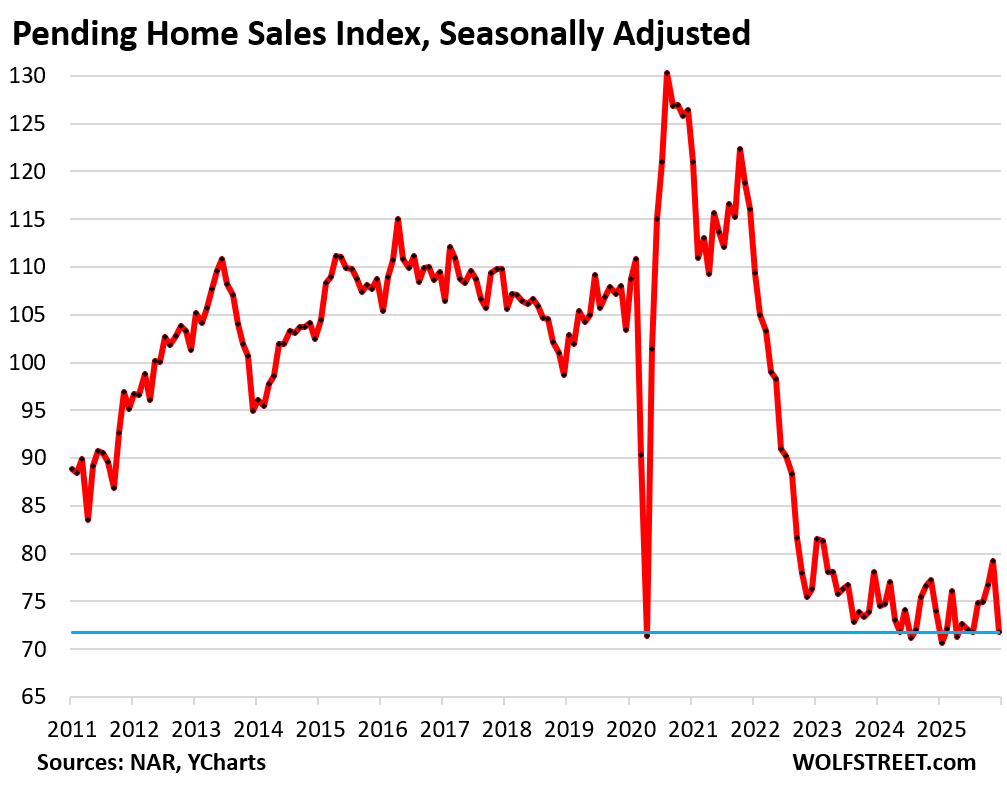

For the US overall, worst sales for any December on record. The housing market took a bad turn, from already low levels.

By Wolf Richter for WOLF STREET.

Pending home sales, which track the number of contracts signed in December, plunged by 9.3% seasonally adjusted from November, to the lowest level for any December on record in the data by the National Association of Realtors, which goes back to 2010. Compared to December 2010, during the Housing Bust, pending sales were down by 21.5%.

The market is now well into its fourth year of the collapse in transactions, and there has simply been no improvement.

Pending home sales compared to the Decembers in prior years (historic data via YCharts):

- 2024: -3.0% (year-over-year)

- 2023: -8.1%

- 2022: -5.9%

- 2021: -38.2%

- 2020: -43.2%

- 2019: -30.6%.

The metric of pending sales tracks contracts that were signed in December but that haven’t closed yet and could still get canceled because buyers cannot afford homeowner’s insurance, or cannot sell their own home, or for other reasons. The rate of cancellations has been running high in 2025.

