Big Tech is finally plowing their cash & their investors’ cash into the economy.

By Wolf Richter for WOLF STREET.

Five companies announced that combined they plan to make about $700 billion in investments in 2026. The bulk of these capital expenditures are related to AI with a focus on AI infrastructure – data centers and everything in them and around them, from AI servers to onsite power-generation equipment if the utility cannot supply the juice.

- Amazon: $200 billion

- Alphabet: $175-185 billion

- Meta: $135 billion

- Microsoft: $145-150 billion

- Oracle: $42 billion

The market has not been enthusiastic about this spending binge, fearing that this cash that gets spent will sooner or later come out of share buybacks; and that is already happening.

If these five companies actually make the announced capital expenditures and the funds flow into the economy in various forms, they would amount to 2.1% of current-dollar GDP.

Other companies are also cranking up capital expenditures, though not as much, and the overall capex figures are much larger. So overall, this is a big stimulus for the economy for as long as it persists.

A stock market crash would end the binge. Think of the Dotcom Bust, when the S&P 500 plunged by 50% and the Nasdaq by 78% over a span of 2.5 years. As thousands of companies collapsed and vanished, and the stocks of the survivors crashed, capex and corporate spending got slashed left and right. It triggered a run-of-the-mill recession in the US overall and a depression in the tech areas. Lots of people are holding their breath, but it hasn’t happened yet.

Where will this $700 billion in cash come from?

The cash for these investments of $700 billion would come from a mix of:

- Share buybacks get cut (already happening)

- Share issuance (already started)

- Debt issuance (oh-la-la)

- Their massive hoard of cash and short-term investments

- Their huge operating cash flows.

Cherry on top: There are the massive and accelerated tax cash-benefits for investments in 2026 that will provide some additional funding.

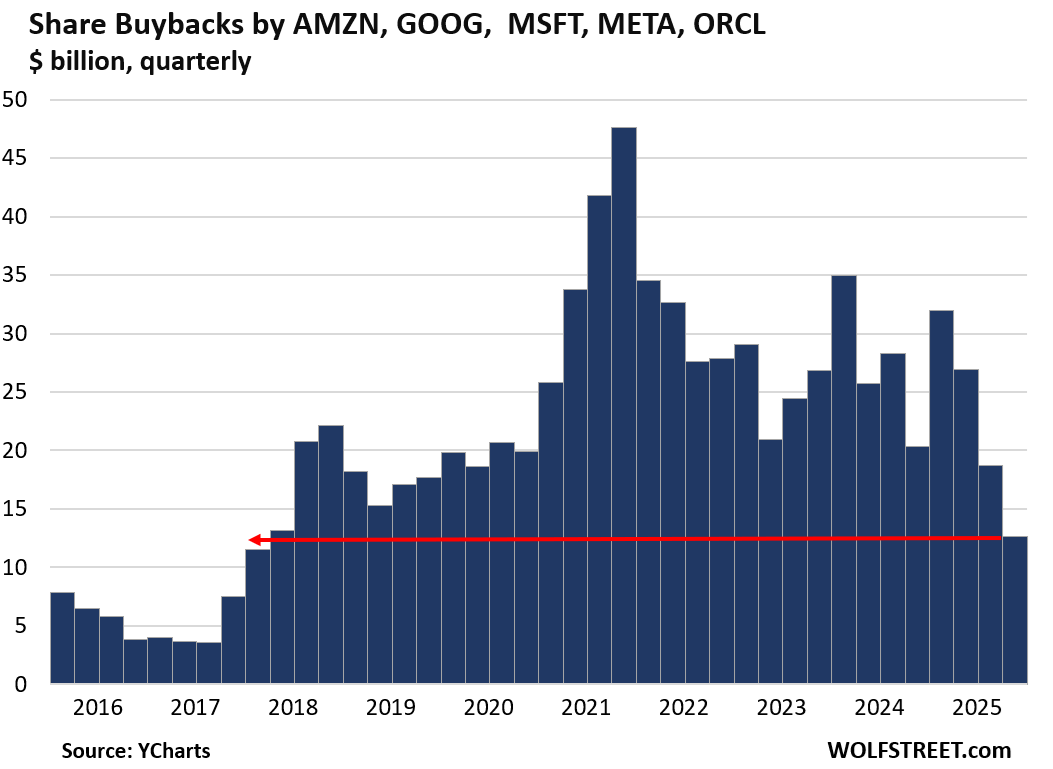

Share buybacks get cut. This has already happened. So actual share buybacks, not announcements:

Oracle flipped from share buybacks to a share issuer, which has the opposite effect of share buybacks. In 2025, it issued $2.1 billion in new shares, largely the result of its stock compensation plans. In February, it launched a $20 billion at-the-market share offering (see below).

Amazon last bought back shares in Q2 2022 ($3.3 billion), and has had zero share buybacks since then, investing the funds instead in its AI endeavors.

Meta cut back share buybacks to $3.3 billion in Q3 and Q4 2025 combined. Share buybacks in the same period in prior years:

- $8.8 billion in Q3 and Q4 2024

- $9.5 billion in Q3 and Q4 2023

- $31.2 billion in Q3 and Q4 2022

- $33.5 billion in Q3 and Q4 2021.

Alphabet cut its share buybacks to $17 billion in Q3 and Q4 combined. Share buybacks in the same period in prior years:

- $30.6 billion in Q3 and Q4 2024

- $32.0 billion in Q3 and Q4 2023

- $30.0 billion in Q3 and Q4 2022

- $26.1 billion in Q3 and Q4 2021.

Microsoft reduced its share buybacks in 2024 and 2023, then increased them some in 2025. The share buyback peak remains in 2021 and 2022.

For these five companies, share buybacks combined in Q4 plunged to $12.6 billion, the lowest level since Q1 2018.

