Pointing at “excesses,” “distortions,” and “imbalances.”

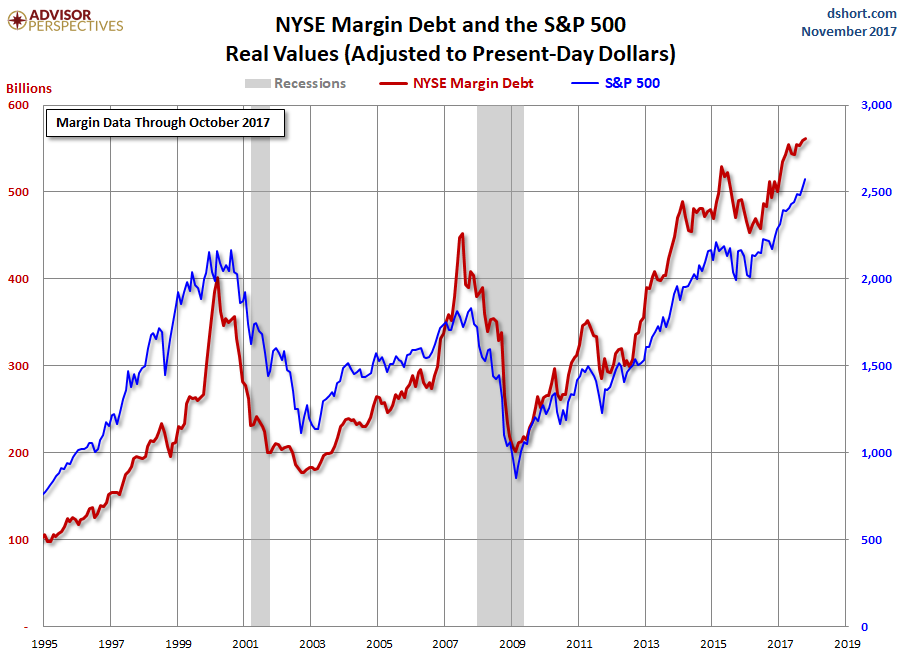

Margin debt in the stock market hit another record, $561 billion at the end of October, up 16% from a year ago, the New York Stock Exchange reported on Tuesday. Margin debt and the stock market move together. And even on an inflation-adjusted basis, the surge has been breath-taking.

This chart shows margin debt (red line, left scale) and the S&P 500 (blue line, right scale), both adjusted for inflation to tune out the effects of the dwindling value of the dollar over the decades (chart by Advisor Perspectives):

Stock market leverage is the big accelerator on the way up. Leverage supplies liquidity that has been freshly created by the lender. This isn’t money moving from one asset to another. This is money that is being created to be plowed into stocks. And when stocks sink, leverage becomes the big accelerator on the way down. When stocks are dumped to pay down margin debt, the money from those stock sales doesn’t go into another asset and doesn’t sit around as cash ready to be deployed and it doesn’t go into gold bars either. It just disappears.

Even the Fed is now worried about margin debt and a slew of other factors not related to consumer price inflation but to assets, asset prices, and debt.

The latest was Dallas Fed President Robert Kaplan on Monday who, in discussing financial and economic imbalances, specifically addressed the “record-high levels” of margin debt.

His premise is that “there are costs to accommodation in the form of distortions and imbalances,” and when “excesses ultimately need to be unwound, this can result in a sudden downward shift in demand for investment and consumer-related durable goods.” Kaplan:

It is of course possible that “this time will be different,” but as I assess the condition of the U.S. economy, I am carefully monitoring evidence that might suggest growing risks of real imbalances, which could threaten the sustainability of the current economic expansion.

Among the excesses he is “monitoring”:

- US stock market capitalization is at 135% of GDP, “the highest since 1999/2000.”

- “Commercial real estate cap rates and valuation measures of debt and other markets appear notably extended.”

- Stock market volatility is “historically low.” He adds: “We have now gone 12 months without a 3% correction in the U.S. market. This is extraordinarily unusual.”

- Corporate debt is now at “record highs.”

- US government debt held by the public is now at “75% of GDP” (with the gross national debt at 105% of GDP), and “the present value of unfunded entitlements now stands at approximately $49 trillion.”

- “The projected path of U.S. government debt to GDP is unlikely to be sustainable – and has been made to appear more manageable due to today’s historically low interest rates.”

