He who panics first, panics best. Mr. Holmes, with no offers in 9 months, missed that train and is chasing prices lower.

By Wolf Richter for WOLF STREET.

So let’s use the example of “Anthony Holmes,” cited by the WSJ, who’d bought a house in a suburb of Tampa, Florida, for $550,000 in 2021 after home prices had exploded. He put another $50,000 into it and now has $600,000 in it. And then he had to move to Virginia for his job. He put his home on the market in February 2024, expecting an easy sale, maybe a bidding war or whatever, and some easy profit. But nothing. Then he dropped his original asking price five times to $583,900.

“I can’t unload the thing,” Holmes told the WSJ. “In eight months, I’ve had zero offers. No one even showed up to the open houses. Nobody.”

We know why he “can’t unload the thing”: price is too high.

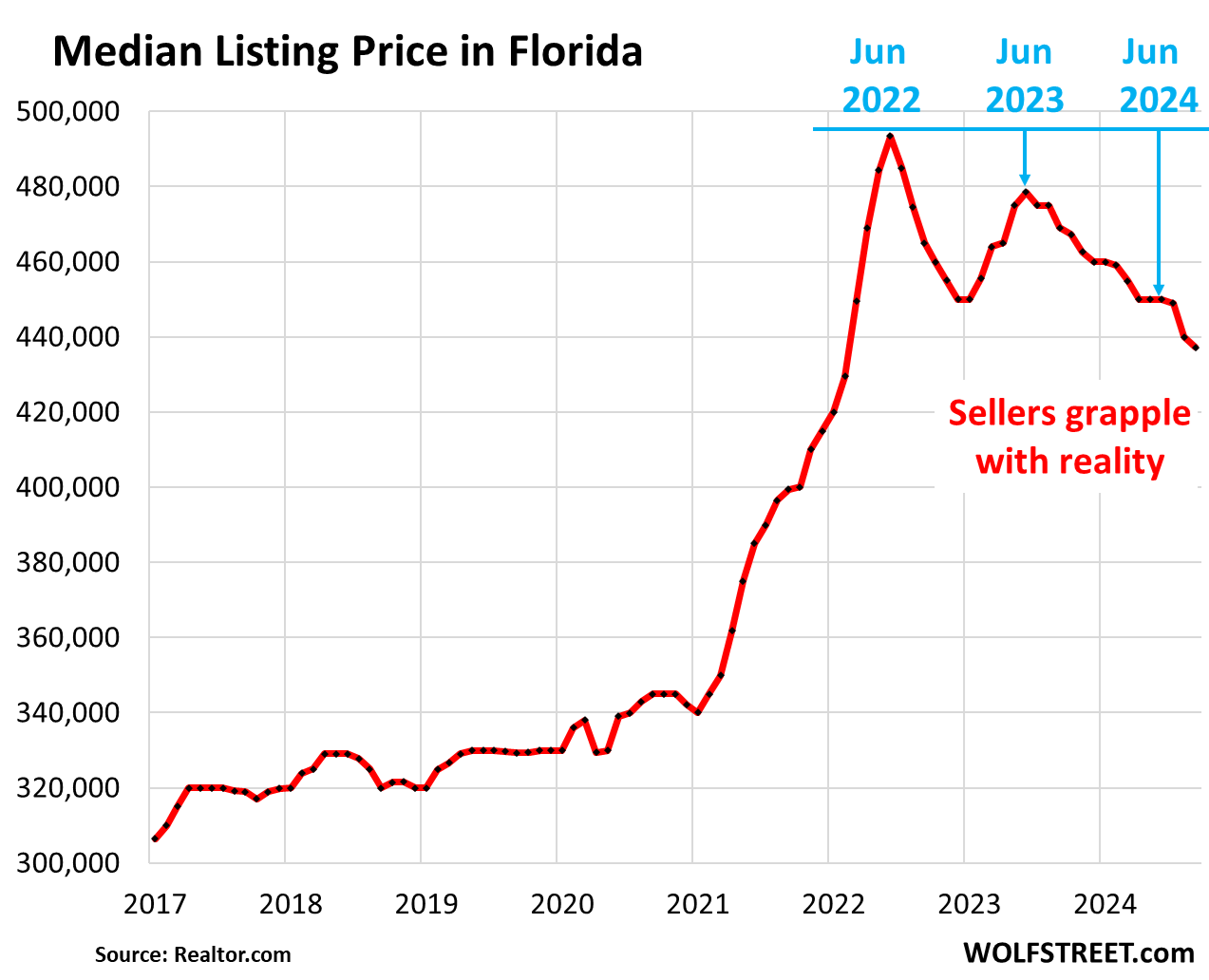

The problem when no one shows up is the listing price, in comparison to similar homes in similar areas. You can sell just about anything if the price is low enough. People are buying homes in Florida, it’s not like no one is buying, but sales have plunged, and the price can no longer be whatever. If no one is interested, the price is too high, it’s as simple as that. And likely by a lot. If it’s just a little too high, you’d get some nibbles. This is the situation Mr. Holmes is looking at, and time is not on his side (data via Realtor.com):

The median listing price in September dropped to $437,251, the lowest since February 2022, according to data from Realtor.com. On the way down, it blew right through the normal seasonal high in June 2024 without stopping, and the slide has accelerated since then.

Listing prices are prices that sellers, such as Mr. Holmes, want or that they imagine might work. It’s not the price that buyers have agreed to pay.

Mr. Holmes spent the past nine month chasing after the faster-dropping listing prices of his competition.

Compared to the seasonal peak in June 2022, the median listing price is down by 11%, and we have the impression that this has just gotten started.

Transaction prices (closed sales) for single-family houses Florida have fallen for three months in a row as of August, reducing their year-over-year gain to 1.5%, according to Zillow data. Condo prices have fallen for the eighth month in a row as of August and are down 2.5% year-over-year, and back where they’d first been two years ago.

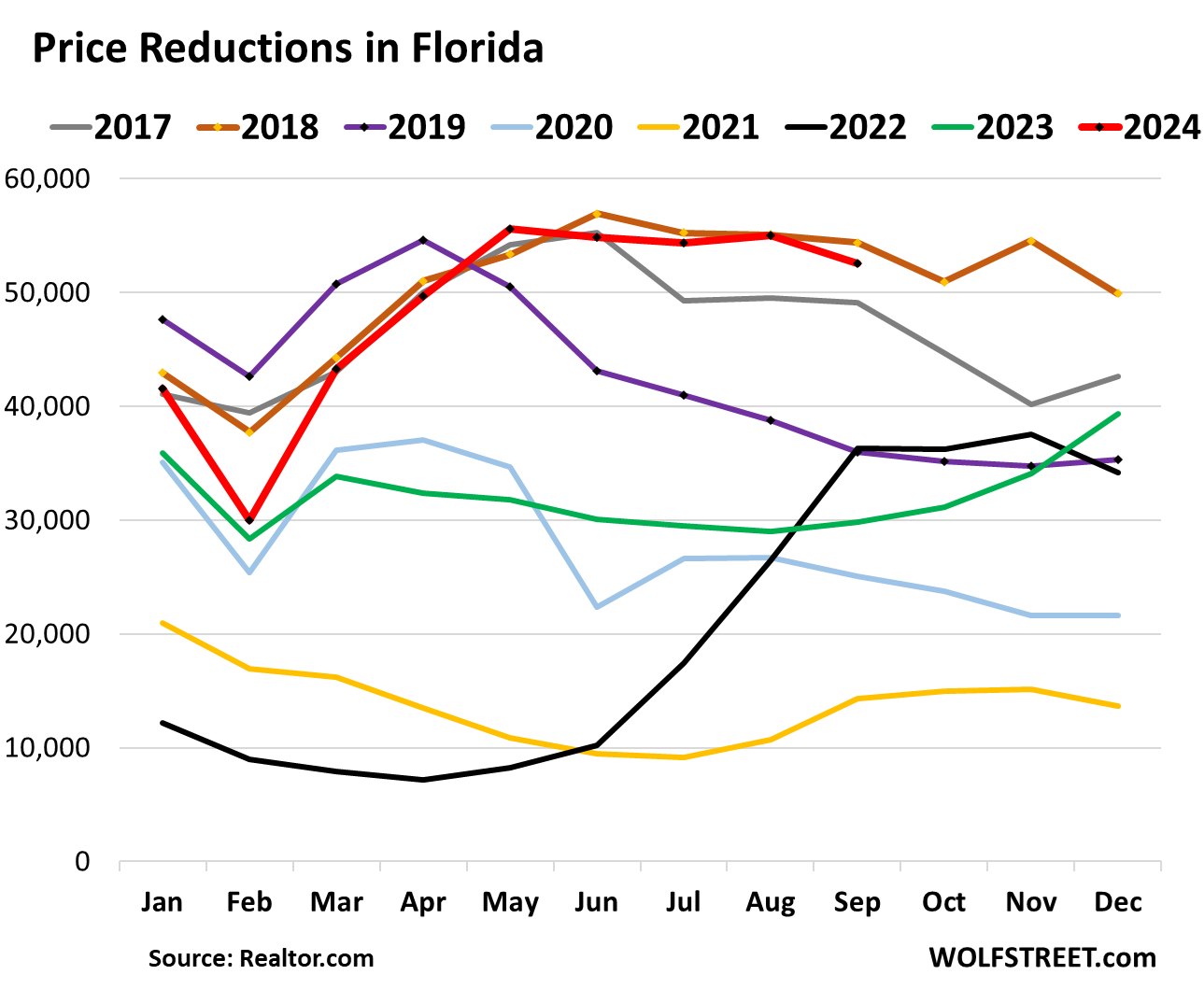

Price reductions to deal with a too-high listing price.

