Share of ARMs originations fell further and is at historic lows: FHFA’s National Mortgage Database.

By Wolf Richter for WOLF STREET.

The super-low mortgage rates of 2020 to 2022 — the average 30-year fixed mortgage rate dropped below 3% even as inflation shot toward 9% — are one of the factors in this frozen housing market, where sales of existing homes have plunged by nearly 25% from 2019 for the third year in a row, and where mortgage applications have plunged by about 35% from 2019. Homeowners who financed and re-financed a home at those low mortgage rates back then and now want to move and buy another home would get hit by much higher mortgage rates and very high prices, and for many the math doesn’t make sense, and they stay put. So we watch those mortgages to look for signs of a thaw. And there is a thaw, but it’s very slow, and slowing.

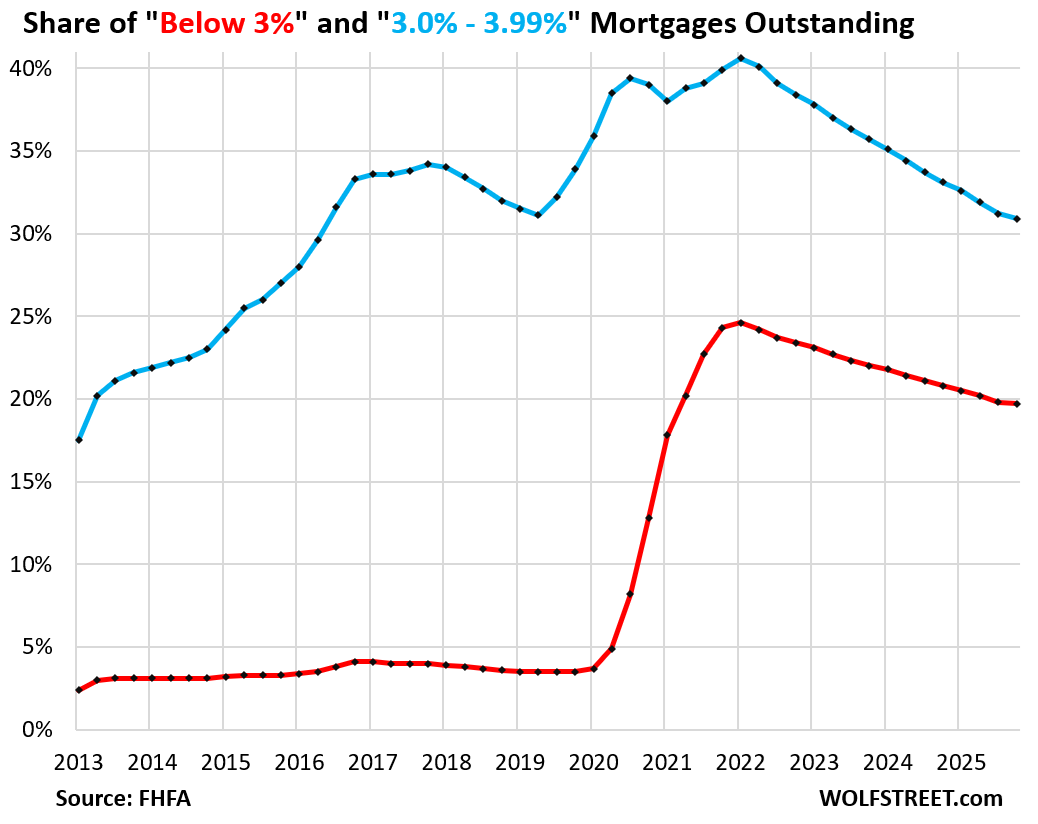

The share of below-3% mortgages outstanding, by number of mortgages (red line in the chart), edged down to 19.7% of all mortgages outstanding in Q4 — the already painstakingly slow progression slowed further — down from a share of 24.6% at the peak in Q1 2022, according to data by the Federal Housing Finance Agency (FHFA) today. The data set goes back to only 2013.

