European banking crisis jumps to the next level.

European bank stocks just experienced their worst two-day plunge ever in the post-Brexit fallout that rained down on the already blooming European banking crisis.

Healthy big banks would get over Brexit and the political turmoil it is spawning, particularly non-UK banks. But there are no healthy big banks in Europe. And non-UK banks are crashing just as hard, and some harder. This is about a banking crisis morphing into a financial crisis.

These bank stocks got crushed on Friday. And they got crushed again today. Italian banks have been reduced to penny stocks. Spanish banks are getting closer. Commerzbank, Germany’s second largest bank, and still partially owned by the German government as a consequence of the last bailout, is well on the way.

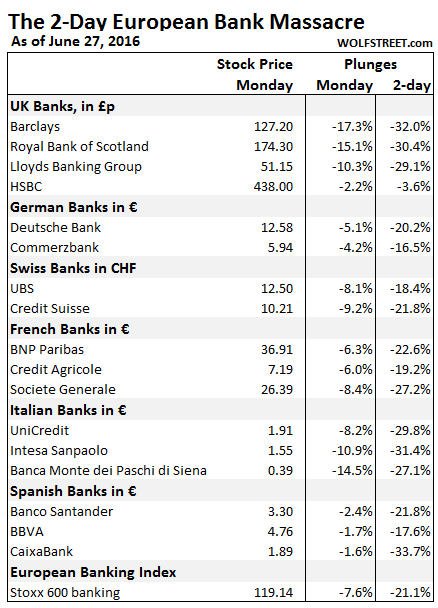

The two-day losses are just breathtaking. This table shows the largest banks by country with their percentage losses for today and for the two-day period:

Note that the European Stoxx 600 banking index fell 7.6% today for a 21.1% two-day plunge! It isn’t just a few banks whose stocks are collapsing!

Deutsche Bank’s infamous CoCo bonds deserve a special word. These hybrid bonds that are just above equity on the capital totem pole had spiraled down, with the 6% CoCos hitting 70 cents on the euro in February. At that point, they and all other Deutsche Bank bonds were propped up by government verbiage and bank money. The bank ingeniously announced it would buy back its own bonds! Like all these transparent market manipulations, the market ate it up, and even the CoCo bonds jumped to 87 cents on the euro. But that didn’t last long. They have since lost 11.5%, including today’s 3.7% plunge to 77 cents on the euro.

In Italy, the banking crisis that has been growing for years has reduced all major Italian banks to penny stocks. It has triggered bailouts of some banks, including the third largest publicly traded bank, Banca Monte dei Paschi di Siena. Now the taxpayer is going to get shanghaied into bailing them out to put a floor under the collapsing share prices and prevent them from going to zero.

Italian banks are bogged down in a sea of bad debt whose true dimensions are still unknown publicly, and that the ECB publicly estimates to be €360 billion. But every time someone looks at it, it gets larger.

According to “a banking source familiar with the government’s thinking,” as Reuters put it, the Italian government is now fretting about a hedge-fund attack on these zombies, following the Brexit turmoil! To counter this attack, the government is trying to figure out how to “protect its banks from a destabilizing sell-off of their shares” that “could tip them into full-blown crisis.”

(I have some news for the Italian government: Your banks have been in full-blown crisis for years!)

The government is thinking about using some kind of taxpayer guarantee and taking a stake in these banks, funded by about €40 billion in new government debt, issued by the second-most indebted government in the Eurozone, after Greece.

According to media reports in Italy, cited by Reuters, the government is already in talks with the European Commission about this sort of bailout. European rules are supposed to end state aid to tottering companies, and collapsing banks are supposed to be wound down involving losses for stockholders and junior bondholders (the bail-ins).

But the government is invoking the exemption in these rules in case of “exceptional events,” which would be the crash of bank stocks as a consequence of investors figuring out that these Italian banks are toast.

That doesn’t mean that bottom fishers and falling-knife catchers aren’t jostling for position to pick up “bargains” among these European banks, as they have done so many times before, only to see banks stocks, after a brief rally, fall once again to new lows.

Contagion is infecting US banking stocks. As I’m writing this, Goldman Sachs is down -1.2%, Wells Fargo -1.3%, JPMorgan -3.1%, Morgan Stanley -3.3%, Citibank -4.1%, and Bank of American -6.1%.

