“It will not harm the pension beneficiaries”: official

This is how the report by Japan’s Government Pension Investment Fund (GPIF) for the March-June quarter – the first quarter in Japan’s fiscal year – started out in order to soothe the frazzled nerves of the people who’d paid into this system all their working lives: the fund is managed “in the long-term, and its investment results should be assessed in the same manner.”

OK we get that. But what a fiasco.

The GPIF isn’t alone. Pension funds in the US and elsewhere are in deep trouble. Many of them have been taking on enormous risks to solve their underfunding problems. It has been called the “global pension crisis.” Some corporate and union pension funds in the US have already become insolvent. Others are heading that way. Local and state pension funds are neck-deep in trouble. Yet, the Fed-engineered asset bubbles have lifted all boats….

But few big public pension funds can hold a candle to the GPIF’s October 2014 decision to dive into Japanese stocks and foreign stocks and bonds near the peak of the Japanese stock market rally.

Actually, it didn’t voluntarily dive into it.

It was pushed into it by the Abenomics-obsessed government and its reckless way of trying to manipulate up the stock market. The goal was to plow 20% to 25% of the fund’s assets into Japanese stocks. At the time, the fund still had about $1.4 trillion in assets, so 25% would amount to about $350 billion. It meant some serious buying over a year or two, which would inflate the stock market.

Add some hype and hedge-fund front-running, peppered with the Bank of Japan’s money-printing mania, which includes purchases of equity ETFs – and you’ve got a value-creation miracle on your hands.

It did work for a while. It worked during the hype stage. And it worked when the GPIF began selling its government bonds to the Bank of Japan and started buying stocks. The GPIF became the biggest buyer of equities in Japan. Stocks soared. Other pension funds followed the model. In June 2015, the Nikkei hit its recent peak of 20,868 (still 47% below its all-time peak in 1989).

But since then, the GPIF has met the goals for its “policy asset mix.” And so the GPIF stopped its purchases. Hedge funds lost interest and bailed out. And the Nikkei has since plunged 22%!

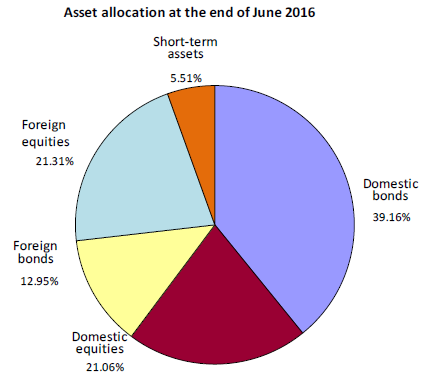

And there’s a special treat. Foreign equities and foreign bonds combined account for over 34% of total assets: a huge bet on the exchange rate, or rather on the wholesale destruction of the yen. But the yen has risen sharply recently.

So how has the Abenomics value-creation miracle performed?

- In Q1 of fiscal 2016, ending June 30, the GPIF lost ¥5.23 trillion ($51.4 billion), or 3.9% of its total assets.

- Year-over-year, total assets have shrunk 8.1% to ¥129.7 trillion.

- In Q4 of fiscal 2015, ended March 31, the fund had already lost 3.5%, or ¥4.7 trillion ($46.2 billion).

- This was the first back-to-back quarterly loss since 2008! But we’re not in a Financial Crisis!

- Both quarters combined generated a loss of about 7% or ¥10 trillion ($98 billion)!

- For the fiscal year 2015, the fund lost ¥5.24 trillion, the fund’s first annual loss since 2008.

From fiscal 2006, when the fund was converted into an independent administrative agency, it showed ¥22.8 trillion in cumulative investment income, down from ¥33.3 trillion at its peak in fiscal 2014. In just five quarters, the fund’s new focus on stocks, risk, and foreign-currency-denominated assets annihilated 31.5% of the total gains accumulated over ten years!

Bitter irony: The only asset class that made money was “domestic bonds,” largely JGBs that the BOJ has been gobbling up. As their yields dipped into the negative for longer-dated maturities under the BOJ’s negative-interest-rate policy and under its buying pressure, prices rose, and the fund made ¥940 billion.

The other asset classes:

- Domestic equities lost ¥2.26 trillion.

- Foreign bonds lost ¥1.52 trillion.

- Foreign equities lost ¥2.41 trillion.

- “Short-term assets” remained flat.

This is other people’s money.

