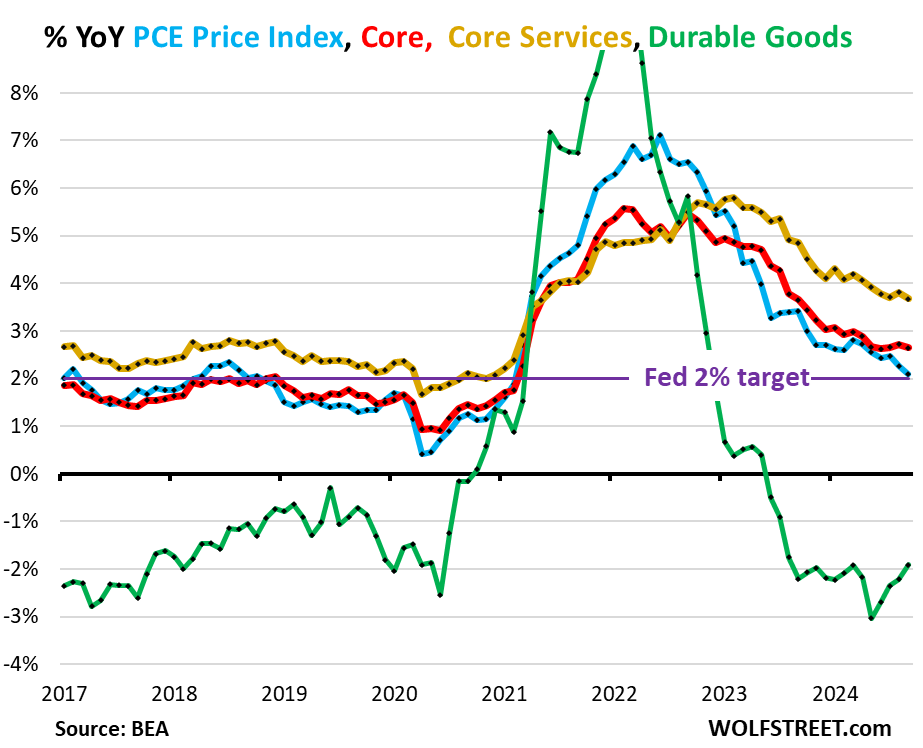

The YoY “core” PCE price index, the Fed’s yardstick for its 2% target, rose 2.65%, with no progress over the past 5 months. But energy prices plunged.

By Wolf Richter for WOLF STREET.

The “core” PCE price index, the Fed’s primary yardstick for its 2% inflation target, rose by 3.1% annualized in September from August (not annualized, +0.254%), the biggest month-to-month increase since April. And August was revised higher (blue in the chart below). This month-to-month acceleration was driven by:

- Core services accelerated to 3.7% annualized (+0.30% not annualized), the biggest increase since April.

