Why Oil Keeps Falling off the Chart

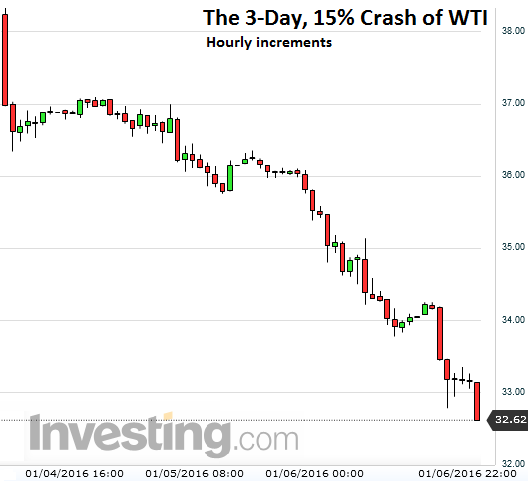

After having been through the greatest two-year loss on record, the price of oil plunged 9.6% on Wednesday and in evening trading. As I’m writing this, WTI hit $32.62 a barrel, a new low since the desperate depth of the Financial Crisis, when it very briefly kissed $30.28 a barrel on December 23, 2008, before bouncing off sharply.

This time, it’s serious. Brent, the global benchmark, has crashed to $32.75, an 11-year low. This isn’t a quick scare that happens during a Financial Crisis. It’s the result of a persistently growing glut.

Since the oil price plunge began in July 2014, every rally, every “opportunity of a lifetime” to buy oil “for cents on the dollar” has turned out to be a falling knife.

This is what the three trading-day, 15% crash of WTI looks like:

The contagion of the oil price plunge has been drifting into other sectors of the US economy, housing and office space in Houston, the state budget in Alaska, jobs, manufacturing…. Investments have gone up in smoke. Loans have gone bad. Defaults, restructurings, and bankruptcies are now a routine occurrence. Banks are looking over their shoulder. PE firms are licking their wounds from their mega-bets on fracking made in prior years, and they’re licking their new wounds from having tried to catch many falling knives.

This isn’t going to be an easy bust to get through. It’s a US problem. And it’s a global problem.

In the US, crude oil production started declining on a monthly basis in mid-2015, according to EIA estimates. But despite those monthly declines, production averaged 9.3 million barrels per day in 2015, the highest rate since 1972, and a 7% increase over 2014.

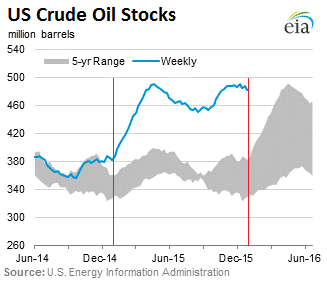

On Wednesday, the EIA reported that US crude oil stocks dropped 5.1 million barrels during the week to 482.3 million barrels. Drawdowns at this time of the year are common. So it left stock levels a monstrous 100 million barrels above the already high stock levels at the same time last year.

The chart shows the hair-raising stock levels. I added the two red lines to juxtapose the already high stocks at this time last year (above the 5-year range, gray area) with the current level:

Note how declines are common this time of the year, but how last year at this time inventories began to skyrocket. It is unlikely that inventories will skyrocket to the same extent this year. If they do, it’s going to get ugly beyond comprehension. It’s more likely that inventories will rise at a pace closer to normal seasonal increases. Even those increases will inflate inventories – if there’s even enough storage capacity available – to dizzying heights by the time driving season begins.

However, the spooky thing in Wednesday’s report was the buildup of 10.6 million barrels in gasoline stocks, the largest weekly buildup since 1993. Without it, there wouldn’t have been a crude oil drawdown!

And all this comes on top of the kerfuffle between OPEC members Saudi Arabia and Iran. It will make any kind of OPEC deal for production cuts unlikely. Iran is itching to ship its production into the global markets when the sanctions are lifted. And Saudi Arabia has its own reasons to maximize production. So unlike prior flare-ups in the Middle East, this time, they all appear to work against oil prices.

