This is how monetary policies have crushed the value of labor.

For the good folks who hope fervently that the Fed doesn’t have reasons to raise rates or unwind QE because there isn’t enough inflation, here is an update on one aspect of inflation – asset price inflation, and particularly house price inflation – where the value of your hard-earned dollars has collapsed over a given number of years to where it takes a whole lot more dollars to pay for the same house.

So here are some visuals of amazing house price bubbles, city by city. Bubbles really aren’t hard to recognize, if you want to recognize them. What’s hard to predict accurately is when they will burst. Normally the Fed doesn’t want to acknowledge them. But now it has its eyes focused on them.

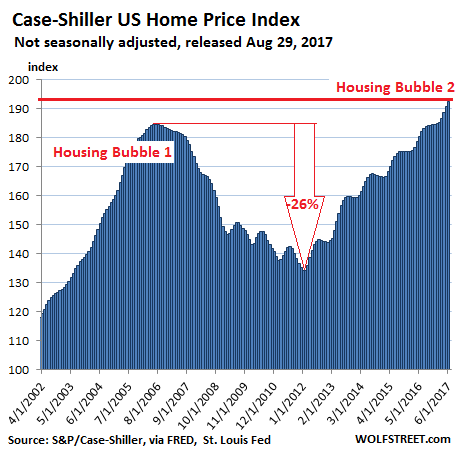

The S&P CoreLogic Case-Shiller National Home Price Index for June was released today. It jumped 5.8% year-over-year, not seasonally adjusted, once again outpacing growth in household incomes, as it has done for years. At 192.6, the index has surpassed by 5% the peak in May 2006 of crazy Housing Bubble 1, which everyone called “housing bubble” after it imploded (data via FRED, St. Louis Fed):

The Case-Shiller Index is based on a rolling-three month average; today’s release was for April, May, and June data. Instead of median prices, it uses “home price sales pairs,” for example, a house sold in 2011 and then again in 2017. Algorithms adjust this price movement and add other factors. The index was set at 100 for January 2000. An index value of 200 means prices have doubled in the past 17 years, which is what most of the metros in this series have accomplished, or are close to accomplishing.

Real estate is local. Therefore real estate bubbles are local. If enough local bubbles balloon at the same time, it becomes a national housing bubble. As the above chart shows, the US national Housing Bubble 2 now exceeds the crazy levels of Housing Bubble 1, and in all ten major metro areas, home prices are setting new records.

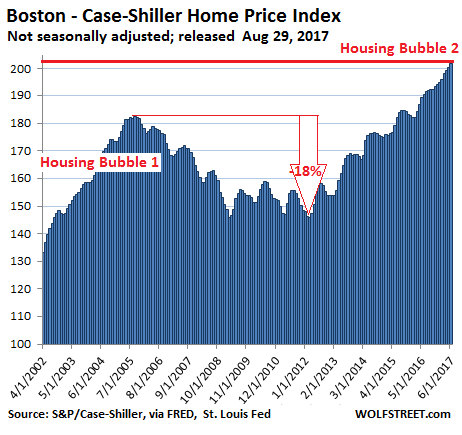

In the Boston metro, the home price index is now 11% above the peak of Housing Bubble 1 (Nov 2005):

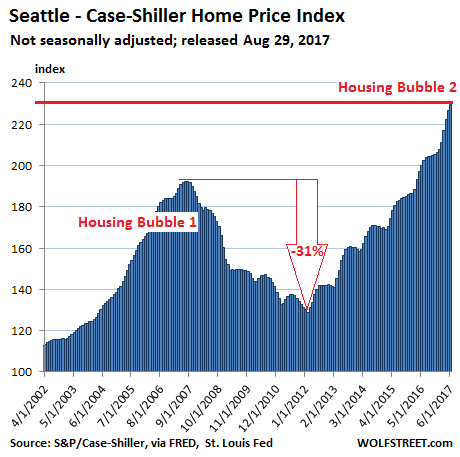

Home prices in the Seattle metro have spiked over the past year, pushing the index 20% above the peak of Housing Bubble 1 (Jul 2007):

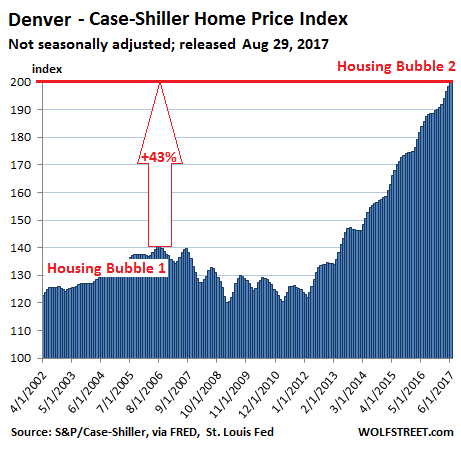

Then there’s Denver’s very special house price bubble. The index has soared a stunning 43% above the peak of Housing Bubble 1 (Aug 2006):

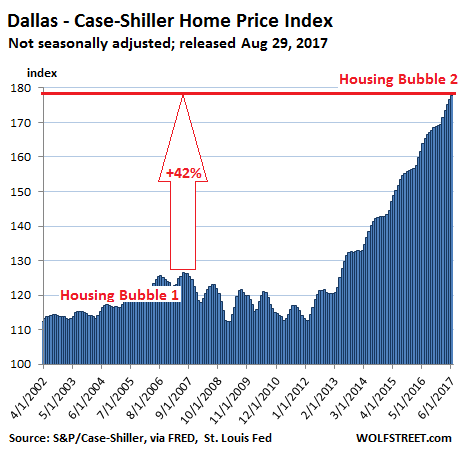

People in the Dallas-Fort Worth metro felt left out during Housing Bubble 1, when prices rose only 13% in five years, while folks in other parts of the country were getting rich just sitting there. They also skipped much of the house price crash. But they know how to party when time comes. The index has now surged by 42% from the peak in June 2007:

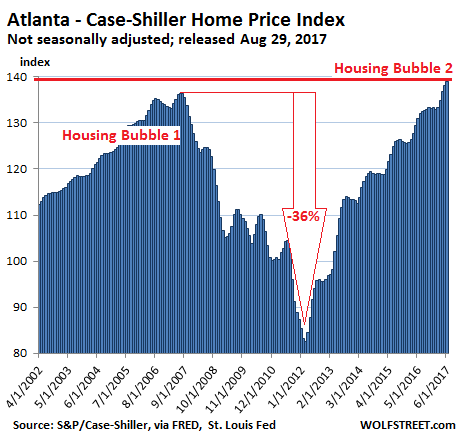

The Atlanta metro, where home prices had plunged 36% after Housing Bubble 1, has now finally squeaked past the prior peak by 2%, with a near-perfect V-shaped bubble recovery:

