Mega-landlord prepares for downturn.

On Wednesday, mega-landlord Equity Residential – which “owns or has investments in 314 properties consisting of 78,351 apartment units” and whose chairman and founder is the ultimate real-estate market timer Sam Zell – warned for the second time since the end of April about apartment rental revenues.

This time, it blamed a flood of new supply in two cities – the craziest, most ludicrously priced housing markets in the US: New York and San Francisco.

Turns out newly signed leases aren’t meeting expectations in those cities, and they’re dragging down the company’s overall national results.

On April 26, the company had already lowered its revenue projections for properties open at least one year (“same store” revenues) from a growth of 5.25% to 5%. On Wednesday, it knocked the projections down to a range between 4.0% and 4.2% for the second quarter (emphasis added):

The revision is being driven by continued weakness in its New York portfolio and recent underperformance in the company’s San Francisco portfolio.

While occupancies and renewal rates in these markets continue to perform in line with the company’s expectations, new lease rates are not meeting original projections due to new rental apartment supply.

Equity Residential shares (EQR) fell 4% on Wednesday and are down nearly 20% from their 52-week high.

While overall statistics might show that rents are still rising in San Francisco – depending on what data you look at – there is now a lot of new supply piling up, and there’s no apartment shortage, even if few people can afford the apartments being offered, a phenomenon that we in San Francisco have come to call “The Housing Crisis.”

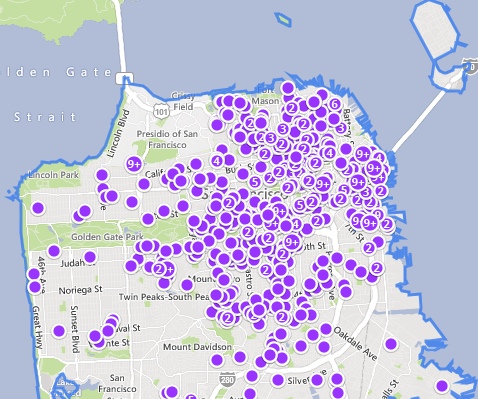

On Zillow, there are 1,248 apartments listed as available for rent. Note some of the dots that say “9+” which are big buildings, some of them with dozens of vacant rental units:

Trulia lists 1,722 apartments for rent. Craigslist, the apartment listings powerhouse in San Francisco, shows 2,500 apartments for rent.

That’s a lot of units for a small-ish place, compared to New York City. San Francisco has a total population of only 837,000 and measures only 7 miles across. And yet, apartment and condo towers are sprouting up like mushrooms.

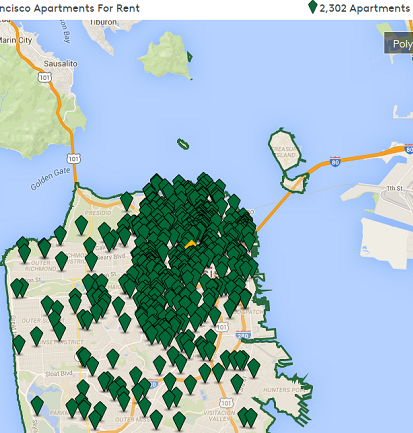

Apartments.com lists 2,302 apartments for rent on its site. Note where the units are clustered. These include areas where the construction boom is most obvious to anyone walking down the street. This is not exactly the image of an apartment shortage:

Of course, the rents are still ludicrous. But according to Equity Residential, downward pressures are materializing when it comes time to sign new leases with growing and increasingly nervous competition all around.

In New York City, a similar trend is playing out, according to Bloomberg:

Equity Residential is among landlords having to work harder to draw tenants in Manhattan as a glut of new apartments gives residents more bargaining power. In April, Manhattan renters were offered sweeteners, such as a month’s free rent or payment of broker’s fees, on 13% of all new leases, up from 2.7% a year earlier, according to a report by appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate. Property owners had to whittle an average of 2.9% from their asking rents to reach a deal, while the inventory of available listings jumped 23% to 6,718.

Sam Zell has seen this coming. This is just the beginning. Both San Francisco and New York are undergoing a phenomenal high-rise construction boom, and the new supply of condos and apartments is beginning to flood the market. Similar processes are underway in other major cities. It takes years to plan, build, and complete a high-rise. And now the flow cannot easily be turned off.

