“Many fear the Fed is behind the curve. The market is even further behind: This is clearly a dangerous situation.”

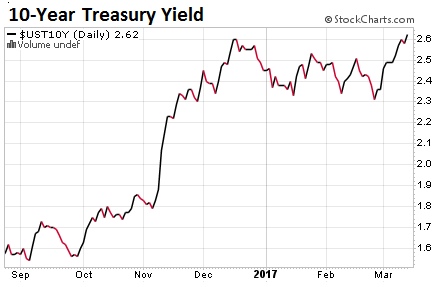

US government debt took another beating today. As prices fell, yields rose to new multi-year highs. The 10-year Treasury yield rose 5 points to 2.625%, the highest since September 2014, when it just briefly kissed that level (via forex trading broker ForexSQ). At this pace, the yield will soon double from the record low of 1.36% in July last year.

This chart shows the progression of the 10-year Treasury yield since late August (chart via StockCharts.com):

When yields were surging maniacally in November and December – broadly called the “bond massacre” or the “bond meltdown” or similar – I pontificated that eventually yields would fall back some, “on the theory that nothing goes to heck in a straight line.” And they did start falling back in mid-December. But that three-month breather has now been totally undone.

Two-year Treasuries took it on the chin too today, and the yield jumped to 1.40%, the highest since June 2009 (chart via StockCharts.com).

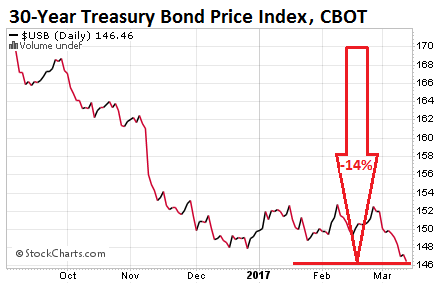

The 30-year yield rose to 3.20%, the highest since July 2015. When yields rise, bonds with long maturities lose the most value.

The 30-year Treasury Bond Price Index has plunged 14% since early October. Hence the “bond massacre” (chart via StockCharts.com):

The markets are coming to grips with a new-new normal, which replaced the old-new normal: a Fed worried about inflation and “over-extended” asset prices, with some segments, such as commercial real estate, being now officially mentioned as big potential risks to lenders. But the markets aren’t coming to grips with this nearly fast enough.

Steve Barrow, currency and fixed-income strategist at Standard Bank, in a note to clients, cited by MarketWatch, put it this way:

Indeed, it is interesting that, at a time when many fear the Fed is falling behind the curve given full employment, near-target inflation, and the likely easing of fiscal policy, the market is even further behind.

This is clearly a dangerous situation because it suggests that if the Fed has to scramble to push rates up, as the – likely – March hike suggests, the market needs to adjust much faster still.

This “adjustment” means that government debt would fall further, and yields would continue to rise.

There are consequence in the real economy, among them: Mortgage rates follow yields of mortgage-backed securities – of which the Fed bought $1.76 trillion to repress mortgage rates to artificially low levels. MBS yields follow Treasury yields with longer maturities. See above “bond massacre.”

And mortgage rates have risen every trading day but one since February 27! Today, the 30-year fixed rate, according to Mortgage News Daily, “is easily up to 4.375% on top tier scenarios with a growing number of lenders moving up to 4.5%.”

That’s the highest rate since April 2014. And it’s up over a full percentage point from the 3.34% low quoted last July.

For the median home price in the US, at $228,900, a full percentage point increase to 4.4% would raise mortgage payments by $1,560 a year. For a condo near the median price in San Francisco, it would raise mortgage payments by $8,256 a year.

And this is just the beginning. The Fed has nudged up interest rates only two little ticks from near zero over the past 15 months.

In a recent barrage of statements by Fed governors, the Fed has been explaining to the markets that rates will rise, not only in March, but several more times this year, and several more times next year.

Before the end of February, bond market participants had brushed it all off, expecting the Fed to start flip-flopping again, and backing off as it had done so elegantly before.

It used to be that the Fed followed the markets. It would timidly suggest that rates might rise, and the bond market just brushed it off, which then caused the Fed to back off in order to not cause the bond market to panic. Now the Fed is telling the market to get in line. The Fed is leading the bond market, rather than following it. That too looks like a new-new normal.

If the Fed hikes rates three more times this year, and a few more times next year, the ten-year Treasury yield could rise north of 4%, and mortgage rates north of 6%. The last time mortgage rates were anywhere near 5% was in February 2011. The last time they were in the 6% range was in November 2008!

But since 2011, home prices have soared, thanks to the Fed trying with all its might to inflate Housing Bubble 2 in order to bail out the banks and the largest institutional investors in the US. According to the S&P Case Shiller 20-city index, home prices have surged 40% over those years and have overshot the peak of the prior housing bubble that blew up so spectacularly.

In some cities, the increases were far larger. In San Francisco, the median house price skyrocketed over 100% since 2012. The median condo price tagged along. But in mid-2015, it encountered the rough waters of oversupply and lackluster demand hampered by high prices, and has started taking on water.

These higher mortgage rates come just in the nick of time, when the Fed’s ingenious monetary policies over the past eight years have inflated home prices in many markets to ludicrous levels, outracing by a wide margin the still languishing household incomes.

Answers are trickling in. Tough luck for New York, San Francisco, Miami… How Much Money Laundering is Going On in the Housing Market? A Lot

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Well, it seems to me that this indicates mortgage rates, and interest rates in general, will be slowly edging to normal. For this saver I state it is long overdue.

What isn’t normal is the amount of debt that all bodies seem to indicate is required to keep the growth facade going. If inordinate debt is required to mask a general slowdown, then what is the point?

There will never be the 4% growth as touted by new POTUS and every other person vying for political power. There are limits to growth, and we are returning to to a more natural situation with higher rates. It is high time people’s expectations follow suit.

For all the hamster wheels in play, I don’t see much lifestyle satisfaction these days. When healthcare is considered to be unaffordable for the wealthiest and most powerful country in the world, something is wrong with the playbook.

Of course, this might also be a way to throw the new ‘Leader’ under the bus, too.

regards

regards

I was getting ready to write much of you already wrote.