At the peak in 2021, these five companies spent $149 billion on share buybacks. If share buybacks of all of them go to zero, that would provide $149 billion in cash compared to 2021.

In addition, there are massive and accelerated tax cash-benefits to investing in 2026, while share buybacks are taxed. So after tax effects, the cash generated by ending share buybacks and investing these funds in AI infrastructure are very substantial (share buyback data via YCharts):

Share issuance: This also is now in the works. Oracle was the first out of the gate. It announced this month that it would raise $20 billion by selling new shares “at-the-market,” which allows it to sell the shares in dribs and drabs over time.

But it’s not free. The price of its shares has plunged by 58% in five months from the high in September, to $142.82. If they fall by another $40 a share, back to where they’d been in December 2023, they’d qualify for our pantheon of Imploded Stocks, for which the minimum requirement is a 70% plunge from the more or less recent high.

Share prices of the other four companies are still sky-high, and they can easily sell shares at very high prices, which would be efficient for them to do, but that would come only after they stop the share buybacks entirely.

Debt issuance. Oh-la-la. Oracle’s capital raise announced in February included a $25-billion bond offering, which was met with ravenous demand from investors (orderbook $129 billion). In September 2025, Oracle had already raised $18 billion in a debt sale. At the end of Q4, so not including the $25-billion debt sale, Oracle had $131 billion in short- and long-term debt.

Meta, which has $85 billion in short- and long-term debt, issued $30 billion in bonds last October. Then it took on another $27 billion in debt, but kept if off its balance sheet via a Special Purpose Vehicle (SPV), an outfit called Beignet, that issued the bonds to fund a huge data center in Louisiana. Meta is backing the bonds with debt-like guarantees. It guarantees the construction risk. Its rent payments cover the interest payments of the bonds. Its residual value guarantee is to be used to pay off the bonds. If Meta wants to bail out of the deal, it has to make bondholders whole by paying off the remaining amounts after the data center is sold. But the advantage for Meta is that its credit rating won’t get dinged.

Amazon, which has $167 billion in short- and long-term debt, pulled off a $15-billion bond offering in November 2025, also amid ravenous demand from investors.

[Update Monday Feb 9: Alphabet is working on a $15 billion bond offering to fund the AI-related investments, according to people familiar with the matter, cited by Bloomberg this morning].All of the five companies have at the moment lots of room left to sell bonds amid huge demand for bonds from investors. Four of them have still very high to stellar credit ratings: Microsoft ‘AAA’; Alphabet ‘AA+’; Meta ‘AA-’ ; and Amazon ‘AA-’. Oracle at ‘BBB’ is two downgrades away from “junk” which starts at BB+ (my cheat sheet for corporate bond credit ratings). But even a junk rating of ‘BB+’ or ‘BB’ would only mean slightly higher yields these days, with still ravenous demand from investors. Everyone is chasing yield.

Their cash hoard. Cash and short-term investments could partially be used to fund capex. At the end of 2025:

- Amazon: $126 billion

- Alphabet: $127 billion

- Microsoft: $95 billion

- Meta: $82 billion

- Oracle: $16 billion.

Operating cash flow. In 2025, four of these companies generated massive operating cash flows (Oracle not so much). All five combined generated $575 billion in net cash flow in 2025. And similar cash flows in 2026 would help fund the $700 billion in investments:

- Alphabet: $165 billion

- Amazon: $139 billion

- Microsoft: $136 billion

- Meta: $115 billion

- Oracle: $20 billion.

Big Tech is plowing their cash & their investors’ cash into the economy.

When these companies don’t blow their cash on buying back their own shares, but instead use the funds to invest in AI infrastructure, they’re plowing their cash, and by extension, their shareholders’ cash, into the real economy, contributing to economic growth. I have long advocated for this shift, and it is now happening, though shareholders won’t like it.

When they issue new shares, to invest the proceeds in AI infrastructure, they’re plowing the cash from these investors into the economy. Shareholders get diluted, but the economic growth gets stimulated.

When they issue new debt to invest the proceeds in AI infrastructure, they’re plowing the cash from these yield-chasing investors into the economy. These investors like that, which is why they’re buying the debt, and the economy likes it. Shareholders maybe not so much, or maybe they don’t notice.

When they use part of their cash hoard, they’re handing Treasuries and corporate securities to other investors, and are plowing the proceeds into the economy. As long as they still have enough cash, everyone is happy with that.

When they use their operating cash flow to fund these investments, the economy benefits. That’s what operating cash flow is for, to invest and grow.

So as long as the financial markets can be kept spinning, this investment binge will continue to be a big stimulus for the economy.

In case you missed it: PayPal Shares Plunged 86% from the 2021 Goofball High and Right into our Imploded Stocks

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The shareholders can go eff themselves, it’s about time these companies made the rest of America wealthier. Our electricity grid is crap, they should start there.

I take it that you are not invested in stocks atm?

Which is superior for the economy.

Infrastructure or an individual share price?

Nobody cares about the economy, we only care about our personal wealth

Lake of Fire for you Stevo……..

AGREE, like totally Sandy:

As someone who made a ton on stocks ‘back in the day’ but OUT of the SMs, and other mkts since mid 1980s when I realized the futility of trying to keep up with the ”big boys,” I certainly agree with both of your clear sentiments, but especially that the USA ”grid” is bad…

IMVHO, the very best thing for the GUV MINT to do NOW is to make every home, biz, warehouse, etc., a source of solar electricity and hot water, and also make the investment needed to provide LOCAL grids independent of nationals…

Clearly, the technology, although also clearly restrained by the lack of investment into basic hard science for decades, is now adequate to make such investments by GV an actually better investment of tax payers money than anything else currently being subsidized.