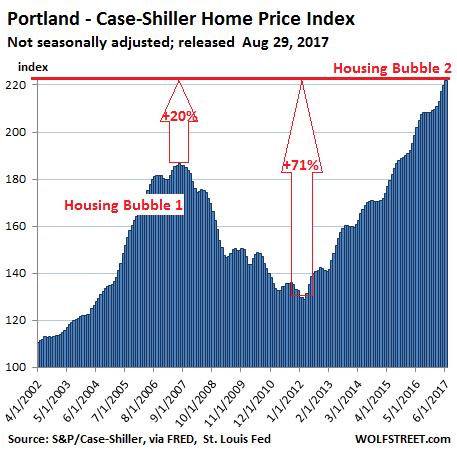

Portland’s home prices have kicked butt since 2012, with the index soaring 71% in five years – not that homes were cheap in Portland in 2012. Portland’s house price bubble is now 20% above the peak of Housing Bubble 1:

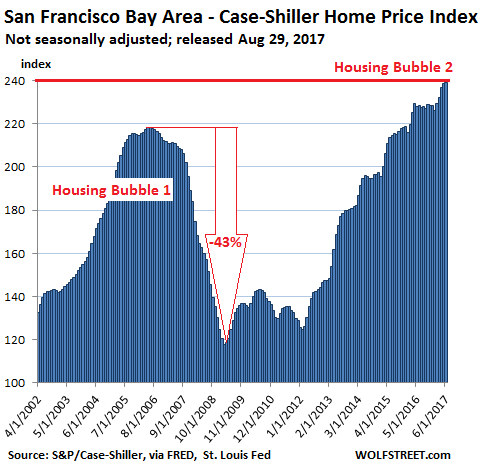

The San Francisco Case-Shiller Index, which covers the five-county Bay Area and not just San Francisco, is now 10% above the insane peak of Housing Bubble 1. During the last housing crash, the index plunged 43%. Eight years of global monetary craziness has sent liquidity from around the world sloshing knee-deep through the streets, which has performed miracles:

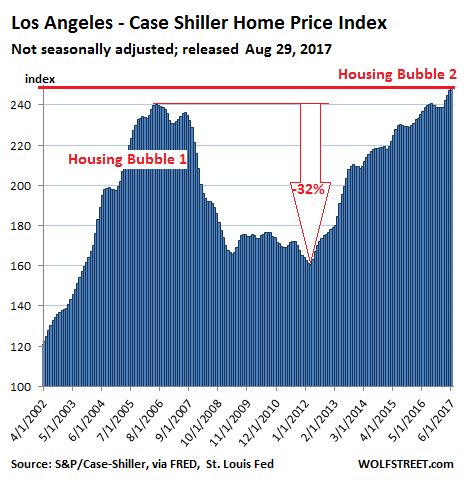

Los Angeles home prices performed similar feat, doubling from 2002 to July 2006, before giving up two-thirds of those gains, then soaring once again. The index is now 3% above the peak of totally insane Housing Bubble 1:

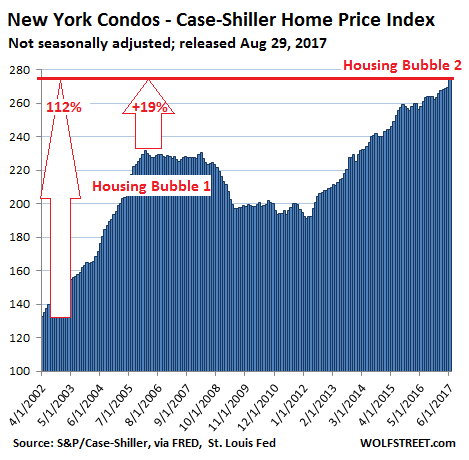

New York City condo bubble never saw the crash in its full bloom. Prices are now 19% above the peak of the prior bubble (Feb. 2006). Over the past 15 years, the index has soared 112%:

While the monetary policies of the past eight years have had no impact on wage inflation in the US, and only moderate impact on consumer price inflation, they’ve been a rip-roaring success in creating asset price inflation.

Asset price inflation means that the dollar loses its value when it comes to buying assets. Wage earners, when they’re trying to buy assets today – not just homes but any type of asset, including buying into retirement plans – are finding out that their labor is buying only a fraction of the assets that their labor could buy eight years ago. This is how these monetary policies have crushed the value of labor.

But this is causing some wrinkles. Ludicrously high home prices in the Bay Area are now coinciding with the end of the employment boom? Read… San Francisco Bay Area Pending Home Sales Plunge

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Nice article Wolf, but i’m not so sure prices are local as stated. After all, banks tend to be national and they all want to create debt. That said I do realize there is still a location factor involved.

Housing prices ARE indeed local. If you travel at all, you would probably look at prices of similar housing to yours in other locales, and marvel at the differences. I know if I relocated my home from Tulsa, OK to Dallas, TX, the “value” would be over 2X higher.

But bank lending doesn’t work this way. At 80% LTV, I can’t walk into the bank and say, “I want to have the amount of my loan based upon the market value of my house relocated to the Dallas market.” House prices (and the mortgages attached to them) are based upon the contract price and comparables for the area, not some appraiser’s estimate for what you could re-sell the house for in a higher-value housing market.

The largest factors causing localized price changes are population growth and an influx of buyers from other areas. If Tulsa were to get an influx of buyers relocating from San Francisco, I guarantee there will be an upward revision in local housing prices. However, this increase would not change the prices of housing in Wichita, KS, a city with a similar-size population and similar housing prices.

In conclusion, my 20 years experience in real estate, both in sales and lending, show that residential real estate pricing is almost entirely local. Over 99% of the price of a house can be correlated to local factors. The exception is showcase spec homes, which are less than 1% of all houses sold nationwide, both measured by units sold and by dollar volume.

Since I recently moved to the Dallas area, I can add some context here. You mention that 99 percent of the price of a house is local. That is simply laughable! It can’t possibly be true after QE1, 2, 3 and the trillion plus in mortgage bonds that were purchased to drive down rates and reflate prices. Of course there are local factors dictating on how the various distortions manifested, but the unfortunate reality is that the Federal Reserve has DESTROYED asset price discovery and any concept of “markets” in general. Why? Well, any thinking person can surmise a guess at who the FED is interested in saving, protecting.

It would seem that you are mixing housing and stocks together as a communal asset class, as you describe the various terms.

More than anything else that has raised both asset classes is speculation, pure and simple, and the ACCESS to money that 80% of Americans had no change of tapping. Banks, hedge funds, those 1%ers and the like drove both of these asset classes to this level as if they were collecting Bennie Babies.

Indeed the disturbing and complete lack of economic understanding of our modern economy by the FED ‘experts’ has place everything in harms way again.

Rinse and repeat, until the group who ends up owning everything is measured in angstroms .

