“Nobody has any taste for risk anymore. All of those exotic loan programs have ceased. All investors buying that paper are gone”: mortgage broker.

By Wolf Richter for WOLF STREET:

The lockdown regime has changed the once booming housing market. Real estate businesses, such as real estate brokers, mortgage brokers, and other types of businesses, and the government offices that make it all work are now considered “essential” under federal guidelines and under California lockdown rules. Social distancing must still be observed. But deals can be made.

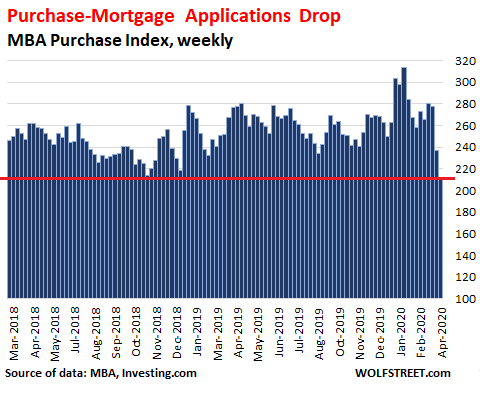

The first glimpse of what the new housing market might look like is provided by a weekly report on the number of mortgage applications by the Mortgage Bankers Association. Today, the MBA released the results for the week ended March 27: Across the US, mortgage applications to purchase a home plunged by 24% from the equivalent week a year ago. Since the multi-year peak in January, purchase-mortgage applications have plunged by one-third:

This is now the second week that mortgage applications have started to reflect the new reality of lockdowns and social distancing. Last week, the MBA reported that purchase-mortgage applications across the US had dropped 15% from a year ago. At the time, the first lockdowns weren’t fully reflected yet as they’d become effective during the last part of that reporting week.

Since then, we got blasted by the first report under the lockdown reality of initial unemployment claims, which had spiked to a horrid 3.28 million, nearly five times the prior record. All this goes together.

In states where lockdowns started first – they were kicked off in the San Francisco Bay Area – the year-over-year plunge in purchase-mortgage applications was the most severe:

- California: -36.4%

- New York: -35.6%

- Washington: -32.5%

And this is happening despite the lowest average mortgage rates in the MBA’s survey data. During the reporting week, the average contract rate for 30-year fixed-rate mortgages fell back to 3.47%.

“The bleaker economic outlook, along with the first wave of realized job losses reported in last week’s unemployment claims numbers, likely caused potential homebuyers to pull back,” the MBA’s report said.

“Buyer and seller traffic – and ultimately home purchases – will also likely be slowed this spring by the restrictions ordered in several states on in-person activities,” the report added.

So, in many markets, it means no open houses. Face-to-face closings are to be avoided. The business still operates with paper documents and lawyers watching over signings, etc. So closings are now tough. But exchanging signed documents through car windows in a parking lot is OK. Under the pressure of social distancing, the doors have opened to modern document technology. In theory, homes can be sold, and mortgages can be written, but it’s now a different ballgame.

“In the past two weeks, there has been a seismic shift in the mortgage lending world that will affect housing greatly,” mortgage broker Dan Draitser told me. And he went on:

“All of those exotic loan programs, such as bank-statement for income and stated-income and lower-credit score programs have all ceased. Done!

“All investors buying that paper are gone! No one remains.

“Lenders are tightening up loan quality for government loans, such as FHA and VA loans. And for conventional loans as well.

“Now it’s higher credit scores, more down, lower debt to income ratios.

“Nobody has any taste for any risk at the moment.

“It is a quickly changing market with everything reverting to low-risk quality loans, which leaves credit extension limited.

“‘Non-QM,’ or basically any loan outside of Fannie, Freddie, FHA and VA, is toast. No longer exists. Being felt industry wide.”

But he was working hard for the wrong reasons: “My transactions are taking three times as much time and effort to get done due to the environment, both refi & purchase.”

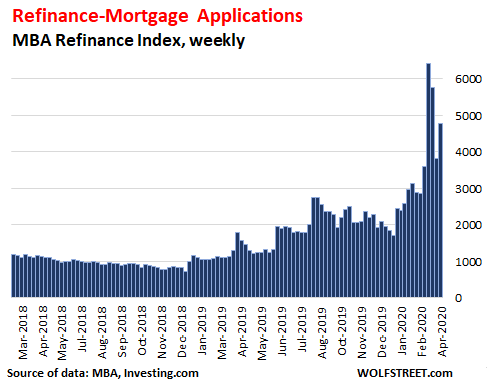

Mortgage applications to refinance existing mortgages (refis) spiked spectacularly over the past few weeks, hitting the highest level since 2003, as mortgage rates plunged. But then turmoil in the market for mortgage-backed securities briefly drove up mortgage rates, despite the Fed having cut its policy rates to near-zero; and refi applications plunged. But during the week reported today, as mortgage rates dropped to historic lows again, refi applications jumped again:

This data is based on weekly surveys by the MBA that covers 75% of all US retail residential mortgage applications at nonbanks, banks, and thrifts. Mortgage applications are not an indicator of demand by non-resident foreign investors or large domestic investors since they can obtain funding elsewhere. But they’re an early indication of local demand by regular folks.

This demand had been strong all last year and earlier this year. But it is now spiraling down. And as mortgage broker Draitser pointed out, the entire risk environment on the lending side has suddenly changed – with risky loans, which were a considerable part of the business, having been pushed off the table.

Neither the Fed nor the Treasury can bail out brick-and-mortar retailers. Read… Post-Lockdown New Normal: Many Brick & Mortar Stores Will Not Reopen, CMBS will Default, Mess to Ensue

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Perhaps, just maybe…we should stop entrusting vital goods and services to industries whose objective is profit and not the preservation of human life?

Wild thought, I know. Dangerous even.

Noam Chomsky on coronavirus on YT in his 90’s with his parrot agrees with you.

Jonas Grimm,

Alot has to be done in cleaning up the media and the government. If corporations and banks had to follow simple well decided rules, this kind of stuff wouldn’t happen “except for isolated cases, which are always unavoidable”. Mortgages and home building are not something government taking control of, would lead to good things.

Right now the first 2 things that have to be fixed are the government and the media.

If you have a corrupt government take control of a corrupt industry, it could easily get worse.

We used to have those rules but they didn’t satisfy the need to unleash the ‘animal spirits’ (ie basically the worst side of human nature) so they were removed during the 80s and 90s.

Yes, and if memory serves, much of healthcare was once off limits to the for profit crowd. I recall a big push to promote for profit hospitals and healthcare in the 80’s.

As we can all see for ourselves now, that has now looks to be a rather large mistake.

MD:

Thank you!!!!

Thomas Roberts:

“…. have a corrupt government take control of a corrupt industry, it could easily get worse.”

The “corrupt” government has been in bed with the “corrupt” mortgage finance business for decades now.

@timbers

Please, Regale us with ur favorite medical advances from the USSR and red China!

Or do u not care about that stuff? U only care that no one is making a profit?

Well, I hope from here on out u never get to pocket any surplus effort u may have put into the world/ market.

Be sure to never use any products in which someone made a profit, my friend. You wouldn’t want to encourage bad behavior.

Heaven forbid someone made a profit making ventilators or n95 masks.

I’d rather get Covid19 than awe that happen, don’t u agree?

The point is that government corruption has to be fixed before increasing the government’s control of an industry or else it could get worse. However, not for this, but, if an industry is super corrupt, to a much greater extent than the government, it might improve the situation, to bring in government, but it’s not a guarantee.