The share of 3% to 3.99% mortgages (blue) edged down to 30.9% — the painstakingly slow progression also slowed — down from a share of 40.6% at the peak in Q1 2022.

The share of below-3% mortgages had exploded from early 2020 through Q1 2022 when the Fed’s interest rate repression – near-0% policy rates and trillions of dollars of bond purchases, including mortgage-backed securities (MBS) – created a tsunami of homeowners refinancing their homes to get these new ultra-low interest rates.

And they’re now very reluctant to give up those mortgage rates. But life happens – death, divorce, an irresistible new job, an addition to the family, the wish to move closer to the kids, etc. – and homes get sold and the mortgages get paid off, and those ultra-low mortgage rates are fading out of the housing market, but at a snail’s pace.

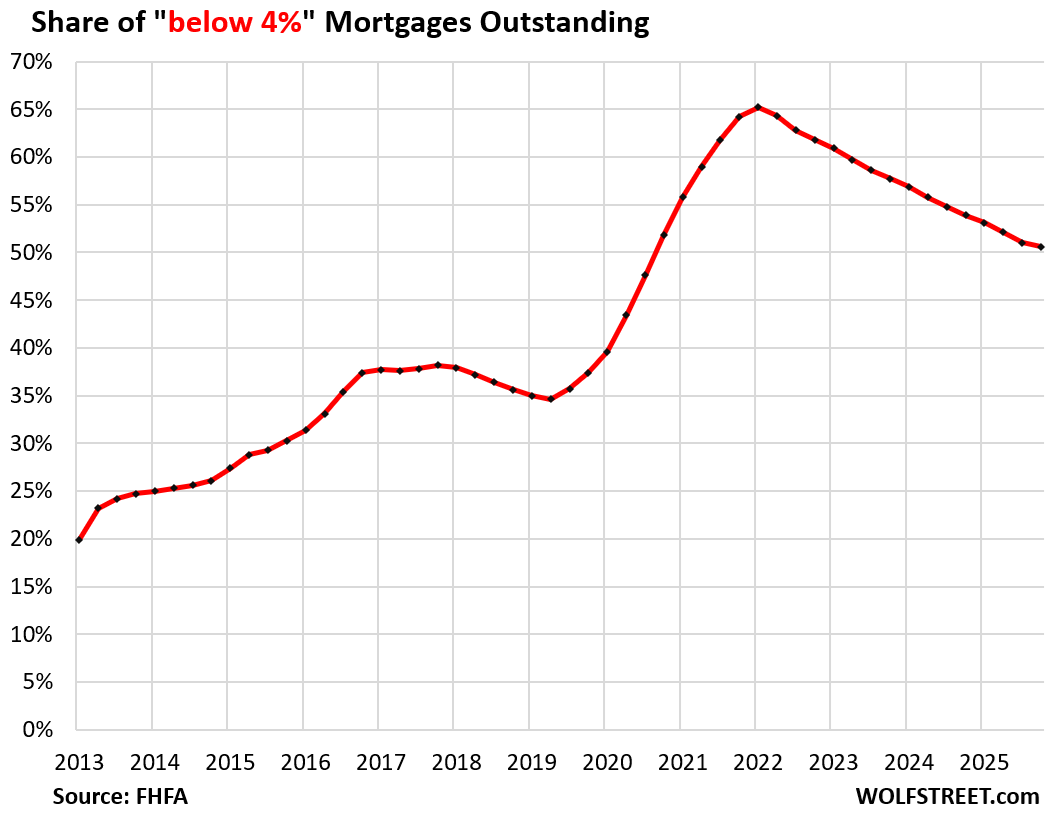

All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.

Combined, the share of below 4%-mortgages declined to 50.6% of all mortgages outstanding. At the peak in Q1 2022, over 65% of all mortgages outstanding had interest rates below 4%.