JPMorgan calculated last fall that the tech industry must collect an extra $650 billion in revenue every year — three times the annual revenue of AI chip giant Nvidia — to earn a reasonable investment return. That marker is probably even higher now because AI spending has increased.

OpenAI, which unleashed the nation’s AI mania with the public debut of ChatGPT in late 2022, expects to lose more than $100 billion through the end of the decade, the technology news publication the Information reported in September.

Companies might never achieve a decent return on these investments. But that’s a problem for stockholders, not for the capex investments or the economy.

So read the article. It explains why for stockholders, this is not an ideal situation. But they have been spoiled for so long. Now they’re going to do some heavy lifting.

How does this affect the companies they’re paying? The data center developers, the contractors, the suppliers?

They get rich.

More like some heavy sinking…

Well, its optional for these shareholders to continue doing the heavy lifting. They can always sell and invest elsewhere…

Love your content. Keep up the good work.

Just updated my article, as the debt sales keep piling up.

Monday morning, Bloomberg reported, citing “people familiar with the matter,” that Alphabet is working on a $15 billion bond offering to fund the AI-related investments.

Tech was the best sector to be invested in during the 2008-09 financial crisis.

As I watch the tech behemoths add leverage, I cannot help but wonder if their leverage was a lot lower in ’08 than it is now. Maybe that was the difference that made them the best performing sector coming out of the crisis?

Hmmm…but maybe tens/hundreds of billions simply going from MS/Meta/Amazon/etc. to NVIDIA/AI storytellers/etc isn’t exactly a broad based distribution of wealth across the US macro-economy.

Data centers employ very few people after construction (and I’m not sure the *construction* phase is necessarily all that hugely labor intensive either).

Perhaps better than sitting semi-idle in the vaults of the Mag 7 (residing in turn in US Treasuries…) but not something really likely to re-ignite a guttering US macro-economy either. (Although I suppose that depends upon one’s medium-term faith in the AI story-tellers).

Perhaps sort of like watching billionaires play cribbage.

Either on a starship or the Titanic.

I’m wondering if 1-2 year puts on these stocks is the way to go.

Written by someone with a BS in economics from Wharton mind you, using the reduce to the ridiculous method. The number, $35/iphone user, is an attempt to make $650B seem unattainable.

1. There are nearly 5B mobile phone users in the world. If the average revenue increase is $2/mo per user thats $120B

2. Regarding streaming, thats 1B subscribers. Again $2/mo is $50B

3. The top 25 companies have $7T in annual revenue. If AI adds just 2% thats $140B

That’s just touching the surface on the revenue side.

What about cost cutting?

If AI displaces just 3% of the US workforce alone at average incomes of 70k, thats $350B.

So there is your $650B and that is just scratching the surface.

I have a tiny retail business and AI, even at this early stage with our limited use, has its imprint all over it in the form of productivity, cost cutting, and increased revenue.

The capex spending these companies are commiting to will without doubt pay huge dividends. These will be perhaps the same or maybe new generation titans of industry.

Many companies will vanish and burn large sums of investors money in the process.

Just as before; new cycle same outcome.

The value of AI investment should be crystal clear to anyone with business acumen. That in no way justifies the valuations of many AI related companies. Two very different topics.

Written by someone almost finished a PhD in economics but decided to get one in computer science instead.

Just because a technology can reduce cost, it doesn’t mean that the savings will translate to revenue. Internet vastly reduced cost of commerce but the amount of profit generated is far lower than the amount it destroyed. For example, Amazon killed brick and mortar business and the the amount of profit Amazon generated is far less than the amount it destroyed.

Thanks to competition from China. GenAI companies make meager profit if at all from its services. All the investment in the world is not going to change that. How much can OpenAI charge for its subscription? The moment it cuts off free services, all the users will flock to Chinese providers. It is as simple as that. Unlike car market, US can set up a tariff barrier, there is no way to prohibit service flow. None of the investment can be recuperated.

“Internet vastly reduced cost of commerce but the amount of profit generated is far lower than the amount it destroyed. For example, Amazon killed brick and mortar business and the the amount of profit Amazon generated is far less than the amount it destroyed.”

Total utter fabricated bullshit. Is bullshit fabrication the art they teach you in economics grad school?

Amazon is just one online retailer (among other stuff it does). Walmart is another huge online retailer, as is Macy’s, as is Apple, as are all big brick-and-mortar retailers, and all online-only retailers. Profits in ecommerce are huge. At the same time, there is still a big part of brick-and-mortar retail that is throwing off huge profits too, the biggest one being motor-vehicle dealers, and grocery stores.

Since 1998, when ecommerce was still just a blip, total profits at all retailers combined — brick-and-mortar plus ecommerce — has multiplied by 8:

AND RETAIL IS ONLY A MINUSCULE PART OF WHAT THE INTERNET DOES.

True. Profits are driven by competitive advantage. A low barrier to entry means a low profit business. The internet reduced the barriers to entry for retail. Thus online retail revenue has increased, retail profit margins have decreased.

Michael Porter

Not true.

1. Typecheck was not talking about “profit margins” (percent); he was talking about “the amount of profit generated” (dollars).

2. Most brick-and-mortar retail has low barriers to entry. You lease a retail property, and you’ve got your store. That’s your entry. Now you just have to run it. Auto dealers are one of the exceptions. They’re protected by state franchise laws, and automakers have to approve any new dealers before they can set up shop.

3. Brick-and-mortar retailers such as discounters and Walmart etc. have long operated on a lower profit margin (percent) to increase their sales thereby increasing their profits (dollars). Lots of retailers do this.

Apple not playing?

Dabbling.

About $14 billion

Apple loyalists will buy whatever they make and not care too much about AI.

“Apple AI how do I read magazines more effectively?”