And, if you do not believe that real estate prices are ‘local’ then perhaps you might consider penning a book for Amazon. I do suggest that you visit Detroit, Baltimore, Newark, and many other places before you pick up a pen.

The local nature of real estate results because when the Fed prints money, it does not go everywhere equally. For example a Tech IPO may create a couple of millionaires in San Francisco and New York and generate 100 jobs between the two metros but may not have any effect anywhere else. Real estate prices also depend on supply constraints which are different in different areas. Where new home production supply closely matches demand and there is good competition between builders, prices cannot drastically rise overnight. Some areas have more constraints than others depending on zoning laws, availability of buildable land, power of nimbys, availability of highways and public transport, influx of jobs or foreign money.

Though median and average prices of homes have reached new highs recently, majority of homes are still below their 2007 valuations

https://www.usatoday.com/story/money/2017/05/03/prices-most-us-homes-remain-below-precrash-peaks/101199766/

This is because of various biases in the data where bubble cities have more transactions skewing the data.

The fact the fedS blanket policy is what has made country wide stupid housing prices possible doesn’t change the fact that local factors are the largest determinant of a homes desriability, and therefor price. As a variable in figuring pricing the fed only pulled one lever. Is just happened to be one that massively raised the bar on what a sustainable home price is even in the face of supposedly tight lending standards.

a house like a car is a liability. there is a critical level where the cost to own and operate exceeds the seed cost of the investment, and then manufactures start giving the asset away, in consideration, and under their terms of use, and a monthly fee. (you can have an expensive Iphone free if you buy their service package) how much does it cost to operate a million dollar home? a classic sports car? you don’t want to know. in point of fact asset values in some items are really about zero. Hussman makes the point differently, he says a stock price reflects a claim on future earnings. while a home price reflects a claim on future liabilities. so why would anyone get involved? because prices keep going higher, you pay more for you obligations later on, and you can leverage those assets. remember the 2007 housing bubble, the home ATM, people were tapping their equity to improve their homes. improving your home reduces the future liability and helps raise the nominal amount of leveraged assets you can draw on.

“…a guess at who the FED is interested in saving, protecting.” Yep. Bankers and bureaucrats. Reflate the loan security so the banker has absolutely nothing to worry about, and keep that inflation number at a steady 2% nationwide so tax revenues climb like clockwork. All quite predictable given that the Fed sits at the nexus of both.

I may be wrong BUT is not the comparison approach to setting a home price, value and eventual sales price based on the local ie: very near to the subject home?? That would be local. And quite frankly QE monies have been given to banks and they are just holding the funds? No?

Maybe a better (more accurate) way to frame it is to say that Housing ‘pricing’ is local, but the rate of price ‘change’ is national/global? All relatively speaking.

There lots of places in the US and everywhere where the same house can be worth 25-50 % more within a mile of the other house. In super status- crazed areas the distance between the right hood and the other can be a few hundred yards. It kind of boggles the mind that anyone wouldn’t know this.

BTW: there’s a good true crime book called ‘Murder in the Hamptons’ where the female villain, a total fashionista bitch, stops talking to a friend because the friend moves from the East Hamptons to the other Hamptons, not far away.

” In super status- crazed areas………” Truer words were never written. And that mindset skews all kinds of markets. And the craziness just keeps getting crazier.

I think its obvious that the FED knows exactly what it’s doing. Your charts say it all.

Since they know what they’re doing I think it near certain there will never be rate normalization, whatever that is. Until people are rioting in the streets for lack of housing there will be no change.

Look at Canada’s housing market , which is still going bonkers after over 10 years!

Since this market is driven by corporate speculation, the consumer is cut out of the loop and this makes the US housing market even more bullet proof – that is the homes don’t even need to be occupied! The prices will rise as more and more corporate money flows in.

As I only see the economy getting worse, rates will stay low and this is very bullish for housing.

Yes, that is saying it cut and dry. San Francisco is at 1.4 million right now. There may be a bit of a correction but in 10 years the median house prices will be well over 2.5 million. At that point, only the foreign money launderers and corporations will be able to purchase houses.

Prices fell 45% here in the Bay area during the last minor adjustment. I expect a much deeper and longer correction this time. 10 years from now we’ll likely see prices at the late 70s early 80s level.

Never happen. The Fed will print $10 trillion next time to prevent it.

They did that last time and prices fell. Prices are falling already in spite of their failing approach.

Seattle, WA, in the house.

woot woot

Land of perpetual AMZN and Zillow options. And the worst plastic shite RRE on the planet.

It’s a permanent plateau, a new normal, a City on a Hill to all of you flyover savages … save me from the madness …

Until it breaks. My sister once owned a home in Kirkland, right on the Bellvue line. It has gone up and down in value. After the last boom they tried to sell as they had already relocated to Camano Island. They tried to sell for over a year, staged with rented furniture no less. They finally had to rent it out to 4 university students for a couple of years. As this latest bubble started to rise, they finally sold to a couple who were speculators.

Bubbles don’t last forever. All it takes is a burp, or another change in technology or the World economic situation. Then, those little farms in flyover look pretty sweet compared to over-priced suburbs. North Korea is a good example to use as a changing force. If hostilities ramp up the sanguine trendy coffee culture of Seattle looks a little worrisome and nothing to base a move to Seattle upon. Amz tanks? Never say never is a good idea. A very good high school friend used to run a steam plant at a Vancouver Island pulp mill. He has always made very very big wages as a 1st class steam engineer. There used to be 5 pulp mills on the Island. Two are now left; one is employee owned and the other has been sold/receivership/sold a few times. The other three were shut and are awaiting demolition. It took recycling and the use of corn stalks for pulp when the ethanol craze (subsidies) hit to destroy the industry, and destroy it did. He now works away making the same big salaries, but he lost every dime of his pension as he was management with no Union to ensure it wasn’t raided as an asset. He lost 35 years of pension contributions to a hedge fund based out of New York.

Boeing? Not worth banking on for a long-term future going forward. Amazon? They still haven’t made profit as I understand it? Silly Valley? Remember the 2,000 tech bubble?

Houston just went underwater and North America’s largest refinery has just shut down. Who knows how things play out in these large over-valued cities. Shelley said it best:

“I met a traveller from an antique land,

Who said—“Two vast and trunkless legs of stone

Stand in the desert. . . . Near them, on the sand,

Half sunk a shattered visage lies, whose frown,

And wrinkled lip, and sneer of cold command,

Tell that its sculptor well those passions read

Which yet survive, stamped on these lifeless things,

The hand that mocked them, and the heart that fed;

And on the pedestal, these words appear:

My name is Ozymandias, King of Kings;

Look on my Works, ye Mighty, and despair!

Nothing beside remains. Round the decay

Of that colossal Wreck, boundless and bare

The lone and level sands stretch far away.”

