A huge force that’s going to fizzle.

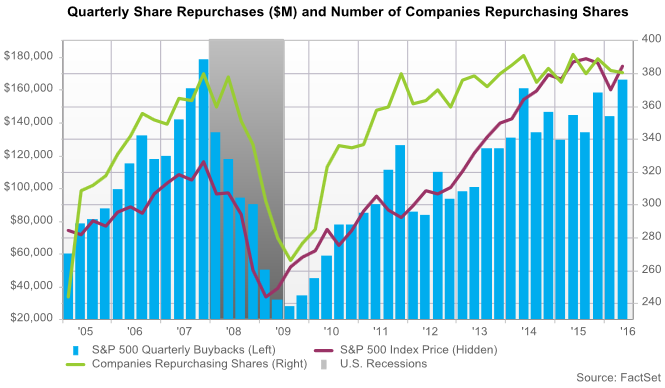

We have another post-Financial Crisis record on our hands!

Share buybacks by S&P 500 companies during the three-month period of February through April soared 15.1% from a year ago, to $166.3 billion, according to FactSet, the highest since Q3 2007, which had set an absolute record of $178.5 billion, just as the Financial Crisis was cracking the glossy veneer of the banks.

The tech sector, whose revenues have been getting hammered by reality, was the biggest spender at $34.4 billion.

The healthcare sector was second. When insurers and Big Pharma aren’t busy buying each other in the ongoing mega-merger oligopoly or monopoly boom, they’re buying their own shares. Buybacks over the 3-month period soared to $33.2 billion, an all-time record for the sector, blowing away its prior record of $24.5 billion.

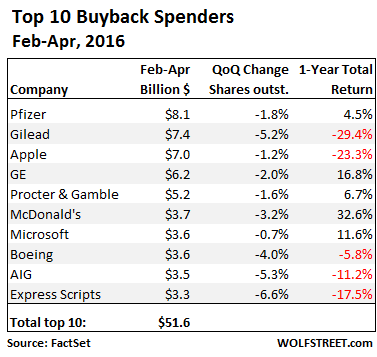

The biggest buyback spender overall: Pfizer with $8.1 billion. It reduced its outstanding shares by 1.5% year-over-year. It was part of an existing $11-billion buyback program and a new $5-billion program that was announced to make up for debacles elsewhere, such as the collapse of its $160-billion merger with Allergan.

Gilead was the second biggest spender, more than doubling its buybacks from a year ago to $7.4 billion, which cut its shares outstanding by 8.7% year-over-year, according to FactSet. This was part of its $15 billion repurchase plan, on top of which its board approved another $12 billion.

Pfizer and Gilead combined repurchased $15.5 billion of their shares in just three months! They pushed Apple, which had dominated the list, down to third place with $7 billion in buybacks. A third healthcare company made the list of the top ten buyback-spenders: Express Scripts with $3.3 billion, up from zero a year ago.

This table shows the top 10 buyback-spenders in the February-through-April period, along with the year-over-year reduction in shares outstanding, and the 1-year total return (including dividends) of the shares. Note the losers (red):

These 10 companies blew $51.6 billion in three months to prop up their own shares, much of it with borrowed money, rather than investing it in productive activities, preferably in the US, to move the economy forward. But no.

For the trailing 12 months, buybacks rose 8.7% to $602.8 billion!

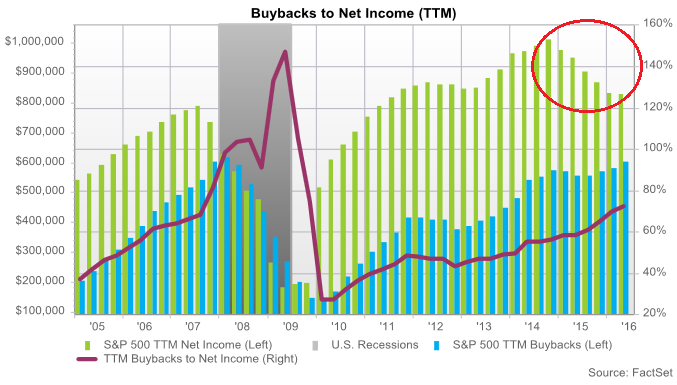

Alas, earnings of S&P 500 companies have been falling on a trailing 12-months basis since Q4 2014, six quarters in a row! The result of soaring buybacks and slumping earnings? 72.9% of earnings were plowed into buybacks!

