Same phenomenon leading up to the last housing bust?

The toxic combination of “competition from other lenders” and slowing mortgage demand is cited by senior executives of mortgage lenders as the source of all kinds of headaches for the mortgage lending industry.

Primarily due to this competition amid declining of demand for mortgages, the profit margin outlook has deteriorated for the fourth quarter in a row, according to Fannie Mae’s Q3 Mortgage Lender Sentiment Survey. And the share of lenders that blamed this competition as the key reason for deteriorating profits “rose to a new survey high.”

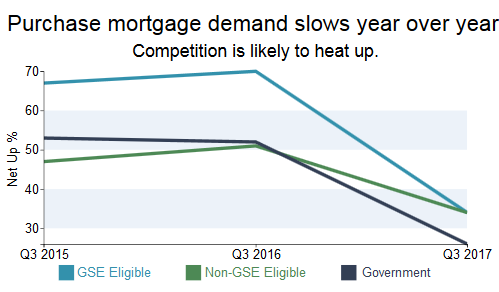

Demand is down for all three types or mortgages:

- Mortgages eligible for guarantees by Government Sponsored Enterprises, such as Fannie Mae and Freddie Mac (“GSE Eligible”), indirectly backed by taxpayers.

- Mortgages not eligible for GSE guarantees (“Non-GSE Eligible”), not backed by taxpayers

- Mortgages guaranteed by Government agencies, such as Ginnie Mae, directly backed by taxpayers.

The survey, conducted quarterly, tallied responses from senior executives at 190 mortgage lenders, from the largest banks to smaller specialty lenders, “to assess their views and outlook across varied dimensions of the mortgage market.”

These executives reported that demand over the past three months has dropped year-over-year for purchase mortgages, “reaching the lowest third-quarter reading in the past two years”:

Lenders also reported declining demand in refinance mortgages: “Overall, the refinance market remains a stark contrast from a year ago, when the net share reporting rising demand over the prior three months hit a survey high.”

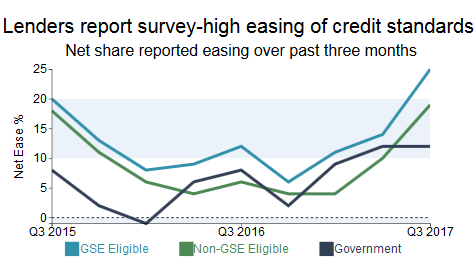

And how are lenders combating this lack of demand and the deteriorating profit margins that are being pressured by competition? They’re loosening lending standards.

Fannie Mae’s report:

Lenders further eased home mortgage credit standards during the third quarter, continuing a trend that started in late 2016. In particular, both the net share of lenders reporting easing on GSE-eligible loans for the prior three months and the share expecting to ease standards on those loans over the next three months increased to survey highs.

Lenders’ comments suggest that competitive pressure and more favorable guidelines for GSE loans have helped to bring about more easing of underwriting standards for those loans.

This chart shows the net share of lenders reporting loosening their lending standards for each type of loan (= the share of lenders reporting loosening credit standards minus those reporting tightening standards):

For all three loan types combined, the share of lenders reporting that they loosened credit standards has been rising since last year and has reached a new high in the survey data going back to 2014.

Easing lending standards under competitive pressures, while mortgage demand is declining and profit margins are deteriorating comes at the nick of time.

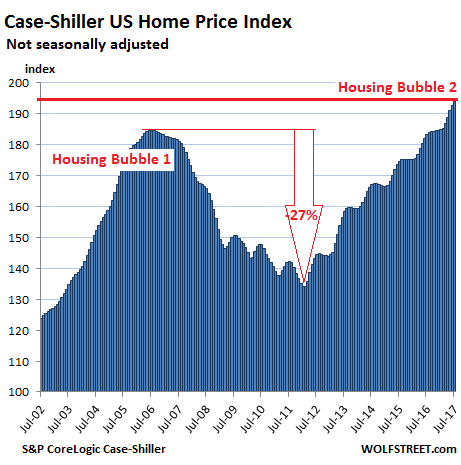

In many urban markets home prices have soared far beyond their peaks during the prior crazy housing bubble. That bubble ended with such spectacular results, in part because lending standards had been loosened so that more people could be stuffed into more homes, and more expensive homes that they couldn’t afford, and whose prices then plunged when the scheme fell apart.

This time around, home prices, according to the national Case-Shiller Home Price Index, are now about 5% above the prior crazy bubble peak that imploded with such fanfare:

So beyond doubt, this is a great time to relax lending standards to get potential home buyers into homes that they couldn’t otherwise buy at these inflated prices. No one in the industry seems to remember the last housing bust and how it ended for the industry.

In these big US cities, today’s housing markets have blown way past the prior crazy bubble peaks. Read… The US Cities with the Biggest Housing Bubbles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What could go wrong?

‘World Economic Forum sources said recent Bank of England concerns about a potential consumer debt crisis were timely since there was evidence that the global banking system was less sound than before the financial crisis and that conditions were deteriorating in some parts of the world. Last month, the International Monetary Fund warned of a “dangerous” growth in China’s debt.’

Via the Guardian.

