Housing bubble, affordability crisis “pushed the market to a tipping point.”

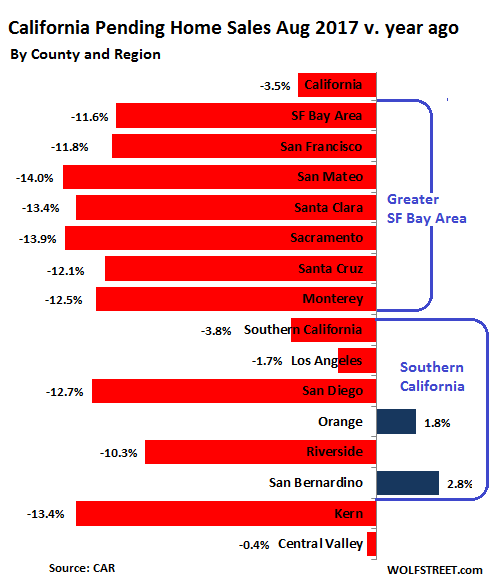

Pending home sales in California fell in August from a year ago, the second month in a row of year-over-year declines, according to the California Association of Realtors, with the Pending Home Sales Index dropping 3.5% from a year ago, after having dropped 2.6% in July:

“As August marks the end of the peak home-buying season, the housing market is showing signs of slowing,” it said. Real estate agents “reported fewer floor calls, listing appointments, and client presentations.”

Pending home sales are notoriously volatile, but the pattern has now become well-established in the San Francisco Bay Area where pending homes sales have been plunging in the double digits year-over-year. And now Southern California is gravitating toward a similar pattern.

The drop-offs are large, and are becoming consistent. This turns pending home sales from an otherwise iffy observation into a worrisome indicator that home sales over the next few months will slow substantially compared to last year.

The biggest problem was the greater Bay Area, with pending home sales plunging 11.6% year-over-year, after having plunged 11.5% in July. It was the 11th month in a row of year-over-year declines. The counties of San Francisco, San Mateo, Santa Clara, Sacramento, and Santa Cruz all saw double-digit declines. Silicon Valley stretches across San Mateo and Santa Clara.

Pending home sales also began curdling more severely in Southern California, falling 3.8% year-over-year, after having inched up 1.4% in July. Only Orange and San Bernardino booked gains. In Los Angeles, pending home sales inched down 1.7%, after still having been in positive territory in July. In San Diego, pending home sales plunged 12.7%, after a 5.8% drop in July.

This chart show the year-over-year changes in pending home sales in August for the major counties and regions. In the list, there are only two counties in the black, were pending home sales increased – down from five counties in July!

Here are the biggest concerns brokers cited:

- Lack of available homes for sale: 35% of real estate agents cited this as top concern, up from 19% a year ago.

- Declining housing affordability/high interest rates: 27%. Confusingly, mortgage rates are still hovering near historic lows, with the 30-year conforming rate still below 4%. Affordability is the combination of home price, mortgage rates, and income. Incomes have come up, but not nearly enough, as home prices have soared. So affordability is dismal, particularly in the Bay Area.

- Inflated home prices/housing bubble: 23%. This is in the same category as the point above, all based on soaring housing costs that many buyers can no longer afford. When potential buyers fall by the wayside, sooner or later, sales will take a hit.

- Slowdown in economic growth, lending and financing, and policy and regulations accounted for the remaining biggest concerns.

The report added that “continued housing inventory issues and affordability constraints may have pushed the market to a tipping point, suggesting the pace of growth will begin to slow in the fall.”

Some more nuggets:

- 31% sold above asking price in August. The average premium paid for those homes rose two points to 12%.

- 37% sold below asking price in August, at an average discount of 12%, unchanged from a year ago. This is an interesting number because much of the real-estate media hype focuses on homes that sold above asking and ignore the larger number of homes that sold below asking.

- 23% cut listing prices in August in order to get someone to bite.

- Multiple offers: The portion of homes that received multiple offers dropped to 60%, from 62% last year. The number of offers edged down to 2.7 on average. The portion of homes receiving three or more offers dropped to 38% in August, down from 42% a year ago.

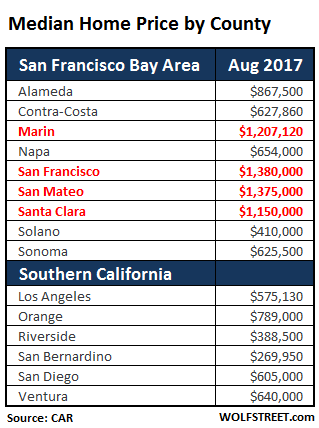

So how ludicrously high are home prices in the Bay Area compared to Southern California, where prices are already very high? (Data via the California Association of Realtors’ August report):

Even in a market with many high-paying jobs, such as the Bay Area, there are limits as to what kinds of prices this market can bear. The sky is not the limit. The first thing to react is sales volume – and within that category, pending home sales that will translate into actual sales over the next few months when most of these deals close. And it’s not a propitious signal.

