Stocks, bonds, real estate, classic cars, art, credits at Ashley Madison, whatever… nearly everything except commodities has soared over the past six years, perhaps not in lockstep exactly, with one moving ahead while others were still declining, but by last year, just about every asset class had soared to all-time record highs.

Asset price inflation, the express goal of the monetary policies set by the Fed and other central banks, worked for a long time. If you got in early, it was one heck of a ride up. If you had a billion bucks in early 2009, you’re now sitting on multiple billions, without having had to think all that much.

It just about didn’t matter what you put your money into, as long as it wasn’t cash.

It didn’t matter what the economy in the US or anywhere else did. It didn’t matter that asset prices no longer made sense. New metrics were bandied about to justify these prices, and it worked, and everyone with money invested in the scheme was in heaven.

But what now?

If everything went up together, everything might come down together, perhaps not exactly in lockstep, but one asset class first, then another. And the question many people ask is this: where the heck are you then supposed to put your money?

The answer is never simple. There are issues with every “solution.” No one knows for sure what’s going to happen next. But here are some thoughts and some numbers….

By Brian Hunt and Ben Morris, editors of DailyWealth Trader, an excerpt from their essay, The Bull Market in Cash Is On:

In late March, we called it “one of the best assets to hold in uncertain markets” in our DailyWealth Trader service. The title has since proven its merit.

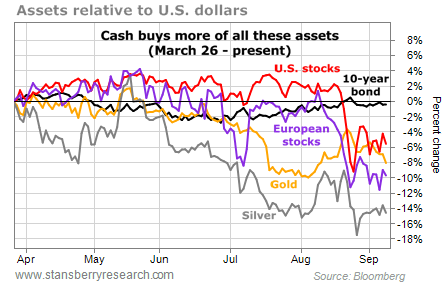

The asset’s value has climbed 6% relative to U.S. stocks and 10% relative to European stocks. Its value has risen 8% relative to gold and 14% relative to silver. Its value even climbed close to 1% compared with 10-year U.S. government bonds, which are considered some of the safest assets in the world.

How has this asset performed in U.S. dollars? Well… it is the U.S. dollar. The asset is cash.

Stocks have fallen hard over the last month. If you had most of your assets in stocks, it was probably hard to stomach. Gold and silver have declined, too, but more gradually. At the same time, the value of your cash has climbed…

Think about it this way: When an asset falls, it isn’t just a bear market in that asset. It’s also a bull market in cash. It’s an increase in the amount of assets you can afford.

If stocks drop 10%, maybe you can buy 100 extra shares of one of the world’s best companies. And you can buy those shares at a better price. If silver drops 20%, maybe you can buy 100 extra one-ounce coins.

This is an important idea to keep in mind today. Global financial markets have broken their primary trends… and are now struggling. And we’re likely in for more volatility in the weeks and months ahead. So holding more cash might let you sleep better at night.

It allows you to weather shocks to financial markets… and to pick up good deals when they appear.

In our March 26 DailyWealth Trader issue, we explained that lots of folks object to this idea:

Many people don’t like to keep large portions of their wealth in cash because they feel like they always have to be “doing something.” They hate sitting still. They see a large cash balance in their account and start looking for a stock to buy… a commodity to buy… anything to buy. It burns a hole in their pocket.

But sophisticated investors have a more useful way of viewing cash. We see cash as “returns in waiting.”

When there aren’t lots of great, low-risk investment ideas out there, the best idea may be to invest in cash. Keep in mind, we’re not saying you should sell everything you own. For lots of folks, holding 10%-20% of their investable assets in cash is a good amount most of the time. During less certain markets, even 30%-40% could be appropriate.

Hold however much cash makes you comfortable. If you’re extremely nervous about stocks, hold more cash. Nerves lead to bad trading decisions. So you’ll be better off. If you’re confident that stocks are headed higher, hold less cash. But still hold some.

We always encourage readers to use intelligent asset allocation as part of an inclusive “catastrophe-prevention plan.” Holding some of your assets in stocks, bonds, precious metals, and real estate will lead to less volatility in your overall investment portfolio.

And cash is one of the most valuable assets you can own. While other assets are dropping, the bull market in cash is on. By Brian Hunt and Ben Morris, editors, DailyWealth Trader

This Chart Shows: Investors Are Losing Faith in the Fed. Read… A Change in Market Dynamics I Find Particularly Troubling

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I absolutely agree that waiting is the hard part. You might have to wait years for the fat pitch. In my private investments I’ve often had to wait several years before seeing serious money. Guys who bailed and sold their shares because things weren’t moving fast enough regret it now.

