They’re investment choices, like bond funds, bonds, etc., not that illusory “cash on the sidelines.”

By Wolf Richter for WOLF STREET.

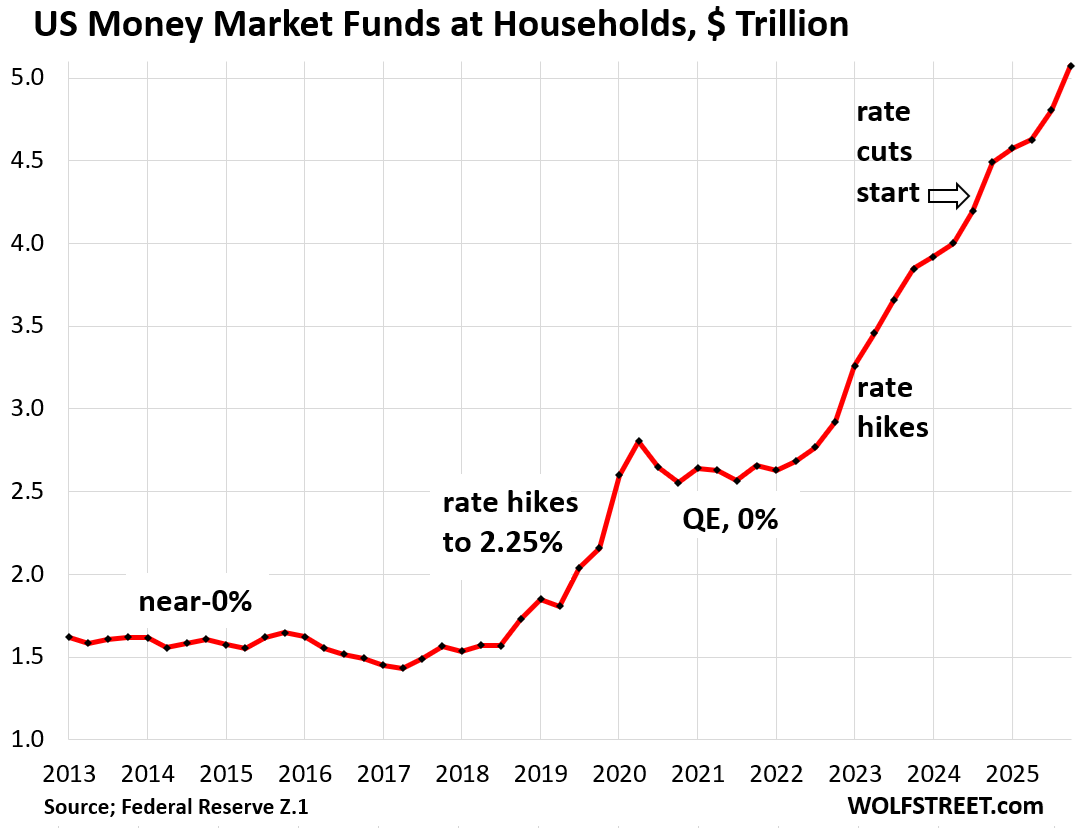

Households poured an additional $269 billion into money market funds (MMFs) in Q4, and their MMF holdings spiked to a record $5.08 trillion. In all of 2025, households poured $583 billion into MMFs, according to the Fed’s quarterly Z1 Financial Accounts. These MMF balances include retail MMFs that households bought from their broker or bank, and institutional MMFs that households bought indirectly through their employers, trustees, and fiduciaries – such as in their 401(k) plans.

This spike in MMF balances occurred even as the Fed was cutting its overnight policy rates, and MMF yields declined in parallel with the rate cuts. But that trend of lower yields is now beginning to reverse as short-term Treasury yields have been inching higher for two months.

At current MMF yields of around 3.5% to 3.6% and at current MMF balances, households would earn $180 billion in interest in a 12-month period. Since Q1 2022, when the Fed started hiking its policy rates, balances have surged by $2.45 trillion.

Short-term yields have begun to rise again. Yields of Treasury bills, one of the alternatives to MMFs, inched up in February and so far in March, as investors took the chance of rate cuts in their time frame off the table. Money market funds follow the direction of T-bill yields with a lag. Short-term Treasury yields are now all above 3.71%.

The 1-year Treasury yield is beginning to price in the chance of a rate hike in its time frame; its yield has soared by 40 basis points from the low point on February 9 (3.42%) to 3.82% today.