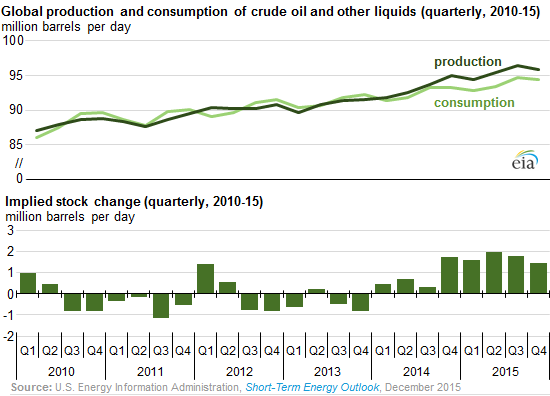

Whatever the daily hopes and fiascos that dominate the oil trade, two things remain fundamental: global production and consumption. And there, things are becoming uncomfortable.

In the fourth quarter, global production of crude oil and other liquids actually dropped, according to the EIA estimates, but so did global consumption.

The slowdown in China? Today, Chinese stocks crashed as trading got going, and after the Shanghai Composite plunged 7.2%, trading was halted. Now everything is stuck. Over the past four trading days, the index is down 12%! Something is seriously wrong in China, whether or not the government wants to admit it. And some of it is hitting global oil consumption.

The slowdown in India doesn’t help…. Whatever the reasons, despite a drop in production, the oil glut just got worse.

In the chilling chart below, the top half shows to what extent global production has exceeded consumption quarter after quarter for the last two years. Note how in the last quarter, both production and consumption declined.

This overproduction, and now declining consumption, resulted in a stupendous increase in global inventories (bottom half of the chart), a trend that started in earnest in Q4 2014. The EIA estimated that 2015 experienced a “net inventory build of 1.72 million barrels per day, the highest rate since at least 1996.”

The global decline in oil consumption in Q4, and the whiff of mayhem so far this year in the financial markets is worrying beyond oil. Though sporadic quarterly declines in oil consumption are not that unusual, but typically they occur in Q1, not in Q4, with consumption in Q1 being consistently weaker than in Q4. So the decline in consumption in Q4 2015, especially if followed by the typical downturn in Q1 2016, comes at the worst possible time.

Already global corporate defaults hit the highest level since 2009, with the US leading the way, while the US Distress Ratio has soared. Read… Global Corporate Debt is Coming Unglued

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Reminds me of the 80s in the industry. Blood ran in the streets of Houston, Dallas, Tulsa, Oklahoma City, and Denver. Oh, I know this time is different. But, there will be major dislocations and the host cities for the industry are going to notice. On top of the staggering debt the industry has piled up, this time around, a significantly higher percentage of the boom driven wells drilled were unlikely to have paid out in what was expected to be the oil trading range. So, when the reality of the state of the industry is fully digested by players and investors, it is likely to be much uglier than many have thought.

Are we nearing the day of capitulation? Or does this roller coaster continue for a few more months?

I didn’t catch the price of TAPIS crude today, but the other day when Brent was around $37, TAPIS was a little over $37.

Back in the good ole days the spread was much higher (IIRC as much as $10) and an indication of the demand for crude from China.

Here in Oz our products are supposed to priced off the Singapore markets, but today gasoline is still selling at A$1.20 a litre here in Melbourne. Still way too high given the price of crude.

Another item to be aware of is the situation in Japan. There a few nuclear reactors are starting up which will hit demand a little and the continual fall in population.

Last year Japan lost 294,000 people. This is the 9th year in a row of falling population levels. Yes, the people are old, but even so the loss of that number of people will have an impact on demand from Japan.

Maybe Japan should consider importing Syrian refugees ;)

Yeah, well at least, for now, that will never happen in Japan and more power to them for that.

Unfortunately, the camel has gotten its head into the tent there as well.

Even out in the middle of nowhere Hokkaido you can find the so called “Religion of Peace”……………..

