The spike of the “non-traditional reserve currencies.”

By Wolf Richter for WOLF STREET.

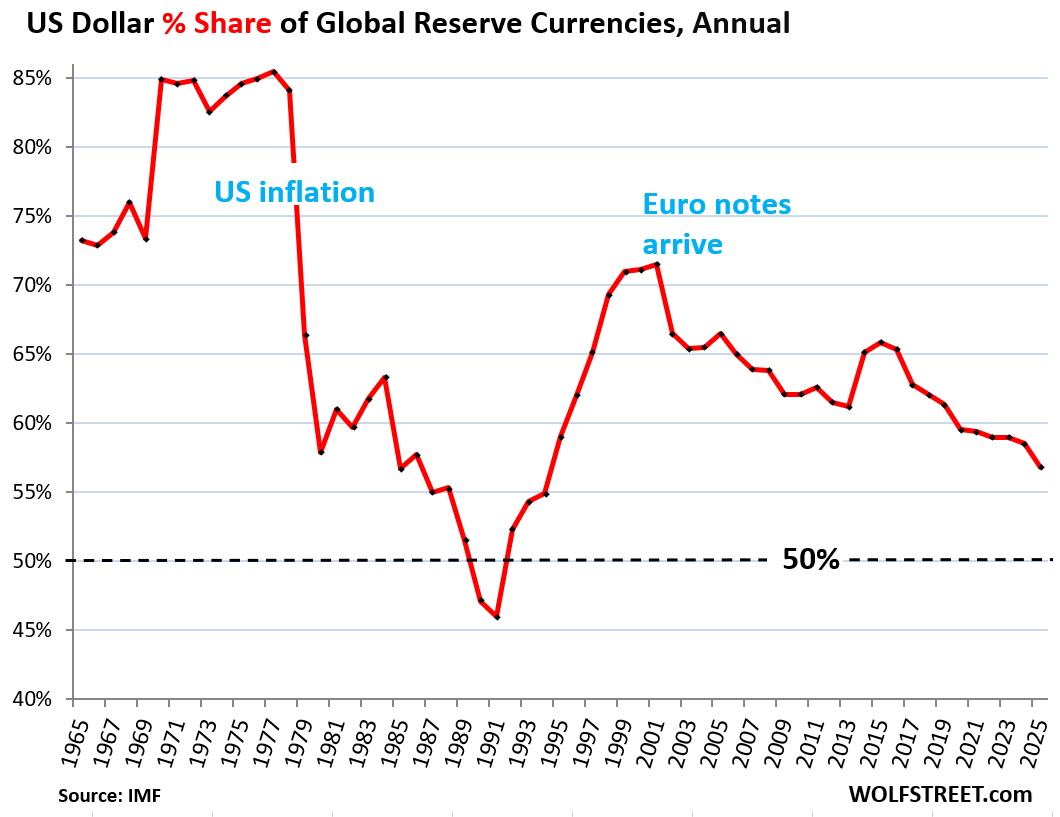

Foreign central banks have not been dumping US-dollar-denominated assets. But they’ve been loading up on assets in other currencies, and their total holdings of foreign exchange reserves have ballooned, while their USD-assets have remained nearly flat for over 10 years. So the share of USD-denominated exchange reserves dropped to 56.8% of total foreign exchange reserves in Q4, the lowest since 1994, according to the IMF’s data on Currency Composition of Official Foreign Exchange Reserves, released on Friday.

It has been zigzagging down toward the 50% line for years. It does have consequences. And it has been there before.

USD-denominated foreign exchange reserves are US securities held by central banks other than the Fed. They include US Treasury securities, US mortgage-backed securities (MBS), US agency securities, US corporate bonds, and other USD-denominated assets.

After a long plunge from a peak share in 1977, the dollar’s share broke through the 50%-line in 1990 and dropped further in 1991. This period from the mid-1970s through 1991 was accompanied by waves of sky-high inflation and interest rates, four recessions, including the nasty Double-Dip recession, and high unemployment. And other central banks lost confidence in the US dollar.