What caught my eye was: ‘that the global banking system was less sound than before the financial crisis…’

“What caught my eye was: ‘that the global banking system was less sound than before the financial crisis…’”

The US is a little better Japan, Southwest pacific, and Europe, are about the same. whereas chian is much worse so on the whole its worse than 08.

china has that much overt a covert debt that it will do more damage to the global system than the US event which was turned global by Greece. When it implodes.

chian is moving its SOE NPL debt problem, from SOE A, to SOE C.

Replacing NPL at SOE A. With a new bigger debt to SOE C. Not resolving it.

You can do that in a central command economy until you cant. Then you get a USSR style implosion. This will be worse in china, as china has morphed from communist, to Mafia Capitalist state.

Without first clearing the communist debts and NPL Mountain’s.

The OBOR initave is simply a huge Money-printing Stimulus can kick.

The hope is that OBOR will generate enough loans and sales, made to foreign entities. That will generate enough income to dig china out of its problems. How many more white elephants can china get away with building in places like Sri lanka at the host nation expense .

Before the third world, click’s on to the real reason’s for the OBOR initiative. Who gets the bill’s, and who the only real beneficiary, will be.

I am sure it is different THIS time…

It is different, in 2007 FNMA and FHLMC held most of the notes, now the Federal Reserve is holding the notes.

Neither of which are preventing the ongoing down draft and price declines.

Exactly.

I think 90% of all loans since 2008 are owned or backed by the GSEs. I refinanced twice since then and each time Fannie bought the loan from the bank I refinanced with.

The GSEs (who do not need to make a profit) will have so many option available. No QE needed as before to bail out the banks.

How about refinancing loans for 40 years to lower payments. Provide some community service in exchange for skipped payments. etc..etc…

None of which will prevent falling prices.

Aba with an ad for lending tree right in the middle of the article

This is so reminiscent of the last bubble except that there is more debt.

Now the FED is up to its eyeballs in debt, the federal government has 2x as much debt on its balance sheets, a lot of the countries pension funds are teetering on collapse, and so many of the corporations are leveraged to the hilt… and we did nothing worthwhile with all this new debt.. Infrastructure is in worse shape and the warming climate has created super storms..

I’m sure this time will be different.

Oh, It will be different all right.

With rates almost at zero and the FED almost a decade behind in raising them, “this time” the FED will probably just have straight up buy all the defaulted / distresses mortgage bonds because to many quadrillions of derivatives in the unregulated .

The only questions is How (not If) “we” and not the bankers who profited, will get screwed into paying for the fiasco this time and How to game it (in a vain and probably futile to compensate for the screwing to come).

The biggest Put in human history…most everyone is leveraged to the hilt on the assumption that the Fed and other central banks will just but their crappy debt if danger of a crisis arises…seems correct, no?

When everybody is betting on the dealer paying-out.

What happens ?

ALWAYS!

Time for an AI (Artificial Intelligence) based government to root out the stupidity of the system.

And to drain the swamp of eternal and newer residents

Hasn’t plane ‘ole “Dumb AI” a.k.a. “New Public Management” caused quite enough damage to society already? Do we need more!? Faster beatings delivered more effectively??

Consider that the current widespread looting, dilapidation, corruption, incompetence in providing core services and general waste in the public services and government was achieved “manually” by using *just* dumb KPI’s, procurement rules, work-flow systems, spreadsheets, databases and PowerPoint.

Then think of those IT-enabled, but mostly manually operated destructive processes, now becoming smart, efficient, out-of-control, with own internal agendas and then setting them loose on people?

I thought echo bubbles weren’t supposed to be bigger than the first bubble.

you got the millennials, (if I remember correctly) the biggest US generation in history, who entered real life just as the dust settled from post-2008 and have literally never lived life without neg/zero interest rates.

what could go wrong?

What point are you trying to make? Millennials have the lowest home ownership rates of any generation at this point in their lives, and their investment portfolios are by and large irrelevant. So while bubbles popping are not good for anyone, they’re far less vested than, say, Generation X or the baby boomers.

Till the time Stock Markets go Up and People are not defaulting on large numbers, this show will go on. I don’t see anything going wrong in the short term.

Just out of curiosity, how did the default rate increased rapidly in the last bust? Where are we related to that now?

Once your mass-manufacturing base has been hollowed out and ‘offshored’. then the only way a country has left to grow its economy is via usurious lending practices and foisting debt onto an ever-poorer paid populace (disappearance of manufacturing means the disappearance of the middle class which was forged by skilled, well-remunerated artisan workers).

So, given that there really is no option other than credit bubbles to support the whole creaking edifice, it should come as no surprise that another – even bigger – credit bubble is what we have.

Meanwhile, in other news, those nasty, nasty commies in China continue to take over the world economically. Apparently it’s all going to end badly, because modern western economic dogma holds that all centralized, command-and-control economies MUST fail.

So we just need to keep on with the closure of the factories, and loading up on debt…and wait for China to implode.

Right?

Correction: disappearance of the middle class was based on the loss of unionized jobs in the manufacturing sector.

Widespread unionization in core mass production – not “artisanal” -industries created the middle class, as we knew it, from 1946-80.