I’m looking forward to higher rates so my retirement savings will provide me with an income that allows me to have a decent life.

Sorry if some people lose ‘wealth’ when asset values fall as a result of higher rates but not my problem. By ‘sorry’ I mean ‘not me, not my fault, blame the globalists and their flunkies’. Trump saved the world. Had he not won, I have no doubt Hillary would have coerced the Fed into negative rates in her first term in order to support free stuff for the underclass and more free stuff for the upper 1%. Central banks and savings confiscation via negative rates would pay for it.

Too soon to declare victory yet, but hopefully by later this year it will be safe to buy into a fixed income fund of moderate to long term, providing it has a decent turnover rate.

Even A 200 basis point increase will provide marginal increase to the return on your savings account. Besides, have you seen any increase to fixed income rates since the Fed Has raised the fund rate 50 bps? No. Rates got up and USA interest payments on debt will be unbearable, rates will go back down along with the markets. Housing is almost 20% of national GDP. Sorry but higher eyes may be here for short while but I’d bet the farm 10 yr T bell hasn’t seen the deepest valley yet.

“Well, it seems to me that this indicates mortgage rates, and interest rates in general, will be slowly edging to normal. For this saver I state it is long overdue.”

Sorry, not seeing this at all. I hear constant claims that ‘the economy is tanking’. O.K, if that is true then rates will stay low, or go down.

Look at the retail calamity that’s spooking everyone in my community. The lack of spending is palpable. Local businesses don’t know what to think, except maybe Amazon is eating their lunch. I don’t think that’s true as I see closures and decline across the board.

Bonds rates are rising because Trumps projects will supposedly require deficit financing. None of this has happened, or will likely happen as Trump is being attacked on all sides.

Any rate rise will be followed by a rate cut this later this year. The Fed is one big joke.

Trump wins with both houses in his party. Instantly rates rise predicated on very plausible predictions of large federal deficits. Obama begged for deficits to countervail against stagnation for eight years. Good economics but hopeless GOP controlled politics. The market is right to predict massive deficits. This will inject money into the private sector and debt will be paid down. Very bad news for the FIRE sector as their balance sheets shrink by real asset price collapse (housing declines when rates rise), by paper asset collapse (stocks fall when inflation accelerates ), and by debt repayment (bank balance sheets grow by lending and shrink when loans are repaid). It’s a perfect storm heading towards the FIRE sector. Long overdue IMO.

If it were only that simple.

There are two psychologies at work. People and algos.

The people who program the algos bias the system upward and the people who run those algos offer leverage to make that happen. Apparently unlimited leverage. Each competitor has the other’s back in this regard. Algos keep the indices up.

People would never do what the algos do. Some duck and cover. Some run. Some fight. Some cheerlead. That’s otherwise called ‘a market’.

People are minor influences today. Unlimited leverage and algos are in charge now.

The question to ponder is ‘how to break the algo programming’. What will it take to make them duck and cover? Since they re nothing more than the representation of people working as programmers, you have to understand the if-then logic they implement. Programs are nothing more than sequence – selection – repetition. Even these. Even the most advanced AI. All programs. If you want to beat an algo, you need to understand the programmer.

The economy will follow.

It’s not as simple as you paint it. The push for DATA is due to the discovery that the data they collect can be totally manipulated by them. If you trust that price on your screen, you shouldn’t. That price may not be real and the demand might not be real. There is no way to know because the control is behind the curtain.

Programmers in finance don’t create the systems, they implement them. Any manipulation of data is by design, with the blessing of those above.

The bigger question is, why knowing all this, people still invest. Crazy.

You are correct – programmers don’t create the system. Technically speaking, it’s from the systems analysts who report to project managers who take orders from the principal. Long ago, I was a business programmer who functioned as chief cook and bottle washer. I was speaking in royal terms. It still all boils down to sequence – selection – and repetition. No matter what the principal wants in the margin. The program is the tool. Beat the program … beat the system.

Awesome comment. I often watch the markets very closely (tick by tick sometimes) and there is no explanation but for algos to what is happening. Pure randomness/humaness would never give this kind of automated functioning.

Your question “how to break the algo programming” is absolutely the right question to ask. I wish I knew the answer, but I am sure we will see it one day.

I heard a discussion about the end game of capitalism, centered on a book by Wolfgang Streek of the Max Planck Institut. His vision deals with capitalism’s solutions to crisises that create even more insoluable problems (algos are a great example of this) and the lack of competitive ideologies that in the past, pressured capitalism to temper its worst tendencies. Here’s the link for what its worth (I thought it was an interesting argument).

http://www.cbc.ca/radio/ideas/surviving-post-capitalism-coping-hoping-doping-shopping-1.3973042

Muito lindo. Grande poeta!

On the larger scale, it’s the globalists vs everyone else. The globalists include socialists and neocons. Socialists want utopia and control. Neocons want authority and control. Both want to use other people and their money to accomplish this. The globalists were winning and nearly in control. Trump tossed a monkey wrench into the works. They are stumbling about somewhat now. Globalists want money, control, and authority independent of nationalist boundaries. All of it.

The ‘market’ you describe no longer exists. It’s morphed into a tool for social change controlled by the globalists. It’s too early to say the direction has changed back to ‘everyone else’, but the globalist momentum has certainly slowed down.

Think of interest rates as a barometer of this fight.

It might be worth keeping an eye on those mixed use retail/office/residential developments that are close to completion. I live here in Bellevue, WA and they are everywhere.

There is also a huge retail development underway in Kirkland, WA called Kirkland Urban and they at the concrete pouring stage on it. There was a huge buzz surrounding that here on the east side. The mood surrounding it seems a little subdued right now.

Some of us may remember the dot com bust along the West Coast in 2001/2002 with half finished office developments sitting idle for the best part of a year.

I get that funny feeling we may be revisiting that on even a bigger scale this time around.

Good thinking on the retail space in these mixed-use buildings. Even office space appears to be in plentiful supply.

This is off topic, but Wolf and others may be interested. Rivian Automotive bought an old Mitsubishi plant on the west side of Normal, IL in January. The interesting thing is that they don’t produce any cars yet, buy have been filling up the plant parking lots over the last two months.

