Whiff of turmoil in the bond market as inflation fears moved to the front and center.

By Wolf Richter for WOLF STREET.

The bond market, which has become very edgy about inflation and future supply – given the ballooning debt – is now seeing the previously unthinkable: a rate hike possibly late this year or next year. That is what the 1-year Treasury yield, the 2-year Treasury yield, and the 3-year Treasury yield are telling us. Those yields have spiked since the war in Iran started.

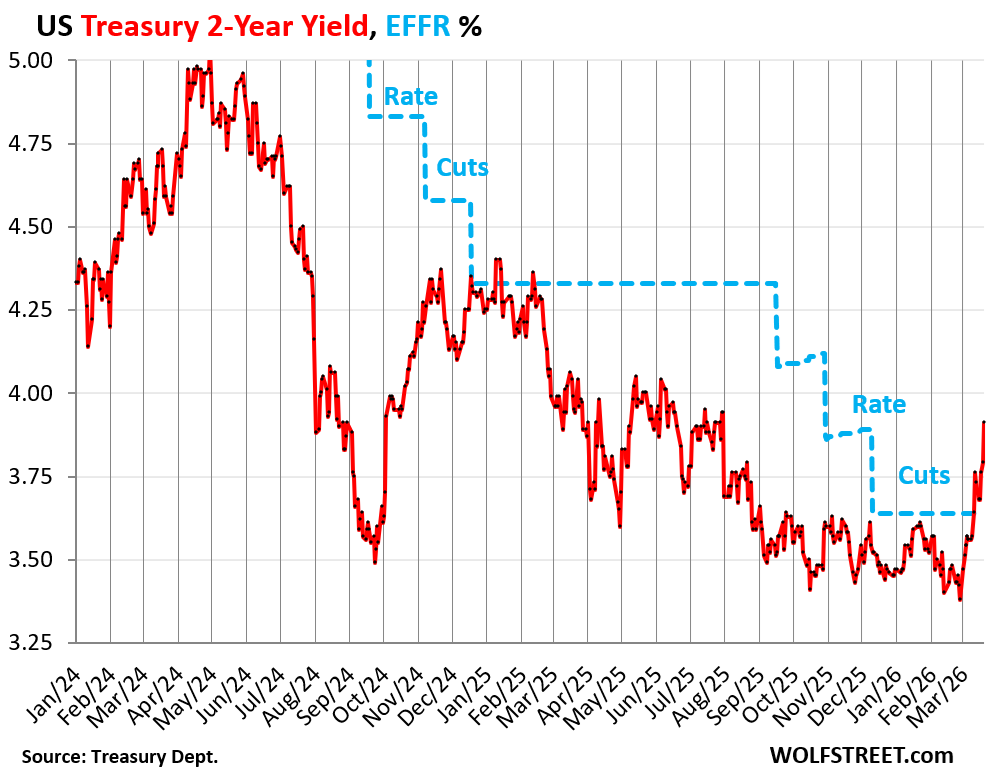

The 2-year Treasury yield spiked by 53 basis points since the beginning of March, to 3.91%. In other words, it flipped from fully pricing in 1 rate cut to fully pricing in 1 rate hike in the span of three weeks.

The 2-year Treasury yield punched through the Federal Funds Rate (EFFR, blue in the chart) for the first time since November 2023, which had been nearly a year before the Fed even cut its policy rates, and is now at the highest point since before the Fed’s last three rate cuts that started in September 2025. The EFFR is the overnight rate the Fed targets with its policy rates; and with the 2-year yield now 27 basis points above the EFFR, the bond market has scuttled rate-cut expectations and replaced them with rate-hike expectations.

Back in October 2024, the 2-year Treasury yield shot higher as the Fed began backpedaling on its rate cut projections, after a lot of the bad data in the prior months was suddenly revised away, and the economy was doing fine after all, the labor market wasn’t deteriorating, and inflation turned out to be alive and well.

The 2-year Treasury yield has a good record of anticipating somewhat distant rate hikes and rate cuts.

