Those yields look too low for what’s coming at the bond market: The next wave of Inflation and a Fed that’s comfortable with 3%+ core PCE inflation.

By Wolf Richter for WOLF STREET.

The US government sold $620 billion of Treasury securities this week, in nine auctions. Of these auction sales, $480 billion were Treasury bills, with maturities from 4 weeks to 52 weeks, most of them to replace maturing T-bills. And $140 billion were 3-year, 10-year, and 30-year Treasury securities.

The Treasury Department reduced the size of three T-bill auctions (4-week, 6-week, 8-week) this week by a total of $55 billion compared to the same week in March and by $65 billion compared to the same week in February, as large amounts of tax receipts are flowing into the government’s checking account in April around Tax Day, including from quarterly estimated taxes for Q1 and from capital gains taxes for 2025.

| Type | Auction date | Billion $ | Auction yield |

| Bills 4-week | Apr-09 | 81 | 3.560% |

| Bills 6-week | Apr-07 | 75 | 3.615% |

| Bills 8-week | Apr-09 | 76 | 3.575% |

| Bills 13-week | Apr-06 | 96 | 3.635% |

| Bills 17-week | Apr-08 | 70 | 3.600% |

| Bills 26-week | Apr-06 | 83 | 3.615% |

| Bills | 480 |

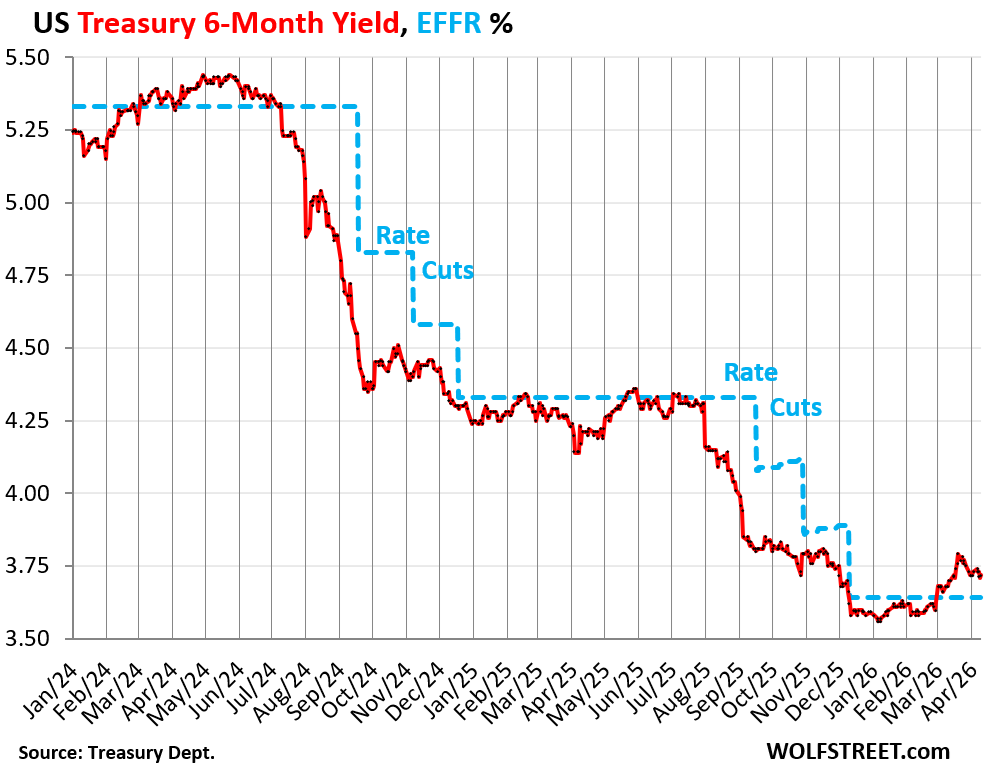

At the 26-week Treasury auction this week, the yield rose to 3.615%, 8 basis points higher than last week, and also 8 basis points higher than the same week in March. This is the “high rate.” When calculated like note or bond yields, it corresponds to an “investment rate” of 3.73%.

In the secondary market on April 6, the day of the auction, the 6-month Treasury yield traded between 3.72% and 3.75%.

On Friday, the 3-month Treasury yield closed at 3.71%, roughly unchanged from a week ago, and solidly above the Effective Federal Funds Rate (EFFR) which the Fed targets with its policy rates (blue line).

The 6-month yield had risen above the EFFR at the beginning of March when the war in Iran began, indicating that the market began to see a chance of a rate hike in its 6-month window.

Of those $620 billion in auction sales this week, $140 billion were Treasury notes and bonds.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| Notes 3-year | Apr-07 | 68 | 3.897% |