Mortgage lenders are complaining about falling demand for mortgages and rising competitive pressures, but they’ve re-discovered a fix. Read… Lenders Loosen Mortgage Standards, as Demand Falls

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, the reason most mortgage providers are loosening standards is because FNMA is actually loosening standards. Most banks underwrite to FNMA guidelines so they can sell off the debt (called QM loans, or Qualified Mortgages).

I don’t know that this is as much of a story as people think it is (though I don’t like the debt-to-income percentage being pushed from 45% max to 50% max. Spending 50% of your GROSS income on housing and debt payments is ludicrous, especially when the economy has room to sink, but so is spending 45%).

When Silicon Valley blows up, housing price in San Francisco will be cut by at least half.

“When Silicon Valley blows up …”

You expect … Apple, Alphabet/Google, Oracle, Facebook, Intel, NVIDIA, Salesforce.com, Uber, Netflix, Splunk, Adobe, Symantec, Hewlett-Packard Enterprise, eBay, PayPal, Wells Fargo, Visa, Chevron, Tesla, Lockheed Martin, Genentech, Agilent, Applied Materials, Cisco, KLA Tencor, National Semiconductor, Xilinx, Brocade, Palo Alto Networks, …

I can go on: https://en.wikipedia.org/wiki/List_of_companies_based_in_the_San_Francisco_Bay_Area

… to all blow up? I expect you to take a massive short position in all these companies immediately.

Sv hous8ng has busted 40 percent last time

If it happens again it’s not gonna be surprising..

A lot of these companies have valuations because of cheap money

Let’s see what the future brings in

Well, we have (lies, damned lies, and) statistics, charts, anecdotes–first person and otherwise–and, lord knows, lots of opinions and guesses. This reminds me of the old joke about the deer hunters who all shot and missed, but figure if they could just average all their shots they’ll get a kill.

Can we agree no one knows what will happen in CA; in a way, 6 or more different states? My guess is the current situation is not like the dot com boom–the companies I cited earlier are stable and, for the most part, profitable, and not likely to ‘blow up?’ Others, like Uber, may be fluff but may also pan out in as-yet-unknown ways? We will likely stumble along, with an inordinate number of out-of-staters following closely, until an external event–another debt ceiling fiasco, or war with North Korea, or ?–causes a serious stumble? Does anyone really believe that if a serious financial or other catastrophe befalls California–the world’s sixth largest economy–the rest of the country will be unscathed? No one in North Carolina lost money in the dot com boom, or a house in the financial crisis? We’re in this together and, like it or not, the US needs California to succeed.

California Bob – I’m at least as patriotic a Californian as you are, and I agree with what you’re basically saying. But an awful lot of our economy *is* fluff right now. The overpriced house, many of them poorly built, and as for the tech companies, on Reddit a while back someone came up with a little program that substituted the word “cloud” for the word “butt”. I think it was called the cloud-to-butt filter or something. Just using that in your mind makes many business names here hilarious. “Put your data on the butt”. “Electric Butt” and so on. We *do* have a lot of fluff that could easily blow away on the financial winds.

I expect the entire state to implode like it does every few years.

You are talking about major corporations that have been around for a while. Most people I know work in start ups writing software that nobody will miss. These companies have sprouted all over the place since 2012. Just as they did in 2006 till 2008. These companies are a function of money and they make no bones of burning through the cash at hand. The big corporations you quote are for profit and they give very little freebies. Oracle, Visa, eBay are all 9 to 5 places that are very business minded. To identify a start up, ask if they get free breakfast, lunch etc.

Even with in these corporations, they have recently added departments that are supposed to function like start ups. They are well funded and work on projects that are completely aimless. Expect them to fold once the start up fad is over. For example, before big data, a way to identify bubble in the works was to look for data analytics projects. You knew the bubble was over when these projects were scrapped.

The big corporations have employees that are usually lifers or they have a bunch of H1Bs waiting for their green cards. The former usually own homes and they are not in the running for new homes or rentals (their pays are lower than market). The H1Bs are the ones who have no clue about the price history and many Indians see a house as a form of investment, whatever the asking price.

The H1Bs impact the rental market the most.

In any case, big corporations are also tightening belts. Visa, for example, is now regularly laying off people (most are contractors, so you won’t hear them getting laid off) and is asking employees to relocate to other offices.

The way I see it, fed withdrawal of 10B a month will probably impact the start ups, which will have a bunch of H1Bs leaving the place overnight. A good way to know the gig is up by looking at ads on how many cars are up for sale. This will impact the rental market a lot. For example, I see H1Bs living 4 to 8 in 2 bedroom condos. They all drive audis, bmws, and Mercedes, brand new ones, but will live huddled up. On a side note, the new cars are a fruit of the subprime auto loans, imo. Once the start ups fold, or corporations send contractors home, these H1Bs will relocate to other such groups and consolidate. How do I know? I lived with people like these for a while and a roommate would be gone just like that.