Trading volumes of bonds and stocks have “markedly declined,” he says, pointing a NYSE trading volume that has plunged 51% from 2007 levels, even as the NYSE market cap has soared 28%.

Margin debt has reached “record-high levels,” he warns: “In the event of a sell-off, high levels of margin debt can encourage additional selling, which could, in turn, lead to a more rapid tightening of financial conditions.”

During a sell-off, “sufficient market trading liquidity is key to managing the resulting increased volume,” he says. But liquidity from margin debt vanishes during a sell-off, just when the selling kicks off in earnest and liquidity is needed the most.

His worries are interesting for another reason: It seems he doesn’t exclude the possibility of a sell-off despite assurances by many that the Fed would never allow another sell-off – that it would instantly step in with another big round of QE. But he doesn’t seem to be worried about the sell-off but about liquidity in the market during a sell-off.

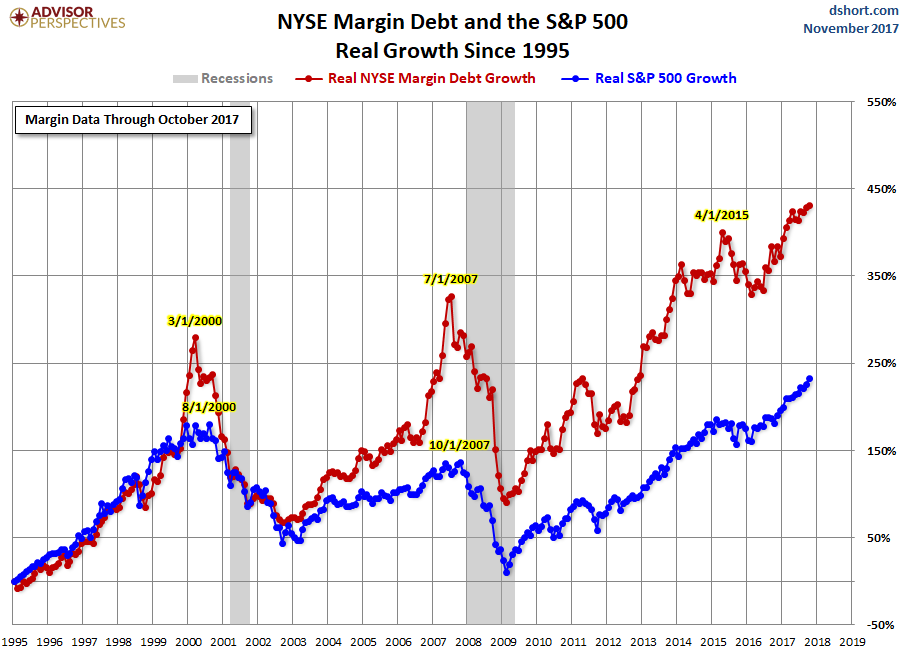

So by how much has margin debt exploded? The chart below shows the percentage growth of inflation-adjusted margin debt and the inflation-adjusted S&P 500 index. Note how much faster margin debt has increased compared to the S&P 500 index in recent years (chart by Advisor Perspectives):

But this is only the reported stock-market leverage. It accounts for only a fraction of the total leverage in the stock market. Stocks can be leveraged in many ways.

For example, executives often borrow from their company to buy their company stock and put up those shares as collateral. Or larger players, such as hedge funds, can borrow at the institutional level to fund stock purchases. Then there are securities-based loans (SBLs), offered by financial firms to their clients. These loans can be used to buy anything, such as a boat or a vacation. They’re called “shadow margin” because no one knows the magnitude, but it’s huge, and it’s booming.

What the Fed is worried about is a replay of the last financial events – such as the 57% decline of the S&P 500 during the Financial Crisis – that were amplified by margin debt. Stock market leverage, all types of leverage combined, not just margin debt, is considered the best thing since sliced bread and makes everyone rich as long as stock prices are rising. But stock market leverage turns into a time bomb on the way down.

Kaplan is among a number of Fed governors who’ve indicated in this manner why rates need to rise (albeit “gradually”) though inflation, as the Fed defines it, remains below its target: It’s about asset prices, debt levels, and risks. They don’t want a repeat of 2008/2009. It seems they want the bubble they created to deflate gradually so it doesn’t take down the economy.

What, a first down-tick in home prices in Seattle? Read… The US Cities with the Biggest Housing Bubbles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

We must always be careful about assumptions/presumptions, but activity the last few days has a modest smell of “capitulation”. The index/passive managers own the market, and ride its’ advances and declines without much repercussion. The active managers are holding on for dear life, as individual stock price volatility and price dispersion have made it basically impossible for them to beat the market. Are we seeing “capitulation”, as active managers fight for their existence and survivability?