With off-shoring, de-industrialization and de-unionization, an ever-higher percentage of the national income now goes to Capital (and especially the FIRE sector), instead of Labor.

There’s your rampant inequality, right there.

“because modern western economic dogma holds that all centralized, command-and-control economies MUST fail.”

So we allowed the US to turn into one?

The inmates are running the asylum.

Well, that’s really not fair, we’ve turned into a dysfunctional corporatocracy. Where TPTB are all trying to win their own personal game of Monopoly. Which is insane when the entire economic system is built upon consumer spending… Hard to have a robust economy when all the money is being transferred into the hands of the few.. https://fred.stlouisfed.org/series/M2V

There is a huge elephant in the room re: US manufacturing 1945- 1975. This X factor is World War Two.

At end of it the US was the ‘only man left standing’

All manufacturing competitors were flattened and broke. The only partial exception was Britain that was broke but only partially flattened.

But in Germany there were signs of life in the bombed and flooded VW works. None of the victors wanted to actually buy into its odd- ball car (everyone including Ford kicked the tires) but the plant happened to be in the British Zone and the cheapskate British Army, now cut off from US jeeps, ordered 10, 000.

In Japan Sochiro Honda had begun motorizing bicycles with small surplus gas engines from gen sets.

That was then. No wonder the US wants to return to the 50’s when it produced 80+ percent of the world’s manufactures.

But they aren’t coming back and the US has pretty much burnt through the post- war bonanza.

But workers seem to succumb to the scare tactics when corporations and their lobbyists invoke “socialism”. Look at what happened at the Nissan plant in Mississippi.

Michael is right. The thing that made capitalism work for the greater good was unions.

BVian, respectfully disagree that Unions made capitalism work.

What made Capitalism work was “That was then. No wonder the US wants to return to the 50’s when it produced 80+ percent of the world’s manufactures.” (Nick) This is what made Capitalism work.

When you control 80% of the productive capacity of the World and export all matter of goods (not services), your standard of living shoots the moon. We saved and produced, not spent and consume.

Now we import all matter of goods and consume everything regardless of whether we can afford it. Quite sad.

If Unions were so great, when the rest of the world caught up with us on a manufacturing basis, we would have innovated and kept pace. But instead Unions fought flexibility and productivity improvements necessary to remain competitive.

Unions served a useful purpose in the early days but failed to adapt to the global marketplace and doomed their constituents.

Dont forget the mass exodus of union mfg jobs the public sector!!! Aint never going to off shore those precious jobs….NEVER…until the well runs dry….then the fireworks will be amazing!

The Chinese are no longer totalitarian communists. Now they’re totalitarian capitalists, which is an improvement insofar as it has allowed them to acquire a great deal of the US economy.

Housing demand isn’t in decline because lending standards are too tight. Housing demand is in decline because US workers have been targeted for wage suppression for 40 years. Loosening lending standards doesn’t solve that. It will just create a much larger problem.

At some point Wall St. will have to decide whether it prefers to cheat US workers before or after they get paid, because trying to do both can’t really work for them.

I get the feeling the Fed isn’t going to get very far with its program to unwind its balance sheet and raise interest rates before it has to backtrack.

It might fix it in the short term because there is always a batch of buyers who would have taken a mortgage if they weren’t denied previously…

But if the Realtors and economists couldn’t find a reason that current price are a bubble, then a few years of lending to unqualified buyers will really make them sound like shills.

“Once your mass-manufacturing base has been hollowed out and ‘offshored’. then the only way a country has left to grow its economy is via usurious lending practices and foisting debt onto an ever-poorer paid populace.”

Yeah, I just don’t think this is true to the extent you guys think it is.

As Nick pointed out below, the golden age of the middle class via manufacturing jobs in the 50s to 70s was largely an anomaly, a function of the rest of world having to rebuild after the war, really low immigration levels, and the bargaining power of labor. None of those things exist today, and there’s no going back. Manufacturing will never build a middle class anywhere in the world again, barring massive regressive changes in technology (e.g. outlawing automation) and/or restricting the ability of companies to move their operations to the lowest cost center. Both of which, I’d add, are about as anti-free market as you can get.

“(disappearance of manufacturing means the disappearance of the middle class which was forged by skilled, well-remunerated artisan workers).”

The middle class manufacturing base was driven largely by unskilled workers with little education.

An entry level factory worker with no skills and no education in the 60s could be expected to start at about $15-20/hr in today’s dollars. Once the unions were broken, mostly by the 90s, those rates often plummeted by more than half– and usually meant a reduction in benefits as well.

Capitalism, baby.

Bingo.

The commoditization of all things manufactured is ultimately a race to the bottom for labor. In the end nobody wins, not labor, nor Organizations as the marginal utility reaches zero. I guess Government wins as they take everything for redistribution (to themselves).

Really comes down to just how much sh*t do we really need. I suspect a “LOT” less than we currently have.

Do we really think the Chinese consumer will awaken? And if so buy anything other than Chinese made stuff. I’m not holding my breath.