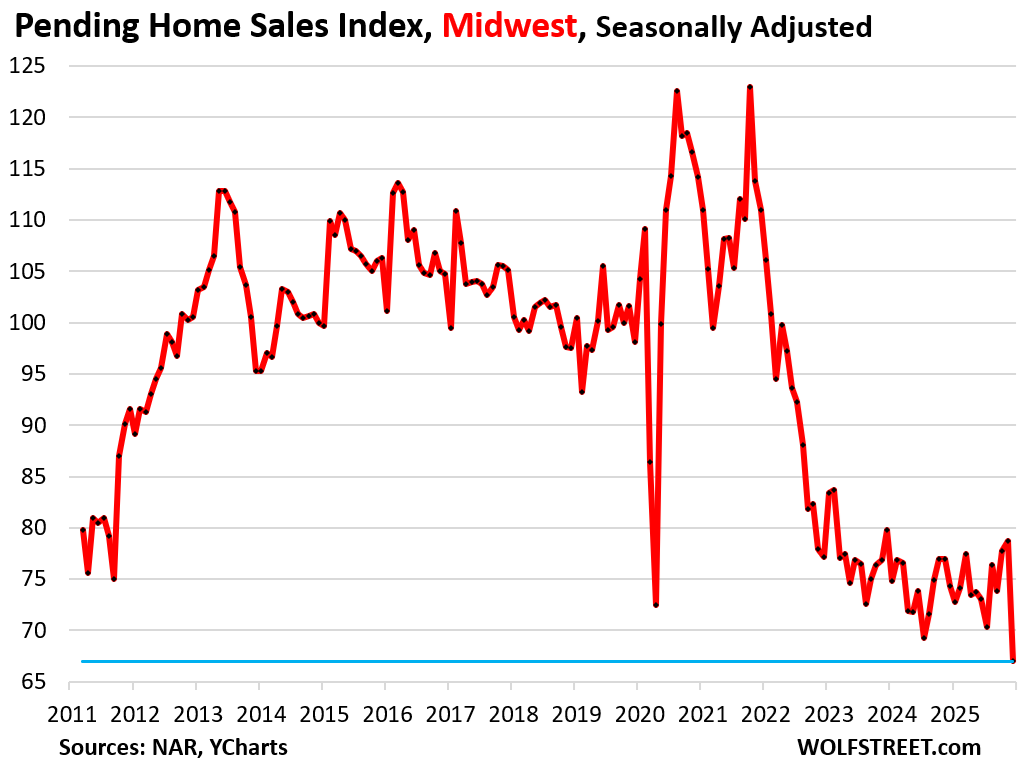

The December downturn in pending sales occurred in all four regions, from already low levels, but was particularly pronounced in the Midwest, where sales collapsed by 14.9% seasonally adjusted to a new record low.

Pending home sales by region.

A map of the four Census Regions is posted in the comments below.

In the Midwest, pending sales plunged by 14.9% seasonally adjusted in December from November and by 9.8% year-over-year, to a new record low level of sales in the data going back to 2010.

Compared to the Decembers of prior years:

- 2024: -9.8% (year-over-year)

- 2023: -16.0%

- 2022: -13.2%

- 2021: -39.6%

- 2020: -41.3%

- 2019: -31.7%.