But then the economy picked up, inflation calmed, the Dotcom Bubble began to perform miracles on a daily basis, confidence returned, and USD denominated assets became desirable again.

Enter the euro. European politicians were talking about “parity” with the dollar until the Euro Debt Crisis began in 2009. Since then, the euro lost share and then stalled, as central banks diversified into other currencies, and since 2021, into dozens of smaller “non-traditional reserve currencies,” as the IMF calls them. Throughout, the dollar’s share zigzagged down toward the 50% line.

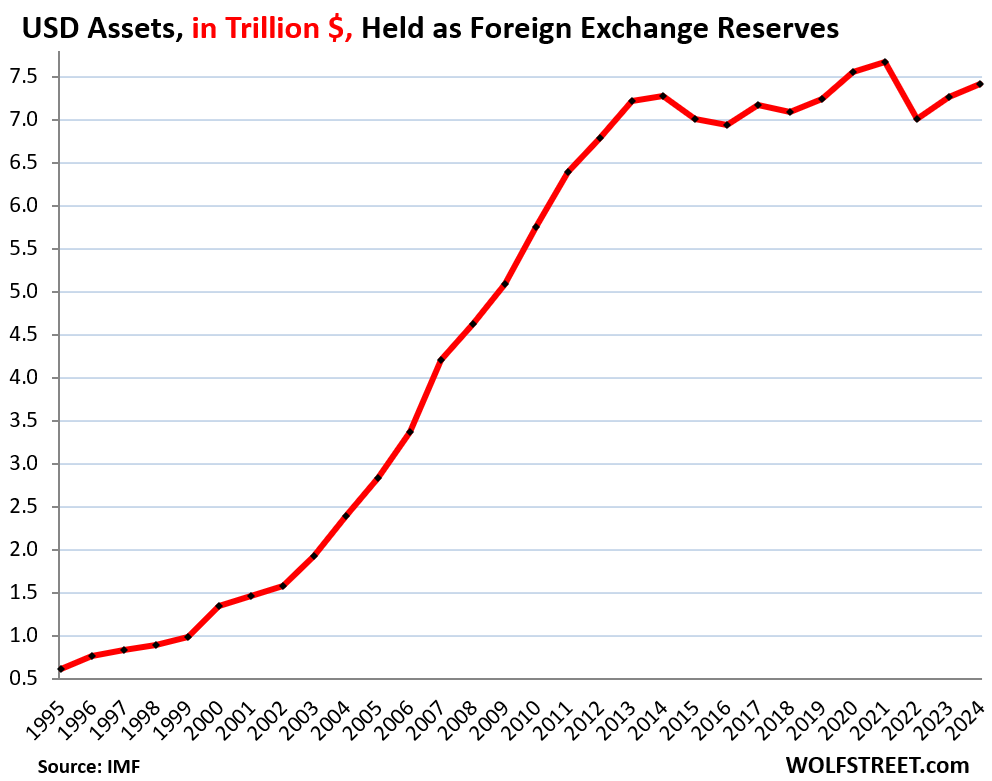

But central banks didn’t dump USD securities.

Since 2013, foreign central banks have roughly maintained their holdings of USD-denominated assets. In Q4 2025, their holdings of $7.46 trillion of US securities were up just a hair from 2014, but below 2020 and 2021.

What has caused the share of USD assets to decline over these years was the surge of assets denominated in dozens of other smaller currencies.

Why this matters: the “twin deficits.”

When foreign central banks buy US Treasury securities and other US securities, they in essence provide some of the funding for the huge twin deficits the US has: the trade deficit and the federal budget deficit. Being the top dog in terms of securities that other central banks buy – having the dominant reserve currency – has enabled the US to run those twin deficits for decades.