RE valuation is certainly local, yet is also driven by external forces. If I could move my home 50 miles it would double in value. 150 miles it would climb 4X. In downturn periods it seems to keep to the same ratio.

regards

Good stuff but Boeing is doing fine, solid profits.

Boeing, The Company…is doing fine for now. The workers and their prospects, not so much as The Company continually threatens plant relocation and closures.

I fail to see a future in the airline industry. It’s going okay with today’s free money but it is a wasteful way to travel and terrible for the environment. Arriving 2 hours before flight time and undergoing screening is one main reason why we quit flying many years ago. Plus, delays, cramped seating, etc. :-)

regards

Thanks for the Shelley, still perhaps the best commentary on hubris.

Some of those dead white dudes were alright!

Couldn’t agree more. Houston could be the straw that breaks the camel’s back (and maybe breaks Trump too – I don’t see him being able to respond effectively to this kind of disaster).

People can’t get a return on their savings, and that’s a huge problem.

I received the funding notice today for one of my employer retirement plans. The return assumption is 6.5%. The plan is invested 30% in stocks, 55% in investment grade debt, and 15% in high yield debt. The plan appears susceptible to a general market drop.

I expect most retirement plans have similar investment composition. This makes me think the Fed will do anything to avoid a general market drop, and do anything to create some inflation. Inflation would help retirement plans by increasing investment returns and decreasing the real value of pension payouts.

Hopefully the general population will dethrone the Fed’s governors before they screw workers and savers like that.

No, there is one thing they will NEVER do to create some inflation: push to give workers more money in the form of higher pay and better benefits. They will try any crazy, inane scheme short of putting money in the pockets of the lower 85% of US earners.

Ha, ha. Yes, this is true.

On the subject of whether real estate is local, I’d say “yes” but less than it used to be.

Chinese investors are pushing up Seattle, Toronto, and Vancouver prices. S. Americans and C. Americans have long pushed up Miami prices. Californians are pushing up Austin, TX prices.

There is a lot of “excess savings” sloshing around with no where to go. Obviously, the big wave is Chinese but investment by Americans elsewhere in the States I think has grown a lot in the last 15 or 20 years.

It’s all borrowed money.

“… the general population will dethrone the Fed’s governors …” Bobber, how the heck can that goal be achieved?

Wall Street basically owns the Executive and Legislative branches of the federal government.

Hopefully the general population will dethrone the Fed’s governors before they screw workers and savers like that.

In 2008, Ron Paul ran on an explicit platform against the Wall Street-Federal Reserve Looting Syndicate. He got 5% of the vote. While the sheeple claimed to be upset about the Wall Street bailout, they turned around and voted for a Goldman Sachs-owned snake oil salesman pitching “hope and change” or the even worse GOP “alternative,” John McCain of Keating Five fame. So it is fair to say the vast majority of the sheeple are A-OK with being bent over by Wall Street and the Fed.

In 2016, Trump ran as an economic nationalist, but once in office wasted no time surrounding himself with globalist swamp creatures and “former” Goldmanites. Meet the new boss, same as the old boss.

Until the great mass of the sheeple become awake and aware and reject the crony capitalist status quo and its Republicrat duopoly water carriers, nothing is going to change.

how true! the fed will pop this bubble when they are ready. Total criminals. ” death to the money changers”!!

Ron Paul would have done fine if he wasn’t a right-wing loon.

Dear Wolf,

What is a bubble that cannot be popped?

A lot of folks (me included) have been talking of bubbles but see nothing popping so far.. doesn’t mean nothing won’t ever.

All I am saying is you cannot call an inflation in an asset class as a bubble irrespective of the mechanics that may have caused the inflation UNTIL such a time that the pricing of the asset collapses beyond a certain threshold.

As i have said in your blog previously, we might be in a twilight zone – such that the popping up of the bubble might get delayed a long road down the time OR may never happen.

Considering the SF bay area, irrespective of declining y-o-y job growth in silicon valley that you had highlighted, house prices are still going up..

And despite China supposedly tightening money laundering i see a lot of mainland Chinese in greater SF bay area open houses.

I really wish the bubble to at least hiss out some hot air if not deflate to allow me to not commit financial suicide by buying overpriced housing – but hope and truth are different beasts…

Again, not a bubble until it pops..

It cannot be popped if it is not a bubble.

Actually its more like it cannot be popped until it can . Remembering there are many underlying aspects to each and every bubble ( I’ve been posting some of the details of our Denver bubble here for months ) sustaining that bubble giving the appearance of not being a bubble until those underlying factors ability to do so finally falls thru the cracks

Thank you, thank you. I am so happy to see more and more people are talking about “the fed will NOT allow it” or “financial system is so resilient now that we will NOT see a crisis in our life time”. If everybody think so, then it is about time the change will happen.

What wil be the trigger? How can the FED allow it?

The trigger can be many forms, but underlying reason is simple. And when that happens, the FED can not help because if they do, they die.

It is called overpopulation of “mal-investment”, AKA, insolvent businesses that do NOT make money NO matter how much liquidity FED provides. You can borrow today to pay back yesterday and you can do this for a long time, but that liquidity will Never make you a solvent business. I can NOT give you better examples than Telsla motors, snap chats and the like. They call them “tech”, I call them mal-investments.

If providing liquidity by printing can make wealth, Zimbabwe would have been switzerlands. This is so simple and yet the FED makes the world upside down and people confused liquidity with solvency.

Insolvent zombie money losing businesses crowed out sound investments because FED short circuited the market. There will be a day when most businesses get corrupted into mal-investment and FED still want to liquidity it over, people will shook their heads and $ will be toilet paper.

You can argue everybody know Kim family ‘a regime in nor-korea would not last and yet the family ruled this long.

The FED is King Jung Un, and you think he will last forever because he has managed to do so…

“Insolvent zombie money losing businesses crowed out sound investments”

Publicly listed businesses that have no cash earnings, still exist because of cheap money. Yet private businesses with good cash earnings shrink. A recipe for disaster. A slow but certain poisoning.

Even Walmart shows negative Working Capital- no wonder they pay suppliers 90 to 120 days or more. Not the least of the reasons, because they can.

IBM has bought back more shares than their total Retained Earnings.

None of this is possible without Central Banking drawing on the credit of the nation to feed the insiders.

Thanks for clarifying that for us Mr. Greenspan.

If there is no fundamental shortage of a good, yet its price goes up and up, it’s a bubble.

With mortgages, I think you can define a bubble as when the mortgage is higher than you can rent the place for. Because at that point, it is no longer an investment instrument. It becomes a speculative venture. You’re losing money until you can get someone to buy the property for a much higher price.

The bubble pops when people don’t believe that they can sell at a higher price. Question is: what will cause that change in mentality?

I think many would agree that is one easy way to spot a bubble.