There are at least 6000 vehicles so far, with about a hundred being added every day. I have not stopped to see whose cars are being stored, but it looks like overproduction of new cars.

As is the case with all these new “environmental friendly” car and motorcycle manufacturers, the taxpayer is the unsung hero hero: http://www.pantagraph.com/news/local/rauner-welcomes-rivian-state-incentives-detailed/article_74104855-aae1-57d1-85bf-38991c84bedd.html

Intriguing how Rivian doesn’t plan to start manufacturing “cars” until 2019.

You are probably right in your assumption they are leasing out space to other manufacturers to park their excess production: logistic considerations would say those cars are either Ford’s (Chicago) or Chrysler’s (Belvidere).

Thanks!

Buddy of mine just posted a link that happens to tie in with your comment. Maybe this is what you’re seeing.

http://247wallst.com/autos/2017/03/13/gm-has-huge-supply-of-unsold-cars/

Weird. Bloomington is my home town. Haven’t lived there in decades and almost never visit.

I read the Pantagraph story. They bought the closed Mitsubshi plant for a pittance. Almost free. Tax credits amount to a maximum estimated $5000/year for 10 years per hoped for job.

They’re making electric cars. No sales = no income = no tax credits. Their risk, not Illinois. If they are a success, it’s a partnership in putting a white elephant back to work . Close call but otherwise no replacement jobs and no use for empty big factory.

Wow. You just start manufacturing cars with a name no one has ever heard before, and people will be buying like cakes? At least give the car some name people recognize…like Orange.

They are everywhere is not hyperbole.. I live in Everett, WA and travel to Seattle several times a week and never cease to wonder where all of the people are going to come from that will occupy what’s being built.. I read recently the city has 61 cranes running and I believe it was in the 41 range just a year or so ago.. I haven’t been to Bellevue lately but it has to be similar.. Our son wants to buy a house and managed to save up $50,000 for a down payment and I have been trying to persuade him to wait until fall; just a wait and see.. Personally, I don’t see how these prices can be sustained. I thought the same thing back the early 2000’s and it took a number of years to prove the naysayers right and this time(if history repeats) will be far worse.. That 50 grand could be as good as gold in a genuine bust..

Your son may be able to buy a home at a lower price in six months, but it may end up costing the same or more if mortgage rates keep rising. That’s a tough decision to make, and I hope it all works out for the best.

Nice, entry level homes in Minneapolis have continued to move steadily upwards in price.

Explain to me how a house costs more at higher lending rates knowing it is artificial low rates that drove prices 3x higher than trend and double construction cost.

Go ahead Dan.

You assumption assumes a lot… that the bust in housing and commercial real estate doesn’t correlate with a general market bust which would become another jobs bust…

Supply and demand would act as you postulate if all else remained the same.. same demand, just higher interest rates would mean lower home prices.. Which in the long run would put David’s son in a better position when he was ready to sell rather than under water..

The part that I assume will happen is not only will interest rates rise but demand will also fail.. thus many of the projects go BK and the new owners sell at a MUCH reduced price.. Which means that IF your son still has a job, he will be much better off… IMO buying now is a fools game… getting locked in to high valuations that you can’t get out of… with out going BK yourself..

Evidently I did not make it clear regarding the cost to pay for a home via making mortgage payments.

A small movement in mortgage interest rates will be easily offset by purchase price reduction when calculating monthly mortgage payments. But if the house price is just a few percent lower, and mortgage rates go up a couple percent, the monthly payments may end up being higher.

Dan,

Considering housing prices are elevated 300% higher than long term trend, the notion that normalization is “just a few percent” lower is laughable.

OK, here we go one last time.

Do you ‘Watch The Lies’ and ‘SingaporeSam’ really think that home prices in Everett WA are “3x higher than trend and double construction cost” & “elevated 300% higher than long term trend”?

According to Zillow, homes in Everett WA rose in price, on average, 12.2% last year, and they predict a 3,4% rise this year. The median home value there is $307,000, and list price per square foot is $187.

https://www.zillow.com/everett-wa/home-values/

The Economist published an interesting stat in August of 2006. As of 1 January 2001, the aggregate home value in the USA was $14T, but in five years that had skyrocketed to $23T. After the market crashed a few years later, that number had dropped to just over $15T in mid ’09. Today we are pushing back up to around $25T to $26T for the best I can ascertain (it ain’t easy to find this stat). So if we add 16 years to 1 Jan. ’01, and add new construction, we have not quite doubled in total aggregate value. The best metric IMO is median cost per square foot.

In Minneapolis, the current price per square foot is $212, and for the Twin Cities it is $175. I paid $55 per square foot for my Sears Craftsman bungalow in south Minneapolis 22 years ago.

Now, I promise to, in the words of Rambo, “Let it go.”

I’ll straighten this this out Sam.

Dan…. Clearly you don’t understand. Current housing prices are 300% higher than long term trend and double construction costs.

Using your own flawed numbers and they’re 400% higher than long term trend in Minneapolis. The fact you overpaid by 50% for a used house 22 years ago (1998 construction cost then were in the $45/sq ft range for lot labor materials and profit) has no bearing on anything.

San Francisco condos are getting cheaper. Well, not cheaper. Prices have begun to edge down from their ludicrous levels to still ludicrous levels.

Yup, same thing in Boston and surrounding areas, new construction everywhere. Even towns that were considered gritty, blue collar areas have “luxury apartments”, all new construction.

I am also waiting as the market is too insane here for buying or moving to another rental although I fear it will just get worse before it gets better…

The mantra around here seems to be “buy now or be priced out forever”. If the low inventory continues, they may be right.

Funny you should mention that. Here in San Diego a new hotel complex began to be developed last year near the airport/waterfront. Actually the space was/is to be home to three new high end chain hotels, Marriott and Hyatt I believe. Anyway, the ground work began about one year ago to stabilize the site, layout the parking (even to the extent of paving it) and landscape the entrance.

Then it stopped, and for the past six months nothing has happened. The crews evacuated the area, fences were put up to keep the site secure from the public and that was the end of it . I work next door to the site and each day walk by wondering what happened?