I have been in the institutional arena my entire career (35+ years), and the valuations and other traditional metrics used are screaming to me to get the hell out of the market.

It is never “this time is different”, it always ends the same way.

This time, it’s different (ha ha ha).

Too hilarious. Ms. Yellen is shocked, SHOCKED! to see gambling going on in this establishment.

After over $20 trillion of printed fiat currency the Fed wonders why assets have exploded in value.

Let the record (and history books) show the Fed’s only concern during this era of free money was that inflation was inflation too low! More and more inflation is the Fed’s solution for every problem – easy solution for anyone who has never had to work to earn dollars.

They worry about it, but they don’t do anything about it. Spineless fools.

On the contrary. the FED is not worried about anything as they and the banks will always be isolated form their bad management. This is just part of their continuing disinformation program. Margin debt only grows because they allow it to do so.

I agree. My understanding is the Fed has considerable power to discourage/reduce margin borrowing but have they actually used that power? Nope. Only talk talk talk.

“Show me the money” Mr. Fed, cause you ain’t got any when it comes to actions.

Well, if they did the responsible thing then all the money guys and the right-wingers would scream that they are “throttling the economy” and “working to undermine the duly elected President” and “stifling growth.” Since we have no fiscal policy worthy of the name (other than throwing money at the military industrial complex, the medical mafia, and the insurance companies) all they can do to stimulate the economy is create endless liquidity and allow idiotic levels of leverage. There is no Plan B.

Well James Levy,

IMO the Fed can do something to benefit the broad working class economy: Buy up student debt and announce a permanent suspension of payments until further notice, in affect zeroing out debt amongst the very people who will turn around and spend the money they now have into the general economy…as opposed the Fed’s current policy of giving ever money money to the Ultra Rich.

They have started to do something about it, in tiny baby steps: raising rates and unwinding QE.

“Tiny” is the operative here. It’s the old “soft landing” business.

James: I don’t know if you’re old enough to remember, but Paul Volcker was railed against by Congress and every financial type out there. He calmly smoked his cigar through it all. I thought it was just political theater. We get nostalgic and think he was wise, the right thing to do. I’d say he was lucky. People believed that he would slay inflation, so he did. Robt. Shiller reminds us that inflation is fueled by belief – belief in the stories we tell and retell.

Indeed. They’re all praying for a soft landing. Because the alternative would be ugly.

Indeed. They’re all praying for a soft landing. Because the alternative would be ugly.”

Not only that, a controlled soft landing (if possible) is “Their Job”.

Again to the comment you replied to No matter what the FED does, for a segment of the Population, it is ALWAYS wrong.

As soft landing is in the interest of all, except the Bottom feeding Predators/Scavengers.

No worry.

“Investors” need only escape to bitcoin – it hit $11,000 yesterday.

Bitcoin seems to be valued in dollars but it’s not. It’s valued in tethers. Go try to redeem those tethers for dollars at 1:1 and see how far you get. Bitcoin’s valuation is in USDT.

All the FED has to do then is prevent a sell-off and Just keep buying forever. Pretty soon there will be only one buyer of all things: the FED.

So is bitcoin a currency or an investment?

AND why are you quoting it’s “value” in what the cryptotards claim isn’t real money? I heard one cryptotard call the US $ toilet paper and then proceeded to tell the group it’s “value” in the same.

Why would I buy anything with a bitcoin when it’s “value” will be double within………you pic the time frame…….??

bitcoin is in a massive bubble.

I suspect that margin trading is now a major source of profits for the discount brokerage firms. The interest rate spread between the Fed funds rate and retail margin interest rates has widened out considerably since the Great Recession even as online stock commission rates have tumbled.

The interest on all that margin debt has to be several dozen billion a year. Margin loans are not at the low rates that treasuries or even HYG are at.

Nov 28 (Reuters) – Wall Street indexes hovered near record levels on Tuesday as investors digested comments from Federal Reserve chair nominee Jerome Powell and shrugged off concerns over progress of the U.S. tax bill.

doesn’t sound like the Fed is worried at all. I have been looking at a number of charts and it leads me to the conclusion that a rate collapse is likely. Inversion of the yield curve. If the Fed is doing the Twist II, it hasn’t registered, and it may be the bond market is too big to steer around easily, and the Fed is busy dropping old paper, if that paper is of the correct duration they should be able to lift long term yields. They have a saying in the Fed, “don’t fight the markets”. The markets think win win, financials have lately diverged, but yesterday got almost all of it back. The market is are certain rates will rise, and bankers profits, and that there will be ample liquidity. The charts are less sanguine.