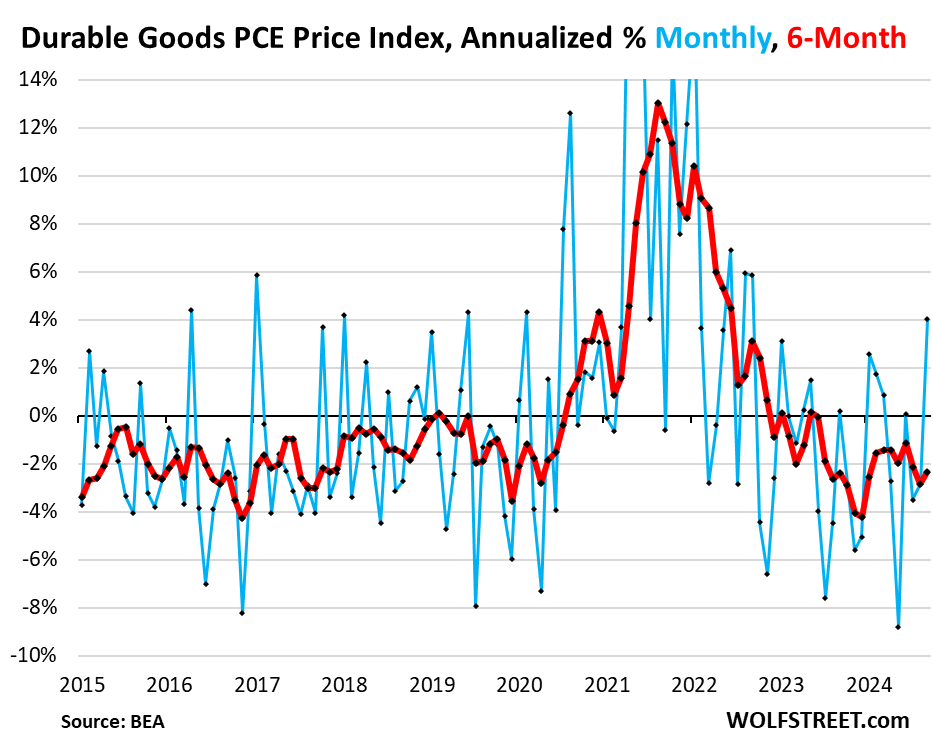

- Durable goods flipped from a series of month-to-month declines (negative readings, deflation) to a positive +4.0% annualized, the biggest month-to-month jump in prices since September 2022.