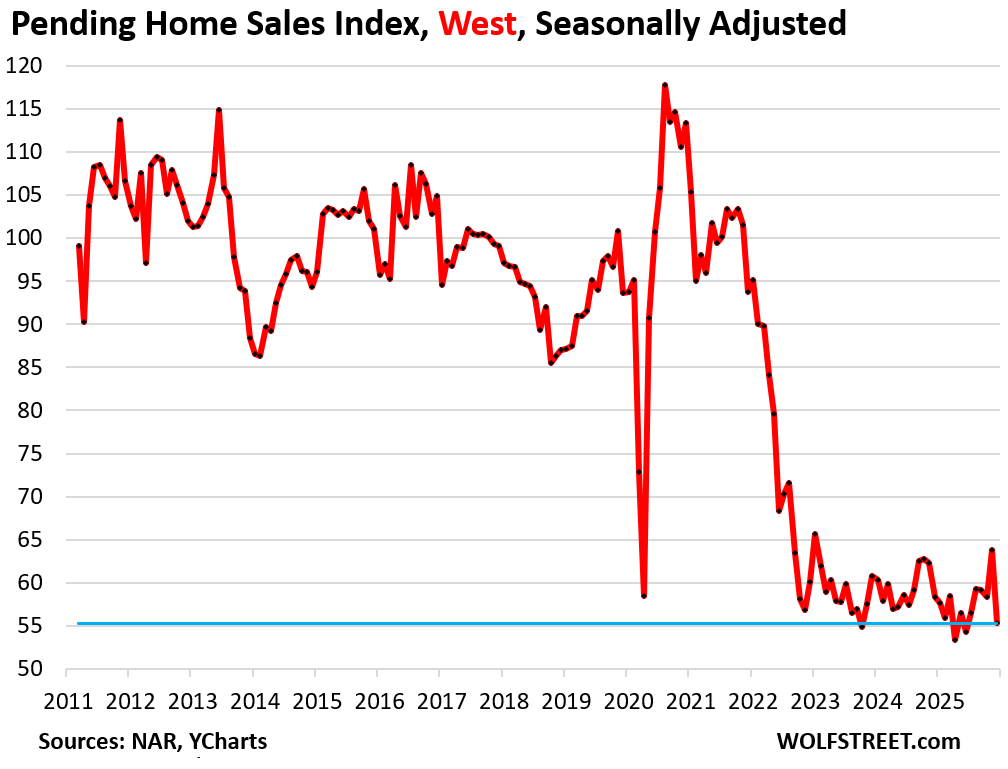

In the West, pending sales plunged by 13.3% in December from November, seasonally adjusted, to the worst level of sales for any December on record, and to the fourth-lowest level of sales for any month.

Compared to the Decembers of prior years:

- 2024: -5.1% (year-over-year)

- 2023: -9.0%

- 2022: -8.0%

- 2021: -41.0%

- 2020: -51.2%

- 2019: -40.9%.

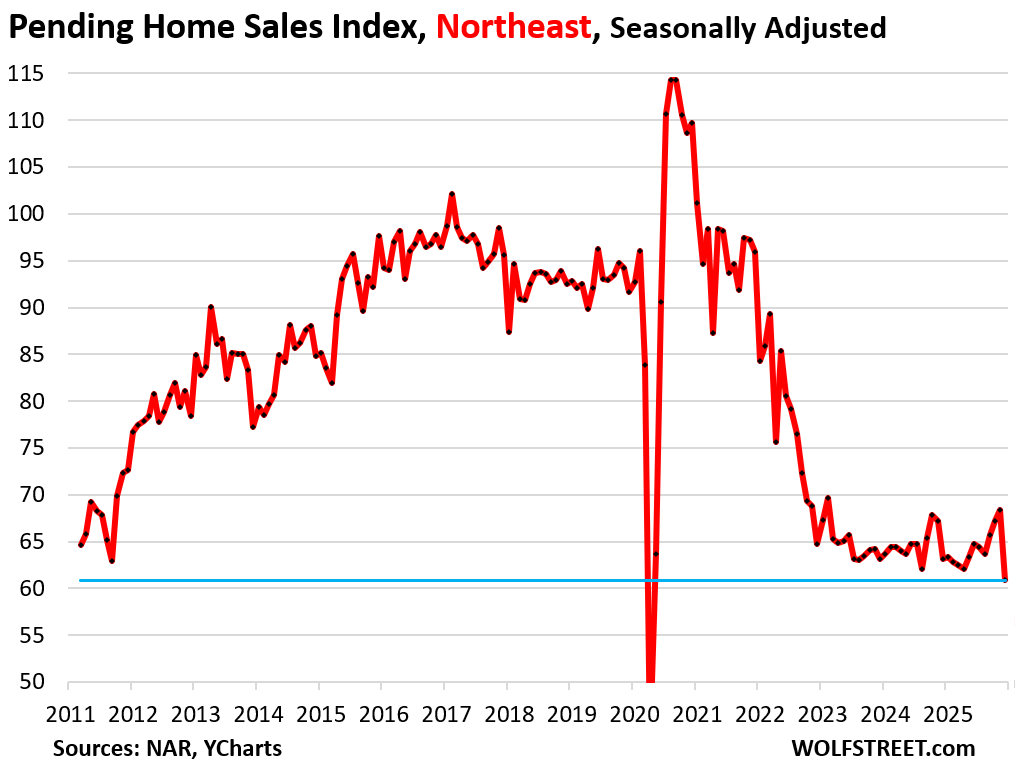

In the Northeast, pending sales plunged by 11.0% month-to-month, to the second-worst level of sales on record.

