But their massive capital gains, realized and unrealized, are not included here.

By Wolf Richter for WOLF STREET.

Americans’ personal income – which rose 4.3% year-over-year in November to an annual rate of $26.4 trillion – came from their wages and salaries, from their small businesses and farms, from their rental properties, from dividends and interest income, and from transfer receipts from the government, such as Social Security benefits paid to retirees. And we’re going to look at that in detail.

But the massive capital gains are not included in this income, neither on homes nor on investments, which is a huge factor in the US:

About 65% of households own their own home, about 62% own stocks, a significant part holds precious metals and cryptos. But the massive capital gains – realized or unrealized – over the past many years are not counted here as income.

Stock ownership is widespread: 87% of households with more than $100,000 in income own stocks, according to Gallup. So is that the upper crust?

The median household income for married-couple families in the US was $120,217 in 2024, per the Census Bureau. “Median” means that 50% of all married couple-households made over $120,217 in income in 2024, and 50% made less than $120,217.

So, well over 50% of married-couple households earn more than the $100,000 threshold for the 87% stock ownership category.

For nonfamily households – a person living alone or unrelated people living together – the median household income was $49,848 in 2024, according to the Census Bureau. And the overall median household income was $81,604 in 2024.

Among households with incomes between $50,000 and $100,000, 71% are invested in stocks.

Even among the lower-income households (less than $50,000), 28% hold stocks, according to Gallup.

And it starts early: Among young people (18-29 years old), 44% are invested in stocks. Gallup did not provide data on holdings of cryptos, and young people are deeply into them. And Gallup didn’t provide data on precious metals either.

All these investments – real estate, stocks, cryptos, precious metals – had huge price gains over the past 10 years, leading to massive realized and unrealized capital gains, but they’re not included in the income figures here.

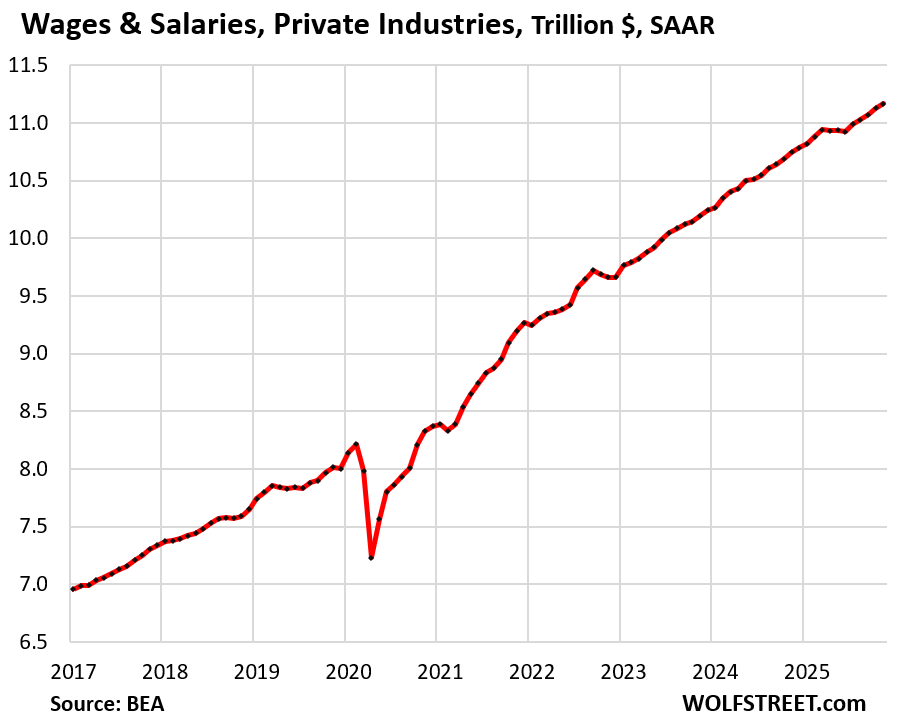

Wages & salaries in private-sector industries rose by 3.9% year-over-year to an annual rate of $11.2 trillion, according to data from the Bureau of Economic Analysis.

They accounted for about 39.2% of pre-tax personal income.

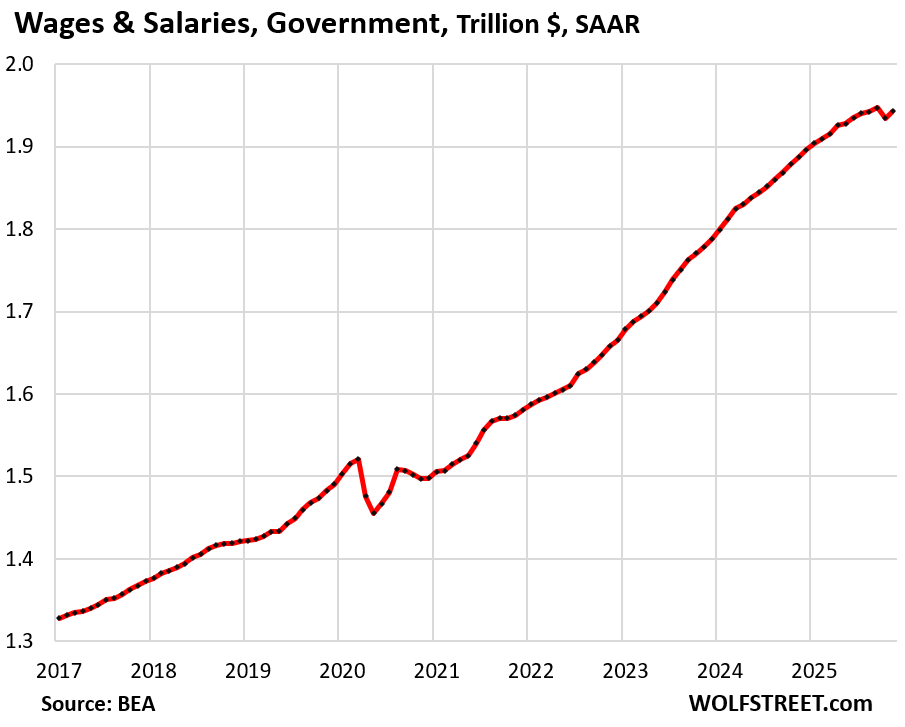

Wages & salaries in government rose by 3.0% year-over-year to an annual rate of $1.94 trillion in November.