“Do we really think the Chinese consumer will awaken? And if so buy anything other than Chinese made stuff. I’m not holding my breath.”

chinese immigrants mostly only buy “chinese Stuff’ so for the mainlander’s who are instructed by the CCP to by only chinese manufactured good’s, not a chance.

ccp china says what the west wants do hear at meetings about trade then continues its policys of china first destroy the west with trade.

Already they have played and delayed P45 by nearly 25% of his term over any real change to chinese trade policies, or market access regulations.

They are distracting him with the DPRK, playing him and America like a violin.

Nothing will change, until the CCP, is FORCED, to change.

Chinese are already the big dog in asia as far as tourism goes. Everyone wants their money. South Korea coming on strong in the #2 position, which is part of the reason RocketMan is doing what he does.

And dont forget they have bought a lot of foreign goods – mostly RE!

Well I have a different perspective about unions impact on capitalism. Unions, with strike induced demands, forced unreasonable wages on industry often for just tightening bolts. No skill there. This forced industry to move to lower cost locations. Look at the move to southeast U.S. for automakers where unions were absent and the move across ocean too for lower labor. Manufacturing moves to where there is lowest labor cost with dependable labor source. No one else to blame because we did it to ourselves.

Was mgm to going to do those jobs? Nope. Mgmnt makes up goofy rules, designers create Edsel and workers get to kearney about how much they suck and cost to employ. Then they hire suicidal slaves in China to make the crappy products Mgmnt and creative to sell to people with no jobs.

That’s pure genius from our elites.

Thanks for reading my comment S but I’m not quite as negative on manufacturing.

I have to say, as a manufacturer, Germany just effing fascinates me. It is running the world’s largest trade surplus, 300 billion or 50 % more than China’s at 200 billion. But that income is going to about 8 % of China’s population.

Germany’s debt not its deficit is 70 billion. Or less than one month’s QE back when the US Fed began. ( If I recall it was 85 B a month)

I don’t know why it bothers having a debt, it’s like us having a 50 dollar Visa debt.

Manufacturing as % of GDP is double the UK’s at 10 percent.

It’s not just autos, nor is it all big outfits. The place is full of under 500 employees cos making all kinds of precision stuff, almost nothing in Walmart. It makes a lot of stuff (like Japan) that makes stuff, e.g. computer controlled machine tools. A lot of these are family outfits.

The type of customer it caters too will often toss the lowest bid automatically and the supplier will often tell him upfront that it is not a price competitor.

GM famously insisted on the ‘China price’ for its ill- fated ignition switch that would shut off at highway speeds.

But GM probably didn’t insist or even want the China price on its own factory equipment.

I think we should keep Germany in mind because the culture is not THAT different from ours. They are way more likely to speak English than the French.

Some differences: The MBA until recently was unknown. The oldest degree dates from 1995 (Heidelberg) and was more a reaction to competition for foreign students than a demand by business.

Half the high school grads go into apprenticeships.

The relationship between business and labor is better than in the US and much better than the UK.

Large unionized outfits like VW have a union guy on the board of directors. I don’t know whether this law or just practice.

You are right on the money. But no one has listened to this for decades and are not going to hear you now….. It is pretty much “all over”. It just takes a long time to cycle through the disaster……………

There is a chorus line to apopular song in our part of eth world by a semi local artis so it mau=y not have travelled weel.

Part of it “Some peopel they never learn”

The whole song was about this sort of, Economic,Relationship, and Social Vices, idiocy.

“But this time it will be different” “Yeah Wright”.

What will be different is that this time I am better prepared to deal with it and profit from it.

Wonder if the buyers needed/will need mortgages for the following properties:

https://www.domain.com.au/news/holy-smokes-batman-australias-batcave-mansion-sets-property-record-20170925-gyo14a/

https://www.domain.com.au/128-crosby-road-ascot-qld-4007-2013628833

Make sure you take a look at the video in ‘photo 17’ in the above web site.

Some fantastic views of Brisbane. Especially for you Yanks who may never get a chance to visit the wonderful world of Oz (At least for some!!)

By the way – that’s what you can get for A$10 million in Brisbane.

And if that isn’t your ‘style’ for around A$7 million you can buy an apartment in the heart of Melbourne.

https://www.domain.com.au/252-350-st-kilda-road-melbourne-3004-vic-3004-2013855568?utm_source=the-age-mobile&utm_medium=link&utm_content=position1&utm_campaign=masthead_featured_listing&utm_term=2013855568

Again take a look at the photos and the video in photo 22 which gives you some nice views of Melbourne

I recently heard that the August rush to close before school did not happen in the Chicago suburbs this year. I still hear the realtor rhetoric that inventory is low because everything is selling so quickly. There are houses for sale in my neiborhood that have been sitting for months.

We’ve seen this movie before and know how it ends.

Get ready for another taxpayer-funded bailout of the greedy and reckless financial institutions who foolishly underwrote mortgages for F**ked Borrowers (FBs) who were manifestly non-creditworthy.

Nobody is credit worthy anymore because nobody has job security. Most of those non credit worthy people have worked a lifetime for nothing. If I had to do it over again, I would never have bought a house, ever. Stay mobile.

You guys don’t give millennials enough credit for seeing through the BS. They can see where their parents landed up after so much work and sacrifice. They can see it wasn’t worth it.

