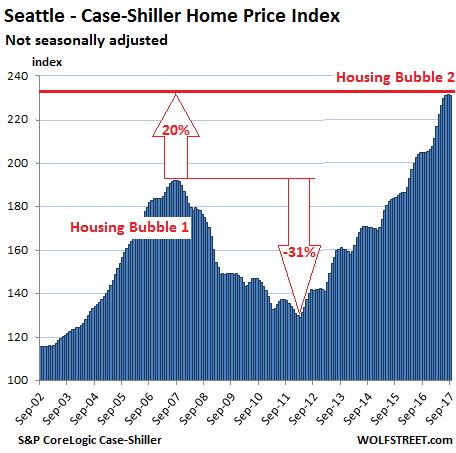

What, first down-tick in Seattle?

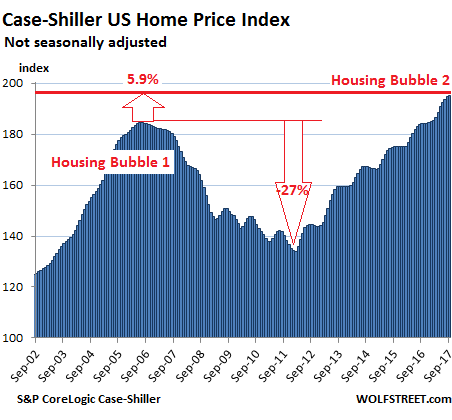

The S&P CoreLogic Case-Shiller National Home Price Index for September, released today, jumped 6.2% year-over-year (not-seasonally-adjusted). By comparison, consumers’ nominal disposable income (not adjusted for inflation) rose only 2.9%. When population growth is factored in, this disposable income on a “per-capita” basis, hence for consumers as individuals, grew about 2%, less than a third of the jump in the national home price index. This disconnect, year after year, adds up after a while.

The Case-Shiller national home price index has now surpassed by 5.9% the crazy peak in July 2006 of Housing Bubble 1:

While real estate prices are subject to local dynamics, they’re also impacted by the consequences of monetary policies, particularly in places where the liquidity flows to. This creates local housing bubbles. When enough local bubbles occur simultaneously, it becomes a national housing bubble. See chart above.

And here are the magnificent local housing bubbles of major metro areas in the US:

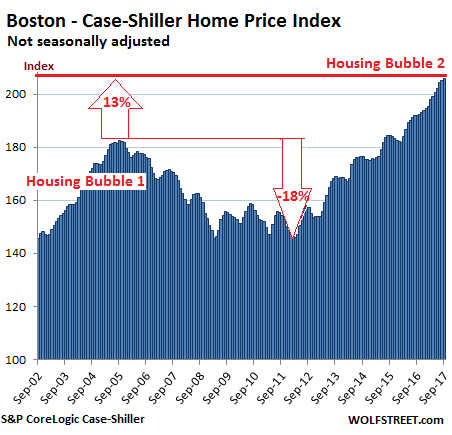

Boston:

The index for the Boston metro area ticked up again on a monthly basis in its relentless manner and has surged 7.2% year-over-year. During Housing Bubble 1, it soared a blistering 82% from January 2000 to October 2005, before the plunge set in. Now, after six years of price surges, it exceeds the peak of Housing Bubble 1 by 13%:

Seattle:

The Case-Shiller home price index for the Seattle metro declined a smidgen on a month-to-month basis from the record set at the last reading. It was the first monthly decline since January 2015! First sign of a let-up? Maybe not yet. The index is not seasonally adjusted, and a slight downturn this time of the year was not unusual before 2015. The index is still up an astounding 12.9% year over year and is now 20% above the peak of Housing Bubble 1 (July 2007):

The Case-Shiller Index is based on a rolling-three month average; today’s release was for July, August, and September data. Instead of median prices, the index uses “home price sales pairs.” It looks, for instance, at a house that sold in 2011 and then again in 2017. Algorithms adjust this price movement and incorporate other factors. The index was set at 100 for January 2000. An index value of 200 means prices have jumped 100%. For example in Seattle, the index was at 230.9, indicating that prices have soared 130% since January 1, 2000.

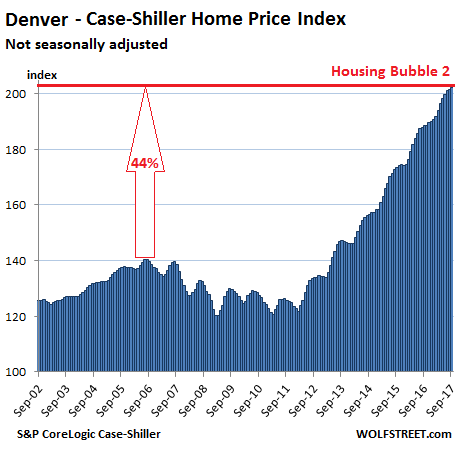

Denver:

The index for the Denver metro ticked up on a monthly basis, is up 7.2% year-over-year, and has surged 44% above the prior peak in the summer of 2006. When Housing Bubble 1 was inflating in many big markets, home prices in Denver gained “only” about 12% in four years but were spared much of the crash that hit other markets on the way down. But in 2012, Housing Bubble 2 erupted with a vengeance:

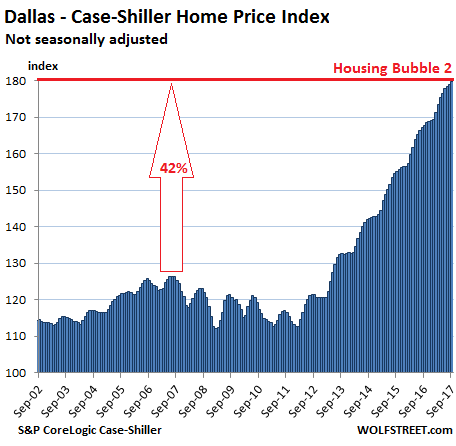

Dallas-Fort Worth:

The index for the Dallas-Fort Worth metro rose again on a monthly basis and is now up 7.1% year-over-year and 42% from the prior peak in June 2007. During Housing Bubble 1, when North Texas home prices rose “only” 13% in five years, a sense of very unwelcome housing sanity prevailed, but this changed in 2012:

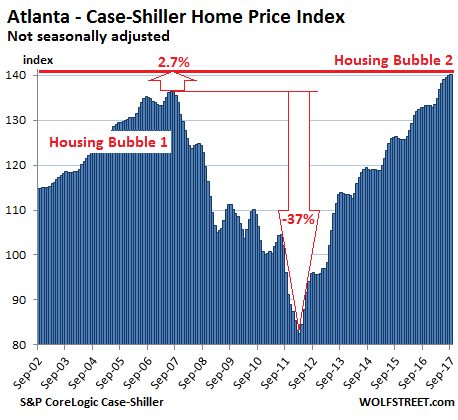

Atlanta:

Home prices rose 5.4% year-over-year and are now 2.7% above the peak of Housing Bubble 1 in July 2007. From that peak, the index plunged 37%. It’s now up 70% since February 2012:

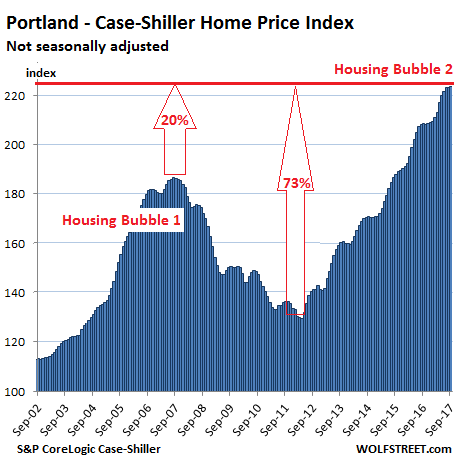

Portland:

The Case-Shiller index for Portland inched up again on a monthly basis, but barely — in line with a seasonal flattening out of prices. The index and is up 7.3% year-over-year. Prices have soared 73% in five years, are 20% above the crazy peak of Housing Bubble 1, and have ballooned 123% in 17 years:

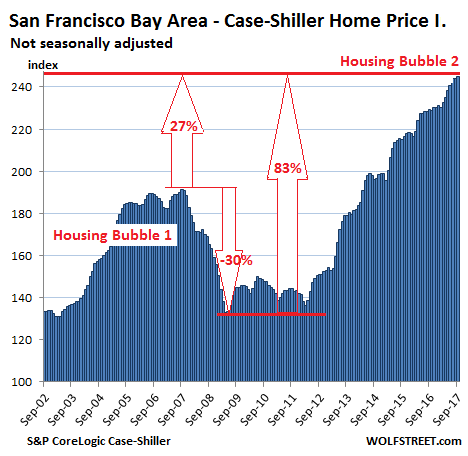

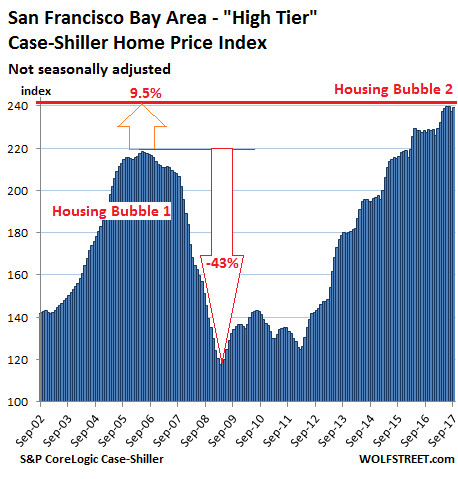

San Francisco Bay Area:

The index, which covers the county of San Francisco plus four Bay Area counties, rose again for the month, after ticking down last month. Monthly seasonal declines this time of the year are not uncommon. It’s up 7.0% year-over-year, up 27% from the crazy peak of Housing Bubble 1, and up 83% from the end of the housing bust, when the liquidity from central bank monetary expansion washed ashore in the Bay Area:

Case-Shiller also offers a “High Tier” index for the five-county Bay Area. This is sometimes taken as more indicative of price movements in the county of San Francisco itself due to its home prices that are much higher than in some of the other counties in the index.

The “High Tier” index has been flat for the past four months and is up 5.2% year-over-year. The index tanked 43% during the housing bust but has now surged 9.5% past the prior peak during Housing Bubble 1:

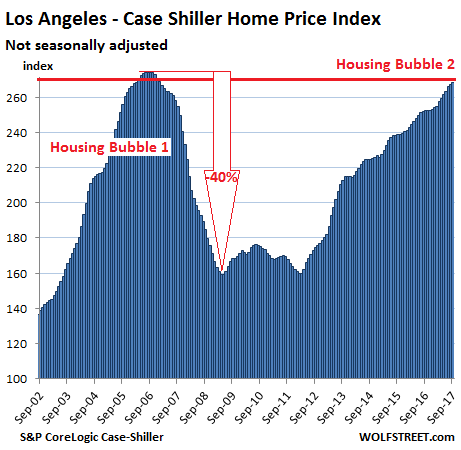

Los Angeles:

The index rose for the month and is up 6.2% year-over-year. Few cities can compete with LA’s beautiful sugar-loaf Housing Bubble 1, where home prices skyrocketed 174% from January 2000 to July 2006, before giving up much of it on the downhill side. The index has skyrocketed since the bust but is still 2.2% shy of its prior insane peak of July 2006:

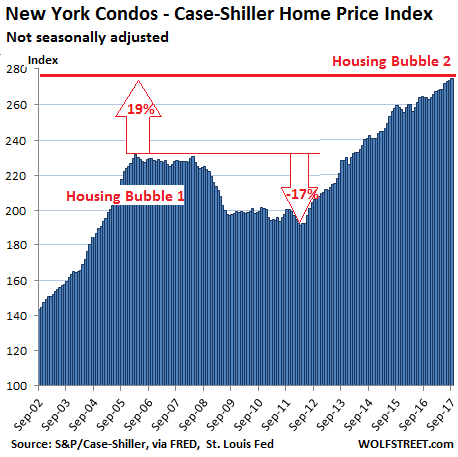

New York City Condos:

The condo bubble in New York City inflated another notch and is up 4.0% year-over-year. The index skyrocketed 131% from 2000 to February 2006 during Housing Bubble 1. It barely deflated during the bust before the Fed’s flood of money inundated Wall Street. The index is 19% above the peak of Condo Bubble 1 and has soared 175% over the past 17 years:

These charts are images of asset price inflation. A home whose price jumps 50% in five years didn’t get 50% bigger. Instead, the purchasing power of the dollar with regards to these homes has been crushed under the Fed’s policies that infamously produced no wage inflation, moderate consumer price inflation, and extraordinary asset price inflation. These policies have devalued the fruits of labor with regards to assets, as housing costs are eating up an ever larger chunk of wages — hence the “affordability crisis” — which doesn’t make for a healthy economy.

The housing market in California is getting tripped up by “eroding affordability and persistently low inventory.” Read… Housing Bubble 2 Hits Rough Spot in California

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What we all want to know, and is literally the million dollar question, how does this end and when?.. Are we looking at a mirror of 2008 or will this be worse with the whole world tottering on the brink? Slum dwellers of San Paolo have squatted an entire city. Are they a harbinger or will some patches hold this together?

I live just north of Seattle, whose madhouse construction has swallowed up suburbs and towns in all directions, but have yet to meet anyone who can afford what’s being built. Now over 70 cranes just in metro Seattle and many more in environs have catered to the tech boomers but we will either run out of techies or those who are being squeezed with rents, now higher than what was considered a decent middle class just 5 years ago, unable to buy what the techies are producing or anything else..

I’m an engineer from Seattle. Over a five year period my rent increased from $795 to $2800. I left the city to escape the seemingly endless rent increases but kept my job (part time) working outside the office. Now I’ve purchased an old VW camper van to live in and I’m heading back to Seattle to resume work full time (with health benefits so I will no longer be subject to the Obamacare tax). I don’t anticipate owning a house or renting again for the rest of my life, as a wage earner my pay cannot compete with speculative low interest hot money so for me housing is a thing of the past (at least until I can retire and get out of the U.S. – I’ll be sure to let the government know where to deposit my social security welfare check.). Anything the ultra wealthy investor class speculate in will become off limits to the rest of us – I hope they don’t start to speculate in grocery futures – and now they have become enamored with old VW’s so my van should continue to appreciate at least as well as a house (but with none of the tax advantages).

I have friends who worked at Boeing and the Kimberly-Clark mill in Everett, before it was blown up in 2012, who lived in motorhomes doing the 3 day stay dance at Walmart and casino parking lots.. These guys were making over $100,000/year but didn’t have the down for homes whose prices were rising faster than they could save for a down payment.. Good luck to you, Van..

“but have yet to meet anyone who can afford what’s being built”

The ONLY people I know who can afford a home are those who inherit them. Based on a chart Wolf posted a while back the median house in OC would have taxes of ~$820 a month or 50% of what my current rent is…….so forget about it when you include the actual payment and insurance….it’s completely out of reach.

I don’t see this ever changing either. I don’t understand WTF these people do for a living that can afford these insane prices.

From where I sit I see no future in the USA.

One more thing, I know a girl who inherited a house and her yearly taxes are less than $1000.

Indeed. Owning a house has become hereditary. Frankly the San Jose I live in is a Dickensian dystopia. I was talking with a lady yesterday whom I strongly suspect was homeless or very marginally housed, who used to work in a wafer fab. She was an “etcher” and “worked with engineers”. I talked about myself being a component-level repair tech and in the late 80s, was able to have an apartment in Costa Mesa just a short distance from Newport Beach, pay my student loans on time, had motorcycles, never cooked at home, etc. We both agreed we expected things to get better, and instead they got worse. And here we were, in our mid-50s, jobless or nearly so. And we’re doing better than tons of people here. The number of people carrying their whole lives on their backs, or in a shopping cart, or on a bike trailer that’s barely recognizable as such; repaired and jerry-rigged until it’s a conglomeration consisting perhaps of an old gate and two wheelchair wheels, the bicycle trailer hitch bar only being original.