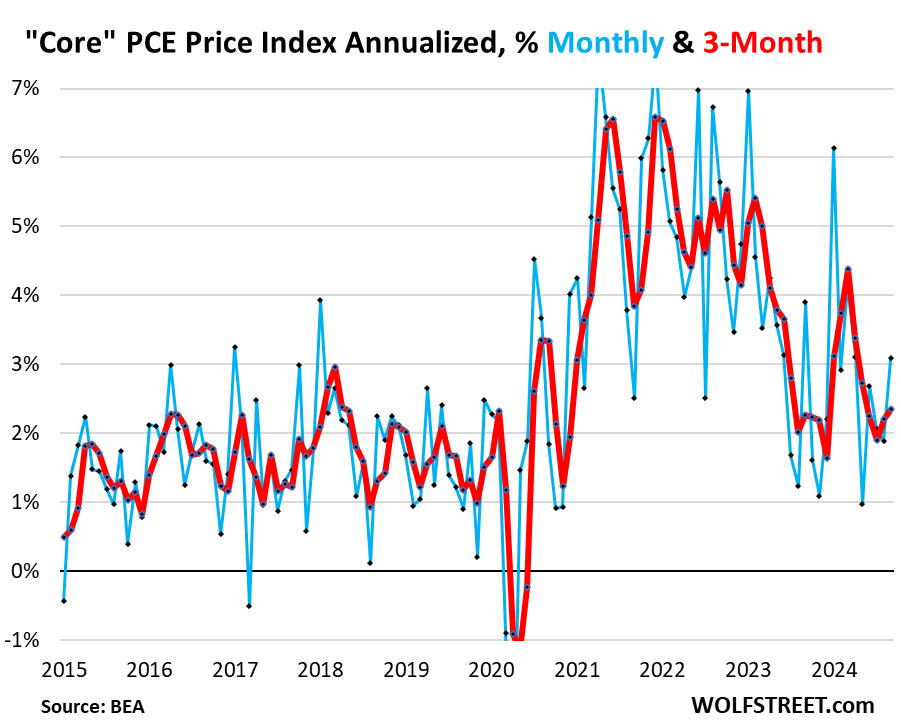

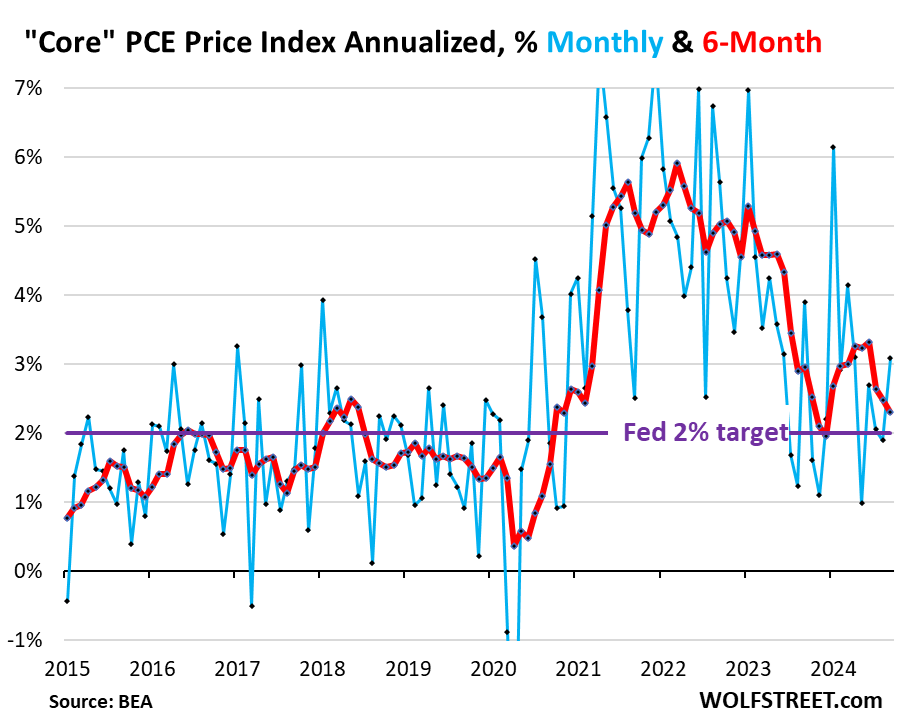

We’re going to look at it on a month-to-month basis (blue), and on a 3-month, 6-month, and 12-month basis (all of them in red) because the developments in recent months get washed out in the 6-month and 12-month indices.

The 3-month core PCE price index accelerated to 2.35% annualized, the second acceleration in a row, and above where it had been in August 2023, with a big spike in the middle (red).

This “core” index attempts to show underlying inflation by excluding the components of food and energy as they can jump and drop with commodity prices. We’ll get to the overall index, which includes food and energy, in a moment.

The 6-month core PCE price index decelerated to 2.3% annualized (red). It remains higher than it had been at the end of last year:

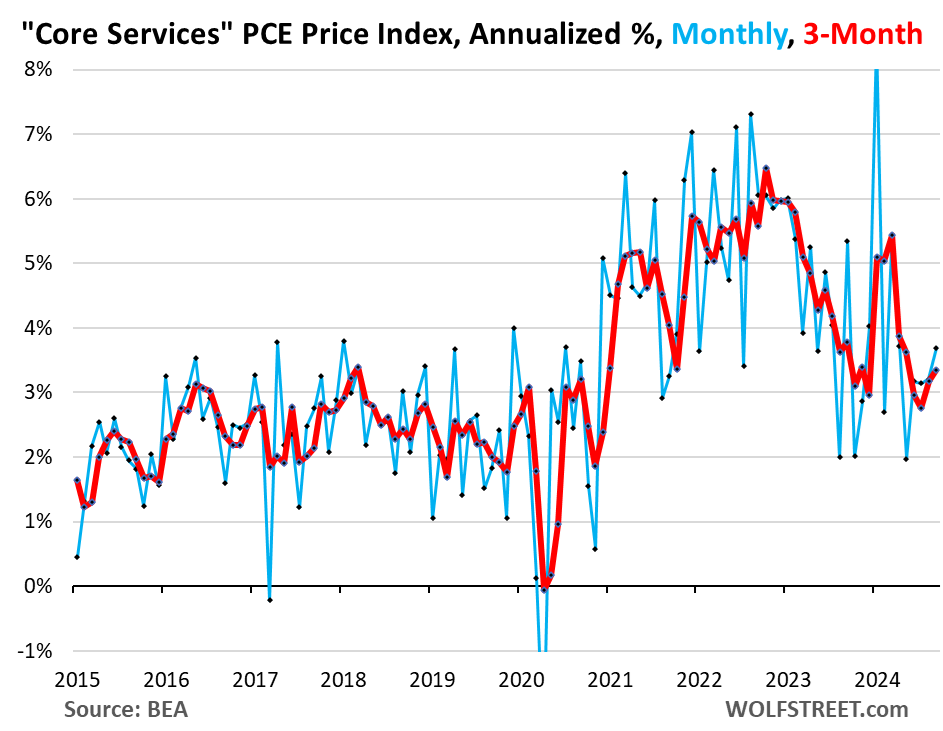

The “core Services” PCE price index accelerated to 3.7% annualized in September from August (+0.30% not annualized), the fastest rise since April. And the prior two months were revised higher (blue in the chart below).