Will the housing prices fall? Not unless the Chinese stop using the homes here as a tool to launder money or our IRS decides to enforce some laws. I don’t see either happening, but the hope is that once the rental market cools, those who are buying homes as investment property will not stop buying at such elevated prices. Arbitrage should dictate that home prices fall. This is provided that the deflation in start up jobs is sufficient to not provide alternate demand for the homes that are becoming cheaper at that time.

Chinese are already defaulting everywhere. Most if not all of them financed using ARMs and downpayment assistance(loan).

wow. my hair is blowing out behind me.

Remember the telco industry? Did you expect on the equipment provider side Nortel, Motorola, Lucent, Alcatel, Marconi, Siemens all to merge and effectively vanish?

Facebook – may be profitable but price / earnings assume stability and growth but regulatory attention can change trajectories as IBM learned decades ago. Wells Fargo faces a double whammy from financial sector pressure and governance. Visa is under pressure from alternative payment providers.

Intel has been struggling as already a while ago their decade long tic-toc release rhythm had to be extended and just recently they seem to run into problems transiting to 10nm. Intel is a bell-weather company for semiconductor based tech. They stumble others fall.

Tech has a bright future but semiconductors/software which is key in S.F. is facing headwinds while renewable energy, battery, electric car and fixing infrastructure all are clamoring for attention.

I think “blowing up” can be interpreted in a number of different ways. And yes, some of the companies on your list are blowing up others are slowing down while others are still growing. Bay Area hiring has slowed down considerably, a fact studied in a few articles on this website.

Let’s come down back to Earth,shall we? an Economy,even California is comprised of a little more than software geniuses and spoiled Apple/Google employees. Try and step out of your limited little high tech Bubble and open your eyes and you will see: Gardeners,Sales Clerks,Teachers,Handymen,Car Salesmen etc etc. so please spare me the “California is invincible” Story. i have lived here since the 70s and have seen several Boom Bust cycles unfold and the Downturns where brutal every time. this time is different because of Fakebook you say,really?

California budget 50% if from Bay Area tech salaries

personal income tax…seems unsustainable

More evidence Silicon Valley is going to ‘blow up,’ any day now, just you wait and see:

http://www.mercurynews.com/2017/09/29/exclusive-microsoft-buys-north-san-jose-land-campus-eyed/

SV housing blew down 40% during the last minor correction. The forecast for the current correction is much deeper…… say…. 65% lower.

I’m unsure if I should feel some sense of sympathy?

Naah. I’m a bay area homeowner (inherited house) planning to sell next year but this nonsense must end. Let the bubble burst and I’ll sell at a fair price. I do hope house prices come down in the central valley where I want to retire. They have shot up in the last six months…I wonder why?

“I’m a bay area homeowner (inherited house)”

I don’t know a single person that has bought a home since 2010 they all have inherited them. I don’t know a single person that can afford to buy the home they currently live in….one guy even said “I couldn’t afford the taxes at the current home price” He bought that long ago and is on a fixed income…….he will die there….no matter what the fuck happens to his hood (he hears gun shots every weekend….northern Anaheim) he is stuck there for life.

Yeah, I made sure to include that detail. I came back to the bay area in 2008 (I was born here) after living elsewhere for 15 years and couldn’t comprehend what was going on then, and I don’t now. I don’t know ANYBODY who has the money to buy here.

Gender X – Everyone in my family who has a house now – 5 out of 5 – married it. Parents screwed up (moving to Hawaii will do that to you) so there was nothing to leave any of us. There’s a nonzero chance I may inherit some piece of a multi-million dollar place in SoCal, but I’ve learned how to hold my breath.

So far the only inheritance I’ve gotten was 10 grand back in the early 90s. I used half of if to pay off the last of my college loans and some to buy my first car, and a few odds and ends.

Very few people in California get major things like houses by working for them. It’s like trying to empty your local lake with a teaspoon. You inherit them or marry into them.

Oops!! 2 out of 5!

Prop 13. Thanks for the lack of affordability in CA…

I don’t think you understand Prop. 13. Prop. 13 actually LIMITS how much your property taxes go up each year. So, if your house doubles in assessed value, say it goes from $100K–taxed at 1%–to $200K in one year your taxes will not double, they can only go up 1%/year. If you sell your $200K house, the new owner will start at a tax rate of 1%, or $2K. More than you were paying, but not excessive compared to some other places:

https://en.wikipedia.org/wiki/Property_tax_in_the_United_States

The ‘damage’ done by Prop. 13, depending on where your sympathies lie, was the loss of a massive tax base that funded our (once world-beating) schools and other public services (yes, and public servant benefits and pensions).

Of course one of the reason for low inventory in cal is prop 13..

Other people may say whatever they want .. But one of the reason for sure

“Of course one of the reason for low inventory in cal is prop 13..”

Incorrect, but I understand the confusion. Property taxes are assessed at 1% at purchase, Prop. 13 only limits tax growth while an owner lives there. It’s the step up in taxes, not Prop. 13, that keeps people–who plan to stay in the BA–from selling their starter homes for better homes, thus limiting the supply of starter homes.