In September, there were 52,554 listings with price reductions in Florida, the second highest for any September in the data going back to 2016, behind 2018. They have surged by 76% from September last year.

Mr. Holmes’ five price reductions came off his inflated asking price and have been way too timid and too slow, attested to by the fact that no one came to any open houses.

It doesn’t matter to buyers how much money Mr. Holmes put into the house; it’s irrelevant to them. He said he’d like to break even, but that’s irrelevant to buyers. The buyers are going after deals instead of paying whatever.

Listing prices need to be reasonable in the first place, and when they don’t catch, price reductions need to be bold and stand out in this field of competition, because there is a lot of competition now (data via Realtor.com).

Big institutional investors have turned into net sellers.

The big single-family rental landlords have years ago switched to building their own build-for-rent subdivisions, with leasing and maintenance offices and common amenities – the hottest trend in homebuilding. These communities are more efficient to operate than individual houses scattered all over the place.

In their earnings calls, some of them started spelling out last year that they were selling some of their scattered rental properties that they’d bought out of foreclosure during the mortgage crisis, and especially in 2012-2014 when Blackstone and others piled into this market, with encouragement from the Fed. Now, after these massive price gains, they’re making huge profits on the sales even if they price the house aggressively. They’re the pros, they know what they’re doing (Who are the Biggest Landlords of Single-Family Rental Houses and Multifamily Apartments? Who Owns the US Rental Housing Stock?)

In Tampa, Orlando, and Jacksonville, institutionally owned single-family houses account for nearly 5% of the listings over the past 60 days, according to an analysis by Parcl Labs, cited by the WSJ. Institutional investors own between 2% and 4% of the single-family houses in these three markets and have been net sellers – they’re reducing their portfolios – in those markets over the past 90 days.

That’s the competition Mr. Holmes has to deal with.

These companies don’t have $600,000 in their houses. They bought them during the Housing Bust for a fraction of that, and they’re making huge percentage gains if they can sell them for $400,000.

Every month that Mr. Holmes doesn’t sell his vacant home is an expensive month. The carrying costs are substantial, even at the lower mortgage rates of 2021, and the insurance premiums, oh-la-la. A vacant house is a money-suck, and prices are heading lower.

You can’t lose money in real estate is the biggest propaganda BS line ever, as even the smartest institutional investors and lenders in commercial real estate have been re-learning over the past two years.

But he who panics first, panics best has been forgotten. Mr. Holmes missed that train already. And now there’s another hurricane that he wouldn’t have had to deal with, if he had priced the house aggressively in February, underbidding everyone else, and selling it quickly for the least possible loss.

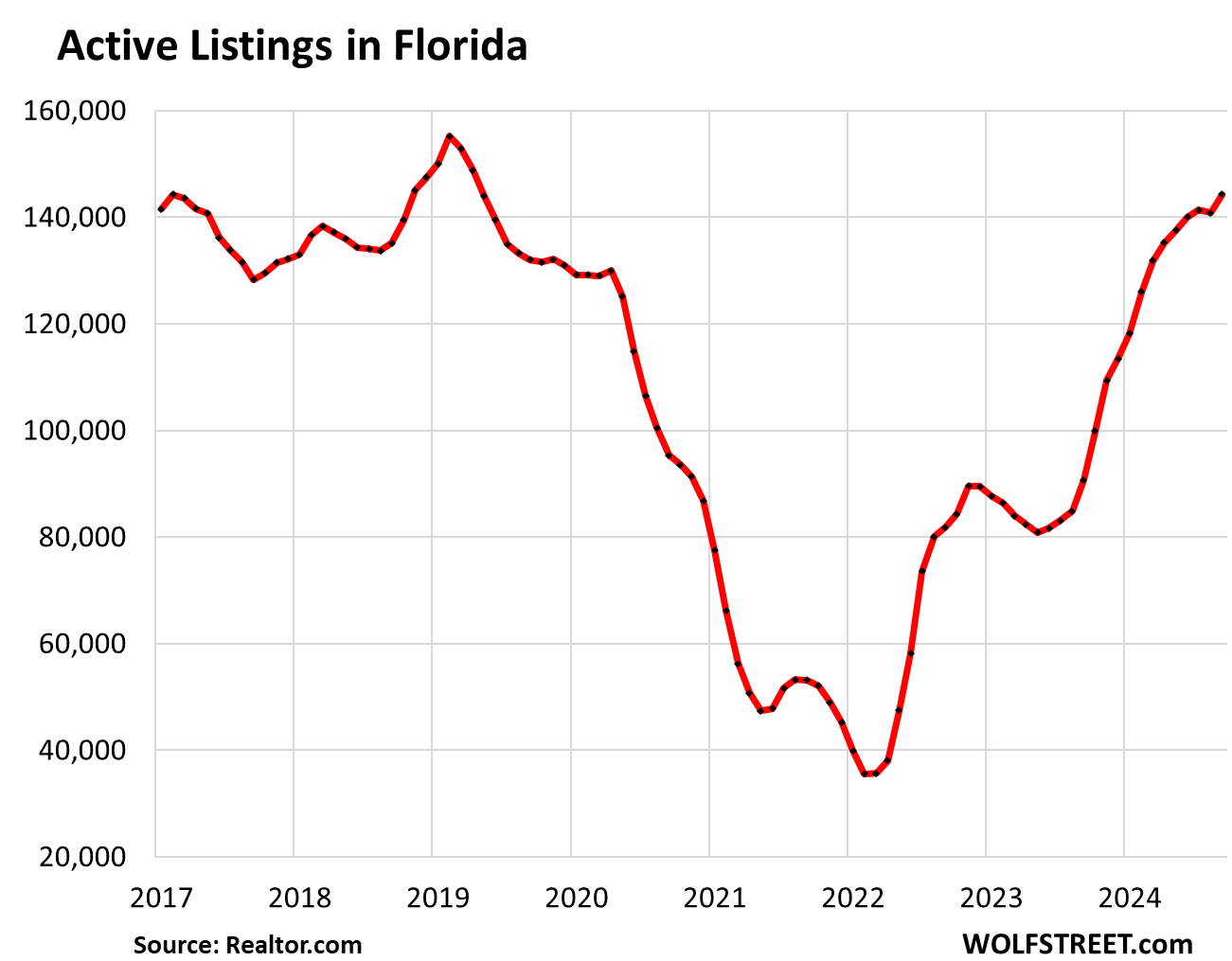

And inventory – the competition to Mr. Holmes – is piling up, put on the market by similarly nervous home sellers.

Active listings pile up.

Active listings (total inventory minus listings with a pending sale) surged 35% year-over-year in Florida, to 185,696 listings, the highest for any September in the data going back to 2016, as demand has wilted and as inventory gets stale because prices are way too high (data via Realtor.com).

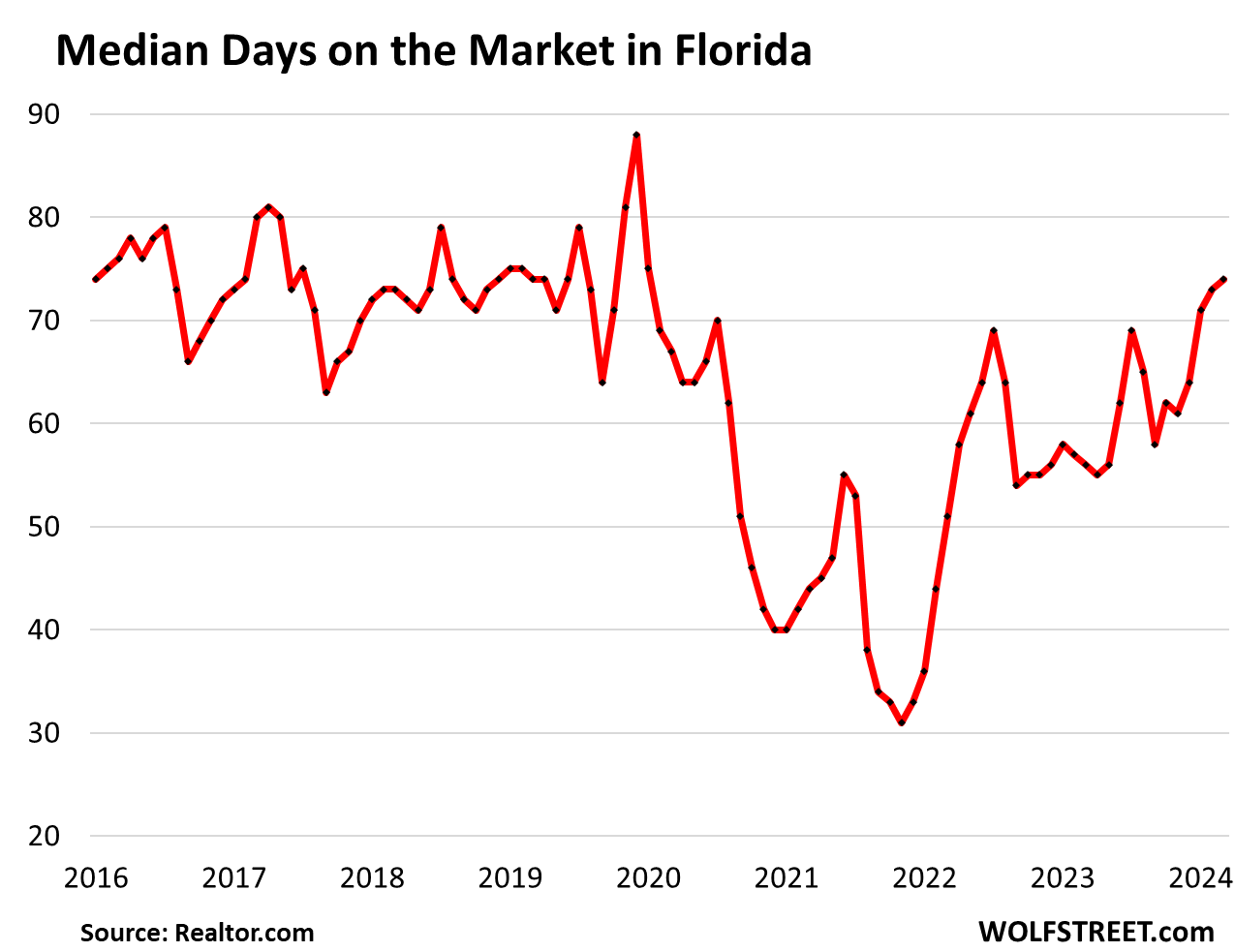

Median Days on the Market drag out.

