Even from Japan – whose export producer prices are soaring.

The oil price collapse that started in 2014 pushed down input costs that companies – the “producers” – faced. And producer price indices, which measure inflation further up the pipeline, plunged. But this is over. And the biggest export powerhouses in Asia that have ballooning trade surpluses with the US, show how.

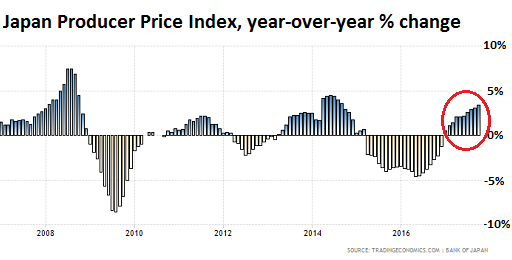

The Producer Price Index in Japan – the “Corporate Goods Price Index,” as it’s called there – jumped 3.4% in October compared to a year ago, after already climbing an upwardly revised 3.1% in September, the Bank of Japan reported on November 13. It was the tenth month in a row of year-over-year gains and the highest annual rate since September 2014, by which time the collapsing energy prices were mopping up any inflationary pressures (chart via Trading Economics):

On a monthly basis, the index rose 0.3% from September. But excluding “extra charges for summer electricity,” the index jumped 0.6% month-over-month.

The biggest movers: Nonferrous metals prices soared 22.4% year-over-year, petroleum and coal products 15.8%, iron and steel 9.7%, and chemicals and related products 3.6%.

On the negative side of the ledger there wasn’t much activity: prices for electrical machinery and equipment edged down -1.1%, for business oriented machinery -0.4%, and production machinery -0.3%.

Export prices in October jumped 9.7% year-over-year in yen terms and 3.8% in contract-currency terms. Export prices of Metals and related products soared 25.8% in yen terms and 17.7% in contract-currency terms. Chemical and related produces soared 16.3% and 11.8% respectively. Other primary products and manufactured goods prices jumped 10.3% and 4.2%. All three of them soared in double-digit percentages just from September!

Japan has exported $101 billion in goods to the US so far this year.

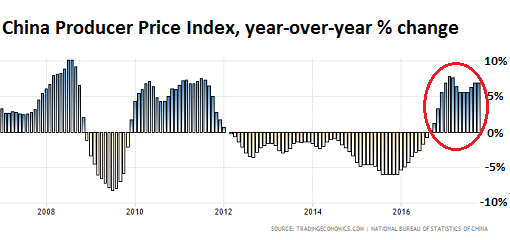

China is the trade giant: it has exported $365 billion in goods to the US so far this year. And its Producer Price Index for October, which was released on November 9, painted a similar picture, only hotter, with a year-over-year surge of 6.9%, the 14th straight month of gains (chart via Trading Economics):

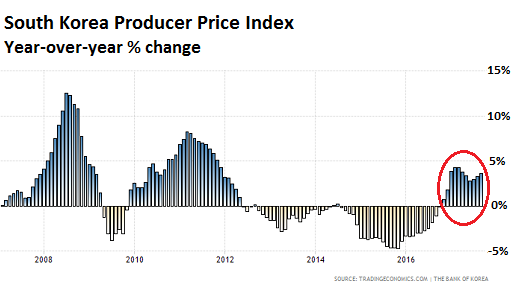

South Korea, another Asian export powerhouse, with $53 billion in exports to the US so far this year, has not reported its October PPI yet. But its September PPI jumped 3.6% year over year, the 11th month in a row of increases (chart via Trading Economics):

These price pressures will work their way into the US supply chain and come on top of other price pressures that have been building up in the US recently.

The Consumer Price Index for September already rose 2.2% year-over-year, up from 1.9% in August, and 1.7% in July. The relief from dropping energy prices has faded. Now energy prices are rising. But the inflation story doesn’t just play in the realm of goods. Prices for services have been rising too, with the CPI for services without energy rising 2.6%. And at the moment, globally, there isn’t a whole lot in sight to push inflation in the US down. But there are a lot of indications emerging, such as the PPI data above, that inflation is in the process of heating up. Bond market, are you awake? Nope, lulled to sleep.

Asset price inflation has already been rampant for years in the US. Here’s Silicon Valley. Read… The Cities in Silicon Valley with the Biggest Housing Bubbles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The price of iron ore has recovered from year lows of just under US$50 a tonne.

I also believe that coal prices are up as well.

Oil – already mentioned in the article.