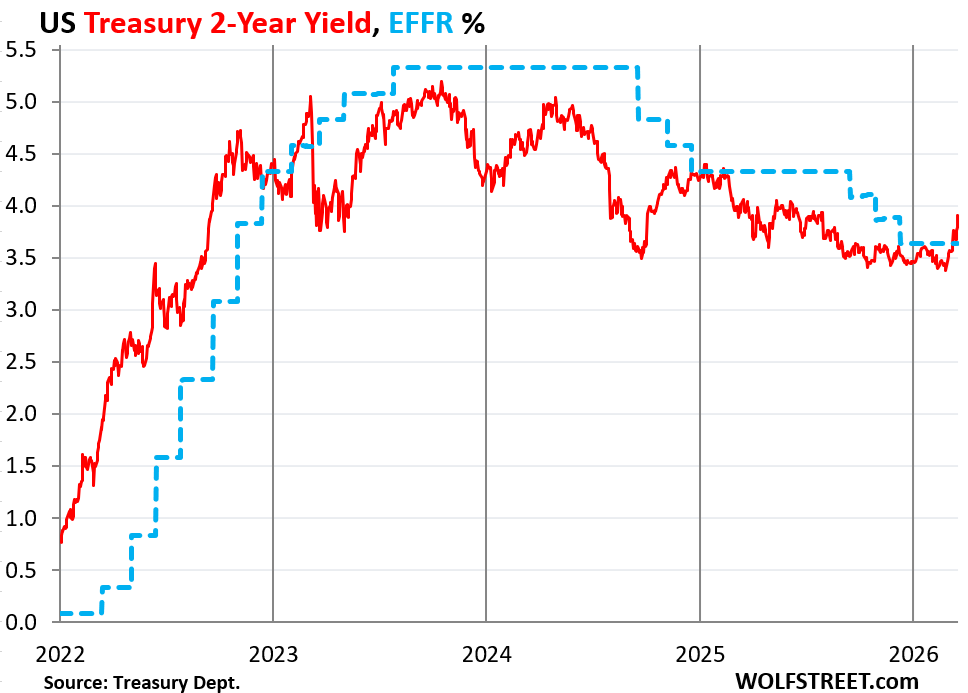

Here is a view going back to the beginning of the rate hikes in this cycle. The 2-year yield stayed ahead of the rate hikes until the end of 2023, when it started pricing in the pause. It anticipated the 100 basis points in rate cuts in 2024 several months ahead of time.

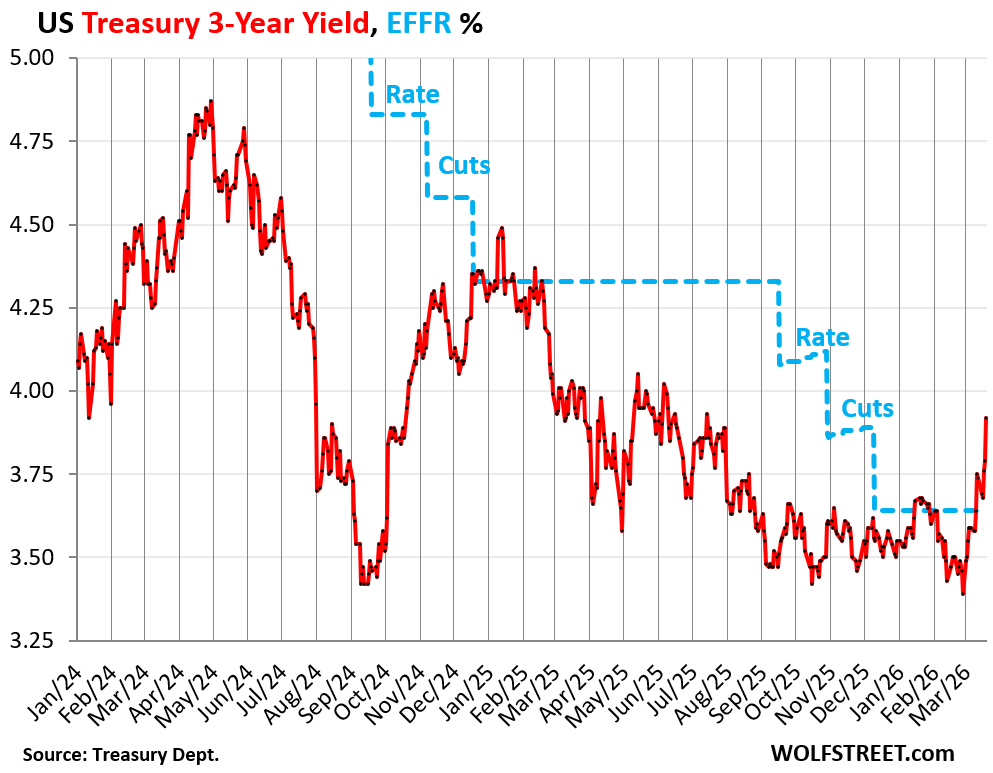

The 3-year Treasury yield spiked by 53 basis points since the beginning of March, to 3.92%, the highest since before the last three rate cuts in 2025.

