“Improving affordability conditions have yet to induce more buying activity”: National Association of Realtors.

By Wolf Richter for WOLF STREET.

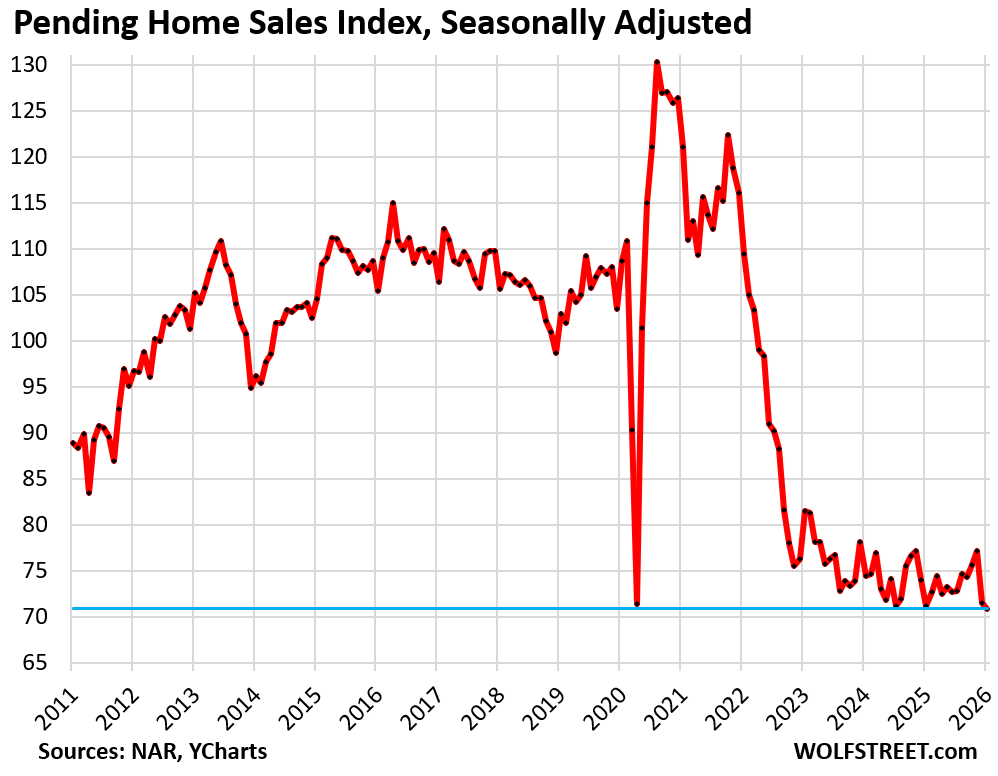

January was bad, following the plunge in December. And prior months were revised lower. Pending home sales, tracking the number of contracts signed in January, declined by 0.8% seasonally adjusted from the downwardly revised December, to the lowest level on record in the data by the National Association of Realtors, which goes back to mid-2010. Compared to January 2011, during the Housing Bust and the first January in the data series, pending sales were down by 20%.

“Improving affordability conditions have yet to induce more buying activity,” the NAR stated.

Pending home sales compared to the Januarys in prior years (historic data via YCharts):

- 2025: -0.8% (year-over-year)

- 2024: -4.8%

- 2023: -13.0%

- 2022: -35.2%

- 2021: -41.4%

- 2020: -34.8%

- 2019: -31.1%

- 2018: -32.9%.

