“We are looking at real carnage in the junk bond market,” Jeffrey Gundlach, the bond guru who runs DoubleLine Capital, announced in a webcast on Tuesday.

He blamed the Fed. It was “unthinkable” to raise rates, with junk bonds and leveraged loans having such a hard time, he said – as they’re now dragging down his firm’s $80 billion in assets under management.

“High-yield spreads have never been this high prior to a Fed rate hike,” he said – as the junk bond market is now in a precarious situation, after seven years of ZIRP and nearly as many years of QE, which made Gundlach a ton of money.

When he talks, he wants the Fed to listen. He wants the Fed to move his multi-billion-dollar bets in the right direction.

But it’s not a measly quarter-point rate hike that’s the problem. Bond yields move more than that in a single day without breaking a sweat.

The problem is the risk investors piled on over the past seven years, when they still believed in the Fed’s hype that risks didn’t matter, that they should be blindly taken in large quantities without compensation, and that rates would always remain at zero. Those risks that didn’t exist are now coming home to roost.

They’re affecting the riskiest parts of the credit spectrum first: lower-rated junk bonds and leveraged loans. Gundlach presumably has plenty of them in his portfolios.

Tuesday, the day Gundlach was begging the Fed for mercy, was particularly ugly. The average bid of S&P Capital IQ LCD’s list of 15 large and relatively liquid high-yield bond issues – the “flow-names,” as it calls them, that trade more frequently and include big issuers like Valeant Pharmaceuticals – dropped 181 basis points to about 87 cents on the dollar, for an average yield of 10%, the worst since July 23, 2009.

“Momentum was fully negative, with all 15 constituents in the red,” LCD reported.

Among the big losers: California Resources. Its $2.25 billion issue of 6% notes due 2024 plummeted 10 points to 45 cents on the dollar.

They were issued in September 2014 as part of the company’s misbegotten spinoff from Oxy. Last September, when I wrote about this masterpiece of Wall Street engineering, the 6% notes had just plopped to 66 cents on the dollar. The company – its shares closed at $2.69, down 73% from their 52-week high – is now trying to inflict a debt swap on its bondholders, and these 6% notes, as LCD put it, “will be left out to dry as a small, stub piece of unsecured notes below a new second-lien series.”

These kinds of debt swaps are now all the rage – a form of default where existing bondholders and stockholders feel the discomfort of evisceration.

Also engaging in these sorts of bondholder-I-love-you-so antics is Chesapeake Energy whose 4.875% notes due 2022 “tested” just under 30 cents on the dollar, down from nearly par a year ago. Another debt-swap paragon, Halcon Resources, saw its 8.875% notes due 2021 drop to about 30 cents on the dollar, from 75 a year ago. And so on. Debt swaps instead of bankruptcies. For bondholders, the outcome may be similar.

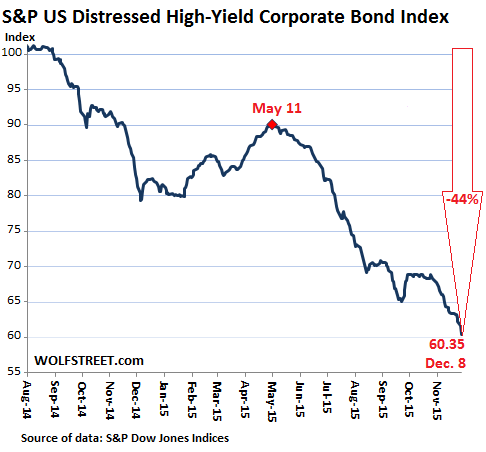

And so the S&P U.S. Distressed High Yield Corporate Bond Index, which tracks these sorts of bonds whose yields are 1,000 basis points above Treasury yields – dropped to 60.35, a 44% plunge from September last year:

The iShares High-Yield Corporate Bond ETF HYG, which tracks the broader high-yield market, dropped to 81.06, a low it briefly pierced during the panic in October 2011 when the euro-debt crisis and a threatened default by the US during the Congressional debt-ceiling farce knocked down global bond markets. Before then, the last time HYG was this low was in July 2009.