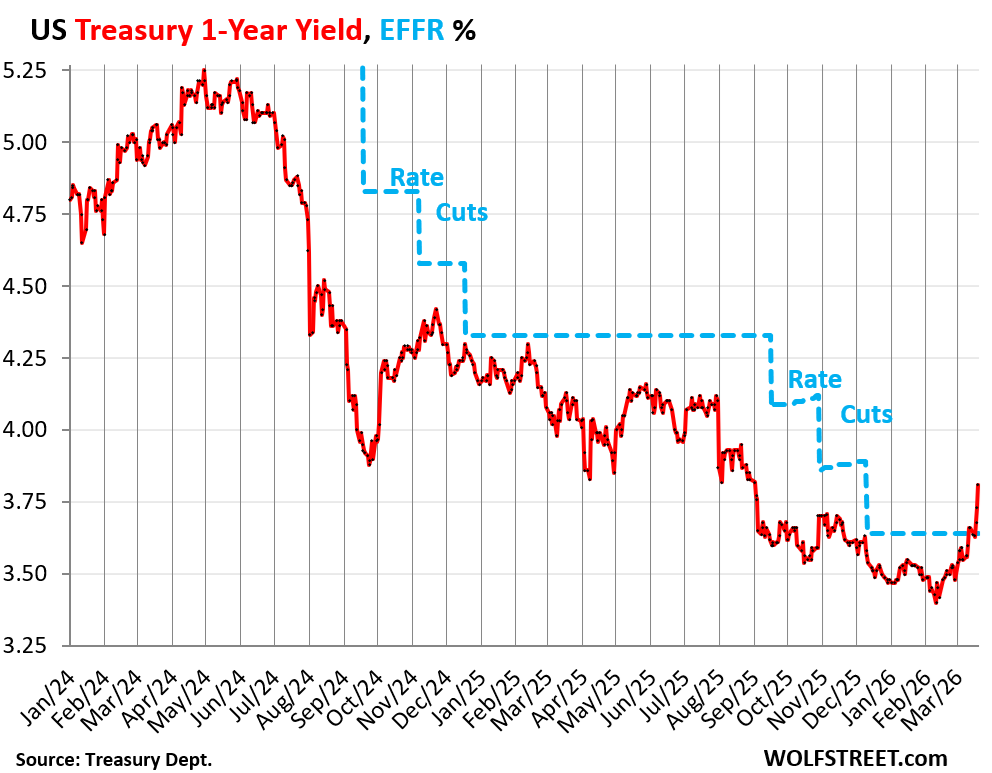

The 1-year Treasury yield shot up by 33 basis points since the beginning of March, removing the rate cut from its less-than-one-year window, and pricing in the potential for a rate hike by late 2026.

Inflation fears are now front and center in the bond market.

This spike in yields started at the beginning of March after the war in Iran kicked off, which caused energy prices to spike, and they spiked even in the US, which has purchased only minuscule amounts of crude oil and petroleum products, and no LNG at all, that were shipped through the Strait of Hormuz.

The US is the largest producer of crude oil and petroleum products in the world, and the largest natural gas producer, and is a big exporter of gasoline, diesel, jet fuel and other petroleum products, and the largest exporter in the world of LNG. This is not a shortage problem for the US, but an inflation problem tied to global commodity prices.

Fertilizer prices in the US also spiked, though the US is a huge producer of fertilizers. The oil and gas industry, and the petrochemical industry in the US are minting money right now because their selling prices have shot up.

There were already inflationary pressures for months before energy prices began to spike: The Fed-favored core PCE Price Index, which excludes food and energy, accelerated to 3.1% for January, the worst in nearly two years. The Fed’s target for it is 2%.

Gasoline and diesel prices have already shot higher. Consumers pay these prices directly by filling up their gasoline or diesel vehicles.

But fuel prices worm their way into prices of goods (as transportation and material costs rise) and into services such as airfares where a major component is fuel. Sometimes, energy price spikes are one-time events that fade as soon as energy prices plunge again; other times they trigger larger and broader inflationary pulses that can get way out of hand, such as in the 1970s.

Powell was clear about it in the FOMC meeting press conference: The Dot Plot median projection was still for one rate cut in 2026, but “if we don’t see that progress [on inflation], then you won’t see that rate cut,” he said.

At the moment of the FOMC meeting on March 18, the bar for a rate hike was still high. But it’s only March.