The median number of days a property sat on the market for sale before it sold or before it was pulled off the market rose to 74 days in September, matching September 2019, and both are the highest since 2017.

This metric is a mix of:

- How aggressively sellers pulled listings off the market if they didn’t sell;

- And how fast properties sold that did sell.

When sellers get more desperate, they leave the property on the market, rather than pulling it off quickly, and they might try reducing the price until it sells. In that dynamic, the days on the market lengthens.

So we wish Mr. Holmes best of luck.

But he doesn’t need our wishes or luck; he needs to cut the price boldly and pronto, understanding that buying the house during the craziest housing bubble ever was just a high-risk bet that didn’t work out, and that happens, and he might be out some money. But he would have been out a lot less money, including nine months of carrying costs, had he priced the house in February to underbid everyone else and to sell it quickly and to wash his hands off it with the least possible loss (if any).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m glad to see Mr. Holmes suffering. Schaudenfraude or whatever you want to call it. A very large contingent of people are sitting on homes that were supposed to be escalating in value to eternity, and they’re discovering that there’s something called a rational market. Hopefully, all those who bought “high” are forced to sell “low.”

Spread that schadenfreude please, we need some in Cali too. The hubris around here is even more suffocating that Austin or Miami.

Don’t forget, housing is a leading economic indicator. If there’s a real, business-cycle recession, housing will probably lead the way. Housing price drops are slow compared to a stock market drop.

I’ll bet a lot of home owners

and especially older condo owners want big wind to take out their buildings

many are going to collect insurance and walk

You got to mention “big wind” though….which may lead some to wonder, “why now”?

Capitalism will just get much more vicious….unless maybe democracy does….always hope.

Not happening in Cali because no oversupply from building boom and not sinking under the ocean like Florida.

Fausterion,

Coming to a property near you… (highest since Nov 2019, with sales in the dumpster):

Florida does seem like a special case. Constant threat of hurricanes getting worse every year due to the climate crisis? Rising sea levels? Increasing tropical diseases from mosquitos, etc? No thank you.

Admittedly I’ve had lucky timing on my hom in CA. Bought in 2014 not at the bottom but kind of close. Refinanced to near 2% loan and property has doubled in value in 10 years.

Sure inflation takes a chunk and there is upkeep, insurance and taxes, but I have to live somewhere. My mortgage never goes up, unlike rents. At this point I could rent my house and pay my mortgage and make some monthly income to cover maintenance, insurance and taxes. I’d rather live here.

Had I just rented instead of buying, I could have invested the difference until a couple of years ago when the cost to rent eclipsed my mortgage and housing costs. As of now, I’d be paying more in rent AND have no equity. Sure, investing let’s say $15k to $20k per year into the market for 10 years might come close to my equity, but the capitalgains exemption on the sale of a primary residence is an amazing benefit and tips the scales stronly in favor of buying when I did. I probably wouldn’t buy a house at this time though, as prices seem overheated. For real estate investing right now- maybe multifamily? If I start seeing tons of agents signs everywhere and lots of foreclosures maybe I’ll buy a smaller place for vacations and just rent it when I’m not using it and then eventually retire there and just cash out of my house. I realize I have been lucky so far and I suspect the home prices will go up and down over time, but mostly up. No way I would ever buy in Florida, in a flood zone, in a wildfire area, etc. That just seems unwise. Climate change IS real.

When stock mkt rolls over all of Cali will tank

The thing no one is talking about is the giant spikes in taxes and insurance. In Florida, the average tax and insurance costs for a new purchase are going to set you back about $12k a year on a $700K home.

In the CA metro areas, with average home prices in the million dollar range, the hit for taxes and insurance is in the $15- $18K a year range depending on fire risk assessment.

When you start talking higher end homes, the numbers just get stupid…

I’ll throw in East TN and that’s especially bc of the well to do up staters from NY NJ and other states buying with cash. Plus current owners who have been here forever know they can get whatever number they put on it. Still plenty of greed, the only cure would be for buyers to go off the grid and take a stand….not me not going to be someone’s victim…

IMHO, the main problem is that Mr Holmes treated buying a house as a short term investment rather than a long term place to live. Historically, people purchased houses for the long term as a place to enjoy life and raise a family. If you planned on only living in a location for a few years, you rented. It is only within the last 10 years while the Fed was blowing up this latest bubble, that selling within a few years might be profitable (and maybe 2002-2006 during the first bubble). People have short memories.

As a huge fan of Wolf’s charts, the only guarantee of making a profit with a house is to hold it for 12 years based on Wolf’s excellent charts covering the last 40-50 years. The worst case was buying in 2006 and selling in 2018. I would plan on worst case this time around also. If you plan on staying 12 years, then buy. Otherwise, prepare to be disappointed.

I don’t think he necessarily treated it as an investment. I’m sure he had a job where he was working remote and expected that to continue forever. His employer called him back to the office, and now he has to sell.

His mistake was buying a house at all when his situation was likely temporary, and certainly buying at that ridiculous price.

You are probably correct about being forced to sell due to his job.

I think he had high expectations of short term profit since his initial list price was 635K. His delayed dropping of the price probably now means he still has hope of minimizing his losses like any investment.

You are definitely correct that he paid too much and should have rented with his employment uncertainty.

Endorsed. Houses are for living in.

Correct. And it’s awesome when tenants pay to do it!

Shelter is a basic human need….like GOOD food.

And both in moderation. And exercise, even just tensing up all over from time to time, as I do, being unable to walk much.

Exercise actually “pumps” the immune system contents around the body. Like blood. it has vessels, but no heart (a few animals actually do have an “immune system heart”), so we rely on check valves like in out veins to pump fluid around from node to node.

Therefore some exercise to squeeze the vessels and pump the fluid is required. Bio lesson for the day. No charge.

Fixed cheap diet and cheap hygiene experiments still in progress, but going fine.

Both=all…..AWESOME error.

It takes 5 years to make back the overhead in buying and selling your primary residence. If you time it wrong then it could take 10 to 15 years. I don’t feel sorry for these so called small timer investors who try to use housing to make a short term buck. A home is a place to live, period. Speculate in something else to make the quick buck. Most of these “whining dogs” who are getting killed by the repeat of the 2006/ 2007 housing market in Florida are losers.

A home/house is whatever I want it to be. I could tear it up and use it for firewood if I chose, I bought the damn thing. Hope I didn’t ruin your fantasy of, a home is a place to live in, a happy place, a safe place to raise a family.

Generally an investment like a HOUSE will be cared for so it keeps it’s value so, no need to report me to the house patrol.

Next thing you’ll be telling people what a woman is….go ahead, I double dog dare you.

There is no buy and sell at a profit quickly. You need to stay in the house at least 2 years. Otherwise you’ll get hit with capital gains taxes.

Bob E. Good advice!

There is this utter nonsensical trope out there that a house is an investment. It is not. A house is a necessary shelter. If one is married and has kids, it’s a great environment to be in, but it is expensive. If one is single or has no kids, it pretty much does not make any sense except to see it as a speculation. There’s much easy speculations out there for one to dabble in.

signed: a 65 year plus house owner.

Tropes are silliness, and stating homes are never investments is another one.

A home CAN be an investment, but is not automatically one.

It’s backwards. Shelter is necessary and a home is one of many types that meet the need.

Notice the people here mortgaging 30 years at 7% in this market nearly all caveat “I know I just made a horrible financial decision, but my home is not an investment, it’s a place to live and I got what I wanted.”

It was never about any deliberate investment decision to actually cash flow money or they would have bought a triplex.

It’s rationalizing a (overwhelmingly poor) decision.

I NEVER advocate a young family but their first home for themselves. But, they are free to do anything they like.

If they do so anyway, you were never going to talk them out of it. I have no positive experience doing so except with my two sons.

I personally own 15 homes that are worth millions and cash flow 100s of thousands.

I still view every home on the planet as a possible investment, it simply has to meet the criteria.

It’s all a matter of perspective. Tropes exist for a reason.

“Pilotdoc” is a trope.

Btw, you sure others buying millions in housing for you is a good thing? It’s not like you need the money……

Pilotdoc – I for one would call shelter an investment in my future regardless of whether I ‘lost money’ on it or not. What’s the value of a roof over your head? Pretty high I’d think.

