But household incomes got left behind, even in Silicon Valley.

Ten years have passed since the peak of Housing Bubble 1 in Silicon Valley. In 2007, home prices were crazy. After they began diving, accompanied by a deafening layoff boom, everyone called what had happened before a “bubble.” But in early 2010, the layoff boom flipped around and turned into a dizzying hiring boom, and home prices bottomed out in late 2011, as global liquidity was once again washing ashore.

Now, ten years later, the hiring boom that has created hundreds of thousands of jobs in the Bay Area is stalling. And home prices?

Let’s start with the most expensive Bay Area town first: Atherton, with a population of less than 8,000. Only a few homes are sold every month. Currently, 25 homes are listed for sale on Zillow, ranging in asking price from $2.8 million to $22.8 million. Some of them have been on the market for well over a year (including 945 days). With few sales every month, the median price can be a very jumpy.

For example, Forbes, when it called Atherton the most expensive zip code in 2015, figured that the median home price was $10.6 million.

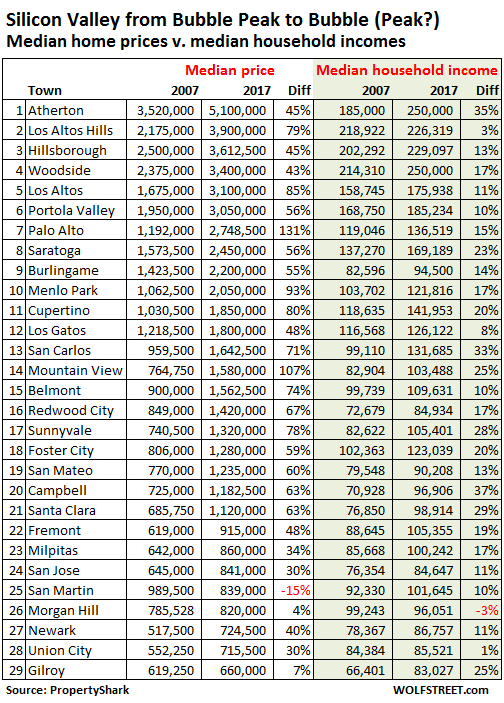

In its new report on the 10-year changes in property prices and household incomes in Silicon Valley, PropertyShark placed the peak of Atherton’s Housing Bubble 1 in 2008. Prices “took a tumble in 2009 and 2010, only to rebound and grow even faster over the following years,” it said. After perhaps a few low-brow homes sold, the median price was at $5.1 million (as of August 31), up 45% from the prior peak.

In terms of income, based on IRS data of “Adjusted Gross Income” (AGI), Atherton was in sixth place nationally among zip codes with at least 1,000 tax returns. Its tax returns sported a median AGI of $2 million.

The Census Bureau, using its survey data set of household income – income from all regular sources, including interest and dividends but not including capital gains and other one-time events – figured Atherton’s household income at $250,000.

So Atherton is probably not the most representative example for Silicon Valley because it is such an outlier in its small size, its sky-high home prices, and its hard to plumb incomes.

A step down, in the second most expensive town in Silicon Valley, Los Altos Hills, the median home price – all prices include single-family houses and condos – surged 79% from peak to peak, from $2.2 million in 2007 to $3.9 million in August 2017. That’s a gain of $1.7 million. But median household income ticked up only 3% over the period to $226,300.

In the third most expensive town, Hillsborough, the median home price jumped 45% from peak to peak, to $3.6 million, while the median income rose 13% to $229,100.

Several steps down, the center of Silicon Valley’s venture-capital ecosystem, Palo Alto, is in seventh place, with a median home price that surged 131% from peak to peak, reaching $2.75 million, while the median household income eked out a gain of 15%.

The seven most expensive cities of the 29 on the list experienced peak-to-peak home-price increases of over $1 million! At these prices and with these dollar-gains, they make San Francisco look like a forlorn outpost in the boonies.

The table below shows these 29 towns that make up Silicon Valley, in order of median home price in August 2017 (data via PropertyShark):

Note that Mountain View, in 14th place, saw home prices more than double from the prior peak, with the median price soaring 107% to $1.58 million, while household income rose 25% to $103,500.