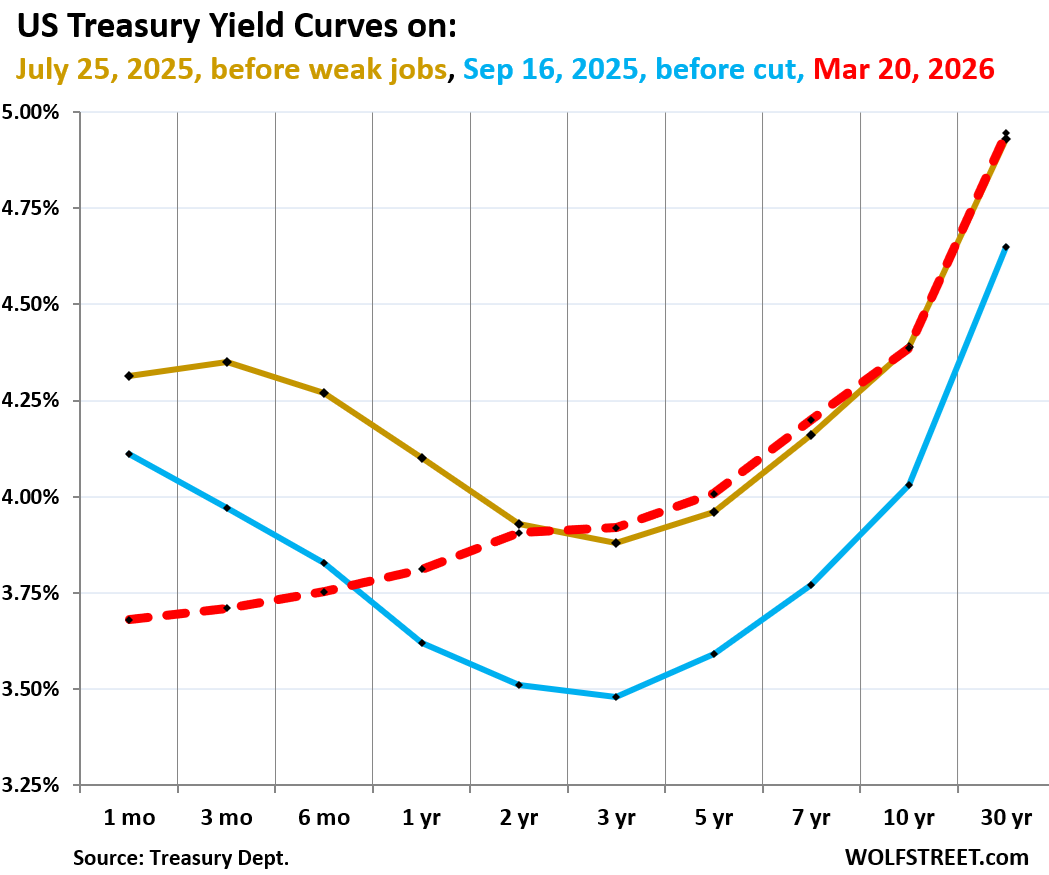

The yield curve solidly uninverted this week. What happened is that yields at the very short end up to the 3-month yield didn’t move much, sticking with the status quo of no rate change in their window. But the longer yields rose, and the yields in the middle – 1 year through 5 years – rose the most, which eliminated entirely the sag in the middle, that had been formed when for the past three years, those middle yields were lower than both, short-term yields and long-term yields.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates in 2025 and 2026:

- Red: Friday, March 20, 2026.

- Blue: September 16, 2025, just before the Fed’s first rate cut in 2025.

- Gold: July 25, 2025, before the labor market data turned sour again.

The 1-month yield (3.68% on Friday) is bracketed by the Fed’s policy rates (3.50%-3.75%) and closely tracks the EFFR (3.64%).

Despite the turmoil, the borrowing must go on.

The US government sold $606 billion of Treasury securities this week, spread over nine auctions, including 10-year Treasury Inflation Protected Securities (TIPS) and 20-year Treasury bonds.

Of these auction sales, $571 billion were Treasury bills, with maturities from 4 weeks to 52 weeks, most of them to replace maturing T-bills.

| Type | Auction date | Billion $ | Auction yield |

| Bills 4-week | Mar-19 | 91 | 3.615% |

| Bills 6-week | Mar-17 | 92 | 3.635% |

| Bills 8-week | Mar-19 | 86 | 3.635% |

| Bills 13-week | Mar-16 | 96 | 3.610% |

| Bills 17-week | Mar-18 | 69 | 3.610% |

| Bills 26-week | Mar-16 | 83 | 3.570% |

| Bills 52-week | Mar-17 | 54 | 3.485% |

| Bills | 571 |

And $35 billion of the auction sales this week were Treasury notes and bonds.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| TIPS 10-year | Mar-19 | 21 | *1.896% |

| Bonds 20-year | Mar-17 | 14 | 4.817% |

| Notes & bonds | 35 |

The issuance of 20-year bonds was halted in 1986 and was restarted in 2020. So the entire issue of 20-year Treasury bonds this week adds to the overall debt as it replaces no maturing 20-year bonds because there are none out there in the wild that were issued before 2020.