In October, there was a drop in income as employment at the federal government plunged by 179,000 jobs, largely the result of workers who’d volunteered to exit earlier in 2025 but who, as part of their severance package, had continued to receive salaries through September 30.

So the uptick in income in November from October did not set a new record, but was below the September record.

Government wages & salaries accounted for 6.8% of pre-tax personal income.

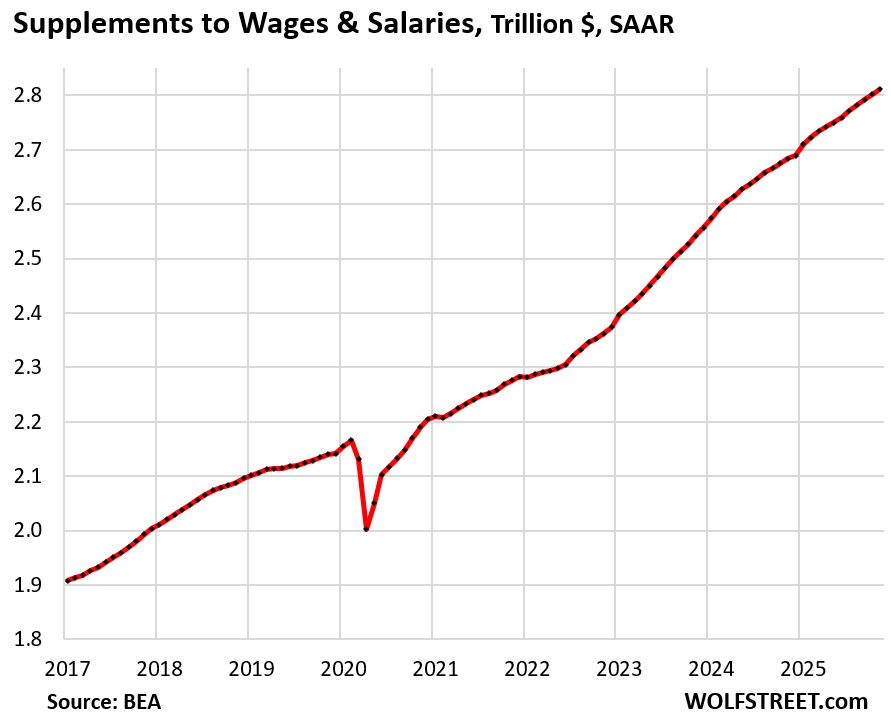

Supplements to wages & salaries rose by 4.8% to an annual rate of $2.8 trillion in November. These are the amounts employers paid for their employees in two categories:

- $1.89 trillion: Employer contributions to 401(k)s, retirement funds, and pension and insurance funds.

- $0.92 trillion: Employer contributions to Social Security, and other government social insurance.

Supplements to wages & salaries accounted for 9.9% of pre-tax personal income.

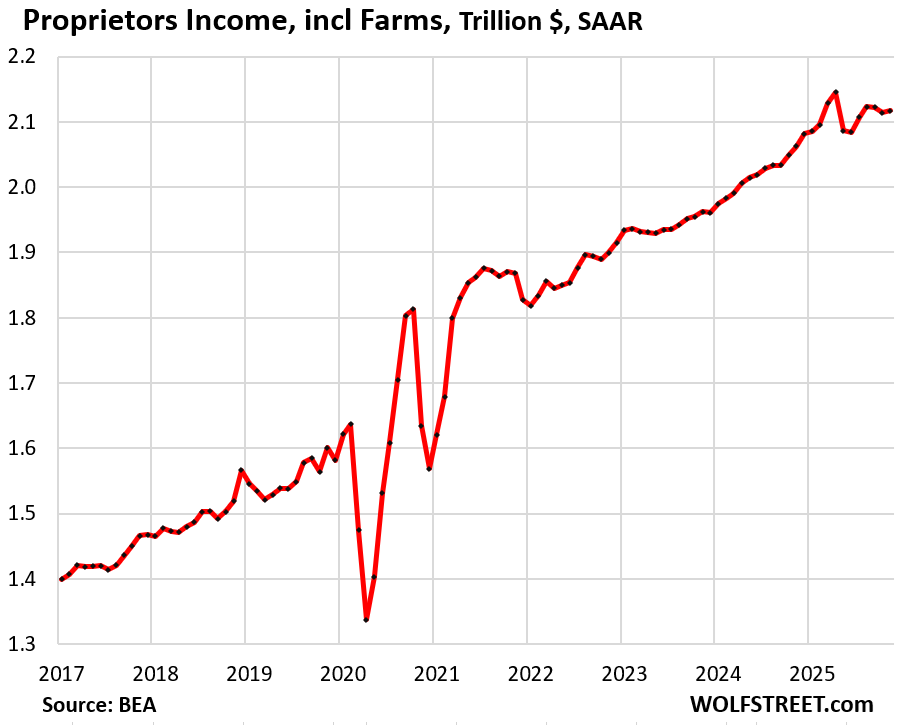

Proprietors’ income from personally owned small businesses and farms rose by 2.6% year-over-year to an annual rate of $2.12 trillion, nearly all of it from businesses ($2.05 trillion annual rate), and very little from farms ($68 billion annual rate).

It accounted for 7.4% of pre-tax personal income.