That is of course unless there is a rent bubble. It does appear at least some cities are experiencing rent reductions due to rental oversupply. It’s also possible a tech bubble could pop in say the bay and cause rents to collapse.

Yes yes Real estate is local, BUT the banking conspiracy to hook tax donkeys into a credit habit is global. See Nick Kamran’s post on this board from March 4 – where he notes that nordic interest only mortgages can go to “40, 50 and even 100 years.” (Are 100-Year Mortgages Next?) So John is right – and as noted by other authors – all fiat creation is from the banks via fractional reserve debt extension. The great depression survivors of the 1930s are dead, but I can remember my mother continuing to talk about the horror of debt from that period. That lesson is long forgotten. So this bubble won’t end until the banks get in trouble worldwide, and that will happen… who knows? But it will likely be some butterfly that provokes a psychological stampede of greater fools towards the exits.

The Chinese property bubble will need to pop and the Nasdaq will need to correct by at least 10% before we see any reversal in price direction in most of those cities mentioned above.

New construction of MFH’s crashed by 34% last month Y/Y but the new construction of SFH’s is firing on all cylinders.

I’m watching the monthly number on SFH permits and starts as well as reports from major builders like Horton, Lennar and luxury builder Toll .

Moreover, it may be worthwhile to pay attention to earnings reports from Home Depot and Lowe’s for Same Store sales numbers, profit margins and guidance. Those guys have been on a tear for the last several years, so i think those companies, China, and the Nasdaq all need to roll over before we can see an end to this absurd global liquidity expansion.

I don’t think that poor restaurant, shopping mall and auto sales numbers by themselves are sufficient to send the US economy into recession.

The Chinese property bubble is already popping….its just the Chinese figures are so fantasy to begin with that covering them up is easy.

The REASON the Chinese bubble is popping is that the Chinese insurance industry is collapsing due to the gov’t finally realizing that most of the ‘insurance policies’ being pedaled by the insurance firms were nothing more than pyramid investment schemes designed to raise money with little collateral and recourse. In the past three months, every major private insurer in China has been under regulatory scrutiny after the Chinese gov’t got tipped to what was going on after they ‘disappeared’ a major executive in China’s largest private insurer.

Proceeds were being used to buy ‘real assets’ both in China…but more specifically, OUTSIDE China using various chains going through Australia, Singapore, Hong Kong, and New Zealand cutouts. Since insurance products could exploit a loophole that avoided China’s tightening capital and ‘investment’ controls in an attempt to prevent a rapid (and disruptive) currency crash (via everyone seeing China’s currency reserves shrink dramatically).

“the (Chinese) ‘insurance policies’ being pedaled by the insurance firms were nothing more than pyramid investment”

I don’t know if it would be easy or hard to spot an Insurance Pyramid Scheme in a country that is entirely a Pyramid Scheme.

@akiddy111 “new construction of SFH’s is firing on all cylinders.” Sorry to “burst your bubble” but if you goggle “Doug Short Housing Starts” and look at his graph – you see that the present day activity is just above the LOWS of 1960s, 1970s, and 1990. In other words, it has RECOVERED to RECESSION levels. I would call that firing on one cylinder out of 6. All the millenials want to live downtown and they don’t want their old farts suburban McMansion – smart move with the Tax Donkey taxes that get raised yearly.

Yes the chinese bubble is popping, so is Canadas and now the US.

– Disagree. The words “monetary policy” assume that the FED sets the FFR but it only follows the 3 month T-bill rate.

– The game that’s being played is called “Chasing yield”. The newspaper I read, gave yesterday another example of this kind of game. A number of pensionfunds have invested in a Private Equity fund in the hope to get a higher yield on their investments. The PE company was surprised to see that they were able to raise that amount of money in such a short time.

Interesting article.

I note that as in other posts population growth has been ignored as a reason for some of the increase in prices.

Look at Denver:

So for 10 years the price of RE basically went nowhere (2002 to 2012) and then it took off like a rocket.

The population over that time period increased by about 140,000. From 2010 to 2017 the population increased by about 15%.

Did the number of houses in the area increase enough to handle the demand or was supply restricted causing prices to increase as shown in the chart.

By the way in the same period of time Melbourne, Victoria increase from around 3 million to just around 5 million people now and the prices of houses surged.

The population of NYC and Boston have not changed significantly in decades, yet prices continue to soar. Population certainly can be a factor, but you’d need to do some serious legwork to see where it is and where it isn’t.

I don’t know about Boston, but NYC easily has over a million more people living in it than the early 80’s, especially if undocumented immigration is taken into account. Additionally, Manhattan, Brooklyn and western Queens are getting heavy in-migration by ever-more affluent people, jacking prices higher.

A single rush-hour subway ride, compared to decades past, will demonstrate that.

Undocumented immigrant (illegals) are hardly affluent.

You’re right, they’re not, but I know they exist, since they’re my students – I teach immigrant high school students in Queens – and they’re living doubled and tripled up in the further reaches of the outer boroughs.

Look at my original comment, and you’ll see I referred to Manhattan (where everyplace is The Gold Coast), much of Brooklyn, and western Queens. In those areas, gentrification is beyond the beyonds, and high rents colonize ever more parts of the city.

Even the South Bronx (SOBRO) is showing early signs of gentrification.

Rents are falling in Manhattan and Brooklyn.

That very well may be, but it isn’t having much impact yet on poor, working and middle class New Yorkers, who are still being displaced from huge swaths of the city.

An 8% decline on a $5,000 per month apartment isn’t very meaningful to people living near or below the median income.

20% decline on the median ($2000) is much more meaningful. Give it time.

We shall see; it’s long overdue.

Being from Boston I’d agree that the population has not risen significantly, for every person coming in, another sells their home they’ve owned for years for massive profit. However, the high end Job market is really on the rise here, specifically in pharma so these people can afford these homes.. 11% over bubble seems safe considering Denver and a few others!!

The price of a house will always expand to the level of the credit available to buy it…

It isn’t an issue of housing supply, it’s an issue of credit supply.

In other words – just good ol’ fashioned usury (a word which has been removed from the lexicon it seems).

“Usury” may not quite be removed from the lexicon, but it’s certainly long gone from any kind of policy and legislative thinking that might rein it in.

Same with medical costs, college costs, etc…all driven by ONE THING: taxpayer and central bank subsidized CREDIT. They think they’ve created a perpetual motion machine with QE, but who knows!

Today’s mortgage rates are usurious?

Would you lend money below 5%?

Now if you want to talk credit card debt, and the vulture used car loans over 20% that is a WHOLE different story and I think usury could describe it.

Once you move an economy from production to debt-based consumption, it shouldn’t be surprising that nothing is really done to rein in housing bubbles.

After all, the main reason people load up and binge on credit card/auto loan debt is because they have the ‘confidence’ that the cash machine which is their house is putting on value on a daily basis.