This path is obviously not permanently sustainable. And the “twin deficits” need to be brought down substantially before something goes off the rails, such as a surge of inflation and much higher bond yields, and all the issues that come with it.

Foreign exchange reserves by currency.

Central banks’ combined holdings of foreign exchange reserves in all currencies, and expressed in USD, rose to $13.14 trillion in Q3.

Excluded are any central bank’s assets denominated in its own currency, such as the Fed’s Treasury securities or the ECB’s euro-denominated securities.

Top holdings, expressed in USD:

- USD assets: $7.46 trillion

- Euro assets (EUR): $2.66 trillion

- Yen assets (YEN): $0.76 trillion

- British pound assets (GBP): $0.58 trillion

- Canadian dollar assets (CAD): $0.33 trillion

- Australian dollar assets (AUD): $0.27 trillion

- Chinese renminbi (RMB) assets: $0.26 trillion

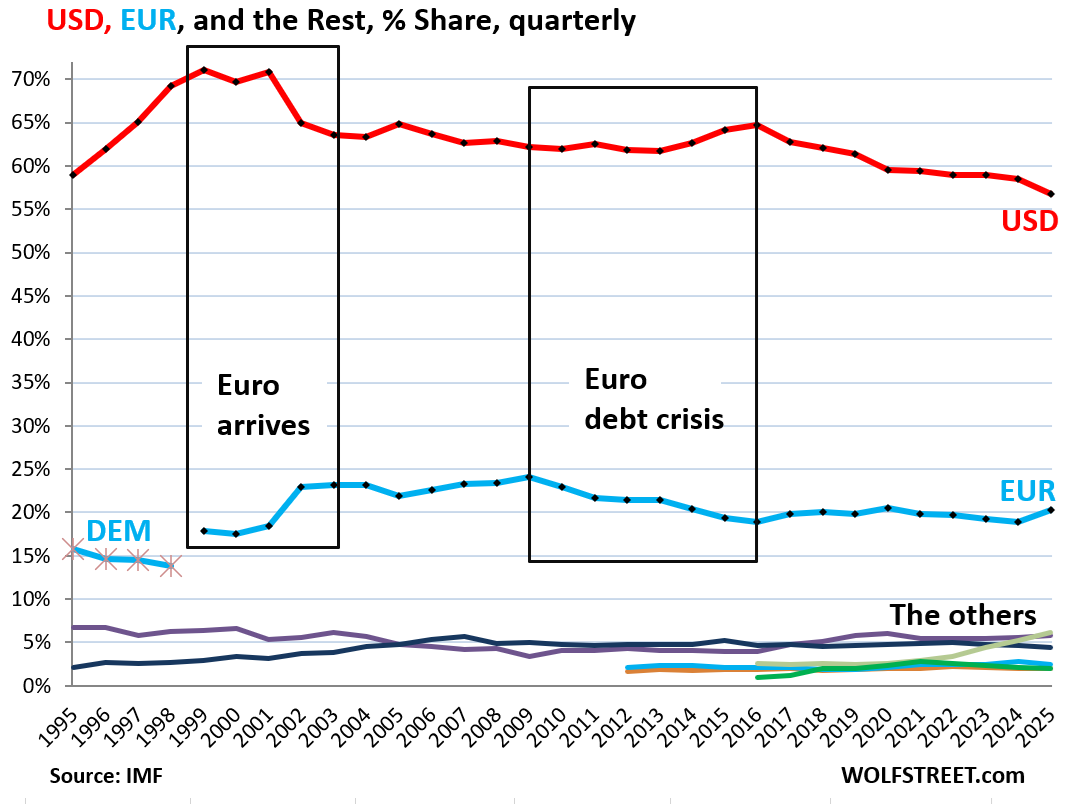

The euro’s share has been around 20% for the past 10 years. Just before the Euro Debt Crisis, it had risen to nearly 25%.

Note the blue “DEM” on the left – that’s the Deutsche mark with a share of about 15% in the mid-1990s. It became the dominant founding currency of the euro.