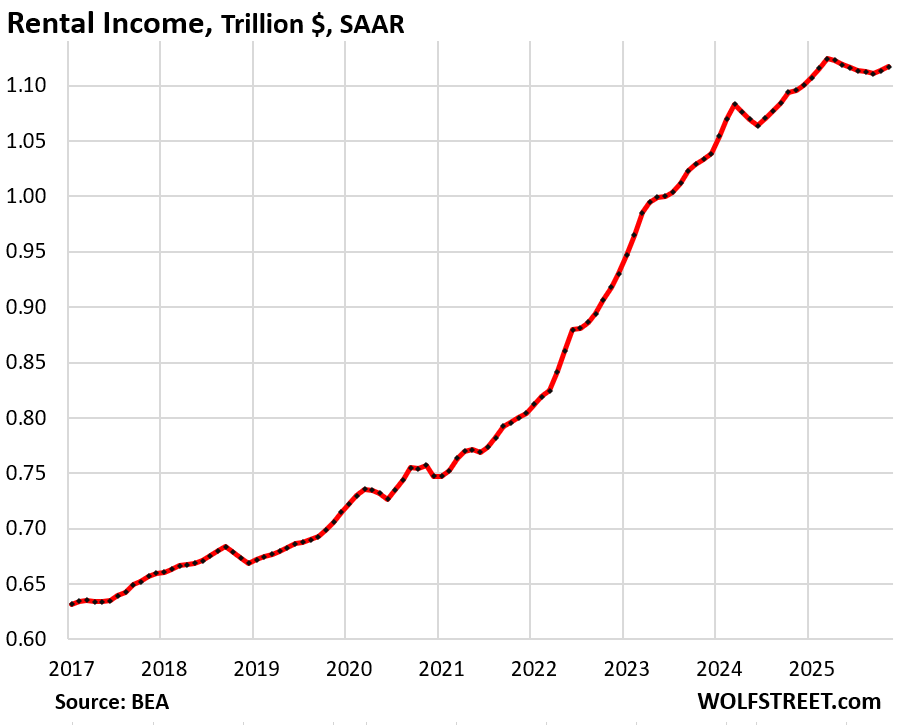

Rental income from personally owned rental properties rose by 2.0% year-over-year to $1.11 trillion.

Roughly 11 million single-family homes are owned by mom-and-pop landlords (1-9 units), and many condos are owned by mom-and-pop landlords, either for long-term rentals or short-term vacation rentals. And these mom-and-pop landlords often have a day job, and managing their rental properties, which is at least a part-time job, puts them into the category of the infamous “multiple jobholders.”

Rental income accounted for 3.9% of pre-tax personal income.

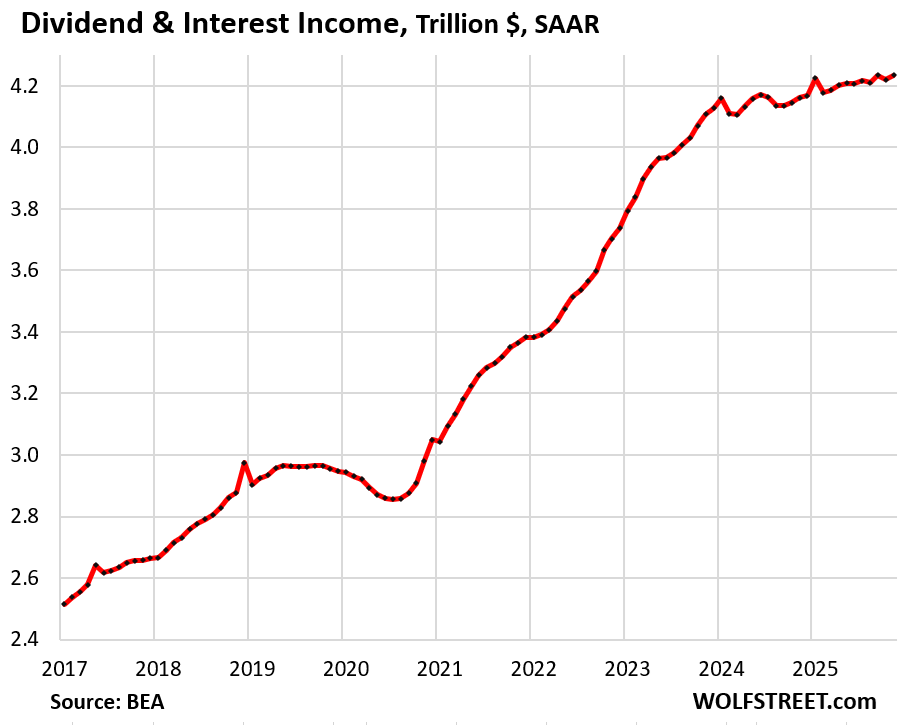

Dividend and interest income rose by 1.7% year-over-year to an annual rate of $4.23 trillion.

Americans hold lots of bonds, money market funds, CDs, savings accounts, etc. Households have $4.8 trillion stashed in money market funds alone; there are $3.5 trillion in CDs outstanding. We discussed that pile of interest-earning investments here.

In addition, dividend income from stocks is substantial. While capital gains from stocks are not counted as income here, dividends from stocks are counted.

Income from dividends and interest accounted for 14.9% of pre-tax personal income.

Personal transfer receipts rose by 8.8% year-over-year to an annualized rate of $5.06 trillion. This includes Social Security benefits paid to retirees, Medicare and Medicaid benefits paid to healthcare providers, unemployment insurance, VA benefits, etc.

- Social Security benefits: $1.58 trillion

- Medicare: $1.27 trillion

- Medicaid: $1.07 trillion

- Unemployment insurance: $0.04 trillion

- Veterans’ benefits: $0.31 trillion

- All other: $0.69 trillion

The year-over-year increase was in part driven by the rapidly growing number of boomers receiving Social Security benefits and by an expansion earlier in 2025 of who receives Social Security benefits, which included a one-time payment of catch-up benefits in April, which caused Social Security benefit payments to surge in 2025.

