For the US, the Strait of Hormuz blockage is a Price Shock and inflation problem, not a Supply Shock. For Europe & Asia, it could turn into a Supply Shock if the blockage persists.

By Wolf Richter for WOLF STREET.

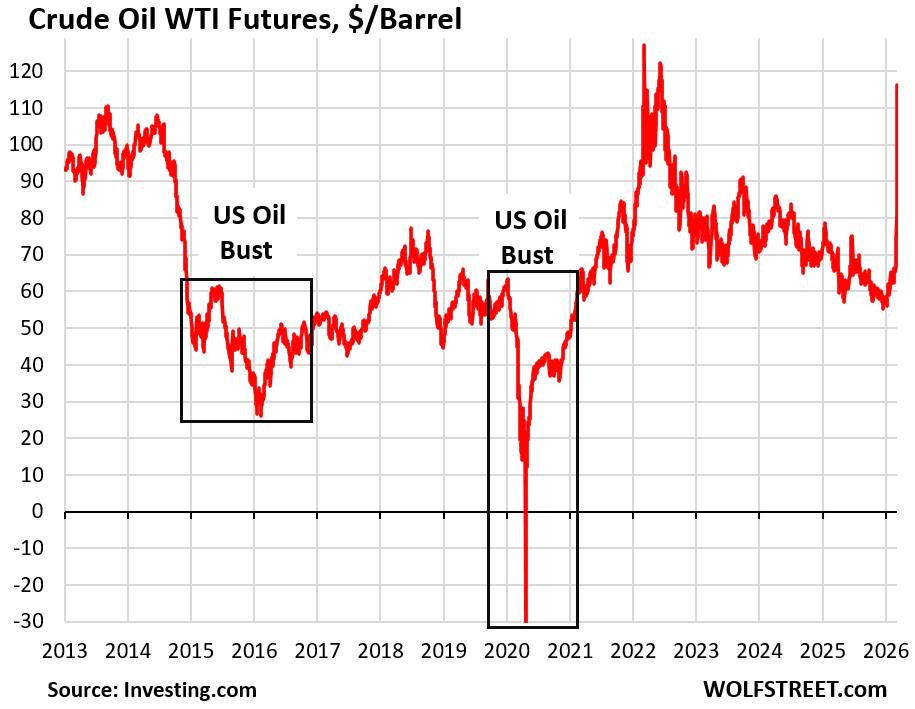

Oil prices spiked further over the weekend. Sunday night, futures of WTI spiked by 28% to $116 per barrel at the moment, amid huge volatility up and down, as traffic through the Strait of Hormuz essentially stopped, and speculation in the futures market went haywire. Since the beginning of March, the price of WTI futures has nearly doubled. This is the same market where the price of WTI futures dropped to an absurd negative -$37.63 per barrel in April 2020. Things can get a little crazy in the futures market.

For the US, this price spike is an inflation problem, and that has already started, and it comes on top of already accelerating inflation; but it’s not a supply problem because the US gets very little crude oil and petroleum products through the Strait of Hormuz.

But for Asia and Europe – in addition to being an inflation problem – it could also turn into a supply problem if the blockage persists, since these economies receive a substantial portion of their supply through the Strait of Hormuz.

Stocks in Asia plunged, particularly in Japan. The Japan’s Nikkei 225 plunged by 6.9% at the moment. Since last weekend, it has plunged by 12.1%. Other major markets took a smaller hit, at the moment:

- Hong Kong’s Hang Seng: -2.5%

- China’s Shanghai Stock Exchange: -1.2%

- India’s Sensex: -3.0%

- Singapore: -2.7%

The comical Kospi, a tiny stock exchange that had spiked like a meme stock through February, is down 7.5% for today at the moment, and by 19% from its peak at the end of February.

US stock futures are all in the red at the moment:

- Dow futures: -2.1%

- S&P 500 futures: -2.0%

- Nasdaq futures: -2.3%

The US Treasury 10-year yield jumped by 6 basis points in overnight trading, to 4.21% at the moment, in slow recognition of the inflation problem coming its way.

For the US, it’s another price shock, not a supply shock. In 2024, the US imported about 0.5 million barrel per day of crude oil and condensate through the Strait of Hormuz, the lowest in nearly 40 years, accounting for 7% of total crude oil and condensate imports and for only 2% of US petroleum liquids consumption, according to the EIA.

The US is the largest producer of crude oil and petroleum products in the world, and exports more than it imports.

US refineries import crude oil and export diesel, gasoline, jet fuel, and other petroleum products.

In 2025, the US exported 10.7 million barrels per day (MMb/d) of crude oil and petroleum products.