Al, is this the building site: http://www.sandiegouniontribune.com/business/tourism/sdut-san-diego-in-midst-of-hotel-building-boom-2016feb20-htmlstory.html

Seems like there is a lot of Hotel overbuilding going on in San Diego:

http://www.sandiegouniontribune.com/business/tourism/sdut-san-diego-in-midst-of-hotel-building-boom-2016feb20-htmlstory.html

Yes Dona, reference is made to the project there calling it “Two midrise properties within Liberty Station are under construction”

But note that this article was printed in February of 2016, now it’s a year later and the project has apparently stalled evidenced by the lack of any activity for the past 6 months.

The article goes on to list the projects at Liberty Station as a Hampton Inn and a Marriott Townplace which it says are “under construction” and at that time they were. It also states there is a Embassy Suites also “planned” for the same location.

At this point I wonder if they ran out of funds, could not adequate stabilize the site which is mostly fill material, or ran into trouble with the Coastal Commission? At any rate something seems amiss and I’m waiting to see if it reverts back to a park and ride that used to occupy the place for years before the ground work began.

Alan, keep us posted. I am very curious now.

I used to live in Bellevue (Lakemont) for 10 yrs. Moved to SF East Bay 6 yrs ago.

Saw lot of the old decrepit single or 2 story store fronts in downtown Bellevue get torn down for the mix use building around 148th. Even the SF Bay area is seeing this phenomenon. Closest TD Ameritrade office in Walnut Creek CA moved to 1 of these new complex and I got thoroughly lost out of underground parking as condo complex was stil being built while the retail1st floor was in operation. Bellevue TD Ameritrade office also moved the mix use building while I was living there.

I’m used to seeing the mix use building outside US but the retail spaces on the 1st floors must be expensive rent and with the fall of retail stores and restaurants struggling as noted by Wolf – not sure whether many will remain as empty spaces.

Let’s see if I have this right: Drop rates to sinful lows to prop up prices, rescue gamblers and deny savers any income, forcing savers into risky assets, then raise rates and stick it to everyone who swallowed the bait.

All this was accomplished in about 8 years, longer than previous bubbles due to the magnitude of the prior bubble.

Rinse and repeat.

I’m not convinced the FED is behind the curve but It seems obvious they’re the shadowy figure behind the curtain of theft and deceit.

And the general public accepts it, along with a long list of other shady practices.

Unless you are absolutely stubborn like i am and have stayed out of the whole thing refusing to part with my money into this mess…

I like your breakdown, Mean Chicken, I have seen several Real Estate cycles in my lifetime, this uptick is different from the one in 2006; that speculation was fueled by “No Doc” loans. This up cycle is full document with qualifying ratios, so I am confused where the buyers are coming from. Here in Orange County, there is a huge appetite for $700,000- $1mm. Is the economy really that good where these folks can qualify using W-2’s ? If they can really qualify based on “real” income; where can the bubble be? I see many more folks driving new MBZ and BMW’s and Teslas as well. I’m getting nervous! Your thoughts?

Yes echo the thought

If the buyers are qualified where is the risk and wher the bubble going to burst from ?

Wash (decrease rates to near zero), Lather (fill the boat full of people who can never pay back the loans with loose lending), Rinse (increase rates, double adjustable mortgage rates mortgage payments, push debt ridden consumers into upside loans default and bankruptcy), and of course Repeat….. The animals are running the zoo.

Well alpha predators, are animals, so you are probably correct.

The fed isn’t running the scheme though its simply a wheel in it.

Everybody blame the, FED. Instead of looking for the real orchestrater’s, its SO EASY.

Really well put, banksters are running amuck on their purpose, neo capitalism is nothing more than bank led fascism.

All the time Obama sat in the White House, the Fed went softly, softly, catchee monkey with interest rates, because “economy, you know”,”don’t want to upset the apple cart”.

Now we have a new President and all of a sudden they grow a pair and announce rate hikes, because “economy, you know”, “can’t let get things out of hand” and damn the consequences.

Am I alone in thinking this is quite a coincidence?

I see the same thing. If they tank the US economy – Trump will be so busy dealing with fall out it will be that much more difficult for him to push agenda that is not supported by “the elites”.

But – at the same time – appropriating blame for the coming s**tstorm is key. And the R states and D states aren’t going to change much – it was short list of R/D or D/R states that put him firmly over the top. Trump will circle the wagons – very visibly – around those states (e.g. coal states and rust belt states).

My two cents is that Trump is playing a long game and has his eyes (already) on the mid-terms. There are plenty of R’s in the Congress that are openly hostile to Trump – but I suspect they don’t think he will get in the middle of their primaries in 2018 and support a new favorite R for the general with some Trump style rallies. That is VERY unconventional – but exactly what I think will happen.

This will put the fear of god in the R’s that stick around knowing they might be next in line. This will make Trump’s second two years much bigger than the first two – and if Trump can pull off a second term … that is when the hammer of revenge will come out and start smashing stuff … the Fed included if they buck him the whole way.

Regards,

Cooter

I agree. They have no idea how PO people really are out here.

Great again eh LOL. He cares so much for his flock LOL

Coal Country Republicans Set to Cut Mine Safety Inspections

http://www.huffingtonpost.com/entry/coal-country-republicans-state-mine-inspections_us_58c85cade4b022994fa2eeca?xdu59we7862p22o6r&ncid=inblnkushpmg00000009

Interest rates have a relationship to risk.. All during Obama term, risk was growing.. IMO it really didn’t matter who won as far as this was concerned, risk has returned, just look at the commercial real estate loans and the retail sector.. or the exploded condos all over the place all wanting (needing) twice what any employed person could possibly pay for them..

No conspiracy against Donald, he is his own worst enemy.. He just loves controversy and he is getting it in spades. The interest rates needed to rise years ago to prevent all of what is going on right now.. Housing peaked while income from actual work has been sluggish at best.. Way to much commercial real estate. Stocks at highs but mostly over buy backs funded by to cheap money. SubPrime auto loans not doing so well. Students who can’t find work paying enough to pay back their loans. To much stuff and not enough customers who can afford the stuff at the prices needed to pay all those people who push papers (digitally) for a living. Debt does have consequences.. and compounding it at low interest rates increases the consequences dramatically.

No, I have believed this is what would happen all along. I knew as soon as the “Great Orator” was out of office the chickens/vultures would come home to roost.

