In a broader sense, there has been no progress at all on inflation in eight months.

By Wolf Richter for WOLF STREET.

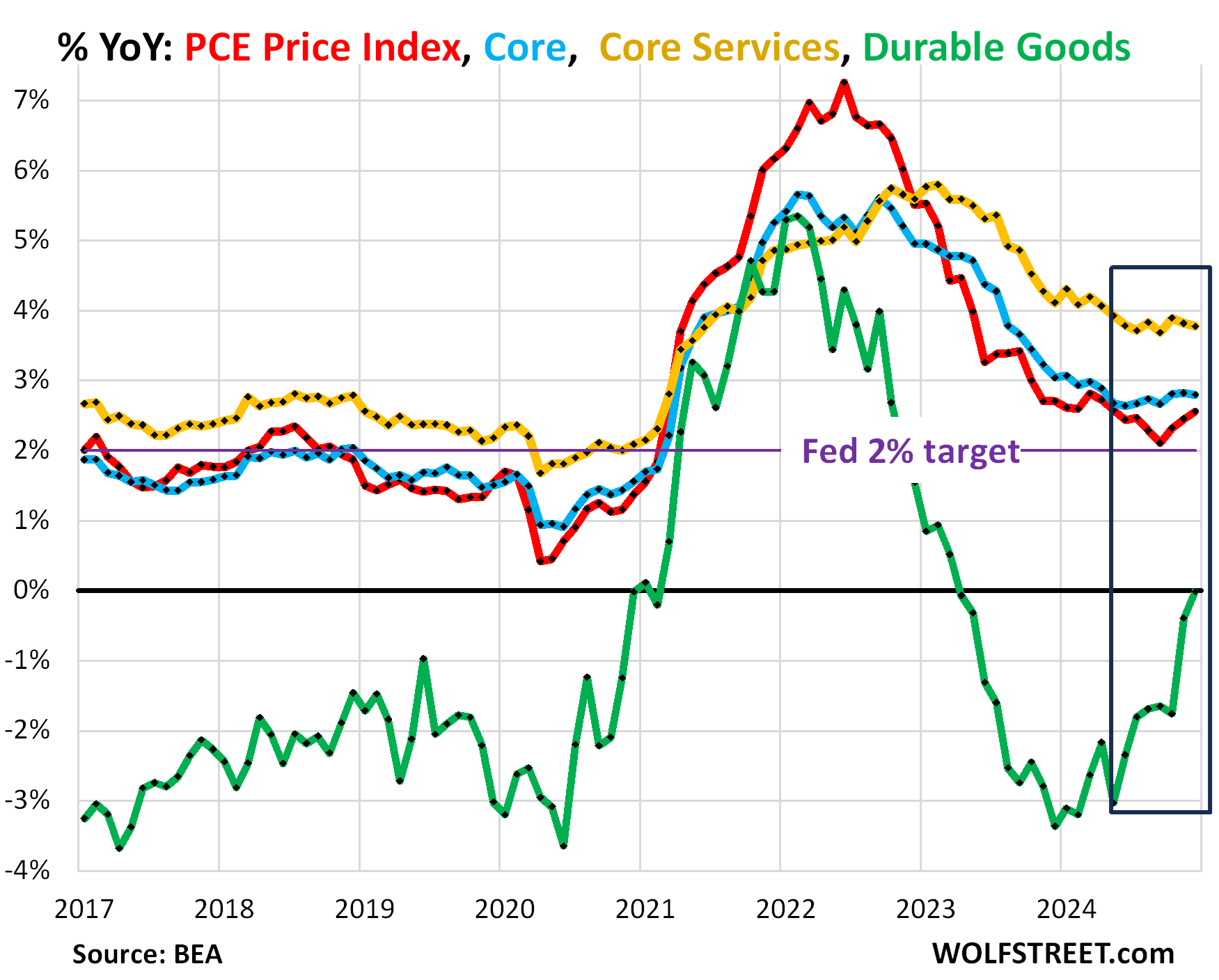

The sharply falling prices since mid-2022 of energy such as gasoline, and durable goods, such as motor vehicles, had contributed a lot to the cooling of inflation measures. But prices cannot fall forever – they can rise forever, but they cannot fall forever, and they stopped falling. And on top of it, services inflation has gotten stuck in mid-2024 at too high levels.

As a result, overall inflation indices, including the PCE price index released by the Bureau of Economic Analysis today, have started accelerating again on a year-over-year basis. The driver of inflation has been and still is in “core” services, which, at 3.8% year-over-year for the core services PCE price index, remains substantially higher than before the pandemic (yellow in the chart below).

In a broader sense, there hasn’t been any progress on inflation since May (black box in the chart below), with the Fed’s favored inflation measures well above its 2% target, confirming the Fed’s pivot this week to a wait-and-see strategy.

The PCE price index accelerated for the third month in a row, to 2.6% year-over-year in December, the worst increase since May 2024 (red in the chart above). The Fed’s target for this measure is 2%.

The “core” PCE price index, which excludes the volatile prices of food and energy products, remained at 2.8% for the third month in a row, and these three months have been the highest since April (red in the chart below). The Fed’s target for this measure is 2%.

The “core services” PCE price index has gotten stuck at around 3.8% with only minor fluctuations for the seventh month in a row (yellow in the chart above).

This year-over-year rate in the core services index is between 35% and 70% higher than before the pandemic (ranged between 2.2% and 2.8%).

As we’ll see in a moment, on a six-month basis, which reacts faster but is more volatile, there has been no progress at all for 12 months.

Core services are about 65% of consumer spending and include housing costs, insurance of all kinds, health care, education, subscriptions, transportation, broadband, personal care services, financial services, food services & accommodation, etc.

The durable goods PCE price index has ended its historic plunge, and on a year-over-year basis, the index is at the 0% line, meaning no change year-over-year (green in the chart above). In late 2023 and early in 2024, the big negative readings of about -3% contributed a lot to cooling the PCE price index as well as the core PCE Price index.

The durable goods category is dominated by new and used vehicles, which have seen huge price spikes in 2021 and 2022. Used vehicle prices then plunged through mid-2024, but in recent months started rising again. New vehicle prices have been sticky at very high levels and have barely come down. Durable goods also include appliances, furniture, computers, cellphones, other consumer electronics, sporting goods, such as bicycles, etc.

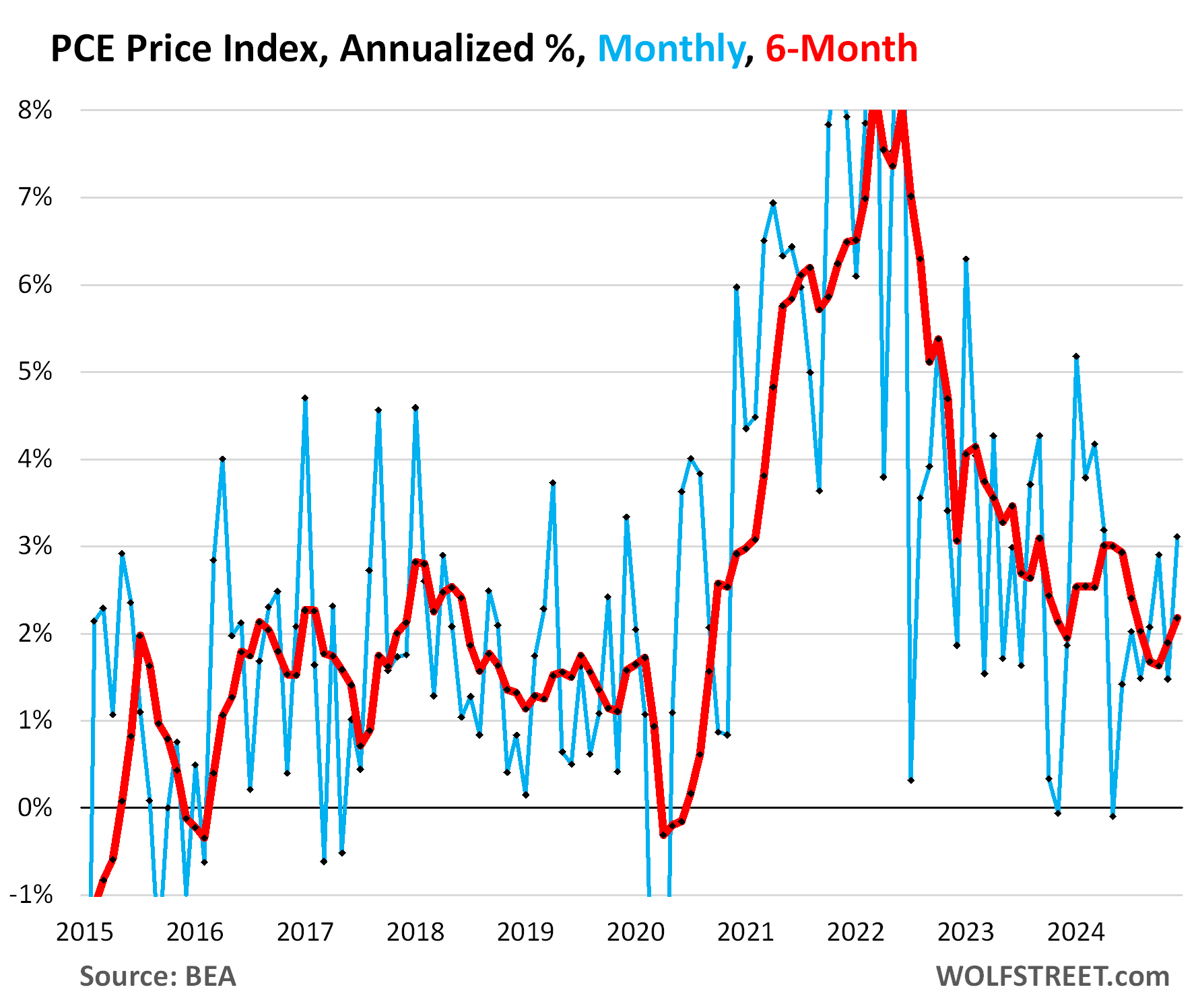

Month-to-month and six-month.

The PCE price index accelerated to +0.26% (+3.1% annualized) in December from November, the worst increase since April 2024 (blue in the chart below).