Personal transfer receipts accounted for 17.8% of pre-tax personal income.

The massive spikes during the pandemic were the annualized rates of the stimulus programs, forgivable PPP loans, etc. Annualized rates roughly multiply a monthly figure by 12, and seasonally adjust it, so when unique things happen, such as a one-time stimulus payment, it is also multiplied out as if it would occur every month for 12 months in a row to produce an annual rate, and then over the next few months when those one-time payments no longer occur, it all collapses again. I have loudly but vainly complained about annual rates during the pandemic, when they were producing these grotesque results in a lot of economic reporting:

![]()

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Why are stock dividends counted but capital gains from stocks not counted?

Where would that be counted?

Capital gains are not counted in personal income; they’re not counted in GDP either. Nor are losses. When money from capital gains gets spent on goods and services or invested in fixed assets, then it’s counted in consumer spending and GDP.

Thanks wolf for that clarification

Unrealized gains would make that more clear what is not counted. Once realized and subject to tax, they are counted.

Bullshit. RTGDFA. This is not about taxes but about tracking consumer incomes, which EXCLUDE CAPITAL GAINS REALIZED AND UNREALIZED.

YOU don’t get to decide what is included in this income figure. The BEA does that. RTGDFA

It must be unrealized gains

The point of GDP is to count what the country produced. That’s hard to calculate so we usually use identities to work it out from things we can easily measure, usually expenditures.

In theory this is equivalent to GDI (the sum of all incomes), but sometimes differs a little due to data availability and uncertainty.

Both measures exclude capital gains because they are not a thing that was produced.

real GDP should be reported instead – ie NON-GOVT entities

nearly 40%+ of GDP now is from GOVT spending/ie debt

36% total including state and local government. Federal is 22%

Also, every country that spends a smaller percentage of GDP on government is much poorer and more corrupt than us. Japan, Australia, and New Zealand are closest, but they’re all at 40%.

1. That 40% figure is BS. Combined, federal, state, and local government consumption and investment accounted for 17% of GDP.

2. The GDP data release always includes a measure without government and without trade. All you have to do is my articles on GDP, because I give you those figures of GDP ex government, including this chart below.

It’s called “Final sales to private domestic purchasers,” a measure of the private US economy. It excludes exports, imports, government consumption expenditures, government gross investment, and changes in inventories. It covers about 87% of GDP and represents the core of the private US economy.

Final sales to private domestic purchasers rose by an annual rate of 3.0% in Q3, the best growth rate since Q4 2024, to $21.0 trillion.

https://wolfstreet.com/2025/12/23/whoosh-went-the-economy-in-q3-the-fed-needs-to-watch-out-economy-is-running-hot/

Why would you count capital gains until the stock/asset is sold? Until that point, they’re just numbers on a computer. You don’t lose it gain anything until it’s sold.

… And I should’ve read on until people mentioned unrealized gains already. Nothing to see here.

or one could consider what Wolf just said

The median household income for married-couple families in the US was $120,217 in 2024, per the Census Bureau. “Median” means that 50% of all married couple-households made over $120,217 in income in 2024, and 50% made less than $120,217.

I’m probably having a bit of fun when I say that the statistics sited above indicate that the all important middle class is thriving.

The tonic of funny money has that effect, historically speaking

Another way to look at it, is that the charts are tracking *spendable* income – as an old professor used to say “money you can buy beer with”.

If I understand your definition of “capital gains” you are talking about *unrealized* gains – so those funds are not really spendable (and are actually pretty theoretical, once you think about it).

There is value in focusing in on just *spendable* funds in the charts – for me they provide a broad (very broad) sanity check on reported GDP figures (which, due to their aggregated nature across sectors/entities, can be harder to grasp/intuit/believe…).

Despite these “personal income” charts still falling a few trillion short of reported GDP (which shortfall I’m sure there are roughly reasonable justifications for), at least GDP and Aggregate Personal Income figure are (very) broadly in line.

Which is useful (I think it is a very, very, very good thing to cross check huge gvt metrics for sanity – since a *lot* of gvt metrics may not really be measuring exactly what the mass of people think they are – their methodologies/exact calculation being a lot trickier than that).

“these “personal income” charts still falling a few trillion short of reported GDP”

Good lordy.

1. GDP doesn’t measure “income.” It measures “spending” (consumption) and “investment.”

2. GDP measures the entire economy, including businesses and governments, not just consumers.

Ok, thanks.

Kind of confusing, because it is taxed if you sell it for a gain.

By the way, bear with me, I am still learning…haha

One would think realized capital gains would be included in a metric somewhere, even if not in this particular metric. I know the IRS thinks that I must pay income tax on any capital gains from stock sales.

They’re not included in GDP either. None of the economic growth figures includes capital gains. And that’s how it should be. Once people spend those gains, then that spending is included.

I love your clear and concise answers.

Understood as to GDP, but it seems like a poorly-designed metric for measuring income. If I make my living by buying low and selling high, and live frugally, the metric fails to accurately report my income. Just because I’m re-investing my gains rather than buying stuff doesn’t make it any less income. However, this metric seems designed to hide such income.

There are other measures that track wealth, and how it changes. Or you can just look at the indices of the stock market, the housing market, the crypto market, etc. and you get a feel for the capital gains and the changes in wealth they engender.

That’s how I make my living, and yet it seems to me a lot like my capital gains are simply wealth preservation in the face of inflation that I get the pleasure of paying taxes on.

“Just because I’m re-investing my gains rather than buying stuff doesn’t make it any less income”

Until you *realize* those gains into spendable income – how *real* are they?

Stock values fluctuate every single minute of every single day – occasionally with *huge* volatility – are those “values”/figures really the same thing as the money tracked in the personal income charts?