MMF yields are determined by the instruments they invest in. Prime MMFs invest in repurchase agreements (repos); Treasuries and agency securities with a remaining maturity of less than 1 year, but largely less than 3 months; short-term asset-backed commercial paper; certificates of deposits with big banks (lending to banks), overnight reverse repos at the Fed (ON RRPs are now down to near $0 as the Fed pays only 3.5% on them, less than T-bills and less than repo market rates of around 3.62%), among others.

Treasury MMFs stick to short-term Treasuries and ON RRPs at the Fed.

Very short-term yields, such as repo rates, roughly track the Fed’s policy rates, which are designed to form a floor and ceiling for short-term market yields, especially the gigantic repo market, to which MMFs are big lenders. Since the December rate cut, the Fed has kept its five policy rates unchanged between 3.50% to 3.75%, including at the FOMC meeting this week.

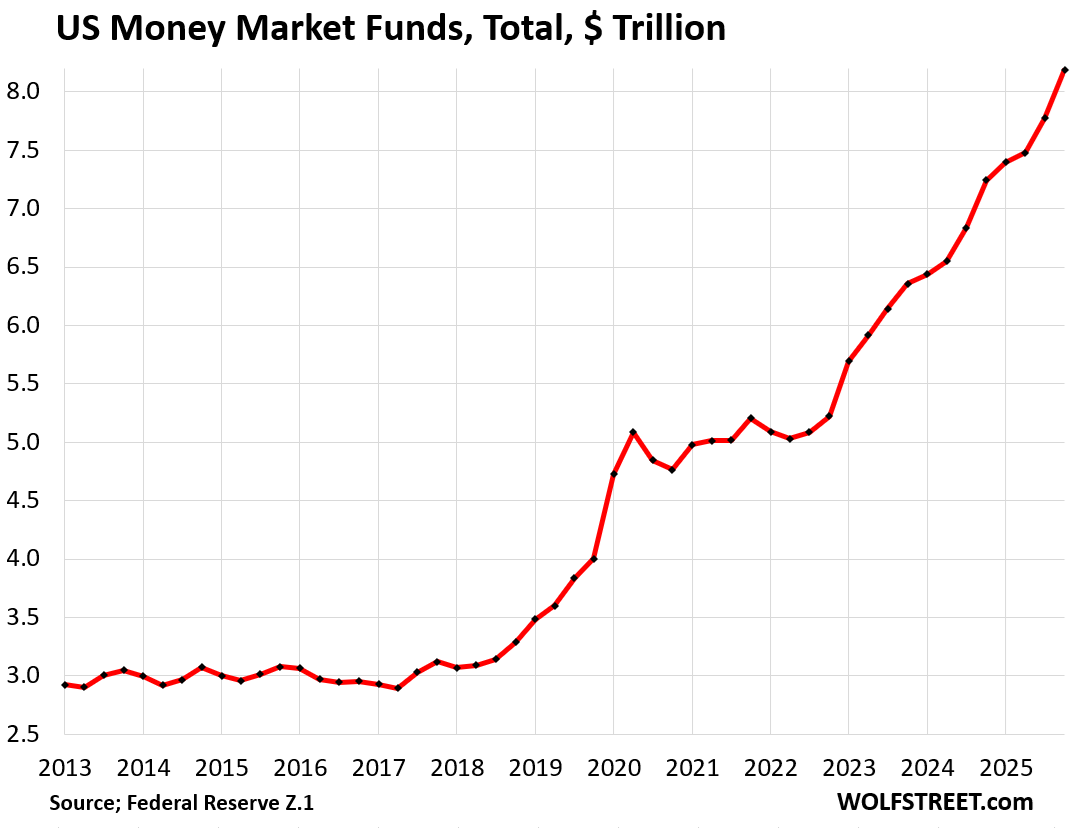

Households and institutions combined poured $416 billion into MMFs in Q4 – including the $269 billion from households.

Total MMF balances ballooned to $8.19 trillion – including the $5.08 trillion held by Households.

Since Q1 2022, balances have ballooned by $3.10 trillion, including the $2.45 trillion from households.