Compared to the Decembers of prior years:

- 2024: -3.6% (year-over-year)

- 2023: -3.5%

- 2022: -6.0%

- 2021: -36.5%

- 2020: -44.5%

- 2019: -33.9%.

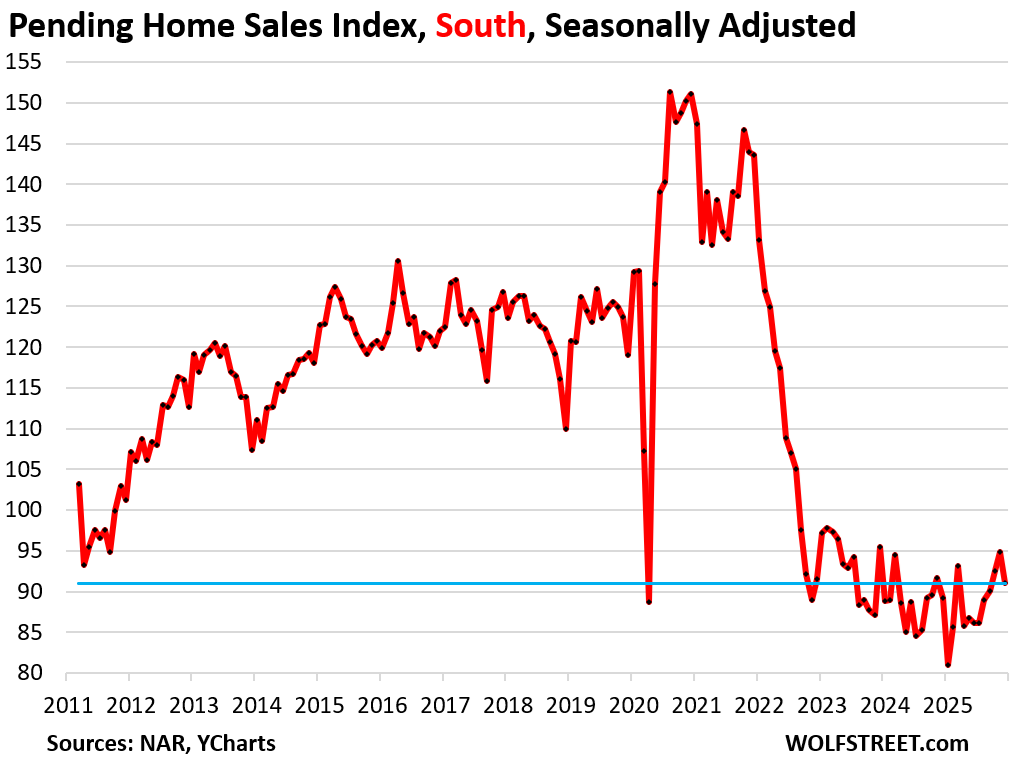

In the South, pending sales fell by 4.0% in December. Compared to the Decembers of prior years:

- 2024: +2.0% (year-over-year)

- 2023: -4.7%

- 2022: -0.7%

- 2021: -36.6%

- 2020: -39.8%

- 2019: -23.5%.

At fault are the ultra-low mortgage rates of 2020-2022 that ended up destroying the housing market in two ways: By causing prices to explode in a two-year time span, and by “locking in” homeowners with ultra-low mortgage rates who now cannot afford to move, which has destroyed the dynamics that come with a functioning housing market, such as mobility, where people are able to move.

