The big divergence. Here’s what’s going on.

By Wolf Richter for WOLF STREET.

For well over a year, there has been somewhat of a puzzle: How financial conditions, as tracked by broad measures such as the Chicago Fed’s National Financial Conditions Index, have been getting looser since March 2023, and are now at the loosest level since November 2021, even though the Fed has hiked policy rates to 5.5% at the top end and engaged in $1.7 trillion in QT so far in order to tighten financial conditions. Powell has been pushed many times on this point during the FOMC press conferences.

But financial conditions are not getting looser everywhere. Bankruptcy filings by larger corporations reached the highest level in 13 years. There is some trouble at the low end of the junk-bond market and the leveraged-loan market. And Commercial Real Estate is stewing in an epic mess, entailing countless defaults and massive losses for equity and debt investors and for banks, with the result that credit has tightened around its neck, so much that refinancing maturing loans got very difficult or impossible, leading to numerous repayment defaults, and many multifamily construction projects are now on hold because they cannot get financing.

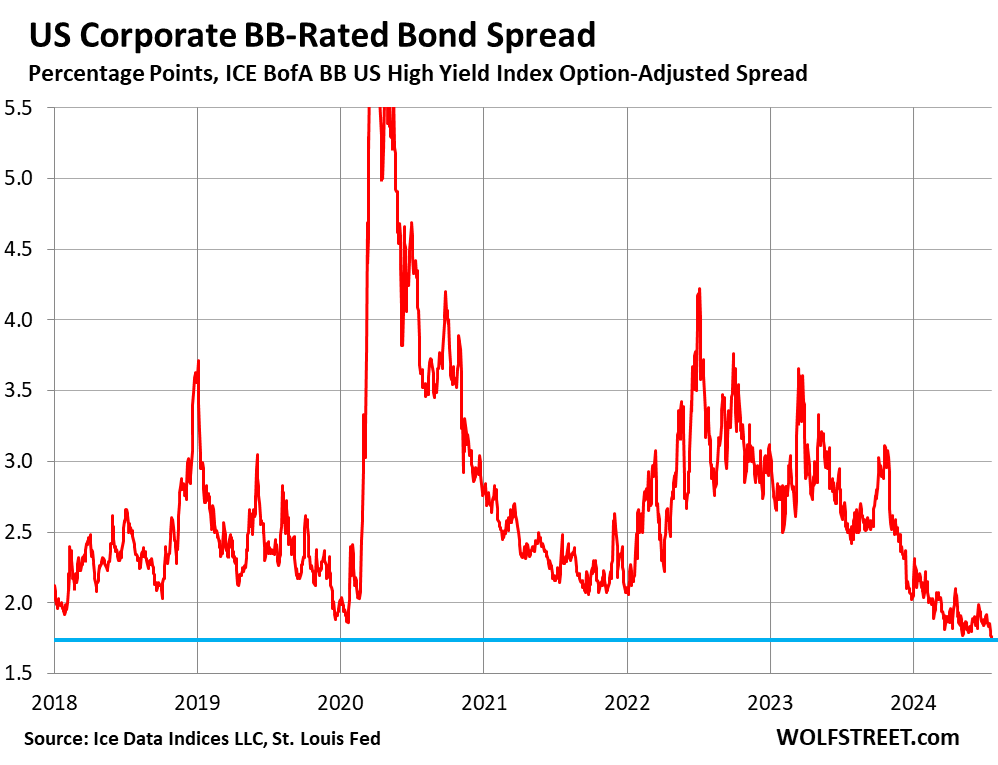

But the higher end of junk bonds is in la-la-land. Spreads of BB-rated junk bonds have narrowed to just 1.75 percentage points as of Friday’s close, according to the ICE BofA BB US High Yield Index released today, the narrowest since 2007! BB-rated bonds are at the top end of the junk-bond spectrum (here’s our corporate bond ratings cheat sheet). In other words, BB-rated debt has moved even deeper into la-la-land, under massive demand from investors.

