, and the dealer invoice cost not only for the vehicle, but any additional equipment offered in various trim lines. I know exactly what the vehicle is worth before I go for a test drive. Once the wife and I have decided on the vehicle, we write a check for the amount we are willing to pay. Once you’ve presented it to the sales agent, they really do not want to give it back, but they really want to try and coerce more out of you. My favorite line they use is “if you need to, we can finance that extra $500 we need to get this cleared through the F&I guy”. I always laugh and point out that it’s not that I don’t have more money in the bank, they’re just not going to get it for that car I was looking to buy. I stand firm and walk if they cannot make the deal work as I’ve offered.

At the bottom the economy is in terrible shape. With all the retail closures many people who were just surviving are now unemployed. All those people with multiple part time jobs may not qualify for unemployment benefits in their states. I can see the desperation in the increasing crime rates where I am.

I just read that Winn Dixie may be the next business to file for bankruptcy, so the downward spiral continues. More job losses at the bottom. With the high food prices, they should be making money.

I was just in a Goodwill and all the cars were fairly new in the parking lot, people are buying clothes there not at the mall, carts full. I was also at the rather high end mall and there’s not much activity there.

I cut through a street on the wrong side of town to avoid traffic on my way to work every morning. A couple of years ago, I saw a prostitute walking down the street for the first time. I’m an IT guy and a little naive about these things, but a young woman in a miniskirt shouldn’t be making eye contact and waving at an old bald guy on his way to work.

Over the last couple of years, I’ve probably seen 20 different women, often 3 or 4 on the same little street. I’m guessing these gals had no chance at gainful employment, started using drugs for fun, and are now in real trouble.

The speed of the deterioration on the low-end is amazing.

” I’m an IT guy and a little naive about these things, but a young woman in a miniskirt shouldn’t be making eye contact and waving at an old bald guy on his way to work.”

Could it be that she thought you were an Uber driver, and was trying to hail you for a ride?

You cannot merely hail Uber drivers on the road, otherwise how can the company use their own metrics to make jaws drop by showing they grew 126% in a single month?

Perhaps she was trying to get his attention to sell him some delicious fresh fruit and vegetables? That’s what roadside vendors do in South Asia, well apart from the miniskirt part.

Low rates, securitization of bad loans, defaults, enabled by brain dead academics guided by economic theories that haven’t been relevant for half a century. Haven’t we been here before?

Credit card debt surged YOY by 8%, the most of any category! I have ramped up my credit card spending over the last couple of years, from maybe $1000 a month to $3000 a month — to get 2% cash back. I pay it off every month. I suspect many others are doing the same, as we move away from checks and cash.

Is this considered “credit card debt”? If so, it may be a big part of why it is growing so fast.

There’s no unified definition, but generally speaking purchases/cash withdrawals/whatever made by credit card which are paid off before the grace period runs out are not considered “credit card debt”.

Credit card debt is usually considered such when interests start to be charged, meaning after the grace period has expired.

@Petunia I have lived in this predominantly Black area for seven years, there have been more than 7 Caucasian families move in in the past 8 months.

There automobiles aren’t matching up with the area, if you know what I mean.

People aren’t eating out here as often either. Texas Roadhouse right down a couple blocks is always overloaded, not in the past 3 weeks.

The traffic has slowed to a crawl in this area, which is definitely drastic, gas prices have people sitting it out in this University city.

Go Pirates!

The little area in Melbourne where I live has completely changed over the past ten years.

The first thing that you will see that is different is number of fancy, imported expensive cars. Never saw a BMW, Jag, or Merc parked in a driveway around here then. Now they are are all over the place. The last house to sell on my side of the street has two BMW’s and a Merc. The house next door has the Jag and the house next door just bought a new AMG 63. Going the other way you find the couple of X5’s and another AMG 63. That is just my street alone.

The other day I was walking the mutt in the village area and there was a Mclaren parked on the side of the road and another day I was being tailgated by a Maserati. The new or generally new townhouses in the village are the ones that usually have a couple of nice imported German cars – gotta move the X5 out of the way so the Merc can be driven.

(Remember that new X5 will set you back A$150,000 or so here….)

The second is that price of houses around here has exploded. Not like in the ritzy, near CBD suburbs where 3 million bucks is normal, but seven figures is nothing to be surprised at anymore in and around the village and the number of houses with listing prices in that price range now makes up around 1/3 or more of the available RE for sale. Even seven figure townhouses are not uncommon. And yes, we have had an influx of Chinese buyers in and around the village area including my street.

The other thing that has really changed is the surge in population and the resulting increase in traffic. You don’t want to be caught in a school zone in the morning or afternoon and going down the road to the shopping centre on Saturday afternoon as that will result in a trip that takes two or three times as long on a weekday and you’ll have trouble finding a parking spot as well.

The population explosion in the and around the village area has been possible by ‘making more land’. This is done by knocking down the single family houses on the 800 to 900 square meter blocks of land (1/5 of an acre or so) and putting up three or four townhouses.

Further out south of the highway (referred to as the ‘breeder’ area by a neighbour) they have not only done that, but carved up the land in all directions and put up houses on stinking little 300 to 350 square meter blocks of land. The price on these houses is about 1/2 of the places in the village area. Where there was nothing but farms and truck gardens there are now endless rows and tracts of houses. You can drive 10 kilometers down south and all you will see is houses.

Looks just like Japan to me.