These wounds among US banks are just cosmetic compared to the bank massacre happening in Europe, where the ECB is now fully engaged in trying to deal with a Financial Crisis under the cover of Brexit Chaos. Read… ECB Blows €400bn on “Brexit Black Friday” Bank Bailouts

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Great reporting, Wolf. Keep it up.

Meanwhile, it was reported that Royal Bank of Canada started charging for some bank accounts in their Caribbean branches (several islands). I guess if you want to release a test balloon, you try it in a banana republic, first.

Never let a crisis go to waste.

“Lehman moment” of 2016.

No doubt about it, but there is an important difference too. When Lehman crashed, the FED still had some credibility, but that was then, and this is now.

“Hey Mon” moment of 2016,

if d’Cynic is correct about the Caribbean branches…..

What happens when the depositors want their money?

Then the bank calls a bank holyday. And the saver can forget about his savings. Happened before, happens now.

Ah!… bank ‘holyday’….

….yeah… the banksters are such ‘saints’…

That question occurred to me. What depositor guarantees exist with these banks? Are they uniform throughout the EU?

Larger question–what is the relationship between a bank’s share price and its day to day viability as a business? Could a bank’s shares go to zero, but the business itself survive?

The relationship of a bank’s share price to its viability is a question of confidence. Would you invest in a zero value institution or even do business with it? I hope not.

Can a zero value bank survive? Yes, if it is nationalized, bailed out, or backed by taxpayers. I differentiate between bail out, which can be done with depositor money, what they call a bail in, as opposed to just sticking the taxpayers with the bill.

As far as depositor guarantees, I don’t know about the EU, but in America deposits are owned by the banks, and the depositors are creditors of the bank.

In the EU as well as US and Canada, who, I guess follow the dictat of the BIS, the deposits are insured up to 100K of the respective currency: Euro, USD, CAD.

For all practical purposes, there’s no such thing as an individual bank bailout, or bailin of a significant bank; there is only bankruptcy.

Why? Because if you bailout a bank by taking a government equity in it, deposits and business would flow into that bank since it is guaranteed by the taxpayer. And how does such bank compete in the marketplace? It is even more guaranteed than the current implicit guarantee: moral hazard on steroids.

Yes, depositors are just unsecured bank creditors. But they’re insured. Big difference.

I’ve had deposits with 3 banks that failed and were taken over by the FDIC, including Mbank in Texas, which at the time was the FDIC’s second largest loss, and including WaMu (a 5-year CD with a fat interest rate). Gotten my money back, including interest, every time, thanks to the FDIC’s deposit insurance.

Deposit insurance really works – even during the Financial Crisis!

I appreciate the thoughtful answer.

So next question (this probably sounds like Econ 101), why not nationalize banks? I hear the screams of “socialism”, but what we seem to have right now with taxpayer bailouts is reverse socialism.

Is there a workable example of a large banking institution being nationalized? Seems to me it would be like single payer healthcare–a necessary service becomes a function of the state.

RE: …why not nationalize banks?…

Is there a workable example of a large banking institution being nationalized?…

This was a state owned bank from the git-go

https://en.wikipedia.org/wiki/Bank_of_North_Dakota

It would seem that is would make more economic sense to create new SOE/SPE [state owned enterprise/state promoted enterprise] depository banks possibly with state charters, allow the TBTF banks to go into receivership, and transfer the viable accounts to the SOE/SPE banks. This would also “wash out” the “golden parachute,” bonus, and “deferred compensation” claims.

FWIW: Requiring the municipal and country governments to conduct all business through the state bank would allow much closer monitoring of income and disbursements, and most likely limit fraud because of the money trail. Depending on the bylaws in the articles of incorporation, such a state bank could also limit executive/director compensation to “human” levels, and require most of the capital/deposits investment to be in domestic in-state activities.

Nationalize to Stabilize.

Its been done before in Various ways. The nationalizing country itself need’s to have a reasonable debt levels (so forget southern Europe) or the problem simply hammers the currency further…

The question being at what price, and not with bond holders, and creditor’s (Beyond savers) made whole.

The state itself must be managed to make sure the NPL Balloons are not simply held and allowed to roll on forever.

The NPL balloon’s are what is ultimately behind this mess in Most Bank’s.