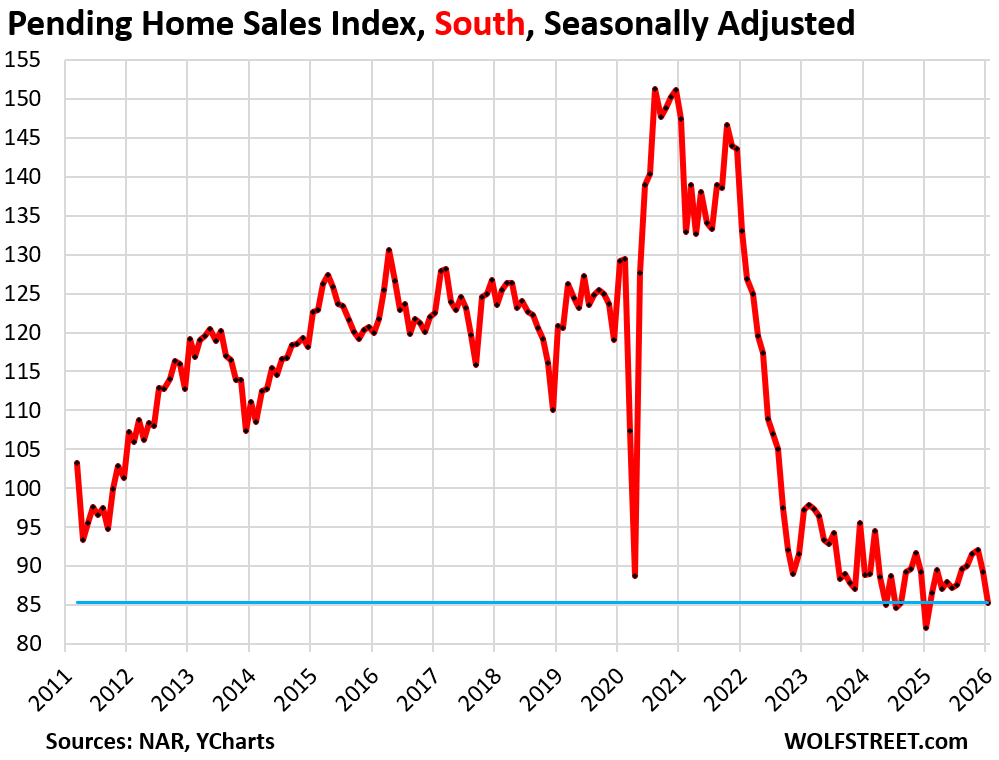

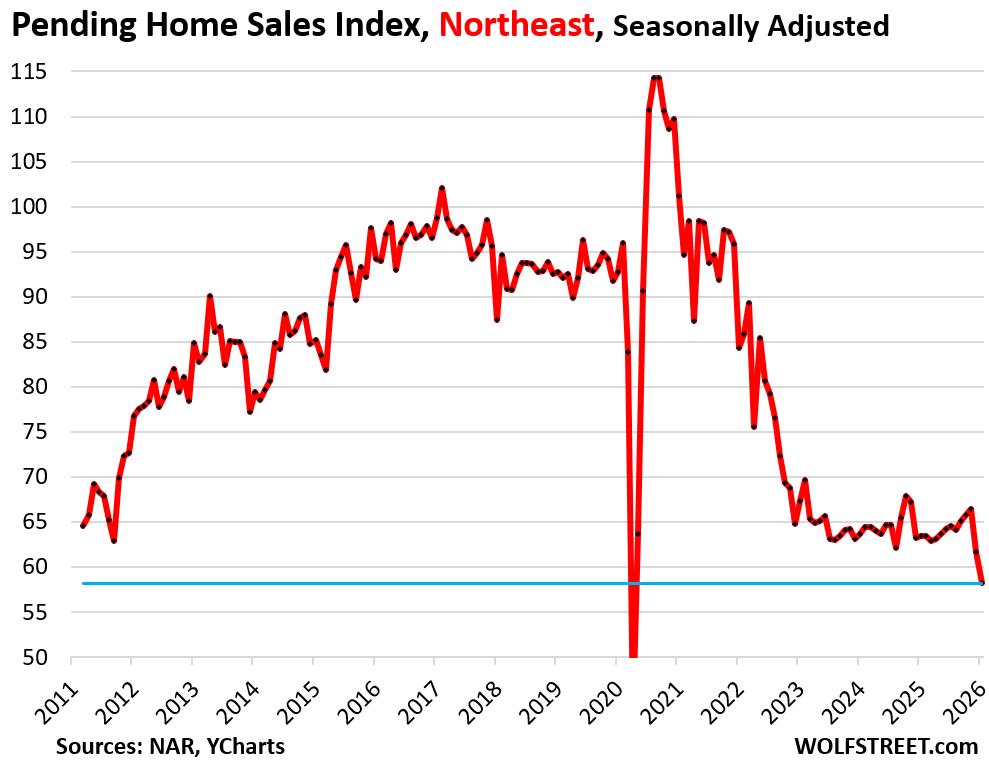

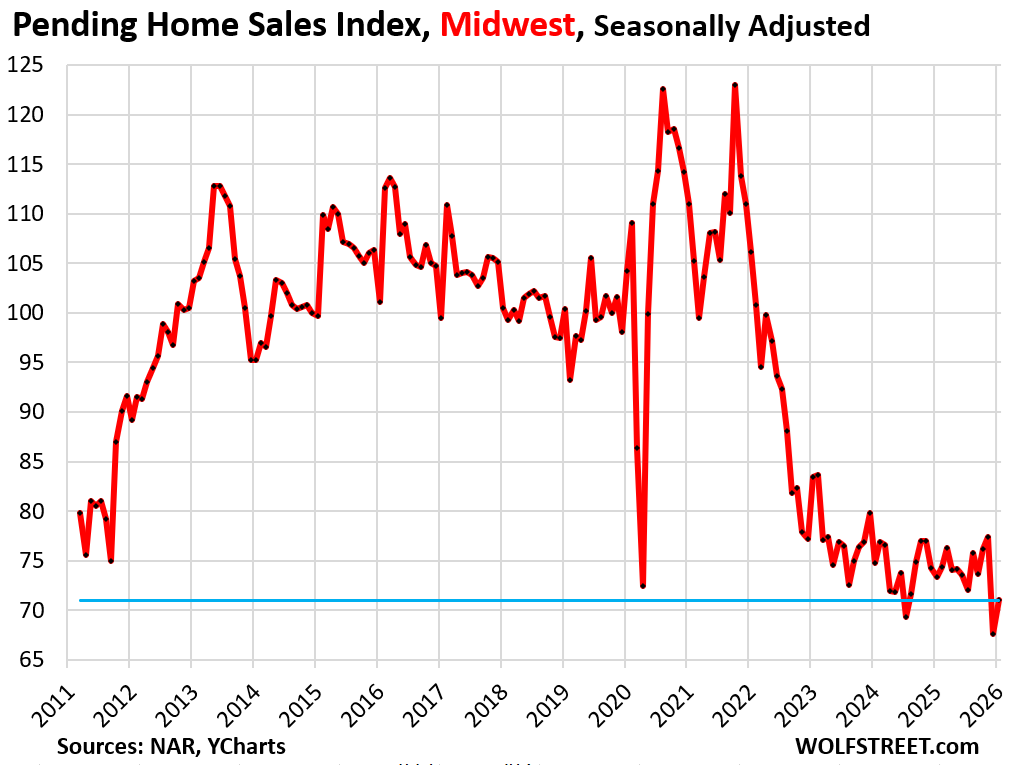

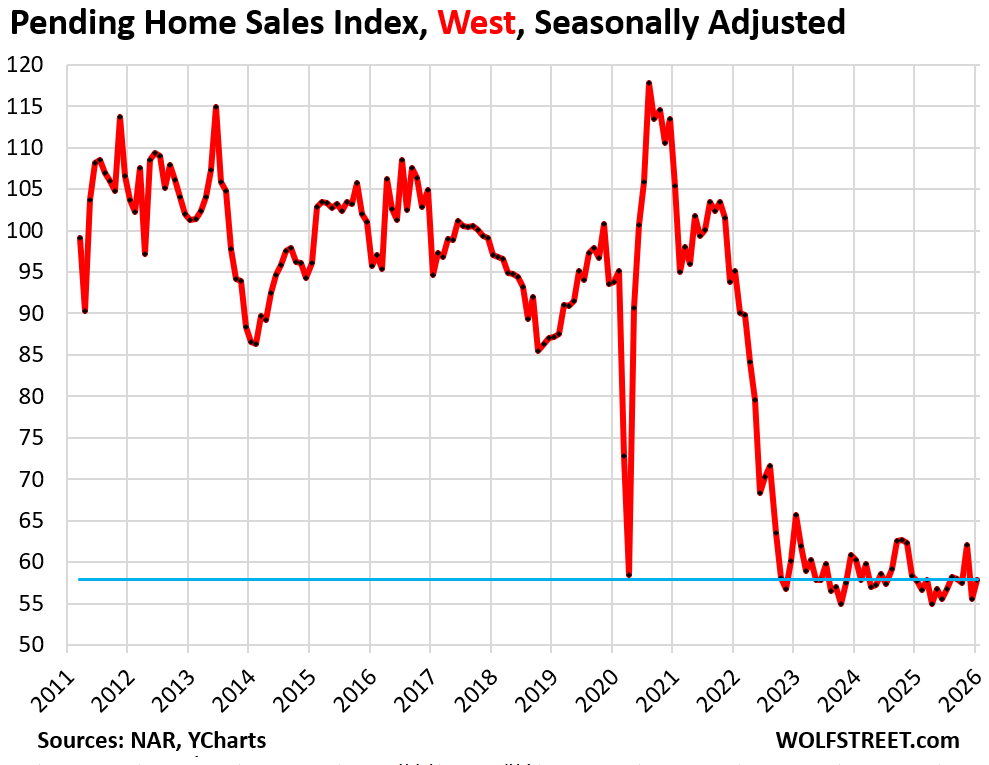

Pending sales dropped sharply in the South and in the Northeast but rose in the West and Midwest on a month-to-month basis, seasonally adjusted, see charts further below. This comes after the drop in December in all four regions.

The metric of pending sales tracks contracts that were signed in January but that haven’t closed yet and could still get canceled because buyers cannot afford homeowner’s insurance, or cannot sell their own home, or for other reasons. The rate of cancellations has been running high.

Pending home sales by region.

A map of the four Census Regions is posted in the comments below.

In the South, pending sales fell by 4.5% in January from December, seasonally adjusted, following the drop in December.

Compared to the Januarys of prior years:

- 2025: +4.0% (year-over-year)

- 2024: -3.9%

- 2023: -12.2%

- 2022: -35.9%

- 2021: -42.1%

- 2019: -29.4%.

In the Northeast, pending sales dropped by 5.7% month-to-month, to the second-worst level of sales on record.

Compared to the Januarys of prior years:

- 2025: -8.3% (year-over-year)

- 2024: -8.6%

- 2023: -13.5%

- 2022: -31.0%

- 2021: -42.5%

- 2019: -37.3%.

In the Midwest, pending sales rose by 5.0% in January from December, seasonally adjusted, to the third-lowest level on record, after the 12.7% plunge in December to a record low in the data going back to mid-2010.

Compared to the Januarys of prior years:

- 2025: -3.3% (year-over-year)

- 2024: -5.1%

- 2023: -14.9%

- 2022: -33.1%

- 2021: -36.0%

- 2019: -29.3%.

In the West, pending sales rose by 4.3% in January from December after the 10.6% plunge in December, seasonally adjusted.