Core services include housing, healthcare, financial services & insurance, transportation services, non-energy utilities, communication services, recreation services, food services & accommodation, and “other” services.

The 3-month “core services” PCE price index rose by 3.35%, the second acceleration in a row, and the fastest increase since May, and higher than it had been in October last year:

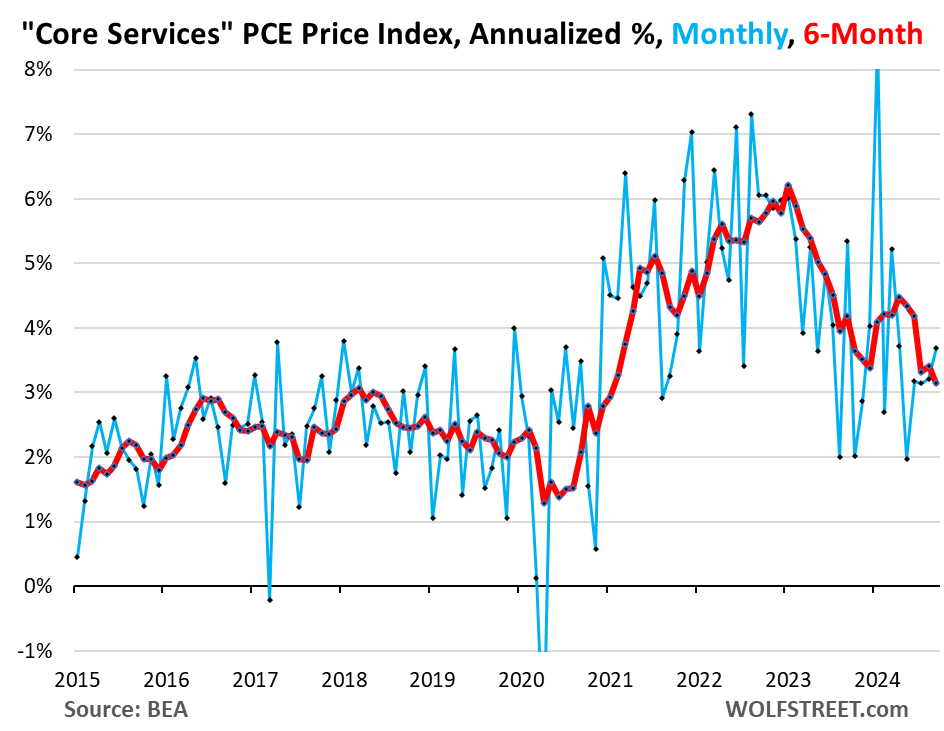

The 6-month core services PCE price index rose by 3.15% annualized (+0.26% not annualized), the first acceleration since April.

The durable goods PCE price index jumped by 4.0% annualized (+0.33% not annualized) in September from August, the biggest increase since September 2022, after a series of negative readings (deflation) in a row.

Durable goods include motor vehicles, recreational goods and vehicles, appliances, electronics, furniture, and other durable goods.

This sudden increase was driven by price increases in motor vehicles – we have seen this turnaround in motor vehicle prices from sharp drops to significant increases in other data – household furnishings and appliances, and “other” durable goods.

The 6-month index and the 12-month index became less negative, the 6-month index at -2.4% and the 12-month index at -1.9%.

The index tends to run in a slightly negative range during normal times amid manufacturing efficiencies, technological improvements, and globalization. It’s the services that have been the driving force of inflation for many years. During the pandemic, durable goods prices spiked due to the sudden demand fueled by the stimulus funds that made consumers suddenly willing to pay whatever; and that phenomenon met tangled-up supply chains, all of which gave companies enormous pricing power, and they used it:

12-month core PCE price index: No progress for 5 months.

The “Core” PCE price index, rose by 2.65% from a year ago in September, compared to 2.72% in August, 2.66% in July, 2.63% in June, and 2.67% in May, so rising roughly at the same pace for five months in a row, and well above the Fed’s target (red in the chart below). So no progress over the past five months at all.