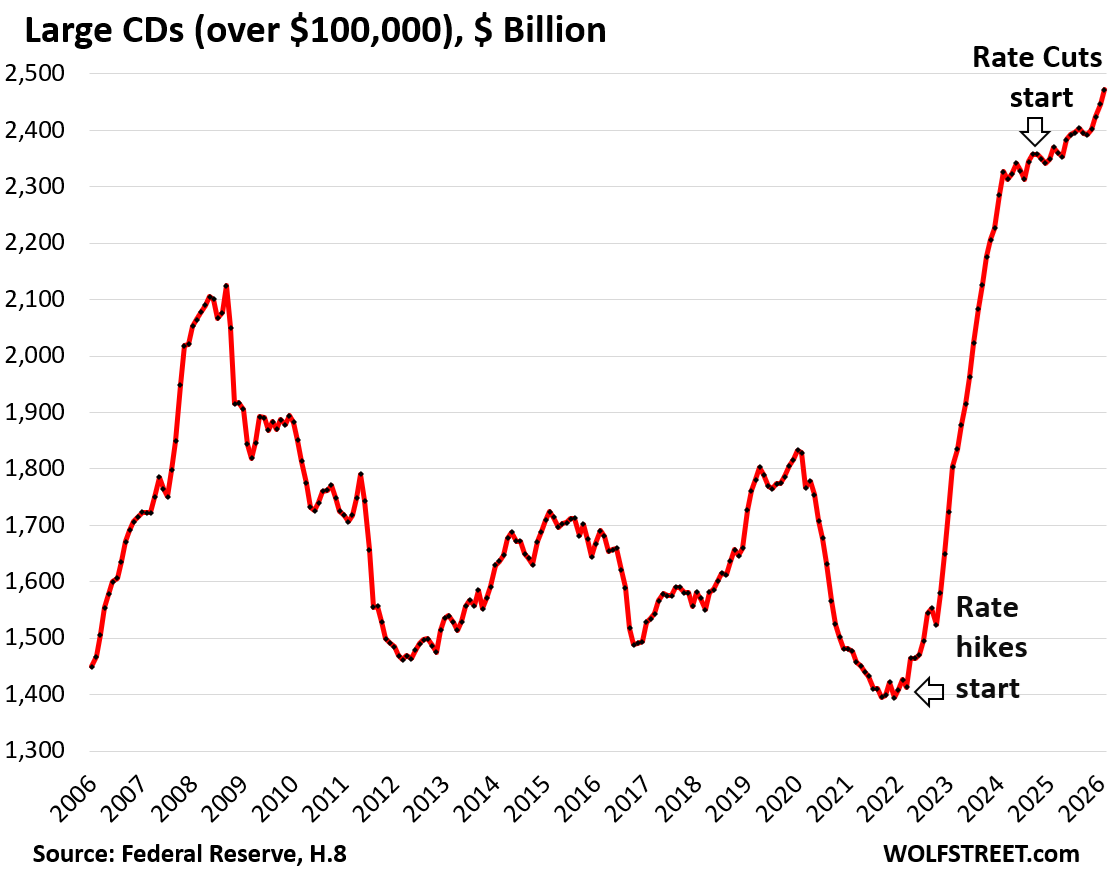

At banks, large Time-Deposits (CDs of $100,000 or more) rose to a record $2.47 trillion in February, up by $26 billion from the prior month and up by $70 billion year-over-year, as per the Federal Reserve’s monthly report on bank balance sheets (H.8). The FDIC insures CDs up to $250,000.

Since March 2022, when the rate hikes began, and continuing even as the rate cuts began, large time-deposits have surged by $1.06 trillion. The rate cuts since September 2024 have only slowed the increase, not stopped or reversed it.