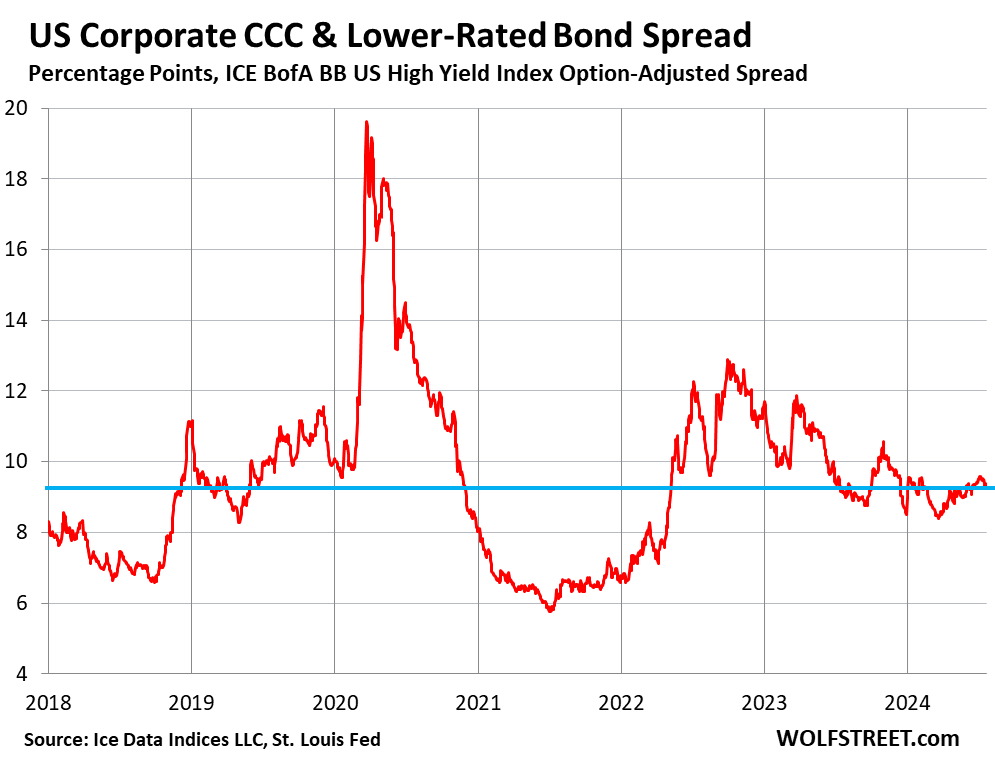

Lower end of junk bonds in purgatory. Credit spreads of CCC-and-lower-rated bonds, the low end of the junk-bond spectrum just above “default,” have narrowed since October 2022 to currently 9.3 percentage points over equivalent Treasury securities, according to the ICE BofA CCC-and-lower US High Yield Index. But that yield spread remains substantially wider than during the Good Times, as bankruptcies and threats of bankruptcies have been accelerating.

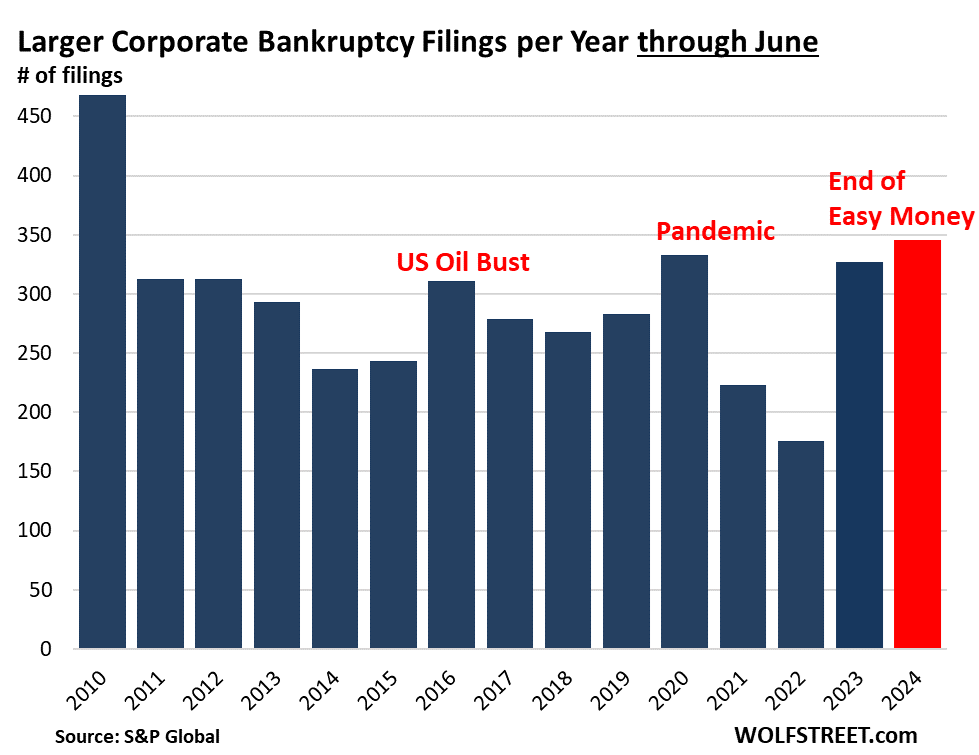

Corporate bankruptcy filings edged past the pandemic high, to 75 filings in June, the highest since 2010, by publicly traded companies, or by private companies with publicly traded debt, according to data by S&P Global. These levels of bankruptcy filings are still not high compared to the mayhem in 2008 and 2009, but they’re now higher than during any month during the intervening years.

We looked at two of the June filers, as part of our Imploded Stocks, both among the largest filers last month: Chicken Soup for the Soul and EV SPAC Fisker Group.

In the first half of the year, 346 companies filed for bankruptcy, also the highest for any first half since 2011, just a tad higher than in the first half of 2020.

Companies file for bankruptcy because they cannot get new funding to service their existing debts: Under the supervision of the court, the company is either liquidated, with creditors getting the proceeds from the asset sales; or is able to restructure its debts, which usually wipes out equity investors, transfers ownership to creditors, and leaves some creditors with haircuts. Growing bankruptcy filings are in part a result of tighter financial conditions, when investors lose some of their exuberant appetite for funding risky companies with more debt capital:

Leveraged loans: distressed debt exchanges surge. Leveraged loans are loans issued by junk-rated companies that banks originated but sold to investors, including to loan funds. Some of them are securitized into Collateralized Loan Obligations (CLOs). And they’re traded, and there are indices that track them. It’s a big market, roughly similar in size to the junk bond market.

PitchBook’s LCD produces a dual index of default rates for leveraged loans: one that covers hard defaults only; and the other that includes distressed debt exchanges that occur without defaults.