/s

There model seems to be paying Gemini and to a lesser degree to use their models. Smart play in my mind.

@glen Totally agree on Apple. Why invest a gazillion dollars in something guaranteed to blow up when you can just buy access to the platform guaranteed to be left standing when tears have dried. Same thing they did with Search, instead of developing their own, just cut a deal with Google. Gemini is likely to one of the remaining platforms, they’ve got DeepMind and will be just fine after OpenAI goes down in history as the MySpace of the AI world.

Apple doesnt do software very well. They have other strengths, but software is not one of them. However, that inability has allowed them to dodge a bullet. Rather than making huge bets on stuff that is not part of their core competence they are wisely contracting from Google for it.

Microsoft, on the otherhand have gone into AI full throttle and in doing so seem to be damaging their Windows francise with Windows11 premature embrace of AI.

Apple will watch the mistakes of others and perhaps fall into the right balance as they often do.

The big winner in computing of the whole AI deal might turn out to be linux. It wont be long before all the major linux distros will include very competent AI based admin applications that will relieve Linux users of having to know much of anything about packages, cron, bash, IP interfaces.

I don’t know if the AI capex will be a net boost in productivity fr the overall economy or not. But it will be an interesting experiment. All the big tech firms for the last 10 years have been net sources of global liquidity. Now in practically no time, they are net consumers of global liquidity. Thats bound to have some sort of unanticipated impacts.

Sandy,

Myspace is a fun analogy. Altman is really just really a marketing guy who will simply say anything to get more money and try to stay relevant. My guess is if Open AI doesn’t go public they at least sell some of their stuff. ChatGPT is almost synonymous with AI but that will change. I uninstalled it and use Gemini or DeepSeek now. According to Altman himself that ad placement means the end is near.

@danf51 instead of sudo being a command, it will become an actual admin!

“They (Apple) have other strengths…”

Reality distorion field (for one)…engage…

Apple outperformed the Nasdaq this week by simply not doing anything significant in AI.

The illogical thinking of every company in America…except for goosing the stock options.

Stock buybacks when stock prices are insane.

Issue more shares when stock prices plummet.

“Share prices of the other four companies are still sky-high, and they can easily sell shares at very high prices, which would be efficient for them to do, but that would come only after they stop the share buybacks entirely.”

The customers of these companies are not you and me, nor the mom and pop shareholders. Their real customers are the Wall Street whales and market movers who are happy to trade short term losses for massive long-term gains. From that perspective, those moves are very logical.

Yes, absolutely logical thinking given our economic system. They don’t view themselves as part of the collective society but separate from it. Nothing new of course but just so much more obvious now. That said, plenty of money packed into pension, IRAs, 401Ks and so on, so in most people’s interest to keep it inflated.

“so in most people’s interest to keep it inflated.”

More, perhaps…but not really *most*.

what public stocks will be the best positioned to profit from all this capex spending ? just a question for all you smart commenters and wolf…………thank you for your attention to this matter. please LOL

Seems like cat has been benefiting but it’s stock is pretty high already so not sure chasing would be wise here.

Lotta questions in the ai narrative in my eyes but the biggest is how does it impact the job market.

Will new jobs created by AI come even close to replacing jobs lost?

Is Elon right and is ubi the long term answer… and is there an appetite for that with 40 trillion in debt our doorstep?

How deep does the NASDAQ have to go down before the faucet turns off?

Lotta stress on tech and software in particular lately does not give me high confidence that this will last much longer but I have an open mind

Energy commodities, power generation, and construction equipment to name a few

These investments are fantastic to see.

Agree and disagree. I agree that, between plowing this money into investments and doing stock buybacks or dividends, the former is better.

But the real problem is that the Mag7 have so much operating cash flow in the first place. Since this cash flow has grown far faster than the economy as a whole, it means they’re taking more and more of the pie. Their monopoly/oligopoly pricing power assures that.

I don’t consider that a good thing.

Monopolies and Oligopolies are never a good thing, and anti-trust action against them is almost always a good thing, unless its being used as a way to curry political favors. The big tech companies should all be broken up like AT&T was to create competition, lower prices for consumers, and weaken the power of the billionaires that own these companies and our government.

Is the 700 billion all in the US? Or is there a breakdown by region?

700 billion/52 weeks = $13 billion a week or just under 2 billion day. The Chinese abacus is now much larger/longer. I can’t fathom this amount.Scary all these techno nerds with so much money. Good luck to all the players.

While the general idea of “plowing cash back into the economy” is directionally correct, the specific content of the capex, in this case, is mostly wasteful and ridiculous.

We do not need more “data centers.” And when we blow capital on this stuff, it is no longer available for things we really do need. The only benefit that the real economy will derive from this is a very short building boom of a few years’ duration – a classic boom town cycle. We can ask the shale patches in South Dakota how well that worked out for the folks there.

This seems to be a real dilemma. If AI “works” (it won’t, but let’s just pretend for argument’s sake), then it will displace millions of workers in the real economy, who will be jobless and broke while the efficiency gains accrue to the billionaire class. If it doesn’t work, then we will have wasted all this capital by building Ozymandian monuments to digital nothingness.

It’s hard to see how anybody benefits from any of this.

That’s a silly comment. Just like cars will never work because of yada yada yada, and we don’t need no effing cars. Horses will do just fine.

AI works and has been used everywhere already for years, and its use has been expanding at a very rapid pace, as have its capabilities. You just didn’t notice? Maybe get out a little more often?

I just listened to the Nobel peace prize talk about AI.

Their words were “it’s uses are shallow at the moment”

And “obviously this massive build up will crash just like the .com bubble”

these are Europeans , smart ones, real smart.

Hehe , so who knows

AI is being used for protein engineering for new medicines for incurable diseases. I hardly think this is “shallow.”