The six-month PCE price index, which irons out some of the month-to-month squiggles, started reaccelerating in November, and in December rose to +2.2% annualized (red):

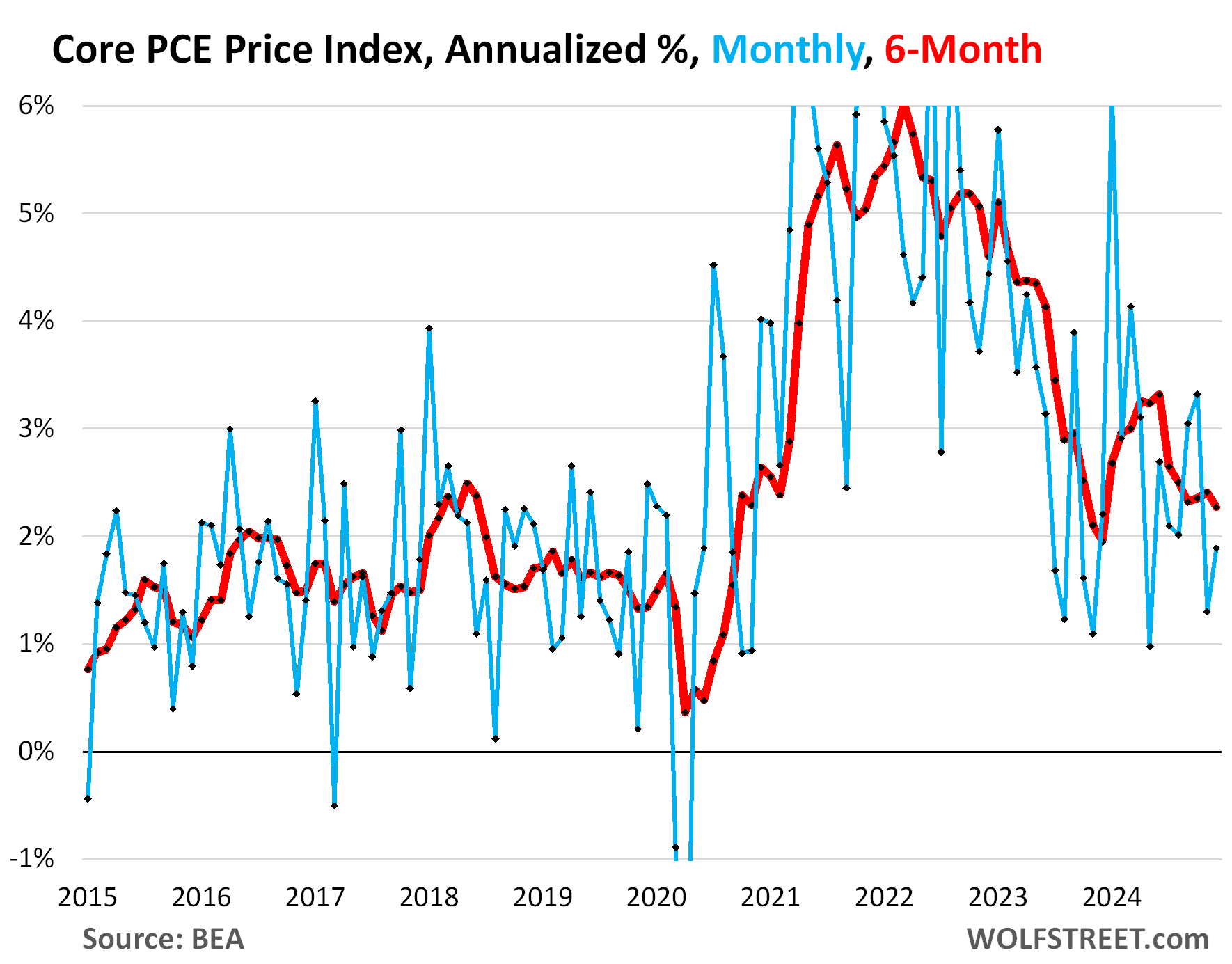

The “core” PCE price index accelerated to +0.16% (+3.1% annualized) in December from November, the worst increase since April 2024 (blue in the chart below).

The six-month core PCE price index has been in the 2.3% annualized range for fourth month in a row (red):

Inflation is festering in “core services.” The core services PCE price index accelerated to +0.29% (3.5% annualized).

The six-month index has been accelerating slowly since the July low point and in December rose to +3.4% annualized, right back where it had been in December 2023, and despite some volatility, there has been no progress at all in a year (red):

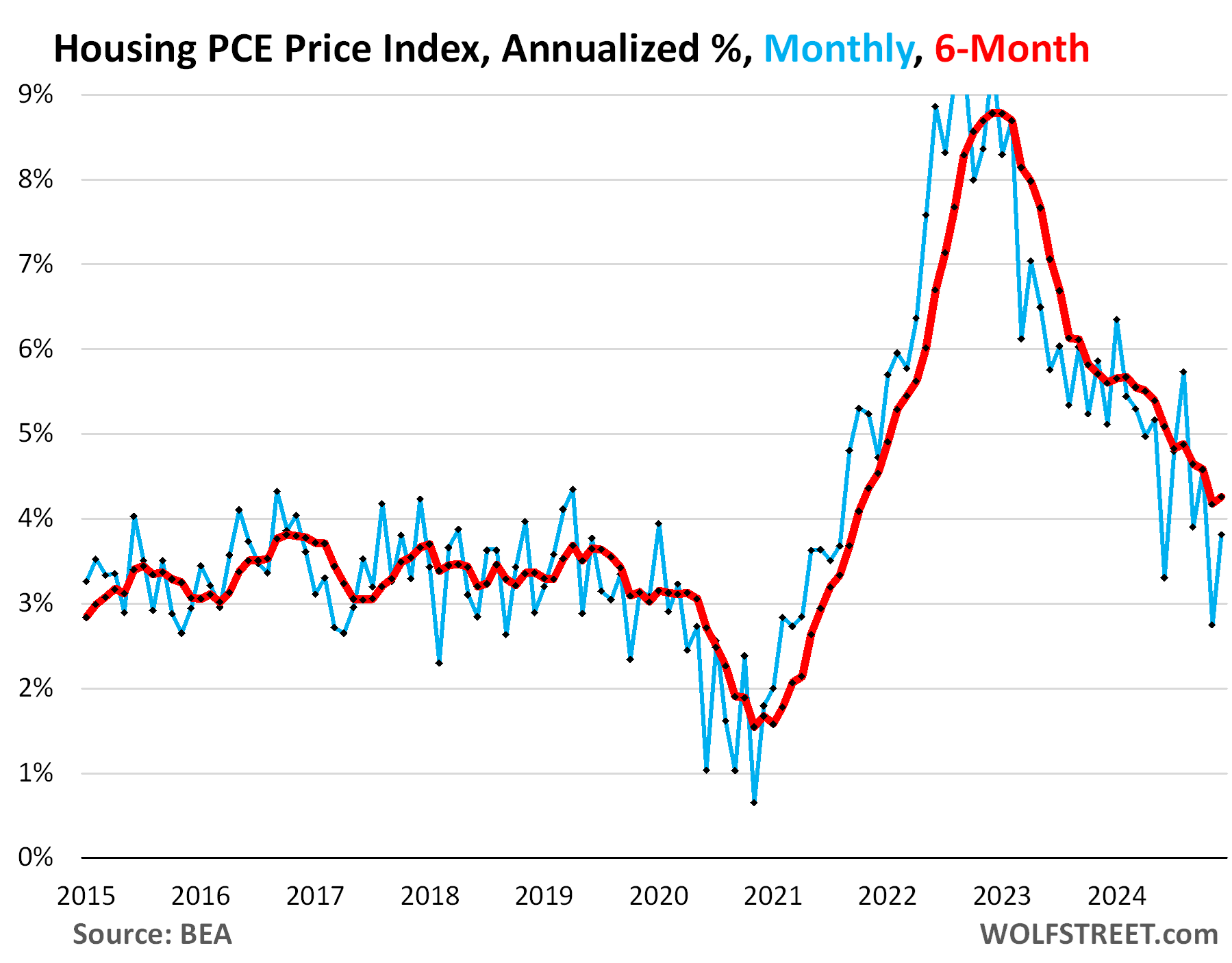

The PCE price index for housing costs (rent), the largest component of the core services index, has been decelerating in a zigzag manner for two years.

But the six-month average, which irons out a lot of the zigzags, is now showing that the deceleration stalled. It accelerated a tad in December to 4.3%:

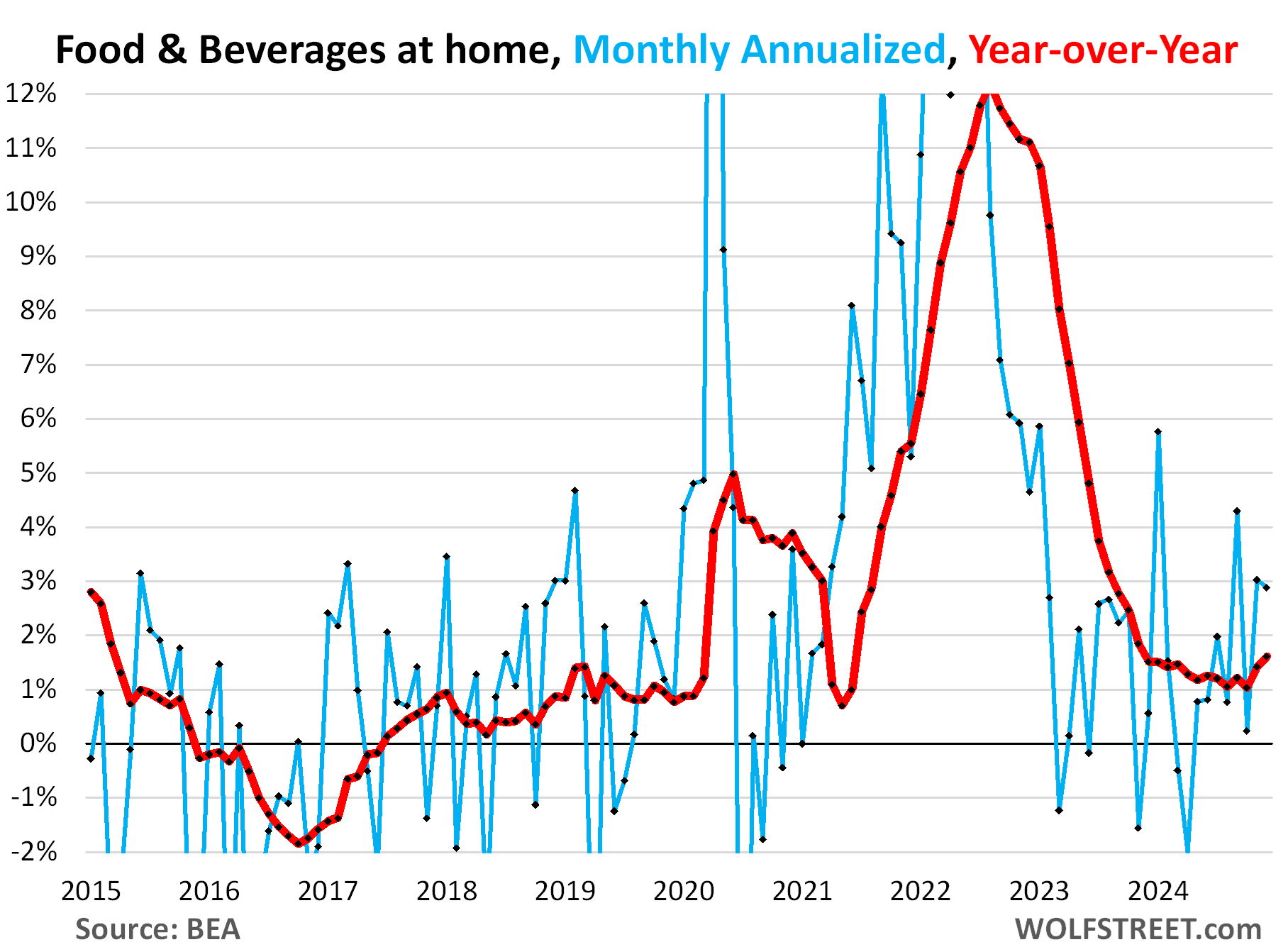

Food inflation has started to accelerate again. Food prices have been very high following the spike through 2022. Since then, the pace of increases of those prices (that’s what inflation measures) has slowed dramatically. But recently, food-price increases have started to accelerate again.