The issue here is that distressed companies, holding the bankruptcy gun to their lenders’ head, talk their lenders into the potentially lesser evil of restructuring those loans with a substantial haircut for the lenders, which reduces the company’s debt load. With a distressed debt exchange, the company bypasses default and bankruptcy, but with a potentially better and more controllable outcome.

Distressed debt exchanges are an alternative to restructuring unmanageable debts in a bankruptcy court; they’re a form of default but are not always included in default rates.

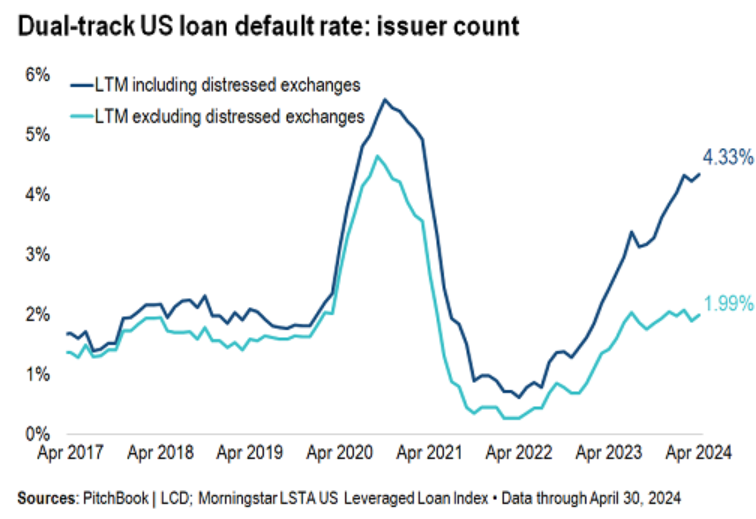

In June, the default rate of leveraged loans, excluding distressed debt exchanges, ticked down to 1.55% by issuer count, back down to roughly pre-pandemic levels (light blue line).

But the default rate that includes distressed debt exchanges was at 4.31% by issuer count, more than double the pre-pandemic levels. This indicates that companies at the low end of the corporate credit rating scale are having substantial difficulties, and also that lenders are willing to make lesser-evil deals to keep the companies out of bankruptcy court where lenders could fare worse (chart via PitchBook):

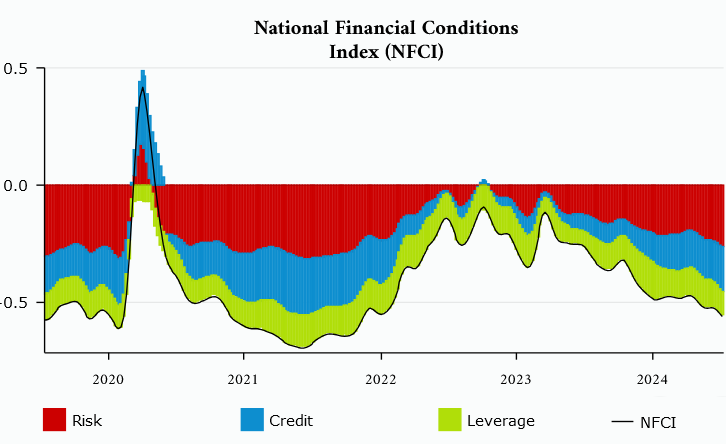

But broad measures of financial conditions move even deeper into la-la-land. Overall measures of financial conditions in money markets, debt markets, and equity markets have been loosening steadily since March 2023, and last week dropped to the loosest level since November 2021, when the Fed was still doing its near-0% policy and massive QE, according to the Chicago Fed’s National Financial Conditions Index (NFCI), which tracks over 100 data points.

In November 2021, the Fed had just started to talk about tightening its policies. That talk and then the first wave of rate hikes caused financial conditions to tighten, which peaked in October 2022, then wobbled along those levels till March 2023, after which they began to loosen again. This is the Chicago Fed’s NFCI, showing that overall financial conditions – despite the mayhem in some corners – are as loose as they had been before the pandemic.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

How interesting…. much like our societal structure, there seems to be a large historical gap between the have and the have nots..wealth gap is the highest in modern history, this seems to be the case with Corp America as well, the divergence between Mag 7 and the rest mirror this pattern as well…perhaps not by accident.

Thus what rotation.

I’m very concerned about the gap in competitive advantages (and access to capital) facing smaller businesses. I want my dentist to be a local office, not the result of some “roll-up” by remote private equity oligarchs squeezing the local character, life and soul out of it. This is not a new issue — I recall WalMart being complained of, decades ago, in terms of the effect on towns. I can’t stop evolution, but this mismatch in stock holdings is perhaps another sign of this? Maybe it takes a sector downturn to shake out the “me too” investing concentration. Something like that happened around 2001. But would the Fed ride through that? When would it deploy a rescue (with all the moral hazard), and after how much damage to the smaller firms?

Great article that cites so many of the incongruities that currently exist in the equilibrium that currently exists. While un- sensationally capturing the nut, the kernel.

The absurd mis-pricing of the equally powerful negative side of average.

The word is devolution. Just because it’s the latest doesn’t mean it’s the greatest.

@phleep the private equity oligarchs have been slowly working to eliminate small business for my entire life. Every year there are less and less small banks, CPA firms, dentist offices and restaurants. The ruling class hates small business owners and is doing a great job replacing them with “workers” (who need a job to pay off their massive student loans).

