Magic trick turns into toxic mix.

Stocks have been on a tear to nowhere this year. Now investors are praying for a Santa rally to pull them out of the mire. They’re counting on desperate amounts of share buybacks that companies fund by loading up on debt. But the magic trick that had performed miracles over the past few years is backfiring.

And there’s a reason.

IBM has blown $125 billion on buybacks since 2005, more than the $111 billion it invested in capital expenditures and R&D. It’s staggering under its debt, while revenues have been declining for 14 quarters in a row. It cut its workforce by 55,000 people since 2012. And its stock is down 38% since March 2013.

Big-pharma icon Pfizer plowed $139 billion into buybacks and dividends in the past decade, compared to $82 billion in R&D and $18 billion in capital spending. 3M spent $48 billion on buybacks and dividends, and $30 billion on R&D and capital expenditures. They’re all doing it.

“Activist investors” – hedge funds – have been clamoring for it. An investigative report by Reuters, titled The Cannibalized Company, lined some of them up:

In March, General Motors Co acceded to a $5 billion share buyback to satisfy investor Harry Wilson. He had threatened a proxy fight if the auto maker didn’t distribute some of the $25 billion cash hoard it had built up after emerging from bankruptcy just a few years earlier.

DuPont early this year announced a $4 billion buyback program – on top of a $5 billion program announced a year earlier – to beat back activist investor Nelson Peltz’s Trian Fund Management, which was seeking four board seats to get its way.

In March, Qualcomm Inc., under pressure from hedge fund Jana Partners, agreed to boost its program to purchase $10 billion of its shares over the next 12 months; the company already had an existing $7.8 billion buyback program and a commitment to return three quarters of its free cash flow to shareholders.

And in July, Qualcomm announced 5,000 layoffs. It’s hard to innovate when you’re trying to please a hedge fund.

CEOs with a long-term outlook and a focus on innovation and investment, rather than financial engineering, come under intense pressure.

“None of it is optional; if you ignore them, you go away,” Russ Daniels, a tech executive with 15 years at Apple and 13 years at HP, told Reuters. “It’s all just resource allocation,” he said. “The situation right now is there are a lot of investors who believe that they can make a better decision about how to apply that resource than the management of the business can.”

Nearly 60% of the 3,297 publicly traded non-financial US companies Reuters analyzed have engaged in share buybacks since 2010. Last year, the money spent on buybacks and dividends exceeded net income for the first time in a non-recession period.

This year, for the 613 companies that have reported earnings for fiscal 2015, share buybacks hit a record $520 billion. They also paid $365 billion in dividends, for a total of $885 billion, against their combined net income of $847 billion.

Buybacks and dividends amount to 113% of capital spending among companies that have repurchased shares since 2010, up from 60% in 2000 and from 38% in 1990. Corporate investment is normally a big driver in a recovery. Not this time! Hence the lousy recovery.

Financial engineering takes precedence over actual engineering in the minds of CEOs and CFOs. A company buying its own shares creates additional demand for those shares. It’s supposed to drive up the share price. The hoopla surrounding buyback announcements drives up prices too. Buybacks also reduce the number of outstanding shares, thus increase the earnings per share, even when net income is declining.

“Serving customers, creating innovative new products, employing workers, taking care of the environment … are NOT the objectives of firms,” sais Itzhak Ben-David, a finance professor of Ohio State University, a buyback proponent, according to Reuters. “These are components in the process that have the goal of maximizing shareholders’ value.”

But when companies load up on debt to fund buybacks while slashing investment in productive activities and innovation, it has consequences for revenues down the road. And now that magic trick to increase shareholder value has become a toxic mix. Shares of buyback queens are getting hammered.

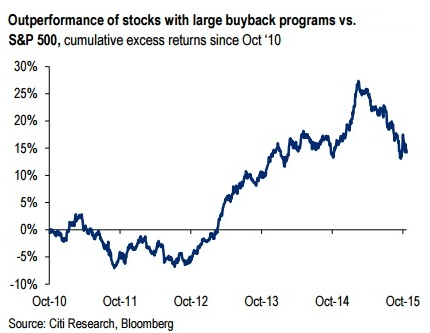

Citigroup credit analysts looked into the extent to which this is happening – and why. Christine Hughes, Chief Investment Strategist at OtterWood Capital, summarized the Citi report this way: “This dynamic of borrowing from bondholders to pay shareholders may be coming to an end….”