There is only one town — San Martin, near the southern end of Silicon Valley — where home prices haven’t quite reached the peak of Housing Bubble 1. At $839,000, the median price remains 15% below the prior peak. However, household incomes have increased 10%. In neighboring Morgan Hill, home prices now squeaked past the prior peak (+4% to $820,000), but median the household income, at $96,051, is still down 3%.

Of the 29 towns, only eight have median home prices under $1 million. This includes San Jose, the largest city in Silicon Valley. The remaining seven are somewhat removed from the heart of Silicon Valley.

The above table depicts a story of crazy home prices and dizzying price increases in Silicon Valley since the prior peak. This housing bubble, fired up by global liquidity and cheap credit, is by far greater than any other before it.

And it also shows that household incomes – in what has become a national theme – haven’t moved up nearly enough to deal with the surging home prices. These numbers combined form the “Housing Crisis” where even relatively high incomes may not be enough to pay for a modest home.

House prices in San Francisco experienced a record luxury-volume spike in October. But most homes sold are condos, and they’ve hit a ceiling. Read… San Francisco House Prices Go Nuts, Condo Prices Stall

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

10 years from now? Take today’s number and double it? The ability of this country to create bubbles is numero uno.

The ability of this country to create bubbles is numero uno.

“This country” didn’t create the bubbles. The malignancy on this country known as the Federal Reserve did.

Takes two hands to clap. You can lead a horse to water, but you can’t make it drink.

The Fed presents the people with an opportunity and the masses jumped in, with everything, EVERY single time.

Next you’ll say, God created us, therefore we are all not responsible. Hoorah!!!!

Of course we’re not responsible if God created us. He is.

The Fed presents the people with an opportunity and the masses jumped in, with everything, EVERY single time.

The Fed didn’t just “present the people with an opportunity.” By simultaneously debasing the currency with QE-to-Infinity while imposing ZIRP and near-ZIRP rates, it created asset bubbles while simultaneously bilking savers and pensioners out of interest income and virtually forcing them to “invest” in Wall Street’s rigged speculative casino. While the greed and recklessness of individual “investors” – soon to be bag holders – certainly played a central role, the blame for the current asset bubbles, and the systemic risk they pose to the U.S. and global financial systems, lies squarely on the Fed and our political elites that aided and abetted these Ponzi markets rather than acting in a prudent and responsible fashion to ensure sound money and honest markets.

Another central bank-blown Ponzi market hits new highs.

The last bubble outcome resulted in a minor 45% price decline. I expect a much larger decline this time.

Income isn’t paying for these houses. Foreign money and stock options are.

Too right, DM. Back when we worked in the Valley, we knew people who would just walk into the bank manager’s office and plunk down their stock options paperwork. Instant mortgage, no questions asked! Our friends thought we were crazy that we weren’t doing the same thing.

Didn’t they have to make payments on the mortgage?

Before the Gods seek to destroy someone, they first make them go crazy.

I went crazy twice, but I am still here. I guess it doesn’t work all the time.

The obvious solution is Silicon Valley should apply their social networks, big data, cloud and AI technology to resolve this problem.

In March 2003, Apple stock was worth $1.24 per share. Today it is worth $176 per share.

I barely had a modest $10K to invest in 2003. My crystal ball was broken. I only put in $1K and could have walked away with $140K today had I not thought there was a bubble 2 years ago. I had rode the 2001 Tech Bubble up and down. Paranoia has its price.

I know people who had $100K to invest in 2003. Some put a modest 10K in Apple.

They had $1.4M from this investment this year before they rolled it all into a house and paid cash for it.

Some modest tech stock investments bought by the many optimistic lucky are driving this new bubble.

Silicon Valley Old Timer 40 yo Dinner Conversation.

Spouse 1: Dear, do we have enough money in the bank to replace our 25 year old carpet?

Spouse 2: Not enough in the bank with the high cost of living around here but I recall buying some Apple Stock back when I was 25. Let me check on that.

Spouse 2: Woohoo it’s better than the lottery, dear! That piddly $10K I invested in 2003 is now worth $1.4M! Forget the carpet, let’s just pay cash for an overpriced house!

Spouse 1: Sounds good dear. Did you invest anything else in stock back then? Please try to remember what you did with our petty cash back then.

Spouse 2: I seem to recall another 20K I invested in LSI back then. It seems to be worth $2M now.

Spouse 1: It is a shame you have been too busy working the last 15 years to realize you really didn’t have to work at all. We have been such suckers.