Regarding private equity buying dental offices as well as medical practices, I know a lot about this. A lot of factors have caused this trend:

1) Enticing immediate cash up front offers for these owners of medical practices

2) Burned out, overworked dentists and doctors who are getting reimbursed less every year. Everyone else’s wages go up, but theirs go down, or they have to work twice as hard to make the same money as 10-15 years ago.

3) Increasing red tape, billing and compliance issues with owning the practice. Headaches.

4) Millennials who are the new dentists/doctors coming out don’t want to work that hard. And they are in debt up to their ears. They certainly don’t want to “buy in” to become partners or take on new debt.

5) Due to #4 above, many dentists/docs, say, in their 50’s will not be able to sell their practices to the new generation millennials. So—bingo— here comes private equity with a big check to buy their practices. A match made in heaven.

Of course the patients are the big losers in the end.

“The ruling class hates small business owners”

B.S. More like investors find ways to make money, and buying small businesses is another way of doing so.

Money pools up via PE and various forms of funds in ways that weren’t so common awhile back. That’s been the driver for this change, not some “ruling class” with a plan….

So what does commentor Gatto think the purpose of the Heritage Foundation (and it’s similar ilk) is?

@phleep

pp. You must love Big Retail. It’s not enough to shop there. Please proceed to Room 101.

Wolf,

Not to get apocalyptic, but the more I read about parallels to 2007 the more concerned I get.

I rewatched The Big Short last night and was struck at how the disconnect between fundamentals and technicals played out in early 2008 with mortgage bonds.

Timing is always extremely difficult, but do you think the size of the debt pool at risk is large enough for this to get into contagion (not asking if it will happen, more like if you see big neon red lights)?

I know you asked for Wolf opinion. Let’s see what he says.

I have been in the banking world since 1988, primarily in SW FL. The GFC was caused by lax lending standards in the housing market, rating agencies looking the other way, financial engineering on WS and overbuilding. Since 2010, mortgages are hard to get, everyone refinanced into 3% rates during Covid and UE is at 4.1%. For those reasons, this is not 2008. Housing prices may move 5-15% lower, but this is not the GFC.

Tim,

Thank you for your insights, and I agree with you that single family lending will not be the epicenter of the next crisis.

If I had to guess, I would expect corporate bonds will be.

Usually the thing that causes the last crisis doesn’t cause the next one.

It’s always the punch you don’t see coming that knocks you out.

“Everyone has a plan ’till they get punched in the mouth.” Mike Tyson

A 15% move lower in housing prices combined with ~3% inflation for the next 4-6 years means houses will lose a LOT of value by the end of the decade. And they need to to be affordable again.

there’s never one cause. you can always point to a past event, find some causes, and say that it’s different because those causes aren’t there.

but people being overlevered is a common theme in america. how long can people with their 3% mortgages pay them if they lose their jobs? with unemployment at 4.1, houses won’t drop much, but what if unemployment rises to 6? or even 7 or 8%

the main reason the spreads between junk and treasury is so tight is that the market is absolutely convinced that recessions are a thing of the past, and that they’ll be replaced with inflation and printing.

if every recession results in stimulus and printing, they’re probably right.

Franz,

re Unemployment and housing comment

US calculates unemployment using “those actively looking for a job” to engineer the stats lower to a 4.1% rate. If calculated as per Canada it would be at least 5.1%. Canada is at 6.4% right now using the all people not working criteria. U rate is at least 1.3% higher here, but there is also no worries about maintaining medical coverage etc as it is provided. My point being is that the locked in 3% is what is keeping housing prices from a collapse in the US, and not so much the unemployment rate. This year at least 70% of Canadian mortgages are coming due as the max term is 5 years. So far, housing price reductions have really yet to hit. Sales are way way down where I live, but no one has reduced their prices beyond a token cut. We’ll see?? We might be the canary.

If people can’t pay a mortgage at 3%, even if they lose a job, try 18% which many of us went through in the early 80s. This situation is nothing. people just bought too much house for their position, or as my Dad used to say, “live a champagne lifestyle on a beer budget”, and thought it was normal.

Unemployment rate up here increased to 12% in 83, and probably to 15% where I lived. I sold my house to move for work after working away for years and still broke even not counting sweat equity. There are many solutions to hard times for home owners like renting out a room, converting a basement, quit dining out, only shop sales, no vacations. etc etc. My nephew is a renter in Victoria and is madly looking to move, find a room mate, or even relocating. There is a long way to go before a collapse. I’ll believe it when ‘skip the dishes’ is a distant memory and people ask what is exactly a nail salon?

Maybe Govt supports will no longer be possible with continued currency debasement? There will come a point……

Paul S,

“US calculates unemployment using “those actively looking for a job” to engineer the stats lower to a 4.1% rate.”

Jeeesus. The US (BLS) has SIX unemployment rates, from broadest (U-6) to narrowest (U-1); You picked U-3, the red line. “…to engineer the stats lower to a 4.1% rate” is stupid BS.

Paul S: Brampton is in the bellwether GTA. A condo sold there in last few weeks for 237 thousand less than it sold for in 2022. It sold over list, of course, in the high 700 s in 2022 and has now sold in the mid 500 ‘s. It went through nine listings/reductions to get there.

I’m kind of a layperson here but I’m still skeptical of the argument that ’08 was caused by subprime and lax lending standards. I think that was the proximate cause of the collapse, but the ultimate cause was the fact that housing was in a bubble to begin with, and “anything that cannot go on forever, will stop.”