Thus GOP must go nuclear and ram through deficits of epic proportions or economy will tank and they get the blame. Anyone who thinks republicans actually hate deficits is not paying attention. In less than a year Trump appoints his guy at the fed to monetize his deficits. Economy booms. Dollar will weaken but it’s too strong now. Trump will be remembered as the great currency manipulator.

No, you’re not alone, but I don’t buy it one bit. It doesn’t make sense. They’re going to purposefully tank the economy and ruin their careers because of Trump? The Fed is truly incompetent and really do believe based on their data that the economy is getting better, that inflation is ramping up, and that rate hikes are necessary to stave off the worst. The reality in the grand scheme of things is we’re still stuck in low growth, and still trying to stave off deflation from the 07-09 financial crash. And it’s still coming. And it’s going to get worse.

They’ve been talking rate hikes for YEARS. Three rate hikes this year and more next year? Laughable. It took about one week after recent Fedtalk when the market started truly buying rate hikes for high yield credit to start showing signs of fracturing, for oil to collapse 10% (and still dropping), and for the yield curve to flatten to its smallest point since… 2007.

The Fed is living in fantasy land if they think they’re going to get six rate hikes in the next two years; they’ll be back at 0 – 0.25% before they get to 1.5%.

If oil keeps dropping, say bye-bye to the inflation numbers in the CPI that are causing the Fed such concern. They’ll be backtracking real quick.

Its NOT about price inflation, its about WAGE inflation to the fed. They will do anything to keep the plantation economy in place, and a big part of that is making sure the proles never gain a foothold in the american dream by working hard. The framework they built means success comes only through political connections – connections which they control. Thats why you see the clowns in the fed raising rates years after we’ve been hammered by price inflation (not the bogus stats the govt publishes either). Their real fear is a strong nation and a strong middle class, which DJ Trump wants to grow with his policies. Mark my words, the fed will do everything they can to counteract this, they want a 1 world plantation economy.

“Their real fear is a strong nation and a strong middle class, which DJ Trump wants to grow with his policies. ”

Really, what policies.. not rhetoric but actual policies.. He talks about helping the middle class and American jobs but Trickle Down has shown to be a joke on the Middle Class. So far the only policy he has put forward has included massive tax cuts for those who already have the most and his idea of a tax break for the middle class is a HSA. Which is a joke because the only people who can afford those don’t need them.

His ideas of Private Public Partnerships for infrastructure means I will have to pay lots of tolls and fee.. And We the People lose control of our own assets.. How does that help the middle class?

Bringing the jobs home? In India, educated workforce will work for $400 per month. How can we compete with that? Bring it home and what? Pay a bare minimum middle class wage of $20 per hour.. that is $3360 per month. Plus taxes and benefits.. Oh no benies! That is why these jobs left. The cost of our washer and dryers and vehicles would cost more than any of us could possibly afford. Mexico pays more than India and Vietnam but we have to transport a lot further..

Cutting education will be good for whom? The statistics so far on Charter Schools has not been all that good as far as academic results and who is going to teach the disadvantaged? And what do we do with the existing schools, many of which still have building bonds to be repaid..

Just so much rhetoric and yet as I analyze the programs so far I am much less than impressed. I am totally discouraged.

This is not going to go the way you dream. The Dream Team isn’t even on the stage, just the bully pulpit.

Pretty soon you yanks will have 30 years at the same as our 1 year ARM’s.

We are at 4.87% on the ARM’s right now so you have a way to go yet. Also there are no caps or annual restrictions on ARM’s here in Oz.

People here think that we have ‘cheap’ mortgage rates, but they are sky high compared to other parts of the world.

Just another example of how we get ripped off for everything here in Oz.

feds will announce a fresh round of bond buying will start buyin bad mortgages ,buy stocks to keep markets propped up,buy cars and pickups on dealer lots,buy ivanka’s new line,buy kmart,sears,jcp,radio shack,buy oil futures,buy abandoned factories to use as fema camps,buy cnn,buy Syria and north korea,buy the eu,buy the treasury,buy obamycare,bubbles must never ever pop

maybe the feds will open up an AMAZON account.

lol

Not really a joke. The Japanese and Swiss National Banks have been creating virtual yen and CHF and buying shares. The Swiss going so far as to buy shares of foreign companies like Apple. Taken to extremis, a Central Bank could create ‘money’ and buy up the most valuable real assets on the planet. Real Estate, oil fields, old Ferraris. Anything and everything could be bought simply by expanding a Central Bank’s balance sheet.

yes the bank of japan has bought up over

one half of the NIKKEI’S etf’s . sounds like

nationalization of private assets.

“The Swiss going so far as to buy shares of foreign companies like Apple. Taken to extremis, a Central Bank could create ‘money’ and buy up the most valuable real assets on the planet.”

The SNB is one of the few who can/could do that, and not plunge their currency.

The SNB would not mind a bit more CHF weakness, maybe that’s why they let everybody else know, they are doing what you claim.

I would not put it past the SNB, to claim to be doing that, when they are not. The SNB uses a lot of devaluation jawbone tactic’s.

The Asset ledgers of the SNB are not that Opaque. That the public can see, what stock, and what volume of it, they own..

FED has been talking about raising rates for years. It took a run away bull market in paper assets for them to find the courage to rise it .25 a couple of times. The minute the market shakes the FED will turn tail. Of late the higher rates trade is a crowded one

Still looking for a favored starting piece in this domino game. By my reckoning, the starting pieces are China with double-sixes, the Teurozone with double-fives, Japan with double twos, and the good ol’ USA with double-ones. Rickards sez that China will be unreservedly underreserved (way < $3T) at the end of 2017 due to leaky holes in their capital dike. Then the Soros style "pounding" lol of the Yuano will likely push over multiple pieces, as China is forced to open the floodgates of float and let the Yuano settle at its natural level. The buckee, as the largest of the pieces, will undoubtedly float higher. Second in the game play is the Teurozone – where all the sovereigns and their banking minions have been rotting for so long that there are only bones left to dress, assuming the emperor had any clothes there to begin with. Likely that the smallest draught from Draghi or storm from the east will set the dominos in motion, perhaps starting with Italy, though Spain, Portugal, Greece (with enough shepherds crooks substituting for pitchforks), don't forget long-suffering Ireland, and France also might come out of its denial and see its financials flutter and fall over. Thirdly is Japan, but I think they have managed to glue their dominos in place using some advanced sort of fish glue. Finally there is the good old USA – it may take an avalanche of pieces from 'cross the pond to set its own pieces in motion. As with all chaos theory type observations (see also jerk circuits), some randomness is likely, even statistically guaranteed. Good luck out there and stay frosty.