On a month-to-month basis, the PCE price index for food rose by 0.24% (2.9% annualized) in December from November.

The acceleration in recent month has caused the year-over-year index to accelerate again, and in December it rose to +1.6%, the biggest increase in 13 months.

Food is included in the overall PCE price index, and the sharp deceleration of food prices was a contributor to the deceleration of the overall PCE price index, and that may now be over as well.

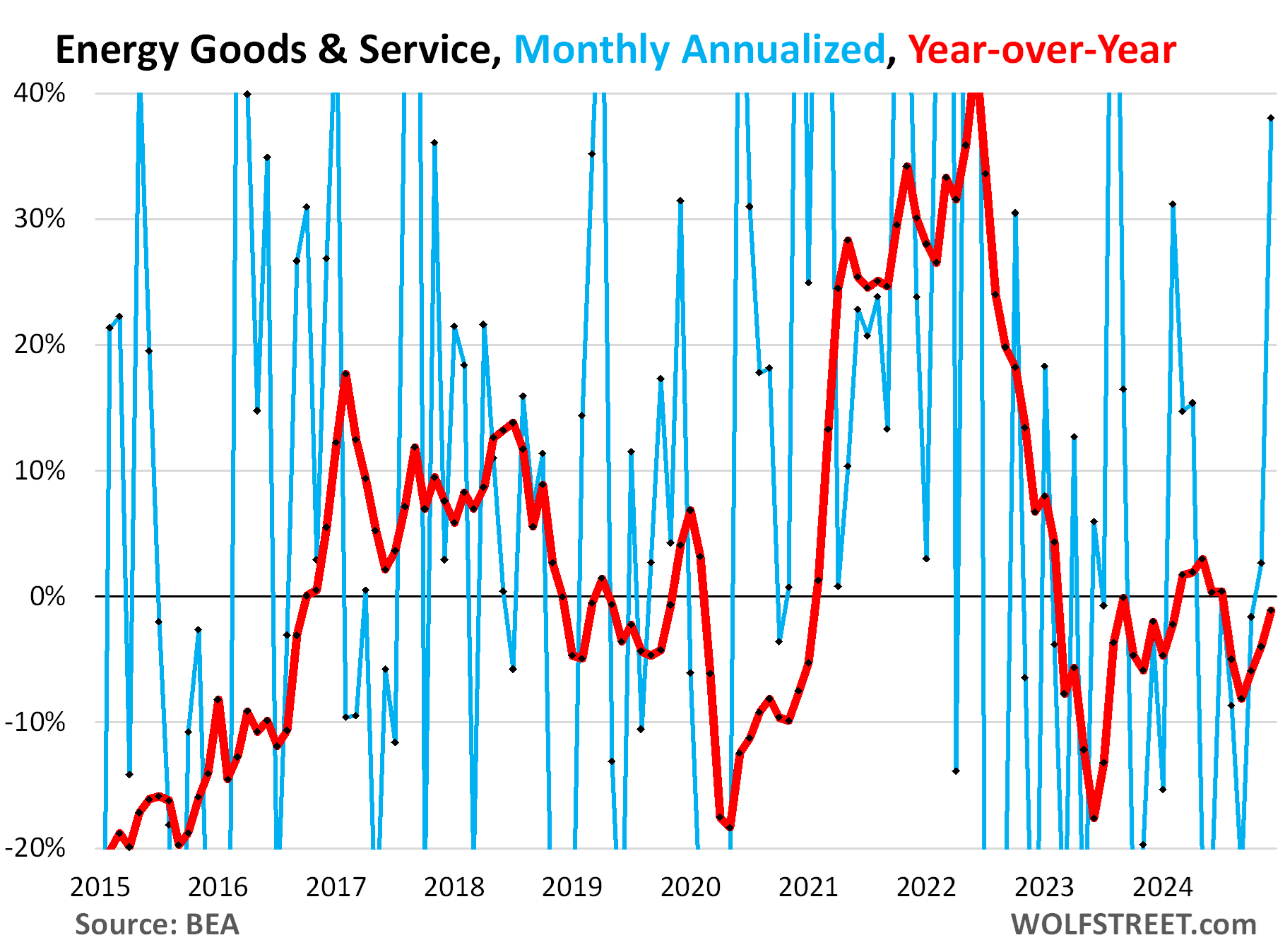

Energy prices spiked in December from November by 38% annualized, the biggest increase since August 2022. So here we go again.

These are prices of energy goods and services that consumers buy directly, such as gasoline, natural gas piped to the home, electricity, propane, heating oil, etc.

Year-over-year, the PCE price index for energy is still negative, but barely at -1.1%. Energy prices weigh heavily in the overall PCE price index. They cannot and won’t drop forever, though they’re very volatile and can plunge for a long time, after a big spike. They were a big contributor to the deceleration of the overall PCE price index in 2023 and 2024, but that help may be fading out:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am sure DEI is the cause of stuck inflation…cure would be lower interest rates, yeah that will fix it.. /S

Definitely getting my popcorn out for this one..

I think we need price controls and college loan forgiveness.

Yeah all that college loan forgiveness that was going on everywhere in the world all at the same time. Yeah that’s why inflation was high worldwide. Don’t forget your other talking points about immigrants!

college loan forgiveness

ONLY IF COLLEGES pick up tab as they should for all defaulted loans

With housing, we already have supply side controls in the form of zoning and permitting. Price controls on the demand side would simply make the market fairer (in the form of citizen-only and occupant-only purchasing and rent controls). If you want a “free” market, you’d need to remove the supply-side controls and let me build wherever, whatever and whenever I want.

I am in agreement with the citizen only and occupant only requirements for single family, but also know that occupant only would seriously restrict the ability of people who want to rent a house to do so.

Citizen only seems like a no-brainer, but I can see dozens of ways around that.

Also, nobody wants a free market. They might say they do, but when someone wants to build an apartment complex in their SF neighborhood, even the most devoted free market advocate starts howling like a banshee.

Yes, because more and stricter rent control always results in so much more and less expensive housing.

If government were just more forceful in controlling every aspect of private property, then there would be so much more really cheap housing available for everyone.

History has proven that to be true. Well, maybe not in this country, but in Russia, North Korea, Cuba, Venezuela, China…..it has been very successful.

Nothing says free market like “price controls”

‘History has proven that to be true. Well, maybe not in this country, but in Russia, North Korea, Cuba, Venezuela, China…..it has been very successful.’

Should there be a requirement that a sarcastic comment adds a sarc tag? Venezuela?? The failed state where millions risk lives to trek thru the jungles of the Darian Gap to escape?

Not the case if developers own the political process.

I see it every day in FL.

The college loan piece was mostly about young people not being able to afford houses and car payments because they were debt burdened. You can argue taking out loans for education all you want, but the NAR and AAPC hold more sway at the policy level. They want to sell houses and cars to young folks and that debt is in the way.

College loan forgiveness was about buying votes.

Wrong, Doug. Biden wiped more loans as he was going out the door. Too late to buy votes this year, and way too far from the next election for the gratefulness (or really, entitledness) of recipients to stick.

Wrong Gatto….Biden initiated the process well before being forced to exit stage left.

And the debt wasn’t forgiven. It was passed on to taxpayers.

When I went to the state college in the late 60’s mostly to avoid the draft, it cost 200 dollars per 16 credit semester.

There was no way that even the imbeciles would be able to go bankrupt from student debt.

A different country.

1990 was 1100 per semester. I remember clearly because it, books, and car insurance wiped me out every 6 months.

Damn, that’s FUNNY!

Nope. The cure is going to be tax cuts for billionaires and big corporations, combined with higher tariffs at the border. Combined with chasing all the foreign born farm workers out of the country.

That will fix it for sure. (sarcasm)

What?? You mean I will have to start cutting my grass myself again? /s

The wealth will trickle down any time now.

Wealth is trickling down – to shareholders. The people spending are the ones with investments that are going extremely well.

> Wealth is trickling down – to shareholders.

Finance 101: diversify from a job to a broader stake in the economy, e.g., by holding real property and stocks. It was a slow climb over 40 years for me to do it, with self-discipline every inch of the way. I was in my mid-later 30’s before I had saved enough for a house down payment, by doing things like not eating at restaurants. Also, quitting every costly bad habit permanently. My foundation is saying no — to myself.

Reality: look at what DOGE is cutting! The graft and corruption in the system is immense. And that’s not even broaching line items like billions in DoD that can’t be accounted for.

Another example, I know someone who had an “insider” look into early contracting for the Ukraine war. No auditing at all. The profit margins were a nice 10%+ on billion dollar contracts. Lotta other things associated with this money laundering including who and where as well as what happened once “things” arrived in Poland.

Look at the data published today for how USAID moved moneys – talk about a huge tail all directed to Ukraine!

Haha! But you see if inflation starts to go up again we can fix it merely by…*spins the wheel they apparently put in the Oval Office*… turning off the government!

What’s that? The ink isn’t even dry and we’re already being sued by 22 states? Oh fine spin it again…aannd “Blame Obama!” One of my favorites!

The Russians have the right idea. Flat 13% income tax rate after a reasonable personal deduction.

The Russians are also ok with their Billionaire oligarchs as long as they stay out of politics.

Of course the State has taken effective control of a few important segments of the economy and funnel a share of profits from those outfits into the State Treasury…Oil and Gas in particular.

Much of the MIC is also state controlled. In the US we’ve always assumed that free enterprise would ensure better quality weapons and superior quantity. Increasingly neither assumption appears to be true. Maybe we’ve been wrong or maybe free enterprise just does not exist in the MIC and what we have is something else ?