Of the 6.7 MMb/d of petroleum products that it exported, 2.8 MMb/d were finished motor gasoline, distillate (such as diesel), jet fuel, and petroleum coke; and 3.1 MMb/d were propane, ethane, butane, and natural gasoline (a liquid hydrocarbon mixture of pentanes and heavier compounds that is blended with gasoline to change the ratings for octane and vapor pressure).

Even refineries in “oil island” California are doing it. The US exported 1.1 MMb/d of petroleum products, mostly diesel and gasoline, to Mexico (here is the WOLF STREET discussion of US production, imports, and exports).

So for the US, this is a “price shock” – another one of many, the last oil price shock having come in 2021 through mid-2022.

It’s not a supply shock, such as the US experienced in the 1970s, when the Organization of Arab Petroleum Exporting Countries imposed a total oil embargo against countries, such as the US, that had supported Israel during the 1973 Yom Kippur War. At the time, the US was critically depended on this supply, and shortages arose, along with price spikes.

But for Asia and Europe it could turn into a “supply shock.” If traffic through the Strait of Hormuz doesn’t recommence relatively soon, it would hit supply at the local level. They have strategic petroleum reserves, and other storage facilities. So for some time, there will be enough supply. But eventually, supply in those areas is going to take a hit unless traffic through the Strait of Hormuz resumes.

Not all crude oil from the Middle East goes through the Strait of Hormuz: Saudi Arabia and the UAE have large-capacity pipelines that bypass the Strait of Hormuz. The EIA reported:

“Saudi Aramco operates the 5 million-b/d East-West crude oil pipeline, which runs from the Abqaiq oil processing center near the Persian Gulf to the Yanbu port on the Red Sea. Aramco temporarily expanded the pipeline’s capacity to 7.0 million b/d in 2019 when it converted some natural gas liquids pipelines to accept crude oil.

“The UAE also operates a pipeline that bypasses the Strait of Hormuz. This 1.8 million-b/d pipeline links onshore oil fields to the Fujairah export terminal in the Gulf of Oman.

“The pipelines do not typically operate at full capacity, and we estimate that about 2.6 million b/d of capacity from the Saudi and UAE pipelines could be available to bypass the Strait of Hormuz in the event of a supply disruption.”