And these other people are beginning to get restless. They’d paid into the system all their working lives, and now it was being squandered on some Abenomics gamble. The Japanese have been through stock market routs before. It’s all a scam and a bad joke, many feel. And many stay away from it as far as they can.

To soothe rattled nerves and deflect a public backlash, GPIF president Norihiro Takahashi blamed the strong yen. The dollar-yen exchange rate had been “developing without a clear sense of direction,” he said because it was going in the wrong direction.

And he blamed Brexit. The vote happened a week before the end of the quarter. It caused the yen – still one of the global safe-haven currencies that folks flock to in times of turmoil – to rise, which caused Japanese stocks to dive, he said. And it also caused the value of overseas investments to fall when they’re converted into the stronger yen.

“The results of the UK’s referendum turned out to be different from what the market expected,” he said, blaming the hapless Brits for having voted the wrong way.

And he blamed the US unemployment data in May, which had been “much worse than forecast.”

He didn’t blame the strategy of chasing after risk wherever he could find it, at the peak of the central-bank inflated market. He didn’t blame the decision to dive into exchange-rate risk, with 34% of the fund’s assets in foreign currencies. And he didn’t blame the failed market-manipulation aspects of Abenomics. But don’t worry….

“Even if market prices fluctuate in the short term, it will not harm the pension beneficiaries … we invest from a long-term viewpoint,” he said. For this gamble to work out, the yen will have to get crushed and take much of the Japanese wealth with it. Are the Japanese ready to give up much of their wealth? Hardly.

Bonds are in the biggest bubble ever. Stocks in the US are at all-time highs. Central banks have been printing money for years – and still, the GPIF got clobbered. What if this is as good as it gets? What if stocks and bonds return back to earth? Then he’d have a lot more explaining to do to the pension-fund contributors whose money got eaten up by the schemes of Abenomics.

The BOJ is already fretting about the next crash and is building up a big pile of dry powder. Read… Bank of Japan Prepares for Crash Triggered by Fed Tightening

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I can’t work out why the “global pension crisis” isn’t getting more attention from market commentators. Clearly, we’re living in a low interest rate environment, not just in Japan, but globally. Low risk sovereign bonds are yielding next to nothing, so how can pension funds assume 7%+ per annum returns? They are massively underfunded and this issue must be recognised. I think it’s a looming crisis.

Pension funds that purchased long duration bonds have been insulated from the decline in yields, but eventually the bonds will mature and pension funds will be forced to buy new bonds with significantly lower yields. Even long duration sovereign bonds in many countries are now yielding next to nothing.

As Wolf has pointed out, pension funds and other investors that are saving for retirement are being forced into high risk assets. This could easily become a big problem as asset price bubbles continue to inflate. History tells us that it’s asset price bubbles and reckless lending that ultimately derail economies – witness the unsustainable rise in house prices in the U.S. leading up to the GFC – and many warning indicators are currently flashing red. We have the biggest bond bubble in history and real estate prices are unsustainably high in many countries, fuelled by low interest rates and the search for ever diminishing investment opportunities.

So why are central banks continuing with their ultra easy monetary policy initiatives? I think it’s clear that the long term adverse side effects are far worse than the benefits associated with the short term boost in demand resulting from low rates and quantitative easing (and it’s questionable whether the monetary policy initiatives are actually boosting demand anyway). To me, it seems like central banks are focussing solely on consumer price inflation while ignoring asset price inflation and other unwanted side effects. It’s like their job spec says that all they need to look at is consumer price inflation and hence they can conveniently ignore everything else.

In Japan, however, I can see some logic in what the BOJ is doing. I think it is clear to most people that the only end game for Japan is for the BOJ to monetise the Japanese government’s debt. Japan has an unsustainably high debt burden, well above 200% of GDP, and the world’s worst demographic problems. What I don’t think is clear in many people’s minds is that Japan is already monetising its debt. There’s been all this fuss recently about “helicopter money” in Japan – ie having the BOJ print money to directly fund the government and, in so doing, permanently increase the monetary base. It’s already happening. As Wolf has pointed out, the BOJ is printing huge amounts of money to buy the Government’s debt. It’s hard to see how the BOJ is ever going to be able to sell this debt and hence it is already permanently increasing the country’s monetary base. They’re effectively forcing Japanese pension funds and other JGB investors, nearly all of whom are domestic investors, to sell their bonds to the BOJ. And when this debt is effectively retired, the government’s debt relative to GDP won’t look so bad. The Yen will also plummet and JGB yields will surge, but this probably isn’t a bad outcome given how severe Japan’s problems are.