I’ve read, but dont know if it’s true that your average Russian can open a deposit account at his bank and get paid 18%. A lot better than the 25 basis points I get on my WF “Savings” account.

I keep visiting the FinCen website to get the latest on if I’m going to have to register my LLC’s with the Federal money laundering police. They want all my identifying info including a picture of the drivers license from ever beneficial owner. I suppose they have the same requirements in Russia, but I don’t know. But I wonder how the difficulty in setting up a business in NYC vs Moscow would be. My bet would be it’s a lot easier in Moscow.

Perhaps we will be surprised by how much economic activity a really big attack on the regulatory state might bring. On the other hand , I’m not sure asset prices like housing can really deflate without a dose of unemployment and fear.

Around here, nothing is selling, but everyone refuses to lower prices. That won’t change without hardship and fear. I can’t really bring myself to pray for hardship and fear to come my neighborhood.

Inflation in Russia is about 10% and accelerating. And the ruble has been collapsing against the hated USD. I don’t think the Russian economy – which is smaller than the economy in California, and maybe smaller than the economy of Texas – should be any kind of model for the US.

The Russian State Bank has interest rates at 21% and mortgages at 30%…

Also a bit bad for your personal health to have any political opinion, be a male of military age, or an oligarch in Russia. But if don’t mind a harsh life, dying a poisonous death, on the battle field, or fall out of a window of a tall building or high inflation then maybe the Russian model is for you!

‘The Russians are also ok with their Billionaire oligarchs as long as they stay out of politics.’

This deserves to be framed.

Lots of people love Russia until they spend 6 months there. The honeymoon ends real quick.

Nick,

More like Russians have no politics cuz they have zero and I mean zero ability to affect their “government”.

One guy makes all the moves with the blessing of St. Petersburg power brokers.

Their economy is the size of a small non important country. They shouldn’t even be in any convo about the world.

Other than being one of a few countries to possess nukes, they don’t matter in the least.

It’s silly to even acknowledge them.

We have the Cubans and Brazilians ready to invade Miami; and the Ugandans and Columbians are poised to make a run for the border. The entire issue can be learned in the movie: “Escape from LA,” specifically in the discussion with Mr. Snake Plissken held outdoors on the grounds of the Los Angeles deportation center. Solving the inflation self induced crisis is just going to have to wait.

Maybe this will calm your fears:

Elizabeth Strater, national vice president of UFW, said:

“I talked with contacts in citrus harvest and almond/pistachio/wine grape pruners in Kern County about this claim. This claim is not accurate.

There was no day where 75% of workers stayed home. The fear and anxiety is significant, people are downright terrified, but they still need to feed their families. An industry wide absence of 3/4 of the labor force did not occur. It is plausible to me that perhaps at a single employer a specific rumor or threat could significantly impact attendance and operations, but not industry wide.”

Yeah, that’s good sarcasm! And remember that the really serious DEI

is in the low tax rate that the wealthy get, so if Congress agrees to lower their rate even more, we’ll get an even stronger economy! More sarcasm…

Sounds Like Bernie.

Railed for taxing millionaires…until he became one.

Now he chases the billionaires. Corporate big Pharma

gets his blessing.

I would hope learning to farm would be more enjoyable than learning to code.

Tom, you’re spouting nonsense. He’s modestly wealthy ($3m) due to his success as an author and his salary/pension from the federal government, and a good chunk of it is being “house rich” from appreciation of his 2 modest homes. He lives very frugally and gladly fought tooth and nail to tax the rich progressively, even if it negatively impacted himself. He’s a pretty selfless guy and al it’s silly to target him with that nonsense.

Nonsense??

How much did big pharma put behind Bernie?

He was fighting “tooth and nail” for these “modestly

wealthy” companies.

But yea…it has negatively impacted his life!!

Bernie’s 2020 Pres campaign got $1.5MM from Pfizer out of over $200Mm he raised. Are you under the impression that he pocketed that money???!

You’re lucky Wolf fact checks economic data and not politics, he’d tear you a new one. “Big pharma” as well as every other corporation/company has donated precisely $0 to Bernie Sanders, because they cannot donate to individuals, only to PACs. And Sanders has never accepted a cent from a PAC. Any money received from pharma wasn’t from corporations- it was the researchers, HR staff, engineers, and janitors working for pharmaceutical companies, typically making very small donations. It’s fine to hate the guy but you need to learn how political donations work before spreading BS.

I Googled because I was curious how you could come up with something so stupid and ridiculous, and found that you’re repeating lies spread on the media, mostly by anti-science anti-vax RFK, who couldn’t tell his asshole from a wormhole in his brain. When dumb or biased sources spread information, you should consider their motive and look into it before spreading BS.

@Ben R, just want to thank you for your last reply. It’s pretty fxxking hilarious to hear accusations of Sanders shilling for big pharma.

While I agree with BenR’s argument vis PACs, the data is conclusive, he neglects to share other data: the sectors dominated by small contributors and corporate contributors.

With a few exceptions, since 2006 Sen Sanders haul has exceeded the average for Senate candidates.

When I think of Sen Sanders, which isn’t often (he was permanently moved to the sidelines by Obama after all), I can’t help but reflect on the line form Purple Rain: “How’s the family?”

Tax cuts for rich seems likely to maybe, tariffs at border maybe but they’ll end up mild if so , chasing the low cost labor out is just a pandering ploy. The vast majority of them will stay because that’s what the political donor corps and businesses that they work for want. And the majority of Republican voters dont care much about the topic to actually vote for politicians that will really be strict, not just talk strict.

Not so.

The driver is that it would be too expensive to deport every illegal immigrant – and accomplish all the other objectives. That was part of the actual decision process by members of the transition team. Insider info.

Lol, yep the mega donors and the chief’s staff are circling the wagons. Now us frontiersman have to wait and see. Hasn’t this circus been a repeat before? We need to get rid of some of us, really fast, that will cure and right the ship.

The entire CDC site was scrubbed today. If there’s a breakout of anything, we aren’t going to hear about it.

Their lab scientists can’t order a liter of solvent right now. Supply money is frozen. This really needs to be temporary.

One more reason to watch the bottom fall out of the stock market.

IDK,

I see a lot of over-inflated, over paid, over educated,

over titled do nothings begging for plumbers.

Maybe that explains it, see services inflation.

How to fix it, more plumbers?

Correlations in financial markets seem to be coming apart in all kinds of places.

There’s a bunch of people (part of my job) trying to figure out how to get more people into the trades. The Silver Tsunami is hitting a bunch of industries very hard and there have been decades of rot induced by middle class parents steering their kids away from jobs where they get their hands dirty.

Even the trades themselves are kicking themselves for allowing things like shop class to be removed from high school curriculums. They stood by while their future was being killed off in favor of computer labs.

@Sandy it keeps getting harder and harder (and more and more expensive) for me to find people to do work at apartments. I find myself doing more and more “blue collar” work since it often takes me longer to 1, Find someone who can come out and 2. show the inexperienced guys that do come out “how” to do it that it takes me to “do it myself” (just ysterday I snaked a laundry room drain myself). Most boys in the 60’s 70’s and 80’s grew up working with tools and fixing things around the house and working on the car in the garage with Dad. I can tell that “most” of the young trade people today didn’t grow up working with tools (in the same way people watcing me play golf can tell that I didn’t “grow up playing golf”)

I spent the bulk of the final 8 years of my career trying to promote the trades to young people and their families in a primarily white collar suburb — it was a thankless, uphill task. I don’t regret it, because I believed in it (and still do) but I have no illusions about either my own success in the project nor the bigger picture where acceptance of the necessity of some cultural transformation around this issue is concerned.

I’m making around 110k in a MCOL area before 30 years old. In 3-4 months I’m slated to be bumped over into another division at my company making ~140k.

I drive a truck for a living and usually work 60-70 hours a week and have 2 hours of commuting everyday unless I sleep in my car at work. It took about 4 years to climb up into a decent job where I am and a lot of luck. A couple years spent homeless living out of the truck, spending 3 months on the road at a time making 40k/yr. It absolutely sucked and honestly, it still sucks and I hate the job and industry but at least I make decent money now.

Meanwhile the 1-2 times a month I have to talk to my parents it is the same monologue from either one about how I should quit trucking, go to college, sell all of my stuff, move back in with them, clean their house and fix up the yard, get a degree in “computers,” and get a white collar desk job and find a girl in college to marry and have kids with.

Meanwhile, all the IT jobs pay half what I make unless you get lucky by knowing someone, the political/corporate system is firing Americans to bring in visa-slaves, and the college costs are through the roof.

But pointing this out just means I’ve been brainwashed by Democrats because I moved away from some shit hole Southern state.

I hate my job and working my life away but I have a realistic chance of buying a cheap fixer upper house, paying it off, being debt free, and in a decade or so being able to transition to a normal 40 hour a week and close to home job that pays the bills. The whole “gotta get that piece of paper to function in society” is the real brainwashing at this point. Basic laborers in construction are making 30-35 dollars an hour here. Even trades that require degrees like machinists don’t even pay that well. Local machine shops pay 25/hr for associate degree machinist jobs. Residential electricians and plumbers are making 40/hr. Concrete jobs and heavy equipment can pay mid 40s/hr here.

Seems like for the working class, the more formal education you have the worse you’ll be financially. It’s absurd that knuckle dragging welders in job shops pay 30/hr when a manual machinist who can read prints and a vernier scale caliper gets 20/hr.

YouTube it?

Eventually someone will get the shit to go thru the pipe going downhill.

Lol

@motorcoty, I see a lot of plumbers and blue collar workers who love technology, or sometimes hate it but need to use it anyway, that are whining and begging for help getting their shit working. People like technology and there’s a lot of demand for it. It’s also a very stressful industry that requires a ton of education and specific skills. My work involves the intersection of IT and electromechanical systems, they are both very important, but a lot more education and knowledge is needed for the IT side of it (even though plumbers and electricians will be much more important if/when SHTF).

Reminds of the GREAT episode on South Park where Randy want to fix his oven. He teached his kids by saying, “What you do is pick up the telephone” This was late pandemic, so no handyman is available. He goes down to the local Home Depot where there are often handymen hanging out, but this time all he sees are white-collar workers with sign “Acctg services available”, “Lawyer Sevices”, “Scripts and screenwriters” Computer Programmers” etc etc.

Later, the blue collar trade workers are riding around in fancy cars… Funny as hell.

Classic. They blame their colleges for giving them worthless degrees instead of actually teaching them how to “do stuff…” But when they try to get revenge they can’t figure out how to assemble the catapult and have to call the handyman! The Randy storylines are the best.

This one is particularly fitting for this forum too- it demonstrates how everyone outbidding each other for the handyman contributes to insane service inflation (and not even due to the greed of corporations, but the laziness and lack of initiative of the general public). Matt and Trey are on another level.