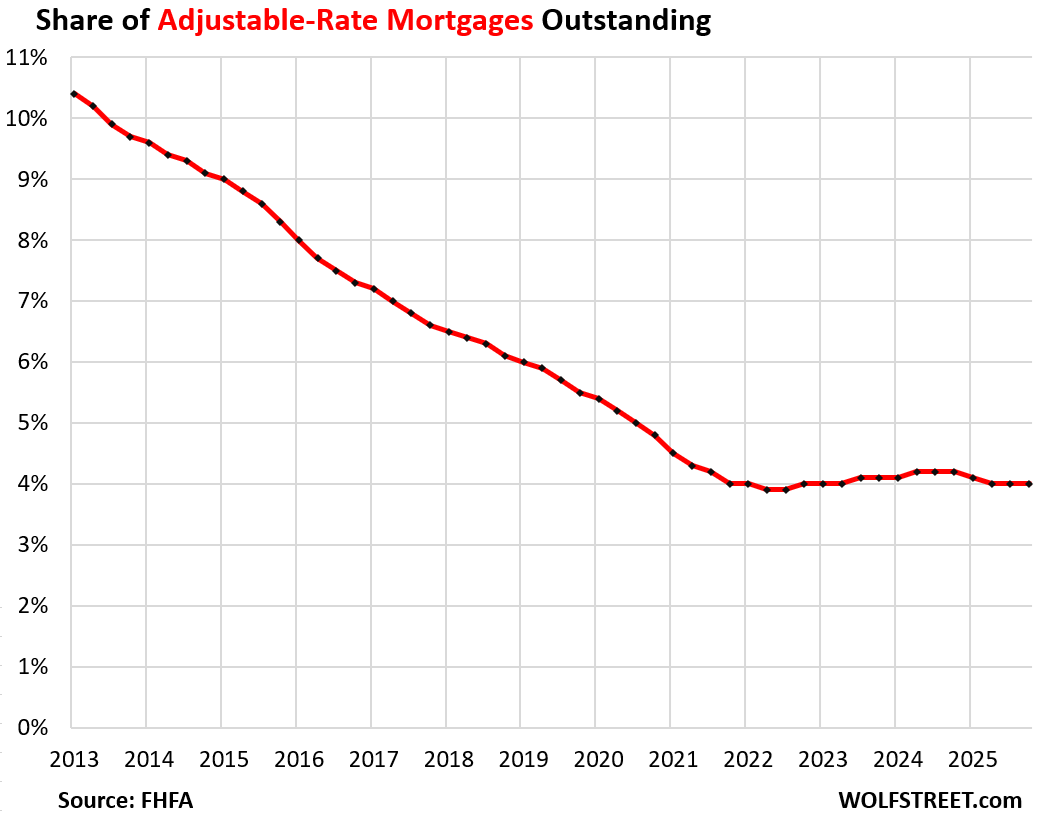

The share of Adjustable-Rate Mortgages outstanding has been hovering at low levels since 2021, and has remained at around 4.0% in 2025, down from over 10% in 2013, the extent of the FHFA’s data.

Some ARMs had rates below 3% even before 2020, which is one of the factors why the below 3% mortgages (red line in the top chart) was between 2.5% and 4% before 2020.

Homeowners with ARMs that were originated when rates were low experienced payment shock when their mortgage rates adjusted as rates began to rise in 2022.