Look at their NPL to stock and capital ratios now their stock levels have moved in the direction of reality. The only thing keeping many Southern European banks afloat today is the ECB.

Many of them are effectively UNDER WATER, unless their stock values very quickly rise.

Fitch, S&P, and Moody’s, should be speaking on this, loudly, now.

Their speech’s would of course be the breaking straw’s for some, hence their silence.

Their is manipulation in the system, frequently not however, in the manner the anti bank, anti rich, conspiracy theorists, claim.

Mary,

There are many examples of really “public” banks. There is at least one state which operates one, they deposit all state receipts into it and finance public projects through it. Japan has a post office bank which I understand is very popular. These are nationalized institutions which operate for the public good.

I especially like the post office idea because it is accessible to everyone, however, they would definitely need to improve the service.

Thank you Mr. Richter for telling it like it is. You are correct, there is a big difference between an insured depositor and the other creditors of the bank. Too many in the ALT media fail, either intentionally or unintentionally, to make that distinction. Ellen Brown, for example, tells people that in a bankruptcy derivative creditors get paid first even before depositors. This is not completely true and is misleading. Insured depositors get paid first by the FDIC. The FDIC then stands in the insured depositors place in the bankruptcy proceedings. Ellen Brown knows this but continues to mislead people by saying that derivative creditors get paid before depositors in her interviews. Some other people, like Bill Holter, believe that because derivatives are traded in an FDIC insured bank that derivatives are FDIC insured. This of course is false. And some people when talking about bail-ins say that because depositors are unsecured creditors that depositors are include in bail-ins when the truth is only uninsured depositors that are in a systemically important bank could be included in a bail-in under the current law.

There are only a handful of people that have any real credibility with me. You happen to be one of them.

Money back?

HA HA HA, you’re joking? Tell me you’re joking.H AH AH HA HA HA…..money back? You’re cracking me up dude…..HA HA HA

Time to let the term “Moral Hazard” mean something, once again. If it were the Piazza Mfg Co. they would file for bankruptcy. Let the Banks do the same. Liquidate the bondholders, shareholders, and people with money above any ‘guaranteed’ maximums.

Let the bad bankers names be known as well. Prosecute any banks and PEOPLE who committed Fraud.

So I’m NOT a nice person. Deal with it…

This is the most infuriating aspect of the ongoing bailouts. Moral hazard is for the little people. Wall Street banks are too important to suffer the consequences of their poor lending decisions.

Oh yeah, and Goldman Sachs? When your counter-party goes under in the regular world you don’t get 100 cents on the dollar from the government. You get in line with the other creditors in bankruptcy court and accept pennies.

In the US at least, an individual can be banned from the securities and futures contract business by administrative action. By extension this should also apply to banking via the FRB/FDIC/OTS/etc.

We may be in a position where we require TBTF banks, but not the TBTF bankers, and indeed there appears to be no plausible reason why the existing banks cannot/should not be replaced.

To codify the process, an analog to the “point” system for suspension/revocation of drivers licenses used in many states may be helpful. Basically every violation of security/banking laws/regulations is assigned so many points, depending on the severity of violation and amount of loss. The [expiring] points would automatically accumulate against both the individual and the firm, and their occupational/business licenses would be suspended when the accumulated points exceed a given threshold, with revocation for repeated/egregious violations.

Well unfortunately in the US, we have an Attorney General who sat on the Fed’s New York Bank’s Board of Directors from 2003 to 2005 under then Bank Pres. Timmy G..

Thanks to President Obama and Congress, we have the Department of Justice run by a Wall Street insider. Justice for felonies committed by JPMorgan and Jamie Dimon means paying a fine and getting Congress to pass your lobbyist’s pre-written Bills into law. Remember what transpired on 16 December 2014!

The concept of Moral Hazard is outdated as it implies that these people actually have morals, which they obviously do not.

American taxpayers will end up bailing out European Banks. Watch. It’ll happen.

I believe that has already happened. Several years ago, in fact.

Yes. It was called QEII and the main beneficiary was the US subsidiary of Deutsche Bank, followed by Credit Agricole, Santander etc.

With what? The US is broke..

I guest the FED can print $’s if that is what you mean.

Looking over the deck chairs on the Titanic, I noticed that HSBC has done astonishingly better than any of the other chairs. What’s that about?