“Matt and Trey are on another level.” Indeed — not least among their accomplishments is the evergreen “Team America” …

Don’t worry everyone! The federal government is investing resources to banish the inclusion of pronouns in email signatures. Screw inflation, you need to focus on what matters!

Who cares?

They are weak blowhards that couldn’t do something right longer than 3 days.

The wheels are already coming off. Reagan judge balls up the orders and throws them in a wastebin. Puts his feet up to finish an episode of matlock.

And the old dodge dart musky odor is just making the fed workers want to resist harder.

shoulda been scrutinizing inflation instead of sidetracking into gender pronouns in govt. email signatures whatsoever.

Maybe pivot to ZERO QT!

Why not? /s

…….but don’t call that a “bailout”, call it a normal way of good policy.

The heavy weighting of housing would seem to suggest that it is the core of the problem.

And, considering the monumental importance the Fed has put on “wealth effects” during the long night of ZIRP (turning real interest rate cashflow declines into vaporous asset inflation), they are likely terrified of the flipside “poverty effect” of significant housing asset price reductions (think about how central housing inflation is to the current crisis and how relatively little political hay has *really* been tried to make of it – by either party. They are in a box canyon of their own making and they know it).

Considering the potential political capital, neither party has said very much about housing inflation – because they are terrified of touching the mechanisms behind it.

The terrible problem is that housing inflation has to come down but the powers that be are absolutely terrified of the “poverty effect” they think that means – thinking their phoney-baloney, ZIRP summoned housing “wealth effect” saved the country for 20 years.

In the long run, the only thing that saves countries is international competitiveness, not paper-driven asset valuation manipulations.

(Along these lines, Trump’s tariffs are likely fairly terrible ideas – but the US is so debilitated and so deluded about it, that those tariffs might be necessary to create some space/time for industrial rehabilitation. Or they could simply become the next heroin).

“they are likely terrified of the flipside “poverty effect” of significant housing asset price reductions”

I’d jump for joy if I woke up tomorrow and my house was reassessed at 50% of its current ‘value’ tbh.

The tariffs may or may not succeed in the long run. They are in place precisely because international “competition” is not conducted in free markets. Other nations have had tariffs in place that antedate Trump’s moves for decades, intellectual property theft is real, currency devaluations, capital flow controls, subsidies, the whole ten yards are part of the equation. That Trump is using tariffs for reasons beyond competition (e.g., border control) can precipitate dysfunctional behaviors. We shall see.

Let the festering continue ( or not):

From Fed Schrödinger Cat Model:

“Employment has grown persistently since 2021 (albeit at declining rates), and the unemployment rate has stayed low. Under this view, inflation will remain elevated for as long as the labor market remains tight.”

Very clear now that the 100 basis points cut since September of last year was a mistake.

Then fatzilla attacked North America.

Who coulda seen that coming?

Mr. Wolf writes: “In a broader sense, there has been no progress at all on inflation in eight months.”

“Inflation is always and everywhere a monetary phenomenon.” Milton Friedman

When you let off the brake, you keep moving. Sooner or later there is either a recession or increase in interest rates to cure the inflation that the monetary authorities created themselves. Alternatively, inflation will demand higher interest rates for the debt; solved through borrowing or more Quantitative Easing (QE), but the inflation the stop gap measures cause is a “positive feedback loop” that is the definition of an unstable control system.

With due disrespect to Uncle Milton (and there’s no shortage of that) inflation is always and everywhere a distributional, and therefore political, phenomenon. In the end it’s about power.

So wild that people continue to repeat that quote as old Milton was proven wrong repeatedly very shortly thereafter. That was more than 40 years ago when people realized that velocity of money was not only not constant, but not even predictable.

But it’s simple to understand so people keep using it.

“For every complex problem there is an answer that is clear, simple, and wrong.”

HL Mencken

Empirically, this is about as correct as anything in economics. Show us a single instance of significant inflation anywhere in the world in the last century that wasn’t accompanied by expanding monetary supply.

In the other corner, 1970s and 2022-2024 USA, Weimar Germany, every country in South America for almost all of history, and pick your country in Africa. Basically every modern instance of significant inflation.

So, punditry is in disarray at the moment. Some project the US is headed for stagflation, others believe a debt trap lies in the future. Which is more likely? Different solutions implied.

Progress has been transitory?

I’ll say this again, as it didn’t seem to get posted last time. As Wolf is documenting, the overall trajectory for inflation is up. The Fed knows this and doesn’t want to look like they have lost control. Tariffs incoming as well, that will increase inflationary pressures.

Keep trimming the balance sheet Jerome! LOL!

I have not seen one single thing out of the new administration that mentions inflation. Not a focus. It got them elected, but now not even on the table.

What is mentioned is a “painful transition” as we on-shore jobs, and reach something Vance is throwing around as autarky. Whether the US can reach full economic independence and remain the world’s reserve currency is over my pay grade. But I do want to watch from well out of blast range.

All they seem to be doing is the Project 2025 stuff, which only a few months ago was polling below 10% and they were all acting like they’ve never heard of it.

Meanwhile, nothing at all on prices, and suddenly 25% tariffs on Canada and Mexico starting tomorrow, apparently across the board including oil, unless that too changes at the last second.

Everything I’m seeing is like the exact opposite of what got them elected. It’s totally chaotic and goes against basically every poll even among Republicans. The approval ratings are already starting at a historic low. It’s really inexplicable.

They’ve been working on getting this type of control since 1974 and budget purview went to congress. They hit the trifecta and now all control rests in the exec branch. Except the Fed. We’ll see how that plays out.

This will all end badly for everyone not already a billionaire.

“It’s really inexplicable.” It would be inexplicable if this were NOT the case. He ran on lies and conned America to enrich billionaires last time. You’d have to be pretty dense to think this time would be different.

Thank you @BenR for the sanity. I’ll be watching from a distance, but probably not far enough to be comfortable.

I should clarify it’s inexplicable for me that everyone had so much warning they were planning to do this, and that none of those warning are turning out to be overstatements, and they still managed to con so many people into this.

…yes, plenty of warnings there, but when broadcast to a nation recently analyzed as 71% literate, with 50+% of THAT group only reading at sixth-grade level or under, not difficult to see why those caveats were not particularly effective. A result of our long-term not really caring about education, at public AND family-level, as a crucial long-term source of national vitality…

may we all find a better day.

The medicine for inflation is very bitter (recession, high unemployment). It takes some suffering before politicians are bold enough to administer it (the Fed doesn’t operate outside the political sphere – for example, if a monetary policy action would help war aims, they would do it).

Bernanke touted the “high pressure economy”, with inflation being accepted at 3 percent.

Inflation likely played a role in the “red wave”. In the late 70s some 40 percent of the house of representative was voted out (if you google “incumbency rates open secrets”, you can see a chart).

However, high private debt can act as a brake on spending and inflation, it seems to me. The New York Fed Report on Debt and Credit shows very high household debt. The Money Velocity chart from FRED shows a strong rebound around the time inflation kicked up. Perhaps the powers that be are looking to see how 3 percent inflation with high debt works out.

“The New York Fed Report on Debt and Credit shows very high household debt.”

I thought household debt was at an all-time low vs e.g. 2010.

Uncle Sam is the one running up the credit card bill these days…

There are a LOT MORE people, and they’re making a LOT more money. So household debt in relationship to disposable household income — which is what matters — is VERY LOW (New York Fed data)

https://wolfstreet.com/2024/11/13/household-debt-delinquencies-collections-foreclosures-and-bankruptcies-our-drunken-sailors-and-their-debts-in-q3-2024/

I see these people everyday in traffic.

They clog up the off ramps of Raleigh, slowing down the highways.

Even the fancy new toll road sections are very packed.

I have no data to back this up, but my gut feeling is that the low EBT numbers are because of 2008. Millennials (in my circle, so this is anecdotal) are extremely debt averse.

That could just be my friend’s and I though.

That’s not what the data says. Millennials are following the typical pattern, it seems, though maybe a little later than others. They’re now the biggest home buyers and mortgage applicants, which is natural at their age. When they first set up their new households, they’re also using their credit cards for stuff like furniture that takes them a little while to pay off. They’re leasing or financing their cars, roughly like others. I don’t see an unusual debt aversion in the group overall.

The decline in the burden doesn’t come from a decline in the debt, it rose. But income rose a lot faster than the debt.

There is another medicine for inflation. With it’s own set of ill effects.

“Hard” money, serial number accounting, very basic fixed amount of money in the system. Interest rates must then be zero as interests by it own generate money.

The bigest downside, at least political, is that the government can not spend more than it tax.

Every regime of the sort you describe fails — without exception: see n-many “gold standard” abandonments for details.

Every fiat money system have collapsed too. Usually within less time than the current system have existed.

The reason that “gold-standard” and the like fails often is down to interest rates. With a fixed amount of money system, interest can not be applied as interest generate money.

Think gold coins, interst do not generate gold. Whatever the interest rate , if you want more gold you have to dig for it.

Fiat money sysem do not have that problem, with checks ans balances the amount of money is always heading towards infinity as an exponential function.

A growing economy needs money to grow with it proportionately or else the economy gets strangled. Money growing with the economy proportionately is not inflationary. That’s where the gold standard fails because in the huge economies of today, you cannot dig up enough gold to keep up with economic growth. And it would be nuts to let a metal strangle economic growth.

…just for fun, rather than looking at the ‘hard’ or ‘fiat’ monetary systems as center stage of the proceedings, perhaps examine and consider the general character and standards of business ethics by the population of a nation in the use of either of them…

may we all find a better day.

The FFR has been at its current level (4.25-4.50%) or higher since January 2023. As Wolf said, trailing-12-month core PCE has been firmly stuck in the 2.7-2.8% range since May 2024.

I have a hard time believing simply holding it there for longer will get it down to 2%

Nothing that lower interest rates, tax cuts, bigger deficits and wide ranging tariffs can’t fix.

These charts are going up and down, with no sustained improvement towards the Fed’s goals for inflation. It looks like inflation is not going away anytime soon.

Over the longer term it increasingly looks like the inflation rate bends towards the Fed’s interest rate.

Potato chip bags getting smaller and larger: at a higher price.

And, many more examples.

B

Ooops!

should be smaller and smaller.

You had the “larger” part right the first time – Americans’ sweatpant sizes from the potato chips.

I read once that Wal-Mart lobbies very hard to keep all those snack isles on the approved SNAP food assistance list. Lots of big profits there. Not a lot of profit on chicken and broccoli.

Seems like eventually it will be like the GS cookies – you get about ten per $6 box now I think. I still buy them to support the kids though.

We have to find a way to pay off the deficit before we go bankrupt in 5-10 years.

Any ideas?