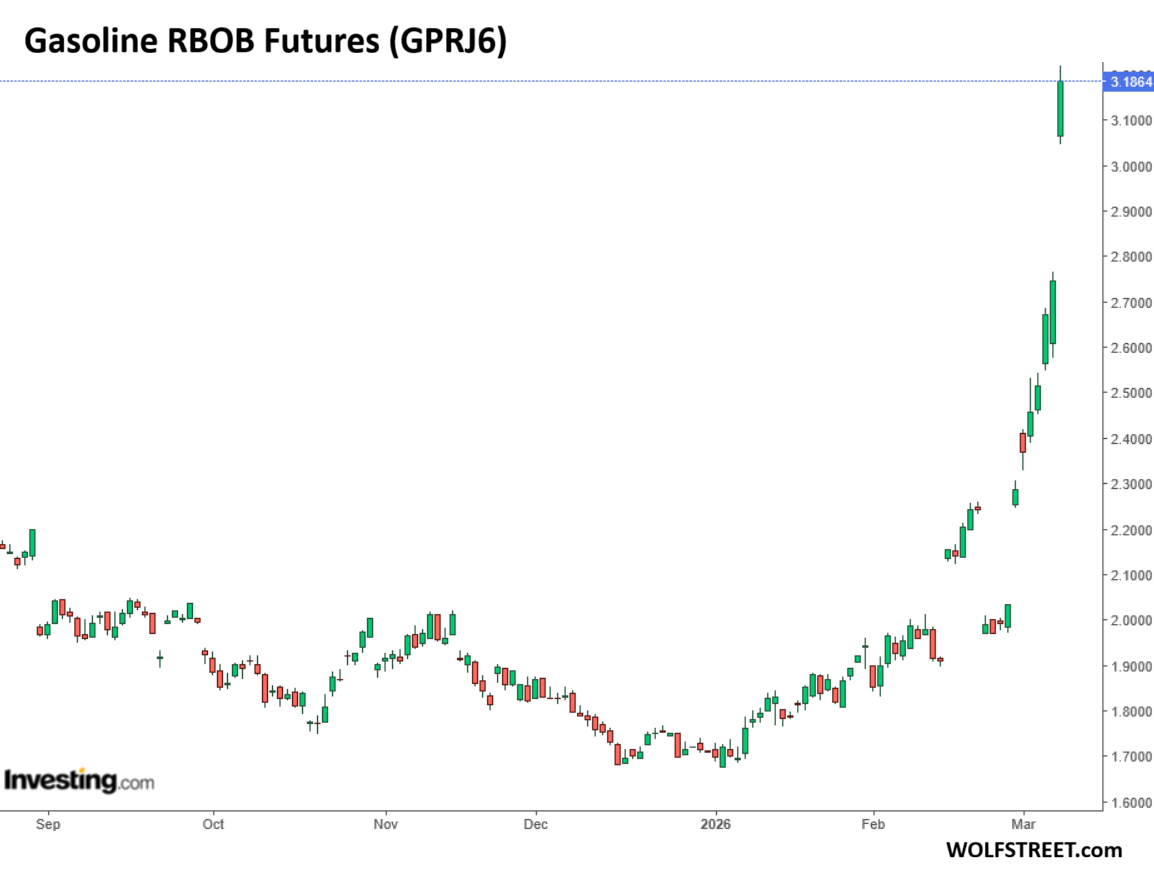

The “price shock” in the US becomes inflation quickly. Spiking oil prices drive up consumer price inflation, such as measured by the Fed’s preferred PCE price index or by CPI, in two ways: directly very quickly, and indirectly over time.

Consumers get hit directly and immediately by spiking gasoline prices – and they have already started spiking, though the supply situation is unchanged.

Gasoline futures spiked by 16% from Friday, amid huge volatility, to $3.18 at the moment in overnight trading on Sunday. They have been rising all year, from about $1.71 at the end of December (daily chart via Investing.com):

Consumers may get hit indirectly by higher fuel prices as shipping costs rise that companies eventually add to product prices or shipping charges.

Airfares are heavily dependent on consumers being willing to pay higher fares, but a lot of airline travel is discretionary, and consumers tend to delay travel, or forego it, when fares are too high, and as demand sags, airlines end up cutting fares and eating the higher fuel costs – the portion they didn’t hedge – and lose money, and their stocks crater all over again.

Ground transportation prices, such as rideshare fares, could eventually rise.

The huge petrochemical industry in the US is a massive buyer of petroleum products. It produces all kinds of materials that form the basis for plastics, synthetic fibers, building materials, fertilizers, lubricants, adhesives, and many other products. The industrial giants in the petrochemical industry buy their products largely with long-term contracts and are not directly impacted by sudden spikes in futures prices. But if those futures prices stay high enough for long enough, it will impact their costs.

So the all-items PCE price index and the all-items CPI for the month of March, to be released in April, will reflect the price spike in gasoline in March. The indirect cost increases will be slower to come to the surface.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Maybe this will be the pin that pop the market bubble finally….well at least pop the AI bubble if nothing else….on the other hand, a week in, this can get real ugly real quick….I think the way things are playing out, it might just give our usual FOMO, buy the Dip peeps a second guess and second pause before resuming BTFD momentum…

Either way, tomorrow’s market will be interesting, bloodbath ensured….wasn’t someone recently declaring, we should be talking about the Dow at 50k? oh the irony…

If markets drop below last April’s tariff tantrum, then you’re onto something. We have a long way to go before dear leader TACOS though.

Yeah good point and unlike tariff, I don’t think our DL will be able to TACOS his way out of this one as easy as tariff which is strictly within his control. He unleashed this beast or let the genie out of the bottle and there might not be any path to put that genie back in….the market and decades of forever optimism might have us off guard from one fell swoop…

Sudden inflation spikes are really nasty because wages don’t immediately jump with inflation. During the last inflation spike in 2021/2022, wages rose a lot, but didn’t keep up with the spike in inflation and fell behind. When inflation softened after mid-2022, wages continued to rise, but faster than this cooling inflation, and it took two years before wages caught back up with inflation.

With inflation accelerating in recent month, and wage increases cooling, it has been nip and tuck. So the inflation coming our way will outrun wages once again.

The volatility is just crazy. Like I said, “Things can get a little crazy in the futures market.” WTI has now plunged $16 from two hours ago and is back at about $100.

I’m seeing reports of Japan releasing its oil reserves for the first time, and G7 talk about also tapping reserves. FWIW, that seems to have coincided with the futures drop from about 118 to 104.

The entire market has been crazy for months with whipsawing becoming the norm. A single story can either calm or spook the market. Thankfully interest have been high enough to just watch from the sidelines. Unfortunately if inflation pops like 2021, nothing is safe from losing value.

VIX (Stock volatility index) spiked to 30 today, values it only reaches in times of crisis. Last time it reached this level was the tariff scare in April. Extreme values of over 50 are only found in big shocks (global financial crisis of 2008, COVID shock, and, surprisingly, this past April briefly).

sure glad US has full SPR – ooops it’s empty

thanks joey biden

1. When Biden took over, it had 638 million barrels in it. Now it has 415 million barrels in it. So not “empty.”

2. under Biden, the SPR was used to push down prices; same as the discussions and decisions now underway under Trump.