Consider the source, the Nobel Peace Prize was previously awarded to Barry Obama who went on to assassinate roughly 3,000 people.

“Nobel peace prize talk about AI”

🤣🤣🤣🤣❤️

What kind of bullshit are you going to cite next???

Europeans are miles behind on AI and tech in general, which is a huge problem in Europe, and causes a lot of handwringing there, if you pay attention to the European media lamenting it.

I’d recommend watching the documentary “The Thinking Game” (free on YouTube). It follows the child chess prodigy who started DeepMind through his creation of an AI model that eventually won the Nobel Prize in Chemistry. The uses are not remotely shallow.

LLMs are a different story, those are overhyped and will crater the economy when everyone realizes that they aren’t going to remove millions of headcount off the payrolls.

Yeah….put all Bio-reality in silco….sell many more useless or damaging pills….maybe get a “Nobel”, too……..earn even more speaking creds……

There are other types of “opinion creds” that can be chased down to individuals on various “oversight boards”.

But here are the simplified results…..am noticing speed making a comeback like 40’s-60’s……enjoy.

Sure, but BigTech is not doing it to better society, but so that they can harvest our data, sell it for marketing purposes, and make money.

When Henry Ford rolled out the Model T, of course, he was trying to make money, but the people who bought the cars wanted them.

Do Americans want the “product” that Google and Meta are using their data centers for?

TSonder305

Most uses of AI are not consumer-facing at all. Companies use AI, from your healthcare provider down to small businesses for internal stuff. This is not new.

Wolf, I agree on a lot of the software, especially some stuff I’ve been using at work (although I don’t see it as revolutionary as many do). My concern is solely with regards to the Mag7. I can’t shake the feeling that whatever they produce will be good for them and bad for society as a whole.

“whatever they produce will be good for them and bad for society as a whole.”

No disagreement there.

Yep as an engineer in the upstream energy business we have had AI for 3-4 decades but on a much more limited scale . AI will only make the tasks easier and maybe prevent some very costly mistakes that won’t ever be known except maybe stats .

People will benefit .

Robo driving should reduce insurance costs and maintenance costs and save lives .

The integration of Quantum computing and AI is also underway.

Another missing piece is that these new technologies, at scale, can solve problems that were unapproachable in the past.

While forecasts for societal impacts are value judgments and have merit, one can’t help but observe that society is already hosed up without much prodding from AI.

I agree with your comments on the worst case labour impact and the social problems it could cause. Humans derive value through work. AI doesn’t spend and consume either which isn’t great in an economy driven by consumption.

Larger deficits unless tax reforms take place.

However, at the minute AI effects are unclear. And we likely underestimate how it develops.

AI infrastructure build out won’t require labor from multiple industries?

AI system-of-systems won’t require maintainers and operators?

AI system-of-systems will relieve corporations of all the duties associated with data management?

AI won’t require cybersecurity specialists?

AI won’t have positive and negative impacts across the entire economic system-of-systems?

AI won’t have its associated change management processes?

AI won’t spawn new industries?

I don’t hold a crystal ball. But we have seen these waves of creative destruction before. Yet, here we are.

In my own mind, I think AI will be like other ground breaking technologies. There will be early adopters who fail, there will be growth leading at some point to commoditization and then the downside of the curve as tech progress moves elsewhere. There will be winners and losers. There will be pronounced changes in social relationships, legal systems and distribution of wealth. There will be consequences we haven’t conceived yet.

I was at Fort Meade when a friend was tasked to assist designing one of these mega data centers. Can’t go into details due to classification issues. I held the right clearances with some need-to-know to see a small piece of the planning early on. It’s amazing how many infrastructure and human activities one of these very complicated SoS take to build, operate and maintain. Human actors fit into every step. We don’t know with certainty who the job losers and winners are going to be. We don’t know what new jobs will be created as challenging problems are solved with proposed solutions that will require humans to innovate, operate and sustain. We don’t know what the external diseconomies are going to be.

Buckle up. This roller coaster ride has already launched.

Off my soapbox.

AI will easily replace search engines and can take nearly half a trillion dollars in ad revenue.

This is almost a done deal.

If AI replaced search engines, why would any business pay to advertise on it?

The way Google search works now is regular search plus AI. It’s an enhancement, and there are ads on the page if it’s a topic that triggers contextual ads. So Google: cheapest cars. You’ll get the AI summary at the top, and then below it the car dealer ads. To see them, make sure your browser doesn’t block ads.

I wonder if AI will be able to convince firms that 90% of advertising dollars spent is a complete waste of $$$. Tesla does ZERO advertising. Apple has mostly stopped advertising. But no marketing VP is ever going to admit to the CEO, “The hundreds of millions of $$$ we spend every year on ads is not contributing anything to our revenue.”

Intelligent Dasein

Agreed

I dont know how you dont see the use cases for them? so many people are way off the mark…so AI is now doing PHD level work…that is only a small part of it. LLM’s are a game changing technology- anyone who thinks differently is just out of touch. I am personally working on stuff that will lower our costs by several BILLION dollars and it’s not far off stuff- it’s this year stuff. Because you use Chat GPT doesn’t make you an AI expert.

This AI data-center boom echoes railroads or fiber, massive capex before we really know if the productivity shows up. We are probably already running into diminishing returns on scaling, but the spending just keeps going.

Also, big part of the AI story is “augmentation” (not replacement, as they say) one person doing the work of many. But if that’s true, what happens to the other workers? Let’s say mass layoffs don’t happen, the idea then is that productivity would rise because output per worker goes up. But if AI lets, for example, one lawyer do the work of three, or one marketer produce 10 times content, or one analyst run 100 times simulations. Do we really need 3 times more lawsuits or 10 times more ads or 100 times more reports? I would think not. So the extra capacity doesn’t automatically translate into extra spending.