| Notes 10-year | Apr-08 | 46 | 4.282% |

| Bonds 30-year | Apr-09 | 26 | 4.876% |

| Notes & bonds | 140 |

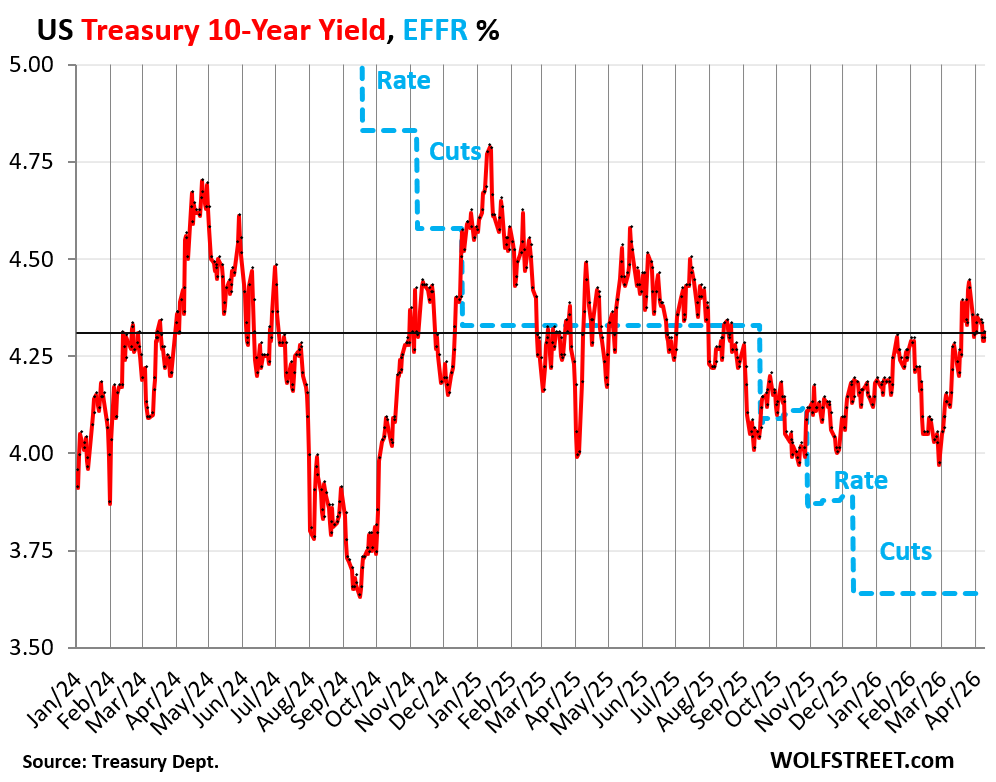

The 10-year Treasury note sold at the auction on Wednesday at a yield of 4.282%, up by 6 basis points from the auction last month.

In the secondary market on Friday, the 10-year Treasury yield closed at 4.32%. Higher bond yields in the market mean lower bond prices for existing holders.

Longer-term yields are determined by the yo-yo of the bond market and reflect the bond market’s views of the future – especially the path of inflation and the tsunami of supply of Treasuries to fund the ballooning deficits.

10-year notes outstanding increased by $26 billion this week: The $46 billion of 10-year notes sold at the auction this week at 4.282% and maturing in February 2036, replaced $20 billion in 10-year notes sold at auction in April 2016 at 1.765%, that had matured in February 2026. So with this week’s auction, the total amount of 10-year notes outstanding rose by $26 billion.

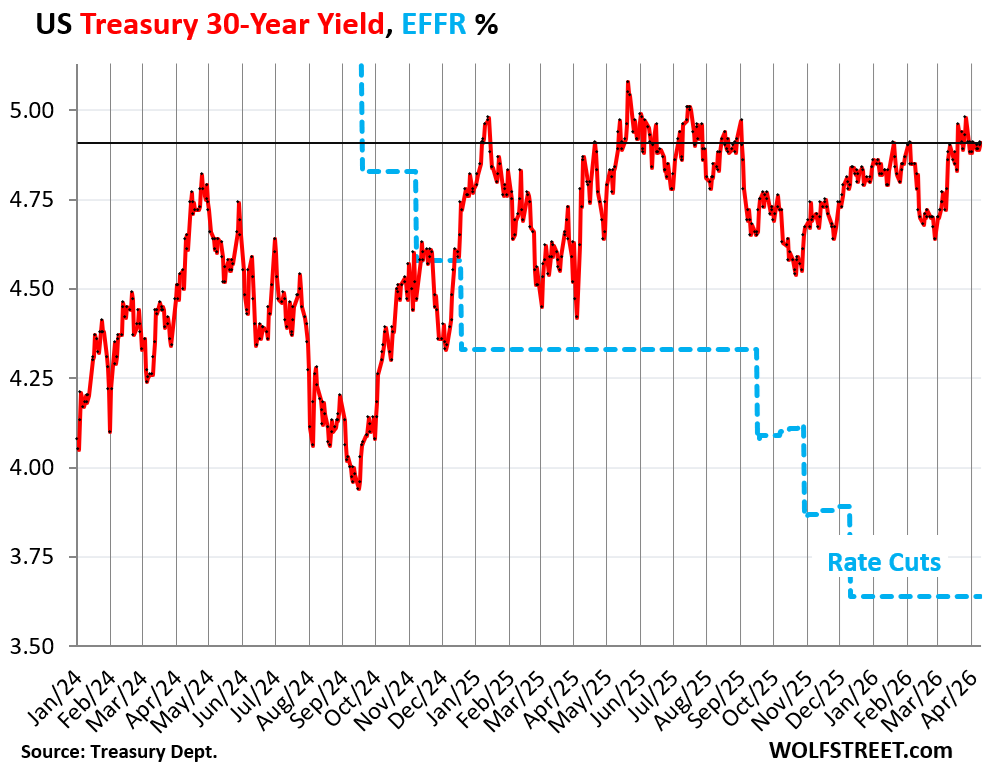

The 30-year Treasury bond sold at the auction on Thursday at a yield of 4.876%, a hair higher than a month ago.

