They get debt slaves deeper into high-cost debts they can’t handle.

[Update, Nov 20, 2017. Did the Cleveland Fed come under pressure from the peer-2-peer lending industry after posting this data? It didn’t say, but I was contacted by a PR firm that referenced the Marketplace Lending Association (of which LendingClub, featured below, is a member) and informed me that the Cleveland Fed had pulled the report and posted this update on its site:Since working paper no. 17-18 and related commentary on peer-to-peer lending were posted on our website on November 9, the authors have received several questions about the composition of the underlying data set they used in their analysis. In light of the comments received, the authors are currently revising their paper to further clarify the data sample they used in the study. Their revised paper will be posted as soon as it is completed.

End of Update]

Peer-to-peer lending commenced in the US a decade ago when investors – now mostly hedge funds, banks, insurers, etc. – could lend directly to consumers via online platforms. LendingClub, the dominant player, went public in December 2014. Shares shot up to nearly $30 over the first few days, but are currently at $4.20, after a 23% plunge last Wednesday when it slashed guidance, and after a 2.4% dive this morning.

Now the Cleveland Fed came out with an analysis that focused on the consumer end of the business, called the loans “predatory,” compared them to pre-Financial-Crisis subprime mortgages because they’re now showing very similar delinquency characteristics, and fretted what these P2P loans, given their double-digit growth rates, could mean for financial stability:

Based on our findings, one can argue that P2P loans resemble predatory loans in terms of the segment of the consumer market they serve and their effect on individual borrowers’ financial stability. The 2007 financial crisis illustrated the importance of consumer finance and the stability of consumer balance sheets.

Loan balances outstanding have soared 84% in four years, from $55 billion in 2013 to $101 billion in 2016, according to the study. Nearly 16 million US consumers had personal loans via P2P lenders at the end of 2016.

Given these growth rates, “the P2P industry has the potential to destabilize consumer balance sheets,” the report said. “Consumers in the at-risk category – those with lower incomes, less education, and higher existing debt – may be the most vulnerable.”

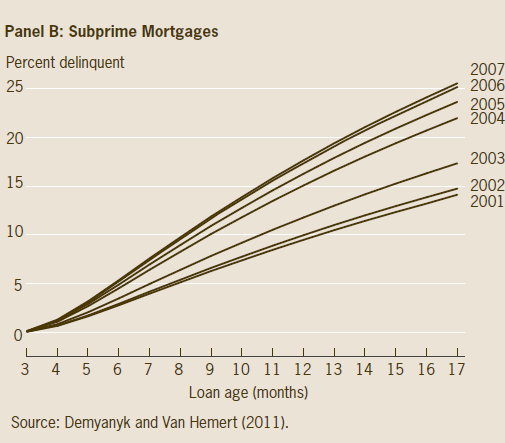

And delinquencies have surged “at an alarming rate, resembling pre-2007-crisis increases in subprime mortgage defaults, where loans of each vintage perform worse than those of prior origination years.”

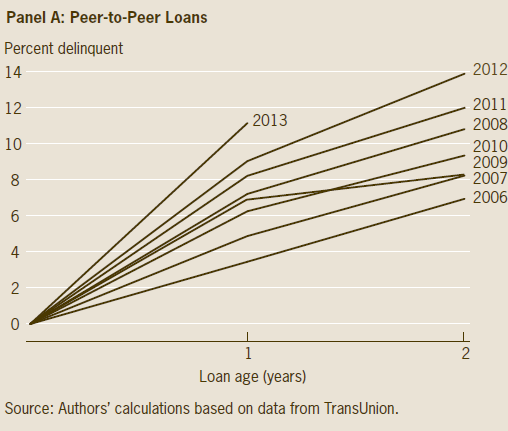

This chart from the report shows the delinquency rates by loan vintage, with each vintage showing higher delinquency rates. Loans issued in 2013, the last vintage examined in the study, show by far the highest delinquency rate after the first year, over 11%:

The chart below shows a similar pattern of rising delinquencies by vintage, but this one shows those from pre-Financial-Crisis subprime mortgages:

One of the most often cited benefits of P2P loans is the idea that consumers take out a fixed-term installment loan via a P2P platform to pay off their expensive credit cards, and keep their credit cards paid off, thus lowering their borrowing costs.