Yeah you can get it cheaper somewhere else, or compare it to rent or whatever, but I for one prefer living in places I like. That’s worth a lot to me and is worth paying for. Investment is the icing on the cake if you can do some math and don’t get greedy about things.

And everyone and their brother is a real estate “expert”. The next sentence from Mr Holmes’ mouth will be something along the line of : “Well, I’m not going to give it away”.

Re obstinate sellers…

I see a nice home near Sarasota, sold for $1,185,00 in 2022, that was listed for $1,300,000 in 2024. Price has been reduced a tiny bit since then.

If you accept the “deal”, you get a home for a price that is 10% higher than the peak, plus a RE tax bill that increased 50% from 2021 levels, from $10,800 to $16,700.

Sellers are now testing the limits of FOMO.

As a general matter, I see so many homes for sale in FL that were just recently purchased in 2022. Why? Are they investors looking for quick gain, hoping to capitalize on momentum. Are they people with FOMO regret, living in the home, who paid too high a price and now want to eliminate downside? Are they looking at 50% increases in their RE bills, plus doubling or tripling of insurance costs, and saying “I need to get the F out of here!”? Are people overextended and disappointed they cannot refinance at a lower mortgage rate? Are estate sales picking up?

I think the selling pressure is coming from lots of angles right now, and another huge one will be added if the job market declines.

Two more possibilities, one, they bought it during the work remote period and are now selling because their employers expect them back in the office, at least on a hybrid schedule. My guess is they tried to find jobs down in Florida and couldn’t, at least not at the salaries they needed to sustain those houses.

Two, they don’t like Florida. A lot of people visit it and love going to the beach in the middle of the winter. It’s not all vacation when you have to actually live there.

I wonder if “Anthony Holmes” Tampa subugb home is in a western or eastern suburb. Having a big hurricane heading for Tampa might actually help him if his home is not flooded or destroyed. After a big hurricane or wildfire many homes are usually destroyed and the people that lived in them usually need a place to rent. If the market rent will cover his taxes, insurance, mortgage and a management fee he can rent the place and sell down the road (a cousin owned a home with zero equity in San Antonio TX in 2016 and was able to rent it and Zillow says it is worth ~$400K more today.

The problem is that it will probably be flooded and destroyed. And then he’ll have a much bigger problem, especially if it’s not a member of the maybe 20% who have flood insurance group.

Living in Florida without flood insurance is like living in Seattle without a raincoat. Eventually you’re going to get wet.

Flood insurance is expensive. My mother’s Holmes Beach beach house got flooded by the Helene storm surge. She has no flood insurance and the repairs will likely cost less than the 10 years of premiums she would have paid. And she says that flood insurance would not have covered damage from the 3 feet of sand in her living room. And repair work can start faster without dealing with insurers. Then again, the house may not be there in 24 hours…

or living in SoCal without earthquake insurance….and let’s say plenty of homeowners don’t have them around here. They can’t afford the mortgage plus sky high premium for the insurance…if they can barely squeeze into the monthly payment especially if bought last 2-3 years…

PI, I think there’s a sizeable deductible on earthquake insurance. Just high enough so the insurance companies won’t have to pay a cent unless the house collapses.

Or like living in CA without earthquake insurance.

Most people in CA don’t have earthquake insurance because it is expensive AND it has a high deductible so minor damage from a minor earthquakes is not covered.

However, like a major hurricane with a direct hit on your house, a major earthquake that happens every 100 years, could ruin your life.

I do think climate change is occurring so the probability of a major hurricane hitting your house is more likely than a major earthquake hitting your house.

Insurance rates for hurricane flooding and earthquakes are high due to the costs involved if it does happen. Both could destroy your house.

The home is miles inland you dumbass ignorant twit.

Asheville NC is hundreds of miles inland, and it got destroyed by flooding from Helene. The storm surge near the coast is one thing. But hurricanes can drop a huge amount of water from the sky all of a sudden. Hurricanes are terrible.

If you think the recent flooding of Asheville is a one-off. Look up Hurricane Agnes 1972 – hit way upstate NY with massive flooding. Was costliest US Hurricane up to that time.

Hurricanes often do lots of damage inland. Areas that are hilly/mountainous have a huge amount of water coming down the slopes very fast. Areas that are flat, can’t get rid of the water quick enough.

Very ugly.

Wolf reminds us that hurricanes can drop a lot of rain miles inland, the winds can also crush a lot of homes when trees come down and even rip the roofs off homes (a friend’s parents had the entire roof blown off their home in Orlando ~50 miles from the coast more than 20 years ago (I forget the name of the Hurricane that did it).

Tina just didn’t really give AI the excellent insult that he REALLY deserves, IMHO. But it’s nice to see a new comment from a silent fan of WS.

AI should think about why she finally chose to comment, maybe?

They will just get another FEMA bailout whilst complaining about taxes and welfare.

Even insurance companies have been closing their purses.

There’s loads of fine print and they have more lawyers than their policy holders do.

I am in a forested area and I know many insurers have basically left the state of Co. in recent years. Same with Ca. And Fla.

I’m not hoping disaster on anyone, but it appears unavoidable. This guy’s a soaker!

What a nightmare. For those whose homes are destroyed, time to move out of the area, rather than rent.

It seems very likely that we’re at a tipping point in Florida in terms of insurance companies pulling out in-mass from coastal areas. I know the Citizens Insurance company that’s state funded / owned is getting stuck with most of the high-risk policies.

I recently watched a very informative mini-documentary about this very issue, and many of the big insurers are pulling out and are being replaced by these lower tier insurance providers who rely very heavily on the re-insurance industry. There’s a company founded by a former Enron exec who is on tape bragging about how his company is cherry picking the low-risk policies and forcing the higher risk policies onto the state-funded Citizens insurance.

Florida is about to go from a mess to a catastrophe in terms of insurability.

All of the big insurers have long ago pulled out of Florida. There are still some big names, but they’re not the national companies. It’s not State Farm, it’s “State Farm of Florida”. A weak subsidiary with funding only from the residents of Florida ready to declare bankruptcy and shut down operations the second that last nickel is spent.

Great point. Likely to be missed most here.

It is a mess they can navigate out of however. Increase in property taxes, start a sensible state income tax for openers. that is how most of the northern states fund the catastrophes that beset them due to weather. And, the northern states have their share of weather events.

Louie, New Hampshire has no income tax.

Half of New York’s income tax revenue goes to fund the state Medicaid.

It’s nonsense to say that that’s how northern states fund their catastrophes.

Oh yeah, I forgot to mention, Florida already has high property taxes especially for people who bought during the peak.

It’s in Seffner, FL, which is east and not desirable and the price is way higher than the other homes in that area that no one really wants to live in. I’m not surprised it’s not selling. He way overpaid for that thing in 2021. 806 Red Ash Ct, Seffner, FL…

Well, at least he has a reference to what the bottom can look like…then again 2015 wasn’t the trough of the market…hmm…

4/17/2015 Listed for sale

$335,000

$97/sqft

Good detective work in finding the house. Mr Holmes should have noticed in 2021 that he was paying almost double the 2015 price. That would scare me.

I don’t know the area but the house looks nice and it is only a 20 minute drive to Tampa (12 miles). That is a very short commute by CA standards. Hopefully 12 miles from the coast is enough to survive a major hurricane.

That was what caused America’s inflation in general. Had Americans just said “ENOUGH! I will not pay 80% more than what people paid two years ago,” inflation would not have taken off like it did. But our people seem to pay whatever they can afford to, not what they should pay.

Not to mention that his price drops are not real drops. Had he really wanted to sell, he would have realized his $625k asking price was too high, and started dropping $25k at a time. His measly $5-$10k drops over 7 months is not moving the needle for anyone. No one thinks “Oh, I wasn’t going to put in an offer when the price was $615k, but now that it’s $605k, let me offer up!”

This guy is an idiot.

It with the hurricane coming Milton. You will be able to buy houses in the area for 40 cents on the dollar! Who wants to buy in the middle of devastating area?

Are you kidding??? If you haven’t any idea at all about the destructiveness of a FLA hurricane, live the space clear.

Having lived the majority of my adult life on the east coast of Florida (40 years). People who haven’t lived here a long time tend to jump to conclusions that may not be accurate. This is enhanced by the media which focuses on sensationalizing major events (esp weather). You are completely accurate. Many houses will survive with minor impact, but many will not. There will be plenty of people who lose their home or need housing until their damaged home is repaired prompting a mini bidding war for homes in decent shape. Good comment.

You know what I am going to say…wish I can see this same thing happen in NorCal and SoCal too, unfortunately, the dynamic is different, and likely won’t see anything similar soon or ever…also wonder what the % of institutional listings is like in SoCal, probably minuscule compared to that 5% in Tampa, Orlando..etc

Once again hoping I am dead wrong on my assessment but not holding my breath either.

You need to step out of that insane bubble. Last time when i lived there I hit a 2-3M open house and went straight to the fridge, lol. Fat agent with rings on every one of her fat fingers was talking the spec mansion up but it was easy to point out all the wasted and pointless details. This was in the hills of Santa Barbara by the way. When this thing crashes there will be a ton there for sale, lots of folks love their jobs too.

West coast will be impacted with stock mkt bubble pops.

It’s not a shortage when u have constant population outflow

“If you’re the first one out of thje door, it’s not panicking.”

– Margin Call

LOL… that was a REALLY good movie.

I hope everyone in the path is current on their auto, home, boat, business, and hopefully separate flood insurance policies. Once the storm passes, begin the process of the vast majority unfortunately receiving quick denials from their friendly adjusters.