Dodd-Frank is a good example it’s a corrupt law. It exists to be extremely complicated and push out small banks. It needs to be replaced with the much older Glass–Steagall act “who’s repeal is a large factor in current economic problems” and other more simple well thought out things.

The media in America is corporate controlled and divides the population and lies, thus allowing government corruption to flourish.

If you have good media and a well functioning government than the corporations and the banks can be kept in line while still making money.

RagnarD:

On Tuesday, 10 March, I was fitted with two defibrillator plates; one on each side of my torso and given a 200 Joule biphasic cardioversion. Bingo! My heart was back in sinus rhythm.

Up until the Berlin Wall fell, we in the West had only monophasic defibrillators. A quick shock to stop the heart, and another to kick-start the heart – without changing polarity.

But these commie scientists, Igor V Venin and Naum L Gurvich, who were from Lviv, Ukraine and Moscow, figured back in 1967, that it’s better to run the positive charge from a person’s back to stop the heart, and then flip the polarity around and have the positive charge restart the heart from the front right side of the chest.

By 1969, at the USSR Academy of Medical Sciences, these two and their buddies Tabak & Bogushevich, figured that it’s best to use a ‘quasi-sinusoidal pulse’. The first shock should be 5 ms, and the second shock should be of 55% of the first.

In Russia in the 1970s their hospitals had biphasic defibrillators. Fifteen or so years later, we had them in the USA.

Russia has always had brilliant mathematicians and physicists.

Ragnar,

About that Communist health care:

Life Expectancy, Cuba: 79.74 years

Life Expectancy, USA: 78.69 years

That’s going to take the reversal of over 40 years of dogma which preaches that the economy is more important than human society – and indeed, that the latter does not even exist.

Expect to be called a ‘commie’ more than a few times if you persist with this subversive thinking, for that’s the way the propaganda has trained the great unwashed to react to anyone who apparently doesn’t buy into the creed of unlimited greed and total self-interest.

You mean it’s our duty to capitalism to die for it, in our homes, alone … according to the right. Praise be the dollar, God bless the banks, the lord has spoken.

re: “… the propaganda has trained the great unwashed to react to anyone who apparently doesn’t buy into the creed of unlimited greed and total self-interest”

Probably the same ‘great unwashed’ who are now sending death threats to Dr. Fauci, presumably for contradicting the Grifter-In-Chief (let’s see if that gets by Wolf’s filter ;)

Do you work for free? I bet your income was a major part in your decision to choose your current job.

I visited the healthcare system of countless countries.

And can unequivocally say that those that count on selfless humans to do a better job are usually the worst. By far.

Cuba being a good example. Basically no healthcare to speak of. No medicine. No technology. And incredibly bad surgery.

But but…yes I know it’s a very poor country. Socialism does that.

Ok how about France?

Rich country, half socialised healthcare: horrible. Docs are very smart and well trained. But the bureaucracy is dominant, and care rationed. Severely. Unless you frequent upper echelons of society you’re out of luck. Especially in an emergency.

You talk the good word to us unwashed.

But you don’t know what you’re talking about.

And if you want to work for 50k, please donate your excess cash.

Easy.

Not holding my breath.

Maybe you can lead by example and run a childcare operation for free for your neighborhood.

And perhaps you could read what he wrote. He said not for profit, not free.

@timbers

Who gets to decide how much reserves a non-profit is allowed to accumulate?

For example if a non-profit accumulates some extra funds is it OK to have one month expenses in reserve, or 12?

And who gets to decide how much the president of the non-profit makes?

And if the president of the non-profit hires his cousins for profit construction business, is that OK?

It’s so exciting to figure out who get’s to boss the non-profits around isn’t it? Because being the boss of the non-profits requires a lot of skill and education- very important job!

We really need to straighten this out because obviously non-profit orgs are the solution here. I mean look how many innovative solutions that allow humanity to support the life of billions of people on the planet today have come from non-profits! Transportation, technology, farming, medicine, manufacturing- All of the advances came from non-profits, right?

Timbers,

All that “nonprofit” means in practice is that the amount of money in excess of production costs (input costs, labor costs, etc) goes to the executives running the “nonprofit”, instead of shareholders who put capital in to get the enterprise started in the first place.

“Nonprofit” does not necessarily mean cheaper (which I assume is the goal of your posturing).

There are plenty of “nonprofit” colleges, hospitals, etc. that charge a fortune – if they were truly cheaper, a huge percentage of customers would have shifted to “non-profits” a long, long, long time ago.

In the long run, the only way to make things cheaper is to make their production more efficient or the product more effective.

Even capping salaries (which seems like your true intent) is only going to limit the supply of people going in to the hardest, least pleasant, but perhaps most necessary jobs.

Not for profit is usually an accounting scam whereby no taxes are paid and the profits (very real ones) are diverted by the upper echelons via mega salaries and/or enormous benefits (house, car, secretary, trips,”research” giant retirement funds , pensions, etc….

That’s how it works in the real world.

Are we talking about policy or Jonas Grimm?

Why would you sat something so stupid and petty? Perhaps due to your propogandized conditioning?

While he is a bit crass, he is essentially correct.

Way too much rhetoric about this problem is people yelling about what other people should do, rather than what they themselves are going to do.

YouTube vloggers calling for an anti-profit revolution while dressed in high end fashion and producing their content on a $4,000 MacBook Pro are almost cliche at this point… i haven’t seen many people declaring a willingness to sacrifice *their own* profits for the Greater Good.

Which is why “getting profit motive out of the system” has a 100% failure rate in human history; even socialists want profits for themselves.

@ Canadian –

Grimm’s statement:

“Perhaps just maybe … we should stop entrusting vital goods and services to industries whose objective is profit and not the preservation of human life?”

Old-school’s response:

“Maybe you can lead by example and run a childcare operation for free for your neighborhood.

The medical system in the USA is a joke. It has been bastardized by many interests including insurance companies, big pharma, corporate hospitals, the American Medical Association, medical educational institutions, student loan providers, etc. with the support of the bought and paid for government.

There has been a lot of lobbying for money in the medical industry. (I noticed my Doctor was very quick to offer prescriptions, particularly after he was visited by a “cheer-leader” drug rep. I knew them both, and they both “profited” from drug company perks.) Call me cynical, but I suspect there are times when the actual health of the patient is a secondary concern.

The Canadian system is also a joke.

In general, centralized health care with a limited supply is a joke.

A true fix would be to make it as commoditized and as competitive as the tech business, or retail, or even automotive, but thats something opposed by all.

If you want health care to be affordable, accessible and falling in price, set Walmart, Target, Amazon and the Koreans in motion.

Instead, the “debate” is between poor quality rationed private care or poor quality rationed public care.

@Jonas Grimm

Your government is very eager to preserve your life, they promise. Your government is also eager is insure your wealth. Your govt is terrific at providing vital goods. Your government is eager to protect you from those filthy people who are motivated by profits. Because nothing is more evil than a business owner who actually tracks their income and expenses and is trying to increase their income!

All your government requires is all your freedom and all your wealth to be entrusted to them, and your vote. Your government assures you that history shows that the wisest people always place their entire trust in government.

Thank you. It does get a little depressing going through some of these posts.

Yes it does get depressing. However, we need to keep things in perspective.