But rates vary, as they say.

At Lending Club, for example, P2P borrowers are categorized by grades A to D, reflecting the probability of default. On average, around 40% of loans are awarded a grade of A or B. These higher-rated borrowers are considered least the risky and are charged 8–12% interest rates. Borrowers with grades C or D tend to be riskier, and their annual interest rate can go as high as 30%. These interest rates do not compare favorably with credit card interest rates.

(I constantly marvel at the absurdity of having these kinds of double-digit interest rates on any consumer loans when the Fed’s target for the federal funds rate is only 1% to 1.25% and when banks pay next to nothing on deposits. But that’s how life is in our special post-Financial Crisis era).

If consumers use P2P loans to refinance more expensive credit card loans to lower their interest costs, then total debt balances of those consumers should remain the same or “if anything” decline, with cheaper loans replacing more expensive loans. But that’s not the case.

Instead, the report observed that total debt balances of consumers with P2P loans were increasing after the P2P loan origination year. It found that on average, within two years of the P2P origination year, balances of non-P2P debt had jumped by 35%.

And in a different way of looking at it, the report found: “P2P borrowers exhibit a 47% increase – rather than a decrease – in their credit card balances after obtaining P2P credit as compared to matched non-P2P borrowers.”

So consumers paid off their credit cards with the proceeds from the P2P loan and then turned around and charged up their credit cards all over again, and now they had both, the P2P loan and credit card debt, to deal with. Hence soaring default rates…

Which takes us to another point that is often hyped: “Do P2P loans help in building a better credit history?”

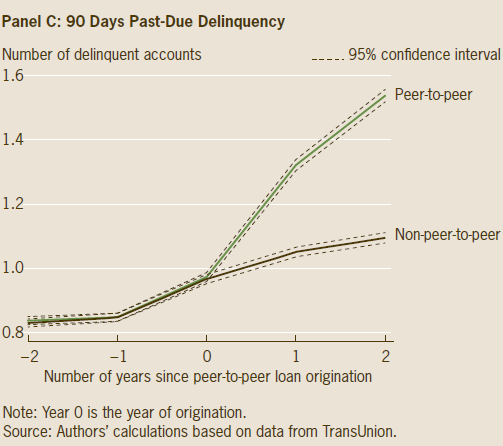

The answer is no. The report found that credit scores dropped “substantially and delinquency rates rise after taking on a P2P loan compared to non-P2P borrowers.” See chart above.

We also discovered that numerous measures of derogatory events (number of past due accounts – both revolving and installment – and number of bankruptcies) significantly increased for borrowers who took out P2P loans. These results indicate that P2P loans have the capacity to worsen borrowers’ prospects for future access to financing.

But consumer borrowing is what’s propping up consumer spending, which is what’s propping up US economic growth – and economic growth around the world. These debt slaves are our heroes. To keep them spending, and borrowing at usurious rates, credit card companies have some special deals for them. Read… How US Debt Slaves Get Trapped by “Deferred Interest”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Are P2P loans generally secured by a claim on some assets=, such as a house? If so, what type of priority might such a loan have in the pecking order of the creditors?

Depends, for Lending Club, the auto loans are secured by …. the underlying auto. But for the personal loans, nothing.

And @Wolf, you marvel at the double digit returns. Why? Lending Club’s personal loans are UNSECURED loans ala credit card loans. I didn’t check the return on ABS backed by credit cards, but the rates should be comparable.

I “marvel” at any consumer loans with an interest in that 12-30% range, including credit cards, not because they’re offered — no, that’s logical — but because consumers actually sign the dotted line and borrow money at these rates.

People who borrow at these rates live from paycheck to paycheck. They already cannot afford their consumption and borrow to fill the gaps. How could they possibly afford to pay 20% or 30% in interest on a significant amount of money?

I just marvel at how people take on these loans. I mean, sure, I understand, people want to buy something, and they don’t want to do the math or think clearly about money or the consequences of that kind of debt, and that’s why they do it, but on some level it just leaves me “marveling.”

Ah I see. That’s Murica though.

Murica proves that higher education is not the answer either, because I am willing to bet that plenty of educated people will belong to the above.