So Equity Residential has been unloading what it can. In its earnings release in April, it reported that during the first quarter it acquired three properties with a combined 479 units, but unloaded properties with a total of 26,126 apartments:

“Collectively, these dispositions produced an Economic Gain of approximately $2.4 billion and an Unlevered IRR of 11.8%,” it said at the time. And there would be more “anticipated 2016 asset sales.”

What is the company doing with this moolah? Deleveraging!

It retired about $2 billion in principal of secured and unsecured debts, the majority maturing in 2016 and 2017, “in order to maintain the Company’s existing credit metrics and strong credit profile.”

It’s preparing for tougher times. And it did so even though it had to pay $112.4 million in prepayment penalties. But when the dust settles a few years down the road, it will have the moolah and credit flexibility to go on a shopping spree.

But we’ve been warned, in between the lines: “No one has ever accused me of not being a realist,” Sam Zell told CNBC a few days before the company issued its warning. He was dissecting the markets for office and apartment buildings in major cities, explaining that they have already peaked and that there would be a downtrend. Then he got even gloomier and hammered ZIRP. Read… Ultimate Market Timer Sam Zell: “Know What the Problem Is?”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Trees don’t grow to the sky!” is as true for real estate as the financial markets.

It appears that we are being yet again offered the [forced] Hobson’s choice between continuing booms and busts in the real estate markets (and the severe impact this has on the aggregate economy) and much more intensive monitoring and intrusive regulation of the real estate markets (which will also have severe impact on the aggregate economy). It appears the real estate markets and its underlying finance have become too complex, international, and arcane for the “free market” to continue to function, in yet another example of killing the goose that laid the golden eggs.

This is not to say that a full or complete statist “solution is required, and it is likely that a combination of actions at the local and national level should be adequate, for example:

At the local level limit total “spec” residential and commercial building permits based on the projected total need of the community as determined by rational objective analysis using the available data and accepted methodology such as Econometrics. The downside is this can generate serious “rent seeking.”

At the national regulatory level, [e. g. SEC, FDIC, FRB, IRS, etc.] tighten promotional regulations and increase financing oversight to require plausible [not just well-written] business plans and projections, with high enough interest rates and enough developer liability to discourage “animal exuberance” and “speculation” with other people’s money.

It can’t be done. I have lived in several up and coming areas and the first casualties of high real estate prices are the working class residents. There is always an outcry about work force housing and subsidies, but nothing ever comes of it. The local politicians don’t have the courage to stand up to the big money.

Thats very true İn my town of Sag Harbor NY someone wanted to build low income housing and nothing ever came of it The homeowners in the area were afraid it would damage their home values which is a very likely fear

George

Yea – good solution – take the decisions out of the hands of people making real money investments and give it to corrupt local “planning agencies” staffed with government lifers.

Yea – that’ll work better.

How ’bout this: assuming you can definitively relate real estate boom/bust to wider market damage (I more or less agree with this general proposition), increase reserve requirement for banks making RE loans, and perhaps limit the amount of leverage an RE firm can have. That uses market forces (pricing) to change investment behavior…and it’s simpler to write about than actually implement.

Its already out of the hands of real money investments. Everyone is being shepherded into risky/crazy investments by a bunch of bureaucrats in central planning politburo.

In this city there are about 50 mostly middle and large size Apartment buildings, spread all over, that cater to the income of the individual-kind of a well kept secret. Not just to low income, but teachers, Police and Firemen and ordinary people who can no longer afford to live in the city limits. Rent calculated by income at about 35%.

The bad news: you are regulated by bureaucrats-who are very inept-but its not Section 8. But its better than living in a shack or on the street or 50 miles out of town.

RE: …take the decisions out of the hands of people making real money investments…

————————-

This is where the problem originates in that the real estate “investors” [more accurately speculators] put minimal amounts of their own money at risk, and much of what is at risk is not money at all but bank credit.