Ahahaha, only the naive or the braindead will believe Megacorp Greed Inc would pass their gigantic oil savings to end consumers.

They are always playing the “heads I win, tails you lose” game for us all. That is also why end demand is slumping despite the superficially low raw crude prices.

You bet Lee…

You’re getting the same shaft as we get (Canada), and we’re a big producer (but the profits are all multinational thanks to years of conservative corporate hacks).

Anyway, my contribution to your comment is to add the nefarious step of converting to litres (not sure when it was done in Australia but it was the seventies here ). I’d just love to see them post those huge $5.60/gal signs and try to justify the profits they extract!

The global economy is mired in “no growth” land, the US and EU programs of QE or whatever they want to call it these days to goose the economy is a total bust, the Chinese juggernaut of 7% annual growth has been revealed to be a fraud (big surprise here), the US, Saudi Arabia and Qatar are fighting a proxy war in Syria vs. Russia, Iran and the Syrian Government, and Saudi Arabia seems determined to pump as much crude as possible until either they or the global competition go bankrupt. I’m not sure what then end game will be but it won’t be pretty.

End game is ‘probably’ a few governments around the world will collapse…as to which one’s and when, that is anyone’s guess.

in 1942 german u-boats were sinking ships off our coasts.

and that was one of the better parts of the world.

things aren’t so bad.

have a piece of cheese.

Global economy is also mired in debts galore created out of thin air FIAT currency.

BTW – debt is either paid off or defaulted, even the debt can kicked down the road.

Are there any non-fiat currencies?

Gold and silver until Nixon “SHOCK” abolished the link.

From Nixon Shock wiki: The Nixon Shock was a series of economic measures undertaken by United States President Richard Nixon in 1971, the most significant of which was the unilateral cancellation of the direct convertibility of the United States dollar to gold.

Funny as many if not all FALL of empires whether it be famous Roman and Chinese had to do with reducing precious metal content on their “currency” till they all imploded…

There’s an old saying: “the cure for low prices is low prices”.

Banks have supposedly cut back on lending facilities to many of the weaker credits in the oil patch. If so, look for bankruptcies, forced mergers etc. later this year–all of which should result in declining production–at least a modest positive for commodity prices. Maybe the back half of 2016 provides some pricing relief.

Forgive my potentially ignorant comment/question, but will oil BKs and forced mergers allow the price per barrel to lower for the new owners of that oil? Thus lowering the cost of production and allowing the US to be more competitive with cheap Saudi oil?

Hi Frontrow,

Not ignorant at all. Very good question actually. Yes, the new owners who purchase/acquire distressed assets do so typically at a much lower cost basis than the distressed seller. They’re typically wiping out equity investors and buying the asset for a fraction of the value of its underlying debt. No guarantees they’ll make a profit but they do have a lower cost base which helps a lot. But my point was also that the weaker credits in the energy space will lose access to financing and that a portion of this capacity will simply shut down and be removed from the market as uneconomic. This should begin to help balance supply and demand thus support prices. However, if demand continues to drop then we’re in an infinite regress of financial pain.

Thank you. I agree that energy will definitely lose access to funding, but there has to be some kind of price support for these distressed assets, there is some value. I suppose someone will come in eventually and take the risk that prices will stabilize or rise. If the capacity were to shut down, who would own the defunct asset? I guess the answer could be “no one”, but I’d have to guess someone out there would be able to get a low enough price (market price) to potentially produce. But what do I know? This will all be very interesting to watch. Thanks again!

regarding:

“WTI hit $32.62 a barrel, a new low since the desperate depth of the Financial Crisis,”

And? The only difference is that the new ‘desperate depth’ was backstopped and papered over this time around with abunch of QE. The crisis never disappeared, it was only turned into opportunities for the connected and a chance to gamble with other people’s money.

I was watching CNBC this morning while I rode my ‘bike’. I heard Cramer talk about the Macey carnage (oops plans). He said, “Macey’s sales were down because of the WARM weather, (I kid you not). He said if the weather was colder they would have sold more winter coats.