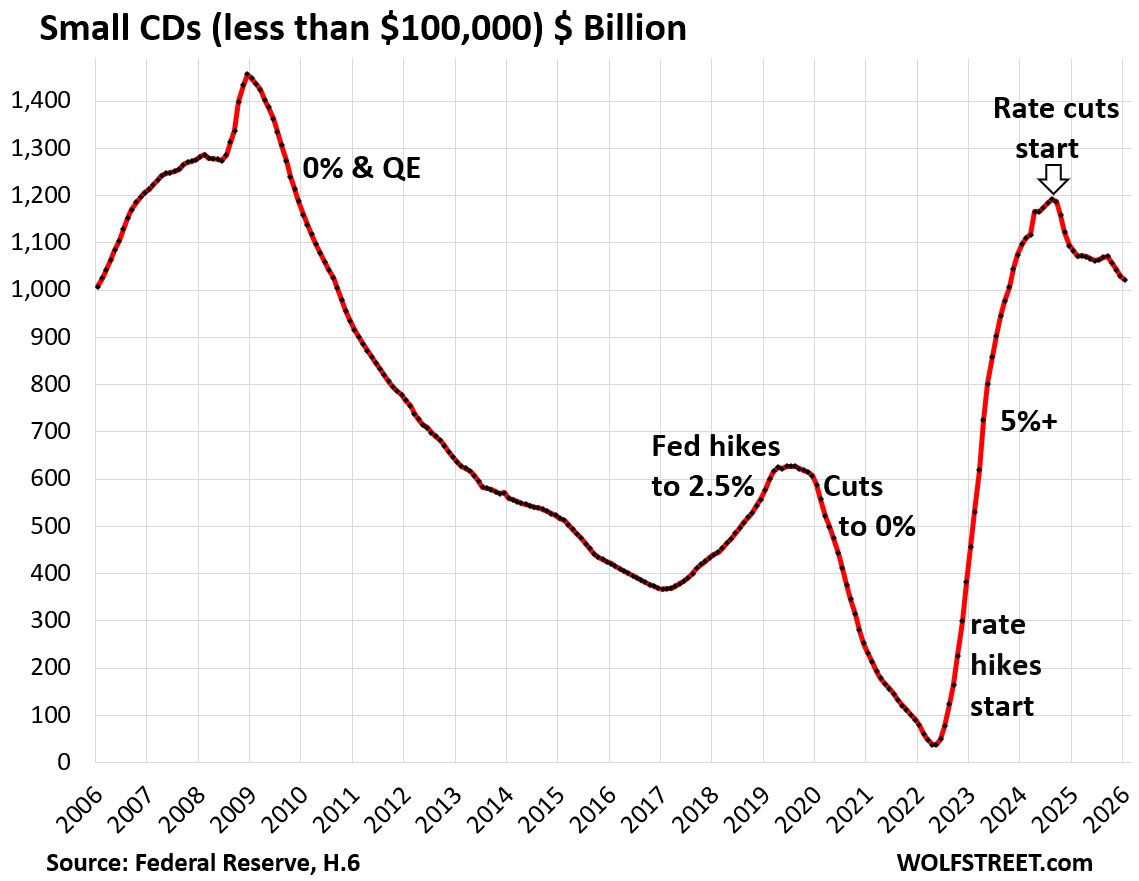

But small Time-Deposits (CDs of less than $100,000) fell to $1.02 trillion in January, per the Federal Reserve’s data on money stock (H.6). Since September 2024, when the Fed started cutting rates, balances have dropped by $170 billion.

Smalls CDs react fairly quickly and strongly to interest rates offered by banks. They’re not “sticky” at all. Investors shift into them and out of them depending on yields that banks offer. By early 2022, after two years of near-0%, balances of small CDs had dropped to near zero. But when the Fed started hiking rates, balances exploded.

Not “cash on the sidelines.” Money market funds and CDs are low-risk investment choices to earn a yield, similar to bond funds, T-bills, corporate bonds, government bonds, etc. They’re not that illusory “cash on the sidelines” that’s suddenly going to pour into the stock market when the floodgates open upon a divine signal to magically drive stock prices higher. Crypto is not “cash on the sidelines” either. Nor are gold and silver. They’re investment choices that are not stocks.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Howdy Folks. Correct Lone Wolf, too much cash in the mattress and closets. Wife and I moved some into a Fund based on the stock market.

Buy the dip…..

Same,

Seems to be a pretty good discount. Though one could kick themselves if you look at around spring of last year.

Hoping this is a 🐻 and not just a 🐻 scare. But who knows.

I hope my extra gas money payments are keeping poor OPEC children clothes and fed. 😂

The asset markets are severely overpriced by at least 40 pct.

Dont buy now. wait a while

Agreed, but it always helps to highlight the metrics you use. A good one to start with is the SP 500 PE ratio compared to historical norms.

The data in the charts is suggesting much lower. NASDAQ just closed before support of 22k. This coming week is critical. 22k may turn into resistance. If it does, I’m watching the 20, 16, and 14k levels. 20 and 16 are major Fibonacci levels and 14k would be a full market reset. If you don’t understand any of this, my suggestion is just wait as it will go back up there again, unless Trump really screws us over.