3. The peak of the SPR was in 2011, and then oil was released in small amounts over time since it was decided that the US, with its massive oil production now, would no longer need it as much. By the time Biden took over, it was down by already 90 million barrels.

4. the US isn’t going to run short on oil, as it did in the 1970s, so from a supply point of view, the SPR is not needed. But it’s good to have to hammer down this kind of crazy price speculation in the futures market.

I’m already tacking on $50 fuel fee to work daily

expect others to do same

can’t wait to see how much product prices skyrocket

companies already said they were going to raise prices

now they have cart blanche to do so

Hope people trade in those silly huge work trucks they drive so fast in.

It’s a kid trend now. Filling one of those up at 40% higher gas prices, has to suck.

Sufferinsucatash: once all the young men start selling their grocery getters, tradesmen will have an opportunity to buy a gently used truck at a discount.

Bubbles are psychological beasts – The mindset behind this one has escaped me for some time. This one has proven resilient. But someday it’s going to pop.

Interestingly, if you overlay the accumulation/distribution study on SPY, QQQ, DIA, IWM and HYG on shorter time frames, you see a positive divergence starting back on 2/26. Seems like there are some in the market that believe, at least for now, that this will get resolved shortly. I’m watching this closely to see if this positive divergence holds up.

The price jump is due to uncertainty, not to an immediate shortage. In fact, there is at least 7 months of oil available at current use rates. This time provides opportunities for additional sources to come on line – Saudi Arabia has already announced increased production. As always, when uncertainty decreases, prices decrease, Straits closed or not.

If the war spreads, more oil production may disappear. This risk is being priced in.

Oil flows until pipelines get bombed or sabotaged.

Ukraine cutting of Hungary and Slowakia from Russian oil is a sample of that.

Geopolitical tensions are now having a tangible effect on the general public. It’s not the first one in my lifetime, but I hope it isn’t the last. Lots of misinformation online in the last few days, I’m glad you’re reporting with hard statistics Wolf, I hope cooler heads prevail during all of this.

Finally.

I was like where is the wolf report on The Biggest Issue in 20 years?

The Middle East is on fire. Not good. Not good.

I already discussed much of it here 5 days ago:

https://wolfstreet.com/2026/03/03/oil-jumps-but-its-not-the-1970s-anymore-us-crude-oil-production-hits-record-net-exports-soar-imports-decline-further/

I swear I blink and miss so much!

A flurry of activity.

Suffer,5 days makes a world of difference in war,with straight at least a shooting gallery and oil refineries being attacked many nation wide with desalination plants next being hit the rise is expected.

On average gas in my area has as of Sunday on average gone up .50 a gallon,will be keeping a eye on this

Well at least Joe Biden isn’t president anymore. Yes, the world is burning down, but the boredom was unbearable for American attention spans.

For Europe the more pressing concern might be access to LNG rather than oil. With Russia gone as a key supplier the Europeans turned to LNG to fill the gap, believing in security of supplies from Qatar and US.

However, with storages running low and Qataris declaring FM the Europeans are really held over a barrel here as they are competing with Japan and Korea for supplies.

They could just burn scottish moss.

A wee bit laddie

To add to the misery, in the EU wages haven’t kept up with inflation (currency depreciation) since ‘price compensation’ (what is called COLA in the US) has been abandoned in the 1990’s.

One example where i live: counsel taxes have gone up 70% in the past ten years. Mainly because house prices went up. Our income has gone up only 17%, despite promotions and moving to better jobs. BTW the house is still in the same place, doing the same job.

Fortunately we’re headed out of Winter.

Europe is buying expensive oil. Asia will get oil from russia if all else fails. They manage.

But the poor countries, especially those without strategic oil reservers will suffer a lot. If transportation was 50-80% of your wage before the current price shock, you can imagine how they will struggle now. And those are the places where the current price level means more power cuts for electricity, people skipping school because of transportaition costs and farmers going without fertilizer.

Anyone paying attention to geopolitics for a couple of decades could see oil, minerals, and precious metals reaching these levels. It’s all been in the making, thanks to the worst crop of western politicians.

Should have taken them out in the 70s

Buy Exxon!

I did, at its low a few years ago, while everyone else was buying AI speculative. Now that the 4 Gulf Countries are going to pull the AI investment of over 4 trillion from Trumps build US crap. HAHA. I’m a retired Geologist, and the world still runs on oil and natural gas!

Elon musk gonna double Tesla prices.

No gas needed!

