It might not make much difference now, but it would during a housing crash.

By Wolf Richter for WOLF STREET.

Trump is pushing Congress to pass legislation that would block landlords with 100 or more single-family rental homes from buying additional existing single-family homes. The idea is to prevent a surge of concentrated buying in a handful of markets that would distort prices further. These landlords could still build their own single-family rentals, or buy build-to-rent developments from builders – thereby adding to the housing stock. But they could no longer buy existing homes.

Even if Congress passes legislation to that effect, it won’t have a big impact on the market currently because:

- The very biggest SFR landlords have turned into net-sellers of existing homes they’d bought in 2012 and afterwards, and they’re now building their own, or are buying build-to-rent developments from builders.

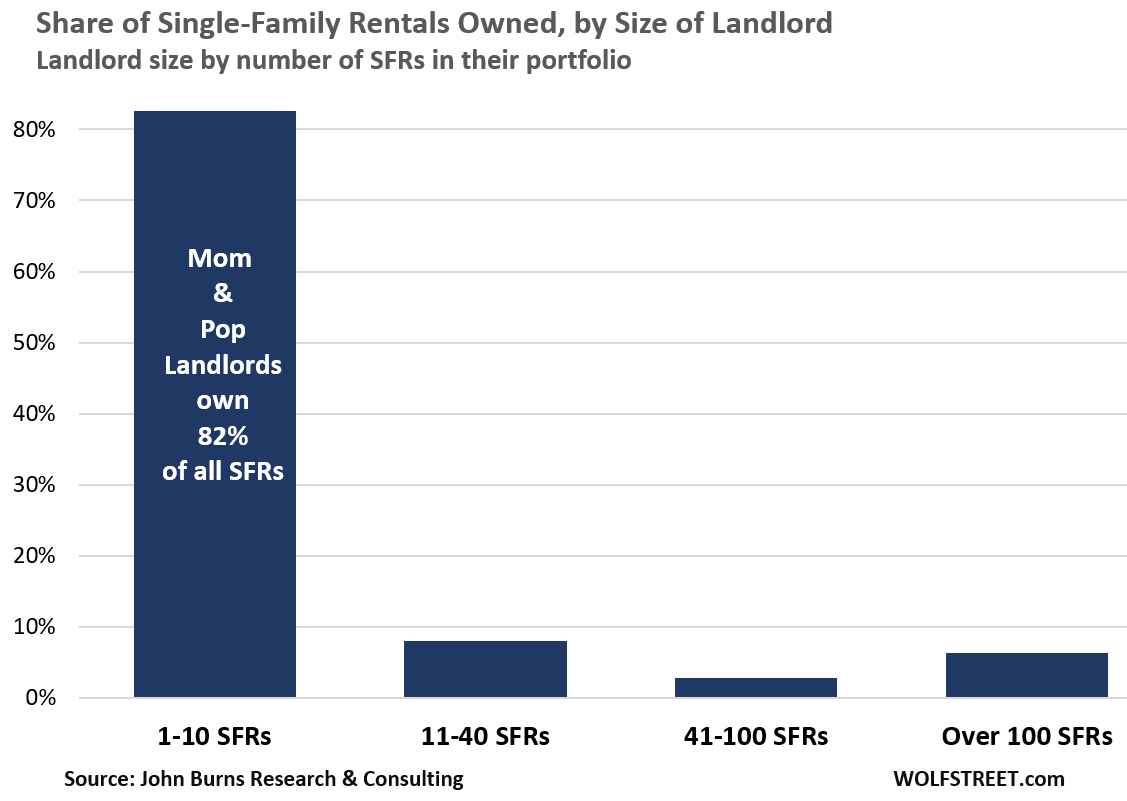

- As a group, by far the biggest SFR landlords are mom-and-pop landlords, and always have been, and they would not be impacted by the ban.

Only about 6.3% of the SFRs are owned by landlords with 100 or more SFRs, according to John Burns Research and Consulting. Only those landlords would be affected if the ban becomes law.

But mom-and-pop landlords with 1 to 10 SFRs own 82.6% of single-family rental properties. That’s the force to be reckoned with – and always has been (data via John Burns):

Owning rental properties has always been a classic investment choice for retail investors. They have been buyers of single-family rentals through thick and thin. Many homeowners became landlords when they bought another home, moved into it, and rented out their prior home, instead of putting it on the for-sale market, and then repeating it multiple times over the years.

But unlike big institutional investors, mom-and-pop landlords are largely invisible, though they represent a mass of buyers that quietly swarm all over the place looking for their next property, and driving up prices in the process.

Huge institutional landlords are relatively new in the single-family rental market, a product of the Federal Reserve’s efforts in 2011 and 2012 to get firms to borrow vast amounts of money at very low rates and buy thousands of homes out of foreclosure to create demand and pump up prices – and thereby provide relief for the banks.

This created a handful of gigantic single-family landlords and a bunch of smaller institutional landlords with heavy concentrations of SFRs in a few markets. When they went on their concentrated buying binge in 2012 and on, it did pump up prices.

But in 2022, the biggest SFR landlords started selling some of their scattered-site properties at huge profits after prices had spiked. And they’re not buying existing scattered-site homes anymore; they’re too expensive at current prices that don’t pencil out, and they’re too costly to manage.

They’re adding to their SFR portfolios by building entire build-to-rent developments, or by buying purpose-built SFR developments from builders.

