My frustration is boiling over. This is very serious. A lot depends on halfway accurate CPI inflation readings.

By Wolf Richter for WOLF STREET.

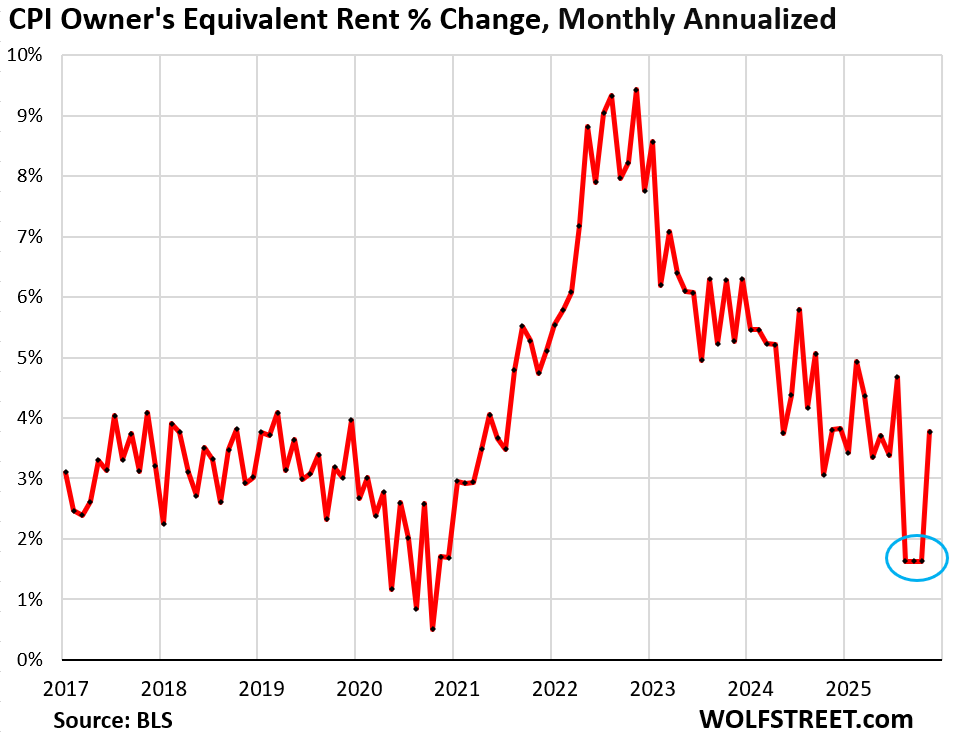

Today’s CPI report for December by the Bureau of Labor Statistics still didn’t fix the massive issues with the CPI for Owners Equivalent of Rent (OER), the biggest component of CPI, weighing 26.4% of the all-items CPI, 33% of core CPI, and 44% of core services CPI. And due to the unfixed issues in September through November, it continued to substantially push down year-over-year readings in December for the services CPI, core CPI, and all-items CPI.

The issue first cropped up for September, when the month-to-month increase of OER did a suspicious outlier-plunge. Then with no data for October due to the government shutdown and apparently no data for November either, the September outlier was carried forward through November, which substantially pushed down overall CPI.

The December index value for OER then jumped by 0.31% (+3.8% annualized) from November’s basement outlier level. BLS has apparently no intention of fixing the issues with the September through November OER (circled blue in the chart), and the year-over-year inflation readings will remain downwardly manipulated by this issue through August 2026.

A lot depends on halfway accurate CPI inflation readings, such as Treasury Inflation Protected Securities (TIPS), long-term commercial lease contracts with CPI riders, Social Security benefit levels for current and future beneficiaries…

Not to speak of the Fed’s monetary policy decisions, for which the Fed looks at the PCE Price index which uses the data from the CPI plus some data from the PPI, but with different weights and methods.