I guess it all depends on whether AI creates new categories of spending or mostly optimizes existing ones. Either way, I think it will be less than the capex implies.

It’s like the Adam smith pin factory.

AI taking jobs frees humans to do other more important jobs.

As the specialized slower pin masters can do something more beneficial for the nation.

In theory

Automation has worked very well for the economy over the past many decades.

Offshoring to cheap-labor countries and for tax benefits, and then importing those goods, has been a disaster for the economy and national security.

It was surreal to me that the second point you make was basically incomprehensible to those in US government and business until the past few years, when all of a sudden they realized how vulnerable the USA is relative to e.g. China. We are now in another cold war type scenario with at least 2 major adversaries in China and Russia. The situation had to get very far gone before they even had a clue. I sometimes still wonder whether they’re fully awake to the threat.

And labor.

Excellent comments/insight.

There is an increasing amount of information coming out about the limitations of Large Language Models (LLM) that the AI industry hopes will go away by super scaling. Everything I’m able to glean so far is that the super scaling won’t fix the intrinsic problem.

What this means to me is that at least for current LLM technology, the results of AI will have to be checked if 100% accuracy is required. If this is true, the application of AI (while still large) will not be the “rule the world” theme we have often heard.

I go back to the legal usage. Yes AI can assemble some pretty impressive contracts…but, they will still have to be reviewed by someone that knows their stuff. And if one doesn’t do the basic research to form the contract, how does a reviewer know where the error(s) are? Where the context is not correctly assimilated.

I am forming the belief that AI (at least in the current LLM technology) is not going to provide the types of massive productivity that is being claimed. And scaling the LLMs up to massive levels) is not going to eliminate the underlying weakness (hallucinations).

The problem with this line of thinking is that it conflates AI with LLMs.

It’s like saying the internet is just eCommerce.

AI is the paradigm, a platform that can be developed into a wide variety of things, in an equally wide variety of ways.

The permutations are probably nearly infinite.

Scaling a bad solution has never been the answer (and often doesn’t stop people from trying: see all commodities boom/ bust). It also is not preventing the competition from continuing to innovate.

Dismissing the potential of technology is simply foolish or wishful.

Sounds like it’s going to supply more of the blue collar labor jobs needed in the economy for a while until the robots cometh anyway.

The profits from the productivity gains that do show up will continue to accumulate to the top as have the computer boom gains over the last 30 years. Our “new” K shaped economy will be even more divergent.

Just gotta watch out for the political power grabs as AI starts tracking our every move for the corporate and sovereign types… may not even have to wait that long as they’re in the woodworks already. Seems a pretty good chance they’ll manufacture consent for handing over democracy using the data to herd the masses around again.

More strong men will save the day for sure. /s

You can’t tell where the freed up resources will be deployed. No one in the 1920s could predict that the great grand children of the out-of-work farriers would become website designers.

Similarly the smart people all predicted the demise of Standard Oil when electric lights were introduced in the 1890s. As predicted the demand for kerosene for lighting dropped, and at that time gasoline was a waste product inherent to the refining process.

The problem is that the freed-up resources are _people_ .

Unless we’re turning them into human sausages, there’s a bit of a problem.

As one of 5 ”estimators/analysts” of construction costs with a very good company in1985, with no computers,,, WE did about 6MM per quarter…

As the only such employee in 2009,,, I did about $40MM per quarter! With computers, but without fancy software, though I helped, when asked, to review and vet on screen takeoff and other similar software being developed at that time, even though I could do what that software did faster and more accurately AT THAT TIME.

So far as I have been able to discover from reading, lately, AI is very likely to provide similar cost efficiencies sooner or later.

You were faster and more accurate than bad software running on a base 3.4 GHz Core i7?!!

Not messing with you. That’s impressive.

Railroads are a great example. Every major railroad in the U.S. went bankrupt in the 1890s. A result of over investment that failed to make a profit. The demand for rail services increased rapidly, but capacity investment outpaced demand. The failure of these projects to meet profit expectations, caused bankruptcy and led to an economic panic and market crash.

Wrong…Southern Pacific Company of Kentucky controlling Southern Pacific of several states, Central Pacific, Oregon & California, and numerous other subsidiaries never went bankrupt period. Around 1900 it was the third largest railroad covering a greater distance and had steamship connections from New Orleans to New York (Morgan Lines). It also came to control Pacific Electric Railway of California. It was one of the biggest companies in the United States. It was not folded until the 1930’s when a new Southern Pacific of Delaware was opened. Ultimately, the railroad entity, less all the assets given up in the Santa Fe merger, became the core of Union Pacific Corporation and reportedly absorbed that subsidiary railroad. It was then re-named as Union Pacific. Technically, if accounts are true, it still has never gone under.

It’s not hard to reason it out using the examples you cited. How much of a force multiplier was the railroad? Or the Internet? Or Wireless comms? Or satellites? People will be freed up to do other things, which they will. It will make society better not worse, there may be people left behind, there will be lots of job losses…but just like with the other things- people will go do the things and work in jobs and we will all be richer and better off for it.

Excellent article Wolf.

Can you now apply this analysis of A.I. spending to upcoming earnings pressures? My understanding is that these “hyper scalers “ have extended the depreciation schedule on the expensive chips they are buying.

Yet earnings pressures are mounting, correct?

The practical use of A-1 would be to get rid of over-compensated executives versus worker bees. A-I does what executive are supposed to do. Manage and guide employees.

As for stock buybacks, they should be banned or taxed heavily. Instead of buybacks, pay dividends. They are only used to boost the churning of stock option awards and how exactly do they benefit when exercised at high prices, then the stock falls? Just for the execs.

Also, where is Tesla, et al, on your list?

Investments not big enough to be included here. It’s among the smaller players, such as Apple.