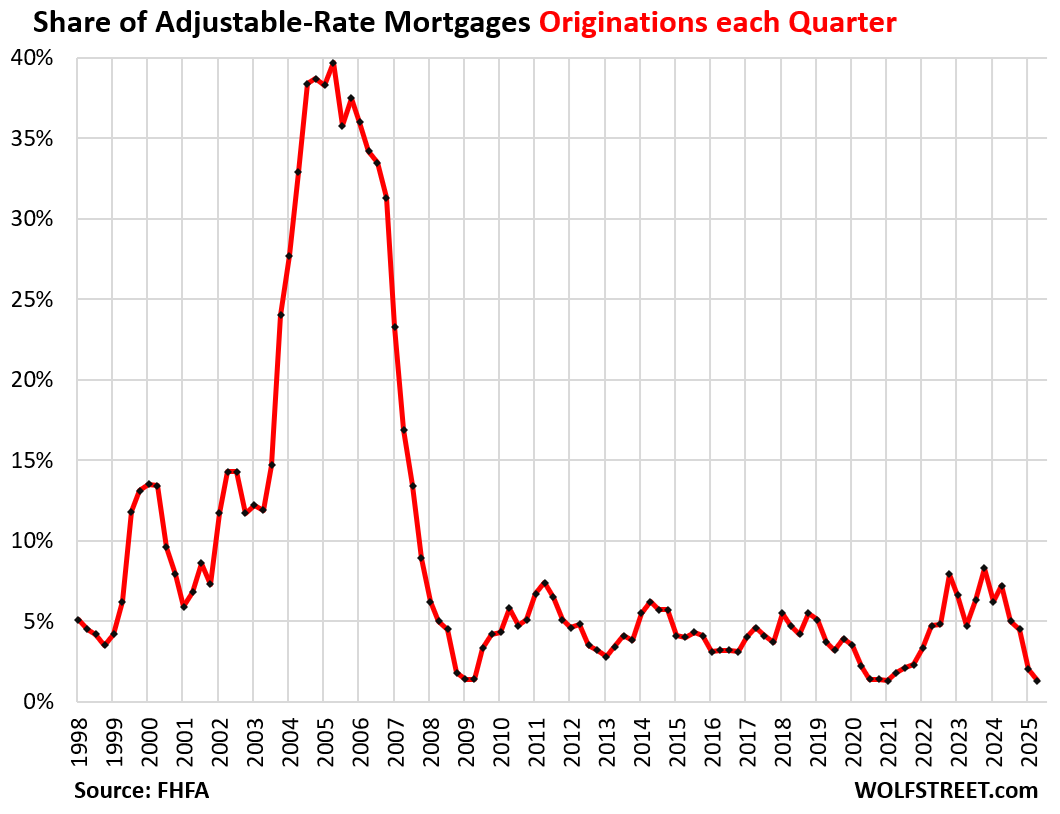

Originations of ARMs (new ARMs being issued in a quarter) remain low and declined further, despite some funny clickbait nonsense articles in the crisis-media about a huge spike of ARMs originations.

In Q2, the latest data available from the FHFA, the share of ARMs originations declined to 1.3% of total mortgage originations, among the lowest share on record in the FHFA’s data on ARMs, which goes back to 1998. But note the ARMs bubble during Housing Bubble 1:

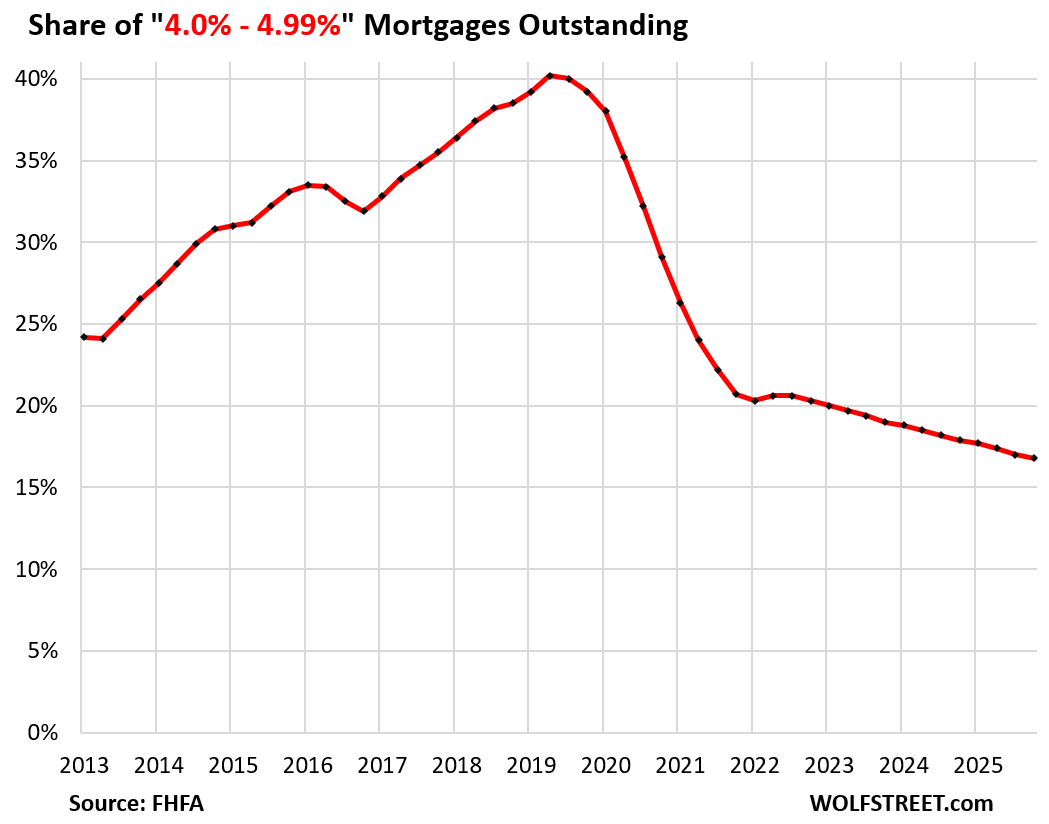

The share of 4.0% to 4.99% mortgages declined to 16.8%, the lowest share in the FHFA’s data going back to 2013, and down from the peak in 2019 of 40%.

Homeowners who had qualified for mortgage rates between 4.0% and 4.99% before 2020 refinanced into the lowest-rate mortgages. In other words, they financed out of this 4% to 5% category, which is why the balance of those mortgages plunged in 2020 and on.

But homeowners who had 6% or 7% mortgages before 2020, due to lower credit scores and other factors, also refinanced into mortgages with sharply lower rates, and many of them financed into this 4% to 5% category, which is why the share of this category didn’t plunge further than it did.