The “core services” PCE price index rose by 3.7% year-over-year, a deceleration from 3.8% in August, and roughly the same as in July (yellow).

The durable goods PCE price index declined by 1.9% year-over-year, but that was a smaller decline than in the prior months, and the smallest decline since March (green).

The overall PCE price index, which includes the food and energy components, rose by 2.1% year-over-year in September, a deceleration that was driven by the plunge in energy prices (-15.2% year-over-year) and slower rising food prices (+1.2% year-over-year).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If money flows, the volume and velocity of money, are still in sync with inflation, then August represented a bottom. Next year inflation will be higher.

Rates should be going up, not down. This is bananas.

If the LNG ”pause” ends after the election, I would expect that while this may be good for GDP, it would almost definitely drive natural gas prices up, and with it the overall PCE index.

It’s interesting that the Biden administration mostly focused on using BS arguments from a notably biased researcher to justify the LNG pause for “environmental reasons”, when a more effective approach would have been to talk about how it would drive natural gas prices from extreme lows and closer to those levels seen in the EU ($12) or Asia ($13).

LOL.

1. that pause never paused LNG exports from existing terminals, never was intended to, and LNG exports have continued at a brisk pace, and they’re exporting all that they have customers for.

2. That pause was a pause of approvals of export applications from NEW LNG export terminals, meaning that when those new terminals would come on line, they could not export LNG until the applications would be approved.

3. That pause was struck down by a judge in July, and there is no more pause.

4. You people are funny.

Again, haven’t you heard? Biden shut down the fossil fuel industry. Hannity & Co still say the b.s. daily.

Wolf, how long do you think it will take for Core Inflation to start nudging headline back up? Will core have to rise up to say 3% before it has any effect on headline?

I guess petrol has fallen so much that it continues to pull down headline? I know food prices have fallen some at ALDI but not really at Walmart and certainly not Kroger.

Thanks!

Top headlines at MarketWatch:

“PCE report for September: Inflation data shows price growth moving toward 2%”

“Fed’s preferred inflation gauge moving towards target.”

“Fed can continue rate cuts on PCE data, Weinberg says”

“The Fed has almost hit it 2% inflation target, but it won’t be easy to keep it there”.

Nary a mention of core or core services.

That second quote is blatantly false because the Fed uses CORE PCE not the headline number. Core is up big m/m.

everything is more expensixe. Try going to fast foos an find out you cant affor it anymore.

Perhaps we found the floor in durable goods prices.

Looks like it.

We’ve already seen that the US legacy automakers will cut production rather than cut prices. New vehicles are way too expensive, after the huge price increases over the years. And so new vehicle deliveries are below where they’d been 25 years ago, despite population growth. But instead of lowering prices, which would boost sales, automakers rather cut production to keep their fat profit margins intact.

I’m saying this because we have seen that new vehicle prices are very sticky on the way down, and there is a lot of resistance to actual big price cuts (except among EV makers, following Tesla). And used vehicle prices look to have dropped about as far as they’re going to drop, and they have started to rise again. So overall vehicle prices might be about to turn from an inflation tailwind to an inflation headwind, and that will show up in core inflation measures.

Funny how this stickiness is prevalent across major capital assets like housing, if not even more so. New builders are lowering prices but doing so by incentives, rates buy down..etc, and existing home sellers largely still refuse to get the memo yet unless forced so.

For the auto and housing industries, we need some forced action to make them not have any options but to lower prices back down to reality. The Ratchet effect is a real B B. Once it’s anchored it’s probably 1000 times harder to make it go back down than the other way around.

As for this ” So overall vehicle prices might be about to turn from an inflation tailwind to an inflation headwind, and that will show up in core inflation measures.” wait until another one or two rates cut and if we are not in any major recession, people will once again lost their freaking mind and disregard the price because they can once again finance their new ride with 3-4% interest for 84 months…inflation tailwind it is…

“existing home sellers largely still refuse to get the memo yet unless forced so”

And judging by price movement, vanishingly few of them are being forced to.