So the raw materials used in Japanese exports have increased and one would expect the finished goods to reflect that although the yen is trading around the 114 level which is a little stronger.

Yeah, it looks like we are entering the the up side of the commodities cycle.

And where exactly will the demand for these non-financial assets be coming from? Unless we have a war there wont be any demand side to your inflation scenario . I can ask a million dollars for a car, but if no one has any money , no one is going to buy your car…..show me wage inflation and then maybe prices will go up…..right now debt is being used to pay interest on debt…..sounds more like a formula for deflation.

Have you priced a car recently, how much the same type of car costs compared to a few years ago? It’s called “sticker shock.” The relationship between demand and rising prices has proven to be very iffy in the real world. Argentina and Venezuela are great examples of that iffy relationship. They’ve had inflation despite sagging demand. Consumer price inflation is caused by all kinds of factors.

Easy credit has replaced real wage growth. For example, just about anyone can buy a car. Easy credit in turn increases demand and that causes prices to go up. It’s not just material cost that impacts price. We are not headed towards deflation until this credit cycle crashes … again. Reminds me of closing down a bar in my mis-spent youth. Suddenly, the lights start flickering and the party is over. Start bracing yourself for the hangover the next morning.

Chris – Indeed. People must be compensating by taking out 8-year loans to buy their cars or something.

I was just reflecting today that I’m paying twice the amount per square foot for a storage space than I was 5 years ago. Of course I’m also making about twice … $7k to $15k.

The $5 baked chickens in the markets are now close to $10, no one blinks at $1 each zucchini squash, $3 a lb broccoli, or $3 a dozen eggs and they’re $6 a dozen if you want the “cage free” kind.

Bus fares are even going to go up from $2 to $2.25. I haven’t driven a car in so long I have no idea how gasoline prices are or the cost of insurance. I’m willing to bet they’re up.

I saw car inflation measured by the Fed was 0. Was I wrong?

No, you’re not wrong. New vehicle CPI year-over-year (thanks to record setting discounts … and the way CPI is calculated): -1.0%

But remember how CPI is calculated: one year, a rear-view camera system is optional for $1,000. The next year, it becomes part of a standard package, and the base price of the car jumps about $1,000. But because you’re getting more “value,” it means 0% inflation as per CPI.

So prices can surge, and there is no change in CPI. It’s called hedonic quality adjustment:

https://www.bls.gov/cpi/quality-adjustment/questions-and-answers.htm

What happened to the oil glut often reported about 12 months ago? Shale gas drilling is still going strong, no?

According to Baker Hughes the rig count maxed in July and has been flat to slightly tending lower. Remember the shale guys need to sell futures on their oil in order to drill.

Typical market focusing on the wrong number. That rig count excludes the DUC (drilled but uncompleted) well inventory in the USA.

That number of wells is round 5000.

When a DUC is being completed for production that well rig IS NOT included in the BH rig count so in effect that stat is meaningless.

That is why you will see the USA production number increasing even if the BH falls like a rock.

The BH rig count will only have any meaning when the DUC count falls dramatically.

OPEC needs to do more than jawbone, revise demand numbers, and lie about production and storage to keep oil prices up.

IEA slapped OPEC’s demand numbers and oil retreated.

OPEC is the leader in the fake stats business in the oil markets.

Yes, shale output is strong. And there is still plenty of oil in storage. But prices have nearly doubled from the low point.

Actually Wolf we’ve had the strongest inventory draws in the last 3 decades this year. At this rate we would normalize by Q1. The narrative of vast oversupply is quickly evaporating as Wall Street (however painfully slowly) begins to emphasize returns over production.

Gasoline and Distillate are already near or below average and if you look at the EIA monthlies vs the weeklies you can see that my industry is having a hard time increasing production.

The physics of the decline curve are relentless and production in Brazil, Venezuela, Mexico, China, Norway & North Sea et al are all decreasing significantly. GOM should peak in 2018 as legacy investment dries up. By 2019 or 2020 at the latest I expect we will be back in the peak oil narrative and probably from then on. Shale will be hard to replicate in other countries without interested landowners, and our reserves are tiny (<15 BBO); all of the super giants we found in the 40s-80s are entering terminal decline.

Should be interesting to see what the fed does with that inflation. Oil prices did their part to create 2008. We will see how it goes this time.

-A geologist in Texas

P.S. I enjoy the hell out of the site. Thanks for doing what you do!

I’d expect prices to surge up and everyone start talking about peak oil, until folks can’t pay those prices anymore, and they crash (along with the economy). Then everyone will pooh-pooh the idea. Rinse and repeat every 6 – 7 years.