I wonder about going “self insured.” I heard a podcast with Charlie Munger who stated he is self-insured and has been forever. His properties are well-maintained , so why should he pay to be in an insurance pool with people who allow their homes to be in worse shape?

All the riders and exclusions make the likelihood of a payout small – wind, flood, high deductibles. I have high net worth and can rebuild.

You have your own road, fire, police, and defense, etc, etc, etc, depts, too?

Or are you just a rugged self-made individual who relies ONLY on yourself….like (har har), Mung?

Chris8101

Self-insurance is easy to do if you’re wealthy and have lawyers on retainer and don’t owe money on your house.

If you have a mortgage, you can’t actually be self-insured because your lender requires insurance, but let’s assume that you could…

If you can barely make your mortgage payments and are self-insured [if your lender would let you], a storm or fire or whatever can wipe you out.

Very wealthy people have a different understanding of life than normals.

Do you do all your own maint, too?

That’s a personal decision. But I will tell you, personal injury lawyers are among the best insured people I know. Yes, there are many exclusions. But there’s also coverage for lots of events. Policies to cover everything at the base level, often supplemented by multi-million dollar umbrella policies among this group (basically in an amount to make suing the owner less attractive). And even flood insurance for whatever that’s worth. At the very least, anyone with wealth should pay the relatively cheap attorney’s fees to consult an asset protection lawyer in every state where they own any property.

Re: “ least possible loss”

You need to copyright that or maybe buy a domain name, maybe sell a book or another great post — no a series, syndicated weekly column picked up globally — this could be Bigger than The Big Short!

Unfortunately, very unfortunately, I didn’t coin the phrase. But it would make one hell of book title.

Maybe “Best Possible Loss”?

Looking for some ’80s financial history books, I just searched on AMZ books for “takeover,” and was stunned how many dozens of titles were just “takeover” or “hostile takeover.” Page after page of identical titles. Most of them, alas, are romance novels.

“You can’t lose money in real estate is the biggest propaganda BS line ever”

Propaganda? more like the Ten Commandments to a lot of homeowners, the going up forever narrative is like prosperity gospel to them…this is especially true in Asian countries like China and HK and much like a cult, you’re a true believer until either you wake up or join the shuttle to catch Hale-Bop

The tide would have to go out an incredible amount in SoCal (and resort NorCal) before anybody in my family would lose a dime on real estate. Like, several multiples of any historical drops. Like, Kim Jong Il sends a nuke or something. Our weird practice was not acting like a flipper for multiple decades, and never taking out a second lien, etc.: just living basically like plain folks in the mid 20th century expected sensible people to live. Is that smugness? No, it is sensibleness.

Having common sense is rare in a mindless state like ca. We are missing 4-7 million homes and possibly much more given the unknown amount of migrants in our country. Insurance taxes and maintenance are through the roof literally. Meanwhile it’s hard to hear me over the sound of the printing press going brrrrrrrr to pay for democrat hyper spending. Middle class is dead

I think the same but I thought the same in 2007 as well as in CA real estate is like religion which can never go down.

Anecdotes:

My friend is paying $30K per year just on insurance and property tax for a simple middle class home, away from the coast, valued at 1.6 mil.

One person I know, is trying to rent his 1.4 million home for 5.2K.

1.6M for an average house was not the deal of the century

Don’t know about Orlando or Jacksonville but for Tampa, maybe there will be quite a bit less active listing after next week?

Loved it! The story format was great. Thanks Wolf.

Mr. Holmes has a ton of options. Maybe his job compensates him enough that he can just eat the loss. Maybe he could look for a new job. Maybe he put 1% down and foreclosure is an option.

I was one of those A-holes holding onto property. In my case, since 2017. I sold it in August at full price. I realize it’s completely anecdotal, but I think the MN market never got as hyped up as Florida.

It didn’t. In Edina, where I have friends, it looks like prices generally went up by about 50% from 2012 to 2022. That’s a lot of course, but in parts of Florida, Austin, Nashville, and others, prices tripled in that time.

I’m from that area (Mn), and the biggest price pressure I heard of was the post-Floyd urban exodus, mostly just eating up inventory (both sale and rental).

Property taxes are a thing, but desirability isn’t nearly as high in the upper Midwest. “It’s a great place to be from,” I tell people.

I see in the chart that Fla. prices doubled in a couple years post-VID.

I live in Florida. You ain’t seen nothing yet. My advice to any home buyers here? You see listings for $600K ? Offer $400K. You see listings for $1 million? Offer $750K. A $2 million listing? Offer $1.5 million.

Eventually you will find someone desperate enough to take it. .

That probably will work better when the person bought many years ago and will still “make money.” The people who bought in 2021 or 2022 at peak bubble pricing will be harder to convince, as they’ll have to take a loss.

In Florida, I expecting even lower values. The tsunami of listings is yet to come. I wouldn’t buy any real estate until after the stock market crashes.

“he needs to cut the price boldly and pronto, understanding that buying the house during the craziest housing bubble ever was just a high-risk bet that didn’t work out, and that happens, and he might be out some money”

Judging by these price drop emails I see now from Redfin and Zillow, plenty around here didn’t get the memo with these pathetic price drop and even increase..here are some for your amusement. Good times

$1,375,000 drop from $1,390,000

3 Beds · 2 Baths · 2,222 Sq. Ft. Placentia, CA 92870

$1,799,000 drop from $1,819,000

4 Beds · 3 Baths · 2,386 Sq. Ft. Long Beach, CA 90803

$1,399,000 increase to $1,299,000

4 Beds · 2 Baths · 2,302 Sq. Ft. Placentia, CA 92870

How dare you!! How dare you tell me that my winning lottery ticket is not gonna make me filthy rich. I’ll list my average home for $10 Million and some sucker will buy it! Just buying a home is the new Lotto. We’ll all be millionaires. And if you suggest otherwise, well you’re a loser. Don’t rain on my millionaire parade, you killjoy.

Phoenix_Ikki,

Respectfully, I try to empathize with your gripes about the housing market. But you constantly cite prices from, quite literally, THE most expensive / overvalued housing market in this country.

It seems like you want a house – have you considered simply looking somewhere cheaper?

@shortTLT to your first point, yes and that’s because where I am at but also worth citing because it’s also one of the most out of whack market when looking at income/housing cost ratio, which further illustrate how insane this bubble is…

your second question, no, not yet. Not as simple as pick up and move, with a high income, it’s all about opportunity, let’s say there’s limited option with my industry for other states and making remotely similar income, plus I can wait it out for another 2-3 years worse case scenario..

Yeah, I hear your gripe. The $1000/sf is eclipsed by the $3000/sf in the utopia I live in!

The bubble money is roosting at the top, as usual. I live in a place I paid about $270/sf and 8 years later I could sell for a whopping $305/sf.

I live in a “Deed Restricted” condo. It’s a trip! Mine includes an appreciation cap (some flavors don’t). I heard Aspen granted an “appreciation holiday” to the tune of 30% a couple years ago.

I’m just stoked that I can’t have my family’s home sold out from under me!

But is it really high income if your cost of living is also higher?

I imagine I make wayyyy less money than you, but where I live (NH / Boston commuter market), prices are surely lower across the board.

For example: moving across the border from MA to NH, my car insurance went from $1800/yr to $700ish/yr. And even with the recent inflation, I’m at $900 and change/yr – still much less than the Boston rate.

My spouse took a big pay cut when transfering from a school just outside Boston to one in NH – she went from $59k to $42k/yr. But she did the math, and everything is so much cheaper up here that it basically evens out. No income tax, her insurance also went down… things like that.

Our household income is just barely six figures but that’s enough for us to live comfortably, even with the expense of homeownership.

Just some food for thought. Btw I know the “just move” bit isn’t always practical… I live where I do to be close to family.

Might be worth it to try offering 2/3 or 3/4 the asking price, like happy Jack suggests, especially if you could offer to the seller directly. I dont know if agents have to report every offer to a seller, even lowball, of if the agent can just refuse and never tell the seller?

There will be some remarkable price drops on houses tomorrow in Tampa that will make the crash of 1926 look minor and there will be an increase in property available with 360 degree water views. Surf’s up!

Not necessarily. Tampa Bay might avoid a direct hit (it hasn’t had one in over a century). The current models show the storm making landfall somewhere between Sarasota and Ft. Myers. That is pretty close actually to where hurricane Ian hit the state a couple years ago – and why that area has probably had the softest housing market in the entire state already.

Perhaps the hurricane season of 2024 will have the same effect on the FL RE mkts as did the hurricanes of 1926.

We who prefer our working folx to be able to afford decent housing without massive guv mint subsidy hope so.

OTOH, the new house across the street, just finished rough framing, listed recently for $1.3MM is already sold according to the builder who was out in person prepping the site today for Milton, hardly affordable.

(In other news, milty just took a more southerly wobble, and as of the 5pm NHC report appears to be hitting the coast between New Pass and Big Pass in the SRQ area, and looked even more southerly in the 8 pm update.)

Greed and fear, as usual. Greed usually wins at the beginning, fear usually wins in the end. Any way to short local housing markets? It would be fun if there was.

Mother nature bats last. I struggle to understand how anyone can afford to live in the path of repetitive hurricanes…

After talking with relatives and friends who live there, it is a matter of perspective and what you fear.

Tampa hasn’t had a major devastating hurricane in 100 years. San Francisco hasn’t had a major devastating earthquake in 100 years. Safe Tulsa hasn’t had a major devastating tornado in 50 years.