At a macro level, think of the huge distortions introduced by trying to include SP 500 aggregate value (at 30+ PEs, due to meth smoking…) versus SP 500 aggregate value (at 15 PEs, the historical average).

You would be trying to compare apples (spendable personal income) and LSD infused oranges (ZIRP-addled asset market valuations)

Otherwise the gains plus the spend would be counted twice .

Not sure on wallstreet with all the trading that occurs in seconds trillions probably changes hands which should not be included in GDP. That money stays within the confines of the publicly traded companies

Logically, from the perspective of the democratic distribution of opinion I think that capital gains should be taxed as ordinary income in the year in which it was realized. Just like the rest of us.

Are annuities, pensions (private, military and civil service), and IRA & 401(k) withdrawals (RMDs) included in personal transfers, or are they too small to be counted?

Distributions from annuities and pensions are excluded from income on the logic that they’re a reduction of your assets you squirreled away previously, same with IRA or 401k distributions.

I investigated a certain class of annuity that had the structure of a zero coupon bond. Designed for reducing taxable income while rolling a traditional IRA into a Roth environment,

A bit surprised one would want an annuity inside a Roth . But there may be some great reasons

I was really surprised to learn 62% of households own stocks. I would have guessed half of that.

It makes sense.

The entire S&P 500 is now simply too big to fail. Imagine trying to get elected if you’ve allowed people’s 401k’s to drop! We will borrow from the future forever, inflation be hanged.

At some point, they won’t be able to stop it from failing.

It’s not that remarkable when you consider many (most?) companies put new employees on 401k auto-contribute (it makes it easier to pass the ERISA discrimination test).

Gabriel,

I think the number of US adults that own taxable brokerage accounts is around 35%. Not relevant to the overall conversation but you can find various breakdowns. I suppose some things fall in the middle as well like Roth accounts but probably a small percentage.

You don’t need a brokerage account for a 401k. 401ks are the dominant way in which Americans own stocks, no brokerage account involved.

Except we don’t own stocks until we “Realize the gains” lol. This is fun. And you’re not allowed to realize those gains until you’re retired. So my question then is how the heck do banks underwrite loans that are made against holdings? SBLOCs? If I can just pretend to realize my gains by getting an SBLOC and pay a percentage rate on the loan instead of a 10%penalty plus taxes for a distribution, then why isn’t every household of that 62% who “own stocks” taking out SBLOCs or are those type of loans only reserved for the companies manipulating their holdings? A guaranteed SBLOC party now Vs. Maybe my portfolio holds value and supports my retirement. Lol right. The answer is those of us that play by the perceived rules always lose because no one else plays by any rules they didn’t make for themselves. And the rules they make for themselves guarantee that they win whether or not those 62% of households with stock holdings win or lose. (It’s cold and snowy here in the Midwest today so I had nothing better to do than rant in Wolf’s comment section. (= Cheers

“Except we don’t own stocks until we “Realize the gains” lol”

You got this backwards. The correct version is: We own stock until we realize the gains (by selling the stocks), at which point we don’t own the stock anymore; someone else does. But we have their cash.

And then you base your entire theory on this upside-down and reverse-backwards line?

Okay it’s backwards but I still don’t understand how SBLOCs work. I will go back and find the article that references them – I had to have missed some important information there.

I have described Securities Based Lending (SBL) and Securities Based Line of Credit (SBLOC) many times usually when it blows up, because that’s when we find out about it.

At a very basic level, it is a way for people with lots of stocks (hundreds of millions or billions of $) to put up their shares as collateral for a big loan or line of credit. Just like a margin loan for little people. You can get a margin loan in your brokerage account by running a negative cash balance. For example, if all your money in the brokerage account is invested in stocks, and there is no cash in the account, you can withdraw cash (for a vacation or a down payment or whatever) and pay margin interest to the broker. You’re borrowing against your stocks when you do that. There is no requirement that you have to buy stocks with the loan. But when the prices of your stocks plunge below certain levels, you will get a margin call that forces you to either sell some or all of your stocks at the beaten down prices or put lots more cash into the account. In other words, you will join the hordes of forced sellers during the market downturn.

SBLs work the same way, except they’re negotiated directly between the rich client and the bank/broker since the amounts are huge and the clients are very rich. The failed First Republic Bank in San Francisco had an entire department that worked with rich people to lend against their shares (often illiquid shares in startups). I knew a guy years ago – a reader here – who was working in that department.

Here is an entertaining example of a big SBC loan that blew up into the face of the banks. Read this. It will help you understand how SBLs work and who bears the risks:

https://wolfstreet.com/2017/12/19/margin-debt-backed-by-steinhoff-shares-hits-bofa-citi-hsbc-goldman-bnp/

@Gabriel remember every “person” in every “household” does not own stock so the percentage of “people” that own stock will be lower.

No. 62% of actual population own stocks. That stat is quoted in both public and private data.

ApartmentInvestor

That’s a BS statement. Think about it.

Are we talking about realized gains ?

RTGDFA

Ha, Badge of honor. Thanks Wolf for posting the definition of rate check earlier today and putting all the work in to put out the stream of information. It’s good site for us information junkies.

People don’t realize how wealthy America is. There are issues but nothing big in the context of the world. With the Trump accounts coming online this year , every child born will have a $1000 deposited in an S&P 500 index fund. That means future generations 100% of Americans will be invested in the stock market. Great way to become wealthy.

*how weathly our corporations are

Fixed that for you!

/s

This cynical way of seeing things and not being positive is the problem. No nation is perfect. No nation.

I don’t think it is an issue of being positive or negative but simply seeing things as objectively as possible. Admittedly the world is complex and people can parse facts how they want, but doesn’t ignore objective reality exists. I do think the approach of always pointing to problems elsewhere serves as nothing more than a distraction however.

Corporations ARE people, my friend.

Let’s not forget that America owns way more gold than any other entity on the planet, and that asset class is seeing huge increases.