You’d think folks would be more thoughtful about their vehicle selections considering $4.00 gas is in recent memory. But, nope.

Respectfully disagree. I’d guess oil will be lower by end of year or early 2018.

Stockpiles are still historically high, rig counts still high, and US production still high. Technology continues to reduce the costs of extraction and production, while alternative energies continue to grow as a release valve for pressure on oil demand.

“The narrative of vast oversupply is quickly evaporating as Wall Street (however painfully slowly) begins to emphasize returns over production.”

That hasn’t been the narrative since 2016, when oil plummeted. The predominant narrative has been OPEC, Saudi Arabia, and geopolitical issues that should supposedly drive oil higher. The narrative has been overwhelmingly bullish as of late. Meanwhile, speculators long oil are as net bullish as they were in March of this year… which, coincidentally, is right when oil dropped from $55 to just over $40 in a span of 3 months.

In my opinion… this article and your comment might as well have called the short-term top in oil prices. Might go a little higher before they turn, maybe even breach $60, but I think we’ll see $40 again before we see $70.

” Shale will be hard to replicate in other countries without interested landowners” Presumably, they’re interested in making money, and shale resources exist all over the world. So if the U.S. has exploited and vastly increased oil production due to shale, why should this not occur world-wide, depressing prices?

@smingles – technology is a catch all term for “we drilled a longer lateral, and pumped way more sand into it” meaning we got better production but we drilled a way more expensive well to do it. Usually this doesn’t pay off. If you believe the wall street hype about “technology” and have no industry experience you are blind and allowing the blind to lead you unfortunately as most of them do not seem to understand what we do for a living or how it is done.

Even as we burn money they cheerlead. This is not entirely sustainable.

Stockpiles are not historically high, we’ve begun to draw close to the 5 year averages of late. I’m not predicting a boom, but last year shale added about 1 million barrels of oil. Between the countries I mentioned in my last comment production declined by about 1 million barrels per day. So market balance was even overall and we added 1.6 mmbopd of demand. Ergo, massive inventory draws globally. We cant keep up. The world loses 5 mmbopd every year to the decline curve, it took shale a decade to add that much.

@ Robert T – part of the reason shale took off so quickly in the US was that landowners own the minerals. so you can work deals with very self interested landowners who want money and are willing to sign deals in weeks rather than spending years going through a government regulatory and auctioning process for individual blocks. There are plenty of shales around the world, some suitable for exploitation and some not. Most of the world doesn’t have the rule of law, regulatory framework, capital markets and self interested minerals owners to allow the rapid pace of development we have here.

Ask yourself, its been a decade since the EIA published its first map of global shale basins. Fracturing the Barnett is no different than the Bazhenov or the Vaca Muerta. Why hasn’t it been done? The answer is political/social and not geologic. The presence of a resource does not guarantee it will be developed. I think they will contribute to supply, but Russia isn’t going to turn on 5 million barrels of shale oil the way we did.

Anyway, we can all agree or disagree, these are just the thoughts of someone privy to the way major oil companies are currently thinking instead of following the wall street narrative.

@Timthetiny

None of what I said is based on the Wall Street narrative– which is much more in line with what you are saying, ironically. I don’t care for “I’m an insider and know more than you, trust me” either.

“technology is a catch all term for “we drilled a longer lateral, and pumped way more sand into it” meaning we got better production but we drilled a way more expensive well to do it.”

Err, no. Costs are going down. The amount we’re able to extract is going up. Your comment reads like it’s from 5 years ago, when that was true. Basically irrelevant today.

“Stockpiles are not historically high, we’ve begun to draw close to the 5 year averages of late.”

5 year averages… which are historically high. See how that works?

“I’m not predicting a boom, but last year shale added about 1 million barrels of oil.”

“The supply surge from U.S. shale oil and gas will beat the biggest gains seen in the history of the industry, the International Energy Agency predicted.

By 2025, the growth in American oil production will equal that achieved by Saudi Arabia at the height of its expansion, and increases in natural gas will surpass those of the former Soviet Union, the agency said in its annual World Energy Outlook. The boom will turn the U.S., still among the biggest oil importers, into a net exporter of fossil fuels.” – IEA, NOVEMBER 14, 2017 (that’s today).

“Anyway, we can all agree or disagree, these are just the thoughts of someone privy to the way major oil companies are currently thinking instead of following the wall street narrative.”