Most of their business is in Asia and presumed insulated from Euro turmoil. We’ll see.

sadly this can all spread. all this will carry over east and west. but the good news is that if it all goes at the same time we will all be poor. together.

“sadly this can spread”.

Recall that INTL FCStone Inc. said it will charge customers 200 percent of the minimum margin set by CME Group, for cleared futures for gold, silver, the British pound and euro currency.

As close of today INTL FCStone Inc. delivered 40 gold contracts and 30 silver contracts. The new margin requirements (+22%) set by the CME to take effect today.

CALL GENTLEMEN PLEASE. ALL ACCOUNTS TO BE SETTLED AT CLOSE BUSINESS TODAY. MARGIN CALL.

Oh JOY !!

HSBC performance? Beijing has much to fear from contagion and hasn’t hesitated to prop up stocks in the past…..?

Greenspan has been on teevee warning about out of control entitlements (for example, pensions underfunded), wonder if he had any part in creating this bubble?

All of this is his fault. He kept interest rates too low for too long and didn’t do anything to control derivatives. I honestly think the guy had no idea what he was doing.

Well, you can dazzle them with brilliance or baffle them with BS. I think Green-eggs-and-Spam was doing the latter. Apparently, he was shocked to find out that bankers are the world’s best thieves.

Greenspan knew exactly what he was doing, lining the pockets of crony bankster friends and politicos, knowing full well the bill would come do after he left and could rewrite history on TV, at award dinners and in his memoirs.

I actually read one of his books, the next to last one, found a stack of them at the thrift store for $1.

Let’s examine the logic here:

The Fed is a private company owned by a certain group of people.

They own the machines that print the money that allows them to control the world.

Now why would they care about enriching themselves or their minions?

Money is irrelevant when you own the machine that makes it.

It is all about the exercising of power.

We can all see that what the central banks are doing is going to explode violently at some point.

Essentially they are stacking dynamite and petrol in their castle and inviting the staff to smoke cigarettes.

This is absolutely not an issue of venality.

You need to ask the question: Why are the High Priests setting up to blow their kingdom to pieces? Why destroy the system on which their power is based?

WHAT DO THEY FEAR?

That’s peak sarcasm what you ask.

What Greenspan was maestro of was Greenspan speak. The financial journos had a job trying to decipher what he was trying to say in his congressional testimonies.

Well, it all sounded like an unprepared student trying to hide his ignorance by using upper class language among the peasants. The questioners were loath to ask a question for fear of looking stupid on camera.

You just HAVE to love the Plunge Protection Team. VIX actually went down!!!

I mean LOL. Whenever I read drivel written by Barry Ritholz on how there’s no manipulation, etc. Hei Barry, just look at today.

And the little boy shouted “The Emperor is buck naked…”

https://en.wikipedia.org/wiki/The_Emperor%27s_New_Clothes

I’m going to have to show my ignorance:

What difference does it make? I’m asking about a Bank’s share price. If the bank is itself sound, then the share price would be meaningless, if all this is just a big moment of chaos. IF the share prices are higher, does that mean the bank is more “sound”. They were higher last week.

Or, let me re-phrase this. Last week the shares were higher. This week is lower. The Banks themselves didn’t change at all in 1 week, so why do the prices, today, mean anything better, or worse, than 7 days ago?

If the banks were that bad, 7 days ago, then today’s share prices should have been….7 days ago. The same markets were buying and selling these bank shares, somewhat happily, last week. Now they panic?

Do you really think counter-parties are happy to do business with a bank who’s share price is cratering to 0?

Didn’t you see what happened to Lehman Brothers, Northern Rock, Washington Mutual, Wachovia to name a few recent examples?

It appears you missed it.

Do you think depositors are happy to have their money in a bank valued a ZERO!

Really? Are you?

Do you think loans made to said bank are just fine and dandy, don’t you think they’ll be called in ASAP?

I mean. Think buddy.

Think.

If the market values a bank as worthless, why should anyone else connected with the bank ascribe any value at all to the bank? And why would you tie up an assets in said worthless bank?!??

THINK MAN THINK!!