Last night I had a phone conversation with my 95 year old step dad. He is still sharp as a tack. He told me that 75 years ago to the day (4/1/1945) he was part of the battle at Okinawa. He was an X-ray tech with the 31st Field Hospital (attached to the 10th Army).

He reminded me of all the suffering he witnessed. Really horrible stuff.

Your words are an example of a strawman argument. He mentioned the profit motive. There a many sectors of society that the profit motive is inappropriate.

Healthcare is one of those, and is for obvious reasons central to what’s happening now, we pushed into the for profit sector, starting at least in the 80’s.

The results speak for themselves with the U.S. widely ranked at best in the middle yet at twice the cost.

@timbers

I completely agree that profit motive should be removed from healthcare.

We should immediately pass a law that whoever invents, distributes, or administers the vaccine for covid-19 has to do it for zero profit.

We only want people to make the vaccine if they have pure intentions, not for filthy lucre.

@Raging Texas…. your response is ani example of strawman argument. The for profit change that occurred in the 80’s was not in development of drugs or supplies in general, but in the institutions that delivered healthcare such as hospitals which were dominated by genuine not for profit organizations. You should focus on facts not not ideology and read up on the changes, many of them starting in the 80’s

Does that mean you’re going to cap salaries? Capex? ect. I’ve seen non-profit’s spend very lavishly on salaries for top exec, excessive travel and entertainment and on buildings and capacity not needed just to get their names on.

Don’t assume just because a business in non-profit that there isn’t enormous waste. Corruption is corruption regardless of the profit motive.

Some industries only earn a 1-2% Net Net profit margin. That’s damn near non-profit status.

The real question is some people trust Government to run things, some trust Corporations, and others trust neither. Both are corrupt to their core and are beyond redemption and deserve neither our trust or money.

@cb

No I’m not proposing anarchy. I’m just running with the non-profit pro-government flow here today.

Along with the non–profit idea, we should also make sure that families hand in any extra cash they may have at the end of each month- that’s profit too. And that they only spend any cash they get on truly necessary things. We need to do this to be sure that people are not working for profit, only for higher motivations determined by someone other than themselves.

It is the nonprofits who are the egregious overchargers these days. And they don’t pay taxes. Why is it so vital that UCHealth build a surgery center in a wealthy suburb that they need tax breaks for that? I’d rather the local ortho group or Health One do it. At least we get transparent financials and they pay income and property tax. Instead, we let a nonprofit do it and they rape us.

Be careful regarding the nonprofit delivery systems. These vertically integrated nonprofit systems use obfuscation as their core strategy and drive health care costs to the moon. Not saying for profit is necessarily better…but the real criminal is the delivery system. Not the insurer.

And the input costs are too high. Allow drug and device imports. They allow providers to be imported which drives down the cost of the doctor or nurse.

Regulate administrative salaries. All compensation cannot exceed a certain percentage of “profit”. The compensation packages a the nonprofit centers are obscene.

here in australia in the 70’s, Medicare was established, free basic health care for all. Best thing since sliced bread.

Are you proposing anarchy?

Thank you. Why is it so hard for some to accept profit motive is not for everything? I’s because of pushing profit motive to the nth degree, into areas clearly not appropriate like healthcare, that doctors can’t even follow the Hippocratic Oath. At any rate the results speak for themselves for all to see…this nation’s for profit healthcare is a world recognized failure giving us middling results at twice the cost. Because profit motive

Oh, he believes in ‘non-profit:’ The Pride of Texas, the shale oil industry has, by most accounts, never turned a dime in real profit.

The sad truth is that nobody, apart from your close family and friends, really truly cares about your well-being.

Regulators, physicians, politicians, supervisors, creditors, partners… their “concerns” for you only extend to the impact that your continued well-being or lack thereof will have on them.

Once you understand that, it’s easier to make smarter choices in your own life… as well as understand what’s truly important.

re: “The sad truth is that nobody, apart from your close family and friends, really truly cares about your well-being. ”

The American ‘Founding Fathers’ understood this over two centuries ago. Their belief was that citizens would always vote their own self-interest but competing self-interests would create solutions, and created a government that reflected that philosophy. There were right, in principle, but massive propaganda and poor education has proven them at least partly wrong. Case in point: There are documented examples of people who got affordable health insurance–not necessarily the best, but at least some–for the first time in their lives thanks to the ACA (‘Obamacare’), but vote for Republicans who pledge to destroy it–and Medicare, and Social Security, etc.–as soon as they get done reducing taxes for the wealthy and connected corporations to zero.

What the heck was the original article about?

And is this website for profit or not for profit?

The housing market and mortgages.

I don’t think Wolf is getting from this site; he makes all his money shorting the stock market ;)

@ Raging Texan

Grimm’s statement:

“Perhaps just maybe … we should stop entrusting vital goods and services to industries whose objective is profit and not the preservation of human life?”

grimm did not compare “profits” to “non-profits.”

He compared the objective of profit to the objective of saving human life.

If you found yourself in a situation needing midical attention to save your life, would you prefer to be in a situation where the primary objective was to profit or where the primary objective was saving your life.

I’ve no doubt that you can pen an interesting answer to this, but before you do, consider your honest preference.

@cb

ok so if I’m gonna die, where do I want to be, for profit or not for profit. . .

hmm. I already had a near death experience so now I’m at peace with life and death. Actually looking forward to next life a lot.

Can I just die at home and leave my wealth ( as in my F-150 and horse trailer) to my kids instead of the local hospital? Does anyone die at home anymore? Do we really need to run up $500k of ventilator bills to the non-profit hospital if I’m just going to die anyway? I heard the hospice-at-home nurses are hot and will give you morphine.

I choose option C. Hot nurse with morphine. While watching my favorite shows. You?

@ Raging Texan –

Well I hope option C works out for you

It would be a shame if you hot nurse turned out to be Ma Barker

You mean we can’t count on billionaires like Musk and Bezo to save us from this crisis? I guess donating 1k CPAP machine is just as good as ventilators…how shocking

Amen. The “Federal” Reserve bankster cartel has printed out so much legal tender (and will doubtless print out so much more) to buy the bad, mortgage-backed loans of the banksters (bad stocks, etc.) that it will be the majority, beneficial owner of most US and a good part of the world’s real estate. I do wonder what their exit strategy will be.

My understanding is that much of the real estate that was underwater in 2008 was still being held by banks, because if they sold massive portions of the total real estate available in many areas suddenly, real estate prices would have plunged in those areas or nationwide. Now, I guess that they will have to hold on to their residential-mortgage-backed securities portfolios for maybe another decade.

It must give the banksters a warm, fuzzy feeling to know that if they make more and more stupid decisions, the “Federal” Reserve bank cartel (which is deceptively designed with presidential appointment of its directors to deceive Americans into believing that it is a true government agency/department but is truly owned by the banksters) will always bail them out. Right now, whatever remained of the value of your retirement savings or home, or of the US’s real capital to pay its over $211 trillion in liabilities (not even counting state and local liabilities, which are also gigantic), is being effectively gifted to the banksters via way, below FMV interest rate loans to their banks, purchases with US legal tender created by the “Fed” to buy banks’ bad loans and bad investments, even SPVs to purchase securities that went down in value, so the little banksters can sell their ownership in failing enterprises without suffering the already incurred losses due to this economic catastrophe, which the US tax payer will then suffer.

I am surprised that most Americans do not seem to care or do not even notice while they are being financially serviced roughly by the banksters and their owned crooked politicians in this way. See Simon Johnson’s “The Quiet Coup” in The Atlantic Magazine.