So I can see some logic in the BOJ’s actions. But they’re desperate and really have no choice. Other central banks have options and I think they’re choosing the wrong one. The Fed, ECB and other central banks have set rates too low for too long. It’s been good for people who own assets, but there’s going to be a day of reckoning. And it’s not too far away.

What if all this is intentional?

The pension problem was comprehensively addressed by many speakers at the ongoing Jackson Hole gathering.

Or was it just my dream after drinking too much on Friday night?

maybe they should use the same solution as the big Dutch pension funds: now that it is finally becoming clear that the pension system is another big Ponzi and promises of gold-plated pensions are just that, next year they are starting to cut pension payments by a terrible 0.7% (which might be repeated in the next years if the situation doesn’t improve). That 0.7% average cut is nothing compared to what the self-employed etc. have been going through lately, but anyway … Because -0.7% is simply not acceptable for former government workers, the unions and some politicians are demanding that the government compensates any pension cuts for pensioners, so they can keep up with the 1-3% yearly improvement in government salaries.

After all, the government can borrow money for less than nothing, so there is no cost involved! I’m pretty sure the current government will be happy to oblige, to some degree at least. So the Dutch can keep their top position for national debt levels (when including both public and private debt) … Why worry about debt, we all know it is never going to be repaid so better take advantage of the situation and sell that debt to clueless buyers, e.g. those from the pension funds ;-)

Don’t know if Japanese government pensions are as iron clad as US public employee pensions but, if so, this is bad news for Japanese taxpayers. Someone ( taxpayers?) is going to have to make up these losses if GPIF benefits can’t be cut.

How this problem can be resolved in Keynesian terms is something of a puzzle. If the goal of Abenomics is to raise demand through wage increases and higher spending how will cutting pension benefits, raising pension contributions or using tax revenue to fund pension fund losses accomplish this?

This isn’t a Japanese problem either. With most US pension funds needing to earn 7.5% or more on their assets to meet their obligations and few now doing so ( my smallish municipal pension fund also lost money last year) Yellen is going to be trying to kick the can down a dead end road.

Oh it is easy. They will issue more debt at negative rates, fund the pension deficit with the proceeds and make a profit in the process on the interest received. Upside down world.

What you are saying is that they will tax savers* to pay for government workers’ pensions. The pawns are not completely powerless, however; they may simply stuff cash in their mattresses (during the era of the gold standard, in the wake of the stock market crash in 1929, many stashed their gold certificates (i.e., dollars worth $10 and up) ouside of banks, which made perfect sense, and even in a fiat regime it makes sense) – or just buy gold or silver with savings not required for day to day expenses.

* a very penny-wise and pound-foolish strategy. It is taught in the college text Economics “savings is the engine of investment.”

The fed will have to step in and bail them out, exactly as Bernanke did with GFC banks. It’s really not a problem. Either way the government will be called on to do it. The price of not doing so will be too terrible to contemplate!

So you are saying that massive world-wide debt creation is no problem (you don’t happen to be a federal employee by any chance?). Read Hans Sennholz’ book Age of Inflation (or hell, any history of the Weimar Republic ) and then tell us debt does not matter.

The Teamsters union is now in the middle of their own election, here in the US, to elect a new president. The younger Jim Hoffa, who is past retirement, is running yet again and will probably get reelected. It is really hard to feel bad for organized labor and their pension funds, when they go out of their way to reelect the people who are impoverishing them.

P.S. For those of you who don’t know, the Teamsters pension fund is in a heap of trouble. They are talking about 50% or more cuts to current retirees.

Let’s hope that some of these pension funds with naughty retirees have to use huge cuts while at the same time seeing government employees like those from the Illinois TRS retire with goldplated pensions. I’m curious for how long the crooks in Washington will get away with that.

I’m seeing similar clashes within society – between different groups of pensioners – develop in my own country. Many teachers here retire with pensions that are worth 5-10 million euro or so, at the current interest rate. Their pensions are sometimes even more than the highest income they ever had when working, no matter how the pension fund performs or how many they paid into it (usually just a fraction of what they are receiving). In addition they can receive the pension from e.g. a deceased spouse and other extras. A self-employed person will have trouble saving more than about 100K euro for retirement in our current tax system: everything above that is ruthlessly stolen by the government to hand out to their own ex-“workers”.