Example:

You buy a house for $100K; you will pay taxes of $1K/year the first year and Prop. 13 will limit your assessed value increase–hence your prop. tax increase–to 1%/yr, even if the value of your house doubles every year (for, say, 3 years to $800K). When the new owner buys your house for $800K, s/he will have to pay taxes on the 1% assessed value, which will be $8K/year, more-or-less.

What DOES limit affordability is one of the arms of inflation: If you’d like to take your $700K profit–I’m ignoring cap gains taxes for this example–and buy a bigger, better house for $800K you’ll be stuck with 8 times the prop. tax. THAT’S what keeps people from ‘moving up.’

Logically, the solution is to sell your $800K house, and move somewhere where housing is cheaper; e.g. where a $200K house is as big/nice as the $800K house in the Bay Area, and fund your retirement with the ‘leftover’ $600K.

I wake up every morning, grateful to be out of San Francisco, The Valley, the Bay Area, California.

I am GRATEFUL everyday.

” I do hope house prices come down in the central valley where I want to retire.”

California is a huge state, and the CV covers most of it. Some areas, like Sacramento, have experienced housing appreciation but others–Stockton comes to mind–have not. Modesto, where I’m from and my parents live, has not experienced major property appreciation, and I pay attention to it as my folks own a significant amount.

Better think this through; the CV isn’t for everyone. I lived there through high school to my late twenties, and plan to move there, but I know what I’m in for. If you haven’t experienced a whole year of weather in the CV, you should know the winters are foggy and dreary, and downright depressing, and the summers are hot, dusty and smoggy. Spring and fall are OK, though.

I lived in Chico for 15 years so I know some of the cons. The north valley is a frying pan in the summer, house prices have always been inflated, jobs are scarce and low paying, and a recent survey revealed Chicoans to be the unhappiest people in the state. What’s not to like? At least we don’t have Valley Fever.

“The Central Valley isn’t for everyone” LOL, no kidding,coastal Californians pay extra for Airline Tickets just so they don’t have to drive though it,unless of course you enjoy the smell of Dung fertilizer and are able to converse in spanish. i’ll take the long way through Death Valley and enjoy every minute….

NO DO NOT.

Not sure for what. Cali just has an unhealthy housing market. We let prices surge until normal people cant afford a home, aside from the well off or those trading a home riding the wave.

I am happy to hear demand is finally falling due to the stupidity of price appriciation, but I am no confident it will result in price drop. There may still be bullshit moves lenders and Realtors can make to build up a bigger crash.

If history is any lesson.. socal has seen many boom and bust cycles

Each time people thought this time is different :-)

“… Cali just has an unhealthy housing market. We let prices surge until normal people cant afford a home”

No one ‘let prices surge.’ California is not a command economy–well, maybe just a little–it’s the law of supply and demand, aka Econ 101. Now, you can argue that NIMBYism and zoning laws contributed to higher demand, but not many of us want to live in another Los Angeles, and every community has at least some of those.

Feelings are not required for this article :-]

Bay area is screwed due to new construction in the city coming to market over the next few years.

Socal will be fine and stable, not much building of condo complexes going on there esp North county San Diego and South county OC

If by stable you mean a dead market with falling prices because thats exactly whats happening here.

Not in the two socal areas I mentioned. My condo went up 30k so far this year and my mom’s went up 50k this year. Prices ain’t falling that’s for sure. There’s literally no supply in the 1-3 bedroom range

They are in this San Diego. Not to mention the for sale signs growing like weeds.

Supposed value before you sell is not the same thing as what you can actually sell it for.

Prices not falling in sd yet

But it does not mean that price won’t and can’t fall

The problem is affordability in San Diego

Median household income is 63k and median price is 540k

Let’s see how long this goes on

They’re falling here in SD. A pretty good pace too.

Prices aren’t shooting up in San Diego. Seems like less is for sale than last years summer, but what is for sale has gone up massively in price in just a year. Average condo in my area jumped about $50k…

Selection in the starter home range is shit.

I agree..

I see the same thing which happened during last time as well

Let’s see what the future brings..

“not much building of condo complexes going on there”

I see the exact opposite in my area, construction is everywhere.

Maybe the conditions are not the same but this is how it began about 2006.. My friend lived in Kingman, AZ who had her home for sale and all of the Calif. folks who signed contingencies on her place couldn’t sell their homes back in Cally.. If past is prologue then anyone who feels some sense of satisfaction against profligate Californians as a kind of justice might just find themselves in the same leaky boat.. The old adage that real estate is local was true until it wasn’t..

60% had multiple offers and 30% went for above asking. Still sounds like a very hot market.

If by hot you mean there is very little attractive housing for sale so when something even halfway decent pops up buyers fight over the scraps…

There is plenty of houses for sale, just no interest. Now rents and prices are falling.

I am from San Diego

I do see good houses but priced insanely

Decent homes are snapped quickly

So am I. Nothing selling and for sale signs everywhere.

Where do you guys live in SD County? I don’t see all these signs. I used to drive through SD as a teenager on the way to surfing in Baja. We would drive across the lagoons and I thought “I wanna live here someday.”