Going east the situation is just as bad. We used to buy eggs from a free range place years ago. Now there are nothing but houses for 20 kilometers. I haven’t been out past the small town out that way for years and years and once you went past that place it was nothing but open space for the next 40 kilometers or so with a few small areas with 10 or 20 houses here and there.

We’ll have to take a drive out there one of these days to see what it is like now – as long as it is not on a weekday.

Ah yes, Melbourne – the world’s most liveable city………………….

The unemployment rate has dropped

Hmm!?

Would some of the confusion about the actual state of the economy go away if one always remember to separate the proxy for something from the values that once upon a time was supposed to mean something?

Like:

The unemployment rate number has dropped

They cooking the books, everywhere, to “make the numbers” then managing and taking decisions based on cooked numbers, sometimes people and government departments using the very numbers they cooked themselves!

No wonder things don’t make a lot of sense.

The upcoming tax cut seems like a loan distribution to me.

They are borrowing on your behalf and throwing it

off the top of a large building .Giddy up

This. I often wonder if the common folks live in a world of debt because they see their Republican leaders, supposedly figures of fiscal rectitude, making it perfectly plain that borrowing so that you can have more goodies is the right thing to do.

If the interest rate is low, why not borrow. If you cant pay because you lose your job, get sick or other reason – whose fault is it? Lenders take the risk so they should take the hit. Nobody put a gun to their head to lend. The biggest crooks around are the scammers who got the US to bail them out in 2008.

As for the US, when Treasuries lose 50% or more of their value when interest rates shoot up, it is nobodies fault but the lenders who propped up the government with their own money.

Sub-prime and loose underwriting. What could possibly go wrong?A match made in hell.

Credit unions hold the auto loan paper they originate, hence more stringent underwriting standards. Probably exemplifies the risks of securitization (i.e. the loan originator doesn’t hold the paper). The article alluded to this.

“But there is no crisis these days, just record stock markets, ultra-low interest rates, a booming bond market, and a growing economy.” Sub prime auto is a small fraction (less than 3%) of the market (mostly mortgages) that caused the crisis. Even if every sub prime loan defaulted, it couldn’t bring down the economy.

Auto lenders were exempted from Dodd-Frank.

The industry fought tooth and nail for that.

Household debt appears to be growing much faster than household income.

This is ample reason for the Fed to continue its tightening program. Debt growth of this magnitude will lead to a crash soon if it is not curbed.

While I’m glad that banks appear to have avoided the worst of the subprime auto-loans, I’m concerned about the separation between the bank and specialty lenders. For example, do the deposits that my parents have at their Santander Bank help finance the consumer lending arm?

Go to P2P to refinance your loan, and then you can get a second car.

What can go wrong?

The true sign of a healthy economy would be 1;The homeless number falling.2:Tax receipts increasing due economic growth.3:Outstanding dept contracting.Gov. stats other than these ARE PURE FICTION.

Tom,

Especially number one the homeless. It’s sickening to read how people think that the homeless choose to live on the streets.

“Boom times”? Sure, paid for by binging on debt. Meanwhile, delinquencies are piling up as the moral hazard created by the Fed means people have no qualms about walking away from their financial obligations.

“But there is no Financial Crisis.”

To be precise, there is no Financial Crisis for the Financial Industrial Complex. For them, things couldn’t be better.

For the 99% who are their victims there is a Financial Crisis , but speaking frankly, the system is in no way operated for their benefit.

I’m in finance and see peoples credit scores everyday. I believe the credit bureaus have artifically hiked scores in the last year. People with current seroius delinquency are scoring 670-690’s…just in range of where even non-subprime banks will buy loans.

This report illustrates what I have been saying since 2006-2009 (Great Recession) in that individuals rarely learn from history, and often create the repeat of history. After working in the banking industry for a decade and a half; and the auto industry for two decades- I can affirm the propensity for people to “expand” their lifestyle amidst stagnation in wages by use of credit. The real highlight here is the delinquency and default rates in sub-prime. This “category” of borrowers will walk away from debt (auto {collateralized} & credit card {unsecured}) already knowing their credit is how they arrived as sub-prime, and they simply laugh at the lenders taking on the higher risk, in return for the higher interest rates. They default and buy a $1500-$2000 car for cash, then either “keep” the mortgage up so as not to loose the house, or they rent- further reducing any “risk”. Credit Armageddon is closely approaching. And, the traditional credit markets will also feel the effects. The old saying still fits….can’t squeeze blood from a turnip!

All of these increase in debt across the various sectors seem to be about the same as the real rate of inflation. Not sure if these can be called a surge in debt.

I haven’t seen a wage increase in 10 years, but I made my own increase in income. Refinanced in 2011, lowering my mortgage rate from 6.75% to 3.5%, with no origination fee: Boom, $750 per month income increase or expense decrease. Then took a job overseas with my employer paying my rent and utilities. Rented out my house in the US for $2k per month; Boom, another $2k per month increase in income. This enabled me to pay of the mortgage last year; Boom, no more mortgage payment. Now the $2k is all income. Learn how to play the game.

You were lucky, and you grabbed the opportunity when it came, and that’s good. Not everyone gets a job overseas on an expat package where the employer pays the rent (and other expenses). These are sweet deals. They’re available only to a relatively small number of people.

Oh, I forgot the point. Which is if you can’t increase your income then decrease your expenses. I drive a 10 year old car and I never finance a car. If you need to finance a car you can’t afford it and you need to buy used. I don’t see how anyone with “middle or lower” income can possibly expect to get ahead buying new cars every year or two and keeping a Harley in the garage. Live beneath your means it really is that simple.