The sheeple are finally starting to see through the land game. which has been used to abus etehm very badly inthe last 150 Years. This means it is almost over.

More and more regulations/laws are being drafted, world wide to force the sheeple to continue play the land game.

More and more cities are making it illegal to sleep in a mobile home in City/Municipality limits, unless it is parked in a high fee mobile home-park.

The techies are not completely stupid when they talk about establishing floating private villages outside territorial limits.

They are even making it illegal with out paying VERY high , live on a boat in a Marina now. In many places it is illegal to live on a moored Boat.

“If I had to do it over again, I would never have bought a house, ever. Stay mobile.”

You are not that free when you have a mobile life.

Actually the boomers who bought 20-30 yrs ago are living in their paid off houses that are “worth” 500k-1mil in Socal.

The timing was lucky, but, worked out.

Assuming the Fed does raise interest rates in December, that would increase the cost of a mortgage. With demand for mortgages in decline, and the Case-Shiller index where it is, could we be seeing a top in the US home values?

Hi Dan Romig,

Surely that’s a good thing if we are now at the top of US home values?.

Saying that a 0.25% or 0.50% interest increase is not going to make a massive difference, if as you say demand for mortgages is down then competition is going to be greater between the banks on the remaining mortgages.

Fed is for sure not gonna raise rate sin December if you hear what Yellen said this morning. Fed would go to any extent to keep the rates low so that the transfer of wealth keeps happening and asset prices stay inflated.

Did you hear what Yellen said this morning? The Fed should be “wary” of raising rates “too gradually.” This is hawkish. So you better put a December rate hike in your calendar.

Apologies, I got it other way.. https://www.usatoday.com/story/money/2017/09/26/yellen-fed-may-have-misjudged-inflation-keeping-rates-lower/703920001/

Read what the Fed heads say, not what the media say about them. For an entire year, the media have been saying that the Fed wont raise rates – proven wrong by the minutes, the statements, the speeches, etc., and by the rate hikes and QE unwind.

There are about 4 Fed gov that are not sure about raising rates. One (Kashkari) will never ever vote for higher rates, no matter what. He’s too worried about his portfolio. He doesn’t matter. The rest are a go. Yellen is now hawkish, and leading the pack. Yellen has said for months that it’s not that much about inflation anyway … they’re looking at asset prices, and the media refuse to acknowledge it.

“Yellen is now hawkish, and leading the pack. Yellen has said for months that it’s not that much about inflation anyway … they’re looking at asset prices, and the media refuse to acknowledge it.”

I wonder if she is getting that nasty tingly feeling in her spine. When she looks at assets (Particularly paper assets), and remembers her underestimation of the projected housing bubble correction effects, from the correction ,she and others saw coming in early 2005.

Let them deny,

Only when they are hurt, seriously, by their refusal to see, let alone accept reality, will they consider, other than their cloud 9 position’s.

Conversely if to many of teh delude see reality at once ther wopuld be more than a correction which is also not desirable.

Hence it would not surprise me if next year there are only 2 not 3. 25 BPS hikes, as the balance sheet reduction starts to kick in, the last thing janet wantes is a scared market.

I haven ot yet found her ” ” name yet most of the tribe acquire one inchildhood sometimes they change as life progresses “Bibi’s” (Netanyahu) never did. Sharon who ended as “The Buldozer” (may he be happy resting with his god) had several in his lifetime. It might have morphed to “oophs” after her underestimation in 2005, of the coming negative effects of the housing bubble, that had to implode. 2008 was. Some BIG “bump in the road”.

Hi Wolf-

What are your thoughts on Peter Schiff’s opinion that the fed has been in somewhat of a hurry to raise rates and unwind QE so they have options when things get ugly in the near future; are they doing all of this simply to un-do it in 2019 to keep the music going?

Great blog BTW, I’m learning quite a bit.

There are two parts to your question:

In terms of raising rates, the Fed is not in a hurry. Rates have been at near zero for eight years, and now they’re lifting them at a snail’s pace. Rates should have never been this low past the immediate credit crisis, which lasted a few months (late 2008/early 2009). And they should have raised them long ago.

During the financial crisis when credit froze up, the Fed acted as lender of last resort under various programs (such as “TALF” and others). That was legitimate in their role as central bank.

But QE was different. It was designed to inflate asset prices — which caused many of the economic problems we have now. Fed should have never done QE. At a minimum, it should have stopped after QE1, and after stopping with QE1, it should have let the securities roll off its balance sheet.

So no, the Fed is not in a hurry. It’s way behind the curve.

To the second part of your question: sure, it wants to have some ammo when problems arise.

“At a minimum, it should have stopped after QE1, and after stopping with QE1, it should have let the securities roll off its balance sheet.”

The FED as it Decided/Was pressured to, continue QE. then made a fatal mistake.

It did not ensure the further QE went to the bottom of the Economy. Stimulating all of the 3economy as it moved up. Profit alwasy move sup its natural as greater “Entrepreneurial risk” is always taken by tiers 2 and 3. Not the 1 St or lowest tier.

The FED could not ensure this, as it did not have the cooperation of the sitting administration, or congress.