And what I’ve seen is a generation that’s dying out now, who participated in the Viet Nam or Korean War, who grew up with vo-tech classes in high school, and had a very good work ethic, so they either came out here or were already out here and worked plenty, because there was plenty of work. So they bought a house in say, Santa Clara, and raised a kid or two, and frankly the kids grew up to be useless druggie ne-er-do-wells. Because their parents coddled them, but also because the jobs are just not there any more. So even if the parent were inclined to, and they’re not because “my own life was hard so I want to make it easy for my kids” they can’t just tell the kid to march over to the factory or join the Carpenter’s Union or something. A job these days in “Silicon Valley” means minimum wage or near it, and for most of these kids they can hustle, selling drugs or engaging in various hustles. And from their viewpoint, various hustled and cons make more sense. And these losers inherit houses. What I describe is not any particular person but a conglomerate; a huge swathe of the population here.

There is a lot of generalizing happening here. Yes, the cost of housing is getting ridiculous, partially due to speculation and partially due to income inequality and the meritocracy. But there are plenty of people who are buying homes after going to college and getting a good job. It’s just that a lot of other people are being left behind. What isn’t talked about is how much having a population concentrated in metropolitan centers is also inflating land values and attracting investors. When will corporations set up in Indianapolis? When will we have a national welfare system so people feel comfortable leaving blue states for red states? Do we need to adjust our immigration policy or is just that we need people to spread out more? How do you raise wages for low skilled workers when there are more of them than low skilled jobs? There is a lot happening but not everyone is living in an inherited house, even in California.

Yes, that’s because she can maintain the lower tax basis her parents had under Prop 13. Her parents likely bought the house for something like 50K so she now enjoys a very low basis. That’s how “average folks” do it!

I inherited two homes in Marin…….and sold both of them so fast—–earlier this year in Jan and Feb— that it would make your head spin.

I moved to West Virginia and purchased a beautiful old three-story Victorian home in a historic district and pay 700 bucks a year in property taxes.

I also purchased a 121 acre farm with an 1860’s solid stone house that needed some work. I rent the house and the property/land to three separate parties

I purchased both properties for about half what I sold one of the homes in Marin for.

Here in the great Mountain State a husband and wife could have Wal-Mart type jobs and still make home payments and do okay.

I grew up in Larkspur/San Francisco and have also lived in Portland. All the metros Wolf Richter has mentioned are hugely overrated. I

truly wonder why many of you still do it.

Someone else mentioned Indiana…..been through there a few times and thought it was really nice state.

Many of you should just suck it up….. forget about the farm-to-table yuppie quant California cuisine, AND MOVE to the heartland and try something new. You never know…you might like it!!

In Seattle there are over 200,000 people that work for Microsoft, Boeing, or Amazon. Assuming spouses work, these families are bringing home over $300k, which is more than enough to afford a $1M home from the bank’s perspective. Add in all the lawyers, accountants, doctors, and small business owners, and there is plenty of salary to go around.

The prices will decline only if we enter a recession and companies have to cut back. A simple drop in stock prices would also do the trick, because people in Seattle have stock based compensation.

Here is the thing. Where did the banks get the money to lend to those 300K salary people? And at what rate? It used to be that banks had to pool money from Alex in San Jose by bribing him a toaster and gave him 4% rate and lend to those Seatle guys at 8%. So if Alex in San Jose is broke, they can NOT lend. That is a mechanism to keep everything in check. If everybody else is doing bad, lending will stop and asset prices will fall and equalize wealth so that Alex can still compete. Nowadays, banks pooled in money from Fed who does the ctrl-p, at 0 rate and lend to Amazon guys at 3.5%, not only that, the institutions funneled part of the money to Stawks and Bonds as well through cheap borrowing leverage.

So “tech” gets compensation from Stawk and borrowed money from banks. Alex is so screwed that he will never catch up.

I am NOT against innovation or evolutionary competition. What I am against is a few guys playing “God” and pick a few friends as winner at the expense of everybody else.

By the way, I am in tech and i get by well. I am saying all of these because I feel the decay around me and I can sense even the tech guys are playing into the hands of the rent seekers and make risky consumption choices and enslave themselves by takin on debt that is stretching their ability to afford. The only winner is the Fed and their friends.

the median “household” income in Seattle in 2015 was $80K. That kinda puts your “families are bringing home over $300k” into question.

And I know a few accountants, they don’t make as much as you seem to think. I had a nice conversation with one over the “giving of the thanks”. She is really worried about the new tax plan cause it’s her opinion that if it passes she will lose half her clients.

what is going on is completely out of wack…..again….. and when the next reality hits I wanna see you back here with the rest of us explaining the how and the why….promise?

p.s. the average Boeing engineer makes $90K…..i just looked it up…..so once again the $300K family income doesn’t add up IMHO.

Everything will continue to be fine as long as the government is ultimate guarantor of the mortgage paper.

Something hasn’t been adding up since about 2012-2013–it’s hard to pinpoint an exact date–in Denver as well and the graph shows that it’s not just my imagination.

The official line is that it’s different this time, which may or may not be the case, but the predictions of wages increases have certainly not borne out–at least not on a level necessary to support the skyrocketing rent and housing prices.

I’m likewise wondering how (or if) this movie ends.

It could be ending as we write but the when and how are the great mystery.. I have taken in step-kid adults that would be either coupled up in small apts with friends or would have to leave the Seattle area. I bought this place in 2010 when the Great Recession was still holding down prices but you’re right about the dates. In 5 years Seattle has gone from a comfortable familiar place to soulless glass towers with a life expectancy of 25-30 years..

I’m particularly watching places like Denver and Dallas, which barely budged during the last housing bubble but have launched into the stratosphere this time around.