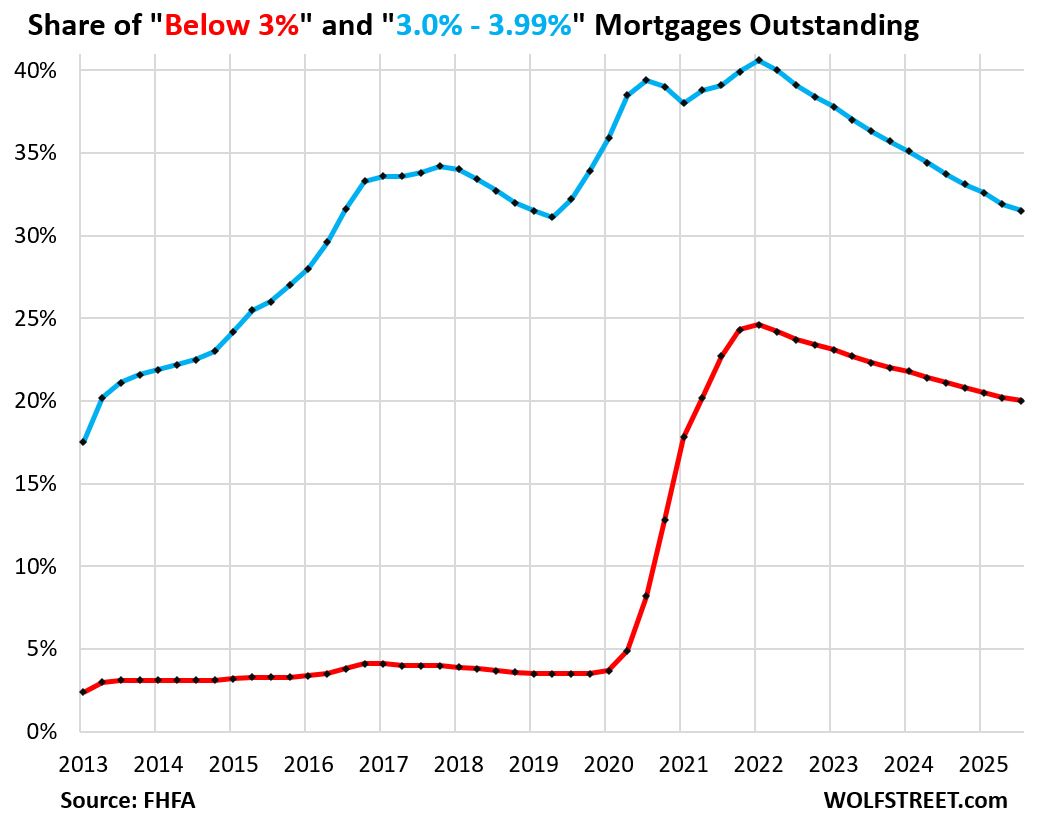

The unwinding of the below-4% mortgage rates is occurring, and so the lock-in effect is gradually loosening as these mortgages get paid off nevertheless, but at a snail’s pace [“Locked-in” Homeowners Nevertheless Pay Off Below-4% Mortgages: their Share Drops to Lowest since Q4 2020

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The four Census Regions of the US:

To realtors who may be struggling to find work right now, try these helpful tips:

– cut back on avocado toast

– make your own coffee instead of buying Starbucks

– get a fifth or sixth job like DoorDash for spending cash

– sell some old NFTs you may be sitting on

The Ministry of Truth states “simulations prove the average meal costs $3”, so you should be able to feed yourself on $15 a day. If you find yourself spending more, you’re living a life of luxury with room for cutbacks.

I’m about to enjoy my piece of chicken, piece of broccoli, and corn tortilla shell.

I wonder what I should have for the one other thing?

– cut back on avocado toast

Sorry, that one is strictly reserved to blame millenials on why they can’t afford to buy a house….

An Avocado is $2 each.

Toast could be $1

cutting up the Avocado, mashing it and applying it to the toast will be another $10.

With tip let’s just round it to $20 even.

Avocado on a slice of bread is a super cheap meal if you prepare it yourself, and don’t buy the $18.00 version at the cafe. Avocados are good, and good for you. It is also easy to prepare. Take avocado…. place on bread… done!