Buybacks are contractionary.

I haven’t felt that way since about a second ago.

The stock market is one place where the real inflation takes place. So borrowing cheap in the artificial world while beating the inflation in the real world makes perfect sense. The question is, who created this upside down environment?

“The Russians”, obviously…

Mr.Richter;

Don’t expect DJIA fall any time soon.Or even in a predictable future.It may dip a little bit.Then it will rise again.And after that it will soar.Because now it is Federal government’s sacred duty to keep it up (and rising).

The Working Group on Financial Markets (aka the Plunge Protection Team),created by Executive Order 12631,signed on March 18, 1988, by United States President Ronald Reagan:

https://en.wikipedia.org/wiki/Working_Group_on_Financial_Markets

The Washington Post. February 23, 1997-Plunge Protection Team:

https://www.washingtonpost.com/wp-srv/business/longterm/blackm/plunge.htm

So did they fall asleep during the past downturns and crashes?

Wasn’t a fed governor recently talking about buying equities in the event of a down turn as the Japanese have done?

The FED does not have the authority to buy anything other than bonds. Congress has to approve any expansion of FED charter to include “a broader range of assets” as Yellen asked for at JH last year. This is why the FED is not a “true” central bank. Clinton was said to favor Brainerd as Fed chief, she shared the goal of an expanded buying mandate for the FED. the only “other” way that the policy can be bridged is by emergency declaration, which you know how that works after 2008. Will the FED get the authority, and is this game with the SNB just another subversion of the rule of law, or the authority of Congressional lawmakers, like secondary market for UST in Belgium. China dumps UST and Belgium buys it.

The danger in this is that backroom deals fall apart faster than the other kind, and private debt creation eventually overwhelms the public debt bureaucracies ability to manage things, mortgages in 2007, which is outside FED purview, and now mortgages (and subprime consumer) again and Bitcoin. If the market crashes the FED will be driving it, because control is more important than nominal gains in the stock market.

“like secondary market for UST in Belgium. China dumps UST and Belgium buys it.”

Russia and china have secondary holding entities in Belgium as do several other nations .

They dont Dump UST in Belgium they simply Move them off of their national books, then use them as and when required. Iran also has a facility there.

Every time their is global tension with the US. A large volume of UST moves into Belgium previously held by Russia and frequently china.

Nobody “Dumps” UST as currently their is massive Demand for it.

This is why china can sell Long Term US Dollar Denominated bonds, as fast as the keyboard operators can enter them. To the Limit they want. The problem with those US $ chinese boinds is will chian pay in $ on maturity or at all.

The Possibility always exist that UST may again become undesirable as it did under LBJ and early Nixon, when the US had to Issue bond’s in Other Currencies for a short time.

That was the result of global displeasure, with a very long running, very expensive war. That benefited the planet, that most the planet did not want to Participate in, or assist in the financing or of.

Then french also forced that situation. By demanding gold in exchange for Mature UST. Which forced the end of “Bretton wood’s”. The french (A Self obsessed Evil Race) have a lot to answer for.

TARP?

Yeah,I was not there to wake them up.

“Come on-lemme show you how to twist

You wanna know how-it goes like this ! ”

(very old song):

Trading begins.DJIA starts falling.At about 10 a.m. PPT finishes their customary fed-gov-employees-morning-cup-of-coffee and starts ACTUALLY working.DJIA stops falling.Then it starts rising.Then it soars.

What is more important is who makes money off those depressingly regular DJIA morning dips.

“I cannot forecast to you the action of PPT. It is a riddle, wrapped in a mystery, inside an enigma; but perhaps there is a key. That key is ??? interest.”

-adapted from Winston Churchill

“What is more important is who makes money off those depressingly regular DJIA morning dips.:”

ME VERY REGULARY.

The FED contrary to your BS comments is not the buyer on the upswing.

They step aside when losses are being socialized and they assist when gains are being privatized.

This is the essential key of the financial system and it’s the only explanation for why/how it can recover from unsustainable leverage ratios.

“Whatever It Takes” means exactly that.