Amazing…the system has cancer and you want to double down? Essentially you say, if only we had the right rules, everything would be better. In actuality the rules are just fine for those who run the game. Current regulations are exactly what the donor class wants them to be. Legislation, regulation, and their implementation backed by force are now simply a product / service that the political class pawns off to the elite / power brokers. Did you not see the failed TARP vote when the vast majority of Americans were not in favor? Then three days later, ooh! it passed! On that day it became readily apparent who truly holds influence and whose interests are being protected (hint: it’s not us).

Equity Residential has/had a big presence in south Florida. I think the market peaked there at the end of last year. Because they are one of the expensive landlords, I think it was easy for them to see the peak.

The house I moved out of in Florida landed up being relisted for $5 a month less than I was paying before they raised the rent. We asked them not to raise it but they said no. They raised it 6% and told us we could expect an increase every year.

I moved from a Portland area apartment last month, we were new to the area when we signed the lease, & once living there awhile realized the rent was about 100$ more than market price. At the end of the lease they proposed a new lease for 150$ more a month. ( 11 % ).

The neighboring apartment had been vacant for 6 weeks. Drove by yesterday and ours is still vacant, too. Dunno wtf they’re doing. I mean it’s possible they own so many apartments in that area that they can control prices, I can’t think of any other reason they’d let units sit vacant.

Does anyone have rental and new condo development stats for Vavcouver BC?

Why is this guy crying wolf when he is also going to be hurt by it? It’s not as if his exposure is zero?

RE: Why is this guy crying wolf when he is also going to be hurt by it? It’s not as if his exposure is zero?

—————–

Don’t conflate personal with corporate liability.

While I have no access to his records, a large portion of the income he derived from real estate may already safely tucked away in a tax haven somewhere, and/or there are many ways to short the real estate market, given the proliferation of derivatives and mortgage backed CDOs/CLOs as well as the obvious ploy of shorting REIT shares.

Equity Residential is a publicly traded S&P 500 company. They’re required to file quarterly earnings reports. And in order to avoid “surprises,” they issue updates in between.

Just put half my rentals up for sale.

What part of the country/world are they in?

NM and AZ. Houses have appreciated in the last couple of years and I’ve had some tenant issues along with rents flattening. It feels like a good time to take some money off he table.

Sounds like a good idea. Keep us posted on your properties. Very interesting.

It’s Hilarious ….Rocket Mortgages are advertising here just now :)

(I am a compulsive reader)

I like their radio ads tho.

Wolf is rolling around in this news like a bear in honey.

How does he reconcile the over 15 year housing bubble in Canada?

Should interest rates stay near zero (they most certainly will) and the Chinese keep investing, the housing party will continue here in the USA. As Wolf has repeated tirelessly, the world is awash in printed money.

Does Wolf think that all the world’s excess Yen, Pounds, Yuan, etc will vanish overnight? No, they will, no they MUST, find a welcome happy home here in the USA real estate market.

Temporary pullbacks are the hallmark of any market.

I’m looking at the data, and I try to see early warning signs. I’ve been through enough busts to know that most people only see busts with hindsight, when it’s too late.

Until the central bank money starts showing up in the wages of everyone, housing faces some real limits that stocks don’t face. People don’t have to live in stocks or rent them, but they do have to live somewhere, either by buying it or by renting it. That’s where reality meets asset bubble. And something has to give.

This website shows the ratio of Silver to San Francisco Housing index.

http://deviantinvestor.com/tag/silver-housing-ratio/

Silver being a place money goes also when it is unappreciated.

That’s funny. The gold promoters think that the money is going to go into gold, and the stock market promoters think the money is going to go into US equities.

Ok I am not a big fan of gold but this is an interesting piece about goldounces/house. And it affirms that Petunia is right about gold being overpriced atm. From 28July15

http://danielamerman.com/va/GHratio.html

“The advantage to the Gold/Housing ratio is that because the value of one tangible asset is being measured in terms of another tangible asset, the dollars drop out of the equation – and so do any concerns about the accuracy of the inflation measure. ”

“The truth test is that the long-term average for the Gold/Housing ratio is 286 ounces to buy a house, and the current ratio is 202 ounces to buy a house. This would indicate that gold is overvalued by 42% relative to average single family residence prices in the United States, even with a $1,126 per ounce price for gold.”

i dont think that gold/housing index is trustworthy due to the gold market being global versus the US housing market which is not and it doesnt take into consideration debt levels and demographics İ will put my money on metals at this point and certainly Not US housing

Gold is a very regional investment. It has more value in places where there is no access to banking and credit. In India they pay a premium for this reason. In America we have many more transactional methods and therefore should discount it.

a bit disingenuous IMHO that Amerman uses a chart going back to the start of massive central bank money printing in the seventies. Of course real estate (slowly) took off and treasury rates started a decline lasting decades.