JR, Best comment posting ever!!!

And runner up goes to whoever posted this last year which was very prescient: https://www.youtube.com/watch?v=hOAkc32dfZ4

So how will they service the massive $20tr in debt with significantly higher interest rates? Anything more than 25 bp will rattle the markets, crash RE and force massive QE which is probably already going on behind the scenes anyway.

In the interview linked below, Kathy Fettke is talking about 50% of the commercial real estate loans that have to be renewed this year are under water. Is it really that bad or am I missing something here? (My English is not a 100% either)

Between 06.30 and 07.30 min.

https://www.youtube.com/watch?v=–79G7F5GFY&feature=youtu.be

Jon, From Bloomberg: A $90 billion wave of maturing commercial mortgages, leftover debt from the 2007 lending boom, is laying bare the weak links in the U.S. real estate market.

https://www.bloomberg.com/news/articles/2017-01-24/a-90-billion-wave-of-debt-shows-cracks-in-u-s-real-estate-boom

When you add this old maturing debt (older construction loans coming due) with the CRE coming on line that is under leased/sold, then it possibly could add up to 50%. If rates go up…KaBoom! I’m sure Pension Funds will be the bag holder to a lot of these loans.

Hot potato theory.

@ TheDona, Thanks for explaining. Jon (NL)

The DOW is overbought. If the Fed intend to raise rates 3-4 times,

they should start now, with the biggest thrust, because the market

is on the cusp of going down. It might be their last chance.

If this is the case I wouldn’t worry abut mortgage rates. Both housing

prices and mortgage rates will go down. So buying a house isn’t a

good investment.

Another option is a government shutdown in mid year, or in the third

quarter. If that is the case, interest rates will pop up and buying a

house now is a huge mistake.

So, in both scenarios the implication for RE is negative. But there are

, I assume, other options.

That’s what I told my son, yesterday, who is on the verge of buying

a nice house, in Houston. My son is in the oil industry.

In my view the Fed will take back the interest hikes as we will see soon another leg down into depression. Oil is down and will very likely be down substantially until mid-year. This will take down inflation and also interest rates. Speculative selling of bonds is at its highest since 2005. This is a very strong sign that bonds will soar to unknown heights.

It is unrealistic that interest rates will ‘normalize’ when debt levels are as high as they are today. Can Japan, Europe and US ever normalize? No. The Fed makes the same mistake as Japan when it prematurely increased rates in 1996 pushing Japan finally into eternal depression. The ECB has done this in 2011 when Trichet played the strong Euro game just pushing Greece and the rest of Europe into eternal depression. Now the US follows the crowd into the quicksand of eternal depression.

The only thing resulting from falling prices is a booming economy.

“The only thing resulting from falling prices is a booming economy.”

That might work if you could have falling prices without negative debt consequences.. Hard to keep revenues up and service debts with falling prices. Unless you can some how get all those Chinese and Indians who make a dollar a day to purchase what ever you are selling. Oh yeah, you just get them to borrow themselves into oblivion.

ochram,

There are already huge cracks in the picture of a’booming economy on the verge of escape velocity’. Online job ads – my favourite leading indicator – are down a huge 350.000 in February, loan and leases growth is on the verge of collapse, oil is down, Atlanta GDP now for 1Q17 is down to 1.2 %…. We will see soon how this works out.

A related risk is the Fed halting its weekly purchases of MBS securities this year:

https://www.bloomberg.com/view/articles/2017-02-22/how-the-fed-could-unwind-its-balance-sheet

The Federal Reserve buys about $30 billion per month (2016) in Agency MBS bonds (TBA Passthroughs) through their FOMC Permanent Open Market Operations (POMO) which rounds to about 70% of everything Fannie, Freddie, and Ginnie issue in a year ( Annual Fed Purchases – $30 billion/year, Annual Agency Issuance – $513 billion/ year – 2015 SIFMA ). 70% of a markets annual demand is a pretty big crutch to give up. I doubt there is another group of bond buyers willing to pick up the Fed’s slack and allocate $360 billion per year to Agency MBS securities at current yields (if sufficient demand at current yields existed there would be no need for Fed buying). This suggests a Fed exit from MBS purchases will require meaningfully higher MBS yields (consumer mortgage rates) to attract institutional buyers, or a meaningful reduction in the number of Fannie, Freddie, and Ginnie conforming mortgage loans offered by banks in proportion the the Fed’s purchases. Both scenarios of higher mortgage loan rates, or shrinking mortgage loan demand are big negatives for housing prices ( with a maximum agency conforming loan value of $424,100 ).

When the building materials sector shows signs of flattening from y/o/y stats, watch out below. It is the only sector showing real growth.

You’re looking in the wrong place. Record levels of housing inventory, falling prices and collapsing demand. At least here on the west coast.

https://www.census.gov/retail/marts/www/marts_current.pdf

Please note what increased in sales. Vehicles and only because of huge incentives. Drugs and beauty supplies because of pharma double digit price increases and beauty products are now a staple IMO. Gas due to inflation. And finally home materials.

The operative metric is y/o/y sales too.

Let’s make this SIMPLE. The great bull market in bonds which started with rates at almost %15 in 1981 ended last summer with rates @%1.37.

Any actions by the Fed are the result of the Fed being behind the market ,not the other way around.

Commercial and residential real estate and stock prices have become dependent on extraordinarily low rates to keep prices up.

What will happen when the entire yield curve moves higher

MUCH,MUCH,MUCH lower asset prices.

Hi

Any outlook on Bay Area housing ? Here prices have been through the roof. However the borrowers and renters are also of very high quality, meaning they are able to put in the 20% down and make the monthly high payments. Most of the folks here who can afford to buy are working for the tech companies. And these tech companies like apple google Facebook etc are all doing very well.