Last year it was the bad weather for an excuse about the economy. Now, it is flooding lowering the refinery demand for NA oil, thus the oil price drop. And, this damned warm weather, of course. Poor winter coat sales. (I couldn’t believe it?)

Got cash? Got land?

regards

Paulo: I was watching some of the financial reporters from various networks trying to low-ball the market problems. They made me think of a cruel animal act from days of yore, where they made a chicken dance on a hot plate. Felt sorry for the chicken; not so much for the financial reporters. After all, they are paid handsomely as cheerleader propaganda shills for the market/Fed apparatus.

Regards to you.

Consumption peaks in Summer, and drops in Fall. I thought that is very common.

The weakest quarter is Q1, which is always worse than Q4. Most of the time, global consumption rises in Q4 then it often falls in Q1.

This time around, it fell in Q4, and if it follows seasonal patterns, it will fall even more in Q1.

but doesn’t the 1st qtr have the most IRA and 401k deposits?

It looks like the crisis mode is coming quicker than expected. I thought that the Fed was going to stay pat at the next meeting, but maybe they’ll head back down?

Desperate times, desperate measures.

Strong dollar, lower energy costs and new rounds of layoffs does not bode well for their “inflation targets”.

One thing already happened. China decided to suspend her own “circuit breaker” rule after having used it already twice in just seven days.

Apparently somebody noticed if all trading halts, the plunge protection team cannot do its job. As I write Shanghai is rapidly soaring, propelled by the Big Four and/or other entities getting the money from them.

China may have gargantuan monetary reserves (not to mention the ability to print renmimbi more or less at will) but in the last seven months they burned through an immense quantity of money to both prop up stock markets and fiddle with the yuan peg. The quantity of money poured into Shanghai and Shenzen alone after the June 2015 crash simply defies belief and probably has Wall Street green with envy.

Now oil. Last month a Rosfnet/Russian government official (cannot really say where one ends and the other begins) mused “Maybe the world won’t need as much oil as we think it will”. Demand has more or less flatlined if not slightly declined in the past two quarters despite there being officially no recession (unless you happen to live in Brazil or Russia).

Again I will turn to China. The Celestial Kingdom has been for the past decade the automotive industry’s Comstock Lode. Far from showing any form of restraint, everybody, from GM to Honda, adopted sales policies to push Chinese to buy as many cars as possible to goose sales, not in the future but damn right now.

Like in the old story, the goose that laid the golden eggs has been killed in the name of making a quick buck. Inventory buildup in China has taken enormous proportions with most dealership having over 200 days in stock right now. Carmakers refuse to reduce production (like Amazon they depend on volume more than profits) and that buildup will continue until either dealers start going under in mass or somebody blinks.

Yes, China’s growth has finally ended and, yes, President Xi’s “crackdown on corruption” has taken its toll on luxury car sales, but I suspect the basic reason is Chinese consumers have bought more cars than they can financially afford at the moment and are having a massive hangover. Unless Beijing comes up with another of its harebrained schemes (like using more concrete and rebar in a year than the rest of the world uses in ten), it will take years for the situation to normalize.

If the quantity of cars (and lorries, and vans etc) on the road remains the same, fuel consumption will either remain the same or slightly decline as more fuel efficient models are introduced and slowly replace previous models.

If we apply the same reasoning on a worldwide scale, it’s easy to see unless the Fed pulls another rabbit from the hat why oil consumption is flatlining or even slightly decreasing.

If we add naval and air traffic to the picture, it gets worse: when an airline orders a new Boeing 787 or Airbus A350, it buys a far more fuel-efficient aircraft than the one it replaces. Modern two stroke diesel engines, the prime movers of naval freight traffic (a market wholly owned by just three companies: MAN of Germany, Wartsila of Finland and Mitsubishi of Japan), are unbelievably fuel efficient.