Here in Oz replace ‘stock’ with RE.

Like the little Mom and Pop shops on the corner lots in the ritzy neighbourhoods that have gone up in value by 6 figures a year for the past ten years.

The businesses don’t make a cent, but the value of the RE underlying the premises make more than any operations.

All tax free too if the place is your home.

Die and pass it one to your kids tax free as well. No death taxes here in Oz yet.

But with the government here spending just like the USA and running up ridiculous deficits they will be looking for more ways to get money to spend on more ridiculous projects and with the current government making a mess of things it will probably be replaced at the next election. The next government will need more revenue and that is the place they’ll look.

Even in NZ where the conservative government had been doing quite well for the past has been kicked out and replaced by a left wing government which will spend up big, implement more ‘social policies’, and undo all of the gains.

I think a prime example may be the locksmith shop *and* lock and safe museum right on Castro Street in Mountain View. I think the guy got some kind of tax break for having a museum, about the same square footage as his locksmith shop next door, and I’ve gone through it. He shows you all kinds of locks and safes and stuff and has you sign a guest book. Well, he’s retiring or something and selling it now, for who knows how many millions.

This is classic survivor bias. Back in 2003, buyin Apple is like buying Sears today. What was the odd and what would be the pay off?

In 2008, there was a guy working for a company called SiPort (i think ) chain mortgaged several houses, waiting to get rich and he had to shoot his CEO, HR manager and himself when he got fired and lost everything.

When a system encourages gambling and punishes working to accumulate value, it is a system of wealth transfer, NOT a system of wealth creation. It is a moral decay and it will directly reflect decay in currencies and productivity.

Essentially people are saying “the houses were bought by money won from the IPOs of money losing companies”, and median salaries would NOT buy shit. This is the system of wealth transfer. And when you are thinking this is good because you are good at wealth transfer, wait till either you got transferred “from” because only 5% will be winners, OR you are the 5% and the mass will unrest and grab back what ever you have taken. This is how all transfer system ends.

Harvey Weinstein parties like 20 years and he suddenly has to face the consequences.

Good post. Yes, labor-earned income is how most people should buy most things that they need to live. If the only way to improve your living standard is to buy into high risk “investments”, the social fabric breaks down or disappears.

The survivorship bias makes everything seem acceptable. Was Apple stock a high risk investment 10-15 years ago YES! Congratulations to those that took a big gamble that paid off, but it was still a big gamble.

I think that’s part of the reason for the politics around the world today.

Investments of all kinds, RE, equities, bonds, etc., etc., etc., need to depreciate. (And I am an investor).

The average Joe (which includes most of my extended family) is not doing well. You can see it in residential relocation patterns: my middle class Californian family is slowly all becoming ex-Californian.

When a system encourages gambling and punishes working to accumulate value, it is a system of wealth transfer, NOT a system of wealth creation. It is a moral decay and it will directly reflect decay in currencies and productivity.

Bingo. When we have our third market crash in less than 20 years, even the dullest of the sheeple, as they see their 401(k) “wealth” go up in smoke, might finally, belatedly, make the connection between the gang of counterfeiters and racketeers at the Fed and the massive swindles being perpetrated against the hollowed-out middle class.

Great post JZ, quite right!

JZ that’s a genius-level post. And it’s not gonna be the top 5%, it’s gonna be the top 1% maybe 2% and yes we are headed into “to the barricades!” territory.

When a system encourages gambling and punishes working to accumulate value, it is a system of wealth transfer, NOT a system of wealth creation. It is a moral decay and it will directly reflect decay in currencies and productivity.

Exactly! I hope you all winced or hysterically laughed at my post.

If the couple I referenced worked hard and made 100K per year for 14 years, they made 1.4M and paid more taxes than a person who sat on the couch for 14 years and made the same 1.4M on Apple stock. The person who sat on the couch could even deduct their losses from SiPort (if they had invested unwisely and survived). The poor working couple couldn’t deduct expenses for a reliable car, gas, bus fare…. etc required for them to make the 100K per year.

Working for a living has its penalties.

I put $10k in Apple in 2003. I sold it when it doubled to $2.48 and took a $10k profit and never looked back. With the extra wealth I began eating larger helpings of cheeseburgers and French fries. It led to some health problems. I wish I had never made that $10k. Give a beggar $1.00 and he’ll be alive and begging tomorrow. Give him $100.00 and he will overdose and kill himself.