Mean – I don’t “get” most of this being a saving-pennies-in-a-coffee-can kind of guy, but I think this scary chart might fit in here since even I understand the velocity of money (M2)

https://fred.stlouisfed.org/graph/fredgraph.png?width=880&height=440&id=M2V

alex,yes and what might we anticipate happens to money velocity m2 when, if ever, the FED stops paying interest on excess reserves?

https://www.economist.com/news/finance-and-economics/21718872-or-interest-fed-pays-them-vital-monetary-tool-benefits

Unlike ’29 crash which caught everybody (well,almost) by surprise and crash of ’87 caused by recently introduced automated trading 2 crashes of ‘2000s were staged events.Like sinking of “Maine” which led to annexation of Cuba.

√

That’s a radical statement there, d.

This site has no up vote system.

(√ ) Works the same.

It looks more like a check-mark, though, or a bit like a down arrow? How about ^ ? I’ve seen ^ used on other sites.

I got the meaning of d’s check-mark. It works for me. He’s been using it for a while.

The Fed caught in a trap of their own making.

Being the buyer of last resort, only there’s no liquidity with which to do so, outside of the printing press. To “normalize” rates would be cutting their own throat, as servicing their ongoing debt cost would be prohibitive.

The higher margin debt is compared to GDP, the more the economy is dependent on credit; And the bigger the accumulated debt is when compared to GDP, the more likely it is that a reduction in credit will cause an economic crisis.

If the Fed prints – and it must – the currency value is reduced. If the Fed raises rates to protect the USD value – which it can’t – the economy tanks.

Damned if it does. Damned if it doesn’t.

There is a break point. Always. Awaiting this occurrence. It comes.

None of this is by accident, it’s intentional. The FED knows they’ve enabled the greater fool trade b/c that’s their job, it’s what they do.

When will people wake up?

Deficits rise and eventually the government is out of assets, and unable (or unwilling) to raise revenue. Their assets are being looted by private companies, and if you are a bit slow to pick over the bones of the US government, or demand your share in the booty, from the bigger vultures, then you will be the loser.

I agree.

Good post.

Another issue to consider is that the vast majority of the $20 trillion owed by the State, is owed to American citizens, and is not to foreign holders of American debt.

If America were to default on it’s debts, it would be the American citizen who would be defaulted upon by the State.

It (raising rates) might be kind of like dieting, very easy to talk about, harder to do.

Besides, the rich need their “job creating” tax cuts, everything else is secondary and can wait.

Not to worry.

The Swiss Central Bank proudly prints money to buy equities for profit. The ECB buys common everyday commercial debt which allows cash to go anywhere, including places where negative rates are not an issue, such as US equities. A couple of billion a month in Fed balance sheet reductions is overwhelmed by these two.

Equities have more to run. The Fed is a bystander. The others combined with the BOJ are crazy, or possibly criminal but legal since there is no law preventing them from printing with abandon. Interesting times are a certainty. Just not tomorrow.

Out of curiosity … could it be or should it be an offense against a nation if one country’s central bank manages its printed currency in such a way that it causes other nation’s financial markets to go to 11 and bring high risk to the savings and investment of the citizens?

Should the Fed’s management complain at how the ECB, BOJ, SNB, and others make them work harder to compensate for the excesses of others?

Didn’t fed do the same for EMs for a decade or so? They complained but Bernanke insisted that US Fed only looks for US interests, and EMs have to institute their own capital controls. US banks were emitting credit like no tomorrow, but credit was bidding up all the world except USA. This happened between 2002-2011.

Yeah, well, that was then. Today, is different.

What about leveraged ETF? How do they fit into these figures? (Beyond the fact that they themselves can be bought on margin.) Are they considered some kind of “partial” derivatives?

As long as banks can create deposits we are all slaves.

You got that right! What I’m wondering is: what becomes of the slaves after they are replaced by machines and no longer needed? I think things will only be getting worse for the debt slaves in the years to come.

Make no mistake about it, as long as you don’t personally own all of the resources necessary to support yourself, you are a slave of one form or another. Banks creating deposits or not.

Stan, learn elementary accounting. Banks deposits are bank liabilities. As loans are spent, cash is reduced and the offset liability is reduced. The books remain in balance. If banks want to lend more, they need to raise cash or wait for loans payments to be received. Hoodoo about the evils of deposit creation are nonsense meant to exploit the economics uneducated and fearful. If you understand elementary accounting, basic T-accounts illustrate the harmlessness clearly.