Most private pension plans over here were one big scam (paying out just a fraction of what they promised, e.g. 10% but my own pension insurance pays less than 1% of what they promised). It probably isn’t much different in other countries. But government workers escape all the mayhem without a dent and will retire on incomes than an order of magnitude above those from self-employed workers and some workers in the private sector. Maybe in my country the retirees from big industry unions will escape too, if the government compensates their pension shortfall. But this will only make things worse for all the others, because they have no one to fall back on.

How long will people (including pensioners) accept crippling taxes to support those ‘untouchable’ government pensions, for people who often haven’t even really worked a day in their life?

“It is really hard to feel bad for organized labor and their pension funds, when they go out of their way to reelect the people who are impoverishing them.”

Sadly that I feel the same about the US electorate. I wonder if US Democracy is a viable form of government over the long term. We can not make national decisions about finance or infrastructure. Fairness is such a strong value that everything is delayed. There is no one in charge of thinking about the country’s future. Everyone wants the other guy to pay for everything.

I am not saying I’d prefer to live under any other form of government, but this country is showing its age in terms of effectiveness. And it is downright decrepit in showing innovation. Instead of working together to solve problems we form tribes to point fingers and tell everyone who is responsible for creating our problems.

“The American Republic will endure until the day Congress discovers that it can bribe the public with the public’s money.” – Alexis de Tocqueville (in Democracy in America)

The Republic is dead. We now have a corporate state, fascism.

Amen, Petunia.

Jefferson said: If they [future Americans] will have a central bank, the corporations which grow up around it will eat of their substance until they live in the streets of the land their fathers fought to conquer.

I did not put quote marks since there may be a word or two difference. But, as you point out, so true.

Agree, but one of the problems is that democracy developed in a much different situation tied to local government. It doesn’t work on a large (national, international) scale, even less so in our current interconnected world that is completely manipulated by the media.

The same BTW applies to much of the financial world, when you depend on people on the other side of the world whom you don’t know and who could not care less about what happens to you, there are bound to be ‘policy errors’.

Apparently the elites (which includes union bosses etc.) think they can get away with this just like the savage rulers from the Middle Ages. We have to make it clear from them that their life and wellbeing depend on a functional society …

RE; the asset that pension funds invest in

The biggest expense a retiree (or anyone) with no other assets than their pension is rent.

A retiree can invest in stocks, bonds, gold, etc, but the only asset they can invest in that will need for certain is a place to live.

If a pension fund invested in apartments- it is entirely possible that this investment could be outperformed by stocks, but the resulting asset can never be useless to the retiree, because it’s the only asset he can actually use, no matter what the market.

It seems that real estate alone is the only asset that is de-risked to some extent, because even if unsaleable, not only can it can be used, the retiree will HAVE to use it.

And although this has nothing to do with the argument being made above, apartment buildings selected by a prudent buyer in goodish locations have actually had a pretty good financial return.

So you have upside, but a limited downside, because if you can’t sell it, you can use it, giving you a return, not as a monthly check, but as a check you don’t have to write.

The main problem with that otherwise creative suggestion is this: the owner of the buildings will always have to write checks for property taxes, and they can rise substantially in a short span of time.

True- and there are strata fees, replacement reserve ( roof) etc.

But the bulk of the monthly payment would be the mortgage which over 25 years the pension fund could at least dent.

My comment is made in the context of either very low bond returns, very risky stocks- what remains.

keep in mind that nowadays a low mortgage rate almost by definition means that you are vastly overpaying for the property.

Recent buyers couldn’t care less about paying back the mortgage after 30 years, but a pension fund should aim to still be in business when the mortgage expires, which means they should care about valuations.

You’ve somewhat described the self-directed pension of real estate investors like myself. We buy rentals with plans to one day retire with a stream of income from rent payments, which adjust to market forces. Interestingly, my wife is from Europe and almost instinctively is yearning to go back and retire with all the freebies and generous European pensitons, while at the same time seeing our rental income grow here year over year.

‘rent payments which adjust to market forces’.

Good luck retiring wealthy from rental income that is based on extracting ever more money from those without their own home. In my country renters already spend on average 40-50% of their income on rent, and with the unlimited asset inflation thanks to central banks, rents have to go up even more just to keep up with rising home prices (as triumphantly told by our own government, since 2008 rents in the Netherlands have increased more every single year than home prices).