In the secondary market, the 30-year yield closed on Friday at 4.91%. It has been on the verge of 5%, and sometimes over 5%, for over a year.

This end of the Treasury market completely blew off the Fed’s rate cuts:

Not with a 10-foot pole at current yields.

At this yield, with this potential path of inflation, with this Fed, and this path of the debt, 10-year paper looks very unappetizing to this observer, and 30-year paper looks even worse.

Inflation, as measured by the Fed-favored core PCE price index has been rising for months and in January and February was at around 3.0%, and that was before the energy price spike.

The Fed appears to be comfortable with 3% inflation, and seems not overly frazzled about inflation going over 3%, and that was before the energy price shock hit, and now it’s going to “look through” the energy price shock for a while and let inflation do its thing.

And maybe that’s the only way the debt – which is on an “unsustainable path,” as Powell likes to say – can be dealt with given the hopelessly Drunken Sailors in Washington: Let it run hot.

Higher inflation, such as in the 3% to 5% range, and higher nominal economic growth beget higher tax receipts, which make the interest payments easier to deal with, and we’re already seeing some of those effects, and years of higher inflation reduce the burden of the existing securities when they mature because they get paid off with devalued dollars.

But it’s a horror show for bondholders if they buy those securities when the yields are too low and don’t sufficiently compensate them for the devaluation and the other risks they’re taking.

That 2% is still the Fed’s official inflation target, but inflation has been above 2% for over five years. The low point was in April 2025, when the core PCE price index was up 2.6%. Even as the core PCE price index was accelerating in the fall toward 3%, the Fed cut its policy rates three times – an indication that it feels comfortable with 3%-plus.

That leaves no wriggle room for buyers of 10-year Treasures at a yield just 1.3% higher than pre-energy-price-spike core inflation rates. The energy price spike could drive inflation substantially higher, and the Fed will bravely “look through it” for a while, which is a bad omen for the next 10 years for investors that bought 10-year paper at a 4.3% yield.

In 2020, investors bought 10-year Treasury notes at auctions at yields below 1%: At the March 2020 auction at 0.85%; at the April 2020 auction at 0.78%, at the May 2020 auction at 0.70%, at the June 2020 auction at 0.83%; at the July 2020 auction at 0.65%; at the August 2020 auction at 0.67%… They were hoping that yields would fall into the negative after their purchase. There was talk of that.

They got their faces ripped off when inflation began to soar starting in mid-2020. The core PCE price index went from the low point of 1.0% in June 2020 to 1.5% in December 2020, to 3.9% in June 2021, and blew past 5% in December 2021 when the Fed was still near-0% and was still doing QE. The Fed didn’t end QE until early 2022, and the first timid rate hike came in March 2022.

Some of those investors that had bought those misbegotten 10-year notes in 2020 were the banks that had believed the Fed’s “forward guidance” of no rate hikes for a long time, and that then collapsed in the spring of 2023 because the market values for their securities had plunged as yields had soared amid inflation and the Fed’s steep rate hikes and QE.

Inflation never came back down to 2%, and the next wave of inflation has started, and the Fed will let it run hot. And maybe that’s the only way to manage the path of the debt, given the Drunken Sailors in Washington.

But for potential buyers of long-term securities, these are treacherous times. Inflation destroys the purchasing power of bonds; a higher yield is supposed to compensate investors for the loss of purchasing power, plus for the other risks and costs they’re taking on. And to this observer, the current 10-year yield is too low for this environment; it’s not compensating investors nearly enough to take those risks over the next 10 years.

In case you missed it: US Government Interest Payments, Tax Receipts, Average Interest Rate on the Debt, and Debt-to-GDP Ratio in Q4 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Please give color to the auction results ….especially the 10 year …bid to cover ratio, dealer takedown rates, and when issued tail…were these auctions weak, failing, etc???

“But for potential buyers of long-term securities, these are treacherous ” Wolf’s phrase.

as have been the gold standard of the dollar system the ten year the currency too the financial community that has determined that holding long term Federal Reserve bonds was the worst investment that a yokel could have made.

Yellow

“The Fed cut its policy rates three times…” The speculation on the web is that if the Straight of Homuz is opened that the Federal Reserve will lower interest rates; Oman is getting in on that action as well coordinating with the Iranians. The Houthis are threatening to close the Bab el-Mandeb Straight, so following the logic, the Federal Reserve again could not lower interest rates. Objectively our inflation is in the hands of Oman, Iran, and the Houthi rebels of Yemen.

“Speculation on the internet” is nearly always wrong; it’s designed to manipulate to move markets their way briefly.

The best available opinion of what the Fed might do with short-term policy rates is the short-term Treasury market.

Visit “Whats going on with Shipping” youtube channel. Its the nearest thing all us nobodies have to actual data on whats happening with traffic through Hormuz. He has been posting pretty often over the weeks of the war. As of last night, almost no traffic.

A lot of ships have been sitting in the gulf for almost 6 weeks. Many may need several days to be ready to sail. The numbers could start to turn around pretty quickly…or not. Even if the bottle is uncorked in the next week, damage has already been done that will take months maybe years to play out.

Yeah, I like that channel “Sal Mercogliano”

Yeah I like that channel. According to him, the supply gap should be starting to arrive about now in the EU and US. It’s taken this long due to sailing times since the start of the war, so current prices reflect only anticipation of shortages, not any actual supply disruption. Inflation is well above target, consumer confidence just hit record low, the debt is about to pass $40 trillion, and the Fed looks like they’re going to go “transitory” again. All of this absolutely makes me want to go buy 30-year bonds.