Compared to the Januarys of prior years:

- 2025: +0.3% (year-over-year)

- 2024: -4.0%

- 2023: -11.9%

- 2022: -39.1%

- 2021: -45.1%

- 2019: -33.5%.

The cause of the housing market being this frozen and refusing to thaw is related to the ultra-low mortgage rates of 2020-2022 that ended up exploding home prices to where they’re too high now; and then when those ultra-low mortgage rates went away, they “locked in” homeowners that had those ultra-low mortgage rates who now cannot afford to move or don’t want to move because it’s not worth the extra monthly expense.

A substantial segment of the housing market – people moving and putting their home on the market and buying another home – has been frozen in this way for a fourth year now. Part of the plunge in sales compared to the years before the pandemic is related to this effect, with these people, as buyers and sellers, having vanished from the market.

The unwinding of the ultra-low mortgage rates is occurring, but very slowly, and the lock-in effect is gradually loosening: “Locked-in” Homeowners Nevertheless Pay Off Below-4% Mortgages: their Share Drops to Lowest since Q4 2020].

In case you missed it: Single-Family & Multifamily Construction: Bring on the Supply just as Population Growth Slows to a Crawl

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The four Census Regions of the US:

This spring season will be interesting, wonder how many will pin their hopes of a spring turnaround and we’re back baby momentum come spring.

This continue decline continues to remind us all the Mexican standoff is well and alive especially if you overlay the price change chart for market such as SoCal. Sales tanking and yet hubris sky high asking price still rampant across OC and LA…as they say, housing move slow but one has to wonder if and when this dam will ever break….

Unless and until sellers are forced to sell, they wont sell.

Renting is much smarter in SD. it takes $10k per month total to purchase after 20% down vs $5k per month to rent a example home in my neighborhood.

In my Seattle neighborhood, it’s $10,000/month to buy or $4000/month to rent. Similar metrics.

Lots of gap to close.

I ran an analysis for where I live in Orange County, California. I compared my current rent to the monthly mortgage payment I would make for the cheapest home on the MLS within a two mile radius having the same square footage. I am renting for less than half what my 30yr mortgage payment would be. It’s madness.

5K a month is $60K in a year that is money lost. I would only agree if I was certain that home prices are coming down(they may). If they continue up, you lose on appreciation and tax deductions

I became rich by renting rather than owning most of my life. I’ve always lived in expensive areas, and investing the money made me much more than home appreciation would have over my lifetime. The only time I bought was in 2012, when I was able to buy a 3 brdrm, 2.5 bath, with a 2 car garage for $240K. I sold it in 2019. It’s worth $780K today accoring to Zillow, about $150K more than I sold it for. Stock market appreciation would double my money since then. It’s not a simple “owning is always better” decision, especially if you understand what is overvalued and what is undervalued, at any given time.

Every month over half of my payment does to pay down principal. 2.5% loan 3rd year in. Even at 3.69% on a 4 wk T Bill the government is paying off my house. I’m thinking there are a lot of folks out there smart enough to see that dropping principal happening every month on their statement. What is the motivation to get out of a situation like that? Job churn is down so really no pressing need to move for many.

Try NYC or Cal. Best move before you get the new tax bill!

There’s not any motivation, unless you have to sell for whatever reason.

But if you don’t have to sell, you’re also not going to be upgrading. You’ll be stuck in that one house.

Waiono,

I am in a similar situation.

The effective rate of a 3.69% TBill in the 24% tax bracket is 2.8% after taxes. If a mortgage is higher than 2.8%, it may be better to pay off the house mortgage unless you can itemize and deduct mortgage interest. The more the Fed cuts short term rates, the worse it will get(ie back to the “normal” it used to be for the nearly 40 years I’ve owned houses).

Selfishly, if 10, 20, or 30 year bonds rise above 5%, it may be better to move there with the mortgage amount to match the mortgage term. You lose the flexibility of a 1 month TBill but have the same safety. Of course, higher yielding riskier investments could be an option if you want to gamble with the house money.

I’m “waiting and seeing” after enjoying the couple of years of 5+% TBills but I’m feeling squeezed along with increased property taxes and insurance. House prices need to drop to fix the property tax and insurance issue.

What flexibility do you lose? Any bond or bill can be bought or sold on the open market at anytime. If you mean flexibility in that you always hold to term then ok but as far as buying and selling, no difference. I would agree more volatility but not flexibility.

AmericaisforAmericans

“What flexibility do you lose? Any bond or bill can be bought or sold on the open market at anytime.”

If you sell a long-term security years before it matures, you can have a big capital gain or big capital loss, depending on what long-term interest rates did since you bought them. so if you think you may need the cash in a few months or a few years, and long before the securities mature, it’s less risky to invest in short-term securities; your gains/losses when you sell them are very small.

Your analysis assumes that real inflation will stay under 5% for a minimum of ten years. Barring a global war that really causes a drop in the human population, I don’t see that happening. It’s not personal, it’s just the math and physics of 8+ billion people all competing for the resources and energy that are required to maintain a decent standard of living. It’s a global economy, period. The genie has been out of the bottle for 70+ years, no putting him back now.