Andrew pepper

No we don’t have to “pay off the deficit.” The “deficit” is an annual difference in flow of money between tax receipts and outlays. So what we can try to do is reduce the annual “deficit.” There are 3 ways to reduce the deficit: cut spending, raise taxes, and a little of both. Enough of it will balance the budget = no deficit.

We don’t even have to pay off the “debt,” that $36 trillion, not in 10 years, not in a million years. But cutting the “deficit,” maybe eliminating the “deficit” with a balanced budget, year after year for years will gradually reduce the burden of the debt over time through economic growth and inflation.

Do some searches on Girl Scout cookies business model and you’ll have a tougher time plunking down your dollars. It’s a machine and the kids see very, very little of it. They have rules now about how much the kids have to sell, so they use their digital links to hit up family members, extended family, anyone you know on social platforms, friends of family members, etc…

The whole thing is rotten to the core, but when you come face to face with your dealer out in front of the grocery store (or dispensary if in California) it’s hard to fight your Thin Mints addiction.

Andrew pepper, along with Wolf’s comments, countries do not go bankrupt. They simply print more money. I recommend a course in Econ 1. Most adult schools have one and it is usually free.

Thurd2, I don’t recommend stopping at Econ 101 — it’s a classic case of “a little knowledge is a dangerous thing” (to the extent that the neoclassical orthodoxy constitutes “knowledge” rather than the religious dogma serious ontological examination reveals it to be)

@ Thurd2,

Countries with debt in their own currency can’t go bankrupt, but it f their debt is denominated in another currency they absolutely can and do, see Argentina repeatedly for one obvious example.

sooner people start buying organic the better. youll have more trust in what you put in your body as the FDA goes which way now??? and per bite/ morsel much more dense flavorful food . I think my grocery bill has gone down since I have been transitioning to organic for various reasons . from cereal/bananas/ grapefruits/ tomatoes/milk/ occas bag of tortillas/wild caught seafood/ small dark chocolate bars for the occas treat….and other….at same time happily cut out that junk food called bread in the process. choices are there.

True

I’m pretty much all organic atm.

The Whole Foods sales are kinda awesome and affordable actually.

Hydroponic is the way to go. Best tomatoes ever. The real secret is to learn to cook properly; buying quality ingredients and cooking them yourself is way cheaper than buying fast-food or eating out in restaurants. Once one also cuts out highly processed foods from their diet, all the better.

@nicko2 I wish the schools would try and get more kids to “learn to cook properly; buying quality ingredients and cooking them yourself” and explain to them that “is way cheaper than buying fast-food or eating out in restaurants.” It is crazy how it was rare to see anyone in their 20’s over 200 pounds and today it is common (for men and woman).

Apartment, back in the day, high schools had a required course called Home Economics, mainly for girls. This was all before our educational system went to hell.

…an interesting historical study (sorry, Wolf), is the legal dilution-wrangling by Big Ag that settled on today’s national ‘organic’ standards, making it easier to subvert and enter the preexisting market-more availability and perhaps ‘better’ than non-‘organic’ products, but mebbe not as ‘good’ as one would think (…we won’t go into the adjacent issues akin to contamination of one’s organic crops by migration of patented GMO pollens from another’s fields…).

may we all find a better day.

All that other stuff is great but bread is not bad, wheat or more grain is healthier but french bread is great too. It perfectly compliments so many things. I eat bread daily and I’m very slim, not bragging just saying, but one needs regular physical activity too.

Greedflation is clearly a thing (PE overlords at my old job sent an expert consultant to direct us how to aggressively implement price hikes with volume reduction in our business, and ways to pursue customer lock-in to make them eat it), but isn’t inflation also something we should inexorably expect from the de-facto legalization of real-time price-discrimination across the economy? The new MO is to set the base price the old fashioned way, then use the tools of surveillance capitalism to gouge the top half of customers to their exact walk-away points. You can literally visualize the sellers filling in the triangle on your econ 101 P vs. Q chart to capture any iota of “consumer surplus” that used to exist. Doesn’t that theoretically have to result in inflation?

You are correct, of course, but this sort of observation is about as welcome as farting loudly in church — good luck to you, because you’re going to need it …

🤣 send me your finished hyperinflated worthless fiat dollars. As a free service to you, I promise I will dispose of them properly in accordance with all applicable laws and regulations.

I’ll pay you 10 cents for each of those worthless dollars if you send them to me instead of Wolf.

11 cents, but you have to send them to me by Feb. 6.

I bid 11 cents

11.1 by Feb. 5.

Screw all these lowball offers to buy all your dollars with worthless cents. Send your hyperinflated fiat dollars to me and I’ll pay you with Fartcoin!

I may have a Zimbabwe $20 Billion dollar bill laying around here somewhere. Would two 10’s be OK if I can’t find it ?

Deal if it is in us silver coins!

Today must be national sarcasm day based on the comments here so far…

ya think????????

:-)

Sorry, couldn’t resist, it being national sarcasm day and all.

It is simply amazing how much greedflation is to blame. But hey, those rising profits aren’t going to fund those aggressive sharebuybacks on their own. As for inflation, welp, Saturday tariffs gonna be fun. So will Powell do the handwave about the price increases due to tax increase? Dunno.

My guess is pause until they have to raise, because dammit, politics.

Stock up folks, it is going to be ugly.

Someday this war’s gonna end…

11:46 AM 1/31/2025

Dow 44,555.87 -326.26 -0.73%

S&P 500 6,045.69 -25.48 -0.42%

Nasdaq 19,644.98 -36.77 -0.19%

VIX 16.30 0.46 2.90%

Gold 2,833.00 -12.20 -0.43%

Oil 72.45 -0.28 -0.38%

You missed the biggie

TNX yield loves PCE and tariffs

I don’t usually comment on non-core inflation, but prices at the supermarket (I shop at Walmart and Sprouts) are going up at a pretty incredible pace. Next overall CPI print should be an eye-opener.

The USA has been firing on all cylinders. Energy independence, technology leadership, AI leadership, etc. Thus we have low unemployment and increase in salaries. This means it is more difficult to get inflation to down.

I am not sure if anyone has noticed that Germany is in the 3rd year of economic contraction. France this past month went into contraction. Canada is hurting. China has been in a mess since COVID. So all of the above countries have low inflation but struggling economies and rising unemployment rates.

Now tariffs are going to hit these same countries the rely on exports.

Anyway, most Central Banks have been cutting rates and signal they need to cut more.

The U.S. is still the best place to be economically even if inflation is sticky.

“I am not sure if anyone has noticed that Germany is in the 3rd year of economic contraction.”

Chalk that up to NS sabotage

And European elites collectively losing their minds with slavish Atlanticism — their descendants will be paying for this for generations.

All depends on what you measure. Chinas GDP growth is stronger and Indias even more so.

China’s numbers are completely manufactured. As best they are exaggerated and at worst complete fiction. Academics, economists, and even China’s premier have said so themselves. There’s a 0% chance they are growing at 5%. Not when SEA companies are chipping away and China’s manufacturing sectors

They manufacture everything else, so …

Oh, and is DeepSeek real?

If the Fed had left QT alone we’d have inflation under control and be cutting rates.

This FED has been exposed. So much so they’ve floated the sale of MBS. Imagine selling an instrument that has finally begun to perform (principle payment) at a loss.

Inconceivable? Hardly.

They’ve been “float[ing] the sale of MBS” since 2022. They aren’t going to do it.

MW: US Treasury yields end at 1-week high as White House readies for tariffs Saturday

Well, here come the “beggar thy neighbor” policies and it is past due.

Wolf,

I don’t see how inflation could come down. Trump and Melanie issued meme coins that are worth tens of billions. This is money created out of the thin air! Trump will issue more coins for his kids and grand kids. Other people like celebrities, athletes, tech people, and business people will join the party. Pretty soon, you are talking about hundreds of billions and even trillions of dollars created out of thin air. The issuers will cash out and spend their money in the real world buying up stuffs like houses, cars and traveling, etc. It will create high inflation if not hyper inflation!

“Trump and Melanie issued meme coins that are worth tens of billions. This is money created out of the thin air!”

No, meme coins are not “money.” they’re empty paper bags filled with thin air that some people trade amongst each other to drive up their price, and some day the price will collapse. OOOPS, I just checked, $TRUMP has already collapsed by 65% from the peak, and $MELANIA by 85% 🤣🎇🍾🎉🎈

But Trump can cash out a big chunk of his coins. That’s real money that he can buy things in the real world.

But it’s not” out of thin air.” He’s simply taking advantage of the people that got him elected and robbing them blind, as he has always done and will continue to do. There can’t be a winner without a loser. See Trump University/his other bankrupt businesses, DJT stock, or the USA middle class paying for tax cuts for the ultra rich for other examples.

Wolf, are meme coins regulated at all? Any reporting requirements? Seems they’d come in handy for some serious money laundering schemes if not.

Thanks for any info as always.

No, they’re empty paper bags filled with thin air that some people trade amongst each other to drive up their price until they collapse, and everyone knows that, and as such they don’t need to be regulated.

And I think this is the correct approach. Let cryptos burn. If people, whose greed drives them to shut down their brain, buy these empty paper bags, they deserve losing everything. That’s risk, and they knew it going in. they gambled and lost. No biggie.

No different than selling paintings of dogs playing poker being sold in front of closed gas stations, depending upon the value of the frames.

@wolf I agree 100%, especially on the meme coins. But it’s easy to underestimate the stupidity of the masses. With large financial institutions, ETFs, and now the US government trying to normalize and prop up some of the more mainstream cryptos, it’s hard not to worry about it being shoved down our throats, especially if weakness begins to show in the USD. You may end up being right, but so far BTC is near it’s ATH. Over decades it has made many rich while only those who bought high and panic sold lost money. So I’m not sure it’s fair to say people are gambling and losing- up until now those who’ve sat out have lost. Fwiw I’m a T Bill guy the past few years, but I have 25% in stocks and 5% crypto (something more environmentally friendly than Bitcoin). I sure hope you’re right in the long-term.

“If you don’t make your product in America, which is your prerogative, then, very simply, you will have to pay a tariff — differing amounts, but a tariff — which will direct hundreds of billions of dollars and even trillions of dollars into our Treasury to strengthen our economy and pay down debt,” he said.

He still thinks the exporter pays the tariff. Kind of like admission to Bedminster or something.

This constant anti-tariff BS is hard to stomach, especially when it comes from foreigners that are being tariffed, Nick Kelly, Canadian.

I’ll just repeat what I said a minute ago about tariffs on Canadian lumber:

The US has LOTS of timber and is a HUGE lumber producer. Logging is a big business here. You city boys need to get around a little, and you’ll see. Or you can just look down from the airplane, and you’ll see too, just like you’ll see the fracking sites carpeting the land.

And the US is also a big lumber exporter. In 2023, the US exported $38 billion in forest products, $10 billion of which was exported to Canada, LOL.