As to why they don’t realize it, you can thank the always-negative media for that…

The US Treasury owns around 8 thousand tonnes of gold bullion which at the official price of $42.42 per ounce isn’t worth more than around $10 billion and it isn’t for sale. Even at market prices approaching an absurd $5,000 per ounce the total value of US officially owned gold is only about 50% of the current federal government annual deficit.

Nice try – that’s book value! Now do market value!

The total value of all gold in the world is less than all the items and services that the US produces in a single year.

I’m not asking to compare gold value increases in the U.S. to the U.S. – compare it to the rest of the world. Gold in our vaults appreciated about $460 bn in 2025 alone, which is more value increase than the GDP of about 82% of countries on an individual basis. Our gold value increase alone was about the GDP of Denmark…

Think about that. Yes, if you compare our gold to our economy it looks small. When you compare it to the value of most economies, it far outweighs them.

That’s just our gold.

And that $460 billion is about what the US produces in 5 days, so who tf cares?

It’s also about 8% of federal revenue.

Of course it’s bigger than the rest of the world. The US is one quarter of the world economy (for now), and the third largest population on earth! Literally every measure you pick will be bigger than most countries in the world!

Man, gold bugs! They know shiny things but they sure don’t know math!

Kirk,

Struggling to comprehend the point you are trying to make or if simply stating a fact that is largely irrelevant.

If America is so Wealthy. What does the money actually buy?

The other side of wealth is access to quality Goods and services. Otherwise it’s just paper in most cases.

But if it’s Gold and precious stones these have their own aesthetic value.

Obviously, US Dollars buy anything and everything for sale in the world that is denominated in US Dollars which account for 80% of all global transactions. Gold and gemstones will be just as beautiful as they are today if gold drops to $20 per pound.

The problem with all this so called wealth, it’s in assets and that float in value. Debt loads are fixed unless discharged in bankruptcy. When wealth equity drops a margin call of some type will be issued.

On another note, watch the news, trust your eyes.

Debt loads can be influenced by inflation significantly. Happened post WWII for example where debt to GDP was reduced from 119% to 40% from 1946 to the 1970s. I am sure other factors were involved but it wouldn’t be this could be the case again at some point although that is purely subjective opinion.

If assets fall in value and we have really high inflation, American people suffer. I was referring to the wealth Americans have vs their debt loads. Or the wealth businesses have vs their debt loads, not sovereign debt…but that is problem too.

I wouldn’t be surprised to see futures limit down on any day this week. Maybe even Monday. Not sure how attractive we are to capital anymore. Cheers

Well, right now it’s purchasing infrastructure. Clean water systems, steel, lumber – all to build plants in America to onshore production of pretty much everything so we can continue to tell the rest of the world to respectfully fluff off. Fun ways to join the party…buy gold, energy, tech, and water ETFs, AI stock, metals, T-bills, bonds and then download draftkings and that other platform and bet against whatever you like on any particular day. The jawboning mentioned earlier in TGDFA is a particularly fun part of the ongoing celebration (=

No, the stock market is not societal wealth. What is societal wealth is the ability to produce. The value in paper assets is the ability to trade it for currency and buy goods and services. Everyone can be a stock millionaire, but that doesn’t do any good down the road if you can’t buy a house or pay for health care.

The US produces ALOT, just not much in tangibles anymore. It’s services and software that dominate production these days.

The US is still the second largest manufacturer in the world by value added, larger than the next three combined (Japan, Germany, South Korea). But the US is also the largest economy in the world, and should be the largest manufacturer. And it shouldn’t have a trade deficit.

And it is critically dependent on China for lots of manufactured goods, and that’s a huge problem.

Very true, but a lot of what is driving the stock market bubble is what I view as unproductive services, and not beneficial services or manufacturing.

Obviously, not everyone agrees as to what is productive.

I watch a game show in France where the winner each day earns less than €1000. I then turn on Jeopardy and watch their winners earn $30,000 a day.

We’re rich in assets, but we also have lots of debt. Average DTI for American households is 1.11 at $63k in debt per capita.

Rich people have most of the debt. Poor people don’t qualify for much debt. Rich people borrow against their stock holdings to finance their yachts and mansion and compounds in Beverly Hills because they don’t want to sell their stocks because they don’t want to pay taxes on them. From Musk on down.

Treasury Secretary Bessent lately has been on a crusade to carry Trump’s vengeance, by attacking Jerome Powell for “losing a over hundred billion dollars at the FED” the last couple of years.

Now long time readers of Wolf will understand why this is and why it isn’t that big of a deal for an institution that makes and destroys money.

However, the ignorant masses will not understand this. They will think it is a legitimate form of attack on Powell’s credibility.

That Bessent is attacking Powell over this shows one of two things:

1. He doesn’t understand how the FED operates. If so, he is an idiot and isn’t qualified for the position he is in. How can the Treasury Secretary not understand how the FED works?

2. He understands but pretends to play stupid in order to up the political heat on Powell to resign. Politicians who intentionally play dumb deserve to burn in hell. Otherwise smart people playing dumb for political purposes is part of the reason the country is in the position it is at.

In the past, Wolf has reluctantly praised Bessent as one of the adults in the room. I would like to hear his thoughts on Bessent’s comments about the FED losing money.

Bessent attacked Powell over the massive QE during the pandemic. He has been attacking Powell several times for that, including the other day that you referenced. The first time he did, it was in an editorial, and I wrote about it. Bessent thinks that massive QE was a huge mistake and in addition to distorting markets, including the housing market, it has been saddling the Fed with big losses since 2022. That’s a problem because the Fed normally remits its profits to the Treasury, but as of Sep 2022, the Fed hasn’t remitted anything, and will not remit anything for many years until all those losses are earned back. That is a big loss of tax revenues for the Treasury Department, which is why Bessent is hammering on it.