This chart by FactSet shows the declining earnings, which I circled in red, the trailing 12-month buybacks (blue columns, left scale), and the buybacks to net income ratio (red line, right scale). The spike in the ratio during the Financial Crisis was caused by collapsing earnings. After share prices had collapsed, buybacks stopped. Companies don’t like to buy low. They like to buy high:

At this rate of slumping earnings and soaring buybacks, companies will soon spend more on buybacks than their income.

But wait… that’s already happening: 146 companies spent more on buybacks during the trailing 12 months than they booked in earnings. Among these heroes: Target, Starbucks, McDonald’s, Microsoft, Oracle, Salesforce….

Shareholder activists – or “corporate raiders,” as they used to be called for good reason – are souring on the practice, perhaps due to recent flops, such as Icahn’s foray into Apple: there were 19 campaigns in the quarter to push companies into this scheme, or push them deeper into this scheme, but only 3 succeeded. That’s down from 31 campaigns and 20 successes a year ago.

Why do we pay attention to this?

Because these buybacks are a huge force in the markets. Investors, leery of plowing money into stocks at nose-bleed valuations while revenues and earnings have been declining since 2014, are sitting on their hands. But someone has to buy, or else stocks dive.

Companies can borrow at ludicrously low rates (and even Apple has issued bonds to fund buybacks) to spend this money on their own shares. Those billions spent don’t show up as an expense. They just increase indebtedness and eat up equity. Buybacks hollow out balance sheets.

But they work on many levels. Programs are announced with the greatest possible fanfare, especially during earnings calls when earnings and revenues are crummy, or when a merger collapsed, and the CEO is desperate to prop up the stock.

The hype alone drives up share prices, or puts a floor under the plunge. When the company actually starts buying its own shares – the “relentless bid” that prefers to buy high to drive up share prices – it creates enormous buying pressure, even when no one else is buying.

And finally, the financial engineering effects take over: the reduction in outstanding shares increases adjusted earnings per share, the number Wall Street rubs in your face above anything else to get you to buy these shares.

This onslaught of buybacks has been the rocket fuel under the rally since February. It has been the one thing that performed miracles, overcoming even lousy revenues and earnings and a languid global economy in face of sky-high stock prices.

It performs miracles – until shareholders catch on to it and begin to rebel. That’s already happening. Then companies cut back. The share buybacks now playing out were announced mostly last year. As for new announcements of buyback programs, well, read…. Share-Buyback Announcements Plunge, Stocks Risk Getting Clocked

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hmmm… I checked on FT.com .. and Bloomberg… and CNBs… and I cannot see this story…

It is a rather interesting story… I am sure their readers would want to know about this….

Nice work!

Brexit looks like they’re leaving. USD on the rise.

#BeLEAVE is it

Yes, Brexit is a black eye for the PTB, the rentiers and other parasites sucking on the economy. Buybacks were a con to seem that the corporations were profitable, but there is only financial profits to be made now. The industrial “dynasty ” is just another in a succession of dynasties lasting no more than 250-300 years. Time’s up!

It would be so gratifying if Brexit were to serve as the trigger to cause the Dow to shed 10,000 points over the course of a week…

Unfortunately, I don’t the criminals at the Fed would permit that much reality to intrude into their fantasy world.

Unfortunately the successful EU exit referendum, is not legally binding upon the GB government. There will now be a period (2 years?) of intense and most likely vociferous debate, within the GB government and public, on how to implement a withdrawal from the EU.

This historic vote has been used as a smoke screen. Taken advantage of by those who wish to further their global domination goals. Working behind the screen to antagonize both Russia and China. While the worlds focus is tuned into the European/British parting of the ways.

The win by the exit vote has thrown the global financial markets into a tizzy, bringing with it a new focal point for the world to pay attention to. Rather than the quickly deteriorating macro political situation, with its bombastic militarist overtones.

There is never good news without conspiracy is there?

Excellent observation! By the end of the day everyone will have your insight too.

