Atlanta Fed’s GDPNow Forecast Chills any leftover Q1 Optimism

In a very unpleasant and totally unnecessary move, the Census Bureau reported this morning that February sales by wholesalers, adjusted for seasonal variations and trading day differences, but not price changes, dropped 3.1% year over year to $427.6 billion.

This sales decline is largely in line with the overall sales decline among US businesses since late 2014. And businesses are finally taking the sales slump seriously and have begun whittling down their inventories. This has hit the Atlanta Fed’s GDPNow forecasts for the first quarter.

Inventories have formed a massive overhang that has been growing as sales have declined. For quarters on end, businesses have not adequately adjusted their orders to reflect the new sales reality. Thus inventories – unsold merchandise – have ballooned, sending the crucial inventory-to-sales ratio soaring skyward to levels not seen since near the peak of the Financial Crisis.

But now businesses are attacking the problem.

Inventories at the wholesale levels dropped to $583.3 billion at the end of February, down 0.5% from January (though they’re still up 0.6% from their levels a year ago). The crucial inventory-to-sales ratio, which measures how slowly inventory is moving, reached 1.36 seasonally adjusted, the same as in April 2009 and higher than in November 2008, after Lehman’s bankruptcy.

On a not-seasonally adjusted basis, the inventory-to-sales ratio hit 1.51, up from 1.47 in February 2015. In February 2009, at the peak of the Financial Crisis, the ratio maxed out at 1.53. At that point, the ordering pipeline dried up as businesses slashed their purchases. This will play out over the coming months again, but gradually.

Rising inventories boost GDP. They represent additional sales by suppliers. “Inventory investment,” it’s called. Thus, rising inventories are often considered “a sign of optimism” — until they reach the danger zone, when they become overhang. At that point, businesses cut their orders to bring their inventories down, and this eats into sales by their suppliers, and it drags down GDP. It can also trigger layoffs and a whole chain reaction of unpleasant events.

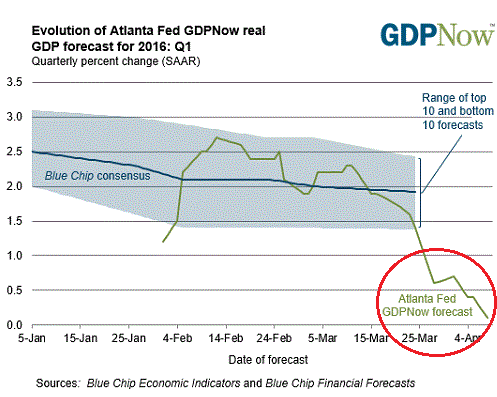

The data-dependent Atlanta Fed GDPNow model reacted to it:

After this morning’s wholesale trade report from the U.S. Bureau of the Census, the forecast for the contribution of inventory investment to first-quarter real GDP growth fell from –0.4 percentage points to –0.7 percentage points.

And its forecast for first quarter GDP dropped to 0.1% annualized — in serious stagnation mode, and a hair from falling into the negative:

The sharp decline from four weeks ago — when the GDPNow forecast was still at around 2.2% growth annualized — is remarkable. This is a result of crummy January and February data flowing into the model.

The GDPNow model still doesn’t include the pile of data for March, so if March turns out to have been a booming month, the GDPNow forecast will turn around sharply, and so we’re left hoping for the best.

Economists are already out there, preventively pointing out that a crummy GDP number in the first quarter is nothing to worry about. It’s the weather, they say. It’s just one quarter, and the first quarter is often crummy, they say. It’s followed by better quarters, which has been the case. We’re already hearing that song, though we didn’t hear that song a month ago.

But there have been too many distortions built up over time, including the inventory overhang. And they make us leery of any over-exuberant optimism for those better quarters to follow.