It’s called reinvestment risk. It’s the risk of rolling over short duration fixed assets like T Bills that offer lower rates with each maturity in a declining rate environment. Meanwhile, other assets might be rising in value, reducing your relative share of wealth.

I may beat inflation for 10 years rolling over T Bills, but if the stock market has gone up 300% during the same period, I’m in big trouble when that stock market wealth starts generating inflation.

It’s why I hold stocks, LT bonds, hard assets, in addition to T Bills.

That is madness. We don’t have that situation where I live in Titusville, Florida. I have a house in my neighborhood that a speculator bought 3 years ago to flip. It’s a 2 story, 3300 sq ft, 3 bath completely renovated inside and out and on the market for $499,000. Can’t even get a bid. Looks like the speculator has decided to stop mowing the grass to save money. I imagine folks would kill for that in SoCal.

Hot and humid weather, on land one inch above sea level that’s full of sink holes. Not my first choice, but at least you have sane people running your government.

You can get $500,000 homes in California no problem, but not in the SF Bay Area, and maybe not in coastal Southern CA. The median price of a single-family home in Chico, CA (famous for the Sierra Nevada Brewing Company and for being just downstream of the Oroville Dam that threatened to break in 2015) is about $450,000. It’s at the beginning of the Foothills, very close to the Sierra Nevada, about two hours from great skiing on a good day.

“Improving affordability conditions have yet to induce more buying activity,” the NAR stated.

Hmmmmm…..,prices still too high/rising insurance/property taxes/home repair costs ect.

I KNOW the nar would not lie but they really do seem to be very dumb.

After jumping like 40% last year, my homeowner’s insurance jumped another 10% this year. I’ve shopped around and it is the same price.

Not sure what I’m doing wrong. It is getting ridiculous at this point.

I doubt it’s you. I believe it’s the insurance companies. They liked the increases they levied during covid, and until we rebel they’ll continue. Perhaps Trump should bash them and open interstate competition. its time!

price of home doubled

then price of insurance is going to do same

if it costs more to rebuild then insurance needs to charge based on higher costs

not to worry

higher property taxes coming your way soon and forever

There’s always the facts. As Wolf has pointed out, corporations will pass on higher prices if they can get away with it. Monopolies like our insurance cartel are a prime example.

Try searching :

“According to AM Best, property casualty insurers made a record $169 billion in profit in 2024—even as they raised prices and pushed for laws to avoid paying more claims, all while claiming the industry was in trouble.”

Be prepared to blow a fuse.

I experienced the same issue. I did have mine raise the deductible to the highest amount they would allow which did lower my annual payment a bit. Of course, that may be dependent on state, location, property value, etc. When checking around I generally found $5000 to be the max that many would quote but if someone know of other carriers that may allow higher, I would love to know.

after 28% increase we got quote to raise deduct from $1k to $5k

savings $254 annually

You need to find out what the actual payout is to rebuild after a catastrophic event – total loss. Unfortunately most insurance policies won’t actually cover today’s rebuild costs. It’s a hard truth to uncover.

When it’s not regulated to any great degree, the home insurance companies can basically charge whatever they want. Like you, my home insurance has gone more than 40% in the last three years. And the hilarious thing is that the US didn’t get struck by any hurricanes in 2025. That doesn’t ever happen. Imagine all that money in claims the insurance companies didn’t have to pay out.

I also believe the home insurance industry is moving towards pushing people into higher deductibles. Going from a standard $2,500 deductible to at least a $4K-5K deductible here in GA is about the only way to slow down the out-of-control price increases.

Ultimately, it’s like everything, there’s not going to be severe slowdown in insurance inflation or possibly even deflation until we have a big recession. Everything is under the same umbrella.

It’s the [there’s no] climate change factor. No, sir-ee, not unless you are an insurer. Or want to control the new Arctic shipping routes….

NAR needs to keep a dialogue going that it’s still glass half full or it’ll ruin the industry even more.

Paging Lawrence Yun….your propaganda is needed in aisle 2…

Real wages are up, but the boomers are retired. When they need

money the use c/c or HELOC at 12%, if their FICO is good. If not: 30%. The boomers are the wealthiest group in history. The gov spend on them $30K/Y, but only $5K/Y on zoomers, according to WSJ chief economist. He suggest to transfer wealth from the rich to the zoomers. The boomers

vote. The zoomers voted for Mamdani.

What they always leave out. When the government taxes us they transfer money to the poorer population. Great, but they grab a big chunk for themselves. Not so great.

“The zoomers voted for Mamdani”

And a lot of Gen X and Elder Millennials voted for Trump for the same reasons in 2024. Lots of people hoping a politico like FDR will do something helpful for them as he did for the WW2 generation. That’s just my read on it.

OK, Wolfman, I’m gonna call it like I see it. You seem to sugarcoat things much more than I would. Above you state – “Compared to January 2011, during the Housing Bust and the first January in the data series, pending sales were down by 20%.” The alarm is blaring aloud – ‘The ship is sinking.” I personally am calling this a Housing Depression – it’s just not obvious yet.