The US also imported $51 billion in forest products, including $20 billion from Canada. So the US had a forest products deficit of only $13 billion (exports minus imports), and its forest products deficit with Canada was only $10 billion.

So the tariffs will shift more production to the US, and Canada is going to lose some production, or its producers will cut their price to compete, and in that case, Canadian producers eat the tariffs.

And on the portion that shifts to US production, there are no tariffs anyway.

Proudly Canadian.

The merits of tariffs are the topic of ongoing debate. Canada has tariffs on dairy. However the point made is that Trump seems to not know what a tariff is. He seems to think it’s paid by the exporter.

Sure, the exporter may decide to ‘eat’ part or all of the tariff to keep the sales, but this is not the same as not knowing what a tariff is.

Sounds like Trump understands tariffs better than you do.

But yes, that big US gravy train that foreign exporters and US importers have been riding to get fat by creating the gigantic US trade deficit may be screeching to a halt. That globalist dogma, that has been promoted like a religion in the US, has done huge damage to the US. It’s time to kick it off the cliff.

I never figured you were an anti-globalist. Interesting.

Canada is now more motivated than ever to sign new free trade deals with the EU and beyond. This is probably a good thing for Canada in the long term.

Remind me to turn over in my grave when the trade deficit comes screeching to a halt and the hundred billion in tariff revenue is going to make us great again.

Tariffs are an inefficient way to rob Peter to pay Paul. And it is much more complicated than you appear to credit it. Whether you agree or not, we are now a huge Global economy, that has been running fairly well due to global commerce. Adding a tariff to Canadian lumber does not necessarily mean America will produce more lumber, it may mean we purchase more lumber from a lower cost country. Same goes for all other tariffed items. Tariffs have not worked well in the past, I expect this to be no different.

“it may mean we purchase more lumber from a lower cost country.”

The point of tariffs is that there is no lower cost country to get the lumber from, so might as well produce it domestically.

This would be true if domestic manufacturers took advantage of the opportunity to undercut foreign manufacturers. What if a foreign manufacturer has to raise prices 10% but the domestic manufacturer sets his price 8% higher? Enough to beat the foreign manufacturer on price but still contributing to higher prices overall?

Escierto

1. SO then you increase production in the US and get all the benefits from that, including the supportive industries, the primary, secondary, and tertiary jobs, the spending and taxes by these people etc.

2. you assume that there is a monopoly in the US that can raise prices at will. But that doesn’t happen. Prices of lumber collapsed in the US over the past two years, and this has nothing to do with Canada. The last round of tariffs triggered no inflation, inflation was low and stayed low.

3. I get so tired of this anti-tariff braindead bullshit everywhere.

Nicko2,

Who is anti-globalist? It’s about sustaining fair and balanced global trade, not ending trade. You missed the point.

We will debate in future but loved the frame re: Russia’s mafia headed by Putin being out of politics

Scott

Premature, yes; ludicrous to mention, no. Perhaps a useful reminder of the extreme dangers of excessive money printing.

“The Z$100 trillion banknote issued by the Reserve Bank of Zimbabwe in 2008 represents one of the most stunning examples of hyperinflation of all time.”

Multiple sources.

It’s an oddly exhilarating and sobering experience to have one of these notes in your hands, even when, thankfully, one is shielded from its realities and consequences.

You can buy “Trillion Dollar” Zimbabwe bank notes on eBay for less than $30 (so you can tell people you are a trillionaire) and buy the “Billion Dollar notes for even less (to tell people you are a billionaire). I bought Malawian 50 Kwacha Note on eBay for under $10 to put in a matted frame at the cabin since it has a cool Land Rover Defender 110 on it.

Joking aside, it *is* the general sense that DC has really, finally lost desire/will and most importantly, *ability* to restrain spending that is the primary, core motivator for *any* cyber-currency (ie, built in anti-print, anti-dilution mechanisms).

Now, even given that impulse, current cyber-coins are still very, very much a riverboat crap-shoot.

Short of the gun, money printing/distribution is *the* primary, ultimate bulwark of Federal power – anything that *really* threatens that power, will eventually have to be attacked, destroyed, or co-opted in some way.

Otherwise the US will become a very different country (likely much worse, then, hopefully, much better) quickly.

It might be the case that the Feds can *openly* convince worldwide USD holders that systemic dilution (“transient…”) is ultimately in everyone’s best interest for baseline social stability.

But if the Feds really felt they could carry that argument – especially among the US general public, money printing would not have been branded “quantitative easing”.

Bottom line, nobody (up to, and including, China) likes to have their savings intentionally and systematically diluted. China, US citizens, dollar holders worldwide, everybody – other than the printing authority.

All the cyber-currency motivations and implications proceed from that fact.

In the past, governments rose and fell over this sort of thing – wars were fought using, behind the scenes, the power of money printing.

Cyber-currency has just altered the form these battles take and the size of the entities that can launch them.

Cyber-currencies are created out of software. And software can be made to do anything in the world you want, including flat-out printing.

Kent,

I agree, but at least ostensibly and to date operationally, I don’t think there has been any proven inflation trap door shown in Bitcoin for example – but there could be (excellent argument for the G to float if BC ever really endangers DC USD…).

And, in the end, it is the dynamic (systemic dilution by a central authority) rather than the particular manifestation of currency competitors (Gold, BC, Oil, whatever…) that matters.

Nobody wants their savings systematically diluted, sub rosa. So they will hunt out something/anything to try and avoid it.

Unfortunately, even before the post 2000 ZIRP crises I think the US G got *way* too comfortable with the operational annual dilution of, say, 2% (“necessary” inflation) rather than having to politically justify equivalent tax increases (to fund DC’s apparently insatiable need/desire to spend) – “government by sneaky bastard” tends to be unsustainable because people catch on and/or the sneakiness becomes an addiction and get abused.

Even if you think that every Federal dollar spent was wise, systemic inflation has become a more and more dangerous way of achieving it.

Cas127 bitcoin is not immune. Look up a 51% attack. This affliction is shared amongst all cryptocurrencies and it is not out of the scope of a state actor.

The medicine for inflation is recession. Nothing else works. Repeat: Nothing else.

💯

And this is BEFORE president Trump throws a few grenades (tariffs, tax cuts, Greenland purchase, etc).

Wonder if he was brushing up on history and got to the Louisiana purchase time in history…

And he put the book down and can’t stop talking about how cool that was.

Gotta keep reading tho.

Genuine question: after reading the comment section it seems like the majority of posters are lamenting incoming tariffs, tax cuts, interest rate changes.

Does the financial sector still generally see Republican administrations as more economically competent? For example, if I met a financial planner on the street and asked them who/why they voted for, I’d expect > 50% to say R because of economy.

People who work in this area, has there been a vibe shift among workers? Is this just a WolfStreet.com thing? Just this articles comment section? I work in education so I’m not familiar with sentiments.

Yeah finance skews R, cuz it’s wealth building.

That’s just the people convincing other people to buy something like an option or stock of some random company. Or otherwise part or let the R guy use their money.

There is a ton of fraud in finance.

Now the academics prob a 60/40 split D, I would guess. Overall I’d say 80/20 R, but some of the big names are riding the rail right by the middle of the road R. Like common sense kinda conservative “boring” “do nothing” with your money R. Those are your “gurus” that are out there. I really love some of the gurus too.

Actually, “academics” are about 90/10 D ( kinda like the mainstream media ) !

Genuine Answer:

The entire financial system is a grift, but the new administration is at least aware of it. If they don’t slow down the pace of wealth disparity, nobody wins. I voted for him 3X.

Do you see Trump’s admin making changes that would help wealth disparity? If so, what would a relevant policy look like?

Slum dog,

They will hire Hoover to make a huge vacuum. It will suck up all monies and put them in rich people’s pockets.

The end.

Rich people hate poor people, and the new admin is prob the richest people ever to hold power.

They hate you! Period.

So you will suffer

I think a start would look like term limits on all elected and appointed officials. 100 percent tax on lobbyists. Repeal of Citizens United.

A lot of assumptions rolled in there…

You identified financial themes being discussed, but you are jumping over the social implications of them. I have just been lurking here for a year or so. I would say you probably have a bunch of pretty regular joes in here of the stock owning class, more than financial planners. (Maybe a good chunk of real estate inestors at best.) Maybe I am misreading the room.

I would say anyone voting purely based on an interest in large profits is an R because they are selling tax cuts and deregulation.

But I think lately, people mostly vote on social issues. Most people are clueless to what is actually going on in the financial markets beyond what some pundit feeds them or some ticker anecdotes spoon fed to them along with some oversimplified explanation of why it went up or down.

This seems to be a pretty well informed group of folks not necessarily in the biz…

But I’m assuming with you…

I would say the one most common theme here is skepticism of the effectiveness of the Fed, especially when it comes to everything outside of rate setting….(Direct monetary manipulation.)

Maybe inflation is like a campfire.

You gotta extinguish it, completely dead and buried, drowned out.

Otherwise don’t be surprised when it comes roaring back.

Of course – the FED probably wants it to come back – in more of a “controlled burn”. Out west we have seen what happens when a controlled burn becomes an uncontrolled catastrophe more than once.

Or maybe it is more like weather, space lasers, and cloud seeding?

If you get struck by lightning then you just know that the Old Testament God doesn’t like what you are doing, so you should just suddenly do the opposite of everything you have been doing in your life?

What on earth are you talking about?

I just bought my pack of cigarettes two days ago. Burned through them almost as fast as my paycheck. What the heck?

Last week I bought my favorite whiskey. It disappeared almost as fast as my pay check. Drinking all this whiskey is so risky.

I can’t take this inflation. I never get a vacation. Ten years ago I was thinking of joining the seminary. Now it feels like I’m ready for the cemetery.

I’m smoking. I’m drinking. I’m doing too much thinking. I’m thinking my money is funny. ‘Funny money’ – Strike that! It’s killing me. Everyone is billing me.

I got no money. It isn’t funny. I’m writing letters to the editors.. I can’t seem to get rid of all these creditors!

Let me say this bluntly – I thought we lived in a free country.

But now I’m feeling like a slave. I’m ever so close to livin’ in a cave.

Bills, bills, more bills. I need to take pills, pills., more pills.

They’ll help me forget my misery. I got a pigeon on the rotisserie.

I make minimum wage, but I have maximum rage. I don’t wanna make a scene but I wanna rage against the Machine.

Poor House George:

WELL DONE!

I just bought my pack of cigarettes two days ago. Burned through them almost as fast as my paycheck. What the heck?

Last week I bought my favorite whiskey. It disappeared almost as fast as my pay check. Drinking all this whiskey is so risky.

I can’t take this inflation. I never get a vacation. Ten years ago I was thinking of joining the seminary. Now it feels like I’m ready for the cemetery….

etc, etc..