You better read this:

https://wolfstreet.com/2025/09/05/bessent-blasts-the-fed-for-qe-its-perverse-incentives-for-fiscal-irresponsibility-its-wealth-effect-policies-that-widened-clas/

Awesome article, thanks

Let’s put it a better way:

Do you agree with Bessent that it is because of Powell’s poor leadership that the FED has lost hundreds of billions of dollars the past few years and it should not continue?

Do you really not understand this?

The Fed has liabilities (reserves and ON RRPs) that cost the Fed interest at rates that are part of the Fed’s five policy rates. At one point, the Fed held $5 trillion of these liabilities costing 5%+, or close to $300 billion that year. That’s on the expense side of the Fed’s income statement. Those liabilities got there because of QE in prior years, and a big chunk of it during the pandemic. When the Fed had to hike its policy rates to counter inflation, the cost of those liabilities soared.

On the asset side, the Fed has the Treasury securities and MBS that it purchased during QE. Most of them are long-term securities. And almost none were T-bills. So the interest income from that gigantic portfolio was a little over 2% and did not go up because they were long term securities with fixed rates bought during QE when QE pushed down interest rates of long-term securities. So they have very low yields.

So the interest rates on the income side remained fixed at a little above 2%; and the interest rates on the expense side soared to 5.25% in 2023 and are still over 3.5%.

This is a classic maturity mismatch. That’s where the losses come from. And it was triggered by QE. Any on the FOMC who voted for QE is at fault. Bernanke and Powell are the big architect of it.

The Fed has long been discussing this mismatch of maturities as the primary reasons to get rid of much of this long-term stuff and replace it with T-bills. There was no maturity mismatch on the Fed’s balance sheet before QE started in 2008.

If the Fed once again holds mostly short-term securities, and it hikes its policy rates, the interest cost of its liabilities rises, but its income from T-bills and repos rises in tandem, and the Fed would continue to be profitable. That’s how it used to be before QE. QE has screwed up everything. The Fed now understands this. Bernanke’s Fed started it and Powell’s Fed drove it to the next level, until it started QT. Bernanke and Powell should be ripped to shreds over QE. They pushed this stuff.

QT reduced both the assets and liabilities in equal amounts. So less interest income at 2%-plus and less interest expense at 3.5%. So the losses are still there but are smaller now.

Paying interest on reserves is no free lunch.

Well let us not forget that Powell was appointed by Trump in his first administration as a replacement for Yellen who opposed Trumps demand for QE, tax cuts, and deficit spending.

IMHO, I think that Powell was incompent

More and more people are investing. Even if just in CDs, index funds, whatever. It is a great thing.

Invest early. Even a small amount. I wish I could have started so much earlier.

I also wish we could revamp our SS system to truly invest in the market and have an actual account. Still have a system for poverty and such.

“I also wish we could revamp our SS system to truly invest in the market ”

LOL! Right, what could possibly go wrong…

…more financialization? No thanks. First fix the too big to fail problem. in the meantime RISK/TRUST is being repriced globally.

Sure leave out my other stuff.

I fell for that pitch in 2000 and voted “W”. Watched them trot Colin Powell out in front of the UN where he presented hand drawings by a graphic designer of the interior of mobile bio-weapons labs. The drawing on my refrigerator was by a 5 year old girl.

At what point is “investing” gambling?

Schiller P/E now is over 40. Does it have to reach 60 before people start to get concerned with risk?

The schiller PE is outdated. Just Google it

I’ve heard all of the justifications for why valuation doesn’t matter. It doesn’t until it does. And then it really matters.

One should not Google something when they could just read the Nobel prize winning professor’s books. He was right not just once, but twice on the prediction of the systemic unraveling of our financial system.

Use the noggin. Not the Google, which you will just find hacks talking nonsense. And worse you will maybe believe the nonsense!

sufferinsucatash, which author is that? I’d like to read. Thanks.

Plenty of inflation incoming!

Thanks Wolf

If you agree that US inflation has averaged 5 percent a year over the past 10 years in the USA, then everything you own has to go up in value by 50 percent over that time period just to break even. If you then sell an asset for the purchase price plus 50 percent “profit” and pay capital gains on the profit, you LOST MONEY.

And who was the person who wanted to place a tax on UNREALIZED capital gains?

The inflation rate was not 50% over the past 5 years. It was half that. So if your assets went up 50% over those 5 years, you still came out ahead after taxes and inflation.

But yes, inflation is a tax on everyone, including asset holders.

I’ll venture a guess that the fortunes of billionaires like Musk, Bezos, etc., as well as those with only $100M, have not relied on inflation. So if a wealth tax is targeted to hit them, and not those with a measely $30M, inflation considerations are not really relevant.

if you reject a comment during moderation, do i get an email explaining what i did wrong?

🤣 No

But since you’re new here:

1st comment: you didn’t like the data because it contradicted your silly narrative, and so you bitched about the data in a ridiculous way. This site is not X.

2nd comment: you bitched about the brightness of the screen of your device while you were reading this site in bed. Change the brightness on your device and don’t blame this website for it, you goofball.

This is your 3rd comment, and it doesn’t exactly hit the bull’s-eye either.

Awesome idea, Wolf – for every comment you reject, an e-mail explanation should be sent to the ‘aspiring’ commenter. 😂😂

We know you sit around all day long.

A great way to promote community outreach! 🥸🤓

Wolf reports easiest to read on the internet. No pop up ads and someone that I trust in charge of calling out misinformation backed by facts.

Thanks

thank you for the lessons.

Meanwhile – “ A January 2026 report from home tracker Remitly has dubbed San Jose, California, the least affordable city in the world.”

Additionally, “ Median Home Price: As of mid-2025, the median home price in San Jose passed $1.6 million, making it the most expensive in the U.S. for the second consecutive year.

Income Requirement: To afford a median-priced home in San Jose, an annual income of at least $370,000 is required.”

Puts those San Jose incomes into PERSPECTIVE.

San Francisco not far behind.