Coastal cities like LA and SF you expect to be volatile and pricey, but something is going on when prices in Texas are going up strongly. It was always the case that when the population grew there was endless flat land and sprawl growth in every direction that kept prices from rising much.

The median house price in Dallas is only $180k. The median house price in Fort Worth is only $120k.

Property taxes run about 2.2%, but there is no state income tax.

Prices have a way to go before they hit stratospheric.

“A third round of quantitative easing, “QE3″, was announced on 13 September 2012. In an 11–1 vote, the Federal Reserve decided to launch a new $40 billion per month, open-ended bond purchasing program of agency mortgage-backed securities. ”

“Because of its open-ended nature, QE3 has earned the popular nickname of “QE-Infinity.”

Three canaries that signal: end is near.

An unimpressive painting MAYBE by Da Vinci shatters all previous records by selling for 400 million plus around 50 million buyer’s premium or 450 total. One joke: why was it sold in a contemporary art auction: because it was mostly painted in the 20 th century. Seriously, the photos pre-restoration don’t look much like the final work, and some well known critics doubt that he painted it, although it is from the period.

Second: Bitcoin hits 10k or near it. What is funny about this, apart from the obvious, is that a ‘currency’ this volatile is not a suitable medium of exchange. Which is supposed to be what it’s for.

It was the threat by the Hunt’s (with the Sauds) to issue silver-backed bonds in the early 80’s that provoked the Fed to raise its rate to 18% and also order the Chicago exchange to stop taking ‘long’ silver orders. The silver-backed bond would have been a competitor to the Fed’s greenback.

They can lower the boom on bitcoin but it’s kind of doing that itself.

But this manic behavior screams ‘end of cycle’.

Not everyone will agree with (3) but I think the craze for robo- financial advisers, armed with the magic wand of AI, is a negative indicator.

Does anyone think the Long Term Capital Management gang of Nobel prize, math wizards did their calculations manually?

.

What caused their huge bets to almost collapse world finance in 1998 was not a flaw in their software it was a ‘deus ex machina’ or powerful external event: the Russian default.

Will the robo advisers’ AI also make them masters of geo-politics?

Computers play great games of chess and GO, until someone, or something, turns over the board.

Most value investors Buffet, Faber, etc. complain that it’s very tough to find undervalued assets. No doubt computer programs are good at

identifying small discrepancies in prices, or picking up nickels.

But I think their fanfare as ‘the next big thing’ confirms Faber’s opinion that ‘all asset classes are overvalued’.

I don’t see how Bitcoin can be anything but a bubble. And if it’s a currency why would I spend it today when 6 months from now it could be “worth” twice as much?

And that’s the other thing everyone keeps telling us “idiots” (the Cointards are sure crowing right now it’s getting sickening but then again so are the RE tards) is what Bitcoin is “worth” in real money.

If you wanna call Bitcoin an “investment” i’ll go along with that and that’s about it.

I do not think Nicknsaid anything about BTC being an investment. He implies it is a “currency” threat like the silver backed notes. What is the definition of “bubble”? I hear people use it all the time and nobody ever defines it. The definition I think is reasonable is “Bubble means NOT sustainable due to underlying fundamental asset valuation or economic activity”. So what is fundamental about a “currency”? It is people’s confidence about what the currency can exchange for. In that regard, BTC’s confidence is on the up curve until the .gov pulls out guns and kill it.

Those are all good market signs.

My gut feeling is that this cycle has gone so deep and so subtle that what ends it may NOT be market signs, but political signs to take down FED or simply transfer the issues to other countries through war.

Reason is simple, there is NO more market this time. There is only CB and their friends against the mass. Looking for market signs may NOT help. The sort of domestic movements to take down institutions of external wars is more likely to end this. It HAS come down to this. No more “market cycles”. Therefore, the end is still far until you see “occupy wall street” becomes “occupy the fed”.

No more market cycles? LOL – you can’t be serious.

Only fools would entertain the thought that they’ve managed to smooth out market cycles.

The market will come down at some point, but there is no reason to believe it’ll be next year or the year after, far more likely to be at some point in the 2020s.

Price fluctuation does not mean it is caused by “market”. Used to be I guess. Now adays, it is what ever fed says it is. Call it Fed cycle if you want. My point is one should look for signs of FED, be it policy signs or political signs, market signs are no longer reliable in terms of forecasting price.

The Da Vinci sale isn’t indicative of anything except money laundering.

Clearly the inflated price paid for this painting was related to money laundering and doesn’t signify the impending end of any bubble.

CNBC reported the other day that a whole slew of new investors are using credit cards to purchase Bitcoin and other Cyrptos….

I think next week CME Bitcoin futures start to trade. That can’t be a good a sign for any neophyte who just jumped on the bandwagon.

There are many more signs, but in my mind these two alone could spell some dark days ahead for Bitcoin/Cryptos

The Trump tax cuts should provide a significant boost to the economy over the next 3-4 years at least so there’s plenty more growth to come.

Buy now if you don’t want to be thought of as a fool and be left behind in a growing economy.

Bargains everywhere in real estate – even in this so-called ‘Bubble’ cities.

Thanks for the as usual informative and interesting article Wolf. I’ve been reading the site for a while and this is my first comment.

It seems that property prices have to be pretty much exceeding basically everyone’s ability to make payments…yet people continue to line up to get deeply indebted for the ‘american dream’. One would think that incomes will have to rise somewhat to keep these values inflating or the dreaded asset price DE-flation will begin. Most people have to be stretching their incomes severely to make these payments unless they came in with lots of equity from their previous home.