Again, your “insider” narrative is one in the same as the Wall Street narrative, which is overwhelmingly (and incorrectly) bullish on oil.

We’ve been under a nearly year-long attempt by OPEC (et al.) to collude and drop supplies / raise the price of oil, and it’s been enormously unsuccessful (and unsustainable). It’s barely made a dent.

And while alternative energies have a looong way to go before they make up significant market share, they are accelerating exponentially. Germany went from about 1/20th of their power supply from alternatives to 1/3 in about 10 years. And again… accelerating. China anticipates doubling it’s share of renewable energy to 20% by 2030. That is a massive disruption.

The idea of oil hitting 2008 prices again is farcical, short of a massive unforeseen disruption (like a large regional war in the MENA). Oil was in an insane, fundamentally unsupportable bubble. The peak oil narrative had little to do with oil hitting $150 a barrel.

This should be interesting. Large numbers of Americans have very little disposable income and those that do are too few to compensate for those that don’t. The blood bath in retail is a clear reflection of that.

The producer prices from East Asia may go up, but will American consumers be able to pay them ? I’m skeptical. We’ll have a better idea when we see the Christmas sales, but if they are poor then the first quarter of 2018 won’t be much fun here or in East Asia.

Historian Adrian Goldsworthy in his work on Rome has shown to my satisfaction that size and inertia can carry a corrupt and dysfunctional system a very long way so long as it can muster just enough of its potential resources to fend off complete collapse. Even after Adrianople the Goths couldn’t win (and eventually lost) because if the Romans marshalled even of fraction of the men and money they had at their disposal, they could not lose. The global order run by capital and its flunkies is right now running on inertia and eating its seed corn, but it still has a great deal of inertia and a lot of seed corn to burn through. So long as no huge challenge emerges, it will stagger along, impoverishing and degrading everything in its wake. However, throw in one moderate pandemic or the serious manifestations of climate change and it is headed off the cliff.

Great commentary. To further support your comments, check out Prof. Joseph Tainter, on youtube, describing the collapse of complex systems (aka: “empires”).

My local mall is already in Xmas mode, Santa, trees, everything is out and it’s not even Thanksgiving yet. Parking lot was pretty full too.

I was in a flea market in the outskirts of town and it was an eye opener. I am used to seeing flea markets with cheap imports, but this was different. There was a lot of old used stuff, stuff I wouldn’t even donate to Goodwill. There seems to be a market for really old electronics, media, cooking things, and clothing. It was like stepping into a third world country.

Some serious audiophiles seek out quite old stereos, speakers etc.

Oddly, some of the hottest enthusiasts for tube- powered amps are Japanese.

A scenario – Rates will rise to a point where something breaks with an approx 9 month lag.

In the meantime imports will suffer as the majority are squeezed by higher import prices irrespective of a strengthening dollar.

EM’s having borrowed in $ will see their own problems whilst an export drop, with a lag occurs, and their currencies, with a lag, weaken.

Bonds, as Wolf notes, are slumbering. 2019?

What could possibly cause a problem?

Don’t forget that Americans are great at borrowing more to make up holes in their incomes. So when prices are rising, consumers borrow more, instead of consuming less, at least initially. But there are limits, and that’s when inflation without wage increases will hit consumer spending.

Good to know, but I wouldn’t be so sure about inflationary pressures. Domestic inflation can happen only if demand is not matched by production. Demand can rise if consumers’ buying power rises. This can happen if wages increase more than productivity. Otherwise the increase of some prices would likely only put deflationary pressures on others.

Now, automation and robots are increasing productivity everywhere, worldwide.

Also the value of the dollar may rise, offsetting some of the effects of this rise of Asian import prices, further widening the US trader deficit. If so, Asian countries will go on buying treasuries at near zero yelds to invest dollars that can be printed at will.

Other scenarios are also possibile, the future is not predictable and depends on the economic and political choices that will be taken, as long as many other factors.

No other U.S. government agency enables the trade deficit more than the Treasury Department. Without all those Treasury notes being bought up by trade surplus nations, there could be no trade surpluses. And without someone to buy all those Treasuries, the U.S. couldn’t afford to be in such monstrous debt. It’s a perverse system, which is beneficial to a tiny sliver of the population, but it’s the sliver that controls the government’s financial policies.

There’s a great scene in the movie “Margin Call,” where one banker, played by Paul Bettany, is lecturing a younger colleague about how mistaken Americans are in their perceptions of bankers. Bettany says that Americans want the system to be “fair,” but actually they don’t want it “fair” but want it working in their favor. It’s the bankers, the Treasury, and the Fed that enable the ubiquitous over-consumption (i.e., the McMansions, the fancy imported cars, all the things that would normally be unaffordable).