A friend pointed out that he has days or weeks to prepare for a hurricane and his house is not perched on a seaside cliff so he doesn’t worry much. You can’t say you have much notice before an earthquake or tornado.

Is any place completely safe from potential devastation?

For us, it was the beauty and isolation of the place. When there were not storms, (99..99%of the time), it was an amazing place to live for many reasons. It helps to be young, and the ability to harden structures.

But once an area is really trashed, (see parts of FL and NC), the community itself changes. There is not enough housing for locals, much less the hordes needed to rebuild. Recovery can be very slow, if at all.

I tend to think about these things in terms of probabilities, not in terms of hundred year increments. The probability of a hurricane hitting Asheville, again, vs. a hurricane hitting Tampa?

@OutWest in parts of the US people live in the path of repetitive hurricanes and “Out West” we have people with cabins on the Russian River and Beach Houses in Capitola with repetitive flooding (flooding about once every decade since their grandfathers built the places 100 years ago).

Excuse me for butting in @outwest but I just wanted to point out wolfs timing on the hurricane and the Florida housing market, a perfect storm. Also he’s probably the only one “out front” turning the narrative on the housing market going south.

Florida sounds like one of the worst places in the U.S. to own a home right now in more ways than one. Inventory is piling up and a major hurricane is barreling right towards it. Someone (in their late 50s) was telling me a few years ago that they bought a home and some condos in Florida with the hopes of using the rental income to “fund their retirement”. I wonder how that plan is working out for them now.

They are probably living under a bridge. Buy high and sell low is no way to fund retirement.

True. They probably are living under a bridge. What makes it even worse is they took out mortgages on the home and condos they bought.

Looks like the pooch screwed Mr Holmes, he gambled and lost. If he would have been a Wolf Street reader he would have been impervious to the pooch.

The Florida housing market prices, peaked at, 485k approx, now 440K.

If gas prices dropped from 4.85 to 4.40 a gallon I would take notice, but if they went down to…say 3.85…

Wolf says the florida “home price” slide downward has accelerated since june so, in Florida, maybe Patience is a virtue…beware the pooch.

No kidding. But the population of Florida keeps going up so these natural disasters and high insurance costs do not seem to be discouraging people from moving there? At least the new residents will be able to buy an affordable home soon now that prices are dropping a lot.

California was like that for many years, until it got “full,” as people perceived it. I think Florida will start leveling out. Texas is huge, so that still remains to be seen.

Texas is full.

David in Texas. So true!

And it will collapse at some point. Too much greed. Feel bad for the normal people owning homes and living in Florida with the cost of hard work and sweat, but investors, snowbirds, airbnbs, “lets buy another one” – they all need kick in the head, and they will get it.

What I’ve learned from this article and comment section is this: if Wall Street Journal calls you about a bad decision you made, decline the interview!

A very emotional comment section, dunking extra hard on naive Florida man. Keep in mind it takes widespread participation to build a bubble like this one. It’s not solely Mr. Holmes’ fault.

LOL! I agree. He has the agency to make his own decisions but this is not entirely his fault. That dubious honor, of course, goes to the worst fed/central bank of all time, led by JPow and the Bailout Boys. It was not unreasonable of him to believe if there there were ANY wobbles in the market (not even actual pain), that they would come rushing to rescue as they’ve done the past decade+. And they may still do so again, rate cuts are coming’ in fast! Maybe even firing up the QE bazooka, too, who knows? You cannot rule that out with those bozos.

I have lost all hope of ever owning a reasonable family home and just hoping to retain a stable rental situation. I just hope that during the last nine months Mr. Holmes had this conversation with his realtor:

Mr. Holmes: I guess I should’ve listed it lower to start with or made more aggressive price cuts.

Realtor: No sh!t, Sherlock!

Most commenters here see charts and think that they the time to sell or to buy is quite obvious: just look at the chart! They don’t consider the context and the sentiment that caused a bubble or a collapse.

Same for blaming the Fed for everything and anything. “Crap. They shoudda done ___” (fill in the blank). The Central Bank learned a very sad lesson in the early 1930s. They wanted to “cleanse the system” – raised rates, thus lowered the money supply, after the stock market crashed. “Clean up” the excesses. So much for that moral gesture.

Not sure about that. As I said earlier, the Fed balance sheet is where it was in May of 2020, but the stock market is double what it was then.

It’s not Fed actions that have caused the everything bubble in the last year or two, but the perception of the Fed put. Enough people believe it, and it feeds on itself into reality.

So the guy in the WSJ article is pricing his home 6% more than he bought it 3 years ago and a couple percent less than his total investment and has a hard time selling? Sounds to me like he’s not “motivated” enough. Not yet anyway.

Note that the graph in the article shows listing prices, not sales prices for the entire state. In the large market I follow in Florida, median sales price and median sales price per square foot is essentially unchanged for the past 3 years.

These kind of sales price figures do not imply any sort of “crash”. Maybe one is coming but it’s not here yet.

I agree that investors could play a big role if a crash does come about. That would really depend though on if the rental market itself becomes softer. Despite all the talk of an “exodus” out of Florida, migration into the state, while reduced since the pandemic, is still strongly positive.

Like the rest of the economy, I would describe the current state of Florida’s housing market as being “in suspension”, with the future direction pointing downwards, but exactly how much downwards is unclear.

If median sales price is unchanged, but volume is down by 50%, that certainly implies a crash, in my opinion.

People typically associate a “crash” with rapidly falling asset values rather than a reduction in transaction volume.

In any case, fewer people are buying because fewer are selling due to being locked in a low mortgage rate. If you aren’t listing your house then you are also not moving somewhere else after having sold your house and buying a different one.

@Max Power wrote” “So the guy in the WSJ article is pricing his home 6% more than he bought it 3 years ago”.

In 2009-2012 I saw at least 100 homes follow this patttern:

1. Listed for peal bubble price

2. Price reduced to a little less than peak bubble price

3. Price reduced to purchase price + real estate commission (often price + 6%

4. Price reduced to exactly what they paid

5. Listed at less than they paid or they gave up and did a short sale or let the lender foreclose

Classic case of chasing the market all the way down…will we repeat it again? Jury is still out for certain regions of the country like NorCal/SoCal. I know couple of people on here have commented they saw this same thing in San Diego last time. With inventory kind of spiking in SD now, will they be the canary in the coal mines for the rest of SoCal? I sure hope so…

Big picture. Enormous amount of business activity (selling, financing, MBS, building, insuring, regulating) is tied to housing. Enormous amount of local taxes depend on housing. Enormous amount of village (it takes a village) culture depends on housing. Nothing changes in housing without some group taking a hit. The number of landscaping firms has exploded. A two employee business (truck, trailer, 2 mowers, blowers, etc) could easily have $250k in equipment financed. Housing business activities replaced manufacturing and farming as career choices. Not a growth sign that Home Depot is downsizing its warehouse space.

As in 2008, when enough acquaintances had told me they were in real estate sales, or had done a cash-out refi to start a business to grow palm trees for new landscaping, or had bought an exurban mini-mansion and refi’d to upgrade granite countertops, etc. Didn’t Bernard Baruch once say something about a shoe polish guy suggesting stocks to buy, as a contrary indicator? If everybody wants in to something, I mostly flee, especially once there is a pronounced momentum. If I didn’t get in early, it is already too late. The swarming crowds are bound to overrun and overdo and exhaust and distort it, while sucking any beauty or quality or serenity out, along the way. It is the cardinal trait of the species in groups.

Sometimes it does feel lonely to be a contrarian, but then I remember something my parents always told me that I have come to call the “Lemming Rule” = “think for yourself, just because everyone else is jumping off a cliff that doesn’t mean you should jump off the cliff too”. It has served me well.

It would be interesting to see a chart tracking how many “real estate agents” there are, and how many hours of “house flipping” TV shows are broadcast. For a while it seemed like everyone was “getting into real estate”. I know a number of people who got their real estate license who had to give up on it because they couldn’t make a living.

Another aspect of being a contrarian is that, either you’re right but the whole time, the world and even yourself is gaslighting you that the position is incorrect so self-doubt sets it along with the loneliness..etc

Or you stubbornly ignore everyone else and are steadfast on being right even though the position is dead wrong, then it becomes a classic case of Dunning-Kruegar…

Yeah ask me how I know about feeling both ways all the time especially when it comes to housing..

Pareto Principle at work. 20% of the agents make 80% of the commissions. Look at the number of RE Agents and the number of transactions annually. Most are not “making a living.”

…climate is what we expect, weather is what we get (…and it WILL weather, whether or not…)…

may we all find a better day.

That be real good, DO!

Some very good information and comments, been looking in FLA think I will wait a bit longer.

I think this board is getting too negative. Florida has had wild real estate swings since about 1890. Last of the boomers turn 60 this year and USA population will hit 400 million in 35 years. Selling a home after a couple years usually loses money. Also Florida has lots of people who want to rent , maybe 10-15% drop but that is not unusual in Florida.

Last of the boomers turn 60, but the oldest of them turn 80 in two years. For every 65 year old retiring to Florida, an 85 year old is likely dying.

Florida dropped by 40-50% in 2009. It’s not different this time.

Wolf needs to re-publish this article after Milton does it’s thing in Tampa. Talk about the insurance liability or lack of any. As a Meteorologist with a Masters in the subject I worked at the the Typhoon warning Center in Guam for 2 years. After that experience and seeing what typhoons can do to housing, I would never buy any property in a hurricane zone, period. With the Gulf water temperatures 3 deg above normal (fuel for hurricanes), you don’t need to believe in Climate Change to see there is some risk here. No one was paying attention. If you look back, I made some posts on this site about the risks here.