I will ask this question to the coastal Cali residents… where is your second choice to live? For me, that is a tough question.

Or… 40% had only one offer, 37% sold below asking, and 23% had to cut their asking price before anyone even got interested.

This does not include the many sellers who pulled their home off the market because it didn’t sell, then relisted later at a lower price. This is a home in my neighborhood:

– First listed in October 2016.

– Listing removed in Dec 2016.

– Relisted in January 2017 with a $411,000 price cut (decimal in correct place).

– May 2017, price is cut another $613,000…

– In July, listing was pulled.

In other words, during the year when they’ve been trying to sell this home, the price has been cut by $1.02 million, and no one bought. This may go through a few more iterations before it sells. If it sells, none of the prior listing prices and price cuts and relistings, will make it into the CAR stats.

There are a lot of sellers that go trough this process, trying to find the maximum price, aiming high and having to lower their sights.

In August, only 402 homes sold in San Francisco. This was down 29% from August 2012 and 25% from August 2013 and lowest August volume since the end of the housing bust.

There are plenty of real estate markets around the US that would like these “problems”. I’ve been selling homes for the last year in slower markets and having 30% go above asking while others are trying to find the top ….Although it’s cooling off, it’s still pretty hot.

Yep slightly cooling off but still hot. And that’s good I don’t want it to keep going up so fast lol. I want it more steady slow grind up.

Keep in mind that there’s a game played in the Bay Area. List prices are set ridiculously low in order to incite a bidding war. Given the custom here, I’m surprised the over-asking percentage isn’t higher.

Yet prices are lower today than they were a year ago.

There are no “bidding wars”. The narrative is solely the creation of housing pimps in the media.

Wolf

Notwithstanding the dramatic drop in the referenced property–I wonder if these are drops from insane to simply ridiculous. I watch the South Lake Tahoe area and I can’t tell you how many listings are priced at double or even triple what someone paid three years ago. One in particular sold for $145k in 2014; asking is $459k today. If the owner can get $250k it’s a GREAT 3 year return.

I attribute this absurd run up to the H&G channel. Too many Flip this House shows.

Only 402 homes in a month?

Here in Melbourne we AUCTION off over 1000 homes in one weekend during the spring selling season with about 75% of those selling.

That number doesn’t include the private sales either.

And compared to SF our prices in Melbourne in most areas are cheap as chips too.

SF with a population of about 835,000 is just one of the cities in the Bay Area. So you cannot compare the City of SF to big cities anywhere. It’s a small place. I can walk from coast to coast in less than two hours.

Yes a lot of prime London is seeing these ‘run for the exits’ kind of drops by the (mostly foreign) speculators.

Trouble is, there’s no buyer for these properties at any price. Non-hedgie/stockbroker locals can’t afford them even at 75% off, and the Russians and Chinese of course start looking for other ways to launder their money and/or evade their taxes. Their capital starts looking for the next asset bubble to pile into – at the moment that seems to be ‘tulip bulb’, utterly worthless startup cryptos.

2018’s going to be fun.

My wife and I bought a house (2bd, 2bath, 1/4 acre) in Manhattan Beach for $699K in 2001, we sold it in 2015 for $2.1M. The prices exploded when Google moved into the area. Now you can’t buy anything at any price. I’m now looking at St George Utah, where I can buy a 4 bed, 3 bath, two acre, outstanding view… for $644k

Los Angeles won the first place award…. we have he worst traffic in the world! We’re #1, We’re #1…. sigh!

I’m based in Sonoma County and last week my office closed 12 deals.

Two sold at the list price, three for more (2-3% more) than the listed price and seven sold for less than the list price.

Not much less, about 5% on average.

This is the final listing price and not necessarily the original list price.

It would take a heart of stone to hear the heart-rending wails of the FBs who bought insanely overpriced housing using borrowed money at the peak of these insane housing bubbles, and not laugh as their “investment” goes deeply underwater.

https://www.businessinsider.com.au/house-prices-beijing-2017-9

I give up …. what’s an ‘FB?’

It rhymes with “Freaked Borrower”.

FB is fakebook, that social disease from that sack of garbage, F’erberg. Just can’t wait for him to run for POTUS. Are we to be spared nothing????

Marty – good guess but it’s FB for “f*cked borrower” – this term dates from the last run-up to the last crash.

Oh, the days. Red arrows. Dudes Hanging Out – the number of which was the DHO index. Cawlumns. Is this child included with the house? We had some real rollicking laughs back then.

In a comment in a previous article from a long time ago–yesterday–Wolf postulated ’employment numbers that are now declining for Santa Clara County year-over-year.’

I don’t dispute this, but would posit that the employment numbers are declining from an extraordinary–and unsustainable–high. I have no stats or fancy charts, just my casual observations of traffic, crowds, etc. and my experience living in the SF Bay Area for 34 years (the last 21 in San Jose).