That’s the way it is supposed to work.

In reality, the Fed can simply create money out of nothingness.

This money is then injected into the system.

Banks can lend it out if they think that they can make a profit.

Nothing of ANY real value has been created.

It’s all digits marked on paper and electrons.

The banks now have a stake in real-world assets that they did NOTHING to deserve.

If the loan goes bad and the bank is about to fail, what happens?

The “losses” are socialized by a merger or creating a “bad bank” or some other subterfuge.

Money is created out of nothing and backed by nothing real such as gold or silver. Profits are privatized into the pockets of the bankers. Losses are socialized by either taxpayers bailing out banks (TARP) or central banks creating money out of nothingness to “buy” the “assets” that are total crap and worth next to nothing, but listed at full value on the balance sheet to preserve the illusion that the bad loans are still live rather than dead weight.

Meanwhile, all of the money created out of nothingness is inflating asset values in the real world like a balloon, and this spasm of inflated asset values with no significant increase in productivity is misinterpreted as “bullish”.

Your interpretation of the “elementary accounting” assumes that the value of money is real, the assets are actually valued correctly, the accounting is honest, and the books are not cooked like a Thanksgiving turkey.

If we lived in the 1950s when people were still mostly honest and crooked bankers were actually arrested for committing crimes, then your interpretation would be correct.

It is a sad fact that fraud is now the rule rather than the exception, and deception is now the standard rather than honesty.

No, you got it right until you went off like a gold sales person and then and confused central bank monetary creation with simple accounting debits and credits, as in normal everyday bank accounting. Then you conflated a set of larger frauds with simple car loans and checking accounts and how basic accounting records their activity. Really, get a real education, not the gold sales view of modern economic activity.

Agree excessive money creation is a root of much evil and that economists are substantially pinheads or complicit with bad people who depend on printed money for various ends.

Even yesterday, Kashcari bleeted about how the Phillips curve must be right in some way because it seems so correct. The Phillips curve relates employment to inflation. It assumes causation. Rather, it reports correlation. The real association is inflation with disposable income. Jobs create inflation when jobs create income as a byproduct. The income and spending it create the inflation. Interest income would create the same inflation. In the past, normalized rates contributed to income generation and the inflation that had no problem hiding. Today, with artificially low rates, there’s far less spending and far less inflation. Yet, economists can’t see it. As I said, pinheads.

Emanon,

Sorry, you got it all wrong. If the money they create has no value, then it should have the same effect on the economy as a pile of dirt. If it has no value, I will give you a valuable bag of fine dirt for everything in your bank account. You will then have something of value and I will have done you a favor.

BTW, if it has no value, then how do you pay for things? Oh, your’s does have value but anything new does not? If it has no value, why would someone sell you gold and accept payment in Fed notes? It seems the bag of dirt would be preferable.

So, the question of the day …

If Fed Notes are so worthless, why will gold salespeople accept payment for their gold in Fed Notes? Why will people sell bitcoins for Fed Notes?

Or, to put it another way, income comes from labor AND income comes from invested capital. This is econ 101.

The Fed and their support of the Phillips curve ignore the creation of income from saved and invested capital and substitute printed money, rate management, asset inflation, and trickle down theory as being a valid substitute for income derived from actual capital that was derived from savings, which was derived from labor or other productive investment. (long sentence)

Again, this is econ 101.

Hence my believe in the Fed populated by pinheads or by individuals who support a hidden agenda.

The Fed probably thinks it funny that many are distracted by gold conspiracy theories or fiat conspiracy theories. Distraction supports the hidden agenda and/or absolves the pinheads who probably feel smug in their models.

I’d suspect stan’s concern is that banks create new money when they lend, giving us glorious these glorious asset prices.

Kent, re-read the reply above. Bank deposit creation from lending is an anomaly of accounting. The monetary creation aspect via the reserve requirement is a math phenomena. Normal risk management supports the daisy-chain aspect. Money printing by central banks and, especially, forced low rates support junk investment, aka asset price pumping and paper flipping.

The fear of bank lending and fiat is junk economics.

“Margin debt and the stock market move together.” Yes, they do. But margin debt peaked a number of months before both the 2000 and 2007 market peaks. Not saying that will happen this time, but may be worth keeping an eye on.

“But margin debt peaked a number of months before both the 2000 and 2007 market peaks.”

The problem with that, is that it is a impossible to see the peak as a “true peak” untill it is in regression.