– But, but, but, but Trump told us he would make America Great Again by …………. lowering the value of the USD !!!

A weaker dollar makes imports more expensive, so if the Fed were to make it difficult for Asian countries to keep their currencies weak, that would be a relatively simple way to raise import prices and inflation targets, because import prices would have to be raised in order for foreign producers to make a profit. But that might hurt banks and the rest of Wall Street, which make a great deal of their profits trading in international currencies, so you can rule that out. While gigantic trade deficits are bad for American workers, they make the financial industry very happy.

You’d have to include the benefits to a substantial percentage of those in the military-industrial complex who could not be kept on the books without deficit spending, plus some percentage of those who receive, directly or indirectly, government monies. You also would have to include the advantage to many of buying much cheaper goods, and foodstuffs that don’t grow here or would otherwise be available only seasonally (I’m looking at you, high carbon footprint vegans). All this adds up to more than a sliver.

Americans are tapped/maxed out. My companies health insurance went up 20% on our 2018 renewal. As the prices of imported goods (is there really any other type?) increase and wages will have to increase or Americans will just purchase less and have to buckle up even more. I see hiring signs in my area and have spoken with owners who are having hard time hiring at current wages. With the various US dependency programs and drug epidemic/college for life, its getting harder finding people who want to work. I think there are many additional factors working which will drive up inflation in the US as well as the commodities inflation.

The advice from the Fed: consumers need to borrow more to deal with higher prices and lagging wages. NY Fed president Dudley said a few months ago that consumers should take out HELOCs and spend this money.

Does not matter whether Americans are tapped out, what matters is whether their credit facilities are tapped out. As Wolf has pointed out, Americans excel in spending money even if they have to borrow.

Inflation in the price of goods (especially imported).

No wage inflation.

How does this end again?

In my white collar work environment I see fast wage inflation for millennials while older workers are pushed out of the workforce.

Fed’s gonna have to hike rates – maybe more than expected – esp. as Saudi’s new leadership squeezes oil market for their own greedy purposes of offloading Aramco (the IPO) into a ‘stronger’ oil market.

But offsetting fiscal policies by Congress (tax reform) & the Administration (regulatory relief) will counterbalance fed’s tightening (I expect)…PJS

It’s amazing how commodity prices rise, asset prices like stocks and real estate soar, yet gold and silver just bounce around an artificial low. The collective energy and level of collusion needed to maintain this must be staggering.

I noticed at Jesse’s Café Américain on Nov 10:

“As the commentators on Bloomberg TV noted, someone literally dumped a $4 billion block trade at market in the gold futures shortly before noon. And as one would assume with such an obvious and clumsy bludgeoning, it knocked the wind out of the price down to the mid-70s. Oops?”

A fair mount of the gold sales in the major markets are “paper gold”, in other words receipts. Those receipts are duplicative, and there is not physical metal to honor them with. The situation arose years ago when bullion was leased over and over again.

In this country each party to the leases had a receipt, but the physical metal was scarce. Much of that leased gold appears to have left the country en route to the Far East. Uncle Sam was perfectly happy to see this because it kept gold prices low. We get more of our national power from the control of the dollar than we do from our armed forces. So,

anything that seems to be a better store of wealth than USD gets Uncle Sam’s immediate attention. That is why I am skeptical about Bit Coin. Uncle Sam can be utterly ruthless when he feels threatened.

and the platinum/palladium ratio. Weird. or gold/platinum. Silver is largely an industrial metal, so does the copper/silver ratio tell us anything?

This thought may have occurred to everyone already but it just hit me: the Fed etc. are puzzled they’ve got real estate inflation but not their 2 percent consumer price index inflation (in Canada the CPI, which excludes housing, gas and groceries, just all you really need)

What if it’s the rise in rents and mortgage payments that is CAUSING the lack of inflation in other areas measured by the CPI by sucking away the money from those areas?

I don’t think the rent increases have been too bad for most of America. It’s only a West Coast issue.

Happy Monday!

My goto line was -you can’t have sustainable inflation without wage increases. Cars have been increasing in price -big time- and their line plant workers wages have gone south . Things have changed and I need to learn much more.

I think you are still correct. In a lot of people’s minds, a $350 payment over 7 years instead of just 5 years is not inflation. And vehicle quality has generally improved, so they can last longer.