Of course the Fed has always had a reason for why the economic environment appears so bleak too the average US citizen

The motor of the USA is the well being of it’s citizens

Medicare is great. It should be available to every citizen

Guess this higher GDP that’s coming with the 3%+ inflation will lead to a Roaring Twenties. That will end well, right?

As long as it doesn’t end up that people with some assets are forced to sell at depressed prices to those who already have lots of assets

The Roaring 20s came after a double recession (from WW1 and a large deflationary recession in 1920). The decade was actually deflationary: the dollar gained 10% in value over the entire decade.

The Great Depression was also deflationary, with the dollar gaining in value by 6% a year.

That time from 1920-1933 was the last time there was any significant deflation in the US.

Well wealthy people are about to lose 50 pct of the asset prices because affordability is a mathematical prediction that my AI model pointed out and suggested I should be pissed off about stuff

I still consider myself a novice in matters of finance. Most of what I have learned has come from this site. 2%, 4%, 6%… even 8% return isn’t enough for 10 or 30 years given the last 5-years of this inflation. No way. Just look at fuel for last 60-days.

I get the ‘cleanest shirt in the pile’ theory but maybe it’s time to go shirtless and get a little sun.

AGHM-

The concepts of a “bond ladder” and “rate-pegged maturity targets” might be useful tools to you.

“Bond ladder”, as the name implies, involves spreading your bond commitment over multiple maturities to protect you from BOTH rate increases and rate declines. As rates rise you’ll have some money coming due, but if/when rates fall, you’ll be happy you have some bond effectively locked in at yesterday’s prices. Nothing new here…

“Rate-pegged maturity targets” determines how far out along the yield curve you’re willing to stretch. E.g. in the current rate environment where you get into the high 3’s in the 3-4 year range, you maintain a 4 year ladder. If/when rates rise to 5% on 5 year bonds, you’d add a 5th year to your ladder. On the other hand, when rates drop in the market, shorten up your ladder. (Shrinking or stretching maturity range can be done very conservatively and cost effectively by making adjustments as your shortest maturities roll over.

To Wolf’s point (“ …the current 10-year yield is too low for this environment; it’s not compensating investors nearly enough to take those risks over the next 10 years.”), if rates were 10% on the 10 year treasury, the calculus would/should induce a re-think on committing a sliver to longer maturities. Same with every other maturity.

Simple and effective way to hedge the “yo-yo.” (Not meant to be a “trading” technique, in my opinion…) Keeps your income relatively stable, too.

Of course, this strategy get’s complicated by the broader asset allocation questions about portfolio allocation between stocks, bonds, cash, etc.

I’m turning to ETFs which pay dividends, I don’t see any value in t-bills anymore, like Wolf said, the reward is shit for the lockup you commit to.

Well one never knows

For most of us eating, housing, education, love along the way,

the last thing that money can buy is happiness

As you learn, grow and move from novice to experienced, always go back to your gut call and simple math; do not get caught up in nonsense. If you want to spend your intellectual energy in this area, then try to understand why today’s BUYERS of long >5 year treasuries are doing so. I cannot rationalize it.

I trust a free, open, deep, wide and accessible MARKET; thus I accept every transaction has both a seller and buyer. I just cannot phantom buying 5 year or more treasury today.

I am all ears to learn the analysis

My understanding is that 10 year bond rates reflect discount rate for valuing investments. If those 10 year bond rates go up I would think stock prices, real estate prices and maybe even metals prices will be under pressure.

Maybe that’s true, but why didn’t stock prices plummet when the 10 year rate tripled after 2022?

In theory, perhaps, but not in practice. The discount rate is a useful CONCEPT, but it is hard to determine. Why should the 10-year note be the discount rate? Particularly when it depends heavily on price-incencitive purchasers like the Fed, foreign central banks, and insurers and banks?

Higher inflation per se is a positive for large corporations that usually have pricing power. It is also great for the Wall Street since performance and bonuses are determined in nominal values. Inflation is bad for the stock market only when the Fed gets serious and engineers a recession to fight inflation or the government tightens fiscal policy. Such a scenario does not appear in the horizon.

To an extremely rough approximation that’s true, but it varies based on lots of factors and is often slow to readjust. The so-called Fed Model, in which investors choose between bonds and stocks based on expected yield (expected stock yield is reflected in price/earnings ratio) is roughly true over very long terms, but with substantial variations favoring either stocks or bonds over long periods of time (decade or more)

The 1970s called. They want their economy back.

Well that is an insightful comment that calls to mind an era.

A panoply of the visions accrued during a lifetime.

I’ve been reflecting on why the likes of the Bank of England routinely under-predicts inflation rates. Part of it is presumably a déformation professionnelle – they are full of economists who are likelier to trust a model than the powers of observation and reason.

But part of it is age – a youngster of forty or fifty will have no memory of the inflation of the 1970s, so his instincts are no help either.

Thanks for this Wolf, you voiced a thought I’ve had for a while now: 3% inflation is the new normal as far as the Fed is concerned.

I came of age in the ZIRP era and thus am still thinking through how best to invest and manage my personal finances during years of sustained high inflation.