Everything you say, Julian is true and would seem obvious, but it really seems that half the country is sleepwalking*. In 2008 Societe Generale allowed itself, through lack of safeguards, to be robbed by Jerome Kerviel, who executed a series of “elaborate, fictitious transactions” that cost the company more than $7 billion, the biggest loss ever recorded in the financial industry by a single trader. I really thought so many depositors would leave in disgust that they would go bankrupt- but a few months later, their logo was all over the walls at the French Open, and business went on as usual. Ditto Royal Bank of Scotland. Go figure.

*Google “Hillary Clinton Scandals” and then the list of banks giving her 300 grand for an hour’s speech, and tell me how anyone worried about the state of banking would ever dream of voting for her- but she has a better than even odds at this stage of the drama.

But, if they were “worthless” because the British wanted to be Independent, then these same banks would have been worthless last week.

I guess what I am asking is, if they are worthless, they are worthless and the share price last week didn’t show it, so why the SURPRISE the share price this week shows it when the banks didn’t change, England did.

“I guess what I am asking is, if they are worthless, they are worthless and the share price last week didn’t show it, so why the SURPRISE the share price this week shows it when the banks didn’t change, England did.”

Buddy the EU just GOT CHANGED.

England is a Major contributor to the EU budget.

They need that English money to fund their EU Handouts.

The whole EU economic model, with out the English, is now up for serious review, and is found very wanting. No matter what pretty Positive talk, Junker (The English hater) and co, put on it

There is UNCERTANTIY (you should know Markets hate uncertainty) about the future EU.

Confidence in England has taken a hit. That took Sterling to a 31 Year low, and an average 30%, off its Banking Sector, stock values..

Confidence in the EU, has just been run over, with a fleet, of very large excavators.

Confidence is even more important than uncertainty, with out Confidence, a currency is worthless.

Look at the garbage (Garbage not Junk) Bond’s, the ECB is buying.

They are either trying to devalue, by undermining confidence in the currency (as they agreed not to enter into direct competitive devaluation’s) or bailing out their buddy’s with German Taxpayers money. That Germany may not hand over. Neither will help The Eur, or Club-med Banking stock values.

Sterling has been hammered first as it was heavily shorted. The Euro’s turn is coming and it will be worse. Much worse.

The only thing currently holding up the Eur, is so many country’s using it, in Europe.

When those Italian and Spanish bank’s star falling over en-mass, and at some point they must, things will get ugly for the EUR.

Basel II They insure each other. With Derivatives.

Cashless society? I would not be surprised if there is not a world-wide run to currency. Sure, it may be just paper, but it is more than a digit down at your branch bank’s server.

Just think. 300 million Europeans all trying to get, maybe just 500 Euros each out of their accounts so that HAVE sense of security.

There is no where near enough currency available.

Bring it on, bring it on – hoo-rah!

Jubilee time!

Wolf,

Great as usual. Is it your opinion that Brexit collateral damage is going to be significant?

We don’t even have Brexit yet (right now, they’re just talking) – and there’s already damage!

It’s a confidence game. Central banks re-propped up that confidence during the Financial Crisis. But by now, central banks have lost their credibility. So when confidence fails again, central banks are unlikely to be able to pull the same stunts. And when confidence goes in this over-inflated asset bubble, there just isn’t anything else to prop it up.

In terms of the real economy in the US, I’m not sure. The Financial Crisis didn’t hit the real economy until Hank Paulson told Congress that the world was ending, and that he needed unlimited power to bail out the entire financial system. This shocked business decision makers on main street, and they stopped ordering to preserve cash. And it shocked consumers, and they stopped spending.

In a little while, I’ll post an article on the US service sector and how it might deal with Brexit chaos.

I’ll keep my eyes on it.

We are soon going to see what would have happened in 2008 if the central banks had stood back and let the situation play out….

Only this time the collapse is going to be far more thorough …. far more epic…. and the central banks completely powerless to step in.

The Apocalypse cometh

I agree with EH about a run on notes…as I mentioned before, during the Lehman Bros. crisis, my bank had a sign up in the lobby that said “No deposits will be accessible the next business day Including CASH.”(caps mine). The tellers a year later denied it had happened–I wish I had a picture. When things get hottish I trek to the bank on which my paycheck is drawn and cash it immediately. And of course I have my bill-paying account in a separate bank than my paycheck bank. And I have written down on paper the addresses of my utility (mortgage) payments do I can pay them if TSHTF(to protect my credit rating).

If TS Truly HTF, then your ‘credit rating’ might be the least of your worries !