Swamp – unfortunately, many are ignorant of the fact that the Laws of Thermodynamics are not subject to governmental implementation or repeal…best.

may we all find a better day.

When I bought my new (antique) house in late 2021, I promptly sold my previous home. I probably could have gotten slightly more had I waited, but I didn’t want the responsibility. I learned a long time ago from my own venture into being a landlord that I just take RE too personally; not a good job/investment for me.

My only regret is that I didn’t refinish the floors in the new house before rushing in (even though we always said we would…)

@MussSyke we refinished the original top nailed hardwood floors in my almost 100 year home about 5 years ago. My advice it to find an expert in the kind of floor you have and remember “skilled labor is not cheap, and cheap labor is not skilled”.

Also, one of my all-time favorite contractor sayings: “Cheap, fast, or good – pick two”

It might be where in Tampa he is. What I can see occurring is have and have nots at city levels. 20 years ago cities were more uniform with suburbs – I’ll assume that is where he lived. Today, some suburbs are vastly and quickly leaving others behind as population changes occur. You could have a home sold for 125k in 1999 sell for 1 million in one suburb and in a different suburb of the same town, that home would sell for 250-350k. No idea but that effect could be in play in Tampa.

A lot of strange things are occurring with how fast, and in the utter chaos in which Americans live today.

Florida attracts the best kind of newcomers, old ones who will neglect their housing eventually, all of South and Central America’s money launderers, and motorheads who scar up and kill manatees. Anyone living on the coast for the long term is denying climate change. As a vacation spot, it’s awesome, until you consider the total environmental devastation, which most of the above people don’t.

I don’t feel sorry for Holmes. The poor and un- or underinsured natives are becoming worse off with each hurricane strike, especially if they don’t have incomes that kept up with inflation. This article isn’t about hurricanes or sea level rise, but surely the demand for the Sunshine State is waning among people who think for the long term. Who wants to deal with flooding every year?

It’s like no one has learned anything since the swamp lot scams that predated air conditioning, or the first housing bubble. There was some golden age there, but it’s not now.

But the warm winters!

Totally. But I’m sorry for the people born there. Not much of their choice.

But these newcomers, deniers, their decision and their risks.

Spoken like someone who is truly ignorant of what it’s actually like to live in Florida. Well done!

I’m wondering if this repricing mentality, between sellers and buyers will ultimately contribute to a shift in investing sentiment.

The irony here, is the story yesterday about a survey suggesting sentiment was turning more positive— but I think that was for sellers being more motivated to sell. In terms of a wider and deeper dynamic — this reality check for reassessing pandemic bubble prices, collides with in-affordable homes, stocks, groceries and is the foundation of many angry people that have a negative outlook on the Vibesession.

Even here at the WolfSteeet campfire there’s a bit of vitriol and nastiness aimed at people who jumped into the housing bubble. So, does this obvious downward pricing trend spill into other things, like stock speculation? Will people buying into various narratives be influenced by watching home speculator losses?

As home prices fall, there’s going to be more hesitation from buyers and sellers, as they measure risk — versus jumping blindly off cliffs. The increased hesitation will add the factor of time back into the overall equation, for buyers and sellers who will hold out for better deals — but the weak over-levered fools that are way over their skies, will fail and time will grind them to dust.

All I know is that stocks are priced at 200% of GDP. I only took undergraduate classes in this stuff, so I’m not an expert, but this is scary.

The vitriol and nastiness is because each person overpaying for assets feeds on itself, and creates the negative outlook that we have now.

Yep. Don’t hate the players, if you hate the game, don’t play.

Rentals can be a good investment with the right tenants, quite frankly, good people should be able to have a solid and safe home to live in. I am happy to provide that for a reasonable price. A stable, safe environment to live in, has value. price is what you pay, value is what you get.

From a study, published by American Economic Association, whoever the hell they are.

“ From this modeling exercise, the authors found that the US economy benefited from the bubble-driven economic booms. They estimated that the combination of the two bubbly episodes permanently raised the level of US GDP by about 2 percentage points.

However, they also found that if there had been no expectations that bubbles would form at all, then the US economy would have grown even faster. The crowding-out effect of future bubbles more than outweighed the benefits of the crowding-in effect from the two bubbles.”

In regard to the Florida housing downturn or stocks being super overvalued — I think the recent upgrade revision to GDP growth is something to be cautious about — primarily because of inflation dynamics, but also, because of historical periods of Excess GDP growth — and hence, these prior bubbles since the dotcom crash.

In perspective, low unemployment seems objectively great, but it also signals that wages are higher and operating costs are higher — and that eventually eats into profits and places pressure on earnings growth.

It’s kinda the law of diminishing returns, where too much success or growth can cause wobbles in stability. I’m always curious as to why Cisco crashed and burned after its massive dotcom supremacy — and that’s a great example of how fragile a Goldilocks GDP growth burst can send ambiguous signals.

As with Florida or housing in general, bubbles simply become extremely inefficient and basically collapse from their own super nova success.

Needless to say, nividia hype is entangled in positive GDP growth, but it’s incredibly dangerous to see it taking total control of the S&P index — which goes back to that study above, the economy will be better off without this concentrated risk.

When these bubbles pop, getting back to normal growth will be much harder.

A lot of people around the world invest in US stocks because they almost always outperform native indices.

Chicken and egg. Are they investing in U.S. stocks because they outperform native indices or are they outperforming native indices because people from around the world believe they’ll always go up and will invest, no matter how extreme the valuations?

What is amazing is Hilton and Marriott are hitting all time highs. Cruise lines are doing great.

The consumer seems to be still spending a lot of money on vacations still. Which makes me think the FED has pulled off a no-landing.

From what I can tell:

Inflation has dropped below 3%. Public companies are doing well. Leasure industry is doing well (airlines, travel). Unemployment is low. Job creation is good. Housing is flat or dropping the past 2 years. Wages are increasing. CRE is the only blemish.

Am I seeing this wrong?

Meanwhile….China’s economy is a mess. Mexico and South/Central America are a mess. Europe is looking weak. Good to be in the USA the past 12 years. Only other area that is keeping up with the US is India?

Bernard Madoff stole over 65 billion dollars and no one noticed. Some of Madoff’s clients claims were dismissed by the court because the client had withdrawn more money than the client had invested. I think luxurious cruises and hotels use the same accountants as Madoff did. I credit the US dollar being a reserve currency as why sloppy bookkeeping is allowed in some areas of the economy and not others.

Anon – if they’re still in the archives, Wolf’s observations years ago on the long-term deterioration of GAAP and it’s uses make edifying reading…

may we all find a better day.

In my opinion, all of that can be attributed to our gargantuan federal deficit. Reduce the $2 trillion deficit to $1 trillion, and all of the indicators implying that we’re doing well will drop like a rock.

Also, services inflation is still way above 3%. My insurance just went up another 15%. I shopped around, nobody can do better unfortunately. Only so many goods I can fit into my 2 bedroom apartment.

George Carlin: You can’t have everything. My God, where would you put it?

Vail resorts season pass sales are down 3% in quantity. I think that speaks to upcoming winter travel. Also I think I read Airbnb’s nights booked are down nationally. I haven’t looked yet, but I’m curious how Disney Land and other tourist destinations did this year summer.

Hotels could be up because of a rebound in business travel as in office and face to face is becoming re-prioritized. They could also be stealing traffic from Airbnb who’s fees have gotten insane. Hard to say. I also have noticed restaurants that used to be packed on weekends being far more empty (in the suburbs, downtown hotspots still need a reservation). One I briefly worked at while between jobs in 2021 so I’m very familiar with what their weekends used to look like.

Is a recession coming or are things just getting back to normal? hard to say. I think there’s at least some mild slowing from the craziness of 2021 too.

Also inflation isn’t defeated. Give it a few months and we’ll have some bad CPI prints.

Also pretty much everyone I talk to complains about being broke or worried about money these days which I never heard 5 years ago. They are all still vacationing though. Haha. Just complaining a lot.

The no-landing scenario is quite plausible.

What concerns me is the ~$105,000 debt per citizen and high deficit spending in spite of that. To me thats very irresponsible and careless especially to future generations. What if we get involved in more wars, for example, or there are more strikes, or another pandemic. We’re not being careful and preparing for hard times that do come, so I cant be bullish about assets. But if we get back to real organic growth, with the govt staying out of market manipulation, we would have a great chance to succeed.

@ru82 it is important to remember that there is not “one economy” and in the “overall” best of times some people are still losing homes to forclosure and going bankrupt and in the “overall” worst of times there are some people making a fortune in real estate and starting new business. As Wolf’s charts above show the “overall” FL market is cooling, but that won’t stop someone (probably a Realtor who is lying) from posting that a home in FL just sold for $200K more than is sold for in 2021 with multiple offers (unaware that a single comp tells us nothing about the direction of the “overall” market)…

Oh no! Normal!

The charts of counts (listings/days on) pretty clearly show a return to the norm of 2019. Now we wait to see where price levels out. It can’t go back all the way down everywhere with everything up up up from 2019. Florida being tag teamed by two hurricanes so closely together may break it. However, that just leads to a bunch of Floridians picking up and blowing up our Midwest real real estate prices even more. Baby BOOM indeed.

Aptly said: He who panics first, panics best.

This reminds me of my friend in San Diego, during HB1, who first listed his home for $760K but after 3 years of chasing down market, finally sold it at $470K.

