Ludicrously high home prices hit end of the employment boom?

Real estate agents listed three reasons for the debacle of pending home sales in the state of California in July:

Lack of inventory for sale. This was the top reason for 30% of brokers. The math is starting to bite: more people are stuck in their homes as prices have soared all around, and as mortgage payments needed to finance an equivalent or nicer home have moved out of reach.

Declining housing affordability and “high interest rates” – which are near historic lows! – was cited by 28% of brokers.

“Inflated home prices” and “housing bubble” were cited by 25% of brokers.

Slowdown in economic growth, lending and financing, and policy and regulations were other “biggest concerns.”

These issues “may have pushed the market to a tipping point,” the California Association of Realtors said in its pending home sales report for July.

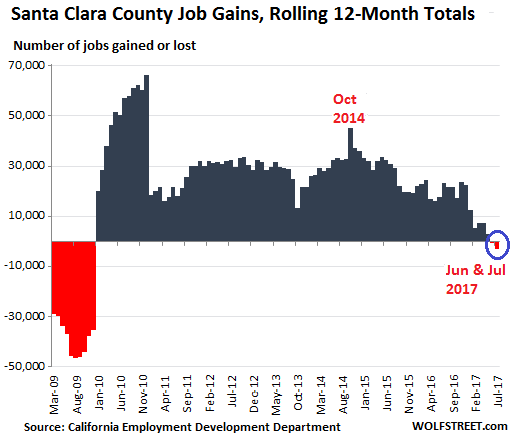

And a debacle it was, particularly in the San Francisco Bay Area, where home prices have become famously ludicrous, while the economy is backing off its previously relentless boom. Employment growth has slowed to a crawl, with actual job losses for the 12-month period in two counties – Santa Clara and Marin – a first since the Financial Crisis.

Overall for California, “the housing market is showing signs of slowing,” said the CAR report. Real estate agents “reported fewer floor calls, listing appointments, and less open house traffic than in June.”

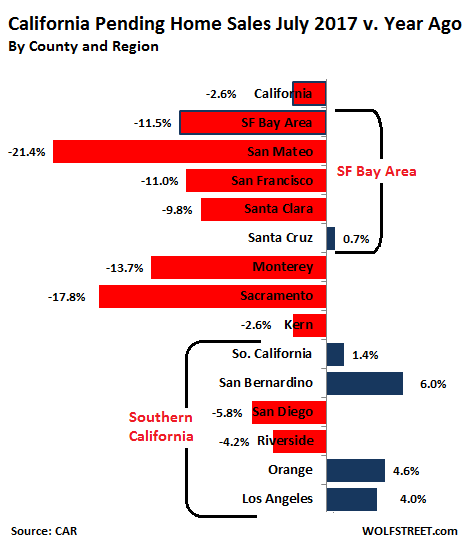

For California, the index of pending home sales in July, based on signed contracts, fell 2.6% from July a year ago on a seasonal adjusted basis. It was the sixth month in a row of year-over-year declines. But the overall decline of pending home sales in the state covers up the strength in parts of Southern California and the dizzying turmoil in the San Francisco Bay Area, where pending home sales got crushed.

In the Southern California Region, pending home sales rose 1.4% year-over-year, “the only major region” with an increase. But real estate being local, there were huge differences: In Los Angeles, pending home sales jumped 4.0% year-over-year; in San Bernardino County 6.0%; and in Orange County 4.6%. But in San Diego, pending home sales dropped 5.8% and in Riverside 4.2% year-over-year.

In California’s capital, Sacramento, where home sales had been hot, they plunged nearly 18% from a year ago.

And in part of the San Francisco Bay Area, pending home sales went over the cliff. In the region overall, pending home sales plunged 11.5% year-over-year. In San Mateo County, the northern part of Silicon Valley, pending homes sales plummeted 21.4%. In San Francisco, they plunged 11%. And in Santa Clara County, the southern part of Silicon Valley, pending home sales dropped 9.8%.

This chart shows the changes in pending homes sales in July compared to July 2016 for some of the major urban counties in California, plus for California overall (top bar), the San Francisco Bay Area overall (second bar from the top), and Southern California:

San Mateo County also has the honor of being the most ludicrously overpriced housing market in the state, with a median selling price of $1.5 million in July, according to CAR data. San Francisco is the second most ludicrously priced market, with a median selling price of $1.43 million

So could the end of the jobs boom in the Bay Area have something to do with the weakness in housing sales? This chart shows the rolling 12-months growth in employment in Santa Clara County. This southern part of Silicon Valley, which includes San Jose and Palo Alto, has started to shed jobs for the first time since the Financial Crisis (not seasonally adjusted data via the California Employment Development Department):

The end of the employment boom has spread across the Bay Area. Santa Clara and Marin counties have shed jobs on a 12-months basis. In the remaining counties, especially in San Francisco, 12-month employment growth has slowed to a trickle. And this comes just as the Bay Area house price bubble has reached highs that worry even real estate agents, as the survey above shows. So it’s not that hard to see a connection.