Take that crutch away and the whole debt-soaked edifice soon starts to creak.

Perhaps the main reason is that they don’t have the money in their pay packet (if they have a pay packet!) to survive without credit. The days of one breadwinner are long gone.

I have a question for the smart people of this site:

I live in Manhattan. My condo appraised 3.1m. I bought 1.3 in 2010. Yes it’s bubble.

My mortgage was 935k but the most I could refinance was 625k last year which is the jumbo max until recently. A max that makes no sense when the average condo in my neighborhood is 2 mil.

People with 30million in cash get turned down also for higher numbers when non conforming (this is a real life example). My question is: why won’t anybody (banks or mortgage bankers) extend bigger mortgages? Puzzled here.

These would be “non-conforming” mortgages that don’t qualify for government mortgage insurance (via Fannie Mae, Freddy Mac, etc.). A lot of lenders offer them, but since they’re not taxpayer guaranteed, lenders charge more for them, and so the interest rate is slightly higher. Look for “jumbo” mortgage rates. The rates are advertised.

Wolf – Thanks for being one of the few to finally post the ugly numbers behind our very special Denver bubble . Though I’m assuming its because we’re still a minor city in compassion to SF etc too few other than the WSJ , NYTimes and now yourself have paid any attention to the abject and unsustainable madness infecting the Denver / Boulder greater metro area real estate market rapidly engulfing Colorado Springs and Ft Collins as well

FYI; re ; ‘ non confomring ‘ mortgages . Though I cannot speak for the rest of the country I can say unequivocally that multiple mortgages on a single property are being handed out like candy here lately to buyers unable to qualify for standard mortgages by private equity and independent lenders .. most starting out as ARM’s to hook the buyer in .

Yes I understand that: but here is my experience: those non conforming jumbos are indeed offered and are advertised, however when you get down to doing the enormous paperwork (very high income of mutliple sources, millions in the banks, large assets , stellar credit etc…..) they WILL deny it. What Im trying to get at is: why do they offer those on paper and deny them in real life. What do they have to lose? (JPM, BOA, Mortgage depot, etc….). Are they not in business to lend? I smell a rat but don’t know what it is.

The closest analogy I can come up with: Delta airlines is affiliated with AFrance and KLM. You can go to delta.com and find itineraries with coshares operated by AF etc……you go thru all the line items and….when time to pay arrives there is suddenly a “glitch” and you can NEVER book those coshare flights.

Im not that paranoid but there seems to be 2 layers : one where business is open and offered and reality when practically it is witheld. It baffles me as to what is the purpose and who controls it.

It is more likely that they will have to retain the jumbo mortgage on their books depending on the amount. The market for conforming mortgages is very liquid and the market for jumbos is not depending on the amount. The entire mortgage market is designed to package conforming loans.

Very large jumbos are really loans to wealthy clients in order to retain their business. The banks know these clients are only borrowing to obtain tax advantages or because their other money is tied up in better investments, usually locked into one of the bank’s hedge funds, or some other investments.

Great questions. I don’t think you’re the only who is experiencing this.

Savvy investors may be more likely to walk away from a Vince McMahon type haircut, no?

https://www.federalreserve.gov/econresdata/ifdp/2016/files/ifdp1186.pdf

Is the question here, why won’t a lender let you refinance a mortgage at a lower interest rate beyond $625k? Am I understanding correctly?

Banks still make most of their money on interest, with fees growing more and more. The genius traders bring in far less than they think they do once you factor in their salaries and bonuses.

Upwards of 70%-80% of loans are for mortgages. Money is created every time they give out these loans. In effect, the banks are the landlords of mortgage-holders of America. They just don’t get a cut of appreciation in a sale. But they also wouldn’t suffer in a loss, assuming no foreclosure.

So, if their primary source of income is mortgage interest, why would they be interested in lowering your rent? Competition? Perhaps it’s collusion that’s at play.

The Fed’s engineered boom-bust cycles every eight years or so have been the most efficacious means of transferring the wealth and assets of the increasingly pauperized middle and working classes to the Fed’s oligarch partners in crime. The Wall Street-Federal Reserve Looting Syndicate, aided and abetted by captured regulators, enforcers, and “public servants” (cough) have used these rigged and manipulated “markets” to set up another massive pump & dump; now that the last of the retail-investor muppets have been suckered in, it seems likely that Goldman Sachs will order its helmet-haired hobbit at the Fed to hike rates and implode the Ponzi, enabling the Great Muppet Slaughter of 2017 to commence.

We will not have honest markets, sound money, or a future for our children as long as the Fed exists and is free to conduct its swindles and scams with impunity.

“I am afraid the ordinary citizen will not like to be told that the banks can and do create money. And they who control the credit of the nation direct the policy of Governments and hold in the hollow of their hand the destiny of the people.” Reginald McKenna, as Chairman of the Midland Bank, addressing stockholders in 1924.

I’ve said this many times . The more you read and listen to the commentary from 1921 to just before the Wall Street crash of 1929 … the more familiar it sounds and reads to todays news and announcements .. almost verbatim . e.g. SSDD … and here we go . Or as a friends song title put it ;

” The dog the dog he’s doing it again “

The pompous prognosticators of 1927-1933. Sounds very familiar. History may not repeat itself, but it definitely rhymes.

http://www.gold-eagle.com/article/1927-1933-chart-pompous-prognosticators

“Gentlemen, I have had men watching you for a long time and I am convinced that you have used the funds of the bank to speculate in the breadstuffs of the country. When you won, you divided the profits amongst you, and when you lost, you charged it to the bank. You tell me that if I take the deposits from the bank and annul its charter, I shall ruin ten thousand families. That may be true, gentlemen, but that is your sin! Should I let you go on, you will ruin fifty thousand families, and that would be my sin! You are a den of vipers and thieves. I intend to rout you out, and by the Eternal God, I will rout you out.”

— Andrew Jackson (1767-1845), addressing the would-be central bankers of his time. No wonder the Powers that Be want to remove him from the $20 bill and replace him with Harriet Tubman.

This just saddens me. This country has been corrupted into a shape that Andy Jackson would be mocked by the common crowd who take on loans they can NOT afford and wait for transferring wealth from other poor working families. It is NO longer speculators VS the common families. It has morphed into common families are competing each other to death by taking on debt they can NOT afford.

House prices correlate inversely with interest rates (e.g. the lower the interest rates, the higher the prices). It is the product of those two factors that determines the size of the monthly payment, which is how the average home buyer evaluates his purchase. If interest rates come back up, house prices will decline.

In Florida insurance curtails price, especially at the low end, because it is so expensive. Some might say that the cost of hurricane and flood insurance contain the prices of the homes that require the insurance.

If as a result of Houston, govt flood insurance is ended, then you will see real estate prices drop like a rock there, because private flood insurance will be very high.