“Hey, My horse has more than “one horse power” ! And he is offended, Henry Ford would suggest such a thing” pssstt!

Great article! Finally, a data-driven analysis of company cash flows and AI proposed investments. This article obviously required actual research on your part, which is generally lacking from other more famous investment sites. Thank you for your efforts.

Seven companies does not a market make. There are another 4,993 US companies in the broader market out there that sell for a lot less than 200X future earnings. Especially in the small cap arena. Follow the cash. What companies have contracts with the AI Big Spenders? $700B is a lot of future revenue and EPS for a lot of great tech companies who must continuously build out support for the AI and Bitcoin mining infastructure. Go back and look at Oil Service companies vs. Big Oil company Capex when Oil prices are high.

Dividends?

Buybacks hace juiced the market while reducing PE ratios. Once they stall, investors will face a real dilemma where ROI will have to increase dramatically to offset PE gains. Apple has been smart to sit this one out and let others spend spend spend biding its time to buy appropriate AI tools for its platforms.

As for economy, there should be concern about inflationary pressures on labor specifically trades like HVAC and electricians. There will be cost pressures on anything requiring chips and memory. Then there’s strains on energy and water. No free lunch.

I have to admit that a part of me is concerned about some of the motivations behind this spending spree. I think it is about more than just building a profitable business. Whoever wins the AI race will have tremendous political and social influencing powers. If everyone just asks AI for all the answers to any questions, then the runners of AI can influence and control how a future generation thinks. Kind of scary.

Regular internet search, totally dominated by Google, has offered this problem for two decades.

“When every one thinks alike, nobody thinks.”

I’d be more concerned about monetization of AI searches. I can search any headline from a news outlet such as Bloomberg, NY Times that have paywalls and receive a summary of the article. And, on top of that AI searches no longer have ads unless you check sources that include ads.

AI has been around for decades under the name of machine learning. There have been positive benefits for specific industries especially medical imaging. However, large language models have issues such as repeatability. Any use that requires the same output for the same input will have issues. This is a big problem for accounting/financial services that require audits.

If the hyper traders – who traded the Mag7 for twenty years, splitting them multi times – lift QQQ to a new all time high, the Mag7 market cap will rise above China GDP, slightly below the US GDP, for distribution. TGA can rise from $908B to $1.5T. Don’t blame Tim Cook and Jensen Huang. Blame wall street. Wall street will send the markets down.

I don’t get how these expenditures are a great economic stimulus. They create a small number of construction jobs, and the chips that fill them are mostly made by machines. Once running, they require almost no human supervision. Great for Nvidia, but who else?

You don’t understand what is happening here.

Read the article again; especially the latter half. The money was sitting on the sidelines; now it’s going back out into the wider economy, at least for some time — and during that time, it may stimulate people to buy more goods.

just like the dot-com fiber buildout, some of this investment will not earn its cost before it’s obsolete. The chips and the servers will need to be written off and replaced in years 3-5 as the technology moves past it. So these companies need immediate payoff because they have to do a lot of it all again in 3 to 5 years sans the land, buildings, and power infrastructure. I don’t see them achieving their revenue goals before obsolescence touches their servers/chips. I think Nvidia come out with new chips every two years.

It is shoot first and ask questions later at AI companies. They are all cowboys. Who is going to end up at the Golden Coral?

So many experts

Wow. The top is in. The last bear giving in :)

RTGDFA?

What does it say about stockholders and investors? They’re paying for all this. See ORCL, as noted.

I should require a pop quiz about the article before people can comment.

Well, semiconductors and NVDA still going strong. And this is what I am talking about. Saying for years that AI is real. For years proven better than t bills and chill. Cheers.

LOL thats actually a good idea.

Now that would be ground breaking. But then we might not see as many ‘retorts’, ‘corrections’, admonishments’ which can be enjoyable(if one is not on the receiving end).

Thanks for the work you do.

Great article Wolf…. I find it interesting that NOONE mentioned the obvious beneficiary of this massive spending. AMD reported last week and their gudiance for their AI chips was lower than expected.

Meanwhile, NVDA STILL has an enormous market share, somewhere north of 85% right now for GPUs and just made a huge licensing deal w/Groq for inference chips and technology not to mention make muti-billion dollar investments in many start-ups with new technologies. CEO Huang is pounding the table saying the demand is insatiable and had the foresight to have previously made long-term deals with Micron and other HBM chip makers to ensure supply in an industry that is becoming very constrained.

All this adds up to the likelihood of blowout earnings for the next few years. UNLESS, of course, something changes or a Black Swan event happens. YMMV :-)

Happy NVDA owner since DEc ’17

power shortage?

Excellent article and insights Wolf.

Pretty amazing to see how money has been moving throughout the economy lately. 2026 looks like it will be a wild ride.

Stock Bubble Update: S&P 500 total market cap now $62.78 Trillion.

Top eight tech stocks (Nvidia, Apple, Microsoft, Amazon, Google, Meta, Broadcom, Tesla) total $22.53 Trillion, or 35.8% of the entire S&P 500.

Micron Technology +AMD together= $784 Billion. Palantir Technologies market cap is now $324 Billion, down from almost a half Trillion, but still far above IBM at $279 Billion. Palantir EBITDA is $1.44 billion, IBM EBITDA is $16.78 Billion. You can’t make this stuff up.

The equal weight S&P and even the Dow are both outperforming the SPY and the QQQ so far this year, so maybe the market is finally sending a message.

Reminds me of 1998-1999 “topping”of the NASDQ. Tech peaked and by 2002 had dropped about 80% but, value and small stocks did well until mid- 2001 and then everything finally went with the trend and got pounded. When it was all said and done the S&P had dropped about 50%. But, this time might be different.