Same. I am trying to learn how to be comfortable with debt. That includes house mortage with my current 3% rate and investing debt (I take a specific margin loan amount and invest it when sp500 goes down a certain level and pay it back in a specific time range).

It figures to me that I should hold the least amount of money paper as possible, and convert a sustainable level of interest debt (less than $150 a month) into assets.

Just an idea to share

I have been structuring my finances the same way, for the same reasons.

ZIRP was always an anomaly. 3% (give or take) inflation is pretty normal for non-recessionary years. What you learn to do in these years will serve you in good stead for most of your life. Good luck!

The long term inflation average since the Fed was created is 2.6%. The 2% target was invented in around 1990 (arbitrarily chosen; nothing magical or supported by research), and the average inflation rate since then is also 2.6%. At 2.6%, money loses pretty much half its value in a generation (30 years), slow enough to be manageable and fast enough to encourage people not to just sit on it.

There have been very few long term periods in which inflation has been below 2%: pretty much only 1950-1965 and 2010-2020. It’s rare and it seems to come in the aftermath of crises.

I suspect that 2% is meant as an aspirational target rather than a true long term average, and that any average between 2 and 3 is generally acceptable to the Fed. They announce 2 to try to keep it from rising much above 3. So you’re not going to see them panic about 3, but as soon as it edges up to 4, you’ll probably see some action.

I came of age during the Volker remedy to inflation which was that the cure for inflation is high interest rates.

There is an algorithm developed by a Fed employee that mathematically predicts the optimum interest rate too control inflation. Based on the model output one of the worst investments is long term government bonds

If the people that have control over such things wanted to squelch inflation they would raise interest ratea

This sounds like the Taylor rule, which currently says the Fed Funds Rate should be about 4.0, just a little higher than it is right now.

I don’t disagree with the author’s sour sentiment on long bonds, and yet I actually this week bought some 20yr at ~5% in my retirement account. Just a small allocation, but I figure the return should provide some “real” return, and as a bit of an insurance policy if demographics, AI or whatever do turn out to be disinflationary, I still have a portion of my portfolio yielding 5%.

I don’t know who to credit for it, but someone once said if you love everything in your portfolio then you are NOT diversified.

Don’t by bonds or other debt instruments. The US has only one choice to lower the debt…inflation.

It is clear that Powell and Yellen were on board with the large inflation impulse that was “engineered” with Covid. Powell seemed to have some level of “mercy” after the big inflation and attempted to put a lid on with higher rates. He seems like a decent sort and must know the real pain that has been inflicted on the lowe K.

Now we have Trump and crew. They want to supercharge the economy with hopes of reducing the deficit to GDP ratio. Other than votes, they seem less inclined to really get inflation down to below 2%.

I don’t know where all this will end, but more inflation stress on lower K is playing with fire.

re: “The US has only one choice to lower the debt…inflation.”

Tell that to Argentina.

Argentina issued debt in foreign currency (USD, EUR, YEN), so it could not use inflation to lighten the load because it doesn’t control those currencies, and it defaulted on those foreign-currency debts. But it has consistently destroyed its peso-debt through inflation and never defaulted on it.

The US doesn’t issue debt in foreign currency.

Great point Wolf

Mike R., you’re way more charitable to Powell than I would be. He might, on some level, be aware of the pain his inflation unleashes on much of the population, but I’m not sure he really cares. I think, in his mind, keeping unemployment low and corporate America and Wall Street doing well, is more important.

The Fed has a dual mandate: 1. protect the value of the dollar by keeping inflation low and 2. keep unemployment low under the Humphrey-Hawkins bill of 1978. The goals conflict with one another.

They conflict on some level, but the mandate is to find a balance.

Prioritizing 4% unemployment over getting inflation under control is not the right balance, in my opinion.

Inflation is great for debtors, and bad for debt-owners. I was hoping for a clean Adam Smith quote but got lost in the rambling before I could find one. There’s like a whole chapter on diluting currency through metallurgy. That dude won’t use one sentence when a dozen will do.

The Fed’s supposed to be the strict parent in this relationship, but right now it seems like everyone in Washington is trying to be the cool aunt. It’s going to be great until all us kids are heading to bed fully wired from sugar and destined for nightmares.

Also, long time reader first time poster. Thanks for the great articles, Wolf!

Only a couple of months before Warsh comes aboard. Interesting times.

The Fed is fine with inflation running hot.

The BLS is fine with skewing OER & healthcare expenses lower to give the “appearance of lower inflation”.

5 years above the 2% target tells you a lot about Powell’s “transitory” inflation theory.

Our societal leadership is not willing to tolerate recession or lower asset prices, so inflation is the only solution left.

If you look at the planned IPOs for SpaceX, OpenAI, and Anthropic, the only way out for those investors is to turn America’s pension plans and 401ks into bag holders. The recession is baked in, no way around it because the ROI math on AI doesn’t math. Everyone is trying to cash out before it hits. The price for not paying attention to what’s going to happen to the index funds is very high if you are within 10 years of retirement.

All good points. Indexing will likely never recover from what is coming.

I suddenly started getting calls from Fidelity—they’re worried I’m under-invested. The same thing happened in 2022. Looking for bagholders is my guess.

Sandy,

The ROI doesn’t currently work out when factoring the consumer market. I think the enterprise market will mature and grow. Obviously nobody really knows but that is my take. Anthropic latest release seems to be much more than hype although points out the dangers of AI more than the benefits imo.