Now, things would be fine and dandy (for oil companies and oil-producing countries) if absolute numbers kept on increasing at a steady pace, like official Chinese GDP figures. But they don’t. We are at or very near peak figures for almost everything for this supercycle.

It doesn’t really have to end with a bang like a great recession. A long, almost imperceptible but unstoppable decline may be in the books.

A work for soothsayers, not us, to predict.

Excess speculation in the oil, gas and tech sectors by use of leverage, eventually will have to be paid for. This is going to require a large amount of debt to be written off.

Global oil and gas exports have fallen to 1958 levels. The direct job losses have been significant, with much more to come. The entire global multiplier of the oil and gas sector down turn is huge.

The ancillary job losses (pipe, drill bits, heavy equipment, transport, even the waitress serving coffee) is very large and growing larger by the day. The amount of global revenue taken out of the system, when adding in the ‘knock-on-effect’ , is 10 to 15 trillion dollars.

The direct, observable effect has been the cliff drop in exports and imports, bringing global trade to almost a standstill.

Absolutely. The knock-on effect of over-production and consumption, pulled from the future, means that the cliff is much steeper.

The spectacular successes at killing the buying power of the labor sector, with automation, consolidation, and off-shoring, has ultimately crushed the consumer too. (Can’t believe these fools didn’t see that ‘we’ are one and the same). Loading us with debt made a generation or so compliant but only put off the reckoning.

With the ancillary job losses, there are no buyers, no velocity of money.

2016 may see the ultimate failure of capitalism.

Yes but when your own compensation is based on the quarterly numbers, most CEOs and CFOs just do what it takes to make the numbers look right so they get theirs…

Pretty lousy way to run a ship of state but that is how it is done. Long term planning seems to not be available to the corporate leaders of today. Just like the consumers who want instant gratification and borrow from tomorrows earnings at a cost, corporations are the same. As long as the money was available, they wanted tomorrows income today..

Cap K –

Steep cliff indeed.

The Baltic Dry Index has totally collapsed.

A disaster. It has fallen 96% in 67 months.

There was NO RECOVERY. Being down NINETY SIX PERCENT!

Global trade has slowed to but a trickle.

WTI was supposed to have bottomed out in July 2015. Then again in late September 2015. Mere wishing thinking.

So much capital has been destroyed that even if the price per barrel were to recoup, it’s too late. Along with that, the operating/layers of production cost of hydrolic-fracturing and bitumen mining and refining is too high. The same thing would happen. High production cost leading to high energy prices leading to slowed economic growth and the inevitable creation of debt. That, in turn, leading to another glut. It’s a vicious loop of which can’t be escaped.

Thanks for posting the low of $30.28 a barrel of oil on December 23, 2008. That’s valuable information. Your records are great.

In my view oil and natural gas and are on different paths.

With every weekly report on oil the glut worsens. I believe there is a large underestimation of the amount of oil stored on tankers, rail cars, and any other place that holds oil, many or all of which are not counted in the reports published each week. In addition, Iran’s oil sanctions are still in effect, but its oil will shortly enter the market and increase the glut.

Natural gas is very different from oil here. Starting with the last fill in 2015, prior to each weekly report, the storage expectations have been overstated. The last fill in 2015 of about 6 or7 Bcf was below expectations by about 4 or 5 Bcf. After that each weekly draw was greater than pre-report estimates by approximately 10% to 20%. Today’s draw was 117 Bcf . The pre-report estimate was 95-97Bcf.

Its not just the return of winter weather that is a factor in the natural gas market. Perhaps production of natural gas is dropping faster than expected. Perhaps natural gas is being consumed or exported fasted than expected. Whatever the explanation, if this tend continues, the glut in natural gas could be eliminated before the fall season.

NY: I haven’t been keeping up with natural gas deliverability. We may be in for a price shift. But, the thing to remember is that there is a lot of gas and it is relatively easy to find and produce. Conventional, shale gas, coalbed methane. As many of us who worked gas prone basins have experienced, when the price goes up, exploration increases, a lot of gas is found and the price starts down.