The answer is there are no answers. But I am sure if there’s a real objective study on delusion, Muricans will be numero uno.

Wolf,

Not all of this imprudently borrowed money is wasted. Many times people do it out of desperation. If you need medical care, dental care, or transportation, people feel like they have no choice but to take a chance. My son almost lost his toes to infection because we didn’t have the $175 deductible for a needed surgery. I know people who needed new tires, eye glasses, or dental surgery to keep their jobs. These loans are sometimes an opportunity for some borrowers. BTW, when I needed the money for my son’s surgery we had no access to credit, we would have taken such a loan had we had access to it.

I’ve struggled to understand people’s poor financial decisions as well. At first I thought it was math illiteracy or a lack of math intuition, or what have you, some kind of intelligence missing. Coming to know a number of people repetitively making these poor decisions though (mostly men) I’ve found out many of them are completely aware of the stupidity of many of their decisions but they continue to do the same thing. What I think it comes down to is just gross impulsiveness. Yes, sometimes people do these things out of desperation, but I’ve seen a lot more of people just compulsively spending money on unnecessary things. It’s an emotional thing, blame it on the inner lizard brain I guess, but standard education won’t help them. They need mindfulness training or something.

I find it absurd that the during the financial crisis(es) that the consumer was blamed for taking on too much more mortgage debt–not the banks and debt houses, such as Goldman and Washington Mutual. The only “predatory lending” I see in this article is Visa and Masterfraud. Of course, they never seem to run out of money to lend, even at stupid rates of 30 percent.

Has the *rate spread* ever been wider, Wolf? Banks *buy* money for 1 percent (CDs) and *sell* money for 20 to 30 percent.

Wolf, there is a reason massive credit freezes would end in a big crash. Because if people actually took the time to think they wouldn’t bother to buy many things.

Easy read

https://en.wikipedia.org/wiki/Peer-to-peer_lending

OK Wolf …. Recently over the last 30 days I’ve been seeing advertisements on TV for a type of mortgage I’ve never heard of nor can I find any references to anywhere being offered by a private equity firm here in Denver and the front range

They’re calling it an Asset Management Mortgage … and from what they’re claiming these AMM’s all but pay for themselves ( yeah right )

So what in the h-e double L’s is this new no doubt toxic form of snake oil mortgage ?

And are we in CO the only ones being sold this bill of goods ?

Who is the company offering this? I’ve found nothing on this.

A company here in Denver called AIM ( Affordable Interest Mortgage ) They used to only advertise reverse mortgages for seniors when suddenly this AMM thing popped up over the last 35 days in their advertising .

I’ve looked around their website and they claim these are two different products though I’ll be damned if I can find anything of substance about what this AMM thing is .. other than them claiming its some miraculous mortgage that pays for itself

You can take out a huge mortgage that you can’t afford to pay because you are retired and on SS. Part of the money borrowed is used to make the monthly payments, and part of it is used to give yourself a monthly payment like an annuity. You do this until you die, at which point the house becomes the property of the lender. You don’t give a ratzass because you are dead. Hopefully you die before the cash runs out.

I still have a grand locked up with delinquent groundfloor.com lenders. Groundfloor.com is a P2P lender for home flippers and builders.

I get offers for these loans all the time and I have bad credit. It’s crazy.

Have you checked your credit score recently? Bad credit has a shelf life. If it happened during the financial crisis, it’s starting to weigh less.

None of this is surprising. Rich or poor Americans just love buy crap. I used to do bankruptcy work for a telecommunications company. It didn’t matter what the income level was, credit card debt was through the roof. Your think that a credit card company would stop sending offers to a person making 25k a year with 125k credit card debt.

“Bad Credit” is exactly why you get those, the algorithms have you down as a Mark, a cash piñata, something to smash for good things to come out.

I bet you also get lots of scummy adds from for-profit schools and fee-based resume services – if you don’t have an ad-blocker installed.