I just bought a new Ford F150 yesterday and my out the door price was $11k less than the sticker msrp. So they are at least willing to deal now.

Yes, they’re putting lots of incentives on them – but not nearly enough. And thank you for the F-150 example… I track the MSRPs for the base F-150 XLT for my infamous WOLF STREET Real-World New Vehicle Price Index (F-150 XLT and Camry LE).

I assume that was a 2024 you bought (2025 F-150s aren’t out yet). The MSRP of the base F-150 XLT 2024 model increased by 10.9% (by $4,680) from the equivalent 2023 model. Higher-end trucks increased by bigger dollar amounts. The MSRP of a 4×4 crew cab Platinum with the big motor and some add-ons probably increased by over $10,000. Ford went nuts increasing the MSRPs like this from one year to the next.

So part of the incentives on the 2024s just undo the 10.9% increase of the MSRP. The remainder, if any, is a true price cut from the prior model year.

https://wolfstreet.com/2023/12/15/the-shocking-price-increases-of-the-pickup-truck-oligopoly-ready-for-tesla-to-mess-up-their-party-f150-xlt-camry-le-price-index/

I’ll update the chart and article in November when the 2025 F-150 XLTs arrive at dealers, likely later in November:

New 2024 are 10,800 out the door to shipping, if you paid more than 27000, that’s a premium.

Father is a retired GM Powertrain engineer, and I’ve been a loyal GM buyer for 20 years, but this is the kind of $#@! that continues Kia/Hyundai’s takeover of the remaining “Big” 3 market share. The Koreans have been on an absolute tear over the past decade, and if they ever build a light-duty truck factory here, it may be game-over.

This is just another example of the shortsighted corporate greed that will eat the domestic manufacturers for lunch. Kids today don’t care about cars, or, even driving really; but, driving is a necessity to live in this country, for the most part.

The Big 3 already offer limited small, affordable options, and with fat-cat pricing on non-competitive family vehicles (Traverse, Explorer, Grand Cherokee, etc.), they are just spiting an entire generation of buyers. If they don’t get people into vehicles now, do they REALLY expect conquest buyers in 10-20 years?! Especially when Kia/Hyundai actually now offer a complete lifecycle lineup and have strong, competitive options for up-sizing? Telluride/Palisade have been selling like candy at fat kid camp.

If they were smart, they would drop enough incentives to the hood to try and regain market share, brand loyalty, and, hopefully, buyers for life. What a bunch of fools. They deserve to go out of business for good…

… but then we’d only be furthering the decline of American manufacturing, which is at crisis levels and rapidly becoming a national security threat.

We need to get rid of these rotten companies and let new ones take over. Hopefully some legitimately new talent starting in America (with execs who can keep their mouths shut about politics) that we could all be proud of.

I would love to buy an American car next go around, but I will *never* buy the trash the Big 3 are slanging, and I will never buy anything that ties me to a nut bag.

I always say it’s very American to be capitalist and vote with your dollars, but the Government keeps working against me bailing these losers out…

I did read a couple of articles that say a glut of oil and nat gas will happen over the next 3 to 6 months and maybe longer. Energy prices may plunge more?

Also, just shoot the grain commodities. Wheat, Corn, Soybeans, and rice are basically at 2008 prices and from the charts indicate they are heading lower.

CL 1M closed between Aug close and Sept close. CL completed #13 of its monthly downtrend.

North America already has an effectively infinite supply of gas for the next 50-100 years.

50-100 years supply is a lot, but it is far from “infinite”

How funny….one glance at MSM headline this morning…inflation is meeting expectations. Didn’t read too much into it, knew I have to get the download here instead. Funny how hard MSM is trying hard to sell the next rate cut is less than a month away…

Reading the data here, not so sure if that’s still the case if Pow Pow is truly data dependent, guess we will find out real soon..

It seems to be the main questions are:

Does the current data tell us inflation is increasing or staying the same?

If inflation is starting the same, how bad would it be if it just stayed at 2.7% instead of 2.0%?

I think the answer to the first question is debatable and arguably there just isn’t enough information to say.

The answer to the second is open to a lot of interpretation. During the ZIRP era, there was a lot of talk about increasing the inflation target from 2% to maybe 3 or 4%, because 2% was a little too close to deflation during the Great Recession.