The Bay Area housing affordability nightmare hits home, so to speak. Read… How Insane Home Prices in Silicon Valley & San Francisco Trip up Jobs Growth

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

One would need to SELL their $1.5 million home in order to have the 20+% downpayment for the $1.5 million home they want to buy. Seems the coastal people have landlocked themselves into their homes.

What good is a home if it takes 2 hours to get there because of traffic? Might as well suck on an exhaust pipe. You could get some fresh air on a hiking trail, but have fun finding a parking spot there.

You could get out on a bike; some of the exurbs have some nice biking areas. But the exurbian is a sort of Ur-Suburbian, and suburbians don’t walk or bike. At least an exurban house will have room for some multi-thousand-dollar exercise machine. To hang clothes on.

Right On! Grid lock during commutes….same on weekends…anywhere!

I sold my house last year in SF bay area and renting till the house price comes down to earth again. It took 3-4 yrs for the Bay area prices to bottom out and while I think price won’t go down to the lows of 2010-11 it may get close if Great Recession comes back, unicorns die off, stock market bubble pops (happened in 2000 and 2008 so due for pull back or 2) and on-line ad revenue slows.

SillyCON valley jettisoned the old hardware stalwarts except AAPL and slow downs on online ad spending and social media may come as a shock to lot of snowflakes toiling away at countless start-ups. Inability for the unicorns to raise more money not to mention IPO points to general start-up bubble about to pop when liquidity dries off.

Sept is the worst month for the stock so watch out for the fireworks which may pop the other bubble – housing.

I just don’t see how that many people are able to buy homes like that…

Using Zillow’s mortgage calculator: a $1.5M home would require an annual income of $225,000 with a $300,000 downpayment and no other debts to keep debt-to-income at 36% (also assuming property taxes of ~1% = $15,000/year). This puts monthly payments at ~$6,750/month.

A single person living in CA with that salary has a take home pay of ~$10,800/month.

So, Zillow says this home is affordable for someone making $225,000/year. But, $6,750/month in housing costs is very spendy when total take home pay is $10,800/month. That’s only about $4,000/month for everything else.

I wouldn’t say $4,000/month ex-housing costs provides for the kind of lifestyle someone making $225k would expect – especially in high cost CA.

And what about taxes?

“A single person living in CA with that salary has a take home pay of ~$10,800/month.”

I think this starting assumption is probably off. I doubt many single people are buying $1.5m houses. So you’ve left of, in all likelihood, a second earner.

Property taxes are still a pretty small part of the total monthly cost of buying a home.

Probably a big deal for retired boomers on a fixed income, but for us now 30-somethings trying to buy a first home at today’s stratospheric prices, it’s an afterthought. (PMI would cost nearly as much as property tax in my neck of the woods, should I not be able to put down 20% or ~$120-140k cash for the median home).

It’s also pretty sad that it now takes 2 full time professionals, making a combined income that’s at the 96th percentile nationwide to afford a suburban home near the Bay Area.

God forbid one ever gets sick or gets laid off. Kids? Student loan debt? Forget about home ownership.

Move aside, “…that many people”. Big all cash buyers still abound, so it seems. These are investors parking money, awaiting a Stock Market crash, or short-term debacle, before it all swings up again.

The average family, seeking simply good residences in the Bay Area, ticking off half the desirable boxes: three-year search, it seems.

Recently bought in the East Bay, $750k. House across the street, vacant, owned by an out-of-town person, with his buddy in the neighborhood, keeping it up.

This could be a first.

Real estate is so overpriced that Chinese in need of laundering of ‘excess’ funds are looking elsewhere. Even ‘free’ money is going somewhere else.

Re the end of the Bay Area employment boom: So is the attached August 20 story, “Job market strong in Bay,” East Bay Times, whistling in the dark?

http://www.eastbaytimes.com/2017/08/18/bay-area-adds-21000-jobs-san-jose-oakland-san-francisco-san-mateo-july-strongest-workers-2017/

They’re using “seasonally adjusted” June to July changes in employment. I use “not seasonally adjusted” changes for the 12-month period from July 2016 to July 2017.