MW: Dow, S&P and Nasdaq book 4th straight week of losses as rate-hike prospects rattle markets

DJIA -0.96% SPX -1.51% COMP -2.01%

1:04 PM 3/20/2026

Dow 45,577.47 -443.96 -0.96%

S&P 500 6,506.48 -100.01 -1.51%

Nasdaq 21,647.61 -443.08 -2.01%

VIX 27.39 +3.33 13.84%

Gold 4,506.80 -98.90 -2.15%

Oil 98.81 +2.67 2.78%

More risk to the downside than up in many other asset classes.

Makes sense even if rates have come down some.

Another rough day on W.S. Have been expecting a taco moment or a press release or something to stop the bleeding and trigger a rally.

Me too. I’m waiting for “Peace talks are going well” in the spirit of “Trade talks with China are going well” that that idiot Kudlow or Mnuchin trotted out every time they wanted a market rally.

I think your conclusion is wrong. The market stallwd in the Q4. It looks like people got conservative and moved to lower risk MMF. Once they become optimistic that money will move back into the market.

But no, every single stock they sold someone else had to buy for the exact same amount, and all the dollars these “young people” pulled out the stock market, other people had to put into the stock market. Money cannot leave the stock market and go somewhere else.

An individual can pull their money out of stocks, but someone else must be putting the exact same amount into stocks by buying what the seller sells. And overall, the money stays in stocks.

The fallacy of the mantra that there is money on the sideline.

As you explain is that money seeks advantage relentlessly

There is a bid/ask price in the stock market. The difference between these two prices, sometimes quite a lot, plus commissions is what someone makes and takes out of the stock market every time you do a trade. It is like a gold rush, the guy selling shovels always makes money while the prospectors lose it chasing the net big strike. Most people simply can not distinguish between investing and gambling.

wait a minute.

1. There is a difference between bid and ask before a trade takes place, so you see that on screen. But by definition, when a trade takes place it’s when bid = ask, a seller pays exactly what the buyer wants, or there would be no trade.

2. Most retail brokers no longer charge commissions. Commission-free trading has been the rule for years.

3. “Most people simply cannot distinguish between investing and gambling.” I agree.

“Most people simply can not distinguish between investing and gambling”

That’s easy, since they are both industries in the service category..

(1) WHO owns/controls the house one is gambling/trading in and (2) what media choices influences one’s preference for either word usage?

Actually I find it all quite comical…..yet with a tragic and obvious end…..eg negative nat gas prices in Texas….so they burn it.

Oh, and what “chosen” media diet reinforces choices made long ago and keeps one’s preferred self image and belief structure intact?

Curious to know if there are surveys or data to show where the money comes from or goes to when these investment types grow and shrink.

Yeah, it’s called the stock market

How will all that cool debt look if rates continue to blow out?

TYX nearing 5 again……

You know what they say about excess debt it becomes the burden of the tax payer, the every day person that is a remarkable example of the beauty of the precision of evolution.

The big banks were paying almost zero percent on cd’s money market’s and savings account forever. Even jumbo accounts were less than a percent. Did not even make sense to deposit.

I was the financial secretary for a charitable organization for a few years. We had $100,000 for our savings. For 2 years we only made $.90 per month on it. Only other way was higher risk or pain in the ass moving it around for only a few dollars more, So we just took the $.90.

Fortunately, things have become more competitive now.

The big banks still don’t pay very much compared to the smaller banks and credit unions for whatever reason…

Not a fan of the big banks, kinda mostly fraudulent. Chase and Wells Fargo are especially fraudulent. Had multiple problems with them over the years…. Refuse to do business with either anymore.

Big banks are “THE MAN”

Credit Unions are “THE PEOPLE”

As someone else pointed out they sure as hell don’t make they”re nut on savings accounts.

They make their nut by the traditional loan sharking play book. honed to a profitable business since the emergence of man in our present form. by the blessed dispensation as being legitimate by the Federal government

It sounds like you are making the argument that “loan sharking” is a needed service.

Making money by offering a needed service is called capitalism.

No one is forcing people to take those loans or deposit money at those rates.

I have been hesitant about putting anything into the stock market.

Currently only about 7% discount from the ATH (on the S&P). With a 52 week range of 4835-7000!