It’s different in the clothing and toy businesses.

Chinese die casts have increased on average 30% this year… when quality is kept the same as it was before.

Genuine Honda GX270 engines, made in Thailand, have increased 15% year on year when buying in bulk and 20% when buying in small lots.

Pistons from Taiwan are up 25% year on year.

Just three examples of East Asian producer inflation.

While I am sure higher raw material prices and labor costs have had a hand in these hikes, they don’t tell half of the story. We’ve had these two items spike previously, often at the same time, and price increases were nowhere near as bad.

All production methods are inherently deflationary, every single one of them, from cold chamber die casting to robot welding, and these deflationary pressures tend to outpace wage increases (chiefly due to increased productivity) and to at least partly offset fluctuating raw material costs. That’s the theory and that’s how Apple can keep an iPhone X under a grand in US dollars. Slave labor alone cannot do that. ;-)

In practice these deflationary pressure are countered by inflationary pressures, the chief among which is by far monetary. The ECB has several times gone as far as suggesting that monetary pressures are the core inflationary driver, and they may be not too far off the mark: that’s why their obsession with being able to reach inflationary targets despite constantly changing the rules.

These big Asian exporters have been particularly enthusiastic “money printers”, and now it’s one of those times when the chicken will come home to roost. Inflationary pressures are outpacing deflationary ones chiefly due to the enormous masses of liquidity sloshing through the financial system which cause, well, that inflation that officially doesn’t exist.

Producer price indexes are harder to tamper with because I cannot replace magnesium castings with potato peelings and completely ignore labor and energy costs. That’s why they tend to reflect inflation better than the long useless CPI, but they also tend to follow different dynamics: a cheaper industrial process will weigh far more on the PPI than on the CPI.

So people are willing to pay more for cars because there a lot of

easy money around.

Easy credit, which is the same as money until it isn’t.

The Chicago School of economics, (M. Friedman etc.) maintains that inflation always has monetary cause.

Of course you will run into the usual rants when austerity (cuts in Gov spending with printed money) is suggested but the same week that another SA country (Venezuela?) lost its investment grade bond rating, Chile obtained it.

Plenty of home-brewed inflation as well. I just checked 2018 Obamacare rates for the two of us. Since we don’t qualify for subsidies, our premiums are $17,400 and our deductible is $13,000. This is for the cheapest bronze plan. So, we’d be expected to pay $30,400 next year before the “insurance” pays a dime. Absurd. We won’t.

Imported inflation is deflationary. (A rise in prices causes consumer deleveraging) Prices are rising in Asia because we are delevering (Fed sells assets, ie) while raising rates. High yield bonds are dropping causing inflation in energy prices. Rather than raising the price of imports Asia lowers the value of their currency. The Prechter analysis calls for a worldwide deflation, but there will be pockets of nominal hyperinflation probably, (gold?real estate?) in markets where real shortages cause an absence of sellers of non-margined assets. This blip in Asian inflation could be nothing, or it could result in positive feedback. The item that global currencies are losing value concurrently is hidden by the relative pricing mechanism and by the expansion of the global monetary base, and creates oversupply, which meets falling demand.

http://my.elliottwave.com/resources/free/inflation-vs-deflation_CTC.pdf

Hi Mr Bierce:

But the things that are going up are not imported (services, school tuition, healthcare, rents, housing, food) and this is what people need, not optional. So how does this factor in related to inflation. Hasn’t the rise of credit cards also changed things over the past half century or so as people can buy things without being able to pay? How would they be able to afford a $1000 iphone in the past? Is this factored in to our inflation thinking and does it need to be? Would it be considered, in a way, money creation?

Thanks

Thanks

Inflation of any kind causes deleveraging. We are exporting inflation to Asia, where the deleveraging has far greater implications. Creditworthiness is the measure of wealth. While your credit improves you need less credit, and you spend less. I think some experts believe an improvement in consumer credit translates into more spending, and that is probably wrong.

US has been doing this for decades, it’s the result of subsidized export of employment opportunity in preference of importing cheep goods for the good of the unemployed middle class so they can shoulder more debt and provide a labor arbitrage trade for offshore globalist citizens..

Trade deficit eventually leads to inflation in a normal world but this has been delayed for the benefit special interest groups by using financial engineering.

Condoned and endorsed by Congress, Wall Street and offshore Corporate America. They’d sell their grandma down the road if they could, to support their coke habit..

Technology is inherently inflationary long-term; not short-term. Low cost borrowing makes cost of shale and fracking oil to be low cost.