Agreed. If you got rid of the federal flood insurance program, property values in Florida and other coastal states would drop like a rock. People could never afford private flood insurance. That act alone would collapse banks due to the loss of collateral values, collapse employment due to the loss of construction jobs, collapse local governments due to the loss of property valuations.

If you want to “pop the bubbles”, just pass a bill to get rid of taxpayer backed flood insurance.

That would be politically untenable. Flood insurance by government is a taxpayer-funded subsidy extended to areas such as coasts and flood plains that private insurance would not offer. As is usual for government programs, it incentivizes the non-viable and irrational – inducing the element of moral hazard for people to build and buy in areas that they might otherwise not.

This is a general observation of your observation that the event in Houston may affect insurance for all areas – not to suggest that Houston in particular is non-viable.

Ditching the mortgage interest deduction is ‘politically untenable’ too but that too is on the way out.

Each of these city’s housing “bubbles” share some common drivers. Most of which have been identified in prior comments.

1) Supply has been restricted. Many boomers aren’t selling, at least not yet. Many have decided to retire in place; particularly if their house has not appreciated greatly. Thus the dearth of modest price used houses for sale. Others with more equity may have taken out HELOCs or decided to wait a few more years.

2) Demand has increased. Overall, a number of younger generation folks are ready to buy. These are ones with fairly decent incomes and/or perhaps a legacy gift from aging parents. This base demand is supplemented in some cities by migration of boomers for better places to live/retire. Denver comes to mind.

3) Demand is also clearly driven by ZIRP and financial repression from Fed. People are looking for avenues to get return on their money. Since you have to have a place to live, the house seems a logical choice.

Having said all this, a couple of thoughts on the topic of “bursting”.

1) Barring a huge national recession with major layoffs everywhere, some cities are less susceptible to a ‘bursting’ of the ‘bubble’. If the economy is not too highly specialized or focused, the city will do better. Denver comes to mind again. On the other hand, Silicone Valley is highly dependent on a hyped up tech sector. If that turns down for any reason, it may not do as well. Seattle comes to mind as well.

Without a recessionary driver (e.g., loss of industry, loss of jobs), I seriously doubt that these house prices will crash, unlike 08/09. That crash had a totally different driver and way more overstretched players.

Also, I don’t believe for one moment that the Fed will be able to raise short term rates much above current levels. Oh, they will talk a good game and perhaps a couple more 1/4 point moves, but that will be it. The US and developed economies cannot survive on higher rates.

Except for more vulnerable locations, I predict that these prices are here to stay for some time. When they ease down, residual demand will step in and bring them up. Likewise, if they move higher somewhat, more supply will likely be created.

So I think these prices for the most part are the new normal across these desirable cities. Again, barring a major recession across the country or in specific cities, as stated above.

I know this isn’t a very dramatic prediction; pretty much milk toast at best. Good for another 5 years or so.

I thought the same in 2006 and many people had the same thinking that these high prices are the new normal.

But the housing busy has happened many times not just one two or three times in the history..

The reasons are all different all the time but the impact was same .. price crash

I think a major recession or depression is around the corner. All the problems for 2008 were kicked down the road, and not solved.

Dallas is an interesting case. Notice the barely noticeable “Bubble 1”. I have friends in Dallas who say they never noticed the 1st bubble collapse. Housing prices never really went up or down, and they didn’t even see a recession (granted these folks are fairly well off).

I was told that Texas was different because their state constitution essentially forced banks to require a 20% down payment on houses. Which, in theory, should put a top on housing prices as you reach how much the average Dallassian has in cash to put down.

However, that theory is obviously junk as “Housing Bubble 2” has taken off in a might way. If you’ve ever been to the greater Dallas/Fort Worth area, you know it is on a flat plain extending I guess to Canada. So there is nothing holding back development as the population grows.

So, my notion of how capitalism and the housing market should work is betrayed by Dallas. Anyone from that area have any insights?

All the western states learned from the mistakes of the eastern cities and incorporated large cities in their states. Houston and Dallas were incorporated as huge geographic entities on purpose. The larger the cities the less demand pressure exists on prices. This is why Texas has always been an attractive place to live, until recently.

Back in the 80’s a company I worked for had a Dallas office. While the pay for the Texas staff was low by NYC standards, they all lived in McMansions which cost them at most one year’s salary. Nobody ever relocated out of Dallas to NYC.

I’m in Dallas. Yes prices are higher than before. It feels like a bubble when you look at all the apartments and condos going up in my area. However, we have a TON of people moving in from higher cost states who look at our home prices and think, “hey this top of the market home is a great deal compared to the market I’m leaving”. The homes in my area are also being torn down and rebuilt with signficantly more square footage, so I’m not sure how that impacts things.

The economy of Dallas has been very strong, and I hear very little concern about the housing costs. Property taxes, OTOH are a constant source of complaint.

“Property taxes”

One of the many reasons why those in a position to actually change things (no, not clueless Joe and Jane Sixpack voters) continue to subscribe to an economic theory and models based upon it that have been proven over and over again to be absolute garbage and which are regularly and effortlessly panned on sites like this. It benefits them, both governments and the ACTUAL owners of governments.

It is not written into Texas constitution to require 20% down payment. Minimum is 5% down but you have to purchase Private Mortgage Insurance to make up whatever the difference to the meet 20%.

I have not seen any collapse of housing with the exception of the 80s S&L + crude collapse. That was brutal. Housing prices stayed solid during the recession and the more desired areas actually saw an increase in value. Now the sheer amount of companies moving here to headquarter has caused a take off in prices.

Correct, lots of land here with no geographical impediments (except Oklahoma border. LOL). There are some real hidden treasure areas in the towns and cities near Dallas and Ft. Worth.

BTW: People from Dallas are called Dallasites, those from Houston are Houstonians….but we prefer to be called Texans first. ;)

Real estate will crash when stocks crash. Same as 2009.

Stocks may crash any moment given all the potential black swans out there. Plus, the stock market is at a level where it could crash under its own weight for no apparent reason other than valuation.

Black swans right now are not bigger than the economic positives like

-record low unemployment

-40 year lows in unemployment claims

-artificially low interest rates

-Consumer FICO scores have never been better.

-wage growth

-corporate stock buyback

-banks are sitting on trillion in deposits

IMHO…. a real black swan will occur when interests rates really do increase, defaults on debt begin to occur, liquidity drys up for new debt, and finally then unemployment claims will start to increase for a few quarters but needs get above 350k.

You forgot the largest positives….

Falling housing prices and massive housing supply.

Lowering interest rates on home loans long term seems to me one of the worst ways to increase home purchasing power for families. Mainly because it gives the same aadvantage of cheap leverage to speculators as well. But also in a general sense, it would seem to be logical that if you give everyone equal access to larger cheaper loans, the market prices will just shift to fill in the hole gap created by our additional spending power.