I have only ever picked 1 peak, Live. EUR/USD.

Bottoms are much easier to pick, Live.

josh, margin debt also increased prior to the 1929 crash. Tax cuts happened in 1924 and 1926 and also contributed to the 1929 crash and the following depression. It is worth keeping an eye on.

Wow, excellent reporting on this topic. Well done. The facts certainly point to another possible margin drawdown feedback loop pushing stocks down. But, I’m still in the camp that firmly believes the central banks (not just the Fed) will never allow it to happen. They could have prevented the bubble getting out of control back in 2013 but instead began another round of QE – they wanted this bubble to happen and they see inflated asset prices as permanent and necessary. “Whatever it takes” means: whatever it takes – even if currencies will be sacrificed.

BTW did anyone else notice during Powell’s testimony he said the Fed has no intention of (ever) of reducing the balance sheet below $3 trillion – that level is the new base from which the balance will only grow in the future. We must all accept the fact that central banks are monetizing debt and there will be hell to pay in the form of inflation – you can’t print wealth.

As is established practice, the FED will shut the gate only AFTER the sheep are loaded into the fleecing corral.

Rinse and repeat.

Federal Reserve, like so many other illegal Arms of Gov, under the Constitution should not exist. Trillions have been stolen from countless people over many generations. Parasites of Humanity !

down_by_the_river asks:

“what becomes of the slaves after they are replaced by machines and no longer needed”

That is why we need to delete the federal income tax on wages, salaries, and tips. Because a tax on jobs kills jobs.

Hey, let’s tax the machines? Then corporations and businesses will stop getting rid of workers and replacing them with machines or foreign labor. But watch the corporations scream because they know a tax on their product hurts their business. Wake up American workers! Quit letting the Feds tax your jobs.

Delete line 7 from the IRS 1040 form!

Because a tax on jobs kills jobs.

I agree completely. My argument is that the very purpose of government is first to protect private property. Therefore, taxes should originate on private property. Wages are not private property. Employees are not private property. Sales of goods and services are not private property.

Secondly, the government has a fundamental responsibility to protect the public property. Those things that are not or can not be private (air, waterways, natural lands). So taxes should also be put on pollution and waste.

Own nothing and don’t pollute? You pay no taxes. Own a coal-fired power plant and have a billion in assets. You are going to pay taxes. The rest of us can make choices on where we want to land.

It’s first job is to protect private property? Not lives, not freedom, not the continued viability of the land that nation is built on–private property? Even Locke put life and liberty before property.

The first government was the Akkadian invaders of Sumer. Their purpose was to divide the available land among themselves and enslave the local population to farming that land for their benefit. We might like the idea of government protecting lives and freedom, but it will be the lives and freedom of those who own the private property. The real versus the ideal as always.

Right on, Kent. Tax the P’s – Pollution, pesticides, petroleum, plastic, and (improved) private property. A good tax policy should tax what you want less of, because that’s what you are going to get. As long as we tax jobs, we will get less jobs.

Except then the taxed things can be reduced to zero ending the governments revenue stream.

“Except then the taxed things can be reduced to zero ending the governments revenue stream.”

They will always invent a new stream.

Margin debt or a major stock market drop is not a problem.

There is only a problem

if the banks refuse to cover your loan when your margin is called.

From what I hear, if you have a job,you are good to go.

These are good points, but this market’s still got further to go. Treasury yield curve is normally sloped and high yield spreads remain very tight. There is no fear of recession in the bond market.

When the yield curve inverts and high yield spreads start to widen, that’s last call for me – I’ll be getting out of Dodge. Until then, sit tight and keep buying the dips. We may have another year or two to the top.

1) The at 23,959 is the peak, or a spitting distance from peak, just above

24,000 pt.

The whole move from the 2009(L) is over.

2) When the inflation rate is 1.7% and most Fed short duration rates

are below the inflation rate, the government pays a NEGATIVE

dividend to investors.

Since most US government debt is in the short duration, the real value

of the debt is falling.

Let me try again : the govt debt is losing value because their debt is exposed to inflation. THEIR debt is not your credit card debt at 18% to 27%.

If you take a mortgage, paying 4%, and after 3 years the inflation rate

will be 10%, your house was purchased for free.

If a central bank, borrow money from investors, paying

(-)0.7% to 0.00%, while the inflation rate is +1.0%, the govt is making money : between 1.0% to 1.7% on borrowing. It took them 40 years of hard work and a lot of investment to reach this point!