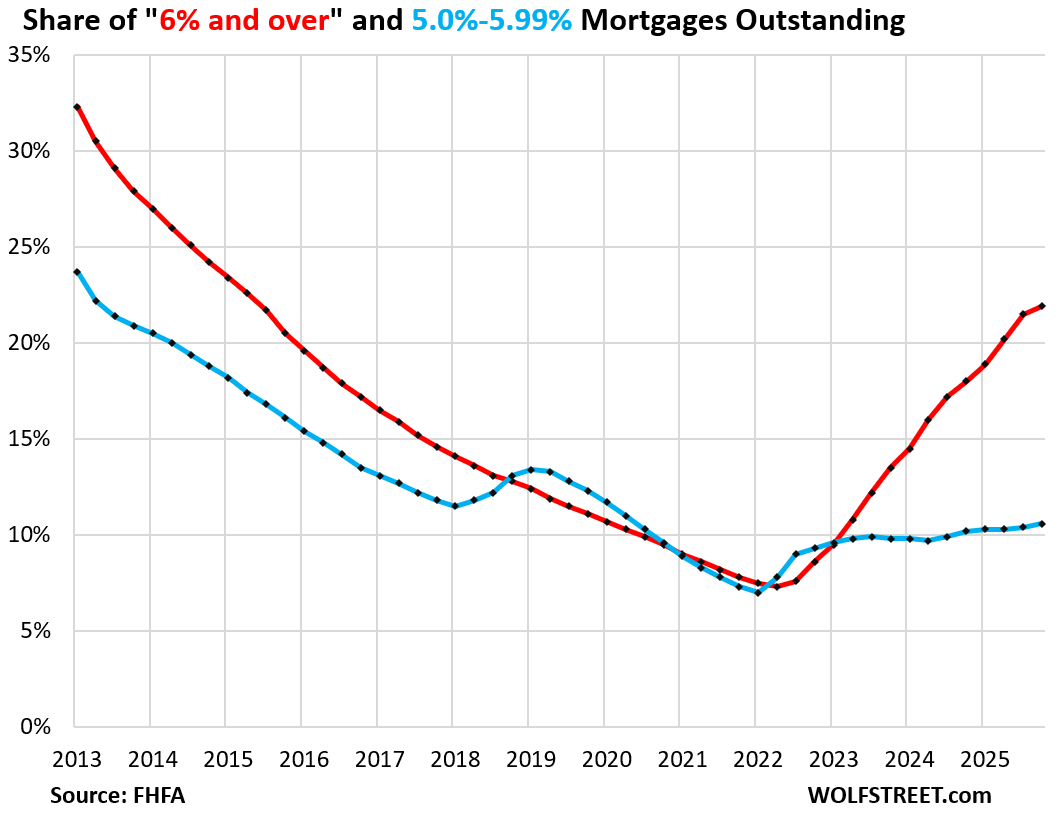

The share of 5.0% to 5.99% mortgages ticked up to 10.6% in Q4 and has been edging higher for two years (blue in the chart below).

There are currently fixed-rate mortgages offered in this range, including conforming 15-year mortgages, but 15-year mortgages are not very popular because the payment is higher.

The share of 6%-plus mortgages rose to 21.9% of all mortgages in Q4, the highest since 2015, up from a share of 7.3% at the low point in Q2 2022 (red in the chart).

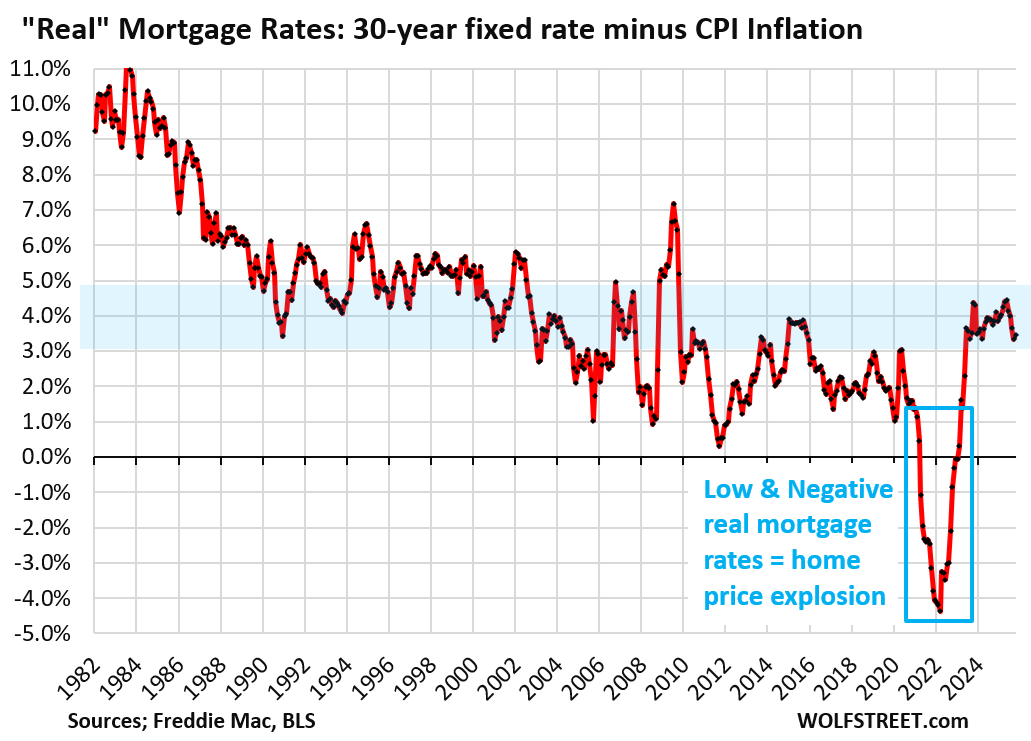

What blew up the housing market. In early 2020, as the Fed imposed its reckless monetary policies, including the purchase of trillions of dollars of MBS to push down mortgage rates, the average 30-year fixed mortgage rate plunged and eventually settled below 3%, even as inflation was shooting higher. By early 2022, the average 30-year fixed mortgage rate was below CPI inflation: negative “real” mortgage rates (mortgage rates minus CPI inflation). This was better than free money!