Here’s my comment, added late, to that article from long ago:

“Here’s a few in my vicinity which I’ve been watching as I’ll be selling in the near future. On almost all of them there was an accepted offer the Monday after a one-day open house on Saturday or Sunday:

http://tinyurl.com/y8u48ut2

http://tinyurl.com/yaw5xxo8

http://tinyurl.com/y88lquhy

http://tinyurl.com/yb2yg8oh

http://tinyurl.com/yb4zkxec

Note the typical ‘on Redfin for X days’ was around 20 days; and the listings usually show up at least a week or two before an open house, and closing usually takes up to a month after a deal.”

The BA is famous for its ‘micro climates’ (it can be 60deg in Half Moon Bay and 110deg in Livermore at the same time). It appears to me that the housing market has its own ‘micro markets.’ My house, and the listings cited above, are all within easy biking, even walking, distance–i.e. < 3 miles–from the new Apple HQ, and only a few more from the proposed Google macro campus in downtown SJ. Homes farther away will not see the same demand (not surprisingly). No big point, just that aggregated statistics don't always tell the whole story. I'll be listing my own old, crackerbox house–3m as the crow flies from the new Apple HQ, about 2m from the immensely popular Santana Row (and the new Splunk HQ), about 4m from the Netflix HQ and maybe 7m from the proposed Google comple– around the start of the year. If anybody's interested–and it's OK with Wolf–I'll post my experience here.

Not only are those crows flying, they’re being served as they fall dead from the sky.

The crows–there are many–who hang out at my house are doing quite well. The cars that park under the tree they roost in, not so good.

Eat up.

California Bob – there are micro-markets indeed. I’m within a mile of very high-up companies, yet the warehouse I live in is renting to us for about 50c a square foot.

I’m poor as a church mouse yet I’m looking at the little snippets of land that can found on Craig’s list for under 10 grand, because maybe they can’t be built on, but perhaps a self-contained RV can be parked there, so at least I’d have a place that’s mine, or two or three of them, that I park at in rotation, without being charged anything more than a few hundred a year in property tax. This is my plan in light of what I realistically think my maximum earning efforts can achieve, and in light of the fact that street-parking RV’ers are becoming an outcast group and trailer parks want high space rents.

Sit tight. Prices are falling.

Same story in Fremont. Poor quality homes patched up go “Pending” 2-3 days after open house.

Poor quality homes but really ugly homes sit for a while because the sellers are too stupid / lazy /poor to put a new kitchen or fancy paint.

Overall even in Fremont which is 20 miles from Apple/Google and 45 mins BART from San Francisco is still a WARM market – not HOT. But could be also because schools are open and people really hate disrupting their kids.

That said prices are at least 10% than last year all over Fremont.

I will not refute that properties are selling in Fremont at ridiculous prices. Homes were sold at the last bubble peak as well.

However as Wolf has suggested I have seen homes removed from the market and rented as well as reductions that are not captured by the realtor statistics when you verify the original asking price to the sold price.

The housing market is like a boat with a failed outboard motor. Its moving on momentum but its velocity is falling. If the realtors are playing games with the statistics things are probably far worse than you think.

To the best of my knowledge, the last housing boom/bust was widespread–there were bubbles even in the ‘flyover’ states–due to the availability of cheap, easy credit and a prevailing popular frenzy. The SFBA is somewhat unique due to the aforementioned job growth and overall desirability of living in this area, and the constraints on housing development (NIMBYism, geographical, etc.). There has also been a massive influx of immigrants–legal and otherwise–who tend to rent the lower cost units (sometimes 8 or 10 in a 2bdrm apt.), thus driving demand and scarcity in higher-cost units and the single-family housing market (and causing the relatively recent phenomenon of whole families, with 6-figure incomes, living in motor homes on the streets).

I don’t foresee a ‘dot com’ style bust, as I think most of the buyers work for well-established companies–Apple, Alphabet, Facebook, etc.–that won’t be going tango uniform any time soon. But, we shall see; if we get a glut of cheap(er) apartments, as I believe Wolf has predicted, things could deflate (but, likely, slowly).

Bob, my for-sale, tiny, crowded, ancient, cracker-box house a few blocks north of “downtown” Sunnyvale is currently excluded from the MLS but has multiple “as-is” no contingency, generous rent back provision, offers from gut-and-remodel investors that range from 95% of to asking. I think I am managing to sell at the peak here. Don’t have the option of completely leaving the area; proceeds should buy newer, bigger, nicer digs in Fremont/Union City for me and my multi-generation family that grew instead of getting smaller when I retired. I am fortunate to have moved here in ’95, just before all the hype started, and also to have contacts in the Chinese/American business community who are some very smart people who know how to make things happen. Wish you the best with your plans.

Thank you. Sunnyvale is the hot ticket now, with the Apple HQ going up next door and almost ‘cheap’ compared to Cupertino. Of course, you heard about the Sunnyvale house that went for almost $800K over asking (it did have a large, apparently subdividable lot)?

My best to you; sounds like you have a solid plan. Fremont is nice, used to live there when it was mostly orchards and flower patches (my mother was the first principal’s secretary for Mission San Jose High School). It still has some suburban charm.