July employment data is always squirrely. There is a lot of hiring of interns and other seasonal employment factors. So it’s essentially useless to compare July to June (and it can be misleading).

The article as a whole has zero credibility because it never mentions the single most important piece of data: year-over-year employment changes. And for a reason! (because it might deflate their hype).

Exactly!!! Each company hires a TON of interns. Our company is not even doing that well and it appears each team has an intern.

I manage teams in San Jose for a tech company.

I think companies hire tons of interns basically as “free” labor.

There is a constant push in winter to get your interns lined up for summer.

As for housing I made the mistake of selling the two houses I owned in 2003. Worst decision I could make.

Im hoping this place burns hard in the next crash so I can use some of my cash to buy again.

Thanks. Very useful.

Thanks. Enlightening.

‘Oxford Economics Ltd. macro strategist Gaurav Saroliya points to another red flag for U.S. equity bulls. The gross value-added of non-financial companies after inflation — a measure of the value of goods after adjusting for the costs of production — is now negative on a year-on-year basis.’

This is off topic but related (RE is a type of equity) and just seems so incredible I had to relay it after just seeing from Bloomberg via Salon.

This is off topic but related and jsut

I think I must have misinterpreted this. He must mean inflation of value is negative. As written it could mean negative value was added overall i.e. the manufacturers as a whole lost money.

False alarm.

Thanks for the article, Wolf! The REAL bubble is in rationale. The generation in charge can rationalize a holocaust. I’m quite terrified of the stupidity. The Jackson Hole ignorance should be the epiphany that the entire planet should see, but everyone just cheers. Yellen’s “not another financial crisis in our lifetime”, and the Draghi ignorance yesterday with absolute BS about the global economy. We are a peak stupidity. I really have to wonder if the monetary boneheads see and comprehend was is happening with cryptos? Do they think it is a cool, new, fad? Everyone believes the stock market, or the housing market, or the bond market bubble will pop first. ALL WRONG…it’s the rationale bubble, and it just exploded.

It’s peak stupidity, but it’s stupidity heading towards idiocracy.

The law of large numbers is apparently taking hold. Everyone knew it had to happen. You could argue there will be a price plateau going forward, but when have we ever seen that? The behavior of the masses is reactive.

What do you think the law of large numbers says?

Interesting as the hot markets in SF, Peninsula and SillyCON sales are taking hit.

Guess greater fool theory will once again prove itself and those tiptoeing into peak housing like 2007-8 will learn a lesson or 2. With Chinese hot money and all cash deals dwindling the peak may be nigh.

I live in East Bay and houses were selling fast within days till June but definitely see slow down… Sold my house bought in late 2011 last year, and kicked myself seeing the price appreciate another 4% but renting ain’t so bad though family still complain about living in old house 60% less sq ft in less prestigious hood…

The effects if their gigantic QE holdings of treasury bonds are sold by the deceptively names “Federal” reserve banksters will push interest rates higher as the market is flooded with treasuries. Interest rates will then rise.

Home prices will collapse as fewer people can afford high interest payments. That unwinding supposedly will come soon. Home prices may be stalling as smart investors figure this out and do not invest in them anymore. Chinese capital export restrictions take out the dumb money, the uninformed Chinese millionaire “communists”.

Thus, prices will plunge.

The markets of all kinds drunk in QE driven ultra low interest rate may due for sober awakening… Only way to tame inflation monster rearing its ugly head is crank up the interest rate which combined with shocks to the economy ushers in stagflation like late 70’s with OPEC oil embargo which was the black swan back then…

I recall growing up in LA back in the 70’s when the mortgage rate was hovering in high teens selling feature was for the new buyer to “assume” the lower rate mortgage from the seller.

As for hot Chinese money, there is $50,000 annual individual quota to get the money out and well to do pay ordinary joes to use their name.

The game has changed from 06/09 time. You have’t git the memo? There is no more free market price discovery any more. Price will NOT drop, backed by currency and believe “them”, it would be enough. The definition of money has changed.

Think about this, if NOT enough people have concerns about what a $ is, they will keep printing to make sure asset will NOT drop so that debtors are afloat.

If enough people starts to wonder what a $ is, everybody will rush and short the $ any way.

So either way you have to SHORT $.

Take on debt to buy a house is to SHORT $.

Your long $ position will be punished.

I do agree that the price is very high.

All I am saying we are living in dangerous times where the every day Joe gets fleeced either way. I think living hedges is better than takin one directional bet.