…just look at the current chaotic scenario happening in Venezuela !!

Do you really think your credit rating is going to matter when the banks all get nationalized(go broke)? Yes, I am shaking my head in total astonishment.

Actually, it’s quite common for employers to run credit checks on potential employees just to get a sense of how responsible they are with money, even if the job has nothing to do with handling finance or actual currency,

A bad credit rating can, ironically, give the human resources drones an easy excuse to screen out your resume or application. If they get 100 job applications and need to winnow them down to 10, they can just eliminate anybody with a credit rating below an arbitrary threshold. Why bother thinking when you can just open a spreadsheet?

IOW, it matters because corporations increasingly treat potential employees as a series of numbers to be computed rather than actual people to be evaluated.

Even if the system crashes, a good credit rating might be the difference between getting a job or not getting a job. Computers and HR drones will still exist, unless we revert to feudalism.

Never underestimate the inertia and blindness of a bureaucracy.

We lived through the Florida crash and our credit is still bad. The reason the credit rating didn’t matter for employment or even renting was that everybody’s credit was bad as well. We were even surprised that we were able to get credit.

When applying for a rental we were up front about our situation and the agent told us they charge for a credit report but don’t actually run it. He said they would be unable to rent out anything if they did. The bad rating didn’t keep us from buying a car as well. They only care that you have a job, any job. As far as employment goes, my husband’s last boss had lost his house and business too. I found the bad credit rating to be mostly insignificant.

I grieve that you lost your house Petunia and will gladly give up my (potential future) credit rating in order to dance on their graves with you :)

But if they hang on by their fingernails I might like to trade some hard goods for a house.

And how many atm’s were shut down for days due to Technical faults (NO cash to put in them) at the same time??.

Cash may only be pieces of FIAT paper. However when the electronics are turned Off. Cash is a whole lot better than a bunch of digits in an inaccessible electronic system. I am looking at abiog pileof cash and wondering wher to put it Wright now.

This is only the beginning. Brexit is not even formalized. Article 50 has not been invoked, It may never be invoked. Something however, will go bang in the Italian and Spanish banking System’s, before this is over, and that could roll into something BAD.

Dont be surprised to see an EU turnaround on Immigration and freedom of movement benefit’s. Before the British invoke Article 50. Leading to another British Election/Referendum.

Remember the referendum is not even Binding.

Also Remember the British a re a BIG net contributor to the EU budget. How many times have the “Tought Guy’s” in Brussels talked tough, Like tehy have been about the Brexit vote, right before they wimped out.

This Merry little mess is only just beginning.

Post 2008, the US had to subcontract some money printing to Switzerland, its own mint being overwhelmed by demand

Any one investing in these banks too big to fail at these prices?

Yes, if/when WFC hits $42 a share, I’ll pick up a bit. Sold my TLO right before market close yesterday (Monday, 27 June).

Can the Fed control the price on 2, 10 & 20 year T-Notes? Compared to most of the rest of the world, these ridiculously low rates seem high. At close, they were: 0.61%, 1.46% & 1.83% respectively. At least if you lend the Fed a pile of cash for 10 years you get a bit more returned to you; contrast that with German 10 year Bunds which are around -0.09% as I type.

I bought CS 100 contracts today. Lets see. I guess all will calm down.

If they get bailed out and the share prices spike — I suggest you spend your winnings very quickly….

The ship is sinking. And the central banks will not be able to refloat it this time

Those fish are made for trading, not eating.

The EU banks where a stick of dynamite looking for a match i.e Brexit.

Wonder if all the cash sloshing around has found it’s final home in real estate and the till is about to dry up? I guess this could be the canary in the coal mine?

>>>>>Deposit insurance really works – even during the Financial Crisis!

Well, MAYBE if its only a couple of Banks in trouble- it there were Regional or National Collapses, The FDIC would be on the next plane to Bermuda saying “So long, Suckers!”

Ya … kinda like fire insurance… if the entire country was on fire…. nobody collects

No, the FDIC would simply ask the Treasury to issue enough cash to cover the bills. It’s called inflating away debt.

You are correct RepubAnon. If the FDIC needs money to cover insured depositors they will get it. What that money will be worth is the question.

The Goldman Hacks boy, Draghi and the Fed old bag will wave their magic wands and presto, the can bounces further down the road to perdition.