The way I see it is that the driving force in a bubble isn’t the price itself; it’s the direction the price is moving. Nobody is worried about the price going up, but if anyone starts to suspect that it might go down, then it’s possible for a mortgage that is entirely affordable to still not make sense to hold. It’s only in that situation that the fact you overpaid – regardless of whether you’re making the payments – come to the foreground, and then it becomes a question of whether you want to “realize” that loss by continue to make those payments. If you *weren’t* in a bubble then you could reasonably expect fundamentals to place some kind of floor under you and for the price to eventually rebound, but in a bubble, driven by irrational exuberance, there is no such guarantee (or at least there wasn’t until the Fed decided to backstop the whole thing).

Instead of saying that we aren’t in another 2008, I think it’s more likely that we are, but that this time around people are reasonably betting that the Fed will print their way out of any correction, and the resulting inflation will eventually make those prices “real”, in the sense that the lenders will increasingly be repaid in devalued currency.

“people are reasonably betting that the Fed will print their way out of any correction”

The bubble is the money. They let the cancer spread to the rest of the body after 2008 because power is important. Money could be considered the heart of the body, and money is now a bubble. So this will be worse, much worse then 2008.

Matt B,

You are starting to channel Ray Dalio. He has been talking about how historically governments print their way out of big debt situations. Because it is the easy thing to do.

That has been the result of every one of these big debt scenarios for the past 500 years.

Excellent observation and well done.

Mortgages hard to get? Maybe harder than fogging a mirror, sure — but they really aren’t anything like hard. People are still being shoehorned into more mortgage than they can realistically afford.

Loan Officer here, I can tell you it is absolutely hard to get a mortgage. Young folks cannot afford the prices, even if mortgage rates were to decline 1%, everything in my market is still unaffordable. On the back end, once the loans are sold off, we’re seeing more buy-back requests and defaults than ever, since I began in the industry back in 2011.

Not sure if you’ve applied for a mortgage recently.

In 2020 when I applied for mine, I had a big ($100k) down payment, yet I had to jump through all these hoops to prove to the mortgage originator that I didn’t fake the money in my account. That was in addition to all the income verification etc.

I was borrowing as much as they’d let me based on my income, which was (part of) the reason for the large down payment.

Tim, although everything you say about lax underwriting is true, the actual catalyst in 2007 was affordability and running out of buyers. Once buyers stopped buying, the weak underbelly was exposed and the rout was on. If not mistaken, today’s SFR market has an even lower affordability index compared to 2007. Perhaps this time the flood of inventory will come from corporate SFR investors and AirBnB investors? I know a couple of local AirBnB investors who are throwing in the towel – they can’t get the top rates anymore and vacancies are exploding. In some local neighborhoods in the Coachella Valley, up to 25% of all homes are short term rentals.

Well in that case, just be a landlord in SoCal. Just like the greedy one that I have to leave behind in Long Beach. Apparently you can charge close to 17% increase to close to $5k for a mediocre townhouse and still get showing lined up.

Don’t be a greedy AirBnB owner, be a landlord that operates like a AirBnB owner instead and get maximum top dollar return and not even bother to fix up the place, then lock your tenant in a yearly lease and go up as much as the market will bear every year..

This is exactly what I also believe is going to happen, especially once there’s a recession. Many of the corporate SFR investors and Airbnb investors are going to flood the market and there will be a glut of homes on the market.

Greedy landlords??

Why would I leave some good money behind when I could pick it all up and be Mr money bags.

Why should the landlord get all weird and give you a break, either fork over the doe or be gone with you.

I had a friend who would call gram for money when he was low, his name was Patrick. When he wasn’t begging gram he was outside Taco Bell late nite begging for free tacos, I liked Patrick.

So in summary, don’t give Patrick tacos or discount rent, don’t be like gram, or Patrick will come calling.

That is amazing Tulip… I watched The Big Short last night too! My Dad and I watched it for the first time. It wasn’t as humorous as the TikTok clips made it seem.

Moreover, this post by Wolf just reminds me of how wrong (and how often) the Masters of the Universe get it on Wall Street. Whether it is the 2005-7 housing market, the incessant belief that the Fed is going to cut interest rates, or the scarping up of distressed Junk Bonds… how do these guys keep their jobs???

The biggest concern following the GFC is that no one was punished, and in fact the same people got promoted.

This helped to reinforce that aggressive risk taking was fine, and that the Fed/government would bail you out if you didn’t go full Bernie Madoff.

What it likely means is that in some corner of the financial world is some unappreciated major risk that some unexpected development (geopolitical, natural disaster, etc.) tips off that causes a full blown meltdown.

@SpencerG good to hear that you are watching movies and talking about the market with your Dad.

@TulipMania & Spencer on Wall Street you get promoted for making money, firms don’t care what happens to a pool of loans you originate and securitize or a firm you take public as long as you make money originating and securitizing the loans and taking the company public. As I have mentioned before I don’t see AirBnBs (aka STRs) having a big impact on the overall real estate market since most of them are owned by the “working rich” who want a vacation home in Tahoe, Aspen or Nantucket and are just renting it for some extra cash when they are not using it. The majority of STRs are in nicer than average locations and will have people that want to buy most of them if the current owners need to sell (unlike the entire neighborhoods of crappy new homes owned by flippers in 2008 that were rushing to sell at the same time)…

Margin Call is worth checking out too if you haven’t seen that one :) People always say this time is different, until it’s not. Hard to know when that will be though. Also it’s usually a slightly different bubble.