There is a good chance that they print enough to price out everybody and turn everybody into rent serfs.

Heard an interesting anecdote the other day from a guy who worked in Hawaii (Oahu) with a chinese national. The chinese guy was a slum lord and always looking to acquire more property but was dismayed the past few years when he got outbid by other chinese, sometimes by as much as 500K! He told my friend that the market was crazy. We laughed – yeah, these guys are no doubt big time gamblers. I got the impression the guy didnt even like real estate, it was just a vehicle to amass wealth.

The article below is about the feds expanding their probe into money laundering. It includes SF in the list of places.

It cites condo prices as being down significantly in Miami too.

http://www.miamiherald.com/news/business/real-estate-news/article168915302.html

FinCEN is doing a great job. Hopefully this will help bring prices down, as long as they don’t get a change of direction from higher up the food chain…

Thanks – I was wondering about that.

Thanks, Petunia.

Wolf, you’ll recall I asked you about this recently, wondering if you had seen an update. (I had mentioned Ricardo Montalban’s vis-a-vis a Malaysian crime outfit.). I’m glad we’re all seeing one.

I never knew that the initial rollout excluded wires. I’m glad that’s being corrected.

I love that broker’s comment that’s like, “Now, no one is going to want to buy anything!”

Right, dumbass. Heaven forbid local individual citizens that have names. ever buy real eatate.

What better place for laundered money than Miami given that it will be under water in a few decades.

The slow down in sales in San Diego is especially evident in the lower to mid tier. We live in a fairly popular condo complex in a good school district. Last year during the summer months we easily had open houses nearly every week. 3 or 4 units in every section were sold.

This year summer is almost over and we have sold maybe 4 or 5 units complex wide? Also local single family neighborhoods have maybe only a couple of homes for sale.

Some of the price jumps as a result are nuts, the same place sold this year versus last year jumped by at least $50k. Condos going for $450k now easily sell for $500-$520k…

I assume employment has a better trend in San Diego though. The question is whether or not employment growth breaks us through a cost of living wall. I assume generally better employment precedes such growth.

I look forward to the day when this isn’t a sellers market. To my knowledge SD has been a strong sellers market since at least 2013, when our family bought our current condo. It has gotten worse every year while I wasn’t paying attention.

So far SD has been a sellers market but won’t for long.

The median income in SD is $50K’ish but median home price is half a million.

The fundamentals don’t support this but for the cheap money and sheeple mentality..

The Denver/Boulder metro area is in pretty much the same boat . Most new jobs being created paying between $30-40k .. with the average single family home now selling in excess of $475k . e.g. the one won’t get you into the other .. unless of course you go the ‘ dark money ‘ or multiple mortgages route both of which are on offer . So whats driving the prices up here ? Out of state ( and country ) investors , local homeowners mortgaging their homes to the hilt in order to purchase investment real estate …. and .. due in no small part to the 420 businesses etc .. money laundering proliferates . Oh … and get this … collectors of MCM homes . Yup … buying them to add to their collection at severely inflated prices with zero intention of living in them

The immediate consequences ? School districts from tawny Cherry Creek ( despite a massive property tax increase ) on down unable to hire teachers … nursing and medical staff shortages across the area … many companies and manufactures unable to draw in new talent etc … all due to the excessive cost of housing in relation to the salaries on offer along with an inflated cost of living and ludicrous property taxes

So yes though few other than the NYTimes and the WSJ are reporting it .. we in the Denver / Boulder metro area ( and to a lesser extent from Ft Collins to Colorado Springs ) are in pretty much the same boat about to spring a catastrophic leak .

Tawny …. have they stopped watering their lawns?

(alex, that’s funny regarding TJ’s use of “tawny! James and i were wondering if that was arty, like rich people like grey beige houses? or if he meant TONY.)

“The fundamentals don’t support this”

fundamentals haven’t supported anything for quite a long time.

based on fundamentals most people are bankrupt

That’s why things would revert back to fundamentals..

Sooner or later

Do you still remember 2008..

You’d be surprised the kinds of people buying these condos though. There are some absolutely staggering incomes and savings.

According to our personal banker the estimate is less than 10% of residential real estate buyers are purchasing upwards of 70% of all homes / condos townhouses sold over the last 24 months

The person that bought my house in SF made almost $400k at a biotech company. So just 3.5x his income.

He put in offer saying that the purchase would be cash if there were any issues with appraisal or loan, and provided copy of bank statement showing $1.5M in his “savings” account.

What was interesting is that the buyer had a special team at his company that assists with real estate purchases. They take care of the coordination and details so their employees can remain focused on work. It must be nice.