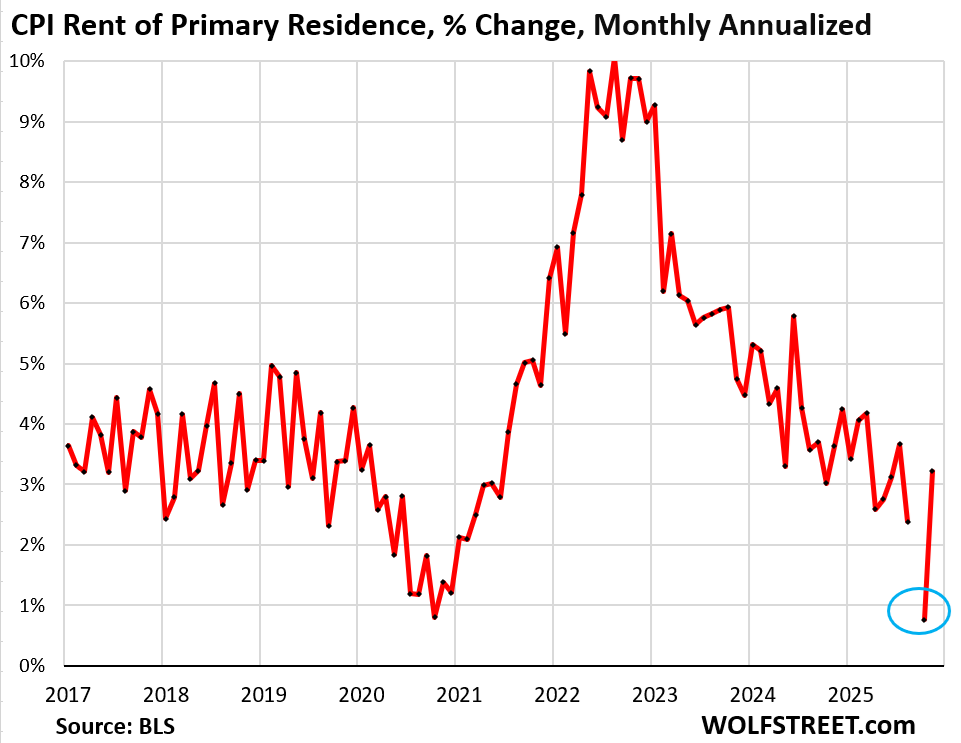

The CPI for rent of primary residence, which weighs 7.5% of the all-items CPI has a similar issue as OER, but not quite as bad since the outlier values didn’t start in September, but in October-November – for two months, instead of three months.

In December, the month-to-month increase was back in the normal range (+3.2% annualized). But the prior two months were below 1%, and unless fixed, they will continue to repress the year-over-year inflation readings for services CPI, core CPI, and all-items CPI through September.

CPI for OER and CPI for rent of primary residence account for one-third of overall CPI, and will falsify the year-over-year inflation readings by a substantial amount through August 2026.