One thing you are forgetting. We have a very stable genius running the show here. Someone told me, “Sir, this is the smartest man that ever lived.” This war should be wrapped with a total and punishing victory within the next three days.

Haha gaslighting worked so far until it doesn’t… Who know..this might be one those FAFO moment

“The huge petrochemical industry in the US is a massive…” campaign donor to the every single Republican president since the 80s, ALL of which launched large wars in the Persian Gulf, causing petrochemical prices to spike.

FTFY.

Trump is no different than Dubya. Invest accordingly.

That makes zero sense. Crude oil byproducts are a feedstock to petrochemical companies. They want oil to be at its cheapest.

Petrochemical products don’t spike in price as fast…ie that shirt or plastic container you are buying takes a while to spike.

One thing to keep in mind about this war is that Iran doesn’t have very many friends over there except militant groups.

It doesn’t mean it won’t be volatile or doesn’t mean you have to agree with it, but they are current launching missiles into Qatar, Saudi Arabia, UAE, and Turkey. Not exactly a good place to be.

Now a ground invasion of Iran would be difficult if not impossible.

Also, keep in mind that Iran has been waging a “war” against us since the 70s.

And remember that there have no American casualties in that “war” against us, except for this week activated by our murder campaign.

Bro, that isn’t even close to true. They sponsor Hezbollah who has killed American citizens and military. They sponsor Hamas, the Islamic Jihad Group, and the PFLP.

You don’t have to like the actions taken lately, but you need to acknowledge that Iran isn’t some “leave us alone, and we’ll leave you alone” kind of country.

Yes. Terrorist groups get their plastic explosives and other ordnance from Iran and other rogue nations. Otherwise, they’d have to make things in pressure cookers like the Boston marathon guys and the bombs would be a lot less deadly.

Your comment is either uninformed or disinformation. Significant casualties have been occurring since the 1983 bombing of the Marine barracks in Beirut. In that one incident, 241 service members who lost their lives.

Then perhaps we should invade Vietnam next. Significant casualties occurred there in the 1970s.

Chris B:

Maybe you missed the “have been occurring since” part. You might have had a point if not for the 2000+ casualties in Iraq due to roadside bombs and the actions of Hamas, Hezbollah, Houties, etc… and there is of course the various direct attacks on US bases.

It’s not the same at all.

BTW, my intent was not to say the current action in Iran was the right thing to do. It was to respond to the “no American casualties” comment. We have been at war with Iran for decades whether we recognize that our not. If you don’t believe me, just ask the Iranians.

The mission in Iran is morphing into a repeat of the IRAQ debacle of 2003 or worse. Now we’re hearing this BS about freedom and democracy for the Iranians, women’s rights in IRAN, big profits for the military industrial complex, CEO’s meeting the President in the oval office, domestic terrorism threats with neighbors reporting on neighbors, threats of ground troops etc, supplimental spending requests that blow up the Federal Budget deficit, inflation and interest rates increasing. It’s going to get ugly if it is not ended immediately. One thing is certain. The midterms will be a disaster for the party in power who started this war.

I mean I know you have been wanting to wishcast a downfall, but let’s stop acting like the vast majority of Iranians want a different government. It is an oppressive regime who recently killed 35,000 of its own people.

Eric86,

You might want to turn off Fox, CNN and BBC. The history of Iran is very complex and none of this is surprising. Take it back to 1953 and everything since then. I am no fan of Iran but I appreciate they are the one solid country that is against US imperialism in the area. There are a lot of oppressive regimes in that area, and Iran hardly is at the top of the list, and don’t forget we created modern day Iran through our actions. We live in a world where the only thing that keeps you safe is nukes.

“One thing is certain. The midterms will be a disaster for the party in power who started this war.”

I don’t think that’s certain at all. The Ruling Party controls the media, so they can convince at least a third of us cell phone drones that whatever problems we’re experiencing are the Dems’ fault, even when they’ve been thoroughly routed from power.

Side note: Look how quickly the Epstein files fell off the front pages when stuff started blowing up. Trump has ensured the midterms will NOT be about his child sex cabal. So the war will end, oil prices will go back down, and the stock market will go up by November. Meanwhile the Dems will have dropped the ball by not having a coherent message.

Any message really. The only message right now from our Dems is (wait – what’s Trump doing right now?) “We don’t like that!!”

The uniparty runs the show. Sure they’ll distract us with an R or a D, to keep us fighting amongst ourselves.

“Ruling party controls the media”… you are so confused. The media is very left progressive, certainly not controlled by Republicans. Second, everyone is entitled to opinions, but facts matter. So do words. This is not a war. It is a conflict. Just as Korea, and Vietnam. That’s why we read Wolf Street, he is very articulate in his language, it makes a difference!!