I hope you will post some more pieces soon about how/why wage growth has been so nonexistent.

The Fed will never allow housing prices to deflate again. If necessary the Fed will provide mortgage financing at negative interest rates. Giving middle Americans an average $250 cut to their mortgage payments (by providing money at subsidized low interest rates) has provided cover for their enormous asset inflation scheme that sent the wealth of the very rich into the stratosphere. After all, how can middle Americans complain about all the money printing and asset inflation when they benefitted as well. The game is over, and if you are a saver (and not a speculator) you lost. If you speculated (in anything – but especially crypto tulips) you made out like a bandit (send Ben a thank-you letter for his self proclaimed courage to act).

I agree. Savers have lost and home/stock buyers have won. Unless debt starts blowing up all over the world. Maybe that will never happen.

That’s what everyone said the last time prices fell 45%.

Down we go!

“The Fed will never allow housing prices to deflate again”

This is the 4th bubble I’ve seen in socal so i’d like to know why the FED “let” the last 3 deflate?

I am in socal and I have heard this “This time is different ” many times

But the fact is .. in socal the real estate has been busted many times before ..

Just personal observations in Seattle seems to show there is no problem with renting or selling the new construction because the techie average base pay is $60 per hour and with OT giving them a very good paycheck. The problem is all of us who have lived here and worked at traditional places where we made real things are caught up in a rising price spiral. A one room with a tiny stand-up kitchenette is $1800/month while a nice upscale one bedroom is $4500/month.. Even well paid Boeing engineers are struggling unless they were owners prior to the boom. The squeeze must at some point slow down sales of cars and retail for everything.. Dollar Tree and Goodwill have been on a hiring binge while Walmarts are less crowded..

People can change the course of this. If people minimized their consumption, shopped for necessities only, and chose Craig’s List, Walmart, Dollar Tree and used goods, whenever possible (which would help ecologically), choose 3-year or older cars rather than new ones, limit themselves to Web services and drop cable tv, and so on, the Fed, & central banks collectively, would be paralyzed. The Fed buys bonds and has instituted measures to keep stocks from sliding too quickly. Are they buying equities or ETFs – backstopping the market? Several (all?) are doing this; China has made that known publicly. The last thing they’d want to have is a market collapse considering that all banks, insurance companies, pension funds, et al, are welded to the market. Of course, the Fed can’t keep the forces of nature at bay indefinitely, so there will be blood. My guess is that they see what’s been wrought from their banking rescue and simply do not know how to stop the monetary cyclotron.

What is confusing me is that housing bubble 1.0 was so bad because of all of the HELOC debt that was used to buy and flip houses. It was a chain reaction that caused so much misery. There doesn’t seem to be HELOC debt, but just large mortgages based on high paying jobs for the professional, tech & creative class. So does this end with a crash like 1.0 where there was a lot of bad debt, or does it just price correct and drag the economy because there is debt, but it isn’t really toxic debt.

Right, as Dean Baker says, this housing bubble is not driving consumption like the last one so when it does pop buyers at the end will lose some money but there’s no wealth-effect. Back then, we used increasing home equity for granite counters, cars, flat screens and vacations that our wages weren’t providing. The financial crisis came after, but it all started with home prices that were rising much faster than historical rates and outpacing rents because house prices would always go up, right?

Right. A price correction is overdue and if you bought anything recently and put down less than 10% you are going to be underwater on your mortgage. But what is the trigger, China’s debt exploding causing Chinese investors to dump all of the real estate they bought?

Impossible…… Consumer Confidence at a record 17 year high.

Probably the downside of consuming too much turkey.

Although I have recommended not doing any shorting, I think I will start initiating some short positions after December 25.

nice if you bought the dip

Wolf your article adds to –

More evidence of the “Everything Bubble”.

Extreme bullishness – especially shorting the VIX ETF’s which now stands at $2.5 billion. How high before margin calls occur?

American corporate debt (junk bonds) spent on share buy backs and dividend pay outs, now stands at $8.7 trillion.

Equity valuations so high as to be stratospheric.

Rampant optimism, ultra low volatility, overly complacent, along with extreme bullishness, spells imminent global market trouble coming ever closer. A massive wave of panic selling causing catastrophic spreads of bid/ask pricing, with corresponding lack of liquidity and spreading global contagion across asset markets. A sellers stampede with little regard to price, valuation or fundamentals. 2008 on steroids!

Not this time. Central banks are standing-by ready to do “whatever it takes”. They will do anything to keep assets inflated and a bid under government bonds even if “whatever it takes” means crushing their own currencies.

When they discovered massive money printing didn’t immediately lead to hyperinflation they became complacent with regards to inflation, now the whole world is addicted and all roads lead to hyperinflation – plan accordingly. It’s amazing that the Fed now talks about an existential need to maintain inflation above 2% and this shocking change to their mandate of “price stability” isn’t even news.

We have crossed the Rubicon and the die has been cast, nothing left to do but accept your fate and if you are not in the protected class your fate will not be a happy one. Caesar is coming.

you are starting to sound more and more like a troll. Not too bad of one as trolling goes but still a troll. You have all the troll triggers covered, touche!

Troll?

That would be an opinion – yours.

Where is your factual counter point?

If you believe the governments inflation numbers, then your Big Mac should have cost you $2.43 today.

So what did you pay today for your two all beef patties, special sauce, lettuce, cheese, pickles, onions on a sesame seed bun?

Heckova job, Ben & Janet.

When millions of Americans become destitute after the next housing bubble & market crash, maybe they’ll FINALLY become pissed off enough to end the Fed and its rackets.