Henc ethe huge finacial paper b an dproperty bubbles we hav etoday.

For which teh FED is only partly to blame. The FED is also teh only one trying to slowly deflate some of those bubbles..

NO matter what tehFED does it is always wrong as monetary policy shifts form whatever status Quo, always feed one, at the expense of another.

Instead of focusing on how FED actions effect groups in the Economy. We need to look at what the FED actions do to the whole US Economy. Long Term.

What the FEd is doing now is long overdue and long term positive for the whole US economy.

2008 was ugly ha dteh FED done what it did in 1929 and sat on it hands it would have been much uglier.

The lesson from the 08 – 16 period is

Monetary policy alone, can not resolve many of the economic issue of modern advanced Economies.

CB’S in times of serious economic stress, operating without the cooperation and assistance of the administration are infact urinating into a financial hurricane. 2008 was cat 4 and teh FED go no real cooperation and assistance from the sitting administration.

The FED also his not receiving much assistance, or cooperation, from the current administration or the current House/Congress.

Contrary to common belief. The FED is not Omnipotent, does not walk on water, and does not have a functioning magic wand.

It is controlled by Humans. Humans make mistakes.

Prices fell here in the bay area 40% the last time the fed kept rates low.

Yes We sure could unless the dollar hyperinflates

I believe we are at the peak of the most recent bubble. There’s a bagholder out there willing to pay me stupid money for my house-which has presumably increased in value by 3 X in the last 15 years-and I know I’m going to kick myself for not selling

True price discovery, when it finally asserts itself after years of extend-and-pretend by the central banks, is going to be cataclysmic for the bagholders who bought into the Fed’s asset bubbles with borrowed money.

Spot on, Bigbie… I lived outside Seattle and 3x is just what I figure I can get and move back to Maine and buy a huge farm on the edge of a wilderness with money left over.. Then I remember the black flies.. I guess I’ll ride this wave like I did the last one..

Poverty, crime and horrific weather or rampant insects. Tough call.

What farming is your expertise?

Meanwhile, home prices keep rising as fools rush in to buy at the peak of the bubble.

http://www.zerohedge.com/news/2017-09-26/case-shiller-home-prices-rise-fastest-pace-3-years-hit-new-record-high

Here in Manhattan, prices are so insanely high that making a million $/year will barely afford you a “family” apt.

What gives? Where will the greater fool come from when taxes are insane (pure socialism here) and interest rates are already rock bottom.

Darn those capitalists. Darn those socialists. They just ruin things for everybody.

In san Diego, median income for family of 4 is 63K/year and median home price is 540K.. which gets you a small town home in decent neighborhood

And gets you a mortgage payment that’s fully half your take-home or more. Do you make your own clothes and forage for food? That’s how they get by in Bristol these days.

Our Gracious Host has frequently commented on RE pricing extravagance in CA. Remarkably, this does not seem a worst-case scenario. But it is much the same in most of the world, where established landowners are well-positioned to fleece the general population on housing costs. Hence the favelas in Rio, for example. And in Britain a third of the land (maybe half) is owned by old Norman families who are actually subsidised to keep it off the market, as was discussed in a previous post here.

For the record, I do not hold a title of nobility. Anymore, those are granted to wealthy aging rock stars who take token payments to do benefit concerts. You know who you are.

Except in theory a family of 4 at that income wouldn’t qualify for a mortgage of 540k, even with 20% down.

A family of 4 making that is generally living in a relatively safe area that has more mediocre schools and is a bit far from major work hubs or a bit more run down. Santee, Lakeside, Vista, El Cajon, Chula Vista or maybe Clairemont.

If you look at the nicer neighborhood zip codes with well rated schools the median household incomes jump to $125k with the upper quintile easily making $200k household.

That median income will barely get you into a $550k 2 bedroom starter assuming you have a down payment of some substance.

The nice areas of San Diego are certainly ridiculously priced compared to 4 years ago. For that past 4 years condos in my area of San Diego have appreciated an average of 8% a year which is absolutely back breaking…

I could have handled 4%, but 8% has pushed stuff to a point where its concerns and pains me to consider buying.

This is correct; no way 5k/mo will qualify someone for 540k even with 20% down. And that is assuming 0 other debts (car, credit card, student loan, etc…)

Foreign oligarchs who spend less than 1/2 the year in the US aren’t subject to US income tax. The Russian who bought Sandy Weil’s former condo at 15 Central Park West paid around $88 million for it. Reportedly, his daughter stayed there while she was at school in NYC. The place even came with a special property tax deal (around 1/10 of 1 percent per year as I recall).

The younger generations now want to rent and be mobile. They don’t want to buy lawnmowers, rake leaves and spend money on big improvements. They want something comfortable and affordable that they don’t need to maintain. The future will be full of urban sprawl with Starbucks and dry cleaner on the ground floor and 1 and 2 bedroom apartments above. Single family homes will lose lots of value when there are fewer and fewer buyers.

Those may mostly be musings of people with so much college debt they couldn’t buy if thy wanted to.

Most millenials I know in San Diego want to own property. And quite a few have found ways to take the plunge. Especially those who got married. But it is all happening later into our 30’s.