Sec Hegseth said this a war for Jesus.

> “The media is very left progressive”

This hasn’t been true in my lifetime, though it was closer to the truth 20-30 years ago than now.

> “This is not a war. It is a conflict. Just as Korea, and Vietnam.”

Hey man, you said it. Not sure that came out the way you intended.

“Dems will have dropped the ball by not having a coherent message.”

This administration has already put out 4 different versions of the reasons for attacking IRAN. Some may make sense in the long term, like getting rid of the Nukes pre-emptivey, but for now it all looks like a Gulf War 1.0 and IRAQ War 2003 all over again. They are moving the goalposts with each passing day. It will take a miracle to get out of this mess which they have created.

The difference with Iraq is that this is allegedly supposed to only be an air war. If we’re doing regime change then how is that going to work? Just keep bombing them until an acceptable leader appears? Nobody seems to know… everyone in this admin keeps contradicting themselves and each other.

Is it possible that the goal is simply to disrupt the oil market and eliminate competition for US frackers and Russian shadow exporters? As well as hand the military-industrial complex another $50 billion? And as a bonus, distract from Epstein? Just make a mess of things over there, declare victory and walk away. That would be my cynical take.

Mankind has been the same since the beginning.

It may be the Thucydides Trap or the Strauss–Howe cycles, etc., we are now experiencing.

This current struggle will resolve but what lies ahead will be something similar to history we have seen before.

This is why God made beer.

Why are US gasoline prices affected at all when practically zero oil products sold in the US come from anywhere other than in the US?

manic speculation, same as meme stocks, or actually many stocks, bitcoin, gold, silver… America has turned into a gambling society where the gamblers gang up with each other to drive the price higher until someone decides to get out, and the others follow.

Correct. And the ticker symbols on the stock exchanges represent nothing more than gambling tokens. As gamblers, we don’t give one shit as to why the tokens move. We just want the volatility. Here’s a great example of gambling token Battalion Oil [BATL]. Don’t eff’n play this highly volatile token unless you know what the hell you’re doing. Buying and holding this token overnight is the very definition of GAMBLING!!!

By the way, always enjoy seeing a candlestick chart from time to time in your articles!

It does feel like tulips bulbs all the way down…for some time now.

Partially because it’s a world market. If prices are going up overseas, at some point, it’ll make more sense to expert more U.S. oil at the higher overseas prices than to sell it domestically for the low prices.

Unless you prevent goods from moving across borders, what happens elsewhere has an effect here.

Not in any way other than with deranged manic inane speculation.

Congress, in a bipartisan effort in 2015, lifted the ban on crude oil exports originally signed into law in 1975. That effectively made US prices match world prices, maximizing shareholder value in the US oil industry.

That affects only a very TINY amount of petroleum products.

Prices are set at the margins sir.

It’s a global market which has both its pros and cons

Because there’s a world market for oil. The people who lost access to their normal supply have started bidding up prices. Some of it is bound to be panic buying and speculation, but if there is less oil available, prices should be expected to rise somewhat everywhere.

Appears a ticket for US oil companies to make huge profits. Supply the same, prices go up, demand the same – gas prices go up for no reason other than the world market forces it up. And, they can pump more for export at an inflated price. A recipe for printing money. A perfect storm for US oil companies.

I believe it was Joe Granville who said that in a bull market the last sector to move is oil and oil stocks. Could this be the end of the market rise since 2008-2009?

The port of Fujairah is just past the narrowest point of the Strait of Hormuz and in easy reach by Iran. Yanbu is not as close but closer than Tel Aviv.

Other aspects to keep in mind is that traffic through Hormuz goes both ways. The Gulf States need finished commodities including food, medicines, machine parts, and a host of others necessary for daily life.

“For the US, it’s another price shock, not a supply shock”

How about those petro dollars not re-cycling back? even if long term, any impact on the printing press and never ending barrowing cycles?

There is no such thing as ‘petro dollars’ as oil and petroleum products amount to less than 5% of US Dollar global transactions.

There are no petro dollars. The US sells more than it buys.

Are you calling Professor Jiang a liar? 😅

Serious question – have you heard what this dude is saying about the imminent demise of our economy due to petro dollar concerns…. … he’s full of shit, right?

My BS indicator is ticking to the right

Ignore that dude and probably best to block his channel. His view and take is very problematic and even if he got something right, chalk it up to broken clock being right rather than he knows wtf he is talking about. His credential is questionable at best and his information is either straight out deceptive with an agenda at worst, misinformed at best…

He is another one of those that thanks to souless YT algo, get prop up everywhere on feeds. Fear mongering and disinformation get view and attention unfortunately….