There are datacenter’s full of every possible kind of digital predator and parasite – engineered to gouge people who are already under financial or emotional pressure. The more vulnerable the people are, the better their “scam-cores” – meaning even shittier deals are offered to them – because those people won’t have resources to come back after the scammers are done!

https://qz.com/819245/data-scientist-cathy-oneil-on-the-cold-destructiveness-of-big-data/

PS –

Back in the day, 2005, we quite innocently used racks full of machine learning and sensor-fusion to detect a tank, versus a tractor or a car, maybe a soon-to-be broken electrical motor in a plant.

Now, similar algorithms are looking to break people for profit, basically.

This guy gets it.

JP Morgan et all have increases YOY provisions for credit losses (14% in the case of JPM. They have also increased their credit card charge-offs.

Banks are loosening lending standards, without getting adequate commercial borrowers.

CC lending standards for individuals, on the other hand, are tightening.

https://www.creditcards.com/credit-card-news/banks-tighten-card-lending-standards-fed-survey-senior-loan-officers.php

That probably explains why folks are rotating between CCs and P2Ps.

I can’t even get the credit card Amazon offers and my bank will only issue me one of those pre-paid cards if I want to build up credit.

I’ve been operating “outside” the credit system since the crash. I have in fact borrowed about 5 grand over this time, and always paid it back.

I find it puzzling that low-income people, in general, use credit so much. Payday loans, pawn shops, Rent-To-Own, etc. Using credit is scary to me anyway (at least I learned something from the crash) but it seems it should be much scarier when you don’t have much money. Because ultimately it is *your* money and you’re paying 30% or more to use it.

Bring back the tight usury regulations of the 1960s.

“So consumers paid off their credit cards with the proceeds from the P2P loan and then turned around and charged up their credit cards all over again, and now they had both, the P2P loan and credit card debt, to deal with.”

Too many people lack self-control, but I’m thinking that there will be no consequences for the imprudent. Ironically, some say that these people are actually the “wise” ones because the debt will be written off anyway. So what if it hurts their credit sore? Will credit scores matter in the near future?

What about the ECB’s credit score? Mario Draghi has pushed European junk yields below the UST “risk free” rates. How will the repercussion from Mario’s “wise” decision be isolated to the deserving? When the everything bubble pops, what will happen to those of us who avoided racking up consumer debts? Nothing good, I think….

Years ago when I was in the service I used to make the 3 for 5, or 5 for 7 payday loan. I occasionally got stiffed, and if a guy had a hardship transfer I would forgive the debt, but I always came out ahead. People knew they could borrow when they needed it, and so they always paid it on time.

I wonder will all of this access to credit eventually dry up? We are such a debt based society and as living standards fall people will borrow to keep up. Either a crack up boom where the currency fails or a deflationary wipeout. Or maybe we just muddle along?

The end game of the elites is a jubilee. They also took loans, but on highly productive assets. When the masses can’t handle it anymore, they’ll scream to high heaven asking for debt forgiveness for everyone not realizing that the elites will be the one benefiting the most. If you think wealth disparity is wide right now, imagine afterwards where elites own EVERYTHING.

More than once I’ve read that our economy is like laissez-faire capitalism for the workers and socialism for the elites. If you’re an elite, there are all kinds of government programs to make sure you make lots of money (from farm subsidies and on and on) if you get too deep in debt you get a jubilee, your kids are sure to get into the best colleges even if they’re dunderheads, etc. While for workers it’s a life red in tooth and claw, counting pennies, working any extra overtime you can get, 3-hour bus and train commutes, and your kids having to be perfect students to even have a chance to get into the local land-grant college.

This is what I keep wondering about. The level of debt in this country-and the world-is ridiculous. It may seem like there will never be another downturn but economic logic indicates that there will be. Once that happens, many of these loans will become writeoffs as too many people have a negative financial worth and won’t be able to pay. It won’t be just mortgages and autos (where there is at least something to repo) but unsecured debt. I’d like to think that all banks have upped their NPL reserves but I doubt it and the FDIC has little in assets to back up the failures when they do come.

In 2014, I tried investing a small amount with one of these P2P companies and followed their recommendation of small amounts spread over many individual loans. Most loans were under $20,000 and the terms ranged from 3 to 5 years. Now with the majority of the loans reaching maturity, I can relate that not only is this apparently detrimental to the borrower, it was not rewarding to the investor either.

My return was below 4% and the default ratio grows every month.