Their chart (via OtterWood Capital) shows that about half of the cumulative outperformance of these buyback queens from 2012 through 2014 has been frittered away this year, as their shares, IBM-like, have swooned:

The Citi analysts, via Bloomberg:

The three-fold increase in share buybacks in the past five years has been the key driver of corporate re-leveraging. In large part, buybacks have been the result of strong incentives provided to corporate managers by activists in particular and equity investors in general…

Companies that spent more on shareholder handouts and less on investments have tended to get higher price/earnings ratios in the market. But there are signs that this may be changing. Recent conversations that we’ve had with equity [portfolio managers] suggest that they have become far more focused on revenue growth, and are placing far less of a premium on any financially engineered EPS growth.

The fact that a basket of stocks that [has] been reducing shares outstanding is meaningfully underperforming the S&P 500 on a beta-adjusted basis suggests that this view may not be that of just the investors we talk to, but far more broad-based.

The performance of the S&P 500 has been crummy this year, in part because it has been dragged down by the buyback queens. Investors are smelling a rat. Financial engineering performs miracles, even with duds like IBM and HP – until it doesn’t.

Results of all this financial engineering? Revenues of the S&P 500 companies are falling for the fourth quarter in a row – the worst such spell since the Financial Crisis. And with the failure of financial engineering, one of the most powerful props collapses under the already wobbly but sky-high stock market.

Junk bonds, a bellwether for stocks, have been warning for a while. Investors are sitting “on large amounts of potential and realized losses,” Moody’s said. Read… Bloodletting 8 Trading Days in a Row: Junk Bonds Go to Heck

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Proving what is good for Wallstreet is not in the best interest of business.

What’s good for Wall Street is generally not in the best interest of anyone other than Wall Street.

Stock buybacks and ‘financial engineering’ are, of course, a result of the Fed’s policy of free money. This new norm is insane! Capital must have cost, and if it doesn’t, the Free Market becomes a rigged market.

Wolf Street readers may want to check out Pam and Russ Martens’ ‘One Chart That Should Make Americans Wake Up’ at:

http://www.wallstreetonparade.com

Financial engineering has been going on a lot longer then ZIRP. The introduction of junk bonds followed by derivatives is the origin. It was also aided by the fall in price of computing power. The ability to model minute by minute with no regulation gave rise to the activity. Now the financial markets are all a bunch of computers competing with each other, and management liking it, because it gives them cover.

Petunia, I was reading not too long ago about the likes of Jay Gould, and others from the era of the railroad robber barons. Selling bonds to get money to pay dividends was one of the old tricks, to juice the stock prices. Sound familiar? Of course! So the ‘bondzi’ scheme is really quite old.

Reading about what went on in the late 1800’s, and how well oiled it was then, well, there is nothing new under the sun. The activism back then matches the current operators.

Thankfully there are people like Wolf, doing a great job of showing what’s really going on. A number one site to get real insight.

The CEOs and boards that have allowed companies to pile on debt to compensate them, thru stock buybacks, should all be arrested. It is simple theft. The boards have the responsibility of safeguarding the assets of the companies and they haven’t been doing their jobs. Everybody in the C-suite has been living large from the productivity of the employees who really produce. We have the wrong people in jails.

You go girl!

Everything you have said here is right on. Change in the opposite direction is far too slow.

I don’t know what makes you so bitter but your comment is totally off.

You are accusing wrong people, they only ask for money, somebody else is giving money. Understand.

OK, if you go to the bank and ask for 1 million and bank manager approves that even though you are never or maybe pay it back; Who is at fault and who should be in jail?

If these buybacks did not happen, what do you think what would be state of stock market and ultimately entire economic outlook?

Buybacks are one way to show investors that earnings per share didn’t deteriorate and keep faith in investing and supporting companies who employ huge number of people, who again buy spending money support others.

Velocity of money. I think there was post on this blog, go back and check.