Private equity firms are already poking around the debris of the junk bond market. “Opportunities in distressed assets” – that’s what they’re looking for, even as they crush existing investors. Read… KKR’s Chilling Message about the “End of the Credit Cycle”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

producer prices for January goods were down 0.7%, after falling 0.6% in February…as a result, i have real wholesale inventories up 0.6% at the end of February, vs a real change of +0.5% for wholesale inventories in the 4th quarter, suggesting an incremental boost to 1st quarter GDP…admittedly a quick and dirty calculation, but it seems it’s not as bad as it would appear…

The Atlanta Fed begs to differ – we’ll see.

i dont necessarily disagree with the Atlanta Fed’s take, Wolf, because they certainly had to revise their previous forecast lower on the large January revision…that’s one difficulty with their algorithm; it doesn’t account for noise or revisions, and assumes a trend in motion will continue…the revision to January revised that month’s wholesale inventories from 0.3% growth to a 0.2% contraction….that in effect cut the January growth in real inventories in half, from roughly 1.0% to 0.5%…i assume Atlanta Fed’s prior -0.4 percentage point contribution to GDP had indicated higher wholesale inventories were more than offset by lower factory & retail inventories…now wholesale inventories isn’t doing much offsetting lower inventories elsewhere…

Have a look at this bloomberg chart:

http://www.theautomaticearth.com/wp-content/uploads/2016/04/USEarningsRecession.png

The economy appears to be hanging by a thread at this point. If this leads to a major recession with oil prices remaining low(won’t last forever) could we see two ugly recessions by the end of the decade?

It is just gravity reasserting itself from 2008. What could possibly go wrong?

With the feds sailing so close to the wind there are lots of things that can go wrong .The longer they stay there the higher the chance of an unpleasant surprise [ for the fed and govt it cant be a nice place to be ]

O bummer to Fed.

I dont care what you do, keep it alive, until I fly out.

Or Else.

The beginning of Hillary will be Ugly, if its Sanders or Trump, it will be an, Epic Economic Catastrophe.

At least Trump is smart enough to call out all of the bad news…called truth… in advance. No sugar coating from him.

İt looks like the FED has indeed painted itself into a corner This will NOT end well people İMO

http://ace.mu.nu/archives/362685.php

April 08, 2016

First Quarter Economic Numbers Look So Bleak They’ll Need the Addition of Obama’s Minions’ Number-Massaging Help

“There can’t be bad economic numbers before an election. If they look bad, maybe you forgot to add the Finageler’s Constant.”

“Whatever the first-quarter GDP number is when reported on April 28, it’s likely to be revised and it could easily be negative — or positive.”

“They’re not going to let it be negative, as that would set up the possibility of an official recession just before the election (two negative quarters in a row). They’ll make sure it comes in at at least 0.1.”

“What difference, at this point, does it make?” The PTB will surely put a thick layer of lipstick on the pig called the U.S. economy. The outcome here is “baked in the cake”, but the MSM/TPTB will spin it/obfuscate right up until Nov. 8th. There will of course be “revisions” in the data after the election. It all comes down to the stock market performance 6-8 weeks prior to the election, although I don’t know why since mostly the 1% own stocks and not the middle class. The wealth effect is a mirage. I’m pretty sure they can manipulate the markets up during that period, after all, they’ve had plenty of practice. The progressives know what’s best for us little people of course, and so 4 more years of a marxist/socialist is likely in store. What else do you expect from a command, centrally planned economy, comrade? The Big House in 2016 for Hillary (in my view).

Politics as per usual.

http://pjmedia.com/instapundit/

“Flashback: National Bureau of Economic Research redefines recession definition to move recession back from the third quarter of 2008 to December of 2007. Similarly, in the fall of 1992, the media hid the economic recovery occurring under George H.W. Bush’s watch to enable the Clintons’ “Worst recession in 50 years” lie. Or as a Time magazine headline writer described it with maximum self-satisfied snark on December 7th of 1992, “Bush’s Economic Present for Clinton.” The economy would grow 4.2 percent that quarter, but you never would have known it from the DNC-MSM until after November 3rd.”

“If voting made any difference they wouldn’t let us do it.” – Mark Twain

“If voting changed anything, they’d make it illegal.” ~Emma Goldman

Time to take a page out of the ECB/Eurostat playbook and include estimates for money spent on criminal activity like prostitution, drugs, illegal arms trading etc. in the official GDP numbers. In the EU this instantly added many percentage points to the GDP number of some countries; bureaucrats can get very productive with the right incentive. I wonder if they are already counting the income streams from human trafficking and terrorist activities, those could probably add some extra percentage points.

Don’t know if there is much left to add to the US GDP number though ;-)

Just how long can the FED maintain this charade?

Short-sell in May and go away?