The Fed is doing the bidding of those who control the Fed and it’s not the working or middle classes. It’s a racket but not because the Fed exists but who is controlling and benefitting from what the Fed does.. Some see a “political class” as the beneficiary but they are nothing but messenger boys scrambling for scraps tossed by their real bosses.. it ain’t us..

Here’s the deal in Seattle. It requires two working professionals to make enough to own a home here that you’d want to live in. By professional I mean each partner is making $100k or better and the two of you have no other debt. If your household income isn’t at least, at least, $175k/year, forget about living in a nice part of Seattle. The Eastside is out of the question.

My wife and I both fit this category and buying here is a stretch.

Seattle isn’t even a very nice place to live. I’m going to hunker down in my van and work another couple of years but those days will pass like a lonely prison sentence. I think gold is a terrible investment but it’s one of the only assets that has not quadrupled over the last nine years so I’m going to save almost every penny I earn and buy gold with it. After two years I’m getting the hell out of here – good riddance to bad rubbish (and loud traffic and mold and drizzle and …misery)

It wasn’t too many years ago that my sister and brother-in-law could not sell their house in Kirkland for almost 18 months. They staged it and finally rented it for a year to some UW students. I figured they were lucky, when they finally sold, to get around $400 K for it. But it is all relative as they had already relocated and retired by then. It would probably fetch a million+ these days, being on the edge of Bellevue. It sounds nice, but the roar of the 405 (1 mile away) was louder than the Oregon coast!! The lifestyle was horrible in my opinion.

Certainly, now is not the time to move to any of these cities; if ever.

My mantra: get some transferrable skills that will be needed anywhere/everywhere, and get out of high-priced Dodge. These skills do not include coding or anything to do with computers. People will always need health care or some plumbing done. Game design or app const., not so much.

On a parallel note, I have noticed the proliferation of motorhome living in all areas, not just in high-priced cities. I live rural and see it everywhere. On my last trip to town I noticed a packed rv site behind a small gas station and convenience store on the outskirts. There must have been 30 rvs tucked away. About a km from where I live a guy is putting in a small trailer court. Many are travel trailers, (2″ thick walls). They are prone to leaking so the big trend is to put up a roof over them. You can buy a used singler-wide mobile for 5 k plus towing. I have even seen them posted for free; just haul them away. People are buying them and throwing them on rural lots; lots that sell for around $50,000.

This was interesting: (Lots more on a quick search)

40 Acres Anaconda, Deer Lodge County, MT

$179,000

Make an offer on this unusual larger parcel, with great access right off of Montana Highway 1. The level land provides a great mix of grass, sage, trees, wetlands and seasonal and year round ponds. With plenty of pasture and grass, this is perfect for horses. Mountain…

Re: motorhomes, there is an entire colony of RVs in the parking lot by runway 25L at LAX where airline pilots live. I can remember when that was a well-paid, prestigious career.

My young daughter was going to leave Chicago for Seattle and got a job offer of $90,000 and refused it because once she tabulated rents or trying to buy anything besides a shack 2 hours away that $90k wasn’t enough.. I find this shocking.. Your description is spot-on..

Luckily Housing bubble 2.0 is subject to location. There are plenty of cities in the Mid-west that are still below Bubble 1.0 even with supper low interest rates.

Bubble 1.0 was everywhere as much of it was subprime based. I own a rental house that rose from $55k in 2002 to $80k in 2007. Right now market value would be $57k. Just barely above the 2002 level. This area was low income and subprime haven in the mid-2000s and lots of foreclosures

Bubble 2.0 is more localized in Cities that command big salaries and have good credit or it is where Chinese investors want to park money.

If you can’t afford a house, or the rent, you could look to a second/third/fourth tier place and you will have a better quality of life, probably a lower salary, but more in the bank at the end of the month.

Toronto is nuts in Canada for housing and rent. A young person can go there because there are plenty of jobs … and city life … but it is bloody expensive. A friend recently graduated from uni, said no to T.O. and moved to Windsor (across from Detroit). He makes less money, but his rent for a 2 bedroom is $750/mth (less and US$600) which he shares with his girlfriend, so US$ 300/mth each. He now saves 1/2 of his take home pay -something that would never happen in a big city. Oh and his commute time is less too … and you can buy a not bad older house for about US$150,000

I grew up in Windsor in the 70’s and 80’s. It was a great place back then, plenty of manufacturing and engineering jobs meant a lot of kids into electronics and computers. Now that manufacturing has been hollowed out and moved to China and gambling moved in Windsor has become Canada’s meth and opiate capital. It’s a sad place to live.

I live in LA now, and I wouldn’t move to Windsor if the houses were $1 each.

What is so good about Portland Oregon, nothing is booming here. Then why house price going up and up .

Portland is booming because it’s an “it” place to live–hip, beautiful, and filled with people “just like you”. It’s not driven by industry or jobs, more by people wanting to live there and get in on the good life–even if it turns out they can’t afford it.

I believe the biggest factor driving these price run-up is low supply in desirable cities and desirable areas within cities. That is because Boomers are not selling. That is because they can’t retire and don’t want to take a step down in housing…..and they like to see their paper wealth increase.

Remember, prices are set on the margin. When supply is low, only a few sales will move the price point up.

Now rental will at some point disconnect as more supply continues to come on the market. That is because developers are stupid and also because they think the Fed will bail them out if things get really bad. And the Fed will bail them out and turn over the properties to HUD and they will become subsidized housing units. This was Obama’s great housing strategy before leaving office (IMHO).