In 2006,2007, everyone thought come what may, home prices in San Diego can never go down.

If Mr. Holmes’ cost basis is $600k, then selling it for $600k three years later is not just breaking even.

If he didn’t own the house, where would he have lived? He probably would have rented somewhere. How much would rent have cost?

Lets say, very conservatively, he would have rented for $2000/mo. That’s $24k/year, and $72k over three years.

If he sells his house for $528k – now that’s breaking even.

@ShortTLT: You haven’t factored in Property Taxes, Insurance, HOA, landscaping, and Maintenance which are a pretty big chunk of homeowner expenses.

Let’s go with a conservative expense estimate of $20k per year for a $600k home. His break-even is now at $588k not $528k.

He would have paid those things indirectly as a renter.

I didn’t actually look at the property, despite the address being posted above. Now that I think about it, a $400-500k home would probably rent for a lot more than $2k/mo.

The rent would include those costs, you’re double counting.

Also, you’re ignoring the opportunity cost of the $110k down payment he presumably made.

Steve B – exactly. He could have had that $$$ in T-bills earning 5.37% for the last couple years.

Low rates turned investors’ brains into mush, as Wolf says.

“If he didn’t own the house, where would he have lived? He probably would have rented somewhere. How much would rent have cost?”

I like the way you think. If I hadn’t bought my house in 2020 before the madness and rented instead I would be out $150,000 by now with a comparable but crummier house (I have a pool). As it stands after 5 years of property taxes and improvements I’m “down” $46,000k.

I admit we do our own maintenance and that might be an issue for busy young people. This also doesn’t include home insurance which is a ripoff if you’re not in a fire or flood zone.

Even with the property taxes, improvements, inflation and housing busts, breaking even is assured. The only reason I even care about that is leaving something to my kids.

Exactly. If I sold my house for exactly what I paid for it 3.5 years ago, then I just lived here for 3.5 years at “cost” rather than paying market rent.

The only loss is if comp rents are significantly less (as they are in many areas) than the cost of mortgage + property taxes + home owners ins or you had to put money into the property.

In the area I live it would be about an $18k a year loss to rent vs buy if you bought fall of 2022 or later and then sold for exactly your purchase price. Plus a loss of 6% of realtor fees + any repair and maintenance costs or improvements to the property.

So I think it depends what area rents are.

Or maybe a better way to look at it is I’ve made $36k in saved rent + ~$36k in realtor fees (assumes selling at break even), so $72k total buy not buying plus the $10-$15k in interest income (call it $7k after tax), so made $80k in 2 years by not buying and then selling at my purchase price 2 years later.

I owned and leased out a dozen houses, mostly 3/2/2 typical middle class instances, starting a little over a decade ago and ending when covid hit.

People get emotionally attached to the “value” of their house. It is truly an interesting phenomenon that I don’t see with cars or any other asset for that matter.

It’s like people think their house is worth whatever the top valuation ever was with no appreciation of market conditions and no realization that housing prices can and do drop.

If you put a typical house (not something particularly unique or special) on the market and you haven’t gotten at least a serious nibble within 3-4 months, lower your price because you are asking too much and you are just going to ride the price down behind the power curve.

I really don’t understand this mindset.

I own my house and I’m really attached to it – the house itself, not some theoretical resale value. The studs, the drywall, my basement that I’ve spent hours fixing up… they’re all more valuable to me than a number on a screen.

Seriously. I can’t imagine thinking of your house as a mere investment or an ATM. Are people afraid of staying? I mean, there are are lots of places to go, but fewer places to stay.

@billytrip I have been interested in real estate, cars and watches since I was a young boy.

For most of my life people who owned real estate, cars and watches I was interested in would mostly talk to me about how to maintain them and improve them.

In recent years is seems like “most” people buying real estate, interesting cars and cool watches care more about the “value” than the actual real estate, car or watch.

Like with real estate the number of “flippers” of watches an cars increased during Covid and with overall values going down the most highly leveraged are the first rushing to sell.

P.S. For anyone looking to buy a never lived in tract home, never worn Submariner or never driven GT3 RS the number for sale keeps increasing and I predict values will continue to drop for a while…

“For most of my life people who owned real estate, cars and watches I was interested in would mostly talk to me about how to maintain them and improve them.”

If you asked me about my house, I’d tell you about my solar panels, tankless water heater, and whole-home water filtration system.

If you asked me about my car, I’d tell you about the exhaust work and custom tune that I uploaded to my ECU.

If you asked me about my watch, I’d tell you its a 10-year old G-shock that’s beat to hell LOL.

But it would never occur to me to quote the theoretical resale values of these things.

I don’t even know the value of my homes in SD. Never looked it up in redfin or zillow..

I do live in one and just do basic maintenance.

Home is something which provides shelter.

Cars: are appliances to me which can take me from point A to point B reliably, safely and efficiently.

I don’t really get attached to things/objects..

Don’t downplay a Gshock, to watch nerds, Gshock is about as solid as it gets. For watch douche, just go shop for a AP or Richard Mille and Rolex, those are pretty much the only brands on their radar.

Solid indeed. The thing won’t die! And I won’t let myself buy a replacement until it does…

Wolf’s new article 2 weeks from now will be titled ‘Free Homes in Florida, Must bring Life Vest.’

Excellent analysis Wolf. Florida has lots of boom and bust cycles. Tampa is usually a nice place to live and Florida does have the unbelievable demand of 250,000 people moving to it annually. That is a lot of demand to prop up real estate. He is still irrational, but not crazy irrational.

Some clown has his home for sale for $700k. No buyers yet. It was listed in July. He has lowered the price by $1K four separate times. I’m not sue what word best describes this. Greedy, dumb, unwise, unrealistic, clueless?

Meanwhile, up yonder a piece, the inventory virus had spread to Atlanta:

“ With 18,180 active listings, September saw the highest number of available properties in metro Atlanta’s 12-county region in 2024, according to recent data from the Georgia Multiple Listing Service.

Nearly 8,000 of these listings were added to the market in that month alone.”

I reckon there’s a bit of contagion with those bubble values and poor folk pushing back a tad.

Random listing example in an area North of Atlanta.

Sold 1980: 81k

Sold 2017: 450k

Selling 2024: 800k

1 story. No pool. No beach. cold winter, hot summer.

Atlanta has cold winters?

In the RE game, you either buy low, sell high….or buy high, sell higher.

I know which one is easier.

This YoY downward trend is what home pricing in the rest of the country should look like already but it’s clear the Fed isn’t intent on it.

I wonder if the reported economic troubles in China has lowered the pressure they historically exert as international buyers. I’ve also read reports on Airbnb oversaturation and fee fatigue coming home to roost and lowering monthly profits for some of the 2022 purchases.

With these in mind, how long before long-awaited downward adjustments become the norm in more metro areas? Because without deflating some of this bubble I expect we’re looking at over a decade of impasse.

Regarding the state RE figures, this may be nonsense but I’m curious. I see where some large condo buildings are facing huge fees for inspection and remediation to their buildings. If one such building with 100 condos gets into trouble, and the owners can’t afford the fee assessments and decide to sell, do those get broken out in the overall state sales figures or are they all lumped together. Just curious if those big condo buildings have any impact on the overall Florida RE trends or if they are just a tiny data blip.

Thanks for great reporting not available anywhere else!!!!

If it’s a regular sale, or listed for sale, it’s in the figures. I’m not sure if foreclosure sales are included in these figures here (if foreclosures become something more than minuscule, I’ll look into it; but for now, they’re so tiny, they don’t matter). Some indices remove them.

The issue of older condo buildings in Florida is now huge. But this will drag out, maybe for years. There are court cases going on. Huge amount of uncertainty hangs over it. But note, this affects only older condo buildings, not those built in the past two decades.

No story here. The pattern is work from home is being curtailed, so job rich areas like NYC, LA, Boston, Chicago, … are seeing a lot of residents move back from places like Florida, TN, and all the pandemic hot spots. So, real estate weakness in some areas and strength in others.

Inventories are rising everywhere, but they’re rising faster in Florida and Texas than in other places.

The problem is that demand has vanished.

inventories are even rising in California:

In 2008, layoffs everywhere. Inventory rose and people cut prices. They had no choice because if was difficult to rent a property, especially for a profit. Their only option was to sell cheap.

Now, in job rich cities, you do not have to cut your price. You can rent it for top dollar, easily, and this is especially profitable if the mortgage was struck at a sub 4% rate. So, equity is borrowed for a new property, and the old property is turned into a profitable rental.

Now, if the job market turns weak, and rentals go vacant, this will all end, and you will see a flood of inventory with drastic price cuts. We will see. I don’t think this will happen because the FED will never get that agressive … they seem to be willing to tolerate inflation.

Sounds nice in theory. Just look on Zillow, how many houses were put on the market, failed to sell, were pulled off the market, then showed up as a rental listing for a ridiculous rent, failed to rent, then eventually showed up as listed for-sale again at a lower price. Because rental demand isn’t that huge, and there’s lots of supply, from all sides, and now this new supply is getting thicker from people who can’t sell their home for what they want, or can afford to sell it for what it would bring.

Boston specifically is at about 30% yoy inventory growth.

Demand in some places is vanishing – it’s so local all this stuff. Where I am there is the clear beginning of wealthy towns and the not towns. Even formerly wealthy towns may find they slip back. That will probably drive the long end of the tail longer.

Washington DC has all these people who supposedly monitor this stuff and it just goes off the rails everywhere you look into it. I don’t think they know what to do anymore in a number of key areas.