However, for some reason, ‘he’ said he wants to maintain home prices high. Huh? Maybe he realizes that if housing prices equilibrate or normalize, it’s party over.

The way I see things, a continuation of these insane price levels will bring on the housing depression. You showed the numbers above. It’s just a matter of time. There is no fixing this mess.

Based on what happened to the economy as a whole in 2008-2012 when housing values imploded, most politicians would say they don’t want a repeat. But he also didn’t say he wants them to go up. Once again, the only cure for the compressed decade of house price increases that happened all at once in 2020-2022 is for there to be flat or slightly declining prices through 2032 or longer. Nobody who got the 2.75% mortgages “won” anything – they just paid the highest prices possible at the time. The only real equity they’ll see for a long time could be through principal pay down.

As he has said, it will be fixed with a combination of rising wages and slow decline of prices. There won’t be another housing-led bank bust because banks don’t have massive positions in MBS anymore. Gone are the days when a Merrill Lynch would have 35-50 billion in underwater CDOs. If there is another 2008 event it will be in AI.

I think there will be a 2000-2003 event in the stock markets due to the AI bubble popping. Which is no big deal since the top 10% own 85% of all equities.

Another stock Klarna (KLAR) qualified for the Imploded Stock list today, this one was incredibly hyped before the IPO and has totally collapsed.

Almost -70% . Let’s see tomorrow …

Good!

Predatory bs products

Frozen markets because wages froze the time prices went up. Lock-in effect of existing homeowners feels more of an excuse for people not to get in and kick their other habits. There’s some sarcasm to that last sentence.

Thank you to the Fed for the golden handcuffs of the 3% 30-year mortgage!

Situation not changing anytime soon

NorthEast and South just came out of an extremely rough winter.

It was warm in the West, and in December pending sales in the West plunged to within a hair of the all-time low, and in January barely ticked up from that.

All of them are down by 30-45% from the same month in 2019.

This reminds me of the nonsense I heard in March 2020 when people said that the COVID virus would die out in the summer because it couldn’t survive the heat.

Meanwhile, there are plenty of cases in Vietnam, Singapore, the Philippines, Thailand and other places where it was 90 degrees…

Major winter storm warning for millions across 27 states as California faces 10ft of snow and East Coast braces for white out this weekend

Forecasters warned that ‘significant’ snowfall could hit later this week and into the weekend, as a brewing Pacific storm has already put much of the West and central states under winter storm alerts.

thankfully it doesn’t snow in the low-lying coastal areas. Just stay off Mt Baldy.

I can still remember it snowing in Berzerkeley when we lived there,,, probably early 1980s Wolf, but could have been some years either way.

It snowed in the greater TPA bay area this year, and down farther south on the west coast, but did the same in the ’80s and also the 50s IIRC…

“ NorthEast and South just came out of an extremely rough winter.”

We’re getting another 8” of snow a little north of Boston later today. Winter is getting caught up here after very little snow the past few years.

8″ of snow,how far north of you from Boston?!

@ best 1-3″ and a lot of rain/mixed bag weather in all the different reports I am watching.

I am a backup snow plow driver and thus need to keep a constant eye on weather and ALL reports I see show nothing close to 8″.

That said,tis New England,can change quickly!

The southern end of metro Minneapolis got about 7″ from Wednesday’s storm, hardly impressive for the Upper Midwest but still the biggest snowfall of this dry winter season. The last few winters have been critically lacking in snow.

Hovland up north did get over 3′ though.

The free money and low interest rates and inflation pop of the covid Crisis caused by our all knowing Federal Government Have terminated the housing market for a long time to come except for the wealthy and high earners

First, thank you for the comprehensive update.

Notwithstanding the gradual reduction in interest rates, the key factor in slow home sales is PRICE. Now perhaps where I live is an exception, but virtually every listing is 10% to 40% above the 2021-2025 selling price or 40% to 100% above the 2016 to 2020 selling price. Couple that with increased taxes and dramatically increased insurance (my insurance is triple what it was 7 years ago) and it’s a recipe for un-affordability.

Anyone else seeing this?

The hilarious thing is people thinking 0.25% will drastically change things. 1%+ isn’t possible with current deficit without risking inflation and tanking the dollar (which as an import country only makes the former accelerate).

With 30-year fixed terms in the US (plus programs like Prop13 , things are going to stay locked for a long time. Decreased mobility will absolutely impact real GDP growth.

If we sideways growth in the overall housing market for the next 15 years, I really don’t give a s$#@. The industry and Fed did this to themselves. Now with negative migration patterns in the US, its going to create even less demand.

This is the exact attitude that is perpetuating the “dream”!

I don’t care, because I got mine.

We’ll have to pry our children’s houses out of the Boomers’ cold, dead hands.

Anecdotally, in CO my brother-in-law is a cancelled contract. On the part of the seller too, who knew? (RE: The rate of cancellations has been running high.)

re – How little additional sales volume it takes to ignite a bubble…

Maybe I am mis-interpreting things (don’t yell, Wolf, please) since using the annual year by year numbers to get a sense of the size of the 2020-2022 (especially *2021*) transaction spike sort of takes a bit of inverted interpretation…but if I am interpreting things right, the transaction surge in 2020-2022 (vs. say 2019) really wasn’t all *that* huge.