Those without kids are more willing to love in gentrufying areas near the city. Most with kids still want to live in the closest suburb with good public schools.

The stigma against renting is still very strong. This tune I think is different in cities like new York and san fran because buying in those areas is just a cruel joke for the vast majority of people.

As these millennials start to marry and have kids; they will want to own a home instead of rent an apt.

Sure; they want to be mobile and free when their hitting the bars and partying; but, once they tie the knot and are poppin out babies the Mrs. will be calllin for home buying. Guaranteed.

As the cost of everything goes up, electricity, fuel, insurance, taxes cost of maintenance and wages for the majority go down the cost of suburbia just gets beyond the ability of anyone. Houston kept the prices down by their lack of infrastructure to a huge cost to everyone other than the developers in the big picture. NYC and most other places made that infrastructure part of doing developments so the costs are much higher.

Going forward adding more and more people to the system is going to get more and more expensive as to do that will require much of the existing infrastructure, sewer, water storm drainage, power grids etc to be rebuilt to accommodate the larger capacity needed. This is what none of those in power want to do because it gets in the way of their game of monopoly.

I say to them, what good is it to own everything if what you own is dysfunctional and all the serfs you control are angry and disenfranchised? I know that if you don’t continue on your quest that someone will displace you.. BUT Maybe you need to stop and think about what the real end game is.. And change your lobbying from your personal goals to what will really make America Great again!

Such a funny dream.. Psychopaths never change with out the proper therapy and drugs.. and what psychopath ever thinks they are a psychopath?

“The younger generations now want to rent and be mobile.”

It’s hardly a matter of preference. Employment in the US is increasingly precarious and poorly paid, and young adults have no choice but to accomodate that.

Companies like Black Rock are buying up homes and renting them at the highest prices the market will bear. San Barnadino, CA, for example, has never recovered from the last collapse, but because of Black Rock housing costs are as high as they have ever been. As Lex Luthor’s father pointed out, “Son, stocks may rise and fall, utilities and transportation systems may collapse. People are no damn good, but they will always need land and they will pay through the nose to get it.”

Long-established trends show that it’s only going to get worse, a lot worse, because no dynamic exists to halt those trends, much less reverse them, because they have been carefully eliminated. One must pity the children, knowing they have no future.

No worries. Help is underway. Millennials are getting the help they need to own properties .

“Lennar Lures Millennials With Offer to Help Pay Student Loans”

http://www.builderonline.com/money/mortgage-finance/lennar-lures-millennials-with-offer-to-help-pay-student-loans_c

“”Eagle will make a payment to a buyer’s student loans of as much as 3% of the purchase price, up to $13,000.

The contribution doesn’t directly increase the purchase price of the home or add to the balance of the loan.””

A FREE LUNCH?

The recipe for this free lunch is disaster…..

“The younger generations now want to rent and be mobile.”

According to a recent Reddit post. The “younger generation” is not buying it that it is better to rent. And you know what they are correct.

A couple things will deflate the housing bubble, technology. Home building is still done using old and mostly inefficient methods. New technology eliminates the need for public services, solar, telephone, etc. The homeowner can live just about anywhere. The idea of a square house on a square block laid out in assembly line fashion just doesn’t fit modern life. The other thing is permanently low interest rates. Every time the Fed has tried to raise interest rates in the last twenty years the markets have crashed.

Telephone is the least of what constitutes a serviced lot. The big one is water followed by sewer.

I’m near an area with a lot of iffy wells and believe me, the last bill I’d complain about is my city water bill.

I’m all for folks getting off grid etc. but this is only practical and desirable for a very small portion of the population.

Can you really go ‘off the grid’ in a city in the USA?

Don’t laws, rules, or regs in many places require a connection to a utility in order to get one of those ‘certificates of occupancy’?

Here in nanny state Oz with all the hype on solar and many people going off grid and turning off their electricity supply, I’ve never heard of anything like that………….

“that demand over the ‘past three months’ has dropped ‘year-over-year'”

Wanna guess what sounds bad with that statement?

CDO’s are making a comeback according to todays (9/26/17) Business Insider’s article by Graham Rapier. The CDO’s are making a comeback due to investors seeking higher earnings. The CDO’s are promoted as earning as high as 20%.

‘A Citi spokesperson reiterated that the products were fundamentally different — and thus safer — this time around because “every part of a synthetic CDO deal is distributed to investors.”

We have lower requirements for mortgage borrowers, and CDO’s back. I thought smart people were running the world. They are all just one trick ponies

In all fairness; the underwriting standards and mortgage products are no where near as risky as they were during the last bubble.

It is truly night and day in difference; and I know from 1st hand experience as a mortgage broker/lender.

We may (or may not) be in a bubble; but, it is not caused by exotic products such as the previous run up.

Actually they’re far worse. We’re subprime nation x2.

Care to expand and provide examples?

Also; please list your expertise/industry you work in.

Art Vandelay The importer/ exporter ?

Elaine has me focusing on the importing

Just in time for QT and the other various central bank tightening schemes intended to squeeze homeowners out of their meager equity and firmly into default.

Reminds me of the good old days leading to the financial melt down when Greenspan was touting variable rate mortgages, in preparation for the squeeze.