Howdy Youngins. CASH is King and always will be for squirrels. Don t let the StockBOYS control your life…Become a squirrel member and you will laugh all the way to the bank at the current news/war/stock/inflation/Govern ment/FED nonsense. YOU could then live your life doing what you want when you want….

Give it another month unless unconditional surrender occurs soon and might be opportunities to buy in. After all, we do have a president who was against foreign wars but perhaps overshadowed by AIPAC. Amazing the list of bad things that happen as a result of unlimited lobby money.

Between you and me, when those missiles hit Turkey … it’s a done deal. This ain’t gonna last, Article 5 or not

Seeing as the Nasdaq just touched green not too long ago, when are we going to give the U.S. markets just a slight bit of credit?

How many hits has it taken and it just keeps stampeding forward? And valuations are trending lower than PY for many lucrative sectors.

If we hit new highs in April I will not be shocked. Still undervalued imho there some crazy prices out there right now. Another week or two of media doom and gloom parades is gonna set us a pre-boom clearance sale. Keep one foot in I’d say, and nimble to jump back in at moments notice.

Cheers!

Bit early in the day to be using hallucinogens, huh?

It’s funny to me because I said the same thing leading up to “Liberation Day”, was insulted and disregarded then…

Feels familiar. We’ll see.

I’m actually green today (as of now) but having a significant position in Circle helped

S&P in the green

Nasdaq in the green

And not only a good day for circle, but my super secret alpha stock #1 holding just went green as well putting me well into the green.

Are yall _sure_ it’s all going down?

I know it goes up and down, could be down tomorrow, S&P could (by sentiment) drop to the mid-5ks 🤷♂️ but would it deserve that?

Me says no – would be one heck of a buying op so stash some USDC and hold 👍

Don’t forget to send your special gift to the plunge protection team. They came to the rescue after being on vacation last week

YOLO, FOMO and Hopium continue for another day….rinse and repeat…

Phoenix_Ikki

You have such a doomer attitude on everything. If you are long term in the stock market you make money. Crash or not. If you sit on the sidelines you don’t make anything. Simple as that

I didn’t say the market wouldn’t end in the green. The algos do what they do. I was responding to your point that the market is undervalued. There’s no metric under which that is reasonably the case.

Eric86, you’re taking the past 15 years and projecting it to the future. Schiller P/E is around 40. To expect to “make money” over the next 15 years either assumes that this type of P/E expansion can persist indefinitely or that we’re going to have crazy increases in productivity. I am skeptical of both.

TSonder305

And you’ll probably end up being wrong. A lot of people don’t even use P/E ratios anymore, and comparing to historic P/E values is flawed. It is a good gut check, but other than that, it doesn’t mean much.

Accounting rules are different, interest rates are different, the companies themselves are different, and there is more money than ever in the stock market, both domestically and internationally.

Over 15 years? I’m very confident that I’ll make good money over 15 years in the stock market. Even if you only ever invested at the peak of every cycle, then you’d still have a decent return today.

TSonder305,

I never said I’m taking the last 15 years. You put words in my mouth to prove your point. Strawman argument.

Returns by decade

1920s: +18.2%

1930s: -0.1%

1940s: +9.2%

1950s: +19.4%

1960s: +7.8%

1970s: +5.9%

1980s: +17.6%

1990s: +18.2%

2000s: -0.9%

2010s: +13.6%

2020s (so far): +14.5%

So 2 decades in the last 100 years have had no return. I’ll take that bet.

All of that is just another way of saying “This time is different.”

What has propped the stock market up over the past 15 years was a combination of ZIRP/money printing and a belief that the Fed will return to that if the stock market drops. That’s it. It has nothing to do with “more money in the market,” GAAP/IFRS or anything else.

People don’t care about valuations as long as the market is going up. When the market stops going up, for whatever reason, then valuations start mattering again. The difference between buying at the previous peaks and now is that the Fed no longer can drop rates to 0 and start printing money again without the admission that it intends to cause massive inflation.

In 2009-2013 or so, they had the cover of “it won’t cause inflation” and in 2020, they had the cover of “it won’t cause inflation, and even if it does, COVID requires it.” Now they won’t. If they start printing again to prop up stocks, watch yields blow out.

Answer me this. If it’s such a sure thing that stocks will only go up, and that valuations will never matter again, why does anyone sell when you go to buy? Why would anyone sell any share at any price if prices are practically guaranteed to be higher in a few months time?

@TSonder305 – check the ex-Tesla; it’s $1.5T market at 372 PE is a massive distortion.