At the peak of the Fed’s recklessness, the average 30-year fixed mortgage rate was below 3% and CPI inflation had shot to 7%, and “real” mortgage rates (mortgage rates minus CPI inflation) were 4 percentage points below CPI – a negative 4% real mortgage rates. This is what blew up the housing market, trigged a historic home-price explosion, and caused massive long-term damage that continues to bedevil the housing market and that will take years to repair.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Sitting on 3-3/8 but not wanting to move regardless. Fortunately/unfortunately, the loan is almost paid off. I have enjoyed investing the “cheap” money.

Looks like the single family home (not condo) housing market freeze is going to be resolved with a whimper rather than a bang. It took 4 years for the below 4% mortgage level to drop 15%. Assume the same going forward, and it will be down to 35% in 2029, consistent with the five years before the pandemic. And, in another 4 years, general inflation and the slow price reductions will take us to a price level not entirely out-of-whack, and where sales begin to pick up again. Absent a huge economic dislocation, I’m just not seeing what will cause anything to change. Wages are rising pretty well, but not spectacularly, employment levels are high, and the people who have been able to afford selling over the last few years will likely continue to be able to continue to hang on to their house and hold out for the price they want. Certainly, in some localities that will likely be different, but for the country as a whole, I’m not seeing what will cause a huge change. Even a recession, unless it is deep, probably won’t be enough to do more than perhaps speed things up a bit.

I have a 2.5% 30 year mortgage. We’d love to move to something with more land but the increase in payments isn’t really appealing. So right now we’re just saving the money up for when we do finally pull the trigger it will make our mortgage a lot smaller. The savings are tied up in treasuries yielding a lot more than 2.5%, the math makes it just make sense.

I would love to know what % of properties with sub-4% mortgages are being rented out versus owner-occupied.

These are the “accidental landlords” of which there is an increasing number. They can’t sell their home because they cannot get the price they want, so they put it on the rental market. Zillow is now tracking them via its rental and for-sale listings, which it can cross-reference. And they’re pushing down rents of single-family rentals. Bring on the supply!!!

But accidental landlording doesn’t resolve the issue of the new home having to be financed at a higher mortgage rate.

I hate the term “accidental landlord” because they are actually intentional landlords. They refuse to sell their houses at market value so they have willingly decided to try out landlording, where they will undoubtedly try to overprice the property. I would call them “market deniers.”

If the homeowner is underwater on the loan, they can’t sell, hence being an accidental landlord.

Very interesting. Thanks.

Net domestic migration is propping up prices in Florida, Texas, Carolinas, & Arizona.

Such eye-opening but gross charts which lay bare the fake and painful market dynamics created by money-printing and interest rate suppression, all designed to benefit already wealthy asset holders.

6%+ @ 22%

Nice! Higher for much longer than TACO or anyone for that matter wants.

If we want lower prices outside of recession, this is exactly what the Dr. ordered to slowly correct massively overvalued home prices.

I’m at 4.5 but it will balloon in about 2 years – I am wondering if I should just refi in at 5.75 for a locked in 30 year fixed (Might not be avail later), and it seems like rates will never get down below 4 again.

It’s hard to say what really will happen in 2 years, but it seems to be the probability of rates being lower is less likely.

Make the maximum amount in extra principal payments while you have this low-interest-rate mortgage. It will make refinancing the balloon a lot easier… you can then refinance that lower balloon with a 15-year mortgage (lower rate than 30-year, shorter term), which will save you a ton.

I wouldn’t be surprised to see some of these below 3% homes suddenly have an “accidental” fire. A lot of people stand to make a lot of money if these home went up in flames. Remember Boston back in the 1970s anyone. There was a documentary about it called “The Fire Next Door”. It should have been named “Arsonists for hire.”