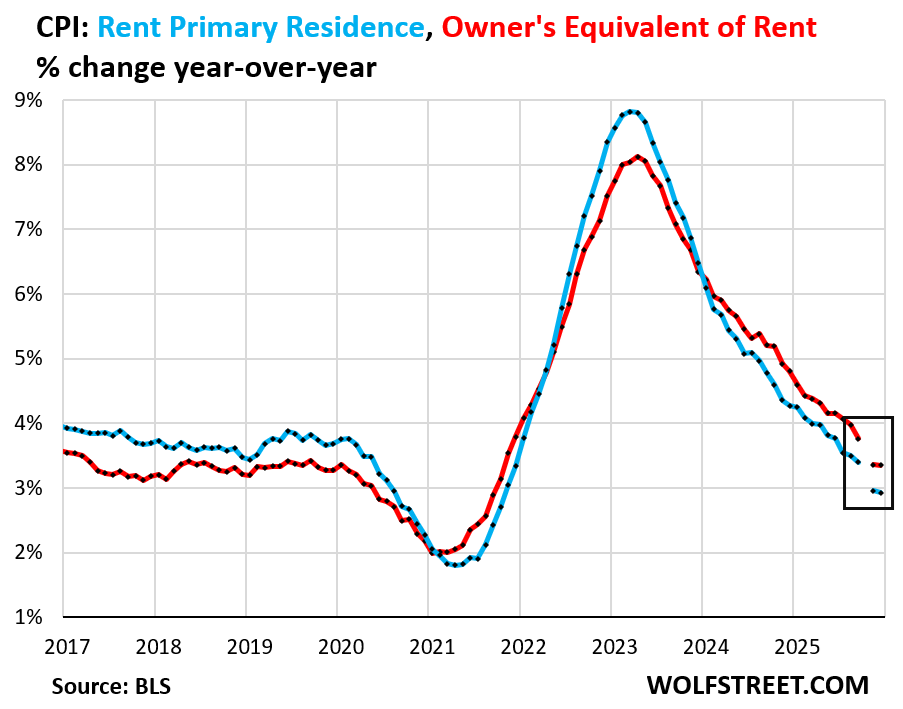

You can see the effect of the manipulation of the data for September through November on the year-over-year change for OER and Rent of primary residence – they adjusted downward by a sudden and large amount: OER adjusted downward from the August year-over-year change of +4.0% to the November year-over-year change of +3.4%.

The CPI for OER is based on what a large group of homeowners estimates their home would rent for, with the assumption that a homeowner would try to recoup their cost increases by raising the rent. It should indirectly reflect the expenses of homeownership as a service: homeowners’ insurance, HOA fees, property taxes, and repair & maintenance – which are not included in CPI otherwise.

The CPI for Rent of primary residence is based on rents that tenants actually paid, not on asking rents of advertised vacant units for rent. The survey follows the same large group of single-family rental homes and apartments over time and tracks the rents that the current tenants, who come and go, pay in rent for these units.

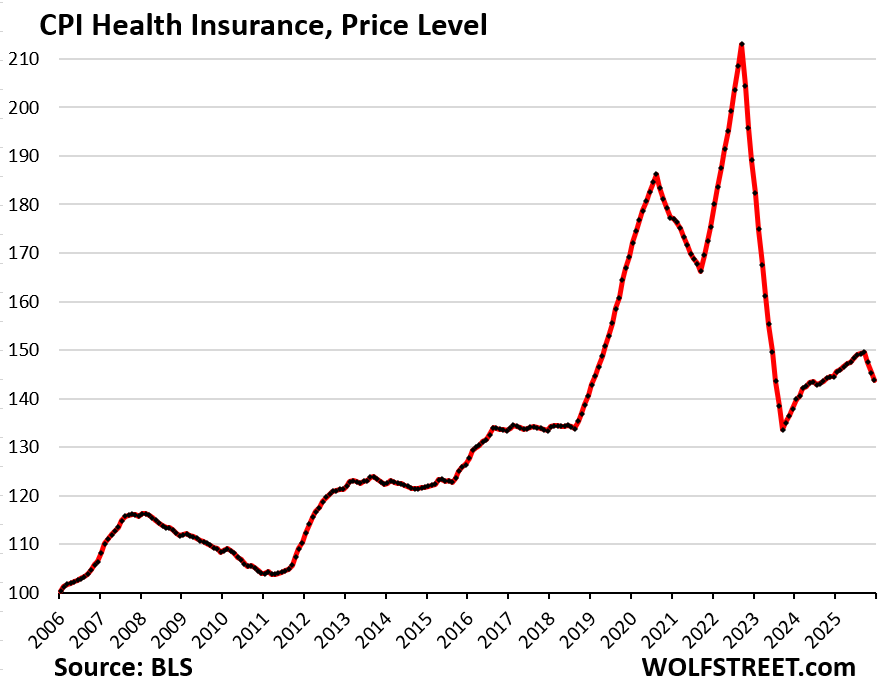

The chickenshit health insurance CPI.