There a few other notable outliers – Palantir’s another

When you scrub out the outliers you may be surprised what you find are the valuations of what remains…

Worth a look 👍

TSonder305

Again, you are answering arguments I didn’t make.

“Answer me this. If it’s such a sure thing that stocks will only go up, and that valuations will never matter again, why does anyone sell when you go to buy? Why would anyone sell any share at any price if prices are practically guaranteed to be higher in a few months’ time?”

I never made that fucking argument. You made that argument up in your head. Why would people sell? Because people miss out on the upside all the time, or they want to derisk, or they are retiring and are derisking, or they have already met their return goals.

Good lord. I gave a 100-year history of the S&P 500, and it has had positive returns in all decades except 2. I’m a long-term investor.

I didn’t pull my money out during COVID. I didn’t pull it out during the 2022-2023 pull-back. I didn’t pull it out after liberation day. If the day comes when bonds look attractive, then I’ll probably move money there.

Shit, I even invested more during the 2022 pullback, and that is now up like 7% but two years.

You can believe what you want to believe. I also never really said “this time it is different” I merely pointed out that just like every “recession” indicator, things change. If you are long term investing and dollar cost averaging, then it doesn’t really make that much of a difference.

Couple of other thoughts on PE – long time investors have long memories. Right? You ask Howard Marks what’s a reasonable PE and he’d probably tell you over 16 for the average company is too much.

But things HAVE changed.

Beat expectations – we sandbag earnings nowadays. Beat rates routinely hit 80% these days. Go back two decades and your beat rates drop to the 70’s; you have to go back to the early 90’s to see beat rates below 50%! No one wants to get caught overvaluing, so we perpetually undervalue when we setup the hurdles.

The next factor is cumulative – the Beat +%’s are routinely higher. Same thing over time – not only do we have more beats, but the beat percentage average has trailed up such that average beats these days could be 15-20% as opposed to the more modest beat %’s of the past decades.

This on top of the PE outliers which make the market look overvalued because some companies just have absurd PE’s – huge companies with large market caps overvalued make the entire market look overvalued. If you can get a look at the S&P ex-Tesla valuation would recommend (believe Matt Ceminaro produces a chart you can review).

On top, you can add that we have a number of high profile stocks that have historically had “high” PEs that have routinely clocked in at “still undervalued” – there’s an interesting case study re: NVIDIA on this specifically. It’s held a PE that many would view as egregiously high, and yet historically if valued by that high PE it’s still been consistently undervalued. The S&P has a number of companies like this with not only justified high PEs, but historically high PE and proven undervalued.

Lastly, if your position in September was that stocks were overvalued, you may want to check again. We have had significant PE retraction across numerous segments including the overweighted Info Tech sector. If you thought it was high last year – well, it’s actually down significantly… so check the Sell By date on your valuation multiples assumption. Info Tech alone has significantly plummeted over the last 6 months but you probably didn’t notice because the market was hitting new highs. Thats what broadening does, and the broadening happened because the S&P 493 were _undervalued_

So – I don’t think it’s as clear cut as you may think regarding valuations.

Tis never too early for shrooms!

The wheels are wobbling:

Inflationary pressures have returned and are accelerating

Real estate market is dead or frozen if you prefer

10 year is stubborn and has gone up along with mortgage rates

Job market just had a horrific report & 5 of last 9 months showed losses

War with Iran with the accompanying oil price shock and now what sounds like a budget busting disastrous regime change policy

Private credit showing cracks; assets marked from 100% to zero and investors gated.

Stock market indexes have gone sideways for months

AI buildout and commercial construction are doing well for now.

Yeah, sounds like a great time to buy!

When asked, I am sure majority of RE agents will still tell you it’s great time to buy even with what you cited above..lol

The wheels wobbled and fell off during 2022 and you could make these same arguments. The SP500 was at 4800 and then lost 25% of its value down to 3600.

The point? Drawdowns are normal and dollar cost averaging wins in the long run. Time in the market is more important than timing the market. Stop being reactionary

I’m hoping for a healthy 6-12 month slow fall to 20% off discount.

DCA in with the old 401k and make some investments at a discount. While all the suckers are selling.

I probably need to do the same for a lot of mine. I have some good cash. I’m waiting for a larger pullback though. Should just do it

In 2022 the Nord Stream pipelines sabotage happen making Putin not happy. I am sure he would like to repay the favor to the west, Saudi Arabia pipeline to the Red Sea gets sabotaged or gets hit by a bomb, oil prices go to 200$

I had a limit buy order for the VOO at 600….and now it is at 624. Should have bought at 609. Oh well.

MW: Stocks close higher after final-hour reversal, as Trump signals Iran conflict could be nearing end

DJIA +0.50% SPX +0.83% COMP +1.38%