This is the environment junk-rated companies are facing: new money is getting scarcer and more expensive for those at the upper end of the junk range. For those at the lower reaches of the range, new money may be impossible to get.

Which is what Energy & Exploration Partners of Fort Worth ran into. It couldn’t bamboozle investors and banks into handing it even more money. It was forced to withdraw its Hail-Mary IPO in September. And on Monday, it announced that it sought refuge from creditors in a Chapter 11 bankruptcy filing, “because it ran out of cash,” as it said in the filing.

The 18th oil & gas driller in Texas to do so. Its leveraged loan, originally $775 million, was syndicated in July 2014 via Citigroup, Credit Suisse, and Global Hunter. It’s now, a year and a half later, in default and according to S&P Capital IQ LCD was quoted at 40/50 cents on the dollar.

When credit was easy and nearly free, any story was a good story. Analysts fawned over them, and it was practically impossible to run out of money because new cheap money would always roll in. But now that era is over. The credit cycle is ending. And investors are getting antsy.

Gundlach has billions of reasons to fret about junk bonds and leveraged loans. But when they swoon, something else happens after some delay: stocks follow.

Junk bonds are the canary in the coal mine for stocks. When credit tightens, the dynamics change for much of corporate America. Financial engineering gets more expensive and fizzles. M&A gets more difficult to pull off. Bond-funded dividends and share buybacks get cut or come to a halt. Defaults wipe out shareholders. Suddenly, risk shows up on the scene. And eventually, stocks start chasing junk bonds lower.

“If this isn’t the peak, we’re probably close,” Green Street Advisors mused about commercial real estate prices, as ratings agencies Fitch and Moody’s, which rate mortgage bonds, begin to issue warnings. Read… Industry Holds Breath for Craziest-Ever Commercial Property Boom to Implode

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

you buy junk, you own junk. You knew it would end badly, but you played the ‘musical chairs’ game and now want the FED to come to you rescue.

No more bailouts for speculators, the days of socialism for them is over and you too.

Made a fortune…great, on the backs of all other Americans who didn’t get one of your silver spoon opportunities which you squandered.

Translation: Gundlach got sucked into the reach for yield.

I don’t feel sorry for Grundlach. The chase for yield in this historically low rate environment results in risky speculation. I do feel sorry for those retirees who were convinced by ‘advisors’ to put a hefty portion of their money in junk bond funds for more income.

Here in Canada Mr.Poloz just announced “negative interest rates” and for majority of sheeple crazed in long lines for Christmas shopping this went virtually unnoticed.

With all the financial engineering most companies engage in, they have turned themselves into hedge funds. They make “profits” from stock manipulation, mergers, and assorted other accounting tricks. There is very little actual production going on in corporate America. You can’t make bond payments with accounting tricks.

I recall Japanese companies having a practice called “tobashi” (to make fly away) by engaging in all sorts of manipulations to boost short term result.

It’s interesting to note two things:

1. The chicken has come home to roost. The biggest banks providing “tobashi” services were mostly American.

2. We may see companies/people literally flying soon.

hmmmm. the distressed index once traded at 100? hmmmm.

shades of 2006.

but this has been known. it just went on for too long.

on the one hand, there may not be enough cash out there to soak up all the opportunities, on the other hand, maybe we’ll muddle through.

can’t say i see rates going up much, unless rocks and hard places are close together.

seems to me the fed is counting on banks, which can’t, and investors, who might not.

I hope the Fed will raise 50 basis points just to give this guy a shellacking. Next he’ll argue that the Fed has a fiduciary duty to his investors.

Ok we all agree to send this guy a bouquet with a note ‘that’s why they call it junk’

But, but, there ARE reasons for the FED to think about not raising- and they are not the effect on junk bonds.