We live in interesting times.

There is no limit to how much money the FED can print other than their own discretion. They can also buy at their own discretion assets and hold them to maturity or forever. Rules of the game have changed since the last recession.

The FED is the master of the world, anyway you look at it, our democracy and rule of law has been perverted. Who gave the authority to the FED to print trillions out of thin air to buy failing private assets?

House prices are going up and will go some more as people have seen the light, when unelected Fed officials can print trillions out of thin air to buy assets, there is no other protection for the working man than buying a house.

House price increase is a reflection of our money being devalued. Eventually prices of everything else will catch up, I dont think home prices are coming down.

Yes lots of people in Tokyo thought like that in 1988.

Nothing was ever going to go wrong then, either.

“By comparison, consumers’ nominal disposable income (not adjusted for inflation) rose only 2.9%.”

Sounds like housing is a bullet proof, high quality investment as long as interest rates stay low. As december will likely be the last rate raise by the FED for years, its time to enter into the housing market with both fists.

There is no ‘right way’ to make money. You will survive and reproduce if you have money, you will die if you don’t make money. Evolution only selects for those who repoduce, not the people pining for some perfect world.

Thus the jack off frat kid using his credit cards to trade stock on margin in today’s world will reproduce and prosper while the austere hard working person who shuns risk is doomed to failure.

So grab a drink, get that 4:1 leveraged margin account and prosper! Bitcoin is coming to real estate and now the real action begins!

“As December will likely be the last rate raise by the FED for years,…”

Don’t count on it. They keep saying the “neutral” rate is 2.5% or so. And they’ve set their eyes on it for now. That’s five or six rate hikes away, just to get back to neutral.

Wolf,

How does the Fed measure the “neutral rate”? Is it the 10 year or a mix of bonds? Where is the neutral rate currently?

Thanks.

Gears be stripped (engine roar) purrs like a kitten!

They don’t really know. It’s a concept or an idea, not a fixed number. But they keep saying that it is lower than it used to be and “likely” in that range around 2.5%. That makes sense because that’s just above the current level of CPI inflation. If CPI inflation goes to 4% for a longer period of time, the neutral rate would be above 4%.

It wasn’t the 17 quarter points it was the talk of 18, 19 and twenty that set stage for Hank darling back in the roaring ’07’s?

Well that all depends on one’s definition of the word ‘failure’, Dennis.

Failure to be a spiv is no failure as a human being in my book.

Once a society turns to financial speculation rather than production as its method of sustenance, then you know that society is deep into its decadence phase and decline is soon to follow.

The working person who actually creates product will have his/her day again soon enough. That is the cycle.

Bravo? Here’s a dollar back from the 225 gazillion we owe you! Bravo?

When you see Hank Paulson on the A.I. its to ring the bell? Is James baker still our guy in Argentina and the city of London? Daddy can I ring the bell? No son bells are for winners!

Bail in bail out!

Bail in bail out!

And two three four! Work it people…….!

Is my new drum skin ready? Can’t keep the ship going without strong beats.

Low-end priced homes are in high demand right now in many RE markets around the country. I think, this is a sign the market is running out of gas.

The ~4% mortgage is still making these homes much cheaper to buy than to rent, in many markets. The cycle is getting old and the Fed is raising rates, albeit slowly. But this will effect mortgage rates, eventually. Low down payments and looser underwriting have become more common and now the FHA is raising thier price limits. The deck is looking stacked for a decline in prices.

Where I live a lot of the housing is purchased by what I would guess are foreigners on work visas or green cards or what have you. If the job market goes South a bit, I would imagine that unlike me they can walk away and return to their home country without any real recourse from the bank. That could happen on a large scale, further depressing home prices.

I know that the local IT contractors tied up in the Democrat ordeal did just that, but took out large HELOCs on their properties they were walking away from before returning to Pakistan (With their HELOC cash.)

The entire build boom is a ill conceived plan to gain critical assets in industrial areas before the next big financial disaster. The disaster will , in my humble opinion, not be a bank crisis, but a much more profound dollar crisis. Wall Street is on the way to pull off the biggest heist ever…they will buy all assets and crash the dollar causing hyperinflation wiping all debt from their balance within a day or two.

//// My model step-by-step

/

1) Inflate the stock market to sell off my stocks, and pull out as much cash from the people [check]

/

2) Diversify my assets to lower risk, bitcoin, real estate, gold, foreign debt bonds [check] – gold breaks this pattern as it has not significantly gained value, don’t quite understand why

/

3) Install trolls in all relevant government regulatory bodies allowing full control [check] – this was probably step 0

/

4) Don’t silence the media, make them a partner in the crime of the century [check]

/

5) Wait for the winning ticket [in progress]

/

////

The answer is simple and repeated over and over again in these comments. Get out of Seattle, California, and the other bubble locations – DUH. Plenty of affordable housing in the South and mid-West.

Just from personal observation one cannot overlook the foreign buyers. Past few years in OC Asians have been buying like crazy. Honestly a higher tax rate should be imposed on all-cash foreign buyers looking to “park” their money here. They’re escaping taxes at home by swallowing up properties in the US while at the same time depriving our citizens a chance to own home. As for affordability…if they’re not all-cash non-residents hiding money then they’re still usually resident Asians that have 8+ people in the house all contributing to the mortgage payment. For example a Filipino “family” moved nearby recently and by family I mean the in-laws, cousin, uncles etc…the whole clan lol Maybe as Westerners its time to rethink our whole concept of the family unit.