The cure for high prices is high prices.

Unless there is hyperinflation.

Then high prices beget even higher prices.

But first… We have some deflation. Welcome to the party!

This is also happening in Toronto.

https://www.bloomberg.com/news/articles/2017-07-06/toronto-home-demand-slides-as-sales-drop-most-in-eight-years

Meant to put a more recent link

http://www.huffingtonpost.ca/2017/08/23/toronto-housing-bubble-has-expired-and-gone-to-meet-its-maker_a_23158813/

Of course, the Chinese are leaving. My HK friend who made a killing on his Shanghai appt is too scarced now to launder or rather convert his money out of the country. In China these days they probably behead people who do that.

I’m sure the Federal Reserve has all of our best interests at heart.

I blow bubbles for my children too, and they love it!

They should sell and move to Texas…they could buy three or more homes down there.

But but… prices are still going up at least in some if not all parts of the SF bay area.

At least in Fremont; houses selling for 750-800K are easily in the 950-1m range.

I cannot imagine who is paying for these?

Not your typical H1Bs who are under-paid because even with 2 incomes they wouldn’t top 200K

Maybe high flying techies in FAANGs some of whose single incomes qualify for these. Google/FB buses do tour Fremont so they have some employees but I cannot imagine newly joining employees springing up a million bucks for a house…

Or Overseas Chinese (?) who export little trinkets to America and do a form of double booking so they keep some dollars here – which are never shown to Chinese authorities. Over a period of time the trickle of dollars parked here (via exports to Walmarts/ Dollar stores) adds up allowing them to snatch houses?

The last paragraph is the only plausible explanation since Chinese authorities are restricting $ flowing outwards since forever. And bigger companies buy Billion dollar corporate assets..

Repudiation / alternate theories welcome

” Not your typical H1Bs who are under-paid because even with 2 incomes they wouldn’t top 200K ”

Statistically speaking the majority are lucky to reach $120k with two incomes . $60k per being the Federal guideline cutoff as well as the target salary for most companies hiring H1B’s . Of course a certain bloviating someone recently promised to fix that by raising the minimum to $100k .. which to date has yet to happen .. and probably never will

I moved from the Valley last year, when looking this year there was less for sale, but a lot of price variance.

I just saw about a 20% overpay near where I used to live. Quite bizarre as it wasn’t remodeled, no central air, and is built on a superfund site (toxic electronic waste form the 70’s). I assume this happened because it was the only unit for sale in it’s price range.

Not sure if money from China is flowing in (it was last year), if not I assume stock compensation is what is driving it. If that takes a hit at any point, housing will go the same way as a lot of the compensation packages I see are weighted pretty heavily with stock.

Wolf, an update from the East here. Home prices in the Atlanta metro are dropping. Local realtor sends me MLS listings and for the past two months have seen more and more “Price Decrease” notifications.

In addition, there are many many more new listings coming on the market. The majority of these include pictures of an empty house.

Bank inventory?

Thanks.

Ok, if we are at the precipice or turning point in this real estate cycle, the 3 million dollars question is,”What is going to happen to all these trophy homes lying empty all over San Francisco?”. Are the all cash gods and goddesses of real estate going to sell to avoid a huge losses in value or stay put as a safe long term store of capital.

The whole lack of inventory narrative is complete bs. So many empty units and air bnb.

The real story has been obvious for years:

1) Low interest rates and easy lending standards.

2) Open borders to foreign buyers, leveraged or not. (I still think a lot of the all cash foreigners are paying with borrowed money. The only question is, borrowed from where?)

3) America’s new landlords, the REITs. This story gets far less coverage for some reason. They’ve bought in droves since 2008. They and the foreigners are responsible for the misleading ‘low inventory’. Yeah, when a single family home becomes a rental, there’s less inventory.

I’m not following you that the proliferation of “empty units and air bnb” implies that there *is* actually is inventory. When realtors speak of inventory, they simply mean the number of homes for sale. If a house is unoccupied or rented out and not for sale, it’s not part of the inventory. There are many reasons why people are not selling their homes (e.g keep prop 13 low tax basis, avoid capital gains tax, prefer not to sell with tenants and can’t easily evict them.) I’m not a realtor, but I’ve been looking at homes for sale, and there are just not that many coming on the market (at least in the East Bay area).

“Inventory” are homes that are listed “for sale.”

Vacant investor-owned homes that are not being marketed and that are not listed “for sale” are not part of “Inventory for sale.” They might be part of “shadow inventory” that may hit the market in the future, particularly when there is a downturn in prices. This number is assumed to be big but unknown.