Where I see the a lot of risk in housing is the significant number of airbnb’s, if travel dies down a lot of people won’t be able to cover their mortgages. Will it be enough to move the whole housing market, hard to say. Local markets with high airbnb concentrations like Denver though could see a big influx of inventory.

I intend to watch that one next.

Nah, this time is different…people are saying it like the Ten commandments in SoCal. It also help their case seeing less than $1M house still being snatch up relatively quick further re-enforcing their belief that this time is truly different.

A lot of people also truly believe that with Sept rate cut, their zillow value will go from $1 to $1.5M in the next round. MSM is already gearing up narrative that loan application spike in anticipation of Sept rate cut..perhaps this time is different sadly..

In Oakland CA there are 1,961 places for rent on Trulia and 680 full apartments and homes available on Airbnb.

Here in the Coachella Valley the early signs of AirBnb investors throwing in the towel are just starting to appear. I know a couple who have given up due to surging vacancies and crashing rates.

My wife and I travel fairly often. A few years ago we always stayed in AirBnBs. Prices have gone up so much that today we don’t even bother looking at them.

Risk, that hard to nail down, butterflies in your stomach, butt cheeks tightly clamped, has been on sale by the world’s governments in programs like QE, for more than 15 years but less than 1 million.

There is an eternity of time to sell before the final bell is rung, settling the price that all financial positions are valued at.

Almost every human that ever lived has considered themselves smart enough to get out just before the price of an asset falls precipitously.

Not just that “dangster”, when it gets into the blood of its victim, this fever, having won hundreds or thousands so easily.

Patience is not an option.

I had a friend who came to see me, he passed through Vegas, when he got here he had no money. He told me that the dolphins were jumping. The slot machine he was playing had blue dolphins, when the dolphins start jumping it was his time to make larger bets, so he claims the dolphins tricked him and took his money.

What really happened in March 2023?

Not sure if this is a tricky question. Feels fuzzy after all those years (1y) :).

But at that moment the inflation was not considered transitory. Delayed but firm Feds reaction. Investors were convinced that the new rates will bring a recession.

Opps, fuzzy! Please ignore ^

I have a slightly different POV than “the Fed thought it was transitory”.

Even the Fed understands that if the wage structure allows a family too purchase a home, priced within the credit limits. Which as it should be.

Trumps first term, Yellen finally began the process of removing the economic adrenaline of QE. The slow but systematic increases in interest rates, potentially, could have slowed the popular economy before New Yorks finest took over.

Trump fired her ass and found himself a conservative employee as Chair who immediately re-instituted QE after a tongue lashing by Trump at the White House which is the gossip I heard.

Fed overreaction to the Silicon Valley Bank situation. They and the FDIC showed that they will do everything in their power to privatize gains and socialize losses.

Among other things, the Fed, Treasury and FDIC demonstrated that they were willing to move heaven and earth to bail out a bunch of tech idiots who kept their operational cash in uninsured deposit accounts in a systemically unimportant bank.

ah yes raising the FDIC deposit insurance limit to infinity..

almost. It wasn’t that the tech bros were idiots, they didn’t give a shit. Arrogance is often misinterpreted as innocence, allowing bully, monsters too roam freely.

If you can avoid the limited number of companies who actually file for bankruptcy, 15% return look pretty good.

Reminds me of the Spartan’s response to Alexander the Great’s father demanding their surrender. “If I conquer your city, I will destroy you all.”

The Spartan response… “IF”

Your comment has stimulated the metaphysical tendency that we have evolved with, called love.

Every time I try to internalize history, I can’t help defaulting to those poor bastards.

Re: “ distressed companies, holding the bankruptcy gun”

Perhaps the tsunami of zombies with bankruptcy guns, is the behind the scenes show that’s helping the extend and pretend cycle to continually, sustainably lengthen the mysterious and missing lag effect.

Perhaps the bankruptcy gun is simply leverage not unlike covenant lite — where two parties continue to agree to on the fly solutions to both of them losing cash.

Be that as it may be in theoretical fantasyland — seems like the growing wave of zombies with guns are pirates that will eventually sink more and more ships.

At some point, too many pirates cause economic harm …

Pirate contagion will result in greater risk to the crown.

Nope. Your entire theory is nonsense because you missed the most important part in the section of the article: a distressed debt exchange is NOT “extend and pretend.” In a distressed debt exchange, lenders accept reality that their investment has lost a big part of its value. In a distressed debt exchange, lenders STOP pretending. In a distressed debt exchange, lenders agree to a big haircut, maybe a 50% haircut, maybe a 70% haircut, which means that the burden of that loan is reduced by 50% or 70%. And the company is less burdened with debt afterwards. A chapter 11 bankruptcy filing can accomplish the same thing, but outcomes are uncertain, and the procedure takes a long time, making an ultimate recovery more difficult.

Maybe that ICE BoA bond index would perform better if it switched to EV?

Personally, I would stay away from any bond longer than one year with a government guarantee.

What is the downside of a guarantee of a 5+pct while waiting for the chaos to resolve itself.

The bond market is in disequilibrium. The constant flow of the US Treasury spending while the obese Federal Reserve balance sheet is a source of liquidity.