How is Santa Barbara doing? I loved that show.

Dunno. Read somewhere–either here or at Naked Capitalism–that that area is down a little economically. I don’t think it experienced quite the job/population growth that the SFBA did. I was down in San Diego a few weeks ago and that area appeared to be thriving–lots of new construction–but they’re starting to experience ‘big city’ problems, not the least of which is a HepA outbreak due to the homeless not having convenient, clean washroom facilities.

As someone who lives outside of California, I have heard a lot about the various housing bubbles in the state, but one thing that I have being wondering about is taxes, not property tax, but income (capital gains) tax. Is this a major source of revenue for the state like capital gains on stocks or is it a non-issue? Did it play a role in the last budget crisis?

YES. California is uniquely dependent on capital gains tax revenues since property tax revenues are so low and since so many people with large equity investments live in California. Property tax revenues tend to be relatively stable. But capital gains tax revenues can boom one year and then just about disappear over the next three years. This is what happened during the last crisis. Cali ran out of money and had to pay suppliers with IOUs.

On the sunny side: I bought some Revenue Anticipation Notes (RANs) when everyone figured Cali would collapse, and they had a great return for the eight months or so of their term.

This is going to happen again. It always happens.

“… property tax revenues are so low …”

I dispute this, on a purely technical, pedantic basis. CA’s property tax rates are probably not all that different from those in other states; the issue is that their rate of growth has been curtailed by Prop. 13. So, the property taxes don’t reflect the current value of the property.

Ex.: I bought my house in San Jose in 1996 for $245K. I am assessed at something around $350K (and pay about $5/year in prop taxes), but I expect–barring an earthquake or NK nuclear strike–to sell early next year for north of $1M. The buyer will be assessed at, I believe, 1%–could be 2%–so will be on the hook for $10K/yr or more.

… further, I read the other day that Texas, and probably other states have NO residential property taxes, which is about as low as you can go. But, they make up for it with higher sales and other taxes.

By then, considering yourself fortunate to sell it for what you paid.

There is a way for CA seniors to take their old tax base with them provided they buy their new home for less than they sell the old one for. There’s also some kind of exemptions on capitol gains, up to a certain amount. I’m not an expert on all this, but my tax man and real estate agent will work it to my advantage to the extent possible. There are times when professional help really helps.

CA Bob, Texas has very high property taxes near the major cities because there is no income tax. I don’t know what you’re reading, but I pay almost $5K on my supposed $150k rental and the tax has gone up 10% per year since I bought it in 2013.

Yes, “low” only for people and companies that have owned the property for a long time, including Intel which has owned its campus since the 60s (?) and pays very little property tax on it. If it sells the property, the buyer will have to pay property tax on the much higher current value.

Property tax revenues were about $57 billion in fiscal 2016 (but it doesn’t go to the State, it stays within the county).

This compares to the State’s “Big Three” tax revenues:

– Personal income tax $83 billion

– Sales and use tax $25 billion

– Corp tax $10 billion

… “I bought some Revenue Anticipation Notes …”

I am all ears. Details welcome!

When Cali is swimming in money, RANs pay very little yield and are hardly worth the trouble. They’re behind GOs, so the risks are higher, and if our beloved Cali goes bust, you might lose a lot. But that’s why they offer a much higher yield when investors fear that Cali might go bust. I’ll be a buyer next time Cali is thinking about issuing IOUs :-]

http://www.buycaliforniabonds.com/faq.asp#13

How to buy:

http://www.buycaliforniabonds.com/opportunities.asp

On a side note, how does one purchase Revenue Anticipation Notes?

I bid on them through my broker before they were issued and I held them to maturity (about 9 months, if I remember right). If you Google for it, you’ll find a list of brokers that California deals with directly when it issues bonds. I think most brokers that have lot of clients in California are on it.

Capital gains taxes are like heroin for the CA state legislature. From what I know, our state’s budget planning all but assumes massive cap gains tax revenue growth and, of course, if it doesn’t materialize it will get ugly.

Hello Cali Bob,

It is state income tax that Texas lacks, not property tax. In fact, Texas property taxes are considered quite high by most, since they are recouping all the foregone income tax.

Ah, OK. Thanks for the correction.

No risk for Cali IOU’s is negligible no matter what the books and stock market says….when push comes to shove Cali has so much Washington muscle they’ll just steamroll the Fed and flyover state ham and eggers to cough up

They had to do IOUs during the last crash, and there was a Democrat in the White House and QE Bernanke ran the Fed.

Building where I live has been having one month free moving special for all studio, one bedroom, 2 bedrooms since 4 month ago. No takers :). The manager is so desperate that the other day I saw her showing the apartments to the kind of people that a year ago she would not have even allowed to enter the building. They keep also decreasing the rent, along with free one month, but no takers.

The idiots think that there are unlimited pool of people to afford apartments at such high prices. Home owners and landlords in Bay area are in for a long steep fall. Enjoy the fall :).

I’ve never understood people who wish ill on others; esp. others who have done no harm to them.