Sam Altman has always been a relatively clueless used car salesman(no offense intended there) as that does seem likely as well as Meta AI being in trouble. Zuckerberg created a meh product that was popular and his only successes have been burning money and a few solid purchases (what’s app and Instagram)

I totally agree with you.

To add to my comment above, since the 2% target was invented in 1990, we have only been below it for 5 years out of 35. It has always been aspirational and not strict. It’s just meant to keep inflation in the 1-3 range.

numbers,

As the Fed uses Core PCE as the measure and target for inflation, note it was below 2% the entirety of 2009-2020.

Fair. During that period there was a lot of worry about deflation and many proposals to change the target or to consider the target to be cumulative (if you are below for a while then allow it to go above afterwards to compensate and vice versa)

High inflation will increase the homeless and help destroy the fabric of society. Inflation is the rich mans grift.

Already happening. Look how unhappy people are.

How so? People with money get to earn real (inflation- adjusted) interest on it. People without money pay real (inflation adjusted) interest to borrow. Positive real rates (high interest, low inflation) help rich people and hurt poor people. Negative real rates (low interest, high inflation) help poor people and hurt rich.

Feb 2026’s personal savings rate was an abysmal 4%. The latest gdp deflator was 3.7%. The latest 10-year constant maturity rate was 4.25%. Real interest rates are insufficient to attract a higher savings rate.

We need high real rates of interest for real investment.

Personal savings rate has been that low since 1999, and started to decline from it’s previous level of around 10% back in 1992.

@numbers: “since 99”

That helps explain the deceleration in R-gDp.

1. Please use the common term and spelling “real GDP.”

2. Real GDP slowed down in Q4 due to a historic collapse of federal government spending in Q4 due to the shutdown (but that spending was only delayed, it’s going out in Q1 and Q2, on top of the regular federal spending); and real GDP slowed due to the jump in inflation in GDP accounts that are not associated with consumers. Total GDP inflation was 3.7% annualized in Q4.

I think what he meant was that real GDP growth has averaged a bit lower since 1999 than before.

I’m not convinced lower savings rate is the explanation, but it’s an interesting coincidence.

It shure sounds that way, doesn’t it. But what if AI kills employment and we have no demand for goods and services? Then we would have a recession. If you had cash to spend, think of all the cheap assets you could buy. Cash can suddenly make you a king.

The bulk of the inflation is in the stock market, not in goods and services. As the Treasury essentially creates money by issuing more and more short-term bonds, those in the investing class continue to pour cash into the S&P 500. Meanwhile, the people in the bottom half of the income distribution are limited in what they can spend, lessening effective overall demand. While the spending power of the investing class is increasing, it will not add to inflation unless they sell stocks and spend the money.

“The bulk of the inflation is in the stock market, not in goods and services.”

seriously?? tell that to my insurances that have double or tripled…or food up over 20% in the past 5 years…etc

“food up over 20% in the past 5 years… ”

that’s a lot less than the CPI for food. You accused the CPI of lying in your other comment, but it seems you don’t know what the CPI actually says. You need to read my articles here. The CPI for food over the past 5 years is up by 31% 🤣 (not funny actually, but your comments are funny)

https://wolfstreet.com/2026/03/11/food-inflation-in-america/

A lot of the food price inflation is due to $100 billion a year in SNAP subsidies. The primary function of subsidies is to push up prices, despite whatever messages are spun about benevolence. Corporations lobby hard to make sure their products are covered by SNAP. If the subsidies weren’t there, prices would be much lower. The same argument applies to home prices and a lot of other things that a true free market government would not be manipulating.

JeffD,

My anecdotal observation is that SNAP eligible products are never on sale, supporting your points.

Question: What evidence might you have for “The primary function of subsidies is to push up prices, …” My interest in your viewpoint is genuine.

JeffD,

Upon reread, my question seems contradictory. Primary function implies intent. So really I’m asking if you are aware of anything documenting the original intent of the SNAP program. Just agricultural subsidy and/or public assistance?

“Government cheese originated in the early 1980s as a way to manage a massive surplus of dairy products purchased by the U.S. government through farm subsidy programs. To support struggling dairy farmers, the government bought vast amounts of milk, processing it into huge blocks of cheddar cheese and storing them, eventually distributing it during the 1980s recession.”

The origins of SNAP undoubtedly originated with agricultural subsidies, and grew from there. I don’t have proof, but I’m sure someone has done the investigative reporting. To me, it seems self evident that it started here, and morphed into something larger.

Certainly, the French decided early on to subsidize agriculture so they would never (simplifying here) be dependent on other countries for their national survival, and I have read an entire French book when I was younger on just that subject. The political nuances to that non-fiction story were facinating.

Food stamps were introduced in 1977. EBT was introduced in 1984.

“The Food Stamp Act of 1977 finally eliminated the food stamp purchase requirement, which mean poor families no longer needed to have cash up front to purchase food stamps.”

They don’t have to sell stocks and spend the money. They only have to feel emboldened to spend the money they already have without selling the stocks (the “wealth effect”) to drive inflation.

I personally never believed the Fed when they said that their inflation target was 2%.

First off, 2% inflation rates during a non-recessionary time are just a historical anomaly. I can’t think of any other 10-year period in American history when inflation was that low while the economy was growing (or even stagnant).