*TIPS yield: With TIPS, the “yield” is established at the auction, and interest payments are made every six months. But TIPS holders also receive inflation protection, based on CPI, and this inflation protection is added to the principal, and the interest rate (which is fixed for the term of the TIPS) is applied to the entire principal, including the inflation protection. As the principal grows over time with CPI, the interest payments increase, though the interest rate remains fixed. So the yield figure, which is low, is on top of the CPI rate that changes with CPI.

And in case you missed the first half of the bond market analysis yesterday: Treasury Yields Spike, 10-Year to 4.39%, 30-Year to 4.96%, Mortgage Rates to 6.5%, as the Bond Market Gets Antsy

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks for the timely response and (as always) maintainnng a cool head in what appears to be a major monkey wrench turning point.

I think mr Powell is happy to vacate his

office soon.

Who knew bonds could be so exciting?

Im happy he’s leaving. Do you know that he said inflation from the oil shock will be transient? Where have we heard that before? And inflation has been rising during his cuts!

Jerome Powell’s term as one of the 7 Federal Reserve Board of Governors does not end until 2027.

Powell has done as much damage to the country as any other single person. He is a cancer upon society.

Agreed

How so?

Overall I always agree with your criticism of FED. They have created this huge asset bubble with ZIRP and QE from 2008. But pinning all of it on Powell would not be fair.

It started with Ben and then Janet. You cant blame all expansion on Powell. He tried QT in 2018-2019. It failed because BEn closed SRF in 2008 itself. Covid was unprecedented. Congress pushed FED with multi-trillion packages. After Covid Powell led FOMC made Himalayan blunder of keeping rates too low for too long and buying trillions of MBS.

Powell also did 2.2 QT; Not many believed will happen. That too in a highly political environment. After Volcker era, now FED is facing unprecedented attack on its independence. I believe history will be fair to Powell.

Powell was the worst ever. He got rid of deposit classifications.

You are correct that QE and ZIRP started before Powell. However, it was Powell who in the face of massive inflation held rates too low for too long creating a huge asset bubble. Housing where I live in AZ doubled because of his action/inaction. This is unforgivable and people of my generation will remember that.

I won’t speak for others, but I don’t pin ALL of it on Powell. While I still believe that the monetary stimulus that started in March of 2020 was reckless, I can excuse part of it due to the unknown at the time.

But continuing to print $120 billion a month, and hold rates at 0, for all of 2021 and part of 2022 was inexcusable. Hell, CNN published an article in June of 2021 titled “Inflation: The Housing Market is on fire. The Fed keeps adding gasoline.”

When CNN is calling you out, you know you’ve gone too far.

Wolf man – one simple, honest question for you –

Why does an ‘entity’ that takes money continuously from every worker through income tax, receives corporate tax, tax on fuel (gasoline) and dozens or hundreds of other taxes, need to keep borrowing money? You’d think they’d be sitting on a Mount Everest size pile of cash!

If you or I acted like this, we might get admitted to the mental hospital, or at least to debtor’s prison. Any thoughts?

The government is borrowing because no one wants to pay the extra taxes it would take to cover the deficit. Borrowing is pain-free, taxes are not (until borrowing isn’t pain-free anymore).

“Borrowing is pain-free”

Not really,people pay everyday extra money for inflation(and hiden inflation).

This is why the debt cycle finds an end,when people can’t afford anymore the price of living.

At some point, the reality of servicing the debt will take away the Easy button. I have no idea when this will be, but a loss of confidence in the dollar, Congress & the Treasury’s / Fed’s ability to manage the negative financial consequences of our gargantuan debt will be the root case. My guess is that 10YT yield approaching 6% would be a warning sign.

“At some point, the reality of servicing the debt will take away the Easy button.”

We’ve already started to see the beginning of the end of the big DC lie (endless borrowing followed by money printing to temporarily offset the consequences of the endless borrowing).

Once the money print “fix” (using printed money to artificially force borrowing’s interest rate down…for a while) resulted in tangible/painful inflation for the general public, the jig started to be up.

In the era of the internet, more and more people will be made to understand that the Fed/DC aren’t some sort of magic unicorn that can poop diamonds forever – the whole Fed/DC/NYC nexus runs on phony interest rates/money printing now – and Americans have felt the inflationary consequences of that for 4 years.

And we are pissed.

Once enough people realize that entitlement benefit insanity/forever wars/etc. are only made possible because their housing/food/etc costs are forever inflated…the jig is up.

The scam only worked in the past because 1) it was of smaller relative scale and 2) it was easier to lie to the public.

No, no one wants to pay extra taxes because they’re excessively wasting the taxes we do pay them.

So you think it’s better they borrow the money that “they’re excessively wasting?”