The rest of the reserve currencies are clustered at the bottom of the chart. But that’s where the action is (more in a moment).

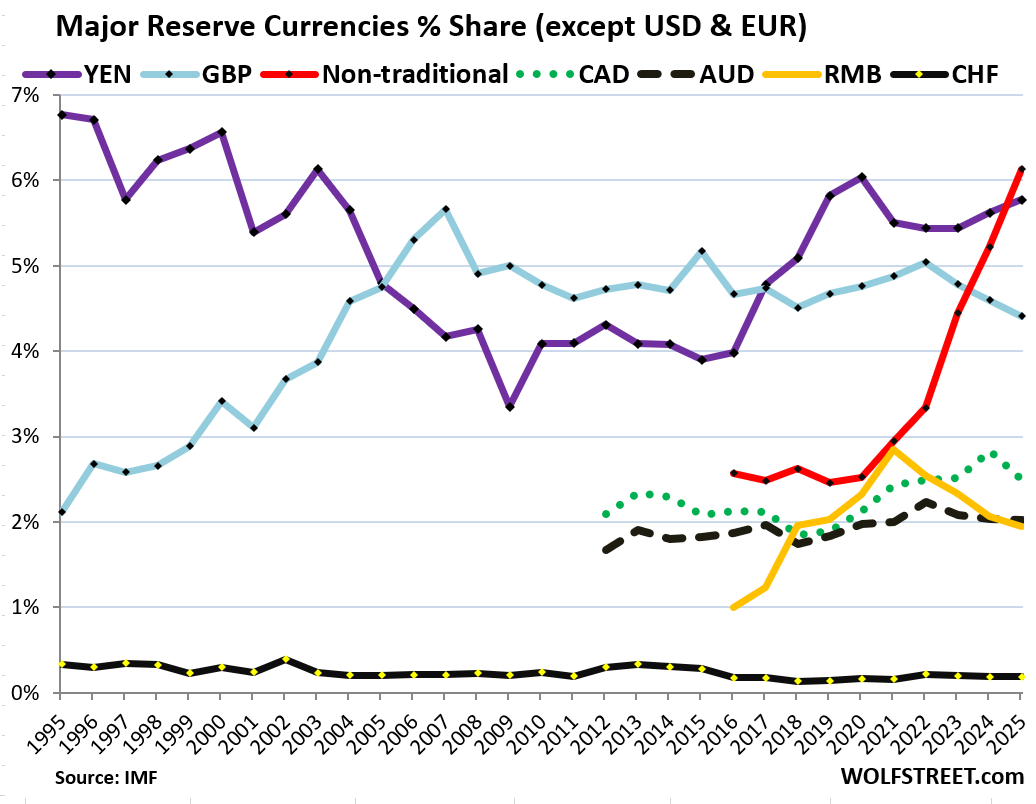

The spike of the “non-traditional” reserve currencies.

The chart below magnifies the cluster of lines in the chart above.

The soaring red line represents dozens of “other currencies” – other than the ones the IMF specifically names here. These dozens of smaller currencies are what the IMF calls the “nontraditional reserve currencies.” Each has a minuscule share, but their combined share has more than doubled since 2021 and hit 6.1%, surpassing the yen.

These “non-traditional” currencies are where much of the diversification away from the USD has occurred.

The share of the RMB (yellow) ticked up to 2.0%, after declining since Q1 2022. China has the second-largest economy in the world, and is hugely interwoven in international trade. But its RMB-denominated assets are not sought-after by other central banks, amid ongoing capital controls, convertibility issues, and other issues.