Secondly, there is a limit to what the Fed can do. Hard to push inflation down when the Legislative and Executive branches are running deficits so hot that the national debt is 20% higher than it was just three short years ago. There is no war or current natural disaster (COVID) that justifies such spending. At some point the Fed has to stop playing the “adult in the room” role and let the politicians start taking the blame for their actions.

What has the Federal Reserve done that is in any way incorrect?

Duh. How about ZIRP, QE, fives years of above target inflation.

The Federal Reserve has been doing QT (Quantitative Tightening) for around 3 years during which time (for whatever good that may do)( of shrinking its balance sheet. The Federal Reserve has no control whatsoever as to what any vendor charges for its goods and/or services.

Exist?

Prevent the panics and depressions that happened pretty much every 5-10 years before it existed?

I think you can call 1980, 2000, 2008 and Covid “panics”

I sincerely doubt they call to the panics of 1871, 1882, 1893, 1896, and 1907, some of which were said to rival the great depression.

Waiono: I don’t think you can call either 1980 or 2000 a “Panic”… they were both recessions that had a different flavor (“Stagflation” in the late 1970s and 1980… and the “Internet Bust” of 2000-2001). Moreover it was the Fed that largely got us out of those situations (although the income tax cuts that came AFTER the Fed started fixing Monetary policy… both times… no doubt helped).

Same for 2008 and COVID. While SOME Fed policies contributed to the bank failures there is little doubt that the Fed prevented the “Great Recession” from becoming the “Great Depression II”… the economy certainly wasn’t saved by lamebrained ideas like “Cash for Clunkers” that came out of the Executive and Legislative branches of government.

COVID was obviously a worldwide catastrophe that central banks all over the globe responded to in much the same way as the Fed… funneling money into the economy NOW and worry about how to pay for it later. Obviously the Fed was late to the party in stopping “Transitional Inflation” whatever that is… but (because $2.1 TRILLION in added spending in 2021 wasn’t enough) Biden’s $700 billion “Inflation Reduction Act” came in 2022 AFTER the Fed had increased its Fed Funds Rate FOUR TIMES already that year. The FFR was literally TEN TIMES HIGHER than at the start of the year and the Fed was just getting started.

Ooohh…ooohhh… not to be outdone Team Trump passed a “One Beautiful Bill Act” that added ANOTHER $2.8 trillion to the Federal Debt even as the Fed was still trying to wrangle inflation to the ground.

So yeah… considering that the BOTH parties in the elected branches of government not only came up with those idiotic names for their bills but also managed to toss $5 trillion dollars on top of an inflationary economy… I am going to stick with my argument that the Fed has been forced to play the role of “adult in the room” for almost two decades now… AND that they should STOP doing so.

Rents are falling. Austin is down 6% YOY. Housing prices have no chance of increasing on the whole while rents are falling. Obviously inflation around 3% is painful and grating but I don’t think the Fed has officially changed the target yet. The moment they do the countdown to a 4% target begins and they know it. We may finally be on the tail end of the “pandemic inflation” – now with an added shock of an unforseen and unnecessary energy price spike. But actual demand for most things is flat and without buyers prices don’t go up. The US is likely, thankfully, now in a period of low or maybe negative population growth and that will allow everything to settle down and catch up. Housing construction, office building realignment, energy distribution. This actually feels more like the calm after a storm than the calm before. The markets are far overvalued but a 2000-2003 type crash is survivable. The top 10% own 85% of all equities, they’ll be fine if prices get cut in half.

The 30-year is for pensions, insurance companies and State governments, not individuals. The 10 year nearing 4.5% feels like a good place to safely park cash and keep ahead of 2.5-3.5% inflation.

inflation is nowhere near 2.5-3.5% …despite what we’re told.

Our personal inflation is right in that range. Some prices go up a lot, other prices go down, some don’t move for years, and then jump, etc. It’s not easy to get a clear picture. If you just focus on the stuff that goes up, and ignore the stuff that doesn’t move or goes down, then you’re lying to yourself, but it sure feels good.

I noticed during the GFC in 2008 that it seemed as if large corporations all had admitted losses in the $3 billion range, as if that was the magic number to admit a little something, but not to worry anybody.

The always 3% inflation gambit seems similar~

It’s possible there is too much liquidity in the system that causes everything (stocks, bonds, and RE) to be overvalued. If so, there might not be any increase in long rates until liquidity is removed.

Long rates might be higher by now if the Fed had continued QT.

That’s a product of an ample reserves system framework. Thus, there are more reserves than needed for day-to-day liquidity needs. That permits the FED to control its administered rates. The US is the only central bank that uses “supply driven” reserves vs. “demand driven” liquidity.

If 10 year isn’t a good deal, what about TIPS? Real yield for those appears to be 2.6%…am I missing something?

You’re not missing anything.

But beware of the unusual tax consequences of TIPS. you will get a 1099 for the inflation protection every year, but you will not get paid the inflation protection until the TIPS matures, so there is some negative cash flow here until maturity. You will also get a 1099 for the interest, but you get paid the interest, so that’s normal. Keeping TIPS in a tax-deferred account (IRA, SEP, 401k etc.) avoids those tax issues.

It’s hard to say which is worse — Treasury bond yields being too low or credit spreads being too tight — given the backdrop of economic instability in the real world. Maybe Warsh is exactly what’s needed to trim the Fed’s balance sheet.