If I play devils advocate, it seems this are not sub prime shit like last time. Why do we think it’s a bubble ?

Thanks

“it seems this are not sub prime shit like last time.”

The difference between a guy on 35 K and a guy on 135K when they loose their job’s.

Is that the guy who was on 135 has a hell of a lot more $ value overhead’s to try and make.

The biggest problem with sub was the NINJA flippers. Who had it set to walk away Scott free, when it crashed, which many of them did.

And more importantly, the brokers who set it up so they Could, who knew it would crash, and the loans would not be paid when it did. Who were never prosecuted or even professionally sanctioned.

Only in America is nothing done about Professional Fraud and Professional Fraudsters.

In fact they just put a career Professional Fraudster, in the oval office.

Let me try since I can NOT sleep. The demand model is the following copied from Mark Hanson’s website.

1. IPO shelter buyers. These are strong hands.

2. W2 shelter buyers. These are priced out.

3. Foreign cash money launder or parking cash in houses. FinCen said 1 out of 3 house purchases over certain price threshold, such as 2million for Bay Area has something to do with money laundering. AKA those foreign cash offers. These are strong hands and they CAN hold through down turns. But will they? They may NOT care about the price, but they do care about the asset is worth the price. If they sense any asset deflation, they can choose to sell to get back their principles.

4. Flippers and rent seekers. This group will exit en mass once it gets difficult. Depending on how leveraged these guys are, this could be the group that is equivalent as 1.0’s weak W2 buyers.

5. Institution land lords from Wall Street. These guys jacked up prices a lot during the past several years. These are strong hands with many exist strategies.

So if you are looking for forced sellers in these demand group, weak hands in group 2 and group 4 may be forced to sell. By then group 5 has already existed, (either dump properties already or let public hold it through IPOs). Group 1 is the strongest since they are shelter buyers. Group 3 may either hold if they forecast inflation and they will dump if they sense deflation.

I have NO data on the exact strength/weakness of these groups so I can NOT gauge.

I do want to point out that those tech W2 shelter buyers may NOT be as strong as you think. Yes, they have 20% down, and they can make monthly payment. But the correct question to ask is “how long can they last if they lose their job.” If they can last for more than 1 year, yes, they are strong hands. If they can last only 3 months due to the down/monthly payment has sucked their savings away for these high price houses, then they are weak hands and they would be forced to sell.

I know above demand analysis does NOT answer your question about future price move. Just to share with you my analysis.

“bubble” by definition means “not sustainable”. The only long term sustainable demand in housing market is W2 shelter buyers, and I know they are priced out under current prices. So that’s where the bubble come from.

For the other demand groups, how long can they last, how strong they are to weather down turns, I have NO idea. But I do know given long enough time, they won’t matter. The only thing they do is to create boom/busts to suck victims in. Those are wealth transfer people, NOT sustainable wealth creation people.

I don’t know where in the Bay Area you’re looking. And there are big differences. In San Francisco, condo prices started to flatten out last year and have assumed a southerly bias. But they’re still sky-high. There is a LOT of supply already on the market and a lot more coming on the market. So the next few years should be interesting. But don’t expect sudden moves. Sudden moves only happen on the way up in RE. On the way down, it takes years.

Thanks Wolf, i am in Mountain View. Prices here and next door in Palo Alto are outrageous. Its amazing what you get for a million dollars.

As for as my eyes can see there are tech companies like Google, Facebook, Apple, Linkedin, etc. Very strong, growing, money making firms. Most of the people who live here are either people who work at these, or those who are cashing out in IPOs.

My point was that people who can afford such high prices are quality buyers. Yeah next few years will be interesting, but i dont see any signs of a “bubble”. There could be a correction coming, which is way different from a crash caused by a bubble.

These are very weak internet companies loaded full of debt. Do any of them actually earn a profit?

Now with rental rates and housing prices falling in the bay area, the fun is just beginning. Note that the typical “buyer” profile in CA has a subprime credit profile.

This is subprime x10.

All of them are wildly profitable. Please take a look at their balance sheets. Apple alone has more than 200 billion in cash.

Again, I am trying to understand all of your views that we are in a housing bubble. Low interest merely is a perfect stimulant for all these buyers to jump in. They bid up and buy this because they can afford to.

Why do we think people cannot afford to make their payments in the future ??

All of them are loaded with debt. Just like CA govt. Near a half trillion and rising. Again…. do they earn a profit?

They can’t afford the house now or in the future.

There is a difference between being able to pay and being able to afford for something like 30 year commitment.

To afford, it means you can save enough each year so that every 3years, you can save enough to cover 1 year’s expense.

To pay, it means you can save zero every year and when downturn comes, you lose your house.

Let’s use W2 income since i know with 99% probability that stock/ipo engine will crash several times for the future 30 years.

Let’s say you have 300K in W2.

Let’s simplify tax, and say after tax you have 200K at your disposal. I know mortgage int is pretax, but let’s simply this.

to afford, you cans spend 150K and save 50K, so that every 3 years, you can get 1 year expense in savings.

You have to assume a family of 3 or 4 to buy houses. Let’s say your expanses would be around 70K to cover basic things, not even including tuitions.

that means 80K for your house. using 4% rate and 1.25% property tax, you can calculate the price of the house. I think 1.5 million should be about right.

Not over 2 millions.

I think MV and PA are like 2 million and 3 million.

Unless you are telling me people who buy there all have 400K or 500K W2, i would say these people that are buying are weak hands and they are likely to be forced sellers when downturn hits.

Now use 5% or 6% interest rate.

JZ

To much logic for many people… and way to much math..

Also there are added expenses besides the taxes and insurance like new roofs and paint and replacing general wear and tear..

It seems to me most people can neither afford to rent or own or be a landlord. The numbers just don’t work out very positive unless you can imagine another era where interest rates lower for 30 years from here.

The W2 shelter buyers are the most stable house demand. I doubt the current price was driven by these W2 buyers though. It was the other demand sources and you have to gauge their behavior to gauge price sustainability. If unsustainable, it is a bubble.

I think the price is about 20% to 30% over priced for W2 buyers. For 30 year debt, that is like 6 to 9 years of your life.