IBM is in the computer business, not the velocity of money business. A company using finance to support its operations is acceptable. A company replacing its operations with financial gimmicks is defrauding its investors. Even if they are really good at using gimmicks, it is EXCEPTIONALLY misleading, and therefore, fraudulent.

Message approved. Most people invest on IBM based on the understanding that it’s a computer company, not a hedge fund. And especially a hedge fund that will surely blow up one day.

Well most people invest in stock market thinking that it is what name says stock MARKET, how about stock CASINO. So if you don’t understand this, stay away or loan your money to money sharks (investment advisors) and sleep dreaming that they will take care of your future and retirement. Those times are gone.

Remember: “Never invest more than you can afford to lose”.

This proverb stood test of time over and over again.

And when this collapses too (remember2008) the CEOs will say “well everyone was doing it”. Remember the quote “when the music plays we all have to keep dancing.” from the financial crisis. These CEOs should be FIRED. That’s why they get the big bucks- to ruin their companies? But increased share price increases their bonus as well and they still get huge pensions etc.

Petunia you are 100% correct. What has happened to America?

They are ruining the country I was proud of.

In search of short term profit and dividends Wall Street has led US companies down a blind alley.

They have frowned on long term investment and R&D as these dent short term profits and dividends.

They prefer layoffs, asset stripping and mergers and acquisitions to boost short term profit and dividends.

Companies that once issued stock to grow, now take on debt to buy back their shares that increase the share price and dividends for the other share holders.

Increasing stock was always much better than debt for investment. With stock you pay dividends depending on how well the company is doing and it doesn’t drain the company in the bad times. Debt repayments stay the same good times and bad.

Wall Street has strip mined the real companies of the US economy and left them in no position to grow without long term investment and R&D.

The UK was the last super power and China will be the next.

Adios America.

To see how bad it is read Michael Hudson’s book “Killing the Host”.

Another common sense and values based comment by Petunia. Right on. Dishonest company practices and company officers are what they are. They steal from us all when they debase our economic health.

I think it’s a theme. I just finished re-reading Bethany McLean’s _The Smartest Guys in the Room_:

”But with trading now the dominant motif at Enron, the company no longer felt it was necessary to have a homegrown supply of natural gas. As an EOG [Enron Oil & Gas] executive summed it up: “They didn’t feel they needed the gas wells and the people. If they wanted to go long gas, they could just do it on the trading floor.” As for the profits Enron had reaped from those stock sales, well, Skilling felt pretty sure he wouldn’t be needing those anymore either, not after he finished remaking the company. What he especially disliked about EOG was that its profits were erratic and volatile, which made it that much more difficult to show Wall Street the kind of smoothly rising earnings that would move the stock.”

Finance and legal people must find threat and risk in those physical processes and material constraints that exist in manufacturing or production. Much better to have clearly defined (and abstractly defined) deals and assets that lock value into the balance sheet and P&L.

John Kenneth Galbraith described a bifurcated industrial system in _The New Industrial State_, divided between the market sector where companies’ results were determined by day-to-day business conditions, and the planning sector where big companies with immense capitalization planned and executed giant projects in their core businesses (e.g. the many-year process of bringing a new vehicle, a mini-van, say, to market.) I think you can see the modern FIRE sector emerging from these giants as they ditched all the lines that got in the way, and made their planning difficult.

Just 6 stocks are keeping the S&P 500 off the floor and account for over 9% of the equity cap of the index, with a valuation over 20X EBITDA !

Amazon

Alphabet (Google)

Microsoft

Facebook

General Electric

Apple

All of them are overvalued by 100% compared to the rest of the market!

What could go wrong? Right?

Financial engineering has become part of US DNA. Note that neither Germany or Japan had Business schools or MBA’s. These days with competition for foreign students intense, every one has to offer everything, but here is no demand for the MBA from business. They prefer someone who knows not business in general, but someone who knows THEIR business. In both countries the CEO of an auto maker is more likely to have an engineering background than B- school or, heaven help us, law. The new guy at VW, who has some work to do, trained as a tool maker! Wonder how many Harvard guys he met there?

If only the stuff about to hit the fan was nice soft poop.

Wolfstreet.com is the only site where we learn as much from the commenters as from the articles, especially from Petunia.