Build to rent has been the hottest trend in home construction for the past four years. Most of these developments have common amenities, and often a leasing and maintenance office, and are less costly to operate than thousands of older maintenance-hungry homes scattered all over the place.

The largest single-family rental landlords.

There are about 11.3 million single-family rental properties. The six biggest landlords own about 430,000 of them.

#1, Progress Residential: “Nearly 100,000” SFRs, according to PE firm Pretium Partners which owns the landlord. Its portfolio of SFRs is concentrated in some markets, with over 12,000 SFRs in the Atlanta-Sandy Springs-Alpharetta metro.

In the years after the financial crisis when prices were low, it bought 65,000 single-family homes “one-by-one.” It later bought portfolios of SFRs from other landlords and Section 8 SFR properties. As prices rose and became too high for rentals, it began to pull back from purchasing homes one-by-one, and since 2022 has essentially ended those purchases.

Since then, it has been purchasing entire build-to-rent developments of SFRs, acquiring 78 build-to-rent developments, totaling over 10,000 SFRs, according to Pretium Partners.

#2, Invitation Homes [INVH]: 97,036 SFRs as of Q4 2025 (86,139 wholly owned plus 7,897 joint-venture owned), according to the publicly traded REIT’s SEC filings.

INVH was founded by PE firm Blackstone during the Housing Bust in 2012 and spun off to the public via an IPO in 2017. Blackstone sold its last shares of INVH in 2019.

Since about 2022, INVH has been selling scattered-site SFRs that it had purchased at very low prices starting in 2012. And it has been purchasing build-to-rent homes from builders.

In 2025:

- It sold 1,356 scattered-site homes for $534 million (average $393,800 per home)

- It purchased 2,410 homes, “almost all” of which from homebuilders in SFR developments, for $812 million (average $336,923 per home). In Q4, all of the SFRs it purchased were built-to-rent.

#3, Blackstone: 62,000 SFR in the US, according to data from Parcl Labs. Blackstone, after it spun off Invitation Homes, got back into single-family rentals by acquiring two landlords: Home Partners of America with 17,000 SFRs in 2021; and Tricon Residential in 2024, with about 38,000 SFRs in the US. Tricon is also a developer of build-to-rent SFRs.

#4, American Homes 4 Rent [AMH]: 60,337 SFRs as of Q4 2025, according to the publicly traded REIT’s SEC filing. AMH, founded in 2012 by Public Storage founder B. Wayne Hughes, was spun off via IPO into a publicly traded REIT in 2013 and in 2016 merged with American Residential Properties.

AMH started its own homebuilding division in 2017, when it pulled back from scattered-site acquisitions. In July 2024, the company announced that its homebuilding division, AMH Development, had completed its 10,000th home in new build-to-rent developments.

In 2025, AMH Development delivered 2,322 newly constructed build-to-rent homes. For 2026, it expects to deliver another 1,700 to 2,100.

In Q4, it sold 646 of its scattered-site properties and held another 1,142 properties for sale.

For 2025, the company booked a net gain of $231 million on the sale of single-family properties.

#5, The Amherst Group: 59,400 SFRs. The privately-owned company is engaged in build-to-rent, bought portfolios of SFRs from other big investors, and bought individual homes and renovated them. It sells renovated homes directly to consumers on its own platform.

#6, FirstKey Homes: Over 52,000 SFRs, according to the company. It was founded in 2015 by Cerberus when it took on the 4,200 SFRs that Cerberus had previously bought from Building and Land Technology (BLT). FirstKey Homes has also become a seller of its scattered-site properties.

But a ban could make a difference during a housing crash.

If home prices plunge far enough, the ban could make a difference in that it would prevent large firms from swooping in and buying up thousands of homes from distressed sellers or out of foreclosure in those markets. Institutional investors have an advantage: they already have the cash, and they have the expertise, they can act fast, and they can load up on properties. And that’s what happened last time. A ban could prevent that.

In cased you missed it: Single-Family & Multifamily Construction: Bring on the Supply just as Population Growth Slows to a Crawl

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I think this problem could be solved in far more simple ways. First, on a local level, states and municipalities can ensure higher property taxes on investment properties.

Two, on a federal level, the 30-year-fixed mortgage, guaranteed by taxpayers, doesn’t need to extend to investment properties. I recognize that it’s hard to qualify at the same lower rates when purchasing for investment, but if you purchased to live in it and then rent it out, you keep your government-supported low rate. Congress could implement some kind of mechanism that causes rates to increase if a previously lived in property is now being used as a rental property.

Or the government could just stay out of it and stop social engineering through tax policy…dare to dream.

” states and municipalities can ensure higher property taxes on investment properties.” Mostly they already do, since they offer various tax breaks to owner-occupants. Certainly they could increase these.

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered.”

– Thomas Jefferson

Curious to see the number of houses for sale during/after the next recession. The Depression caused many forced sales due to county RE tax. I hope I’ve enough cash flow to survive .

Not counting on an IRA as those assets will also be down!

Can anyone explain the possible ramifications from a ban during a crash. It makes sense there would be a difference but I have trouble understanding what the effect would be. Would it possibly be that the housing prices would fall further since there would be less demand due to no large investors?

Yes, it takes away, or at least reduces, a price floor based on ROI.

Start the countdown clock until someone says “Blackrock”…

Anyway, I doubt this will matter. If there’s enough juice in the deals, a manager like Blackstone can create separate entities with 100 each.