“I think the price is about 20% to 30% over priced for W2 buyers.”

LOL.

They’re overpriced irrespective of the buyer….. as in massively inflated by 3x to 4x. That’s why prices are falling.

TBone

If prices fall 30%, i am going to use my W2 money to bid. May be i am catching a falling knife. But if it falls by 67% to hit your 3x number, i think we have something more than financial to worry about.

A decline of 65% would simply put prices back at their long term historic trend…… and accelerate the economy and create jobs like you’ve never seen before.

Curious as to where the low end paper shufflers, mail room, filers, restaurant workers, bank tellers live? Or have places like SF gone completely robotic? Do those collecting the garbage and directing traffic get paid enough to live where the average rent far exceeds most people’s income?

Make a millon$ a year and end up living like people inland who make $50k. If so, what’s the point?

economicminor, Re: where does the average workforce live….I asked the same question from a 3rd generation Aspen local living in the old family house in the center of Aspen. She said Aspen funded a housing authority for the workforce outside of town. At that time, she said there was even busing back and forth.

Perhaps some of these CA cities should do the same.

WHAT IS APCHA?

APCHA (APP-sha) is the acronym for the Aspen Pitkin County Housing Authority. The APCHA program provides affordable housing to full-time or seasonal employees who could not otherwise afford to own or rent a home in Pitkin County. APCHA is different than most housing authorities because you must be an employee of Pitkin County to reside in our housing. Programs such as Section 8 are administered by the Garfield County Housing Authority, 970-625-3589, http://www.garfieldhousing.com.

WHO IS ELIGIBLE FOR APCHA HOUSING?

All full-time employees working in Pitkin County, who meet the income and asset guidelines. We define full time as working 1500 hours per calendar year, roughly 30 hours weekly for the full year or 40 hours weekly for nine months.

HOW IS APCHA FUNDED?

There are two main funding sources for the housing program — a Real Estate Transfer Tax (RETT) and a portion of a sales tax. The RETT is a 1% transfer tax on the sales price of all real estate sold within the City of Aspen only and does not apply to the first $100,000 of each sale. The RETT was extended for a third time in 2001 for an additional 20 years — December 31, 2024; and again in 2008 to December 31, 2040.

Such public workers cant afford these houses. They either live far, or rent in lesser desired neighborhoods.

JZ’s analysis is meaningful.

I dont think all W2 buyers make 400/500K per year. Most of them here in bay area could be in the range of 300K, agreed.

However here is the thing: W2 is not their only income. Stock market has been very kind and folks i know in tech companies have made a ton of cash (sigh, i wish i joined google 10 yrs back).

Still i hear only lots of “ifs” and “scenarios”. Nothing here shows what is the weakness that could trigger the crash. If there is a bubble, it should have been built on weak foundation. Is low interest rate alone enough to justify a housing bubble?

As i pointed before, there is job growth and tech companies are doing well. I do agree that if there is stock market crash, that could mean wealth loss and housing prices correct very fast.

With rental rates and housing prices falling in the bay area and CA at large and default rates ramping up, what are you expecting?

No real answers to my inquiry about where all the workers live. It takes a lot of little people to support all our systems. Can it be that the real house hold income of those who do the real work in the Bay Area is somewhere north of $300k? You mean the cable guy makes (takes home) $150/hr? And the Barista at the coffee shop? And your waiter? And the Bus and Cable Car drivers and mechanics?

And they pay higher taxes and everything yet their real standard of living isn’t any better than someone living in Fallon NV on $50k per year. Maybe not as good a quality of life either.. All for the chance to rub elbows with some uppity ego high tech developer?

Econminor, my thought about the questions of yours.

1. People have been saying the valuation for Google, facebook, LinkedIn, uber, airB&B is too high, so there is a bubble comparing to the real people doing real jobs that make the system work, like electrician, mail man, builders, plumbers etc. It appears to be unfair, and it is difficult to explain. The answer to this is NOT easy, but I will try. Imagine companies like Comcast, AT&T, they deployed the Internet structure and they do NOT make as much money as Google, Facebook and they do NOT grow and they have lots of debt. Why? Because they do NOT have pricing power. They can NOT double their monthly payment, consumer would NOT allow it. But their hard work is being leveraged by Google and Facebook. Those fast speed network enabled video apps and more advertisement, and Google and Facebook has the pricing power. Is this fair? For those hardworking retailers setting up their shops, they find people only go their store to take a look and then go back home and buy on Amazon. Is this fair? People are driving uber for make a few bucks, and Uber takes 25% of the work by leveraging the cell phone technology and fast internet.

The short answer is, it does NOT matter how hard you are working, the power of pricing matters. You have pricing power when you connecting dots like Steve Jobs. Phones, Internet, touch sensors have been around for years, but Steve conncted the dots and made the iPhone and then Apple has the pricing power, but those parts makers do NOT. Apple make billions, and those suppliers makes millions. I have to warn you that for every snapchat, there are 100 chat apps that fails. So the unfairness is due to taking risks to connected the dots. Succesful risk takers gets the power. HArdworking people do NOT.

2. The point of making 300K and live like inland 50K people is the following. To me it is the opportunity to achieve freedom. By freedom, I mean you can stop working and you can still survive. IF you make 50K and live comfortably in NV, you can never stop working. The system guarantees you to work to your bones and die without being able to retire. Although 300K in Silicon Valley can only get you the same quality of living as 50K in NV, you do have a shot of making it big and be free. The point is NOT everyday life quality. It is that opportunity of achieving freedom to retire early.

Can’t agree more. This the reason people live here despite traffic and cost of living

The median house price in Australia is currently standing at $660,000 which is roughly US$495,000 and we are still in housing bubble No.1. So when it finally crashes we will probably experience an even worse crash than the US did in 2008.

To feed the animal we have a Ponzi immigration scheme that inflates the prices with a huge influx of people – mainly from Asia. They buy our houses locking out our youth and then leave the homes empty and return to China. We also have a system where we have a tax deduction for interest paid and then when the home is sold the investor makes a capital gain for which they pay a small amount of tax. Its the new gold rush for foreigners and investors and our government still thinks we are not in a bubble.