Homes that are used as vacation rentals (Airbnb and the like) are also not part of “inventory for sale,” unless the owners change their mind and list them for sale.

Hi Rose & Wolf,

Sorry, I should qualify what I wrote. There are plenty of abodes for people to live in. We don’t need tons of new units.

But more and more residences are changing from being owned by their occupants into being rentals.

So there’s plenty of inventory for living, but our libertarian paradise has allowed much of it to be taken over by REITs, foreigners, and aspiring hoteliers. I’m frustrated with how the reporting tends to imply a units shortage. There isn’t one.

This is a bad trend and it’s leading us back to feudalism. The ‘free markets’ freaks are creating the opposite of freedom, debt servitude.

The free market did not create this. It is the forceful interventions to disrupt the free market by wall street and washington.

Imagine they can NOT borrow printed paper. They have to borrow from savers to pool money on deals.

Imagine when they fail, there is no bailouts and people do go to prison for frauds.

The money came from over seas is because US has been printing to buy goods for thr past 30 years.

The money from REITs and wall streets are pooled from freshly printed papers at 0 rate.

Please think one step beyond what’s seen and obvious.

Very well stated, JZ!!

A factor in California is fallout from Proposition 13, which pegs property taxes to the purchase price of a home. The condo next door to ours just sold for twice what we paid in 2001. Which means the new owner will be paying about twice as much in property taxes as we do.

I have several friends (we are all seniors) who are not downsizing from ridiculously large family homes bought during the 80s, because their property taxes are minuscule.

Must be high end senior’s. Most of the senior’s I know that own outright, or with small ‘tailend’ mortgages, those “ridiculously large family homes” have kid’s and grandkid’s living with them. In a couple of cases, the double car garages have been converted into living space!

Yes, we are talking about people who are comfortably off. But there is also a cheapskate reluctance to pay increased taxes that just seems crazy.

I have friends in a large two and a half story house. The husband can’t climb the stairs, so they have put in an elevator. But they won’t sell and move to a single-storey condo because they bought the house about 40 years ago and pay VERY low property taxes. I cannot imagine the increased tax bite would come close to the cost of an elevator.

I do not know how much this reluctance to sell and buy has decreased inventory in popular coastal locations in California. But I have heard the property tax logic over and over from empty nest couples in their 60s and 70s.

Mary:

Ok, here’s how it works:

o Prop 13 tax starts at 1% of purchase value

o Prop 13 tax may increase a maximum of 2% (of initial tax) per year

You say the home was bought 40 years ago (1975): $150,000 would have bought a nice house.

o $150,000 house = $1,500 year 1 prop tax

o same house after 40 years of 2% increase = $3,300 prop tax

o 2017 $1,500,000 “median” price home = $15,000 year 1 prop tax

Quick online search shows $20-40,000 for in-home elevator.

o Prop tax savings from old house vs new “median” house = $15,000-$3,300=$11,700/year

THAT WILL BUY A LOT OF HOME ELEVATOR (elevator is one-time expense; prop tax occurs every year…)

Look like NYC property taxes are comparable.

Median Property Tax $3,755 (4th of 50)

Percentage Of Income 5.02% (6th of 50)

Percentage Of Property Value 1.23% (17th of 50)

A few hundred buyers and sellers setting the value of billions in property assets.

I’m in real estate on the East coast, I know firsthand that the low inventory situation is very real. Inventory has been steadily declining since 2013. And I believe it’s a nationwide situation. Have read many causes about why inventory is low and have some of my own theories as well:

– We all know institutional (and smaller) investors have snapped up a lot of property for rentals. Rental homes do not have as short a turnover cycle as one that is homeowner occupied. So that drags out the typical 5-7 year turnover cycle.

– In many locations throughout the country, baby boomers are not downsizing. I suspect many are not because they still have their grown kids boomerang-ing back home. I see it everyday. Our kids are taking an additional 10 years to become functioning and independent adults (I believe that’s due to this mindset of treating our kids like little snowflakes, sorry)

– Many people work from home nowadays. If you work from home, then you may not need to move for job reasons and that’s one of the primary reasons for moving. It’s simply astounding how many cars are in driveways of your typical neighborhood in the middle of what would be consider work hours.

– If you need to sell and buy too, it’s a double edged sword. Yes you could sell at a premium but in a sellers market, sellers will not take a contingency to sell your home so you may need to be able to swing two mortgages in order to buy a new home while selling yours. And then you still have low inventory to choose from.

