Bad breath of zero-interest-rate era wafts over real economy.

To the chagrin of the government, China has one export that is booming: capital flight.

Fearing further devaluations of the yuan, a terribly inconvenient crackdown on corruption, political purges, and other mayhem, wealthy Chinese are trying to get part of their money out of harm’s way. Capital outflows tripled to an estimated $113 billion in November from October.

To prop up the yuan in face of this sort of capital flight, the People’s Bank of China has been selling foreign currency, including US Treasuries. As a consequence, its foreign exchange reserves plunged by $87 billion in November to $3.396 trillion, the lowest since February 2013. The export of capital is a booming business in China.

Actual exports weren’t so lucky, according to China’s General Administration of Customs. In November, they dropped 6.8% year-over-year (3.7% in yuan terms), after a 6.9% swoon in October. They’re down for a fifth month in a row. They’re a sign of crummy global demand for Chinese goods.

This has been the story of the Caixin Manufacturing PMI, which tracks manufacturing activity in China via a survey of purchasing managers. It has been mired in contraction mode for nine months in a row.

China is no longer the low-cost producer with an undervalued currency. The yuan is essentially pegged to the US dollar – now ironically called the “strong dollar” – and has been rising in near lockstep with it, except for the smallish devaluations. So China faces weak global demand and a currency that is strong in relationship to the currencies of many of its customers.

Imports fell 8.7% year-over-year (5.6% in yuan terms), having now fallen every month over the past year, a sign of collapsed commodity prices and lukewarm demand in China.

This swoon in exports has hit the container shipping industry at the worst possible moment: Infused with central-bank-managed optimism and flush with nearly free money from global monetary policies, executives of shipping companies have gone on an expansion binge for the past seven years. Drewry estimates that capacity of the world fleet will balloon by another 8% this year, while demand might edge up a measly 1%, if that – the lowest increase since 2009.

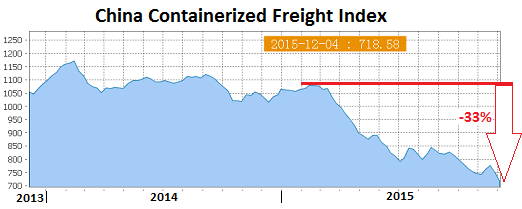

So shipping rates have collapsed: The China Containerized Freight Index (CCFI) for last week plunged 4.3% to 718.58, the worst level ever.

The weekly index, operated by the Shanghai Shipping Exchange, tracks contractual and spot-market rates for shipping containers from major ports in China to 14 regions around the world. Unlike a lot of Chinese government data, this index is raw – and now relentlessly ugly.

It has plunged 33% from the already weak levels in February and 28% since its inception in 1998 when it was set at 1,000. This is what the collapse in shipping rates looks like:

Containerized freight rates rose only in two of the 14 shipping routes last week (Southeast Asia and Australia/New Zealand). Rates to the 12 remaining routes all fell, including 8.6% to Northern Europe, 1.9% to the US West Coast, 3.6% to the US East Coast. Rates to the Mediterranean plunged 14.5%.

And so plays out the central-bank strategy of inflating asset prices by printing money and repressing interest rates to zero or below. The result has been seven years of cheap debt, plowed into all kinds of assets, such as new ships for container carriers, drilling in the US shale oil revolution, or building cement plants and ghost cities in China.

By issuing this debt, companies and governmental entities have burdened their balance sheets to precarious levels. But this debt is an asset for banks and investors (such as bond and loan mutual funds, pension funds, etc.), who, believing in central bank hype, have taken it on, shouldering immense risks in return for a ludicrously low yield.

For a while, these activities of expanding the global shipping fleet – much like building cement factories, copper mines, and the like – inflated GDP. It was part of the central-bank designed “recovery” from the Financial Crisis. But then this capacity and supply turned into overcapacity and oversupply. And rates crashed. That’s when the bad breath of the zero-interest-rate environment wafts over the real economy: plummeting revenues and margins, layoffs, idling or shutdowns of capacity, defaults, bankruptcies, consolidation, and general capital destruction.

In the US, a similar scenario is playing out: as bad as the overall trade deficit is, the trade deficit in goods (without services) is much worse, and even then, the oil trade covers up just how terrible the underlying trade of non-petroleum goods really is, how far and how fast non-petroleum exports have plunged, and how much US manufacturing is getting whacked. Read… US Exports & Manufacturing Debacle Covered up by Oil

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Binaka for Poloz please! The bad breath of negativity…

http://www.zerohedge.com/news/2015-12-08/canada-just-hinted-negative-interest-rates-are-coming

…urp, excuse me please.

My son builds computers and he tells me the price of components is rising sharply. Most of the parts come from Asia. The slowdown in imports seems to be showing up in this market sector.

Why is it the “worst level Ever”? Only if you are in the shipping business. For the rest of the world, the cost of doing international business just got cheaper. That’s not a bad thing.

It was the worst winter we ever had. Well, not if you go skiing. Then “worst” means something else.