@mike

regarding your question about exit strategy, here’s their actual plan:

1) Federal Reserve steals from everyone by printing currency to buy all assets

2) Eventually owns all assets, and everyone else is impoverished by money printing

3) The owners of the Fed, now get to be the masters and you are fully enslaved

So the “exit strategy” if there is one, is either transferring FED assets to the owners, or , the owners leave the Fed with paper ownership in order to preserve anonymity and dazzle the enslaved masses

Who is it that you trust to have the objective of preserving human life? That’s a pretty crazy expectation. Furthermore, who is we? Whatever trip you are on, you can count on me to not come with you.

Wow..Bam…That was quick…Annnnd it’s gone!!!

So Stated Income Mortgages did not end in 2009? Welcome to Fraudlandia!

I just did 90% LTV refi

of course my 800+ fico might have helped

self employed with assets = oops did I say that

1.8% difference before SHTF

There’s never been a better time to buy or sell an infected house!

P.S. at least the mortgage guys can make up the missing volume on refis for a while…

Who, exactly, is going to plunk down their life savings for a home right now. Life goes on of course but taking on debt in the near future for the average American is probably not going to happen until late summer, at best, I suspect.

Yep. The question now is, how low does it go?

Wolf,

Do you see the Bay Area being affected if tech survives this, albeit bruised? Startups may be closing up shop but I’m guessing most of the people working for the big names aren’t being affected and hence not moving out of the area. Given that there already was a net outflow out of expensive California, couple that with startup fever subsiding, does that mean the employees of the big tech players who have been holding out on home purchases due to inflated prices get into bidding wars again. Would that cancel out any slump in prices? I guess I’m trying to look at the different variables here but not sure if I’m close or way off. What say you?

Hard to tell at the moment.

“Big Tech” — such as FB and GOOG — lives off ads, and if ad spending plunges, and there are already signs of it, then those ad-revenue based companies are going to look at their expenses.

Others, like Intel or Cisco, go by hardware sales. Cisco has been laying off people for a while.

I lived in the Bay Area during the last big tech recession in 2001. Post 9-11, jobs went from plentiful to rare and there was such an exodus of people that empty apartments in Palo Alto were going for $700 a month, down from $2,100 a year earlier in the same building.

Most millennial tech workers in the Bay Area have never seen a real downturn; it will be educational for them, as it was for me in 2001.

Canadian,

Thanks for your perspective. This doesn’t *seem* to be a tech recession but you never know I guess. The tech industry today is different in some ways from what it was in 2001, especially due to the Internet. I don’t see the big ones like the FANGMAN being affected severely. Startups yes and there may be enough of them to have a significant effect on the area as a whole.

The preservation of human life is also a profit.

Profit is not reserved for financial terminology. Profit means to gain, to enjoy advantage.

Regarding business as only in it for the money also misses the point. Business is about helping people in exchange for money. The business profits, so do the people that are helped and who reciprocate by helping the business.

Tell that to the thousands of Ayn Rand fanboys clogging the financial field these days. The only thing sillier than an honest true-believer libertarian is an anarcho-capitalist. Hierarchy always ends in abuse, because we’re still the same tribal apes that smashed our way out of the Fertile Crescent ten-thousand years ago. We’re not programmed for long-term thinking or for responsibility of that magnitude.

Real estate may be ugly, but everything else is as ugly or worse, the destructive momentum unstoppable, even if a vaccine discovered tomorrow.

Because the prick at last, has found the debt bubble and the gargantuan explosion cannot be contained.

Our Twilight Zone soon to become a new Dark Age.

There will be scraps offered in return for subservience, obedience, compliance, complicity & serfdom. All men are not equal and you don’t know your masters, nor should you. You may turn & fret in your pen and think it pasture if you will, if it helps.

Never fear. Look to the heavens on a cloudless night and know There Are No Accidents in the Universe.

No inspiring poetic post on how some of the slaves might still escape this bleak outlook; tip the balance, however slight, in their favour?

Keeping your Credit in good standing by differal of your mortgage is better than missing a payment or defaulting on your mortgage which would tank your Credit.

Hmm, that spike in permits and starts over the past year. I wonder how many home builders are going to be stuck with inventory they can’t sell. I guess they will need a bailout to.

Also, city inspection services are probably slowed to a crawl.

That’s an interesting question now that we have the “iBuyers” such Zillow and others. They’re now sitting on those houses they expected to flip, and when they can flip, the housing market will have drastically changed.

Difficult to get a mortgage after your hours were cut back, or you lost your job.

Ever seen a stock market crash and housing bubble burst at the same time?

In Ecuador bodies are rotting without enough resources to bury them.

HI WE JUST SPENT OVER 1200 IN FEES ETC ETC WERE PROMISED A 99K CONDO IN JACKSONVILLE THIS FRIDAY AND THEY CANCELED FINANCING LATE MONDAY WAITED FOR MONTHS AND BIUGHT BOXES ETC ETC NOW WE ARE SCREWED . JOE THANKS

joe,

Thanks for the update.

But please locate the CapsLock key on your keyboard (generally on the left side) and press it exactly once.

KBR just announced a 10% cut to salaries across the board. I think the pain will be felt for a long time to come.

Yup, happened to me. Last Friday git the clear to close on my refi for Monday March 30th only to get a call from the bank late Friday night the bank has pulled the loan off the table. They wanted a higher credit score (10 points higher) and wanted me to pay down a couple of items. This is with a VA loan, still fully employed, a simple refi.

Historically VA defaults have been lower in comparison to conventional and FHA, but, right now, the secondary markets have no appetite for govt loans.

That’s why the credit score increases are happening.

Before, 580 was the minimum, now most lenders are tightening up to 660 and 680.

So, it depends what you score is/was.

Markets, give me a fing break. Markets do not exist anywhere in this country. Price discovery does not exist. Stop talking about mythical markets like they exist. First we had free markets all thru out the early 2000’s, but thankfully after 2008 that shut the GOB of most of the dimwitted believers in that. I’m waiting for “markets” to get the same treatment.

Multiple, competing puppet-masters now count as a free market.

“Now it’s higher credit scores, more down, lower debt to income ratios.”

That is a good policy, and should be the hat trick for mortgage approval I reckon. (Yes, I am jonesing out from a lack of sports to watch – so I put in a hockey term, eh?)

Oh man, think what the auto industry report is going to look like. Those fancy 75k pick-ups just hit a brick wall.

A brick wall at 75mph to boot. But don’t worry, they’re all offering loans of up to 84 months at 0% and even first few payments deferred and or covered.

Pretty much sellers can offer *any* goofy/loose terms so long as the receivables can be packaged into securities that *some* ZIRP’ed saver is foolish/desperate enough to buy.

I expect at least a 50% YoY drop in purchases in the next report.

Transactions are still happening, but there are big changes in how things are being done.

Showings by no more than two people at a time by appointment only, a new Covid 19 disclosure form ( The first one was revised in one week), Agents Visual Disclosure ( AVID) can now be doe remotely by having the seller walk through the house taking a video and sending it to the Agents ( No problems there, oh no).

Moving in is now restricted by shelter in place orders as well.

It’s quite likely that we will see a spike in inventory and sales come mid July after the first wave has mostly passed and buyers are conditioned to the new reality.

Not much of one due to tightening loan conditions.