The health insurance CPI manipulation has been repressing CPI ever since it blew up under the Biden administration. I called it chickenshit back in 2023 for those reasons. And it has gotten worse.

So now, the health insurance CPI:

- Month to month: -1.1% (-13.8% annualized)

- Over the 3 months since September: -3.9% in (-14.8% annualized).

- Year-over-year: -0.5%

- Since September 2022: -32%

- 0% health insurance inflation since February 2019

The chart below shows the price level of the health insurance CPI. It had spiked starting in 2018 to a peak in September 2022, which had been up by 28% year-over-year. At that point, the BLS declared the index had gone awry and tweaked it.

With the current manipulations, the index value is now back where it had been in February 2019, pretending that health insurance costs hadn’t risen at all – 0% health insurance inflation – since February 2019.

It is outrageous to present to the American people this kind of chickenshit index of a big and ballooning expense that plays such a huge role in Americans’ daily lives:

The problem with the health insurance CPI is that it doesn’t actually track any aspect of health insurance that consumers pay. It is based on the “retained earnings method” that tracks health insurers’ financial metrics.

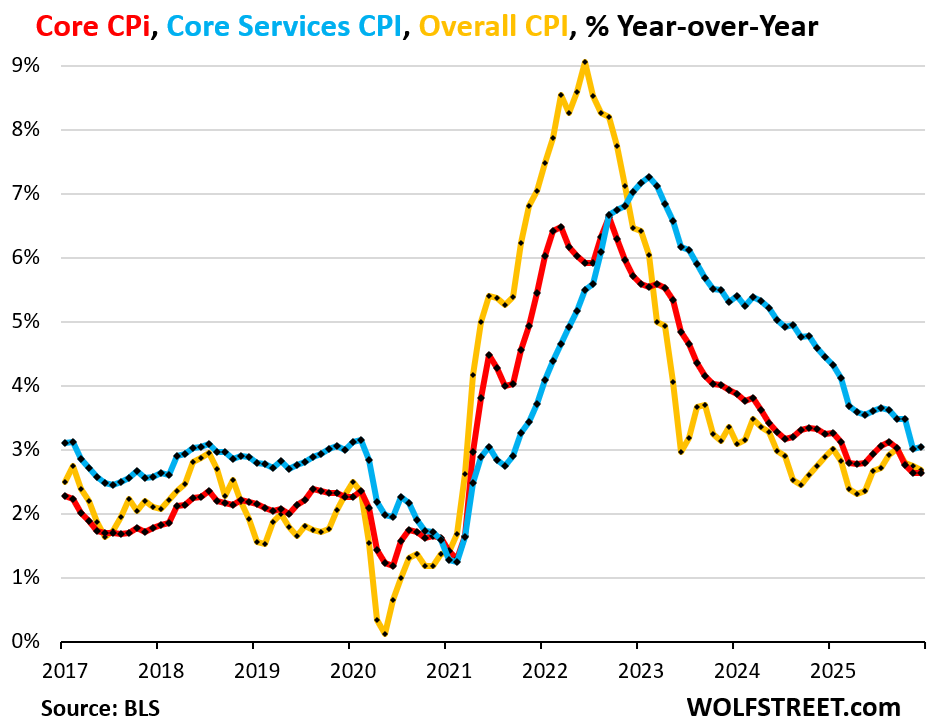

Core services CPI, core CPI, all-items CPI, year-over-year.

Core services CPI (blue in the chart below) accelerated a hair to +3.0% year-over-year in December after the massive deceleration through November, from August (when it was +3.6%). The manipulated-down housing indices account for nearly half of core services CPI. In turn, core services accounts for about 60% of the all-items CPI.

Core CPI accelerated a hair to +2.64% (red). It comprises core services plus core goods (not food and energy). It’s lower than core services CPI due to lower inflation in core goods prices.

The all-items CPI decelerated a hair to 2.68%, on dropping gasoline prices and accelerating food price inflation (yellow).