I’m mostly in cash, bonds and PM now. Almost all of my stocks hit their trailing stops over the past 11 months. Second hardest after being patient is letting go when the price is moving down, hence the trailing stops.

PM are so hated (even more than cash) it’s probably the best contrarian buy out there. It’s been left for dead.

I keep telling people market timing isn’t hard if you only buy when the price is right and sell if you hit your trailing stops. Even before my stops were hit my cash position was growing because I had few places to put new money.

Wolf has done a great job over the years showing how stocks are like a hollow chocolate Easter bunny – earnings up on flat revenues due to stock buybacks and other engineering. Maybe I missed part of the final move up but I am for sure going to miss the ride back down and then that cash is gonna be put to work. After all, rule #1 is don’t lose money. If you lose half your money you need a 100% gain to get even.

what does PM mean in previous post?

Precious Metals (gold, silver, etc.)

Rule 1: The denominator.

I can make anything grow (or fall) if I control the denominator. While folks can piss and moan about the dollar, gold, oil, real estate, bonds, stocks, or whatever, they all have a denominator. A dirty secret of the current market complex is that all fiats are measured against EACH OTHER. It is an express elevator to hell. At the same time, for political reasons, I don’t suspect gold will be the new trade settlement standard in my lifetime.

DISCLOSURE: I own a pitifully small amount of gold and silver as insurance. More to the point, I also prospect because I like the gym fees and the taxes. I like gold. But I am also a (political) realist to the best of my ability/awareness.

If you are bailing into cash, you are trying to AVOID the denominator problem, or at minimum, become the denominator. So get that in your thinking and stop watching the global market EKG. Your emotions will cheat you.

Rule 2: There is no free lunch.

The most basic tenant of accounting is assets equal liabilities plus equity. Let’s go full simpleton and say assets equal liabilities. Let’s say you own an old truck, a case of ammo, a chicken, or a bond. Those things are assets, but they don’t need a LIABILITY to exist – except the bond. It is all “God’s money” except the debt because they have some real life value. Debts aren’t like that, such as bonds, which are only valuable as long as someone carries the obligation, but they pay in the denominator. Or, said another way, dollars are not self defense, transportation, or an omelet, although in normal times these can be bought.

NOT the same thing. Roger that? This is VERY, VERY important to understand if you aren’t “rich”.

That said, cash is a tool to move your “liabilities” from some pencil f**ker to the treasury of a nation. I say this, and to be clear, a deposit at the bank is an ASSET to you the owner of the cash and a LIABILITY to the bank. It is a mini-bond. This is just like a loan to you for a house/car is an ASSET to the bank and a LIABILITY to you the borrower. A deposit is a loan to the bank (at zero interest these days).

By holding “hard cash” one is just going up the food chain is all. Technically, in the US, a Federal Reserve Note (cash) is the liability of the Federal Reserve (not your local S&L)), which is a private central bank. If you wanted cash beholden to the US Treasury, you need to sock your money away in COINS.

As an aside, if the Fed note ever went tits up, the likelihood they would void all coins is pretty low, given the small volume in circulation. This is a good trade for small fry like myself who can keep a can or two of coins laying around, but not so much for a multi-millionaire.

My point is there is a difference between the “cash” choices – it just isn’t obvious in the current situation when they all seem the same.

Rule 3: it is right until it is wrong.

Another way to side step the banking system in the US is to open a Treasury Direct account (it takes weeks – single owner – no trusts). This gets icky, because you are in a whore house at this point and figuring you are going to be holding the only bible when Jesus shows up (i.e. timing your exit if things get all apocalyptic). Chew on that.

However, at the same time, you are not in the BANKING system (i.e. no dependence on the FDIC) and instead have elevated your assets (their liabilities) from the Fed to the Treasury and cut out brokers (who can BK and stick you with the bill).

Quick Review.

(Zero) No debt is the most important objective. One paid for car/truck, basic protection/ammo, rice/beans, and stuff like that. Get there. Screw the other goals.

(One) Cash is king. Nice, crisp, new bills. Under your mattress. Or in your safe deposit box. Don’t discount the fact that it is possible old or out of date bills will be discarded. The fancy new 100s are the best bet for now as they were a response to NORK counter fitting (where it was implied they were given original plates).

(Two) Don’t keep more cash than you (1) need for a few months or so of living expenses/rent or (2) can’t take on a plane. If you need a million in cash, you are doing it wrong. YMMV.