Prices are sticky for Real Estate, it’s going to take a while for sellers to adapt to reality.

Sellers who have the sense to cut prices NOW will get out with a lot more money than those who wait.

My best guess is a 25% drop in the median price by the end of July, there will be a change in the mix because those buying will either have first rate credit and adequate assets or they will be paying cash.

And Vacation Rentals are dead, no longer allowed in Sonoma County under the new rules.

Good news for renters, eventually, bad news for anyone who bought counting on revenue from short term rentals to justify the price they paid.

TEOTWAKI has arrived, adapt or die.

Good thing renters disproportionately hold those “essential” jobs that our country appreciates so much. Pumping gas, ringing groceries up. Highly “essential” minimum wage stuff. But something tells me the 10% will be there to pick up the pieces of the real estate collapse. Again. With taxpayer bailout money and taxpayer-crushing inflation filling their sails. Again. And the American home-ownership rate will slide further down. Again. And the poor will go deeper into debt to fund it. Again.

Uber/Wework kids are finally getting a reality check, wow banks want people with good stable income/ reliable history & minimal debt. ( new concept). The gig economy was always there, young people today made it cool, it ain’t, it was always a means to an end like getting thru uni. Just remember to wear dads tie to the bank even a young bill gates dressed up for clients.

Related in Toronto Canada: the Cresford Group with four large condo projects with up to a thousand pre-sold has been placed in receivership.

Who is / are their lenders?

If you enter Cresford you will find it but I recall the lenders are not the big banks (only 6 in Canada)

People aren’t buying trinkets and useless crap. They aren’t taking out exotic loans. They aren’t going on vacations trapped on cruise ships.

We needs this on a permanent basis minus the virus.

IP, some of us have been living that way for decades. Wife’s siblings all have paid off homes, cash in bank, etc.

Our thing, living where it’s a frequent/regular event to lose electricity, sometimes for a week or two, is to have propane cooking stove, (though only the top burners work and have to be lighted when power off thanks to a USA rule that ALL stoves must be non pilot light a few years back when guv mint made one size fits all rules with NO exceptions,) and food stored (and rotated) properly to feed ourselves and family for a few months, or, including neighbors for a few weeks.

Community thinking, including proper PPE, not communism or crony corrupt capitalism, sooner or later, is THE bottom line that will get us through this event, as has done so many times previously.

Rich folks thinking they can avoid this or other similar events are dreaming IMHO.

Very true also don’t need people to go out many times a week to eat out and go for so called ‘fine dining’

So Wolf, 6.6MM additional UE files this morning, and I am reading at least some states backed up for weeks or digital filing systems completely crashed.

And let’s just wait until testing for this virus ‘ramps up’ to at least 10%, not to mention the possible 50% (though apparently even that will take some time due to lack of basic materials.) And tons of folks (of all ages) still seem to be completely or mostly oblivious.

I am thinking we are going to see a heck of a lot of straight lines in the next couple of months.

Gonna have a new motto for us soon???

Mental, absolutely mental.

Many individuals, families, neighbourhoods even, are going to be having quite serious thoughts about what the hell their stake in society is meant to be as they wait for those support cheques.

Not the lazy timewasters, the upstanding and hardworking people with absolutely nowhere to go right now.

Ugly, Ugly, Ugly state of affairs.

The first part is correct: according to Italy’s Ministry of Health the virus was already in the country around January 15, much sooner than previously thought. The spread pattern is an absolute mess and we are about to see if it dies down according to the models. I try to live in hope but I am not holding my breath.

The second part… this is a perfect storm. The big problem is our economies have been in full stimulus mode since at least 2016: to squeeze any tiny bit of growth and prevent liquidations and minimal GDP contractions we used instruments that should have been reserved first to give businesses and families to have a fighting chance and then to stimulate a quick return to normal. It’s kinda like spending your rainy day funds on a Fabergé egg and then smashing it with a hammer to impress your friends.

All those who hope to “loot the economy” have better pray, and pray devotedly, the present models of a 45 to 60 days lockdown followed by a cautious but swift rerturn to normal are correct, because the risk is not merely that there will be nothing left to llot but that people start rioting in the streets as well.

Our economy has been on full stimulus mode since 2008. And before that how low did interest rates go after the .com bubble? Before your “perfect storm” came on the scene in February, did the federal reserve quit raising interest rates, stop shrinking their balance sheet? Now if they did do that, was that due to the economy being stronger or weaker. What happened in December of 2018? You’ve been conned, the economy has not recovered since 2008. We didn’t get a U shaped recovery. You got an L shaped recovery and now we’re on the next L down to a lower plateau. Who was in charge in 2000, 2008 and currently? Was it the same main players or do we have a new crew who had nothing to do with the last few blowups?

Trent:

I don’t believe anyone formulated the virus to overturn the global economy….but….I do believe that a great amount of “smoldering financial paper trash” will be vacuumed up or scattered to the winds as a result of the (intentional) lack of “oversight”……..

The “Era of the Great Hosing” is about to begin.

Why would people willing to lie about so much, and most of us agree they are lying, not lie about something like this? See my comment above about who was in power in 2000, 2008 and now. Its the same Fing people, so they must really like power because they haven’t gone on to do anything else. If you love power that much, what would you be willing to do to retain it if threatened?

re: “I’m still convinced the convenient virus is still a cover for looting whats left of the economy. Convince me i’m wrong.”

POTUS’ reflexive denial of the seriousness of the pandemic kinda belies this. But, the PTB will make the most of this ‘opportunity.’

“The Day Everything Went to Heck in a Straight Line?”

This article necessarily omits an important rising phenomenon: Sales of rural real estate as an escape destination. It’s starting to be reported episodically – See an article in Reuters, this morning (easily found – citation would delay this post for moderation).

Data will be available. eventually.

Chalk me up in the “pent-up demand” column. Maybe this summer I will finally buy my treed piece of land, and watch my investment grow – independent of the Federal Reserve interest rates!

Don’t wait – you will be too late.

See my post, above.

Beleive me,, even rural real estate would be impacted a lot.

How many people you think can afford to live in rural areas away from jobs ?

@a reader: Your patience would be rewarded.

I was a Principal Broker in a small rural office for a few decades.

I talked to my ex-employee who now runs the office yesterday and she said they were still busy. In fact an offer was written that morning. She said that it had gotten harder to close them due to the safe distance issues with the title companies and that she wasn’t happy because she could no longer attend closings but they were doing pretty good.

She was worried about showing properties with the close contact with the clients but was going to continue doing it until she either got ill or was forced to quit.

I wonder about the legal aspect of all that. You sign a legal document agreeing to represent some person, a seller or a buyer and does a decree by a governor negate that legal obligation? Not like attorney’s when the court closes and you can’t but the title companies are still open in Oregon… as are the banks and lenders.. even though the lobbies aren’t .

Have a look here: looks like land buyers/sellers are saying convince buyers of urgency and not to time markets, and convince seller to wait to list until there is a rebound – and either way, hustle to keep your land selling business going through this: https://www.landbrokermls.com/blog/

Amen

Our phone has been lighting up for new construction this week. We are in flyover country. Might have to change that saying.

Apparently there were a few who paid attention in school regarding population density and contagion.

I still have to believe this hits a brick wall soon. Until then we will crank every day.

Look, RD Blakeslee, I love how you live, as you have explained it to us. But I would die being stuck out in the country like that for more than a few days. My Tokyo wife would die two days before me. And there are millions of people like us who LOVE big vibrant cities with lots of people. That’s why big vibrant cities attract people and why these cities grow.