But the year-over-year CPIs are useless since they’re heavily skewed by the manipulated housing CPIs in September through November, and dogged by the health insurance CPI.

To fix this mess…

Abolish OER, increase the weight of the rent CPI to something like 15% of total CPI, and replace the remaining weight of OER (19%) with separate indices for HOA fees, homeowners’ insurance, property taxes, and repair & maintenance expenses. Canada’s statistics agency, Statcan, uses a system like that. It would still reflect the cost of housing as a service, and not as an asset price.

Scuttle the health insurance CPI method – the “retained earnings method” that tracks health insurers’ financial metrics. Instead, track actual changes of health insurance premiums, deductibles, co-pays, maximums out of pocket, drug formularies, benefits, etc. I know health insurance is complicated. But work with major health insurers, with a panel of companies that offer health insurance plans to their employees, and with a panel of consumers, and nail down the actual increases that Americans face – and they’re steep every year. Don’t tell Americans that their health insurance expenses have not risen at all since February 2019 – that’s just a ridiculous absurdity.

After the health insurance CPI is fixed and reflects the actual price increases consumers struggle with, its weight in the overall CPI needs to be increased to levels that represent the portion of consumer spending that goes into health insurance. Currently the weight of the health insurance CPI in overall CPI is less than 1%, which is another ridiculous absurdity.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“And due to the unfixed issues in September through November, it continued to substantially push down year-over-year readings in December for the services CPI, core CPI, and all-items CPI.”

Hmm…intentionally unfixed perhaps….I mean how else are you going to continue the pressure the FED to lower rates again and again..

or just like KellyAnn Conway used to say….alternative facts baby….

Health costs are like auto repairs etc. ..crooked8

I was waiting on pins and needles for this one! I saw they had “fixed” OER, but was sure the mathematical order-of-ops for getting to annualized data (just point-to-point Dec 25 vs Dec 26 for all contributions, then weighted into annualized. Or what it appears they do, some cumulative math around the prior 12 months M-o-M inflation.)

Thanks for clearing up.

The health care is insulting to the American people. Both premiums, deductibles, and out-of-pocket maxes are clearly significantly up since 2019.

The health insurance metric is absurd. Isn’t the purpose of the CPI to look at things from a consumer perspective?

Probably more effort goes into tracking the price of eggs, which might be one-tenth of a percent of the average household’s spending.

If you are distracted from what matters, the strategy is working!

Daniel L. Thornton, May 12, 2022:

“However, on March 26, 2020, the Board of Governors reduced the reserve requirement on checkable deposits to zero. This action ended the Fed’s ability to control M1. In February 2021 the Board redefined M1 so that M1 and M2 are very nearly identical. Consequently, it makes little sense to distinguish between them. In any event, the checkable deposit portion of M2 cannot be controlled now because there are no longer reserve requirements on these deposits. Here is the reason the Fed cannot control these deposits.”

Some Thoughts About Inflation and the Feds Ability to Control It.pdf (dlthornton.com)

Can you estimate the true yoy cpi if the modifications you suggest are made?

Anyone can estimate it. Results may vary. People come up with all kinds of crazy stuff all the time. But coming up with a system to replace OER and with a health insurance CPI that actually tracks health insurance expenses for most Americans halfway accurately is a very tough undertaking, requiring lots of really smart people, and the cooperation of many companies (corporate data). But that’s what a government agency is for. This is not the job for a guy sitting at a desk. Health insurance is immensely complicated because each insurance company offers different plans in different states to different employers and people, and they’re so many aspects to health insurance.

Isn

t that reason enough for national one payer healthcare coverage?

Clearly yes Lydia, and about time, or waaayyy past time…

But, ya can’t take away the rice bowl from SO many folx, eh?

Turned out that enlisting in US Navy was one of my best ”life decisions.”

Obviously better numbers would paint a better picture and could lead to better policy decisions but in the end the majority of people will continue to believe what they feel or perceive to feel with finances. I’m sure the low approval and trust ratings of politicians translates down to almost anything the government publishes. I’m sure most Americans believe the government will do what it sees is in its best interests of it and its donors at the expense of tax payers. Not like there isn’t a dozen solid examples just in last few decades.