(Three) If you have hard surplus at this point, look at Treasury Direct as a short term strategy. Move your money in and roll it on a 30 day cycle. That gives you 30 days to walk away. No brokers, no fees.

Stay too long, and you have a new problem (come to JC meeting), but that is chess I suppose. Personally, if the dollar shits the bed, I got bigger problems to worry about than my Treasury Direct account (if I don’t have debt).

Stay safe and don’t think you are going to “win” doing (or listening) to what EVERYONE ELSE is doing. The ONLY way you come out ahead is doing what everyone else isn’t doing … and capitalizing on an opportunity.

Regards,

Cooter

P.S. My gut tells me debtor prisons will be coming back. Think you are retired and comfortable? Ring-Ring: Happy birth day Dad, I am in debtor prison.

Why? Because insider bankers are more important than everyone else.

P.S.S. Sorry if I went overboard for the crowd here. But you should all know it is time to buckle up and the ride is not going to be a fun one.

No apologize needed Crazy Cooter!! That was one of the best comments I have had the pleasure of reading in a long time. This is what makes “Wolfstreet” a great site, brilliant minds like yourself sharing their life lessons and opinions. Good on ya mate!

CC, next time make rule number one, get coffee before scrolling down.

Cheers.

While you are paying off debt the investment world is creating it. They are all piling it on, have been doing it for decades and will continue to do it, because there is no risk. If they can’t pay they don’t, and you will. In the end, they will get bailed out and get to keep the assets too. That’s what happened with the banks. The govt gave them the money for the defaulted mortgages and the houses too. It makes me mad when I see “investors” that think the system is going to be in anyway fair when the SHTF. It won’t. The same people will be saved and the same people will be sacrificed.

Not at all Cooter. I’m sure none of us here take the time to comment here to toot our own horns. Our incomes are all over the map, but the one thing we all share is a propensity to be brutally honest when facing the facts. I used to have bad days on the road and mutter to myself that I should have finished college. Not so much these days. Especially when I read comments from folks like Red Flag who has the degree(s) and are in worse shape than I am. Being an old guy, I always felt that at most I was participating in a group discussion with like minded friends or a dialogue, and rarely soliloquy. It is driven home to me of late just how many people read these scribblings who we rarely or never hear from, but they are out there and if we can wake up a few who will wake up a few more until the whole thing becomes a geometric progression, simply because we give up an hour of sleep and type up a comment. We speak to the individual mind; I borrow a line from Marcus Aurelius: we do not herd and feed with the rest. Also from Marcus: no matter what anyone else does or says, I must be emerald and keep my color.

EXCELSIOR, Julian

Well said.

Wake people up little by little and dilute the propaganda bath we are all subjected to.

I warmed to Marcus Aurelius when I read his confession that at times he – emperor of so much of the world – felt like sticking his head under the covers in the morning, it was all too awful to face…..

Neither he nor we can really do that, best to go forward clear-sighted.

Hell, Cooter, that wasn’t a comment that was a column!! And you have described the situation I desire when I look in my crystal ball. Well said.

Thank you Cooter. Well written.

Agreed Cooter amusing. You can’t eat cash (or bonds, or gold certificates that supposedly represent a physical deposit somewhere). They might help start a fire in extreme duress though. So what’s a regular guy to do? My hedging strategy is owning farmland in another country. My retirement savings includes the goodwill of friends and neighbors, the welcoming arms of family, and my good general health. My bank account is knowledge of cooking, canning, preserving, growing, and harvesting food. I’ll take them over a carefully allocated 401K plan any day.

Physical cash should be stashed somewhere though…even a simple power failure takes out ATMs….

The article fails to mention that your cash in the bank is being looted every month by inflation. Inflation which is much higher than the official figures tell us. I don’t care how many Euro stocks or silver I can buy today compared to April. The real question is how many groceries can I put in my bag compared to April, and what about other necessities like rent and health insurance etc. So the short answer is, there is no good place to put your money right now. And that’s no accident, folks.

But wait… inflation loots everything denominated in dollars, not just cash in bank.

Thank you CC – insightful comments.

I learned something: Treasury Direct Account

Good idea.

I do something that may sound crazy: I pre-pay my taxes – real estate, Federal and State. If that money was in a bank account, and the banks imposed a haircut, I doubt that my tax credits would be tampered with. If you make money or own real estate, you have to pay taxes. Pre-payment eliminates that future obligation.

I do this for corporate income taxes too. With zero interest rates, you are giving up nothing. I never make myself illiquid and view the pre-payment as another method to hold surplus in a secure account.