The question is if this period is representative, if it is ‘normal’. In my country there is interesting research about the ‘Herengracht index’ which tracks the prices of homes at the Herengracht in Amsterdam corrected for inflation (wages) . These homes were always the same and kept in good condition, as they were the homes of wealthy merchants. Although the relative value of Dutch homes has varied by a factor of 5 or so over four centuries due to e.g. economic booms and war, longterm there are very obvious borders for valuation – the values have always stayed within the band even though it sometimes took decades to correct excessive valuations.

Only around 2000 (the first top of the Dutch housing bubble) RE values were more expensive than ever in 400 years on a RELATIVE basis. They are even more expensive now. Feel lucky?

As to gold being overpriced: who knows, this is a tiny market that is bounced around by big players (central banks and their preferred manipulators). Dutch home prices measured in gold are much lower now than in 2000, but that doesn’t mean they are cheap …

This website shows the Shiller index in Gold up to Feb 2016 going back to 1890. I am almost convinced that the housing upward trend might continue for a while. That is, that there is time to get out.

Remember the old saying “better a year early than a day late” Once housing starts to implode it will be VERY difficult to sell in most areas anyway

For an interesting look at housing, go to Zillow for your town in US and filter to only show foreclosures…………..

http://pricedingold.com/us-home-prices/

oops i forgot to put this in

100 year Shiller in Gold

What I don’t understand is why anyone would have a home foreclose right now. If the housing market is so hot and there are not enough houses, they should be able to list their house and sell quickly.

I’m in Dallas. It seems there has been a housing shortage for years now, yet there are tons of foreclosures.

Houses go for above listing price here. It has been insane, with rents rising super fast also. It is almost not affordable to live here.

My apartment in 2009 was $1,060 per month. It was a 2 bedroom very nice apartment with a garage. I left it last year when it cost $1,600, because renting a house was only a little more expensive.

If someone could explain why so many homes are in foreclosure in this market of not enough houses to buy, I would appreciate it. Thanks.

I’ll give it a shot: In many instances, banks waited before cleaning out their mortgage fiasco dating from the Financial Crisis. They knew what the Fed was doing – creating another housing bubble – and they waited until home prices rose enough. Since they get money for free, it makes no difference how long they hold the homes. They just hung on to them and waited. Now they’re unloading.

While I don’t have cites, in many cases the problem is being “upside down” or “under water,” where the balance due, including second mortgages, exceeds the current value of the house. This is a direct result of cooperative appraisers overvaluing a home at the time the loan was made and/or “nothing down” negative amortization teaser loans at the market peak.

While a “short sale” at current market price would be the rational course of action for the bank to get the property/loan off their books, this would involve writing down the loan, and a [paper] loss, which the bank management is highly reluctant to do, as this would expose the extent to which the banks and mortgage origination companies are responsible for the 2007/08 debacle, and how much of a “house of cards” they really are, even after billions in taxpayer bailouts.

But current owners who cannot pay for their houses could easily sell them. They put them on the market and sell within days. The question is, why do they not just sell them before the bank takes over? This is a huge amount of houses on the market. People can hardly find a house to buy right now, it makes no sense to let the bank foreclose.

I can see older assets being sold by banks, that makes sense, thanks Wolf. But a current homeowner can easily sell a house in this market. It seems it damages your credit to let a house foreclose.

I’m so glad for this site. It is the only place I can find honest information on these things. Thanks.

>>> “But a current homeowner can easily sell a house in this market”

Yes, totally. It would surprise me to see people default on their mortgage in a market where home prices have been soaring. It’s just obvious that you should sell the home, pay off the mortgage, and keep the remaining cash.

However, here’s another scenario: if they bought at the peak of the prior bubble, and if in their market, housing hasn’t surpassed those prior bubble levels yet again, then a struggling household might throw in the towel and let the bank take the loss.