You see, there is something for everyone. If you want to live on a farm, great, go for it. If you want to live in a big vibrant city, great, go for it. If you want to live in a small town, go for it. Not everyone has to do the same thing to be happy.

But wash hands, use good sense, and stay healthy. This is not the end of the world, but some areas of the country and world will be hit much harder than others.

Been thinking about that Wolf. I’ve had my eye on some rural properties in Appalachia for a while. I love deciduous trees and few neighbors. But I’m not so young (say seriously mature) and rural is work. With our current situation I like the idea of living 15 minutes from 4 hospitals in the suburbs, and more 3 teaching hospitals in the city 45 minutes away. Still have an excessive tool collection tho.

Meantime the Zillow estimate for my Bay Area house is at a record high. What gives?

Zillow’s estimation algorithm is terrible. It does obviously dumb things. I’ve actually written to Zillow with suggestions of a few simple things to fix, they never responded. Zillow doesn’t really care that their price estimation algorithm stinks.

redfin is much better. But still not perfect.

Zillow simply uses comps (‘comparables’). Any novice RE agent can do that. FWIW, I sold my house in San Jose for about 8% over the Zestimate two years ago.

Fake markets based on fake wealth create fake estimates.

It is getting harder by the day to believe in anything.

+100

I believe I’ll have another drink.

House prices are not stock market prices, where nimble traders are in at 9 and out by 10.

The RE estimates are based on sales 99 % from before the stock crash. Even professional appraisals (the kind you pay for) are going to be dicey right now because they can only be based on comparable props from the same area. You can’t always hope to find one 3 weeks ago.

If ever there was a time to ignore historical data on housing to form a today price, it’s now.

Or maybe the last 40 years of falling interest rates? That wouldn’t have an outcome on housing would it? Nah, that wouldnt put a price floor under housing.

The Zillow estimate is a pie in the sky number.

Put it on the market and sell it and close the deal. Then you’ll know what your house is worth.

That would do it. Fortunately, I live in a large development of tract homes, so I can get real information without such a drastic measure :)

During the 2008 GFC, the Case Schiller Index dropped to its lowest level about 6 1/2 years after its peak. If you want to compare it to unemployment, it was more than 2 years later. People tend to hang on as long as they can.

But with today’s through-the-roof unemployment numbers, it’s anyone guess where housing will be.

With so many older people dying to covid-19, I think the housing numbers will be disastrous. Death + unemployment are strong motivations to sell.

Personally, I’d rather buy real estate than stocks so I will be a buyer when the price is right.

I keep hearing how it’s all doom and gloom out there. Millions laid off, companies failing left right and center. So I’m thinking, I bet I could get a hell of a good deal on a new truck, right? WRONG! Other than 0% financing for 84 months, there’s no deal to be had. Dealers are in no rush to sell, which means their sales must be just fine. Or they’re holding on to inventory, assuming this will pass quickly and the pent up demand in a few weeks will be high enough to make it worth keeping the inventory vs selling at a loss now. Either way, the situation is not nearly as dire as the media would make you think it is. There’s the MSM reality and then there’s the on the street reality. And the two are nothing close to the same.

They don’t need to lower prices for you friend, they’re gonna get a bailout, duh! Let me state again, markets do not exist, everything since 2008, or maybe even 2000 has been government FIAT. I love the poster on here who think the government and giant corporations are separate entities.

Bailout or no bailout, they still have to move product. And obviously they’re not too worried about it.

cash for clunkers is coming

Many of those on the Titanic weren’t too worried either – until they were. And the band played on.

Other than the trigger by the CV, the markets actions are explained well by Hyman Minsky’s Financial Instability Hypothesis.

When things appear stable, people take risks. As those risks pay off, more and more people take more and more risks until the leverage and risk has been elevated to god like status..

Then something comes along and knocks one of the legs out from under the three legged stool and the entire house of cards built on top comes tumbling down. The longer the periods of building up risks, the more that falls..

Then no one wants any risk.. for a while until some take some risk and are rewarded and the whole thing starts over.

We are in the stage of the house of cards falling to the ground. This has happened many other times. Maybe never to this extent as this time was a little different but it is crashing now.

Unfortunately for all of us, it just happens to be a Pandemic that is causing it. I hope all of us survive this.. This is a great group of very intelligent people who I very much enjoy reading. Stay safe and well if you can.

How does rebalancing mortgages in the aggregate toward REFIs away from new purchase mortgages affect the industry? In 2007 a lot of people overleveraged their home value, of then to pay medical bills. Just seems that losing new home mortgages would be like government having no bid at a treasury bill auction. How does the system resupply itself? Are people jumping into REFIs asking for trouble?

During the last crash the S&P 500 hit bottom in March of 2009, and by March of 2012 it was up 93% (dividends reinvested), if I have my facts right.

Also during the last crash US house prices trended down and didn’t hit bottom until sometime in 2012. Sticky on the way down.

Invest in the S&P 500 now, wait for SFH prices to hit bottom in 2-3 years, then invest in SFH. If like me you live in an expensive area where average SFH costs $1m+, SFH vultures are always circling and getting a good deal is always difficult no matter what.

In 2008-10 the huge price drops were in less desirable areas. Prices fell 50%+ in those areas. In desirable areas, it was significantly less. So even assuming the worst case scenario, a nice home in a nice neighborhood will probably be about 20% less in 3 years from now vs today.

But prices are only 1/2 the equation. The other 1/2 is interest rate. $1M home at 3.25% is the same mortgage as an $800K home at 4.5%. That 3.25% is available right now. In 3 years, who knows what it will be? Could be 3 could be 4 could be 5. It’s a gamble. Plus you will have paid rent for 3 years instead of paying off the mortgage for 3 years at 3.25%. 3 years of equity buildup at such a low interest rate is tens of thousands of dollars.

What’s I’m saying is there’s no guarantees in any of this.

and mortgage rates might be 2%, or that 1M home might be only 500K?? a lot depends on the alacrity of shadow lenders to get back into the game. at this stage we should assume only those who need to be in the market are buying. Please don’t draw too deeply on the 2009 equation, this time really is different.

Or this whole thing will be short lived and forgotten by late summer. Nobody knows where it’s going. No matter what you do you’re taking a risk and it could be the wrong move.

Correct to an extent, In San Diego, even desirable areas got hit.

I’d guess, lower price homes in SD would be less severely impacted than higher price one.

BTW, I’d rather buy a much lower price and higher interest rate than otherwise. You can always refi to avail lower rates but you can’t lower the price. On top of this, lower price is low tax basis for property tax.

Agree SD saw 35% decline overall, as did much of riverside county even worse in some areas. Been thru this several times, but this time may truly be different. Now live in sun city palm desert and so have real numbers and observations if anyone interested.

Side observation going to local Stater Bros grocery just outside entrance, about 35% customers wearing masks, gloves, protection – none for employees. Lots of really old folks 80 – 90 customers wearing nothing with no apparent signs of protection. We have only had a couple of cases here, but if hit hard lots are going to ride the elevator to the sky.

The biggest drops occurred in Miami, Las Vegas, Phoenix, Atlanta, and the big California cities.

How are these the “less desirable places” (from a RE perspective)?

i believe it was the 2nd and 3rd tier cities that held up much better.

It’s really very early days into this mess.