I did an extensive data mining study of Lending club for a grad project and found that only lendcing club makes any money. They get their fee and you get to gamble on who will default. A and B have the internet rate too low for you to make a good return and the lower grades default too much. You get much better returns with much lower risk in a total stock index fund.

I once used a P2P loan to pay off a BoA credit card. Then I paid of the P2P loan in less than 2 years. So it worked in my case, but I was dead-set on getting out of debt.

Loan consolidation is risky, period. Many people who consolidate debt run up their cards again — whether they use a P2P loan, a personal loan from the bank, or a secured loan. I can see why P2P loans would be the riskiest of all, though.

You have to realize- people are stupid.

Not so much stupid as highly conditioned to be grossly irresponsible and woefully immature. Sophisticated, manipulative marketing has largely replaced culture in the US. Prudence and similar simple virtues are systematically discouraged, while self-indulgence, narcissism, and ignorance are promoted. Deeply propagandized, most of its citizens are as they are trained to be: suckers.

Some are born stupid, some achieve stupidity, and some have stupidity thrust upon them.

Shadow banking is becoming a serious problem globally, eg even the official statistics showed China’s shadow banking scale had increased two times last year, which is why the world had become very optimistic towards China again (vs 2015)……

Just today my wife received a notice from her credit card provider notifying her that the credit limit on her card was cut by 40%. Because she didn’t carry a balance and didn’t use the card enough. Just another upside down characteristic of our cockeyed financial system.

She is no doubt labeled as a bad customer and those need to be removed, don’t they ? And in today’s world she does show very suspicious behaviour, not having used her card balance to the roof ….

Credit card companies are very inconsistent. I have never carried a balance in over 40 years. For several years, I’ve been paying twice a month, with one payment being the automatic payment.

I’ve never had a credit limit decreased, even though I’ve never come near the limit.

I have a card that I haven’t used for several years. They could drop me as a card holder for all I care, but I still get junk mail from them encouraging me to use their card.

I have a FICO score of 837.

No that’s a security reason, if you have a CC you dont use you should lower the limit voluntarily otherwise its a timebomb waiting to go off

Had not thought of that.

Thanks

great article on a different venue for borrowing . It really piqued my interest on this relatively recent phenom , let alone the outstanding amount of loan balances produced from this business model. Since it seems anyone can pony up money for these crowdfunding endeavors. Won’t they be the losers in this game not the borrowers? Maybe we need “predator” investment regs. WR could you do some additional financial journalistic reporting on P2P lending ?

”So consumers paid off their credit cards with the proceeds from the P2P loan and then turned around and charged up their credit cards all over again.”

A guy on (consumer issues) talk radio was bringing this up back in ’04-’06. Of course, the topic at the time were mortgage refis/home equity loans. The repeated questions were ”should I refi/HE to buy a car?” (bad idea, if things go bad you keep the car but lose the house) or ”should I refi/HE to pay off credit cards?” (worse idea, with the plastic ”paid off” new charges rack up quickly).

The only good way to pay off plastic is to pay the bill as quick as possible – to the card company.

I’ve used Lending Club a couple of times. I have excellent credit and secured amazing rates (3.99% and 4.25%) to pay off some credit card debt when I was in a financial bind. For me it was a great option and I am grateful they exist, but I can easily see the trap for people who are worse than I can be with credit. They’ve been sending me offers lately for 5.99% which I would not entertain unless I were really in a pinch. 20-30% is insane, but for some maybe the only option. It’s certainly not as bad as payday loans or car title loans, but yeah if you’re at that level you really need to figure something else out.

I think it might be a combination of several factors that make people take credits with insane rates. Either unability or unwillingness to grasp the real amount paid, or people are used to easy credit and/or they are only interested in the amount to be paid each month or simply pure desperation when they simple can’t cope with the cost of living.

P2P lending is an important part of the “shadow banking” system in China. That means it is not regulated as the stock market or banking is. Besides being a risky place to put your money (I didn’t use the word investment), it is predatory. Earlier this year China cracked down on P2P lending. It’s just a way for Joe Average to become a loan shark while never leaving the keyboard of his PC.