CAT sent the DOW to 50K.

It was only a few years ago that reducing carbon in the atmosphere was a priority. We were supposed to reduce carbon output. Not so much anymore. The energy needs of AI are enormous. If carbon production must be curtailed to save the planet, will we have to one day choose between air conditioning homes and self driving cars as an example?

It just goes to show much of this is politicized. BigTech is considered “left” while BigOil and Wall Street are considered “right.” It looks like BigTech is getting a pass on the electricity usage because they’re on the “correct” side.

Just my perception.

Check out the left-leaning opposition to Elon’s natural gas turbine powered data center in a poor neighborhood on the outskirts of Memphis.

what’s the matter with gold editor in chief ?

They seem to have spent a Billion or two on Super Bowl ads as well!

It is not as bad as the 2000 Super Bowl when 14 Dotcom startups spent multi-millions on ads. In a few years, most were gone or acquired.

Let’s see if Anthropic and OpenAI are still around in 2 years.

I used to joke that when a startup had a Super Bowl ad (or a stadium named after them), they were about to go under.

I wonder how much of this cash will go to imports? Taiwan’s GDP growth in 2025 was 8.6% and looks like 2026 ai investments in US are going to double.

Stanford, MIT, CMU… computer departments are the first victims

of AI.

Possible to tell how much of the debt issued by these companies is bought by Nvidia, OpenAI, and other such companies?

Is the debt issuance part of the mutually-reinforcing investments among these actors?

I’d feel better if the debt were purchased by a broad variety of buyers, as that might signal more confidence in the spending projects.

Continuing the greatest capital and resource mis-allocation the world has ever seen.

Hedge accordingly.

Super Bowl #60: they worked hard for the kicker. He, the MVP, scored over 50% of the points for the Seattle.

Some trouble will come later this year? when OpenAI and SpaceX go public. I don’t expect any disagreements here I guess.

Why are we so worried here, these companies all generate enormous cash flows and will be allowed to account for these expenses in a tax efficient manner, i.e., something approx. 40-60% of Alphabet is for direct capitol investment that can be accounted for with depreciation etc. I’m sure they are not going to be silly with the rest. This spending could facilitate the tax efficient repatriation of large global capitol hoardings.

Also, one must begin to think differently regarding certain categories of data center. Some make cat photos while others may be counted in a similar manner to how many aircraft carriers a nation has. Perhaps not today but very soon.

“while others may be counted in a similar manner to how many aircraft carriers a nation has”

This is a refreshing thought.

“Bismarck Sea” was the last one we lost, Feb 1945, in the battle of

Iwo Jima.

AI will most certainly transform the economy and world. It’s just starting. It’s not really a debatable point. Every company will use it. Many of the commenters think their AI search tool is what AI is….It’s the very small part of it. Nearly every job will be automated and become far more productive. Software development is now 10x, call center work will be 5-10x now multiply that across the entire economy. People talk about open AI and it burning through 100 billion- Yep they might lose money, but Microsoft, Google and Amazon wont. This is good for the economy, money is being used to for capital projects and the cost profiles of nearly every business have gone down immeasurably. It will be the internet x 10.

I think where we disagree is to how to define “AI.” I don’t see it making actual decisions and replacing human thought anytime soon.

Much of human thought is easy to replace: the “hallucinations” as it’s called with AI, that humans think up every day all day long, the BS they fabricate in their brains, their awful memory (limited, selective, and deceptive), their inability to learn much, their inability to think through complex problems and lots of data (they need computers to do that, lol), their inability to handle complex math (computers needed), etc., horrible erroneous decisions, etc. The list is long.

AI has long ago outperformed humans without computers. Humans with computers are a little harder to beat. Humans with AI might be harder to beat still, but then that’s already AI.

Where else you all going to invest if not some tech stocks? I fling computer code for a living. I see what AI is doing. My back-up job of the future is to fix mistakes from AI code unless they come up with AI checkers. If AI checkers are so good, it would take over AI itself. Who knows.

As for outsourcing our jobs overseas. We have two cases: India and China.

China focused on manufacturing while India focused on services.

Who won? China. Youtube this video and watch for yourself:

“THE most advanced city in the world?! How? Let me show you!”

@Ross

Feb 9, 2026 at 4:00 pm

“I wonder if AI will be able to convince firms that 90% of advertising dollars spent is a complete waste of $$$. Tesla does ZERO advertising. Apple has mostly stopped advertising. But no marketing VP is ever going to admit to the CEO, “The hundreds of millions of $$$ we spend every year on ads is not contributing anything to our revenue.” ”

Ross, your comment made me think about what frequently happens when I watch TV series or movies with paid ads on streaming services. When an ad comes on, I automatically mute it and tune out, get something to drink, bathroom, etc. If fact, I can spend an evening watching TV for 3-4 hours, and I can not tell you the contents of a single ad. It is similar to when you drive home from work and you are startled pulling into the driveway as you can not recall any of the route. I have often wondered how many other people do the same tune out process, and if they have a way to measure the effectiveness of the ads. I tend to think not. If they did, they would eliminate most of the ads, and the free streaming services would go belly up.

Nope- a few things for you to noodle on.

There is a saying 50% of ads are wasted, you just dont know which 50%.

when the internet came around, everything became easy to measure- you can see how someone got to your site, what they did, when they abandoned, how long they lingered on a page. Internet advertising is very data driven and analytical. TV ads are the same way now. They have the telemetry to measure everything, and see how much incremental sales/revs/looks etc something drove. Because you get a beer and took a leak during this one ad, doesn’t mean everyone does. Apple and Tesla are very specific unicorns as it relates to ad’s mainly because of thier established brands. Tesla from its founder and Apple because it built a brand over decades…starting with one of the most memorable ads of all time. You are very very off the mark on this.