Wolf said, “The market is now well into its fourth year of the collapse in transactions, and there has simply been no improvement.”

I submit that the asking price is too high whereby reality becomes a step behind rather than ahead. The sellers have to lower the asking price by 45 pct.

The economic prognosis by my reckoning is that the accumulation of wealth by those that least deserve it is plummeting towards rock bottom

The population is hungering for a progressive plan to preserve the bill of rights, employ everyone that wants a job, imo the Canadian PM, Carney, made an agreement with the devil

exactly as the Chinese trade Canadian manufacturing jobs in exchange for the low value agricultural jobs. The same mistake the US made.

And stop buying your daughters so many dolls! We’re announcing a one-doll policy.

I think my family of 4 rarely spends more than $1800 on groceries and we aren’t all that thrifty when it comes to food. I actually think this $3/meal is pretty accurate.

What I don’t know is whether a realtor can afford that right now.

“Pending” home sales “dropping” doesn’t mean that buyers backed out of buying a home listed as “pending” (v. “Contingent”) on Realtor.com et. al.

It means less people put their homes on the for sale market.

The Midwest is bitter cold now and snowy, icy, so few people are looking to buy; therefore, few have listed homes for sale.

Unless I’m missing something.

“Unless I’m missing something.”

Yes. You fell for it. It was December. That stuff happens every December. Over the holidays inventory gets pulled off the market in huge numbers, always. And sales are always low over the holidays. But those figures here are seasonally adjusted, which compensates for the seasonality.

Tough times ahead. It’s taken 4 years for a 4% mortgage to drop from 40% to 30% of all loans. I can’t imagine it being folks paying off their mortgage, rather locked into a smaller home, or cost burdened.

Good article. Curious to see how this trend will affect those with ARMS.

“Curious to see how this trend will affect those with ARMS.”

I have seen more in the northeast homes for sale for this time of year,some move/many sit,have seen in N.H. some better pricing to a degree,perhaps my time is coming.

I will say as a stacker of pm’s am not sure whether to celebrate and party or cry and bunker down,luckily,both options available.

Me too but then I think better to live life and die than struggle to survive. We only have one life and that too limited time ( at least for old folks ).

Different strokes for different folks but I believe in ‘Die with Zero’.

Die with zero is kind of a silly thought process when end of life care is the most expensive unknown cost.

Die with zero is more like Underestimate because I’m greedy.

I think there may be a spark of wisdom within the envelope of your hypothesis.

Life, live it or love it

Not bashing on the data or analysis which is always spot on. Appreciate you putting these together, Wolf. Honest question though, is December really meaningful for us since the “prime time” to sell/list is in the early Spring?

For markets like mine it is. When weather is in the 60s and 70s, people go outside more. Look at what happened in 24 with rates from Nov 23 to May of 24 to see what happened then. I’m not saying the rate of change will be similar, but ultimately rates increase through that time frame. Maybe this time is different?

The data is seasonally adjusted. The issues are about the same every December. And seasonal adjustments compensate for it. NAR, which is always painstakingly optimistic, also made downcast comments about the turn of events.

One month is never all that meaningful, it’s just one month, which is precisely why I give you the long-term charts so you can see long-term how that one month fits in.

Investors love holiday shopping. Banks sitting on foreclosures and people who really need to sell are the ones left, properties that after several months have to drop prices to move. Since it’s relative, YOY, it does matter. One thing the above data tells you is that even flippers are not jumping at the reduced winter prices. They’re not at the foreclosure auctions as much either.

The other negative affect and pandemic era distortion caused by the lack of listings listed above. The supply of homes for sale is held down, preventing normal supply and demand adjustments. People wanting to live in desirable neighborhoods will pay the high price. Prices there are frozen at high levels because of the shortage of listings. In less desirable neighborhoods, we’re seeing price plunges as people drop their prices to get bids on their distressed properties.

Yes there is scarcity of supply of affordable homes. Even homes in desirable areas are waiting to be sold as they are priced high.