If voters were forced to pay for all of it with taxes — rather than by borrowing, which people don’t really feel — then voters would be a little more conscious about who they sent to Congress, and might be a little more careful with their choices.

Both parties, both of them, need to come to terms with the plain fact that spending simply must be cut. If spending was cut a couple of percent each year for 3 or 4 years, while the economy grows, we would all be far better off for it. The problem is that people like free stuff and the press screams absolute bloody murder over even small decreases in the trajectory of spending increases.

Inflation is a tax, and people are paying it. And nobody wants it.

And now we have a $200 billion supplemental working its way through Congress to pay for the War in IRAN. That will all have to borrowed, driving up interest rates and inflation further.

Wolf, not asking for political analysis, but how long do you see oil prices remaining elevated and affecting overall inflation? Is this indicating the market thinks we will see increased inflation for 2-3 years?

Not wolf here but I’ll throw out that this administration knows they need to resolve this well before midterms. That means the interaction with the terrorist proxy groups needs to end and then an additional time is required for oil price to drop and markets to stabilize from the drop. If this is still dragging on in August, political control in the US is at risk of change.

Yeah, sounds like a quick 2 week job huh?

Kinda like how Iraq was a 2 week job.

Easy peasy. Especially with the most competent leadership in the history of the US!

2 weeks to stop the spread.

I remember when Trump said Covid would be over by Easter 2020.

The other thing to consider is energy infrastructure getting bombed etc.,that can literally take years to repair/rebuild.

the midterms are a lost cause for the incumbent party.

just choosing whose donors fleece the taxpayer a little more.

I listened to the Thoughtful Money podcast with Doomberg today. They had in interesting analysis on US/ global natural gas and oil.

Might be worth a listen.

The US is going to collapse again?

Nope.

No doom. Just interesting.

It was actually the opposite of US collapse.

It was regarding United States oil/ gas production dominance, and that relation to current and future AI development.

I thought it was interesting.

No doom at all.

They are Wolf. On a long enough timeline. I think that timeline is within my lifetime. It’s already happening.

Doomberg = Financial Banksy

Yeah…

Maybe so….

Interesting either way.

It really is Silly that the Fed still has 1 Rate Cut…., and considering the circumstances, they had a very Dovish Outlook from there released Policy Statement on Wednesday….

Trump is no fool in picking his Fed Chairman…. as Long as Warsh is his chosen selection in May……, there going to Cut…..,

Warsh past statements on the surface, puts him as a Hawk….,

So why would Trump Choose him ???? Cause obviously he sold his soul, and will Cut Interest Rates….., or he will allow Bessent at the Treasury to have more leverage in lowering rates…..

There are 12 voting members of the Federal Reserve FOMC which sets the interest rate policy and the Chairman of the Federal Reserve is JUST ONE of those 12 members, and it really doesn’t matter how the Chairman votes.

SoCalBeachDude….. , all of the Members are Dovish….. , think about it, even with Iran Hormuz situation, they all are discounting it…. , and have 1 Cut…., As we learned with Powell, actually throughout Fed History, They vast majority of the time they all vote the same way…. , having 1 or 2 dissenters don’t mean Nothing….., when the last time thr Fed had even Half Dissenters in the Vote ???? Exactly Never…… , and as we know they don’t want to let the Stock Market Collapse of the artificial bubble they created, so they will continue to cut…. , until the Inflation situation is drastically high….

The March 20 table on treasury.gov already shows the 10-year TIPS real yield picked up a 2 handle overnight. 2.01% is the highest I see in the table going back to July 2025.

Boy, that escalated quickly.

So we are going to get persistent high inflation, followed by persistent high interest rates.

Then this finally pops the stock bubble after all these years (since guaranteed high rates for a while will be better than the low dividend ratio for most stocks. So everyone will sell their bubbly stocks as that is the ‘rational’ move in this case).

Will be exciting if it actually plays out this way.. the 1970s all over again..

Can’t repeat the 70’s. The Great Inflation was due to the high velocity of money, moving from clerical processing to electronic processing, the removal of gate keeping of time deposits.

Um, electronic processing has absolutely nothing to do with the stagflation in the ’70s.

What’s your lockbox without OCR?

TACO spoke this morning and the DOW pre market flips 1500 points.

Who’s making money on this flip?

Interesting. I only use TD direct for iBonds. I see them on Schwab for ~1.90, which is normally pretty tight to the market, at least for the bills I buy. +10bps to deal with the hassles of TD might be worth it.

Why would the real rate rise? CPI inflation is already covered, so that leaves 1) credit risk, 2) spread between CPI and real world inflation, 3) distrust in the reported CPI….