Reasonable questions to debate.

Another proposal was instead of 2% being a de facto ceiling for inflation, maybe we should target a 2% average, so if we undershoot for a while, we can also overshoot for a little bit.

Average PCE inflation for the last 40 years is now sitting at 2.4 percent

That would make Yellen proud. She considered it a career failure to not lift inflation to 2% during her term at the Fed office.

She can now relax…the goal has been achieved with prepaid deposits for a few more years.

I think that the 2% is not a ceiling but the average. But to have the average you need to first go below 2.

Average for 30 years is 2.0%.

“The inflation rate for consumer prices in the United States of America moved over the past 63 years between -0.4% and 13.5%. For 2023, an inflation rate of 4.1% was calculated.

During the observation period from 1960 to 2023, the average inflation rate was 3.8% per year. Overall, the price increase was 945.29%. An item that cost 100 dollars in 1960 costs 1,045.29 dollars at the beginning of 2024.”

Globalization kept it artificially down in the last 30 years.

if you think you can overshoot to make up for undershooting, then we should be undershooting by 12% for a time to make up for the 3 years of 18%. you can’t have it both ways.

It’s funny to take that data and make that conclusion.

Over 63 years: 3.8%

Over the last 30: 2.0%

Therefore:

Over the first 33 (1960-1994): ~6%

Which 30 year period is “natural” and which is “artificial”?

Conventional wisdom says the first period was abnormally high thanks to the oil shock and the failure of the gold standard. This was a time when inflation went from 4% to 13% and back again.

There is no 3 years of 18%.

There is a 3 year period that averaged 4.8%.

That came after a 12 year period that averaged 1.3%.

The combined average of that 15 year period is… You guessed it: 2.0%

patently false.

2021 – 4.7%

2022 – 8.0%

2023 – 4.1%

with compounding, that was 17.7%

1. Saying 3 years of 18% is at the least a little confusing, since people are used to seeing annual numbers.

2. Those are CPI, which averages to 5.6%. PCE was 4.1, 6.5, 3.8, which averages to, let me see, carry the 1….. 4.8%

3. The Fed explicitly targets PCE, which is known to run about 0.5% lower than CPI. In other words the Fed’s real target is about 2.5% per year in CPI.

My kingdom for an edit button. PCE runs lower than CPI.

“…all of which gave companies enormous pricing power, and they used it.”

This is a reminder that the Invisible Hand of the Market only works when the incentives are aligned properly, and competition exists. When a force is introduced that distorts the capitalistic landscape, it can shortcircuit the good that business does. The ancient ethical concept of a “just profit” has been carried over into modern antitrust activities. This legislative assertiveness, on behalf of the consumer, acts to curb companies’ “enormous pricing power.”

On the Federal Reserve’s official website it says the yardstick is headline PCE not core PCE.

And since August 2020 the FOMC officially announced that they are targeting average of 2% over the long term so periods of undershooting would be followed by tolerating overshooting and vice versa. The FOMC has so far not rescinded this objective.

Since that announcement headline PCE has overshot significantly by more than double i.e. over 4% instead of 2%. So according to the Fed’s own official policy framework they should now be tolerating a few years of significantly below 2% for headline PCE.

Depends on when you start your targeting. The average headline PCE for the last 30 years is now 2.0%.

The Fed’s target is 2% overall inflation on average over time. The yardstick to measure how close it is to the target is core PCE because energy screws up the headline figure, up and down, and the Fed is not going to react to energy prices spiking or plunging.

It its official communications — FOMC meeting SEP, minutes, etc. — it always lists both.

It’s Nov 1st. Inventories of 2024 car models are high. Prices are abnormally high. Incentives are too low. Very few people visit their parking lots. The legacy mfg cut production bc the dealers are saturated with old models (2024).

I would say this is manufacturer and model specific. Stellantis products? Absolutely the case and maybe most of the domestic mfg are experiencing the same thing. Even C8 C06 can be have for $10K under MSRP, although much like the housing market SoCal dealers still have their head up their A$$ with pricing either because they can get away with it or they are too stubborn to budge.