There was a brief window where those with cash for a down where able to truly get homes both cheaper and at low interest. But now the low interest is just a joke because it is the only thing justifying our high purchasing prices. In its absense price would simply have to go down, our people would have to expand their housing budget.

Is this data in real or nominal terms?

Nominal

GDP for 2nd quarter revised to 3.0%.

Inflation? No inflation here –> reduce GDP deflator.

Where’s the beef? – Our leadership kicked the can down the road.

I don’t have data to support my claims so please take my opinion with a hint of salt (or a bag of salt).

The stupendous increase in real-estate price is due to centralization. With the Rust-belt and other regions being obliterated, the new generations are moving to where there are jobs. The employee profile is generally directed and based towards the social sciences/economics sector, incentivised by the world they see around them. Jobs that are present are in service/insurance/banking industry, that for some reason likes to reside in large metro areas (workforce availability I assume). Hence the trend. Though manufacturing and agriculture are present, from the little I have seen it’s not the dominant economic factor.

People are going where the money is, and as long as Wall street has the upper hand, this trend will not change.

Like another person commented, there is a good deal of real estate speculation occurring. Certainly that is partly due to higher rental rates, which translate into higher real estate prices, and widespread beliefs (from personal experience, real estate books and ubiquitous video ads) that real estate usually rises in price. As an aside many of us have lived through exceptional times, from the 1950’s to present day insofar that, despite a few outright crashes in the prices of real estate, the underlying property has continued to well outpace inflation, and in fact has created a good number of multi millionaires. Pretty much everyone now believes that real estate is a good investment. This has to be one red flag for “investors”.

There is another factor in favor of real estate, especially multi family, and that is the US tax code was written for real estate investors (and the oil industry). I sheltered my ongoing income from multi family for years, and then did a 1031 exchange, escaping paying all capital gains taxes. (but the IRS can recover the capital gains if you do sell eventually, but if you die, you have totally escaped paying!) I recognize that this is no better than the government subsidizing solar panels, or Tesla automobiles, or flood insurance. There is no level playing field in the US

The right real estate, if bought correctly can cash flow but you won’t get rich on it unless you’re building it. That’s for certain. Residential housing? You’ll lose your shirt.

Serious question here, I believe all of the data points to a second real estate bubble, however looking at the national data and local markets aside, would there be a significant perception difference if say housing prices peaked in 2007 and then stayed flat for the next decade versus the roller coaster that we’ve seen?

Would the perception still be “Bubble 2” or would it be stagnant/deflating real estate prices that increasingly look like good investment opportunity?

Wolf,

What about income-to-rent and income-to-mortgage payment ratios? Isn’t that every bit as pertinent as examining price alone? I know you alluded to incomes, but I’m curious to see the actual ratio data, especially in relation to historical.

So what happens when rents are dropping? Working on that article right now :-)

There is a relationship between rents and home prices, but it’s not in lockstep, and in some places, the two have separated. Rents have followed behind up to a point, but rents face resistance: you have to pay rent with income. But you pay for home ownership with a low-interest fixed-rate subsidized mortgage whose payments won’t change for years. So home prices can rise far more than rents before hitting insurmountable resistance.

Houston -we have a problem-4 out of 5 effected homes do not have flood insurance according to Washington Post today. Prices will come down fast and remain down for long time. Dallas home market likely to benefit from stronger demand due to replacement and abandonment of Houston by its businesses and people. New Orleans lost a sizable percentage of its population and it has not recovered. 12 EPA designated Superfund sites of the most polluted land along with large tracts of moderately contaminated industrial sites from the oil and gas industry have just had their toxins mixed, spread and redeposited in the yards and well water of whats left. Bubble popped there. Contagion??

https://www.theburningplatform.com/2017/08/27/in-search-of-a-chocolate-babka-in-nyc/#more-157717

When you see hundreds of skyscrapers being constructed with no particular demand for the space, you realize it is all speculation by gamblers posing as developers. And the person providing the easy money for the gambling is our favorite Ivy League troll – Janet Yellen. When central bankers keep interest rates this low for this long they are encouraging bubbles to be blown. NYC is a huge bubble waiting to burst. As we sauntered all over the city, I observed the hottest new retailer – SPACE AVAILABLE. There are vacant storefronts all over the city, including 5th Avenue. A critical thinking person might question the “strong economy” narrative being spun by the politicians and media.

NYC is dependent upon Wall Street greed, tourism, consumerism, and denialism. Yellen’s only purpose in life is to keep the debt based delusions of a failing empire propped up with easy money. When the next financial crisis, created by her easy money policies, arrives, NYC will be ground zero. The vacancy signs are an early warning. When major retailers fail during the “good times” the canary is on life support. The fake economic recoveries in Europe and Asia are built on a quicksand foundation of trillions in government debt.

When the sh*t hits the fan Wall Street banks will be crushed, tourism will halt, construction will grind to a standstill, jobs will evaporate, and consumers will stop spending like drunken sailors. The implosion of NYC will be one for the history books. Without the materialistic delusions sustained by easy money and a Himalayan mountain of debt, NYC is just a crowded, filthy shithole, inhabited by angry, scowling, egocentric, unhappy people. When it all comes tumbling down I wonder whether the bull statue near Wall Street will be pulled down.

Great article and great banter!

1- The QE money was loand to who? Businesses, large biz, Right? Are loans as easy to get as the subprime days for the masses? Ive heard, no! Are 30s+ buying these homes at these prices? I say, no they dont qualify, right? Then you have all the over supply from 2006 that sat vacant, so their and should be enough supply for US buyers, right? So WHO THE heck is pushing prices up? it looks to me like, corporate REIT’S, foreign buyers and people with cash to speculate. Whatever it may be, its borrowed money, and no bubble cant fly through the air without oxygen (possitve cash flow) for too long; money needs to be repaid, business loans dont work without repayment!

Do we know who are buying houses? is their title registry data?

2-Best unemployment data in Years. I just keep thinking about the 2 year rule for collecting unemployment, that was a while back and I think its still true. So what about all the uncounted who are off the grid now? and the people working two jobs part time who are not “employed” makes sense numbers look great, right?

3- When will the buuble bust? When Loans dont get repaid! However, maybe these wallstreet businesses will survive to get the next round of bubble soap to keep to it floating but….

4- statistically spaeking, what type of defaults need to happen where the QE money is endanger and lenders need to be saved. Wolf, its a big data set but we have faith :) Where will we see the cracks? Housing is just one place to look but the QE money is in the PE of stocks, inventory of cars, capital equipment, delayed losses.

Maybe Druckers model is true, our debt ratio is better then most.

If its predictable, their must be an offense!

I haven’t had a raise in 20 fucking years.

Self-employed?