Rinse and repeat.

I think they are still pretty strict going through the process right now, they almost don’t want to play ball in the low end stuff I can afford.

I’ve got plenty down, closing paid by employer, and at 45k a year (not counting spouse at all) with 50 dollars a month obligations they are busting my hump for a 120k loan 40 miles from Boston (way cheaper than rent). Mind you the property was 160-ish last bubble.

What I think they are doing is lowering standards on the high end markets because just that closing payment is enough to payout on the wider ponzi’s…

Incorrect.

The standards are much more strict when it comes to high end or “jumbo” mortgage programs.

I.E. 720 min credit scores and 43% max DTI (debt to income ratios)

To compare/contrast:

Conentional 620 min credit sore with up to 50% DTI

FHA 580 credit score with up to 57% DTI

The high end does NOT have looser standards.

If they are giving you a “hard time” you are working with a loan officer that does not know what they are doing.

Background: mortgage broker/lender writing all types of loans. Conventional, fha, va and jumbo

Incorrect.

The current scale of subprime dwarfs anything previous.

How about some examples to back up your assertion?

Lemme guess, you read it from someone claiming to know it all on zerohedge and referencing some obscure site.

I think you do not know what you are talking about and cannot have an intelligent conversation with someone up to their eyeballs in the industry.

How about refuting it with actual data? You won’t because you can’t.

You are the one making these bold assertions without presenting any data; not me.

What I do know is the industry as I have been in it for 15 yrs.

There are “non-prime” progams these days which are drastically different than the “sub-prime” programs during the last bubble.

The vast majority of loans written today abide by the ATR clause fo the Dodd-Frank rule. ATR = Ability to Repay which is the same as INCOME QUALIFYING

What that means is that loans are underwritten by VERIFYING INCOME; a major component that was MISSING with the sub-prime and Alt-A mortgage products last time.

Once again; you are making baseless assumptions and assertions and providing zero evidence; so don’t come in with that BS to someone that knows the industry very very well.

One needs to “be in the industry” to analyze the data? Nonsense.

PI is quite correct. The credit profile of the typical buyer is less than subprime.

I repeatedly hear that millennials don’t want to buy and when they do they want to be urban. This simply isn’t true, at least not once they have kids. Once millennials have children, they want the exact same things their parents did ~ a nice safe neighborhood where their kids can play, weekend cook-outs and excellent schools. And where I live, that’s the burbs.

Student loan debt and family formation holds them back but they’ll eventually get there.

This is a pretty good comment.

I think life for most, no matter the generational label, slows down once family established. And yes, most will want good schools, yards, a piece of property that isn’t 800 SQ ft.

NC John quoting “data” yet not presenting any?

What do they say? “There are three kinds of lies: lies, damned lies, and statistics.”

Anyways; my point is the following: sub-prime or non-prime programs exist today; I know b/c they are marketed to me as a broker/lender, however, they are drastically different than the previous run-up.

No 100% financing allowed (huge difference)

Everything is income underwritten via tax returns or bank statements (for self employed)

Etc….

I won’t come on here and tell you guys I can diagnose a patient with an illness as I am not a doctor nor will I cite data on symptoms of a illness; however, in my area of expertise I can assure today’s “non-prime” is dramatically different than the “sub-prime” or “alt-A” of old.

Lastly; I am not stating whether I believe we are or are not in a bubble (that I do not know), just stating the facts of today’s programs.

Bottom line.

American financiers are still arranging huge amounts of finance, for peopel who can not repay it in realistic time frames, to buy radically overpriced items.

The US is financing Autos over 84 months, and exporting that finance model as “The Norm”. Just a sit exported the insane housing bubble models that became the 08 correction.

This can only end one way.

Just like last time.

You US lame brains, dont listen.

Whne china is telling you what to do.

And that is the situation you are taking yourselves to. YOU WONT HAVE ANY CHOICE.

The only problem with that, is we will have to deal with the power-crazed chinese strip-miners, as. The world authority, due to US stupidity.

Up in Greenville, SC from which I recently decamped back to Florida, I was surprised to see an ongoing issue with foreclosures (2016-2017) in the very nice subdivision where I lived. Greenville is booming both in job growth and housing prices.

When we put our home up for sale, we discovered none of the buyers have any money for conventional 20% down loans and all of the offers were for FHA 3% down, VA 0% down, or US rural loan program 0% down, plus seller to pay ALL or a big part of BUYERS closing costs.

Luckily we found a buyer where we did not have to pay their closing costs. Our realtor advised all of these younger families have good jobs and can “afford” the higher payments with nothing down, but if anything goes wrong with a job, they have to sell or foreclosure happens.

How are these folks credit worthy in such a precarious situation? Our subdivision was filled with folks living paycheck to paycheck, with very large homes and one or two very expensive cars.

If housing prices merely stop going up, there is no equity to even cover the cost to sell the house.

If the layoffs start, the folks in this situation have no cushion to ride out a downturn…and these are theoretically prime borrowers.

So, even if things are very different from the days of NINJA or LIAR loans, a huge amount of downside risk exists for lenders purely from a standard recession, let alone another Great Recession…