Almost 45% gains from a “liberation low,” all on fundamentals I’m sure! (/S)

I have recently received some inheritance and have a 3.8% high yield savings account. I’m waiting until it’s more like a 30-40% discount from ATHs, as I foresee the volatility and geopolitical implications as not having a quick resolution.

My poor 401k will probably languish, but alas: I’m trying to get most of THAT out of risk too.

where’s the 3.8% hysa? I use morgan stanley; they are currently @ 3.35%

Treasury Direct products are the best options though

Marcus high-yield savings

3.65% APY as of yesterday

Vio bank 4.03%

Yes, Vio at 4.03%. Also, Newtek at 4.20% and TIMBR at 4.15%.

I’m at Western Alliance. I took pause for a moment, as they had some bad loans to write off, but they generally seem solvent?

I think SoFi and some others are competitive in the range. I had literally just searched the highest yield.

I think I was looking at nerd wallet or a similar site for reviews.

Good to see where money is treated well.

Thanks for sharing the info. Beats clicking on a bunch of links.

Kinda funny….

People cancelled all kinds of businesses and CEO’s because of saying the wrong word or having an incorrect business logo.

JP Morgan is a felonious company multiple times over… and admitted it….precious metal market manipulation, bond market manipulation, knowingly funding ponzi schemes….oops we just happened to lose all the Epstien emails.

Dimon was the CEO during those happenings and still is.

Not cancelled, still there.

People don’t seem to worry about the important stuff…

What is more offensive to me than an incorrect business logo or a sad word is POVERTY… fraud, and being ripped off.

I will step down from my soap box now….

Haha

The government is ok with them, so they continue to exist.

If you don’t like the banks give Elizabeth Warren more power. Make her AG or something.

She’d prob dismantle them

I can’t control what the big banks do.

What I can control is avoiding business with them where I can.

Regional banks and credit unions seem to be more competitive to attract and maintain customers.

Dude…JPM is the “Designated Survivor” financial institution in the US.

Every other bank could fail, a total nuclear apocalypse could occur, and cockroaches inherit the earth…but the USG would have structured things so that JPM would be the last human institution standing – JPM and USG are welded at the hip.

Yeah….

There is that.

I am sixty percent cash and 40 percent dividend paying stocks with many of them being NON U.S. large caps. I am happy with those choices. I am certain that this will change in the next few weeks. I am happy with that too.

Also worth noting that household’s net worth nearly reached 8 times their annual after-tax income at the end of 2025. These are averages, so of course that’s not everyone, but it’s still a lot of money.

Take the top 1% (outliers) out of the average and lets see what that tells the rest of us…

They’ve already been taken out of the “after-tax income” that numbers cites, likely disposable income, which excludes capital gains, which is where the rich make most of their money.

The only ballooning pile I know of is that mound of manure out in the neighbor’s cow pasture.

Sammy,you get along with farmer tis a great spot for getting shrooms!

I am friends with a guy with small farm,get milk and butter from him,he lets me stroll the fields with a bag,doesn’t ask me why/I don’t tell him!

I have most of my retirement in equities but I’m 39.

Have a lot in savings getting 3.2%. have a good chunk in vanguard federal money market which gets around 4% but it is tied to bonds. So it is hard to essentially I vest like another 60k into equities when I can get a safe 4 – 4.5% versus a risky 7% to ath

Those are Gov bonds, short term.

The US would have to stop existing for that to be risky.

I have zero funds in the stock market.

All my money is in:

Short term Treasury Fund

Tax Free ST muni bond fund

CDs less than 1 year

Money Market account

If the Trump Crash continues I will be unaffected.

S&P500 is still up about 1000 points since the inauguration.

It’s been dealing with catastrophe after catastrophe!

Think about if you fed it oats every am and just let it run!

lol

🐴

Just blame the uniparty. And most of all the Federal Reserve Bank, and it’s reckless monetary experimentation since 2000 which has enabled uniparty irresponsibility

Here is the thing though, if excess inflation is the thing that comes out of the Trump crash, then the stock market is the place to be.

No other asset class handles inflation better than stocks.

Can you blame “us” Wolf? As long as the orange guy continues to execute ill advised policies, directing the financial markets down, it seems this trend will (and should) continue.

And from what funding source are the buyers generating funds needed to purchase securities that the sellers then place in “cash & equivalents?” Might they be selling the same?

Core deposits are up. There’s been a flight to liquidity.