Most dangerous game being played by young, ill advised, management akin to playing chicken with a rabid pit bull. I say ‘young’ because most management now is young and the boards are older ‘financially well padded’ pets who lost their ethics long ago.

Can today be the day that their stock falls below net physical asset value of the company itself?

Will the bond holders be converted into stock holders when the value has finally dropped to zero?

The management is walking away with cashed-in options and the investor will walk away with wallpaper.

GE is the only company on that list that has withstood the time test. Can they now?

Now that GE has sold off the bank, will they still be able to get FED money at the window as before, or are those days gone for good?

Can Apple stay in business now that Beijing commands “NO MORE sales” and a new color doesn’t cut it anymore?

When the last day of business ends, the executives of these strip mined companies will retire to their gold plated homes, and their names will be forgotten the next day.

After all, it is just business.

GE was bailed out by TARP due to their fabulous leadership. Even owning the biggest propaganda machine in America didn’t help them.

As for Apple, it should have been liquidated the day Steve Jobs died.

Isn’t that the truth …

AAPL = Microsoft in drag.

“Those billions spent don’t show up as an expense.”

The money borrowed doesn’t show up as debt (ie:debt/eq)? Looks like some stocks are trading much lower than reported cash on hand?

This is just another symptom of the financialization of the economy. As has been shown, an outsized financial sector actually crowds out productive investment. Financialization confuses the map (stock price) with the territory (health of the business as an ongoing concern).

Why bother investing to expand production in a time of low demand, or work to enter new markets for your products? It will only lower short term profits, and thus the stock price, for speculative future gains. Instead you can push one button for a low interest loan and push another button to buy back the stock and make a big announcement celebrating your business acumen. The health of the business is no better off than before, but you see results on the map almost immediately.

It is not buybacks. I just did some calculations based on this article’s data. Between early 09 and now, it would have taken an additional $11.7 trillion in spending on the S&P to have it increase from its low of 800 to its 2016 high of 2100. The buybacks (according to the first chart) totaled roughly $3 trillion. So buybacks were only 25% of what drove the market.

Plus, if you look at the chart above, you see buybacks are positive (still taking place) as the market fell in 07-08. If buybacks were driving the market just having positive buybacks–no matter how large or small–would have sent the market higher, not lower. It’s other spending that is dominating market moves.

Buying ONE share of apple at $1 higher price increases the company’s market cap by more than $1 billion ($1 x # of shares). You don’t have to spent $11.7 trillion to increase the s&p market by that amount

Sure you do. Calculate it. The 1 billion you just mentioned is .02% of what it would take to move the entire S&P from the 09 lows to the current levels.

You can’t move Apple’s share price $1 higher by buying one share. Spending $93 cannot cause a $1 billion increase in market share. Just think about that. Even if somehow a trade was accidentally made for one share $1 above the last price, the market price would immediately revert back to the prior last price. Just you go and try it tomorrow and see what happens. See if you can move a valuation a billion dollars by spending 93 dollars. Good luck!

You can move shares higher with relatively minimal buy-backs … all that needs to happen is that you make it understood that if things go badly you are committed to buy-backs…

Institutional money will pile in along side riding the coat-tails…. and the share price surges.

Then you mean the company can do that. We were discussing market participants doing that. Even for the company to be able to do that, you have to explain why they failed to do that in 2007 and 2008 as they were buying back but stocks fell 50%. Even if they could–which means the whole stock market is then about mainly buybacks and not earnings and discounted cash flows and economic growth–it is still the spending by market participants that moves the price higher. You cannot get around the fact of spending. You can’t not get around mathematics.

The usual problem with buy-backs is that they happen at the wrong time: After years of increased valuations for the stocks involved.

The only right time for buy-backs is at the bottom of market cycles, if the company has any free cash available. This is what you want to do: Buy low. You want to set a floor for your stock in a bear market. You don’t want to be the one buying at the top: It makes your foolishness too obvious.

It used to be (and maybe still is the case) that buy-backs were very expensive to do in Europe, since the company involved had to pay tax on shares bought. As much as I oppose government intervention in capital markets, this is a system that might actually be workable: The tax is not on capital formation; instead; it’s on capital destruction, which is what stock buy-backs really are.