Yes, home prices are too high. Been saying that for a long time here.

Meanwhile, in San Jose:

Median household income: $141,500

Median married-couple income: $190,300.

“Given that 24% of U.S. corporate equities and mutual fund shares are held by the wealthiest 0.1% of U.S. households, 49.9% of equities and mutual fund shares are held by the wealthiest 1% of households, 87.2% of equities and mutual fund shares are held by the top 10% of households, and just 1.1% of equities and mutual funds shares are held by the bottom 50% of U.S. households, this gaping combination of massive surpluses and massive deficits gives a reasonably accurate view of the unstable equilibrium that’s at the heart of the growing economic insecurity of American families.”

From John Hussman’s market comment, January 2026.

I’m so tired of this endless BS confusion of wealth inequality (which is a real problem) with this stupid notion that the bottom 50% don’t have anything (which is BS). That’s why you people, including Hussman, are always surprised by the strength of the US economy.

Yes, the top end is extremely rich, but a huge number of people below them are also rich, just not extremely, and another huge number are well-off with big incomes and substantial assets. And another huge number, including many young people, have nice and growing incomes and are starting to build their assets. The bottom 25% are strung out and don’t have much.

You’re throwing percentages around . So now throw dollars around.

The Bottom 50% divide into two groups: the bottom 25% that are strung out and don’t have much. And the other 25%…

So in addition to the home, savings accounts, money market funds, cryptos, precious metals, etc. that these 25% own, they also own by your quote 1% of the total stock market. So the total stock market = $68 trillion. 1% of it = $680 billion. So 25% of US households = 33.5 million households. So on average that 25% holds over $20,000 in equities each. This includes lots of young people that are just starting out. And it doesn’t include all the other assets people have.

I don’t disagree, but the mantra you hear from the financial media and Wall Street is often that we “have” to bail out the stock market to protect the average person. Even if you accept that argument, it’s dishonest of them to leave out that for every $100 of stock market subsidy (if it were to work that way), $50 was going to the top 1%. There’d be a lot less public support for it if people knew that.

Wolf in this post:

“I’m so tired of this endless BS confusion of wealth inequality (which is a real problem) with this stupid notion that the bottom 50% don’t have anything (which is BS). ”

From Wolf’s article on the wealth effect:

“The bottom 50% of Americans holds practically no stocks, no bonds, and very little real estate, according to the wealth distribution data from the Federal Reserve. Many live from paycheck to paycheck. They don’t make enough money to put anything aside. These folks cannot benefit from the wealth effect. For them, life (including housing costs, buying and renting) just gets more expensive as a result of the wealth effect.”

That was from a generic summary of how the Wealth Effect works that did not spell out the details, including what it means for the bottom 25% to 50% to hold 1% of the stocks. Here at the details written in 2022, and they have since then increased their holdings substantially:

“Bottom 50%” (not show in the chart): $69,100 (+$10,500; +15.5%).

https://wolfstreet.com/2022/09/26/my-wealth-disparity-monitor-september-update-qt-rate-hikes-dropping-stocks-bonds-reduce-outrageous-us-wealth-disparity/

In addition, in that article I did not distinguish between the bottom 25%, who have very little, and the next 25% who have substantial assets.

Hussman has been wrong longer than me if that is possible for exactly the same reason. Getting burned during the financial bailout of those that caused the mess in the first place.

Financial PTSD

Wolf, what do you think is going to happen to the value of the US dollar relative to other currencies given the Trump volatility factor? I keep reading other countries are dumping US securities. Canadians are saying that they won’t buy US-made products. Tariffs are affecting not just individuals but US businesses that need specific inputs and now can’t get them without paying a big premium. A lot going on these days, and I wonder how much damage Americans will reap from the things Trump is doing.

First off, don’t say anything negative about tariffs on the Wolf man’s site. He don’t like that.

Second, Trump is only going into his second year and just my opinion he is getting crazier than a hoot owl. If nothing else there is a lot of psychological damage being done and the reputation of the US is being trashed. So over the next 3 years, will the economy be negatively affected? Remains to be seen.

Starting with the first tariff article in early 2025, WOLF STREET got attacked by a tsunami of stupid-ass anti-tariff bullshit comments. Part of the reason was that governments, including officially the government of Canada, exhorted their citizens to swamp US social media, newspapers, blogs, and everything on the web with stupid-ass anti-tariff bullshit. By morons for morons. And this shit got spread around manure-like on a pasture. The purpose was to brainwash Americans with this stupid-ass anti-tariff bullshit to create resistance in the US and pressure the government to undo the tariffs. All of their manipulative shit has by now been proven to be wrong.

But the effect it had on my site was breathtaking. They attempted to “flood the zone,” to where nothing else could be read. I got many hundreds of these kinds of comments, many of them from outside of the US, on every tariff article plus plenty of them even on non-tariff articles. I blocked nearly all of them and crushed the rest manually. But this wasted a lot of my time. On one of my early tariff articles, it got so bad and was such a waste of time and pain in the ass that I closed the comments. Stupid-ass anti-tariff bullshit, often sponsored by foreign governments, and spread by their minions, continues to be blocked or crushed manually. YOU are in Mexico. YOU don’t get to bitch about tariff here at all.

If the U.S. dollar declines, it’s because of our reckless spending, not because of Trump’s tariffs.

The Canadians are basically throwing a tantrum because we’re imposing on them what they’ve been imposing on us for decades.

Miatadon,

There is a chance you suffered acute brain damage from the consumption of the toxic BS in the media about tariffs. That’s a known side effect. But the warning label attached to the media doesn’t disclose it.

I’m not opposed to tariffs if administered sensibly to protect our own industries and workers. I am against using tariffs to replace the income tax, such that fairness in the tax system is destroyed, and the tax burden is moved from the wealthy to the masses. A graduated income tax besides raising money to finance the government, also serves to put a damper on extremes of wealth accumulation.