California Bob, the nation-wide housing bubble blown to ludicrous proportions by the Fed’s financial crack cocaine was wholly dependent on borrowed money. The FBs who drove up the prices caused the prudent and responsible to be priced out of the market – so they were rather directly harmed by the fools who used borrowed money and leverage to drive housing prices up to nosebleed levels, and literally put many in the lower socioeconomic strata out on the street because there was no such thing anymore as affordable housing. So it won’t bother me one bit if these FBs end up living in a cardboard box while the banks who foolishly lent them money to buy into a speculative bubble go bankrupt (although the latter will doubtlessly be bailed out by taxpayers and the Fed’s printing press).

A person born into this society should have a way of finding shelter. You have the same right to shelter as the next person, assuming you want it and are willing to work a reasonable amount for it.

People on the Earth are here only temporarily. To say somebody owns a piece of the Earth is ridiculous. If I weren’t allowed shelter today because of some silly price convention, I’d be fuming. I don’t know why the average Joe isn’t rioting in the streets.

The banks live off the fees of loaning the money. The buyers of the mortgage backed securities will be the ones getting screwed.

section 8 the anti property market neutron bomb

when it moves in…..no matter what the market says, your property isnt worth as much as advertised

Thing is people change homes less than they change cars, if they can change homes at all.

And if you do sell your home, were will you live next?

Ivanka Trump has been forced to make a 30% cut in her wish price to rent her Manhattan apartment.

Forgive my misty eyes.

https://www.mansionglobal.com/articles/75771-ivanka-trump-lowers-rent-on-manhattan-condo-by-30?mod=marketwatch_home_module

1) Demographics. Bay Area depends on H1B influx for growth. Bay Area natives have been leaving for decades.

2) Seattle/Portland is winning in cloud, making them the global IT winning cities. Microsoft Azure and Amazon Web Services are both HQ’ed in Seattle.

3) Rising ARM mortgage rates, which are based on short-term rates. In some zip codes, nearly 100% of mortgages are ARM.

Curious where you going the data for #3

Near 100%arms in a zip code???

“2) Seattle/Portland is winning in cloud, making them the global IT winning cities. Microsoft Azure and Amazon Web Services are both HQ’ed in Seattle.”

And, of course, neither would ever, EVER move from those ‘winning’ cities. Oh, wait;

http://www.mercurynews.com/2017/09/29/exclusive-microsoft-buys-north-san-jose-land-campus-eyed/

Can everyone please stop referring to a generic “shortage” in CA real estate? If there was an actual shortage of units, you’d have more and more homeless flooding the streets.

But there are plenty of places to live. What there’s a shortage of is… affordable homes because the reits and foreigners have bought up so much. There’s a shortage of places to buy for those of modest income. But they’re not homeless and we don’t need loads of more inventory.

My dad is closing on his home purchase in San Bruno, CA for $1.3 million!! He’s a small business owner and has done well for himself, but it hurts me to see him buy a house that over priced..

“My dad is closing on his home purchase in San Bruno, CA for $1.3 million!! He’s a small business owner and has done well for himself, but it hurts me to see him buy a house that over priced..”

Sounds like your dad is a smart man. You don’t suppose he thinks his house will appreciate? Check back with us in a couple years. I thought $245K was a ridiculous price for an 1,140sqft house in 1996; I could get 4 times the house in Modesto for that kind of money (of course, I couldn’t get a well-paying IT job there, but …). Zillow, Redfin, Xome all estimate my house at a little over $1M … I hope to hell they’re right.

Peeps will sell the casa in SF or Sactown, buy a small multi-plex in Reno and create income to live off of, have a roof over their heads and have money leftover for the rest of their lives. Plus, no state taxes! Just saying – I sold almost F&C beach units in 2004 for over $900k… I knew the market would tank (I was a bit early – but never guessed the FED would destroy the financial system) but I thought – I never HAVE TO WORK AGAIN… That property is now worth $1.5MM to $1.6MM, but so be it. I think alot of people will have the same thoughts when the r.e. start to decline. I was younger then and I still love my biz, but it is a comfort to NOT have to do it. Anyone 60+ will, IMO, not wait to long to sell when the prices decline in earnest. Just my 2 cents.

– And more and more (retired) people are fleeing the state of California. And these are all taxpayers. Ouch & OMG.

Yes they “were” all taxpayers.

However – – a old schoolmate of mine, being retired and having little or no TAXABLE INCOME and the property taxes on the grossly over “valued” house (that they owned for nearly 45 years) has a “minable” tax bill.

How much income tax and property taxes are the new owners paying? Consider that the small house sold for 2.75 million…

The state coffers are making a killing off of the new owners.

He is now back home in oHIo – in a larger, newer house that sits on 1 1/2 acres of woods set him back 175k… And he over paid at that number……

Loving every minute of it….

“He is now back home in oHIo …”

We all have an emotional ‘home’ that isn’t necessarily our current place of residence. I expect an Ohio native would be happy to be back ‘home;’ a California native would likely experience severe cultural/weather/environment shock leaving, say, the Bay Area for Ohio.