On the other hand, this inventory and pricing problem doesn’t seem to be the case for Porsche unfortunately…maybe for the Taycan and lower end Macan otherwise people still gobbling them up at high price it seems like

Many here are betting for higher inflation forward. So, stay out of bonds?

Or, consider buying inflation linked bonds and holding them to maturity. Real yields on TIPS are running around 1.7% for maturities in the next 10 years.

‘But energy prices plunged’

A huge factor, maybe THE factor, ex of course the Fed.

Just checked the chart and on June 10, 2022, oil was 117 a barrel.

We are getting a real easy break here. It may not last.

Cheap natural gas is putting a ceiling on oil prices. As long as the former remains cheap, I don’t see the latter getting much more expensive.

– If one Wolf Richter wants to argue that the FED is going to raise /should raise rates then he is mistaken. Mr. Market is still convinced that the next move will be a rate cut of 25 or 50 basispoints. In spite of rising inflation.

– And the yield curve has also gone from “Inverted” to “Steepening”.

“If one Wolf Richter wants to argue that the FED is going to raise /should raise rates then he is mistaken.”

I have no intention of arguing that.

I’m convinced the Fed will not raise its rates this year. I’m 100% convinced. Not going to happen. The Fed made that clear, all you have to do is listen to them.

I’m pretty sure the Fed will cut at least by 25 basis points this year, maybe more.

Does the Fed have a plan or do they plan to let inflation rip?

my guess is they will tolerate 3-6% inflation, meaning they will hike rates if inflation goes over 4% “sustainably” and they will cut rates when it drops toward 3%.

The FED is likely very please with 3% inflation, but they have to pretend their target is 2%.

Just to verify that I am reading this correctly Wolf you think that going forward the fed is fine if inflation runs at 3% as long as their no more big spikes? I thought I remember that you said the Fed would never let the allowable rate to increase past 2% since that would cause the long term bonds to yields to go much much higher.

The Fed is fine as long as it keeps its policy rates ABOVE the inflation rate. That’s the case now, and by a pretty big margin. So the Fed can cut a little and inflation goes up a little, but stay below the policy rate, and the Fed will be fine. The problem arises if the Fed cuts to 4% and core inflation jumps to 5%. In that scenario, if it looks sustained not just a one-off thing, the Fed will likely hike again. It may be a game they’re going to play for years, up-and-down higher inflation and higher rates for years, but not extreme.

What I said was that IF the Fed raises its “inflation target” from 2% to 4%, then longer-term bond yields would reflect that and surge, with the 10-year going to 6%-plus maybe. Looking at the bond market today, with the 10-year at 4.3%, up 70 basis points since the rate cut, I think that would still be the case. Which is why the Fed is unlikely to raise its inflation target.

– I assume that the FED will come up with some idiotic logic to justify to cut / not raise rates.

So what’s your interpretation of “mr market” raising the 10y yield 50bps last month?

Wolf,

These are great charts. A picture is worth a thousand words.

Millionaires and Billionaires are forcing the Fed to run it hot.

They don’t want to lose a single dime in these totally rigged markets.

The Fed cares a lot more about the smooth functioning of the Treasury market than they do about rich people losing a few mil in the stock market.

People have largely paid the higher prices, let’s see how that works as the second wave of inflation hits…

… neither Trump nor Kamala can stop this.

Interesting times.

Table 2.4.4U. Price Indexes for Personal Consumption Expenditures by Type of Product

[Index numbers, 2017=100; quarters and months are seasonally adjusted]

Personal consumption expenditures

Jan 2024 122.115

Sept 2024 123.930

Goods

Jan 2024 114.245

Sept 2024 114.250

Services

Jan 2024 125.930

Sept 2024 128.667

Mr Richter,

You’re doing a great service.

I used to dislike your information.

Now, I look forward to it, even things that my current understanding forbids agreement, thankfully, I am learning past that as internal issue.

Numbers and information like this, can be tilted/biased, but I see these and and now, after about a year following, sometime begrudgingly, and it is making a lot more sense.

No more watching the YouTube fear mongering, or mainstream news fear mongers, just read, parse and digest from decent sources like yours.

All that to say,

Thank you.

Bernard