Wasn’t a quote from TreasuryDirect so I don’t know what you’d see there. There’s a different web page under the U.S. Department Of The Treasury I use as a one-stop-shop for tracking yields. Maybe our host will let this link pass through:

https://home.treasury.gov/policy-issues/financing-the-government/interest-rate-statistics

The real yields I look at are under “Daily Treasury PAR Real Yield Curve Rates”. Their footnote touches the methodology a bit:

“These par real yields are calculated from indicative secondary market quotations obtained by the Federal Reserve Bank of New York.”

I think we have reached the major leagues now boys! ⚾️ 🌭

i sold beer and soda on gas lines in the 70s as a teenager. cops even bought the beer from us 14 year olds. i suspect we are entering another phase of guns and butter inflation for another decade at least. the last bout was 1965 to early 80s. i also lived through a 75% drawdown in house prices in phoenix AZ from 2006 top to 2012 bottom……….i am looking forward to cap rates on properties to get juicy in the next 5 years or so. you do a wonderful job with this blog, on r/e and fixed income analysis.

When the inevitable economic catastrophe comes, 95 percent of the politicians and our neighbors will express shock – and convince themselves that no one saw it coming.

For years the people who have been ringing the warning bells have been dismissed as fear mongers. This is quite literally the most inevitable problem we’ll ever see coming. And we’re doing absolutely nothing to stop it.

We have an administration that 1) holds the presidency, congress, SCOTUS 2) is willing to bypass all constitutional and institutional controls.

With that much raw power, they could:

– fix and rebuild our failing health care system

– fix housing

– fix our tax code

– fix deficits & budgets

– have built out semiconductors industry to keep China at bay

Ask yourself why they aren’t doing any of those things.

Perhaps we should rate countries by how much money they are printing. They all must have a money supply number. Relatively speaking, if the good old USA is not printing money as fast as the other countries are, we could get away with borrowing a little while longer.

Bear flattening?

Flattening? Maybe we’re looking at different lines. I see steepening.

“Most investors spend their time watching the S&P 500. That’s a mistake, because the credit market is the real “tell.” The bond market has been whispering a warning for weeks now, and credit spreads are now shouting it. As of this writing, the CDX Index, a benchmark measure of credit default swap spreads, has climbed to a nine-month high while the S&P 500 sits within 5% of its all-time peak. Over the past 20 years, every time that combination appeared, a bear market followed. Every single time.”

– Lance Roberts

Lance’s comments are usually very balanced and thoughtful. We shall see what happens. I think the Iran situation is far worse economically than most believe.

Lance has predicted 10 of the last 2 recessions.

And, how many “bear mkts ” have there been in the last 20 yrs ?

Those aren’t allowed anymore.

Maybe I am missing this data in the Voluminous information provided. Is it possible to include the amount and interest rates of notes and bonds being redeemed/refinanced? I agree the graphs provide the big picture on interest rate changes. It would be interesting to “see” the amount(s) of debt being exchanged.

I did explain this very thing in this article: the 20-year bonds that were sold replaced nothing because none have been issued since the 1980s, and each issue now just adds.

And I do that with the 10-year notes when they’re sold at auction once a month:

https://wolfstreet.com/2026/02/14/us-government-sold-701-billion-of-treasury-securities-this-week-as-deficits-balloon-bond-math-is-relentlessly-brutal/

From this article:

“Amount of 10-year notes outstanding increased by $29 billion this week. Bond math, as deficits balloon, is relentlessly brutal. The $54 billion of 10-year notes sold at the auction this week at 4.177% replaced $25 billion in 10-year notes sold at auction in February 2016 at 1.73%, maturing on Sunday. And thereby the total amount of 10-year notes outstanding rose by $29 billion.”

It doesn’t make sense to do that with T-bills because the shorter duration T-bills have auctions every week, they constantly roll over, and amounts change a little, and nearly all replace maturing T-bills, except for a small portion.

I do however show once a month the share of T-bills outstanding as a percent of total debt, usually in the week of the 10-year and 30-year auctions. The chart is from the same article I linked above:

Feels like we could easily enter a period of stagflation. Clearly inflation will continue and that could easily be paired with less economic growth and investment should a global recession occur or worse, a global depression. Not sure there is an official way to identify but at least on the surface it seems very plausible if energy crisis not resolved soon.

“I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would want to come back as the bond market. You can intimidate everybody,” said James Carville, Bill Clinton’s chief strategist, in 1993.

So what’s interesting is Trump made a comment this morning about peace talks being productive, which have echoes of “trade talks with China are going well” during Trump 1.0. The interesting thing is that the stock market surged and oil plummeted after the algos picked up on it.