Which is being used to under-price risk. The budget will eventually matter

“Personally, I would stay away from any bond longer than one year with a government guarantee.”

Although I mostly agree with this, I’m pretty happy with my 10-year, 5.98% Fed Farm bonds that I paid basically par for.

Nice, I actually laughed out loud.

Perhaps a good topic, Wolf, would be to dig deeper into financial conditions. There are various measures, right? How do the calculations differ? It looks like FC are loose re spreads, but the absolute level of rates is presumably restrictive. Can you help us think this through?

The allure of purgatory and chasing yield — speculators are conditioned to feel comfortable with greater risks — exactly like frogs bathing in soothing warm water, in kettles, surrounded by flickering candle light, enjoying the warm feeling of a little wine — and sweet lullabies helping their eyelids grow heavy. RIP

The sustaining feeling, like the tulip holder in the 16th century, is current capital gains.

The word bankruptcy is derived from Italian ‘banca rotta’.

After study, I’ve discovered not to long ago if one went bankrupt 3 times they would be killed, Genghis kahn was like that.

At present going bankrupt is common. it also appears going bankrupt could be the the long term objective, our country is on that path now.

As this article points out, the CRE is bankrupt. The outflows exceed the inflows with no prospect that anyone might be interested in leasing their albatross.

No matter that just a few generations ago the CRE was considered iconic and representative of something new.

So many warehouses built recently in the greater Philadelphia region. How could a region need so many new warehouses? Maybe we don’t. Maybe investors built due to low borrowing costs. And now there is oversupply and CRE lease costs have to come down. Sure work from home is part of it. But around here it is oversupply. The newer facilities simply take tenants from older buildings, unless the older places cut the rent. Some will have to walk away. Again the pandemic stimulus (low rates) was not so good an idea – in hindsight. When I got my 1st stimulus check, I was willing to spend $82 for a gallon of Home Depots finest paint. We all spent too much willingly and we still are. We spend and spend yet complain about inflation. Ugh

I wonder how much of the ware house space is replacing the brick and mortar buildings from retail ?

Which in turn are being turn to mixed use residential/service oriented commercial building. Everything is in flux, and demand is being met on all sides by supply of new product

You are overthinking the situation rather than approaching the issue in a multidisciplinary fashion. For instance, hindsight obviously, haunts your everyday interactions.

The rubber band stretches, until it breaks.

The story never changes.

DM: Bankrupt California EV maker Fisker is selling its inventory of luxurious cars for enormous discounts as it clambers for cash

A California EV maker once worth $8 billion has been granted the ability to sell their cars at a massive discount as they’re desperate to raise cash.

Their vehicles were made by a contract manufacturer in Austria, but they stopped making them earlier this year. This company is liquidating:

From June 19: https://wolfstreet.com/2024/06/19/the-collapse-of-the-ev-spacs-fisker-joins-the-bankruptcy-party-others-on-the-verge/

Excerpt:

Fisker never made it to true mass-production. It didn’t even build its own vehicles – they’re made under contract in Austria by Magna Steyr, a subsidiary of Canada-based Magna International. The batteries came from the Chinese battery giant, CATL. Fisker started selling its Ocean SUV last summer. In 2023, Magna built 10,000 of them. But amid reports of all kinds of quality problems, Fisker was able to sell less than half of them in 2023, and promised to sell the rest in Q1 2024.

At the end of February, Fisker warned in a filing that it might not be able to “continue as a going concern.” And it said that it was in talks with a major automaker over an investment in the company and a joint production deal.

On March 18, Fisker said it paused production of the Ocean for six weeks. At the end of March, Fisker slashed the price of the SUVs by as much as 39%, hoping to sell the ones it still had, though it was no longer producing new ones. But it’s hard to talk people into buying a vehicle when the company is about to collapse.

And on March 25, Fisker said that those talks with the major automaker went nowhere. The New York Stock Exchange then delisted Fisker’s shares, due to their nearly worthless nature – just a few cents at the time. The delisting put Fisker in default on its $180 million in convertible notes. Throughout, Fisker has been laying off employees and closing facilities.

On May 3, Magna International said in its earnings call that “production of the vehicle is currently idled,” and its outlook “assumes no further production.” On May 7, Fisker’s Austrian subsidiary, Fisker GmbH, filed for bankruptcy in Austria. On May 19, Fisker closed its headquarters in California. And so that was the end – sealed by the bankruptcy filing.

Fisker himself used to be with BMW and led the design team on the Z8 in the early 200s and he should have know how difficult it would be to create a new car company that would be in any way competitive or profitable and now it’s another predictable collapse.

Yes, he should have. So should have John DeLorean. He was an engineer at Chrysler, Packard Motor Company, and then at GM where he designed the Pontiac GTO and eventually became the head of car and truck production for all of GM. Of all people, he should have known how much money it takes to start a car company and mass-produce a vehicle. And he probably knew, but he assumed that he could get the money, year after year, from investors. But he didn’t.

Picture perfect example of the “Peter Principle”.

…re: John Z. – cue the old SNL ‘Bisquick’ sketch…

may we all find a better day.

In today’s world, not one in 100 people understand money destruction. They do not know what it is, or how it works. They did not understand it in 1928 either, but by 1933 everyone understood it, and it changed their opinions about debt for the rest of their lives.

So, a Great Depression like collapse of a debt bubble like today, Unlikely but maybe.