Sellers can wait, there are buyers out there but can’t afford at current price and/or rates.

I live in Gulfport Florida part of St Petersburg. Homes and Condos between 100K and $450K are struggling. Over 90 days old in the listings. On the other Hand the New 42 Story in Downtown has all of the Condos starting at over 1 million with robust sales. There is another 50 plus storied building with units starting in the $750K and up range that are in progress and over 25% have agreements to purchase. Just an Observation

Why weren’t 100% of all units presold – to then be resold by these condo flippers usually before construction is completed? That’s how it used to be. Preconstruction sales were a big thing. They partially funded those developments. Where are those buyers? Why do developers STILL own those units?

Some developers do not allow re-assignment of contracts, forcing the flippers to close and then re-sell which reduces flipping altogether, but does reduce sales upfront.

Relief is coming. 50-100 basis cuts coming in a few weeks, combined with corresponding declines in mortgage rates. It’s all part of a grander plan! Plus with midterms coming up all those affordability promises definitely will happen. Time to crack a Modelo.

You still didn’t get the memo? In 2024, when the Fed cut by 100 basis points, mortgage rates rose by 100 basis points! The bond market said: ” Make my day.”

The Fed sets its overnight policy rates, the bond market sets long-term rates including those of MBS, which determine mortgage rates. If the bond market is worried about a lax Fed and worsening inflation, long-term rates go up, no matter what the Fed does on the front end.

Should have labeled my post pure sarcasm!

🤣👍

I thought that was a possibility because you assiduously checked off all the points, but here in the trenches, I think a lot comments are sarcasm, when they aren’t. So it’s always good to note, or deal with the fallout.

LOL at your narratives….there’s always /REbubblejerk that will be more welcoming to your point made here, I am sure they will be in agreement to the same sentiment, afterall you often find posts mocking any caution that this bubble will burst soon or some major price correction.

Wish charts went back to the turn of the century to offer greater perspective by including the lead up to, and the housing crash of the late 00s.

RTGDFA

Crazy. The housing bulls assured us sales would boom once 30 yr mortgages went back to a 5 handle. Wrong again bulls. Sales won’t boom until prices come down

I’ve really debated paying off multiple mortgages I have at 2.75%, but with the cash sitting earning 4%, I’m gonna wait a bit….

You’re literally backstopping the entire American Economy. Otherwise it’s all paper mache’! lol 😆

Almost a wash depending on your tax bracket.

You could buy STRC and earn 11%. Stock is liquid.

Mr. Wolf: I don’t really get the West coast graph versus the December vs December percentage data. The graphs look like they drop off a lit more than the percentages would indicate.

This maybe hard to see because it came off the jump in the prior month, and those two lines (left up, right down) may be hard to distinguish. It was a huge drop from 63.8 in Nov to 55.3% in Dec (-13.3%). But the month before, there was a jump. To see it better, you can right-click on the chart and select “open image in new tab” or similar, depending on browser. This will open a bigger version of the chart, and you’ll see.

Thanks wolf

Wolf, I enjoy your reports and find the majority helpful.. I wanted to point out that the residential and commercial real estate market in the Florida Panhandle is alive and well. Lots of construction, lots of demand for all prices and they are closing. In other words a very vibrant market here.

Some people in high places seem to think the problem is that institutional buyers have bought up all the houses, so there aren’t any available for buyers to purchase

Large investors own about 3% of single-family homes. It’s the mom-and-pop investors that own the vast majority of single-family rentals, plenty of them here in the comments too. Mom-and-pop investors own about 11 million SFRs.

That’s why it’s comical for the king to try to address the affordability problem by banning institutional buying. Not that I am advocating for the institutional investors but like Wolf said bulk of investment properties are mom and pop, why don’t we ban them from buying or how about addressing afforability problem by actually dealing with the run away price increase or actually allow deflation of home value…nah, can’t have that, that might be one thing that will actually motivate the asset class to go to the streets and protest like the yellow vest in France or french revolution. Dismantling our system, yeah that they can willfully ignore as long as it doesn’t affect them personally, come after their wealth effect and piggy bank…pitchforks are coming out..