The govt level of debt is rising in order to reduce the REAL value of the debt, when most of the rates are in negative territory.

This debt is clipped by a real inflation.

If they use investors money to buy AAPL, they have an unrealized capital gain, plus $0.63 in dividend each Qt. – they don’t pay taxes.

That’s why we all knows well, that the central banks economist are

idiots, and they never explain, or defend themselves.

With your mortgage, inflation may cancel the interest paid, but you do not cancel the principle for free. One also pays taxes, insurance, and maintenance. Cannot simply subtract purchasing price from selling price to determine how much one made.

Let me moderate my comment :

Central bankers, all over the world, you are the real expert.

I am just one of those guys, who surf the internet, collecting bruising

data from every blogs, and I start believing that I know it all.

After so many headlines I browsed, I came to the conclusion, that I am the expert, and the central bankers don’t know what they are doing.

They typically raise rates, just before recession, how can they miss every shot.

Central bankers, I apologize to you, for insulting you. For so long, I was so sure that I am the expert ===>

not you.

“It’s about asset prices, debt levels, and risks. They don’t want a repeat of 2008/2009. It seems they want the bubble they created to deflate gradually so it doesn’t take down the economy.”

What they want and what they’ll get are entirely different animals. 2000: peak of the “.com” bubble, 2007: peak of Housing Bubble (1.0), late 2017 or early 2018 (my guesstimate): peak of the “everything” bubble. We can go back in time through history – at least to the Dutch tulip bubble of 1637 – to find similar circumstances, but, I’m sure “this time is different”. There will be no financial crisis, severe recession, or other ill effects. The Fed says so (just like last time around). The current bubble is another incarnation of “Frankenstein’s monster” of their own creation; a product of cheap and easy credit and oceans of liquidity. Bubbles always end the same. They couldn’t prevent the catastrophic meltdowns in the last two instances, they’re not going to be able to prevent it this time either. The “time to worry” has long since passed. It was when they started blowing the bubble.

“Humpty Dumpty sat on a wall,

Humpty Dumpty had a great fall.

All the King’s horses, And all the King’s men

Couldn’t put Humpty together again!”

The Fed, all other CBs, Keynesianism/Progressivism have destroyed free markets and entire economies of sovereign nations. The road to perdition, since 1913. End the Fed. Until then, free markets are dead.

“The popularity of inflation and credit expansion, the ultimate source of the repeated attempts to render people prosperous by credit expansion, and thus the cause of the cyclical fluctuations of business, manifests itself clearly in the customary terminology. The boom is called good business, prosperity, and upswing. Its unavoidable aftermath, the readjustment of conditions to the real data of the market, is called crisis, slump, bad business, depression. People rebel against the insight that the disturbing element is to be seen in the malinvestment and the overconsumption of the boom period and that such an artificially induced boom is doomed. They are looking for the philosophers’ stone to make it last.” — Ludwig von Mises (1940)

“Permit me to issue and control the money of a nation, and I care not who makes its laws.” – Mayer Rothschild

“A nation can survive its fools, and even the ambitious. But it cannot survive treason from within. An enemy at the gates is less formidable, for he is known and carries his banner openly.” – Marcus Tullius Cicero, 106-43 BC

Correct me if I’m wrong but wasn’t there market crashes and depressions before central banks and Keynesian economics?

” And when stocks sink, leverage becomes the big accelerator on the way down”

Won’t happen till at least the next election. Buy the dip has served me well, and I pray to it like a god. It always delivers.

I smile when I read posts like this one because it assumes there is some intangible father figure overseeing the markets. The markets are a product of the human mind and do not rely on ‘reality’ for their levels.

If markets do tank it’s because someone’s leaked our plans to nuke N. Korea. I doubt that as gold is tanking.

“The markets are a product of the human mind and do not rely on ‘reality’ for their levels.”

The Markets are a product of the “herd” the herd does not react to mind, but herd action, when it takes flight all flee with no thought simply instinct to go fastest.

Same story in the Chinese stock market collapse in 2015/16. the market boom was facilitated by the margin debt and “shadow margin”(off the count margin debt) which as the result of huge QE. Money from banks flooded into stock market through different channels, and the margin debt together with shadow margin recorded over 6.5 trillion RMB at its craziest moment (the total market cap for Chinese A share was 65 trillion). The market then collapsed as the government tightened the regulation on the margin debt and shut down the channels of shadow margin which lead to a sell-off.