Pre2007 a lot of people got in CC trouble because of medical bills, if you went to emergency without an HC plan they ask for your CC, if you don’t have one they hand you over to Medicaid, they can attach your assets in order to pay for the tests, and if the hospital sees that you are indigent and the state is paying they give the patient every test possible.

Fast forward now you show up at emergency and your CC is maxed out, but you have Obamacare and so you pay the first 20K deductible, or not, you cannot make the premiums, so I assume the insurer hands you over to Medicaid. a much more enlightened system.

With your reference to a “$20k deducible” when you go to the emergency room, you’re trying to be funny to make a point. I get that. And I’m not disputing your point.

But there is no $20,000 deductible under any plan. Period. If you’re covered under Obamacare, and you end up in the hospital, the maximum out-of-pocket allowed under the law, which includes deductibles and co-pays and whatever else, for the entire plan year, is $7,150 (plan year 2017) for an individual. So you as an individual can never be out more than $7,150 per plan year. If you hit that, for the rest of the year, everything else is free, including doctor visits and major surgery. So that’s the time to do your cataract surgery for free.

The maximum out-of-pocket allowed under the law for the entire family – say all four of you ended up in the emergency room – is $14,300. And then for the rest of the plan year, everything else is free for everyone in the family.

These are the maximums allowed under the law. Many plans have lower maximums.

The problem is that over 60% of Americans live paycheck to paycheck with no savings. They get paid on Friday but they are broke on Wednesday. $7000 is like 7 million to them. The hospital would put them on a payment plan. They don’t have a penny to spare now, how are they going to make payments?

You and I can swipe a debit or credit card to pay $7000, but to them it is impossible. They have no assets. If they own a home the equity was spent a long time ago. However, if they work, their wages WILL be garnished.

The Obamacare is not a solution.

34 countries have single payer health care systems.

Anyone interested in a 380 percent interest loan?

https://www.huffingtonpost.com/entry/payday-lenders-democrats_us_5a0a211ee4b0bc648a0d5325?ncid=inblnkushpmg00000009

This sounds a lot like the money lenders in rural India.

Just a comment on human behaviour . . . I live in a housing co-op, we have a member with significant arrears, significant enough that their continued stay with us is at question. They have unstable employment, a shiftless partner, and children. They recently received a windfall from the Canadian government, the result of finally filing their taxes for the past two years and getting back payment on social service cheques that they are entitled to. This amount represented far more than they could save in years of scrimping and saving at their minimum-wage job, a sum that could provide a cushion of security and ease going forward AFTER getting out of debt and securing their place of abode.

Their response? Month-long family vacation in the tropics!

Researching the actual financial behaviour of people, in detail, is enough to make your toes curl.

My father-in-law is a moneylender in rural Thailand — he lends money on land at about 3-5% a month, mostly to people who are borrowing it to pay a job agent for a position working abroad (Taiwan, Singapore, Qatar, places like that). It’s an interesting process to observe, for a couple of reasons:

1) the interest is high, but the actual payment process fairly gentle. The interest does NOT compound, and so it’s basically considered as a large lump sum that has to be repaid. There’s really no such thing as going into default, people won’t pay for months, then show up with a chunk and have it taken off their total. When I asked if the interest compounded, I was basically told that only real bastards charge compounding interest. Thais don’t like that, they consider it unsocial of a moneylender to do so.

2) People often borrow more money than they’ll receive for the total term of their contract — their hope is to extend the contract, or to get overtime. This is kind of irrational — but the option is to continue working as a farmer in Thailand, where you go into debt anyway, buying fertilizer and stuff, and dealing with tiny increments of money for the rest of your life. Borrowing a huge amount and going off to work pouring cement in Dubai is a more active way of losing money, and they do understand that when huge sums are flowing past you, it’s not unnatural that a bit sticks in your pocket.

The internet has been a financial savior to me. Parents and school system provided very little financial education. The financial system has been changing continually since I became an adult in early 1970s. If you don’t self study all the time, you can’t keep up. Old ideas, though valid, no longer apply.

Lived in my car for two years in early retirement to save money. Then bought rural land at housing market bottom, for cash. Now, I could not afford to rent the place I own.

Make do or do without. Better to be lucky than smart. I pray a lot. Many blessings on a shoe string budget.