I believe the driver here will be whether natural gas can be produced at a profit based on the price of natural gas. A great many natural gas plays are dependent not on profit from selling product but on financing, which is largely no longer available.

A lot of statements about how cheaply natural gas can be extracted via fracking are suspect because they are made solely for the purpose of attracting investors and loans.

I doubt that any of these plays is profitable when natural gas is below $3 to $4, and that level is not sufficient to reawaken a boom mentality for natural gas production.

I’m not sure if your readers are aware but the Chinese have imposed there communist laws in the selling of stocks. First it was a 6 month ban on selling stocks, so those stocks came due around now and we’re sold. The next big plunge will be in the Spring. Second they imposed that you cannot sell anymore then 10% of the stock, now they have changed it to 1% of the stock, so it will take you 100 days to sell your entire holding at 1% a day. It’s called kicking the can down the road and not dealing with the immediate problem just like everyone else on the planet has done. China is done. Oil is done. The BRICS are done. move along call me in 20 years for the next boom.

All I hope is that China finally has there revolution over the crash and gets rid of there communist leaders and becomes a democracy.

I don’t think you really want to see a “revolution” in China. Revolutions are bloody and terrible. They usually lead to even worse dictators. And with an economy as big as China’s, a revolution would wreak havoc on the world economy. I’m sure you don’t really want that.

The best hope is that China will reform and get its economic house in order.

Wolf – Your response was much better than mine.

Unfortunately, history tells us that dictatorship, communist or fascist types, don’t do “reforms” at all. They will fight tooth and nail to preserve the status quo and hang on to power to the last breath. To wit, China and its power elite – the Politburo and the business class supporting them – will be no exception. They will not easily relinquish power in order to usher a smooth transition from an obviously corrupt system just so the rest of the world’s economy will not gyrate violently. That’s not in their DNA. So, expect some very disruptive, even violent, times ahead in the Middle Kingdom when the SHTF finally happens, it’s rapidly approaching IMO.

Like I said, war……and not like any other war imho…… Therefore $30 oil will be a distant past when that occurs……. At the same time the dollar will be killed and remember oil is presently priced in dollars…… A perfect storm (sorry for the description) will present itself……… I suspect the banksters (while digging their bunkers) are positioning themselves accordingly.

What a bizarre hope. What makes you think any revolution would result in a democracy? I suspect it would end in tribalism and we know how well that has worked in the middle east. As much as we would like to wave our magic wands and have the world return to the good old days, we are stuck with the world as it is.

The funny thing I have noticed is that the richer the rich get the meaner they get. The wagers of hard working people have gone backwards creating modern day enslavement .the rich are getting richer and the poor are getting poorer in the west a recipe for disaster .

China has the authoritarian streak down pat…they just don’t have the anti-corruption and high standards such as Singapore possessed during it’s ascent.

—-

The difference is, in the west we have the safety valve of democratic elections, allowing peaceful change….China has no such valve.

Peaceful change? From one candidate who is bought and paid for to another – also bought and paid for. And nothing changes…

“…a recipe for disaster.”

Yes, capitalists and bankers seem to be of one mind: market/demand destruction. Add into that FRB policies that have engineered into the mix simultaneous resource misallocation and maldistribution. No Malthusian could have wanted a better perfect storm of destruction.

2016: Oil Limits and the End of the Debt Supercycle

Posted on January 7, 2016 by Gail Tverberg

http://ourfiniteworld.com/2016/01/07/2016-oil-limits-and-the-end-of-the-debt-supercycle/

Great article (unfortunately) ! Everyone should read it.

The quoted article severely underestimates humanity’s greatest assets, innovation and resilience. We’re going into a stock market correction, not ushering in the end of civilization as we know it. Good grief.

Are you sure ? We have been living in a strange environment for years now. Something big is going on.

Something big is always going on, isn’t life exciting? :)

What hasn’t been factored into the price of oil is WAR…… Watch the futures jump to unbelievable levels (now) when that happens…… Could it be all those tankers storing oil for a reason ?