But it was enough to cause a huge run-up in median sales prices (in absolute dollar terms) and to “anchor” inflated expectations for 2023, 2024, 2025,…

Maybe that really isn’t news…but it is disturbing (if accurate) that a relatively small increase (decrease too?) in transactional volumes can have an outsized (read huge) impact on prices…that lasts years and years.

Again, maybe not news…but troubling to eyeball the actual historical data.

On a related note, I recently read that current transactional volumes have gone from 25% investor-based to 33% investor-based.

I know that Wolf has pointed out that the vast majority of SFH investors are mom-and-pop shops (1-10 SFH owned) vs. institutional behemoths (although I do wonder if behemoths would be above using straw mom-and-pops…) but regardless, I think that any SFH investor really has an intrinsically more “speculative” mindset and is much more comfortable than a pure owner-occupant with aggressive use of leverage…and all the evils that can follow from that.

“I recently read that current transactional volumes have gone from 25% investor-based to 33% investor-based.”

What that means, if anything, is SHARE. If overall sales volume plunges by 40%, and sales to homebuyers plunge by 45%, and sales to investors plunge by 35%, then the SHARE of investor sales rises, though sales volume to investors has plunged by 35%.

the biggest SFR landlords have become net sellers of scattered homes and are now exclusively focused on building their own build-to-rent developments. Sales to smaller investors have also collapsed, just not as much as sales to homebuyers.

Yes, prices are set at the margins and a lot of what makes a “market” is one of psychology.

The flip side was that it didn’t take a huge number of foreclosures and sales in 2010 to really drive DOWN prices. The psychological phenomenon works in both directions.

“The flip side was that it didn’t take a huge number of foreclosures”

Actually, I think it really *was* a pretty large number of foreclosures during the “blast crater” years (2008-2012 or thereabouts)

Hazy recollection was that there were about 8 million foreclosures in aggregate, out of 50 million homes with a mortgage in aggregate (so, about 16% of everything possible – that’s a spicy meatball).

Contrast that to the perhaps 2 million (2.5?) bump in sales due to the pandemic ZIRP. And, especially, look how long the pandemic ZIRP has anchored sales price expectations (3 years…despite a 25-33% decline in aactual sales due to inflated expecations/unaffordability).

“How little additional sales volume it takes to ignite a bubble…”

Right, didn’t they call it “spoofing” when JPM did this in the metals markets? There’s dozens of variations on the theme.

Happening daily, in a financial market near YOU!

Lived through the migration of farm workers looking for work to the city. So now I wonder what will happen to all the McMansions along the highways in the Midwest. Should be some fun times for the youngsters when they become empty.

Yes. As I keep reminding my kids “buyers set the markets, not sellers”. Those big houses are only worth what someone is willing/able to pay for them. Yes, that is a trite expression, but there have been huge regional population flows in the US since 2020… and I’m not sure real estates prices accurately reflect them.

So sales are still low, inventory is still high, any movement in prices yet?

If there were, sales would be up.

People still in their trenches. Awaiting the whistle.

Prices too high and many potential buyers are likely wary of prices falling. So buyers are holding out. Sellers are not forced to sell so they are holding out as well. The only ones blinking are those that must sell and apparently there are few of them.

If you look at the graphs above, especially the one for the West, it looks kind of like an EKG strip where the heart is beating and then flatlines (since 2023 onward), or where it goes into ventricular fibrillation, which is impending death (if lifesaving measures are not provided). It truly does.

Is the next stop for the housing market the funeral home?

LOL, yes, yes it is! Those who swore they would never get old will not willingly move into anything that looks like an old person’s home. Their next move will be a funeral home.

All the current noise about taxes and insurance is that they want the equity but, not the bills. For the rest of the population, the only real remaining pry bar to keep the market moving is property taxes.

Peak births was 1957. While the wailing over the unfair burdens placed on our beloved seniors will undoubtedly increase, expect nothing else to change until Social Security benefits get cut ~2032 (earlier if the spike in the 62 take rate continues).

Greedy sellers will keep the housing market in the doldrums. They need to wake up and smell reality. It probably won’t happen until the iron hand of the market hits them where it really hurts. I don’t know when. Lower prices are the only way to get out of this mess. Buyers can patiently rent, especially when monthly rent is quite a bit less than monthly mortgage plus other costs on some over-priced POS.

Housing prices will have to fall a lot more than they have been to spur demand. It’ll take a major crash to spur buyers off the sidelines.

Anyone who thinks prices can just stay sideways for decades until incomes catch up are in for nasty shocks. Prices will indeed stay sideways for decades, after a relatively quick crash that crushes prices to 20% of what they are now.

Great work as always Wolf.