The problem now is that most people can not simply return to a self-sustaining lifestyle. as people could in the 1930’s. The global depression lead to world war two, and an additional 20 million+ people were eliminated just the same. What was global debt back then? What is if now again? War is another way to deal with debt problems I guess. People/countries will pretend all these companies/governments are solvent/matter so long as it suits their interests, then they won’t. Nothing new under the sun folks. Everything is different until it isn’t, like the path to bankruptcy, slowly, then all of a sudden.

Interesting times.

This is exactly what I also believe is going to happen, especially once there’s a recession. Many of the corporate SFR investors and Airbnb investors are going to flood the market and there will be a glut of homes on the market.

Every last STR is ready to be put up for sale when the worm turns, all of them staged to some extent, and glut the market.

XC,

“ all of them staged to some extent”

That’s the interesting contrast to GFC, when tons of people were willing to walk away from homes that needed upgrading with more deferred maintenance. The supply of cheap deals helped speed up a recovery to some extent — whereas now you have a huge supply of overvalued, staged Airbnb STR with owners that will be reluctant to take lowball offers — which will extend a downturn.

Plus, there’s a small case to be made that done STR have turned enough profit to be able to wait out a downturn. However, increasing cash burn and a slower economy is gonna make that a very hard environment to survive in.

I think the eventual prospect of contagion plays a role too, with substantial increases in inventory and less income for STR and CRE— the stars that aligned for the bubble are no longer in alignment!

How high rates should go should be determined by Financial conditions and not by some absolute numbers. As FED’s own indices have shown, Financial conditions were never sufficiently restrictive long enough to root out inflation.

Overall quality of life is impacted because Services became very expensive in last 2-3 years. Day care and Child Care has doubled. My kids Summer Camp cost have literally doubled in last 4 years. My family expenses with same life style have gone up 30-40% in last 4 years. Auto-Insurance with best track record have gone up 30% in last 4 years. Before people jumping on asking me to shop around, I have done that. Still my current provider is still lowest but much higher than what I was paying.

FED has been fooling us all along for last 2-3. After 2-3 years of high inflation, now price increasing have come down in range of 3%. FED is calling Victory.

In 2022-2023, when Markets were not getting message, Powell was pushing back on narrative. After 2023 Dec, Powell is not pushing back on rate cut mania by Markets.

FED has been signalling rate cuts are coming for few months now. In March 2024, Powell told Congress we are very close from easing. Q1 2024 numbers were discouraging. But Q2 numbers promising. So rate cut mania back. This is third year when our rent is going up by 10% after negotiating with landlord.

that’s why the target is really more like 5%, because it’ll be 2-3% during the good times, and 6-10% during the bad times. it’ll even out to 5%. the markets just don’t realize it yet, which is why they are buying 10 year treasuries hand over fist for 4.2%

This article is a great summary of things that keep me up at night, that are under followed by most financial journalists.

Patch: 54 CA Big Lots Stores To Close Amid Financial woes

Following a grim financial report, Big Lots has designated about half of its California stores for closure. Prior to the closure announcement, Big Lots had more than 1,400 stores nationwide.

About two weeks ago, in a filing with the federal Securities and Exchange Commission, Big Lots officials divulged plans to close as many as 40 of its 1,392 stores nationwide, and the discount retailer warned in a regulatory report that it has “substantial doubts” it can continue as a functioning business.

According to my business owner buddies, the economy here in the Palm Springs / Palm Desert area is starting to soften. As a result, CRE late pays and defaults are starting to increase in the local area. We are now working on a second foreclosure in CV. This one is a hospitality property near Palm Springs. The property was appraised less than 1 year ago, best guess it will end up selling at around a 40% discount from the appraised price.

I deal with personal CRE investments and I can feel the wheels coming off in my tech city. A CRE property that I coveted for a while came to market and pre-covid times, I would have snatched up. It used to be long-term leased business, but the folks are gone. But, I let it sit for 180 days empty and they just dropped the price by 10%. No offers and the broker begged me to put any offer. On a vacant property that a 25 year old business faded away.

I told him that the owner needs to be slapped around some more if he finally dropped the price 10% after 180 days. I actually have a use for it, but I think we are no where close to the bottom. I might be wrong, but I think that there will be more deals over the next few years.

Keep your powder dry, folks. Good luck.

Just watched Jack Farley interview which is excellent and a discussion about Fed versus Treasury QE and impacts on economic stuff — like resilience and mispriced assets — and perhaps a reason why CRE zombies are benefiting from stealth stimulus and yield distortion

How U.S. Treasury Is Fighting The Fed | Nouriel Roubini & Stephen Miran on $800B “Stealth QE”

“Jack Farley interview which is excellent and a discussion about Fed versus Treasury QE”

Anyone who says that the Treasury’s buyback of bonds is QE is a card-carrying braindead idiot. And YOU are abusing my site to spread this f**king bullshit.

Does looseness have anything to do with the BTFP remnant?

The Fed stabilized things somewhat post SVB, Signature and First Republic failures. The BTFP has been closed to new lending but prior lending is still out isn’t it?

The failures weren’t CRE directly.

But if it looks like failures are happening, the Fed would probably ramp up the BTFP fresh. Or wrong?

The BTFP is dead. Some small banks abused an inherent flaw in it and profited from it, which pissed the Fed off, and it killed it.

In terms of future uninsured-depositor bailouts by the FDIC/Fed, who knows.