All America’s competitors are now engaged in a currency war. Two, China and Japan actually announced their devaluations- although Japan’s had to be done with market actions over a period of time.

(The audacity of Japan doing this still amazes/ puzzles me. I thought you had to sneak cookies, with stealth,even if everyone knew. )

China just did in one day, twice I believe. ( Can you do that once you’re an official SDR?)

You can see Japan’s result in monthly payments on a Mazda, but no doubt also in Honda, Toyo. Nissan.

As for the home of Benz, BMW, Porsche- VW, Audi. They would be screwed if they were in the old D-Mark, and some heat would be off the $US.

But they’re not. The most competitive economy in the world has a weak currency!

Frankly once you back out trucks I don’t think too much of the USA BIg Three’s prospects anyway, they may be lucky they don’t depend on exports from the US, but the sky high $US sure makes it hard to compete with imports who are devaluing their currencies- by offering NEGATIVE rates.

Oh ya I forgot Canada, in whose currency I parked my feeble fortune just

over a year ago when I sold my house. The Royal Bank asked me if I wanted a $US account. From 90 ish to 73.

Broccoli- 5 bucks a pound yesterday.

And our top guy just said yesterday we might be going negative.

o while it many be virtuous for the US to embrace fiscal rectitude, everyone else is whoring around.

That’s a whole lot of

And with the example of a humble broccoli, you are able to debunk Nobel prize winning economic theories. As a result of the prise increase due to currency depreciation, local producers should get a shot in the arm, and produce more broccoli. But the local producers of broccoli were wiped out in the previous price war, so now only produce potatoes, and have no idea how to produce and market broccoli.

Applies to anything else.

I think Canada is pretty much stuck with imports during winter- but if nat gas is going to be dirt cheap maybe….

i’m wondering when we get another moment like this comedy gold.

https://www.youtube.com/watch?v=SWksEJQEYVU

BTW what’s even more shocking he’s still on the air and still taken seriously.

…”“We are looking at real carnage in the junk bond market,” Jeffrey Gundlach”…

Translation, “Help, I want out now.”

Screw you Jeffrey!

My limited understanding of the bond market is that companies, whose banks for whatever reason won’t lend them any more money, turn to investors instead and offer a higher return in exchange for investor cash.

Banks have different lending criteria which despite the criticism levelled at banks for being too lax in some cases is generally tighter than investor ‘faith’ so if the amount of indebtness that the companies want to take on isn’t of interest to banks (professional money lenders) – presumably the banks have more insight into the companies ability to service more debt – then why should anyone else take a chance?

Most large companies are small companies living on hot air!

The asinine ZIRP and QE have created the ideal environment for Ponzi schemes. Wait until they begin to come to light as they did during the 1989-90 junk crash only far bigger in magnitude that will make Mike Milken and Bernie Madoff look like small potatoes.

Wolf – please find a copy of this song and listen to it before you write your next piece.

“Look for the Silver Lining”

Look for the silver lining, whenever a cloud appears in the blue

Remember somewhere the sun is shining,

And so the right thing to do is make it shine for you.

A heart full of joy and gladness will always banish sadness and strife.

So always look for the silver lining and try to find the sunny side of life.

http://finance.yahoo.com/echarts?s=DLTNX#{“showArea”:false,”showLine”:false,”showCandle”:true,”lineType”:”candle”,”range”:”5y”,”allowChartStacking”:true}

5 year chart above of DLTNX, his flagship fund – not good since mid-2013

On the other hand he has way outperformed the bond benchmarks so he is not doing badly.

http://www.morningstar.com/funds/XNAS/DBLTX/quote.html

He is also dead right about the FED. The Fed should have raised rates 4/5 years ago, and they did not. So they are raising now as our economy and the world economy are weakening. Gundlach is saying that the FED is stupid. No $hit, Sherlock.