The higher up solution is almost, if not worse than the problem…ban 3% investors, 50 yrs mortgage, portable mortgage…etc….dog and pony show at best, at worst, another look over tactic meant to resolve nothing while the divide grow ever larger.

It feels like a standoff. People list at ridiculous prices they at one time saw on Zillow and then when no one wants to pay those prices they pull the houses. With the supply significantly outstripping demand if there’s ever a panic or even the realization prices are trending moderately down for the foreseeable future then I think there will be a race to the exit. For now though people keep listening to the realtors hype, rates are going to drop and prices will sky rocket.

I met a developer for large company and a land speculator while traveling last year and both separately told me that they’re forecasting zero price appreciation for CO for the next 5 years. The problem is the realtors have not gotten the memo and thus a lot of the population who blindly listens to them have not gotten the memo

Also would help if the main stream media would get increasingly negative on housing. Basically something needs to change the collective mindset

Isn’t there an inverse relationship between mortgage interest rates and home prices? Add in the effects of withdrawing the Covid stimulus helicopter money and the increased property taxes associated with inflated home prices and isn’t the resultant slowdown in home sales inevitable?

Structural imbalances that years to create won’t disappear anytime soon, will they?

yes, every single one of my housing articles has been saying that for over three years, including this one:

“At fault are the ultra-low mortgage rates of 2020-2022 that ended up destroying the housing market in two ways: By causing prices to explode in a two-year time span, and by “locking in” homeowners with ultra-low mortgage rates who now cannot afford to move, which has destroyed the dynamics that come with a functioning housing market, such as mobility, where people are able to move.”

Perhaps the American dream is changing and nobody notified all the real estate maggots.

Many younger adults do not want kids or all the crap that comes with owning a home. It may be more than just what someone can afford.

A close friend sold and now rents a very nice smaller place. They love it and the freedom they now have.

I am thinking they may be right. If I sell, I would have more in the bank than rent money for the rest of my life.

I am also certain most children would rather have cash than their parents old home when that time comes.

Just maybe the American Dream has changed.

Trump said he doesn’t want more supply on the market because then the price of existing homes would go down and that would be bad for existing homeowners. Of course, Trump says a lot of things …. I’ll stop there.

As always, his solution requires you to be gold medalist in mental gymnistic to comprehend, us normies just can’t grasp the brilliance behind that big beautiful brain.

We have a HUGE inventory of houses that were built with CHEAP LABOR in the 70s, 80s, 90s, and 20s. Construction workers (a.k.a. immigrants) who were naive/cut off to compensation data and negotiation skills. In essence, they were taken advantage of pure and simple (they had no leverage and were simply glad to have a job). As a result, the equity in these properties went through the roof over the following decades.

Then, social media came along and allowed people who have been a faceless commodity to gain knowledge – and the dynamics change. Those same immigrants (and their successors) became more educated and savvier to their value. Fast forward, labor as well as materials and land “go through the roof” compared to those houses from the 70s, 80s, 90s, and 20s.

Now there is this collision/mash up of “vintage” properties with lots of paper equity (either paid off or very low interest rates) competing with “current” properties with little to no equity. It’s a hot mess…real estate agents try to “compare” houses to price per square foot but it’s analogous to pricing different cars by the pound.

Do you think kids that have been brought up playing video games 24/7 in air conditioned houses want to tight rope walk across a two-story wall plate in Texas’ blistering heat while carrying a bunch of 2 X 4s on their shoulder – good luck with that. And if they don’t, their moms’ will scream on the evening news that Johnny isn’t getting the compensation and benefits he deserves.

What’s the point of my rant…we’re not going back. Single family residences will never be cheap again – never. And any realized equity will be much more modest – not a golden parachute. Those house prices from the 70s, 80s, 90s, and 20s is a fever dream. Over time those older homes will get sucked into an inter-dimensional portal like the house in Poltergeist and vanish. But it’s going to take time.

Couldn’t this just be viewed as smoothing out that apparent jump in November?