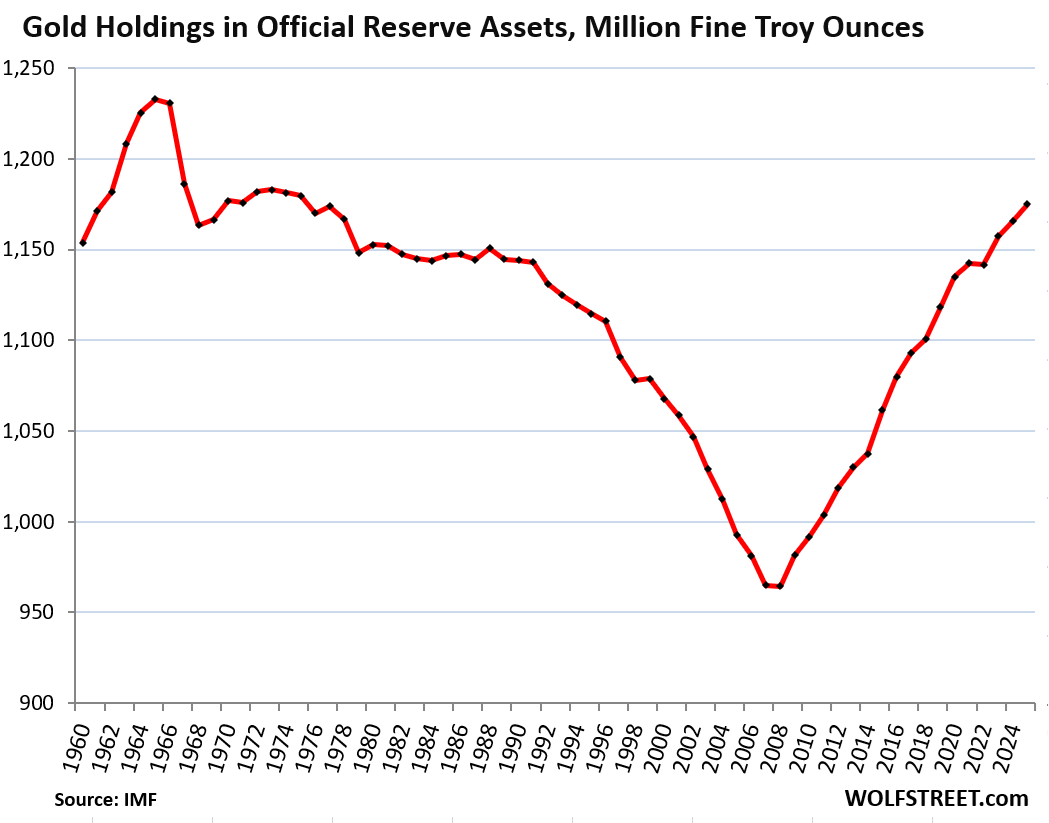

Gold, the non-currency diversification.

Gold is not a “foreign exchange reserve” asset of central banks, it does not involve a foreign currency, and it is not included in the data above, so it doesn’t belong in a discussion of reserve currencies. But it’s part of the broader “official reserve assets” that foreign exchange reserves are also part of, and it is an asset that central banks are diversifying to, as they ease away from the USD, and in that respect, it fits in.

Gold holdings by official authorities rose by 0.8% year-over-year to 1,175 million troy ounces at the end of Q4, back where they’d been in 1977, according to the IMF on Friday.

In 2008 and 2009, when the global financial system seemed to be at risk, these central banks changed their minds about gold and started buying hand-over-fist, after having spent the prior four decades dumping their gold holdings.

In 2025, the price of gold lost its oomph. After a huge years-long rally, it topped out at $5,627 on January 29 and today is down 20% from its all-time high. Despite the drop, gold is still up by 44% from a year ago and by 100% from two years ago. Part of this years-long price surge may have been driven by central-bank buying and by the intense hoopla and hype around it.

Official gold holdings at the end of 2025 would be valued at $5.27 trillion at today’s price, compared to $13.0 trillion in total foreign exchange reserves, and $7.46 trillion in USD-denominated foreign exchange reserves:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Not to worry, USD denominated stable coins will keep up demand for the dollar for years to come (s)