If one buys properties now in the Netherlands with the idea of renting them out, the gross rental income would be in the 2-4% range; that is without any upkeep etc. although property taxes are very low here. If you purchased the rental property before the bubble started (in my country that means over 25 years ago) you sure can retire wealthy, but if you plan to buy now I can’t see how you can win despite the lowest mortgage costs ever.

Renters have to spend their income on other things than just rent, we are very close to the limit of what is possible and their incomes sure aren’t going to keep up with inflation (certainly not when more and more renters are going to depend on pensions). Maybe one can kick the can down the road by renting out single rooms instead of complete homes/apartments (the favorite strategy over here to get sufficient rental income), or time-sharing rooms, but I don’t think that will prove great for the value of the property and it will only postpone the inevitable.

Home prices in most of the West are completely detached from reality, and for rents as well there is only one way IMHO in the long run (more than a few years): down. Depreciating capital, shrinking rental income …

I agree on distortion of rent-to-price ratio in many countries, as well as many cities in the U.S. Yet, there are still many regions of the U.S. with favorable ratios. Knowing when to sell at a bubble top is tough since they go for long like you noted the 25-yr run in your country.

Yes, the US probably has many areas that escaped the current craze. But in the long run I wonder if it will remain like that, if home prices hardly rise now because a region is unattractive (somehow …), maybe it becomes even less attractive once home prices even out across the country (either by a drop in the hotspots, or catch-up in the more remote areas)?

It should be clear to anyone operating at a mental capacity above a neo-morph that central banks do not have best interests of the population at large at heart. For that matter, neither does the government(s). Perpetuate a stock bubble with other peoples’ money so that the insiders can cash out before the sh#t hits the fan and all that wealth simply evaporates. “What about the common folk whose money you are using to further this fraud?” you may ask? “What about them?” would be the answer. All the world is a stage and we are merely players for the entertainment of those who selfishly hold onto wealth and power that they have neither earned nor wield in a judicious manner. We are now at a moment in history where the worst among us exercise the greatest amount of influence in recorded history. Ah well, things have a way of balancing out. There will be blood in the streets before this ends and not all of it will be from the common folk.

Chris – I agree with much of what you said. It is clear that the Fed’s key objective is to maintain the status quo of the large banks and their owners.

For a really good articulation of those ideas and a discussion of their beginnings read The Creature from Jekyll Island –

https://www.amazon.com/Creature-Jekyll-Island-Federal-Reserve/dp/091298645X/

The first time I read this I thought it was basically bullshit, but after the past few years I reread it and I now think it is not.

In the future I see a flood of Japanese citizens taking a one way ticket to Aokigahara ( Japan’s Suicide Forest) if it keeps going at this rate.

That’s better than Muricans. The later will drag the rest of the world to hell if necessary in order to maintain the “Murican way of life”.

As I said before, Central Bankers, etc should be hired strictly on an H1B Visa basis. If they don’t perform, you can just let the visa expire, and everything is self correcting.

We can only hope that the Muricans turn on themselves (at least they have plenty of guns to do that …) before destroying the rest of the world completely; they have been quite busy with that lately and many of them seem to enjoy the party ;-(

The Dirty Double Cross is Earth’s highest honor award for swindling, soon to be awarded to central bankers and their employer elites for executing the greatest transfer of wealth in the history of mankind.

Central bankers are well paid for their opinions, hard work and brilliant strategies.

Of course the Japanese retirement age could be raised to 75…

Or 80…

How about 85..?

Reminds me of an old saying: Borrowing from Peter to pay Paul.

I wrote two books on how insiders are looting pension funds. The Charles Schwab Stock Rip-off and Depression Finance. However, the SEC and the DOJ have no interest in how pension funds are looted. Below shows how Bill Gates boosts his wealth from pension fund money. These are not founders’ shares, they are pension funded shares.

11/20/2014 31,000,000 Gift at $0 per share. Cashed against 401k funds Paid zero for 31,000,000 shares of pension fund money.

10/31/2014 3,200,000 Disposition at $46.76 per share. $149,632,000 Cash out of 3,200,000 shares.

Now add 600,000,000 to 900,000,000 gift shares to the take and you get a sense of the rip-off.

SEE SEC Form 4 Insider stock compensation.

Dr. Michael La Crone