– Believe it or not, there are still many homeowners who are underwater from purchasing in 2005-2007. Ten plus years and they’ve still not recovered.

My concern is that with inventory steadily falling for 4 years now, how do we get out of this? The only thing I can imagine is that there would be some sort of headlines in the news or general mood about the economy that would shake sellers out of their complacency and they would be more inclined to put their homes on market. I believe we need more balance, a healthy market is six months inventory. We’re at about 2 months here where I am. It’s so hard for the first time home buyers, losing offer after offer because everyone is bidding on the same homes. It takes an emotional toll on them and some do give up.

With all of what I said above, I personally feel like something changed in the market in early spring like around March in the middle+ tiers. Realtors in my area are getting quite concerned: homes that come on the market that should get plenty of traffic are getting none to little. Something has changed in the last six months. I suppose time will tell, RE data is lagging and takes time to trickle out. By the time you see a hint of correction in the news, it will already be in full swing.

If you’ve seriously been thinking about selling, I suggest you do so now if you have greener pastures on the buy side. Most of your competition will wait until spring, don’t wait that long. If you want to sell at a short term top, I’d list now and definitely by Jan/Feb.

Winter is coming.

I agree that inventory is very low

But a point would come w.r.t prices that people would realize that it does not make sense to lay these ludicrous prices for a house and there would be a psyche shift…

I vividly remember .. in San Diego on 2004..2005.. many of my friends bought homes via lottery system .. because the number of buyers were lot more than number of houses available in a given new sub division…

The cure of the inventory is simple. Rates become higher than rents and that will destroy the rent seekers and homes will fall in the hands of the ones actually live in it as opposed to a tool for rent seekers who do NOT work and spend 24 hours a day to squeeze from the working.

A tightening housing inventory doesn’t make any sense against the demographic stats.

http://www.worldometers.info/world-population/us-population/

Year population increase in the US is well under 1%

So if it’s not the head count, what has really changed?

Meanwhile in Shanghai, China. sources report a 64% decrease in preowned homes for sale.

”

In June, about 12,200 units of existing houses changed hands across the city, a month-on-month decrease of 16.6 percent and a year-on-year plunge of 49.9 percent, Shanghai Homelink Real Estate Agency Co said in an earlier report”

mobile.shanghaidaily.com/business/real-estate/Housing-sales-sluggish/shdaily.shtml

The government was all talk about deleveraging un till in sold 400bil (yuan) before 287bil was due to mature. The bubble gets oxygen! http://k.caixinglobal.com/web/detail_19937?from=timeline

WHOOPS, 49.9%

Meanwhile, in America’s oligarch-looted real economy, as distinct from the Wall Street speculative casino enabled by $16 trillion in Fed funny-money “stimulus,” a full 78% of the proles are living paycheck to paycheck. This can’t possibly end well.

https://www.cnbc.com/2017/08/24/most-americans-live-paycheck-to-paycheck.html

What do you mean “this can NOT end well”? You mean there will be nobody to hold the high priced bags because majority are pay-check-to-pay-check rent serfs?

The pay-check-to-pay-check serf IS the “end”

San Mateo, other than Foster City, is amongst the worst cities to live in, an yet it has such a ludicrous prices. I call Millbrae the capital of uglies; it’s as if anyone in the United States who is extremely ugly, or extremely old is exiled to Millbrae. Who is stupid enough to pay 1.5 million for a house in such an ulgy city? It’s just amazing. San Mateo is old, dirty, and ugly. Again, except Foster City which is modern, and yet it commands a high price. It boggles the mind.

This is just silly. I probs shouldn’t even respond to a post that refers to a city’s inhabitants as “ugly” and I’m far from being a bay area booster but let’s not go off the deep end.

House prices are nuts on the peninsula but San Mateo is not the “worst” city. I don’t even know what that means, compared to what? If you mean other cities on the peninsula, wrong again. I’ve lived in Santa Clara, Mountain View, Palo Alto and Menlo Park and now I’m in San Mateo. The city has a gorgeous main library, as well as nice branches, a lovely park downtown with a Japanese garden and playground where I visited as a child and took my own kids. San Mateo old and dirty? I wish. I lament the loss of useful stores downtown and don’t patronize the gazillion new high priced restaurants and shops in their place, but that’s happening everywhere. I can get to the San Francisco in 25 minutes, same with the beach. I like it much better than Palo Alto or Menlo park where the traffic is worse and the parking nonexistent.

I never knew I liked it as much as I did until it was attacked so violently, lol. P.S. I work in Millbrae and your assessment there is also incomprehensible.