Trump pleasantly surprises me with his comments about history. The period 1870 to 1913 when tariffs helped make the American economy great, with no income tax, and no Fed.

The history of the Panama Canal, soon to be the American Canal, built, owned and operated by the United States of America.

The acquisition of Greenland, carrying on the expansion of our country by land purchase. Recall the Louisiana Purchase and Alaska, the two greatest real estate deals in history. Also the Gadsden Purchase.

It seems Trump finally has some good advisors and is listening to them.

Third2:

LOL on that one!

Meanwhile “Austrian-Libertarian” Mish has been attacking Trump / tarriffs and is now a staunch defender of the personal income tax system.

Much has changed since 1870 to 1913. America never really owned the Panama Canal, they just had rights to its control. Greenland does not want to be part of US.

Of course much has changed since 1870 to 1913. The point is that tariffs were and can be effective.

If we did not own the Canal Zone, why did Carter sell it to Panama for a dollar. You can’t sell something if you don’t own it.

You do not know what the Greenlanders want or don’t want.

Don’t be stupid.

He did NOT sell it for a dollar, he turned over the rights to Panama via the Torrijos-Carter Treaties. You should probably read them instead of listening to propaganda. And Greenland has had polls already on whether they want to be part of the US. It was 85% NO.

Oldguy. You still believe polls? Then Trump should have lost to Hillary in 2016 and to Kamala in 2024. Polls are crap.

As for Panama, we built, owned and operated the Canal Zone from 1913 until the imbecile Carter sold it. We are simply taking it back. FYI, the Canal Zone was the most prosperous place to live in Central America until we sold it to Panama. Many Panamanians will be happy when we take control of it again.

(Wolf-i’m sure you will moderate me, and, as always, understand, but freeriding excuse-of-an American citizen assholes like this like this I will never countenance, no matter my age). Thurd- admittedly, you may be trolling here for your own amusement, but if you aren’t, and you aren’t personally gonna be in Panama or Greenland on that inevitable front line, field pack dropped, weapon locked and loaded, deployed with, and just ahead of our (prior draft-dodging) Chief Executive whom you’re SURE will stick in the face of enemy fire and give you adequate cover, and prepared to take that incoming round BEFORE we send any another American citizens to subject people somewhere who didn’t ask for, or want us-well, you know where you can go…

may we all find a better day.

Does it matter what Greenland wants? Or even what the American people want? The new regime is now in power and they are going to do whatever THEY want.

How true, the wants of us Peons are insignificant to those in power. We are the “Taxing Units”. remember? That’s really all they need us for.

Wow….The comments today are revealing, the lack of knowledge, hate for Trump, seems like a lot of crying. You do not understand Trump, you are blinded by false media bias. He doesn’t want the canal, but wants the Chinese removed from security. We , the U.S. , per treaty, signed control of canal to Panama. As for Greenland, he want s s military base, and mining rights. A deal will be made, and not as a state.

I was stationed in the Panama Canal Zone from 1970 to 72. There was some anti American ‘Yankee go home’ gathering going on at that time. Torrijos gave a speech that stated (I’m paraphrasing) ‘other countries are blessed with natural resources like oil, minerals and fertile land. Panama is blessed with a thin waist’. The canal is 50 miles of mostly jungle. The main worry at that time was that a small band of soldiers with mortars could block the canal by sinking a ship in one of the choke points. So turning over the canal, but maintaining bases there, may have been more calculated than we think today.

Seems like you are cherry picking…

What about industrialization?

Are we really in a comparable era of large land acquisition?

What about wars or lack thereof?

Didn’t this period end in the Great Depression?

Dude we were poor as shit then.

Only the rich were thriving.

Ever heard the term “The Gilded Age”?

Gilded as in a facade , a fake out, a farce.

Only until 1946 did every American start to thrive.

Let’s read our history better there. Crack open a book and burn the midnight oil fella.

The gilded age had nothing to do with the period leading up to the Great Depression, try reading a book (or at least ten seconds googling).

Coil, with due respect, history’s tail is not only many-forked, but constant, connected, and neverending (for the time period discussed here, recommend Tuchman’s ‘The Proud Tower’ followed by her ‘The Guns of August’). An issue with our current entertainment-and-news broadcast-based zeitgeist is that we have become inured to believing life on the spacecraft, as on the information devices, is episodic, when its actually 24-7, century after century…

may we all find a better day.

There are large leakages in the circular flow of income pushing up inflation, crowding out, financial investment instead of real investment, etc. S ≠ I

Economist John O’Donnell said of the U.S. Golden Era in Economics: “increased money velocity financed about two-thirds of a growing GNP, while the increase in the actual quantity of money has finance only one-third.”

That makes sense since velocity went negative for the first time since the GD during the S&L crisis.

Wolf,

A little off subject, albeit related to inflation, but I would be interested in your frank views on the 25% Canadian and Mexican tariffs. Unless I just missed it, you seem to be avoiding the bull in the china closet. Aren’t tariffs likely to be the new inflation story?And isn’t the gross breach of our international treaties likely to create business uncertainties and reduce profits? Isn’t that the biggest business story? Why is Wolfstreet silent on this story?

“Unless I just missed it, you seem to be avoiding the bull in the china closet.”

yes, you missed it. Read my comments in this thread about tariffs, not far above your comment. Then read this article and my comments to get the whole treatment:

https://wolfstreet.com/2025/01/13/some-basics-about-u-s-tariffs-and-what-trumps-new-economic-team-said-about-tariffs/

It sounds like you are a fan of tariffs, cool, and you are correct, the Trump 1st term tariffs did not produce Inflation but it also did not impact our economy much in other areas. Trump tariffs part 2 will be much larger and more global. I guess we will see how this all works out but I don’t have much confidence. Maybe Trump wants to bring back ‘fortress America’, but it most like will drive other countries to cozy up to China. There are always other countries to buy from in a global economy.

Oldguy,

I’m a fan of fixing what’s wrong with America. Two top wrongs are the twin deficits: the huge trade deficit and the huge budget deficit. The trade deficit was caused by one-sided globalization, driven by Corporate America. Tariffs might hurt stocks because they’re direct tax on profit margins, and 2018 did show that, and was a bad year for stocks. But so what. The trade deficit needs to be fixed, production needs to grow in the US. The budget deficit also needs to get fixed, and the US needs to collect more in revenues to do that (in addition to cutting spending), and tariffs are the best place to go for revenues. Just as simple as that.

One also has to take a stern hard look at the services the US provides to other countries in exchange for providing our consumers to purchase said other countries goods.

For example if we agree buy 10 million in maple syrup from Canada then cananda could agree to purchase 10 million in cloud services from Amazon.

Both countries benefit because our citizens are being employed to produce said goods or services.

You cannot just look at the goods only, it’s out of context.

I am sympathetic to Wolf’s view on tariffs, especially the extent to which they are designed to support strategically important productive sectors in the economy (as opposed to the rent seeking sectors) — if you are interested in the historical perspective on the early history of US tariffs you should seek out Michael Hudson’s “ America’s Protectionist Takeoff 1815-1914”

Wolf I am looking forward to getting myself a mail order bride from Canada after their economy falls apart like my father in law did from Russia in the 90s

Canada’s biggest problem is that their housing sector in the broadest sense dominates the economy. Build housing, sell housing, and then trade housing amongst each other to drive up prices, including for money-laundering purposes, then get rich off those higher prices, leverage those higher prices, and spend some of the borrowed money, that’s the dominant part of the Canadian economy. It’s ridiculous. The government needs to address that, it needs to let housing crash, and create an environment that encourages smart and ambitious people to start companies that create employment and economic activity that drives up wages, and therefor consumption, etc.

The other economic activity that is big in Canada is natural resources. That’s great, but that’s a shaky foundation for an economy.

I agree with your analysis. However I wouldn’t say resources are a shaky foundation. Russia managed to parlay natural wealth into industrial capacity. Maybe the Canadians can too. Probably not though.

Russia’s ruble collapsed against the USD since forever, and it has double digit inflation. Not a great model for Canada.

Howdy Lone Wolf. Thanks for the education on Tariffs……..

Howdy Dumb Idiot. HEE HEE. What magazine has those mail order thingys????? Any shipping costs or return fees?

I didn’t know Wolf was a high tariff man. I am open minded about other views, but what exactly is unfair about Canada’s trade policy vs. the US? We have a treaty, i.e., a binding agreement not to do this. We are breaching that agreement. That something totalitarian states do, but it is unAmerican in my view. We honor our treaties. Trump signed this last one himself. How are our allies going to trust us. The answer is they already don’t.

As for your claims of unfair trade practices, the basis asserted here is fentanyl smuggling, and it isn’t some unfair trade practice, albeit the Canadians may not be saints, and give some government subsidies, at least I think that has been the claim about lumber. If it is about unfair trade why are we tariffing the Chinese 10% and our closest allies 25%? Isn’t the claim that the fentanyl is made in China not Canada?

As for raising tax revenue, it is just a regressive sales tax.

I think Wolf needs to think a little harder about the tariff issues. It isn’t going to resolve our budget issues. And it will push us into stagflation, then recession.

We are rapidly descending into chaos and failed government. It won’t be long until even the market takes notice.

“what exactly is unfair about Canada’s trade policy vs. the US?”

That’s an irrelevant – nay, stupid – question. Tariffs are NOT punishment for another country. That why you people don’t get it. I’ll repeat for the 1,000th time:

Tariffs have two purposes:

1. raising revenues by taxing the gross profit margins of importers , namely Corporate America and foreign producers, which is the best possible way. Last time they were not able to pass it on, because they were already charging the maximum price, which is what companies always do, and some tried to raise prices, and their sales plunged, and then they rolled back those price increases to revive their sales, which is why inflation was and remained below the Fed’s target. Corporate America ate those tariffs in their gross profit margin. If you don’t understand this, you don’t understand anything about tariffs. Calling tariffs a “regressive sales tax” is stupid bullshit and anti-tariff propaganda for Corporate America.

2. Changing the math in favor of local production. Local production makes a huge difference because it creates secondary and tertiary activity, all three of them create jobs, and all those new jobs are bringing in tax revenues.

You people need to make an effort to understand this. Your whole entire comment is BS. I’m so tired of this anti-tariff bullshit.

Dan,

“We are breaching that agreement. That something totalitarian states do, but it is unAmerican in my view.”

To the contrary, America has a long and storied history of violating and breaking treaties. Hundreds of them. Native Americans have long been on the receiving end of America’s propensity to break treaties. Breaking treaties has nothing to do with totalitarianism, and everything to do with the power dynamic between the parties. I don’t like it, but that’s how it’s been historically.

Dan

Why only 10% on china?

Go back and read carefully, and you will get a clue

as to his plans for the de minimis exemption.