>> In March 2003, Apple stock was worth $1.24 per share. Today it is worth $176 per share.

Should it not be $1760 per share in nominal terms? Apple had a 1:10 stock split between now and 2003

I believe the stock history I looked at had adjusted the 2003 price. ie the price in 2003 was around $11. before the 1:10 split

A successful company like Apple rises to extreme success by disrupting (destroying) the value-creation of other firms. With the rise of smartphones and music services – personal camera sales, retail music sales, and many other vertical markets have been decimated.

The next few years, disruption won’t just be in technology. Millennials will not bankroll the continuation of Boomer’s popular brands and services. Boomers’ spending is declining and will continue to decline, every year. Millennials’ is rising. There are some profound differences.

Because median incomes have not kept up with housing prices,it is only logical that there are fewer households which can afford to buy a house if they do not already own one.So more and more people are forced into rentals.This serves to push up rentals,.The combination of both in turn forces people to relocate to other areas.

When people who currently own houses try to sell their houses ,they find that there are few buyers who can afford their price,so they lower their price.There will some buyers at this lower price ,but fewer than before the housing boom ,because median incomes still are not sufficient to buy a house at even these lower prices.Prices go still lower ,and there are more buyers who can qualify ,but fewer than before the housing boom,because many have left the area.Eventually the area enters a recession .and housing prices crash.It is only a question of when

I have a daughter who works in the tech industry in Berkeley.She would like to stay in the Bay area,but will not because she sees little chance of buying a house.She is hardly the only one.The Bay area risks losing a good % of its young workers to other areas of the country,primarily due to high housing costs

That would be a great example of a free market, ie capitalism.

We aren’t in a capitalist system and haven’t been for a very long time.

The winners are picked.

The fed is the largest real estate owner in America.

They will not allow deflation until they loose control, which may be crack up boom?

It’s a shame that real estate is manipulated so high. The young and the future will be serfs until the system goes back to honest money.

And all the time truth is spoken the millennials, gen x, ect are berated by the ones benefiting from the scam. Sad, open your eyes for our future generations opportunity.

r. cohn – what keeps me in the bay area is not only was I born in California, but I don’t see any improvement in my life if I were to leave. Sure, houses may be $10k in flyover country, but what I’ve seen (I’ve been out there) is the jobs, if you can find one, pay so little that you’re not closer to owning a house than you’d be out here. Impossible = impossible.

Left California after a lifetime last month. Just closed a 120k condo 40 mins commute from Boston (but work is 17). Thing was 178k at the peak, 78 at the dip so I’m pretty even keeled.

Way below 30% a month is spent on housing now. I’ll probably get the down payment amount back in the month or two before the mortgage kicks in… And this job is not a stupid tech contract!

Way better than the 50% to housing and all that CA tax when I lived in San Jose back in 2013.

I’m just upset a few acres to do some truck farming were just a tad too much with the student loans right now.

And this is sustainable… how?

As stated by somebody, a lot of this is attributable to Chinese money. When outside money jacks up the home prices relative to local salaries, it’s time for a foreign buyer’s tax. High tech companies should be jumping all over this. They ultimately have to pay for it through higher salary cost Maybe they will.

I agree with a previous poster, you can’t simply put income beside housing prices and assume a statistical one to one correlation. There are a lot of factors that contribute toward the huge run up in house prices in the Bay Area, income is a big one, foreign money is another, lower interest rates etc.

With so many stuff being on the web nowadays many companies might decide to just have a token office on the valley abd just move the rest somewhere else.

The housing market in the Bay Area has to be poised to fall. If you look at Zillow estimates, many are already below current listing prices, and the number of properties selling below asking is surprising when all I keep hearing from mainstream media, realtors and friends already in the property market is “you have to buy now, it will only keep going up”!

It won’t fall even if interest rates go up. Not on the high end. Most of these were cash buyers who don’t need to sell.

If you mean borrowed cash, you’d be correct.

Nope. I mean cash. Cashing out stock options or wired funds from China. No borrowing required.

Newp. It’s all borrowed cash.

It’s not borrowed. Apple, Google, Facebook book are minting multimillionaires on a daily basis. They may take out a loan like Zuckerberg did but they can easily pay cash. Let’s not even mention Chinese nationals who offer cash on $2M homes like cash is a hot potato. In their case, it is.