But the 10-year treasury has barely moved. It’s as though the bond market is either saying 1) we don’t believe Trump’s jawboning has anything to do with reality or 2) we believe that the inflationary pressures that have led to us demanding 40 bps more than just a few weeks ago are not going away and are not 100% related to the Iran war.

Very interesting.

…” Iranian state media said there were no direct talks between the U.S. and Iran.”

The day before Trump said there is no one in Iran to talk to. This is bizarre. 3+3/4 years left is beyond worrisome.

Yesterday when Bessent was asked about the$200 billion war supplemental he said with the joker, sht eating grin: We got the money.

“We got the money.”

That’s true. At least temporarily. There are currently $876 billion in the government’s checking account, the Treasury General Account (TGA).

And it’s “2+3/4 years left”

A 200-basis-point (bps) hike by the Federal Reserve is equivalent to a 2.00% increase in interest rates. If the Fed were to implement such a raise today, the new target range for the federal funds rate would be 5.50% to 5.75%. The Utopia takes courage and conviction to slay the inflation dragon. All the while there will be trillions made by the savers. The Dollar will comeback stronger. The AI bubble comes to head when all the IPO’s launch later this summer. Jeff raising 100 billion capital, who is swimming naked? Who is telling the truth. Lots folks still borrowing on margin who are in trouble if things go the way they should.

There was a narrative being pushed back when rates were 5% last year that the high rates were causing inflation, because those savers were spending all that extra money.

And that high rates were inflationary because they made everything purchased with credit more expensive.

All the while inflation came down from 9 to 3ish.

Some people you just can’t help.

This isn’t the 70’s. What will the interest expense be on that 38 trillion?

LOL.

Wait for it Wolf.

20 year bond grabs a 5 handle overnight.

They borrow because they can grow the economy beyond inflation by doing so. It’d be fiscal folly to not borrow to do so, the economic multiplier effect etc.

They ‘can’ but kinda haven’t for some time now. Preferring economic negative multiplier fiscal expenditure. Aka throwing good money after bad.

Inflation trade vs bond buyers getting fun. Who wins and who loses… been waiting like 15 years to find out haha.

MW: Fed’s Goolsbee indicates door not closed to rate hikes

And Goolsbee is an uber-dove

My favorite SF “citizen” always had the correct response.

“Go ahead, make my day”

Maybe a dove on cheap money. Certainly not a dove on inflation.

MW: Stocks are teetering on the edge of correction territory. Why the ‘TACO trade’ could flop.

A double minded man is unstable in all his ways.

Imo That is Trump personified.

Plan a accordingly.

The insatiable demands of the federal government are crowding out private investment.

people think “More money is better”. It’s not. It’s all inflationary. Look what corporations are doing with more money. Stock buybacks and greedflation, raising their prices, shrinkage. Government, the pentagon and the fed need austerity, not the working class. Hey politicians, stop destroying the dollar!

How ironic. The politicians are doing what their corporate owners tell them to do. See the problem yet?

The price of money or the cost to lend currency (interest rates) into any economy is probably the most important price signal on the planet because it will determine how resources (capital) and talent are allocated. The mis-allocation of precious resources and talent will always destroy an economy. This is made even worse if your system starts rewarding bad behavior (hello MBS). But I digress, It appears that our oligarchs want to destroy the very system that made them so wealthy in the first place. For those of you who witnessed or understand what the former Soviet Union was like after the collapse (late 80’s and 90’s), that is where America is heading, just coming at it from a different direction. I don’t expect our oligarchs to behave any differently.

Hedge accordingly.

I don’t know if this will collapse like they did. But there are echos. For example what productivity are most of the new Jobs making? They’re abstracting an already abstract techno centric role. The initial gains of the 90s and 2000s are questionable in 2020’s.

In other words the value has moved into technology vs the benefit to you and me.

And so as that world creates the smallest circle of winners who build on it’s abstractions, those winners seem to have figured out how to go into politics suddenly. SV is now waving the flag in an F-150 in camo overalls. We’ll see how this all unfolds.

All organisms will do anything to survive, full stop. Eventually, those overall wearing rubes start believing the “lying eyes” and deal with the imposters that are gutting their community.

Nothing new under the sun my friend, the tools/weapons change but that’s about it.

May we all find a better day.

When asked about the meltdown of the 2008 housing bubble and the resulting financial crisis, Alan Greenspan told Congress “we’re not smart enough as people. We just cannot see events that far in advance.”

“We’re” not smart enough? The press was full of warnings for years before, as the press is full of warnings now.

Deficit should be limited to 3% of GDP by law, at least that would enforce some discipline, that’s still nearly a trillion dollars but is manageable with GDP growth and would keep inflation manageable.

Curious if Wolf agrees, but I suspect that 4.5% could be the threshold for the ten year. After that, plumbing starts breaking…