I lived in San Mateo for years. When I did got out of that god awful county, I wanted to kick my face a thousand times for not having left years earlier. Are you really comparing Santa Clara, Mountain View to San Mateo. San Mateo in comparison is like dump; as I said, old, dirty, and ugly.

On top of that the county is brutally after the residents to extract as much money they can from them. Police are abusive and hide behind anything they can to give drivers tickets. Even some of the lights, specially in Millbrae are setup such that they force drivers to make mistake such as reducing the timing of the yellow light so that they can fine them. As I said, one god awful place San Mateo is.

Oh, one more sign that San Mateo is one god awful place; the fine for passing red lights in most areas of Bay Area is $281. In the great old, dirty, ugly San Mateo the fine was $580 or something like that, probably by now it is $800. As I said, a bunch of thieves are running the show in San Mateo.

Silicon valley became one big media relay station.

They receive data, send it to a mixer and transmit, or store in a big

data center for a price.

All within an established band range.

Everything outside this band range is filtered.

Silicon valley media elite can compete with Chinese for RE.

“Filter America” paychecks are not high enough to purchase a small house in San Mateo, Polo Alto, or SF.

In the East, the media produce content shows. Politics, white house,

economy, financial stuff.., Again all within an established narrow

band. The show is run by a high salary conductor and few assistance within the band left & right and even higher salary experts. All in a reasonable support/against their narrow band.

The show must be vivid, exciting & hot, but never allowed to reach any conclusion, because the show will instantly over. The show will kill itself.

Respected academic “researchers” are also well rewarded, because they can throw deadly ordnance at opponents who dare from outside the narrow band.

All get paid well and can compete with Chinese for elite RE.

The view from their opulent beautiful palaces, is completely out of

touch.

No reality in those reality shows.

To keep the show alive, they must became more & more extreme.

There is no feedback loop in those media establishment, asking if they became mad themselves, or something is wrong in

their own head.

Or perhaps, even unknowingly enslaved !!

You are saying the attention of the mass is redirected to unrealistic stuff so that it is comfortably numb when they can NOT own houses and has to live pay-check 2 pay check as rent serfs? And the ones who owns their home are all producers manipulating the mass attention and they are enslaved by it?

Maybe Zillow’s Zestimates were the problem. However a judge dismissed a case against Zillow’s Zestimates with the reasoning that “Z” for Zillow combined with “estimate” connotes that an estimate is just an estimate and seemingly not more or less than an estimate. That’s what I love about law. I hope all the attorneys were well compensated for bringing us this “finding.”

Existing home listings are down across the country. And now new construction is declining as well. The lower end of the price range still looks busy, but the more pricey homes are languishing. With underwriting still pretty conservative and mortgage rates in the 4s, a slowdown is probably all we will experience….unless a recession kicks in.

There are no shortage of houses in most parts of the country. Home listing shortage is a ploy that is used by real estate industry again and again for pumping and dumping. “Buy today, or you will never be able to buy a house. Hurry; there are so few listings.” And people are dumb enough to fall for it; and this acts as feedback loop that pumps up the prices.

CORRECTION:

man, as big and frizzy as i am, i tend to try and UNDER-TELL a story to make it more believable in this unspeakably insane era where even crazy sci fi fiction writers are constantly dumbfounded by reality, BUT i got the price wrong by about a million, which can’t be tolerated on a MONEY site. on another comment thread about uber, i told you all about an old little shack from 1914 that they gutted and turned into condos. the little house apparently SOLD for $1,200,000 a couple of years ago, making the little crazy chinese family some serious bank, BUT the condo on TOP where the dude had the room to place a retro analogue table top football game next to his bike and helmet when the rest of us are living on top of each other in studios or on the street, that one dude bought his little bachelor crash pad for $2,100,000. i apologize.

http://www.realtor.com/realestateandhomes-detail/1330-Hampshire-St_San-Francisco_CA_94110_M26073-91384

What nobody has been talking about at all is the commercial real estate market. It’s in an even more precarious state than the residential market at this time and there are a ton of properties with huge balloon mortgages coming due now and in the next two years, many of which are retail properties. Everyone here knows how well malls and box stores are doing, so how will that affect residential real estate?

We’re covering that, for example here…

https://wolfstreet.com/2017/07/02/silicon-valley-commercial-real-estate-bubble/

Of course as the entire world already knows (and all the real estate agents already know) the number 1 reason is the Chinese money is drying up just like in West Vancouver.

What about high end Palm Springs homes going for 4-7 Million