If it continues, and I don’t see any other path, most global governments that are directly and heavily impacted will be drawn to execute unmade plans to rescue most everybody or we will all go down the tubes including many, many of the “wealthy”.

This situation is entirely unprecedented. The hammer of imminent financial problems was evident; now with the virus threat it is precipitive.

There will be no “escape”.

Stay healthy…..

If 2008-9 was anything to go by, this tightening of credit requirements is just a temporary knee jerk reaction.

As soon as things calm down, governments will say OMG and will quickly reduce credit requirements to spur housing again!

“All of those exotic loan programs, such as bank-statement for income and stated-income and lower-credit score programs have all ceased. Done!”

WTF???!!! I thought that all ended after the GFC!

I’ve taken out 4 mortgages since the last crash. I have perfect credit, high income, lots of assets. Everything is documented. And I had to practically provide 4th grade report cards to underwriters. Every little discrepancy needed and explanation, even once an explanation about where I lived in the mid 2000s. It was something like Experian showed my address at 123 Main St from 10/05 to 10/06 , but Equifax showed it from 02/05 to 11/06. I don’t remember exactly, but it was something stupid like that. An address where I hadn’t lived in over 10 years. And still they wanted to know why there was a discrepancy, and did I really live at 123 Main St, and which were the actual dates. Why they cared? Beats me. But they cared.

People like me have to play by the rules and jump through all sorts of hoops. Meanwhile you have the deadbeats of he world still getting mortgages by breathing into a mirror. Playing by the rules is punished, while being a deadbeat is rewarded. This hasn’t changed and never will in the new America.

I re-fi’d my home and two rentals thanks to HARP–thank you President Obama, we miss you!–and I had to jump through quite a few hoops as well. It was worth it; got 3.25% on the home and 3.75% on the rentals for 30-yr fixed. Haven’t seen 3.25 on a 30-yr since.

Maybe the nit-picking is just a sales technique to up the advertised/come on interest rate.

Most civilians don’t realize just how much pre-planning and psychological manipulation goes into every single sales transaction (selling is *all* salespeople do, every hour of every day – forever. And the vast majority don’t get paid much/at all if they don’t close.)

This is not true in that “Dead beats” who breathe into a mirror get loans. No, the “bank statement” for income programs were for the self employed individual that had good credit and a hefty down payment.

Furthermore, they typically did not use 100% of the deposits for income, there was further underwriting that would utilize expense factors depending on the industry and also had tighter debt-to-income ratio requirements.

You should NOT equate the “stated income” or “bank statement” programs referenced above for the “liar loans” of the previous decade where nothing was verified. That is NOT the case.

I look at SF as a bit of an indicator. Sales in San Francisco Metro are continuing in March with even a $12M+ house sale. Since SIP order (March 16th) – 119 properties went into contract and pending. 45 out of 119 went into contract (status contingent). 74 is comprised of the properties that removed contingencies and those that went into contract non-contingent thus showing as “pending”.

These people are not necessarily making bad decisions. Where do people put money to invest with the stock market whip-lashing and down significantly, metals are at a premium (physical), most bonds except Treasuries scary, art tanking, etc. Many will sit in Treasuries and ride out the stock market but looks like some are choosing premium real estate.

Also will say that if you listen only to certain sites, SF is a dystopian zombie city – it’s not. Outside the areas that have always been bad and some more homeless near the downtown areas – SF is pretty nice city.

“SF is pretty nice city.”

But insanely overpriced by any rational measure.

Even in coastal California, heading inland (or N/S in SF’s case) can reduce SFH costs by a significant percentage.

Agree on $SF but I spend time in Coastal and inland CA and would spend much more for the cooler climate, greenery and overall lifestyle…there is a reason even if tech goes away why it is so much more $ in coastal CA

As the 4 and 8 week Treasury auctions today INCREASED in auction size amounts ( excluding SOMA), $80B for 4 wk and $60B for 8 week; their YIELDS turned positive (from last week’s 0%). High rate is 0.090%

and 0.095%, respectively.

Getting close to the IOER rate.

Didn’t Jared get out from under the ‘666’ debacle recently (thanks to a massive infusion of cash from some people wearing long robes)?

In the last 3 days, the Treasury has auctioned about $330 Billion in seven various 37 to 154 day CASH MANAGEMENT BILLS (CMBs) with high yields ranging from 0.025 to 0.150%

Wonder where the SPVs will get Treasury seed funds. Here’s your answer.

Had they simply increased the sizes of the regular 4,8 and 13 week auctions, their YIELDS would increase much more. Ordinary citizens could at least participate using Treasury Direct and other means.

CMBs on the other hand cannot be purchased from Treasury Direct as they are mainly for the BIG GUYS.

Iamafan,

You should ask Wolf if you could post a guest Treasury “explainer” – I know that you are talking about significant measures…but you lose me in the shorthand lingo.

High housing prices are integral to the Company Store economy. If the new low wage proles can’t swing the payment the durations will grow like in Japan in the 90’s. The Store has had a lot of practice with this since 2008.

As a deadbeat, self-employed, small business owner, I can verify that aside from the late 1990s – there has never been a time when I could get a mortgage By ‘breathing on a mirror’ because of my lack of provable income, job insecurity, and low balance bank accounts. Yes, it’s my fault for not following my banker’s advice and declaring that I made more money, not taking easy tax deductions, and frequently engaging in pocket transactions. I’m hopeful that this mess might finally make it possible to buy a home for my family, even if the world collapses a few days later. I just request that the world let us unpack our boxes before it all goes to hell in a hand basket.

This is true and I quickly dispelled the gross overgeneralized notion that “bank statement” loan programs for small business owners were akin to last decades “stated income” programs.

I understand housing is a very slow movng beat but in my hood ie san diego ca, the homes are still selling as a hot cake generally barring few exceptions

In essence, no impact on the ground as of now. The home prices are insane here for sure

Jon,

“In essence, no impact on the ground as of now.”

You’re not looking at the ground :-]

If you’re looking at closed sales, you’re looking at February and early March at the latest. That was an eternity ago. Everything has changed since.

Amen. Reportedly, NY just told paramedics not to bring their passengers to hospitals, unless they have a pulse. Most people do not realize the significance of that.

Many persons may have heart problems which result in their heart stopping in the ambulance, as a relative of mine had long ago. Paramedics are ill equipped treat heart failures in their moving ambulances. However, in the past, many people are revived with the expert help of doctors in emergency rooms, after their heart stopped on the ambulance.

Now, those persons are already being allowed to die in NY as a matter of policy. As in Italy/Spain, due to a shortage of supplies and medical personnel, will persons who are 65 and over soon be denied ventilators? See https://www.haaretz.com/us-news/.premium-in-u-s-coronavirus-crisis-will-trump-save-the-elderly-or-condemn-them-to-death-1.8687478

In Spain, reportedly people 65 and over are being unplugged from ventilators and those ventilators are being used to save persons under 65 years old. The state governors who are know of this upcoming avalanche and are claimed to be “complainers” by the foolish are confronting these anticipated situations. There is a nationwide shortage of enough equipment and medical personnel in states with growing coronavirus epidemics, which will need more treatment.

In NY, the next six to seven days will reveal who was foolish and who was not. Let us hope that the growth in the number of cases does not overwhelm hospitals in all of these states: however, reportedly, some people have to be on ventilators and have poor prospects of survival even on ventilators. My elderly, wonderful parents would probably be in that situation if they caught this virus.