Wife and I were looking last fall in NY, but gave up. Pickings were slim, though we almost made a play a couple times (would be for a fixer-upper, as that’s all we could afford). But then our apparently national policy of dismantling the economy really set in, and both our earning positions worsened significantly, so moving out of rental is once again off the table. Elder millennial, never owned, this is the umpteenth time this has happened to me.

Outside of the suburbs where home builders are increasing supply, what’s stopping every major centre from staying unaffordable from a buy vs rent perspective? How long has buying in NYC been nearly impossible so everyone just rents? What makes prices “have to” come down? I’ve heard wealthy people say that real estate is something you buy, you don’t sell it. Guessing once you buy at a great price it’s good collateral, as long as you didn’t get into office towers or retail malls at the wrong times

People who are trying to live in the center are buying condos, not single-family houses. Since you mentioned NY City: In Manhattan, there are very few single-family homes. Most of what what people buy are condos and co-ops.

A normal inflation: zero to 10%. A moderate inflation: 10% to 20%. High inflation: 20% to 80%. Rare Pending Sales bottleneck.. Boomer’s assets are the highest ever. RE, 40% are mortgage free, is a large cost center doing nothing all day. If WTI rises above $100 and inflation rises above 10% ==> the US gov $40T debt, RE, SPX and your SS will deflate.

Haven’t seen many economic articles connect the rate of quits to the mortgage lock-in, but it has to be a factor.

Just as tying health insurance to jobs reduces people seeking better opportunities, that sub-3% mortgage is probably costing people meaningful opportunities by now.

One time someone said something about location when asked about RE.

For instance, feel free to buy a ~2800sqft townhome for 1.3 to 1.8m and nowhere, anywhere at all near a US coast. 30 of them right off a 4 lane highway. And they are half sold and finishing the last ones soon. And four ~2.5 million condo units across the street from these 30 are breaking ground. No beach view, just a shake shack. I guess you can lay out in the parking lot sometimes.

~25 more townhome units are lining up to be built around the area at these prices.

“Improving affordability conditions have yet to induce more buying activity”: National Association of Realtors.

What a joke! Housing prices are not affordable by any metric yet the NAR spreads BS. The market won’t turnaround until prices drop by 20-30% and that’s even if rates drop significantly. At this point it’s going to take mass unemployment to push the market back to affordable.

The RE market here in the Swamp is dead. RE agents are leaving the profession and heading up the road to New Jersey to get jobs pumping gas. New Jersey is the only state in the US that will not allow you to pump your own gas.

Fed’s Preferred Gauge Shows ACCELERATING Inflation Trends…

It’s kinda wild to be invested in housing and at the same time look at a demographic pyramid in the US. Boomers like my parents have maybe 5 years before they won’t be able to live in their suburban SFH’s any more. Assisted living is calling. There are tens of millions of older homes about to come onto the market in the next few years.

Meanwhile, investors who expect high inflation are plowing into Real Estate in the expectation that it’ll protect the real value of their assets. Evidence for their thesis is that… investors have been plowing into R.E. and pushing prices up faster than inflation.

I’m no chess grand master, but I know rents (unlike property prices) can only keep up with wages, and I know many of the elders who own a bulk of the housing stock will be selling within a few years. Put these together and you get a trend toward disappointing returns for landlords.

NEVER buy what is making headlines.

The rich are buying and selling moving and grooving same with to automobile market. Jan 2021 2.65% interest rates marks the low end of some even got lower buying points. Imagine your home insurance increasing from $2800 to $7000 in Colorado because all your neighbors file 2 claims for their hail damaged roofs. Inflation has been sticky, man made bubbles and now Mother Nature made bubbles.Its funny how people seem rather mad that the housing market has cooled off to a screeching halt. Maybe everyone got what they wanted or what they needed for the moment. As most socialists states now look to raising taxes inward to take care all residents, even legalizing prostitution in Colorado congress. I will remain in my foxhole with 2.65% rate, never expected insurance to topple taxes, $3 billion collected from cannabis sales since 2012 legalization worst roads, large potholes, and homeless crises keeps growing. Relatively no winter this year and bone dry with lack of precipitation on front range, water reservoirs are at a deficit.

Now – Here’s a humdinger that I’m just noticing.

Two retirement communities close by. Wolf may dispute this, but I have noticed a LOT of foreclosures and short sales in the retirement communities. And a LOT of homes for sale. One is surprisingly cheap. To me, it looks like the Titanic taking on water, before it sank.

Distress signal sent out, but no disaster YET. Key word – YET.

I can’t help but feel sorry and bewildered for the poor elderly people who are losing their homes. Where will they go? Are we staring at the beginning of a homelessness crisis in the elderly population?

I also think it is a foreboding for the housing market in general. I’m not sure what type of economic ‘super glue’ is holding the housing market together, but it can’t last. It’s like trying to patch the Hoover Dam with silly putty.

I’m in Vegas, sellers here (mostly house flippers) are being stubborn, houses aren’t selling, the flippers have discounted a modest amount, but for the most part have been hoping to ride it out, meanwhile, their inventories are growing fast and they are at risk of getting wiped out, which is glorious to me as they need to be punished for their gross profiteering these last few years. Later this year we’ll see house prices really crash down hard.