Spreads being too tight is worse as it adds unpaid credit risk to the unpaid inflation risk of Treasuries. Credit spreads being too tight is also an economic issue — it’s one of the factors that keeps stimulating this economy and contributes to inflation and some of the cockroaches out there in private credit and private equity. For investors it means that they’re not getting paid enough for the credit risks involved in holding corporate bonds or loans further up the risk spectrum, such as BB-rated junk bonds.

I wish there was a movement to call out Powell and FED about their commitment to 2% target. He is just lying to Americans about it entire time after Pandemic. Accept its 3% so people can adjust their expectation.

The paid Wall St. Media at FOMC meeting pressers and other events, always asking when will you cut rates. Powell conveniently looking through Short term inflation risks and focus on short term Labor market zig-zags.

The difference between 2 and 3% is undetectable to most people. Who can tell if their $10 lunch went to $10.20 or $10.30?

Even after 10 years, it’s the difference between $12.20 and $13.40. And who is paying that close attention after 10 whole years.

That’s very peculiar way to look at inflation number and put in real life.

2% inflation doesnt mean Each price goes up in 2%. Food inflation has been been very high in last 5 years. With productivity gains some prices will come down.

In a compound effect. 2% or 3% difference is truly seen as time passes by.

In short run, I can argue even 4% inflation is fine then.

I agree to your point that how many are paying attention? Well only time will tell if Americans are truly ok with high inflation. Nov is not far away.

Food inflation has averaged 4.5% since the pandemic. Things that cost $10 in early 2020 cost about $13 now (yes, that’s on average with considerable variation; that only makes it harder for people to track).

It’s not hard to argue that 5% vs 2.5% is noticable.

Inflation during the Biden administration (2021–2025) was marked by a sharp, post-pandemic acceleration, peaking at a 40-year high in 2022 before gradually moderating. Cumulative inflation over his four-year term reached approximately 20%–21%, resulting in a significant increase in the cost of living for consumers. (U Boys have gotten yourselves in a World of Shit) Just the latest man made crisis, orchestrated by Uncle Sam. You have to go back to 2019 for any sanity regarding inflation. What ever Happens in November midterms, the $40 trillion debt will still need to be serviced. I’m okay with 5.0 to 5.5 on 10 year treasury. S&P 500 drops to 3500. The private credit market can’t be swept under the rung forever. It crazy how much political and religious hate brews around the world, just 2 realize we all tied to the same fate. Oh well, my final destination is the great state of Wyoming for my tax free retirement. I’m sure Colorado will start the billionaire and millionaire socialist tax soon, especially since legalization of prostitution was just voted down in Denver.

numbers,

I limit my inflation assessment to how much 2 tacos at Jack in the Box cost and extrapolate. It has gone from 2 for .99 a few years ago to 2 for 1.69. Crazy times.

They had to make some changes to stay in business. Look at their balance sheet.

Burger chains are losing business given the high price of beef. Noodle and chicken places are doing better.

Fast food inflation is actually pretty crazy high. But that’s mostly a combination of much higher labor costs and the fact that food that isn’t total crap costs money.

Five Guys burger prices have more than doubled in the last 15 years, an inflation rate of around 6% per year, more than double the overall inflation rate.

My theory for the Iran war has nothing to do with the Hormuz access or nuclear weapons….its simply to drive inflation higher. We are so screwed.

Lol. Well that holds up until it brings in a global recession,/depression then we can get back in the ZIRP train.

It’s sector rotation for Wall St. and the stock market.

Real Estate booms, autos boom, insurance booms, big pharma booms, MIC and oil are having their turn now.

peter thomas,

My theory is that the war was an easy way to recapture the news cycle. I see your theory as the price we all (mostly) will pay. I agree the current trajectory is poor.

Wolf, in an article like this, it might also be useful to show a graph of real, not just nominal 10-year yields (i.e. three lines… 10 year nominal yield, 10-year yield minus core PCE and 10 year yield minus CPI-U).

When OPEC embargoed oil in the 1970s they plowed their surplus profits into the US. In particular into US banks which used that source of funding to increase loans to the private sector.

That’s not going to happen this time around. What’s going to happen this time around is no different than the economy being drained by increased healthcare costs. Just increase that a magnitude of order.

That’s funny. You’re still stuck in 2005. You missed a huge development: Fracking. the US has become the largest oil producer in the world, and huge EXPORTER of crude oil and petroleum products (such as gasoline, diesel, and jet fuel), and has a TRADE SURPLUS in crude oil and petroleum products; and it has become the largest natural gas producer in the world, and the biggest exporter of LNG in the world, and has a huge trade surplus in natural gas. High energy prices cause that entire sector in the US to boom. Money that people pay at the pump STAYS IN THE US. And high energy prices REDUCE the overall trade deficit for the US.

There are a gazillion articles about this on WOLF STREET, including most recently:

https://wolfstreet.com/2026/03/03/oil-jumps-but-its-not-the-1970s-anymore-us-crude-oil-production-hits-record-net-exports-soar-imports-decline-further/

https://wolfstreet.com/2026/03/02/drill-baby-drill-for-20-years-us-natural-gas-production-jumps-to-record-exports-via-lng-pipeline-spike-to-record-in-2025/

Would love to know why you think investors are willing to accept current 10 year note rates……with the threat of greater inflation looming on the horizon.

Disagree in the short term …Those charts are saying either rates come down at least 50 bips without warranting additional Fed cuts or the Fed needs to start raising rates.

Since the Fed isn’t gonna raise…