Unfortunately, those persons are likely to be unplugged or denied ventilators if younger people who are more likely to survive need them. Thus, foolish, younger people who want the choice to “risk themselves” are really risking lives of those elderly and of other people with pre-existing conditions: those will be the people denied ventilators, not the younger people who chose foolishly.

In this world, what do you do with all of your cash? TBills … because longer duration Treasuries ( Notes and Bonds ) might suprise everyone with a big jump in yields because of inflationary money printing.

But, you can’t but everything in TBills … affordable single family houses in high end areas always have hungry renters waiting because they want to keep their families safe. Obvious. If you have cash, what else are you going to hold?

Many don’t have cash, so they just spin doom and gloom. That does not work. A better plan is see if you can get a mortgage and get a deal .. if you can get a mortgage. Some idiot will cut the price and sell to you.

Eventually, when SP gets below 2K, you might want to allocate some of that TBills holdings into SP500 … on a trailing basis, 2K SP is PE 15, which might be the first decent entry. 1800K on the SP would be a dream, which trails at 13.5 … just dreaming.

It is nearly impossible to nail the bottom of a bear market. I don’t even try to do it. Instead I dollar cost average through the trough, starting when the market is at least 30% down from the top, and put a little in each week all the way through to the other side when the market goes back up. Generally I try to catch the big dips, but it does not always work out that way. I use mostly the S&P 500 index, but there are other indexes if you want to make it complicated. Bear markets usually last about 9 months, so before you know it it is heading back up and you are making a lot of money. Cash used to do this is kept in a treasury money market account (short duration). I know I’m not making anything on that cash, but it is a convenient and efficient place to keep cash and move it to the index each week. If I manage to get within 10% of the bottom of the bear market I call that success. I then leave it all in and ride that big bull S&P 500 market for 7-10 years. It takes some nerve and discipline (and dry powder) to do this. At some point you may see a property you want to buy and since the real estate market is like a slow moving sloth you can grab a good deal using the money you made as the S&P 500 goes up.

Disclaimer: Doing what I am doing can result in a serious ass-pounding and you can lose all your money.

DCA from what I know is nothing more than a marketing gimmick. It’s no better than trying to time the market. In fact, from the studies that have been done, timing *outperforms* DCA, on average. It’s what called ‘behavioral investing’ where you *feel* you’re doing the right thing by putting in a little amount as the market goes down, akin to investing long-term vs short-term but if you look at the data, it’s completely ineffectual given a large enough sample size with timers and DCA’ers compared.

If you look at it, the big names, the Buffets and the like do try to time things in that they try to catch the dip, the ‘right’ dip if you will (which in the current crash hasn’t arrived yet, according to the prevailing sentiment) and then don’t keep going in with additional amounts, i.e. DCA. If you don’t happen to call the bottom, you don’t, out of luck. But if you think DCA is giving you a fair chance or even an edge over those who do try to time it, you’re mistaken. The numbers simply don’t support the claim.

JP Morgan, who I have understood was the last person to ”corner” the entire stock market, was alleged to have said, “Buy on the basis of fundamentals on the way down, and be prepared to hold through the bottom; and sell on the way up, because you can never know in advance when either the top or bottom will occur.”

Or something like that, the point to us amateurs is that we never have the same relative level of information he had nor these days the oligarchs manipulating the markets have.

Like you said, dollar cost averaging is a marketing gimmick to keep small investors in the game. It’s basically, “Keep feeding coins into the slot machine no matter what.”

It would not surprise me at all if a very skilled market timer would beat DCA. However, it would surprise me if someone DCA invested $100,000 during the trough of a bear market, and bought within 10% the bottom on average, and held for the next 5-10 years, that this person would be unhappy with their investment decision. That would really, really surprise me.

But what if markets hit lows and then just trade in a sideways range for years

Look at how long it took the Dow to go up 600 points after 1932. 40 years ?

Right. So what does DCA get you in that case…negative returns.

That is a possibility. However, this is where the Fed monetizing debt changes things compared to any previous bear market. We could very will get an anemic recovery, sub 2% GDP growth for a long time, and yet the stock market returns will be spectacular.

Not to make a profit, but because it will retain most of its value due to the essential nature of its deliveries, I bought Amazon. It will probably also go down in price but I am sure it will not go into bankruptcy.

I would not hold much cash now, with the Federal Reserve bankster cartel printing/creating US dollars to infinity. Economics and logic can only be avoided for a time, not forever. If you print enough of any currency, and keep printing more, you will eventually get more and more inflation.

BTW – I don’t concern myself with the PE ratio or what any other metric may be at any given time. I also don’t care if the bear market is a 30%, 50% or 70% tumble from the recent high. I concentrate on the cost-averaging dry powder through to the other side of a typical bear market. Too much too fast, or too slow, and you are going to negatively affect your returns, but even if you screw it up a little you are still going to be fine.

Thanks Wolf. That makes sense. It is a little early to try to predict this.

Labor markets to bear markets, nothing to see here, please move along.

40% of the market is over 65, while 40% of the market is under 35.

20% of the market is left to keep it all alive.

Ha ha…Bear markets all look the same!

As west Texas crude flirts with 20 a barrel, this will all be over in a blink of an eye.

For anyone thinking home prices will fall in Canada read this:

Greater Toronto area Canada sales for the month of March are up 23 percent with prices up 14 percent year over year. Prices will move up parabolic once the Covid19 scare is over with yearly increases of 25 to 30 percent. Mortgage rates will plummet soon once the liquidity crunch is over. The Greater Toronto area is the next California.

It’s gonna be interesting to see if the general economy is in the doldrums and the real estate going up and up.

It never happened before but may be Toronto is special and this time is different.

Realtors in my pace are also that we are special in so-cal and prices would never go down

I just got off the phone with a friend of mine who is a realtor. She said with interest rates this low she’s still selling houses.

OTOH, just driving along my street from the entry gates to my house I see 5 for sale signs. I’m not even counting side streets.

There’s a weird disconnect here.

Michael Gorback,

For a Realtor, “selling houses” means “trying to sell houses.” An average Realtor only closes something like 12 deals a year. Many of them close only a few. So her statement makes sense.

Good friend of mine here in SF said the same thing. He closed a deal during lockdown that was started in early February. But with prices so high, he only needs to close a couple of deals a year to survive. Meanwhile, he is “still selling houses,” um, “trying to sell houses” now, following all the new rules and restrictions, in a market where sellers have massively pulled their properties, and where potential buyers see no urge to do anything.

I was trying to browse your site to see if you had a personal contact email, but you don’t. Anyway, I wanted you to read this article

https://www.ksbw.com/article/new-study-investigates-californias-possible-herd-immunity-to-covid-19/32073873

about California. I was sick in December with a bad “flu” – I’ve had the flu in the past but this flu was bad…I was lying in bed for a few days and heavily breathing with chest pain. I’m young too….only 35 yrs old. Anyway, give that article a once over. It explains possibly why California’s virus number have been so low compared to New York.

Thanks. Interesting. Looking forward to the actual study results. If it shows that a bunch of us already have antibodies, it will make a huge splash, and eventually I might even be able get tested myself (no go, currently).

That said… there is a huge problem with all these corona tests bubbling up everywhere in startup land: they have proven to have huge error rates: too many false positives, and too many false negatives. So if the brand-new test they used is unreliable, the results are worthless. So the first thing to do is to establish the reliability of the test.