Sounds nice but it’s incorrect. It’s all borrowed money.

DM: You seem to know it all. Can you please provide us a source of all that statistics of the percentage of people buying cash vs. hefty mortgages they’ll never be able to pay?

I’ve lived in Silicon Valley all my life and have bought and sold many homes. I work in the tech community and participated in some very successful companies. I have several members of my family in the real estate business as well. I see what I’m describing on a daily basis.

My family has lived here for generations and being in the used house business I’ve bought and sold plenty of these rotting dumps. There are no “cash buyers” and in fact entire zip codes are ARM’s.

http://www.realtytrac.com/news/home-prices-and-sales/november-2015-u-s-cash-sales-report/

RealtyTrac November home sales data derived from publicly recorded sales deeds shows the share of cash sales jumped to 38.1 percent of U.S. single family home and condo sales during the month — up from 29.8 percent in October and up from 30.9 percent a year ago to the highest level since March 2013, when 38.8 percent of all sales were all-cash. The 23 percent year-over-year increase in share of cash sales nationwide followed 29 consecutive months of annual declines in the share of all-cash home sales.

DM, larger investors almost always buy with “cash” because they borrow at the institutional level. Or investors buy with cash and then mortgage the property after the deal is done. They do this because it’s faster and gives them an advantage in the buying process. This throws all this “cash” data off track.

No investor goes into real estate without maximum leverage.

Precisely DM. They’re all over leveraged. Subprime, ARMs and interest only.

Fair enough. But my point remains. They don’t have to sell. They have enough assets to cover the loan if needed.

Of course they’ll have to sell. They’re all using HELOC’s to stay current. It’s the hallmark of uninformed speculators in a global bubble.

I used to think this way for last 3 years and the market has proven me wrong – year on year.

I look at Redfin prices though. The following factors together can drop bay area prices:

1) New Tax law limiting/elimination mortgage interest and/or property tax deductions

2) Tightening of H1B visa

3) Abandoning of H4 spouses to get EADs

At least 2/3 need to happen for houses in the 900K -1.4 mil range to fall since these are bought by 2-income couples most of them on H1B and buying close to take home income. Anything above this range is wealthy, not affected by these trends

What a joke. The price of real estate going up for the ugliest, crime ridden cities such Woodside, Newark, Redwood City, Belmont, San Carlos is amazing in itself, let alone going up that much. It seem as if no one really has planned these cities; they have just build up a bunch of ugly houses wherever they wanted.

San Mateo, and South San Francisco are 2 old, ugly, dusty, dirty, congested counties that I don’t want to be anywhere near them, let alone paying that kind of price for them. You have to be one huge fool to pay that kind of price for real estate in these counties.

Woodside – crime ridden?

Isn’t that where Larry Ellison of Oracle lives? And some other Billionaires/// granted they have their private police (er..security) but never heard Woodside as crime ridden..

Joe Montana (49er royalty) has lived in Woodside for years. So do many tech CEOs. Redwood City has blossomed as tech companies like Box have moved in. San Mateo has a thriving downtown and SSF is booming thanks to the influx of biotech startups.

I don’t think you’ve been to the Peninsula in years by your descriptions.

DM: Say so many realtors. Most parts of Peninsula seem to have been built around 1910 and no one has told these people that after half a century you need to demolish the rat house and build a new one on top of it. Most parts of the Peninsula remind me of movies from before World War I.

Larry Ellison lives in many places “Larry Ellison Buys More Land on His Hawaiian Island, and Now He Owns Nearly All of Lanai. With the report of nine more home purchased on Lanai in Hawaii, Oracle CEO Lawrence “Larry” Ellison may own more than the 98 percent of the island he bought starting with his famous $500 million deal in.” And just because a couple of rich people buy acres of land somewhere and build a mansion in a good part of that city, it doesn’t make the city magnificent. Just drive through many parts of Woodside and you puke.

Some of the other towns on your list are arguably ratty with small, old housing stock in places, but I don’t think Woodside belongs on it. It’s been a wealthy, semi-rural area of big forested lots and big houses for as long as I can remember.

“Woodside is home to many horses and is among the wealthiest communities in the United States. The median household income in the town is $212,917, and the median family income is $246,042”