I work in state government where when software projects don’t just completely fail, they simply redefine the definition of success and pat themselves on the back. I don’t see any aspect of government any differently.

Data accuracy is obviously important. The definitional, technical and collection/”curing” issues all need to be squared away. Whether better policy emerges, on the face of things, is debatable. Everything in our society has become politicized to the sixth sigma end of the spectrum.

Causal analysis is a different thing altogether – both for healthcare and insurance. Extremely complicated. More so when trying to model human behavior.

Wolf, I’m attempting to be more informed economically and have enjoyed reading your perspective. I was hoping you could comment on the CPI’s increased different cell imputation rate, which I just learned about recently this past semester. I couldn’t find mention of this on your website. Apologies if I missed it. The data is here: “https://www.bls.gov/cpi/tables/imputation.htm”

What’s your perspective on the different cell imputation rate increasing over the past year or so while the home cell imputation rate has decreased in turn? Is this part of a concerning trend, e.g., cherry picking from a different cell? Or much ado about nothing, e.g., BLS doesn’t have the manpower it used to and is just doing its best? Thanks!

I talked about it at length in this article: It’s what they did with OER’s missing data for October and November: They extended the outlier month-to-month increase in September to October and November. Same with the rent CPI.

Interesting post – yours. BLS explains their approach at

slash cpi slash tables slash imputation dot htm

Not trying to evade controls wolf. I left out the obvious part.

Excellent reporting. Classic case of cooking the books by those at the top.

Insurance is the biggest component of my budget. My auto, home, and health insurance have steadily increased and is noticeable. The cost to home and auto repair keeps going up and up. Healthcare costs aren’t dropping. Consumers know and will vote with their pocketbook even if the data is manipulated to look better. Couple this with threat to Fed independence, Republicans need to worry about the midterms.

No they don’t.

There’s a long chain of causal analysis behind all of this that didn’t just materialize since Jan 20.

Wolf is challenging the technical practice employed and questioning the value of the product – and proposing an alternative approach. This a core problem in statistics that everyone in the field wrestles with.

My insurance costs, HOA fees all have also ratcheted up – a lot. That longer term trend started in 2020 – around the time Covid graced all of us.

The argument over FED Reserve existence could really stand a principled debate.

“Health insurance” is less than 1% of the CPI. It includes the cost of “insurance” but not the cost of actual medical services. BLS says that the total weight for “medical services and commodities” (including insurance) is 8.273%

“BLS has apparently no intention of fixing the issues with the September through November OER (circled blue in the chart), and the year-over-year inflation readings will remain downwardly manipulated by this issue through August 2026.“

How convenient.

With the White House claiming they will be purchasing $200B in MBS, could the Fed simply sell $200B in MBS in an attempt to neutralize the White House’s efforts?

The purchases by Fannie Mae and Freddie Mac of $200 billion in MBS does not involve money creation. They’ll be buying more MBS instead of more Treasuries. That started months ago. It might reduce the spread between MBS and Treasuries, but it might also raise Treasury yields, which would reduce the effects of the narrower spread. This may not have any real impact long-term.

But this is exactly what Fannie and Freddie did before the Financial Crisis, which caused them to implode when mortgages turned sour.

Yep. Talk about being set up to fail.

This is why Fannie and Freddy may never be privatized, despite Trump’s promises. They offer the president a direct way to control bond yields – at the risk of blowing everything up. Bond yields influence economic growth in the short term, and inflation in the longer term. So bond yields can be suppressed right before a midterm election year, especially by a 79 year old lame duck with nothing to lose. The economy will overheat and inflation will start showing up 3-12 months later. But by then the next election is over and Americans already cast their ballots based on how the stock market was doing.

And BTW, here we are starting Trump presidency year 6 of that promise to privatize the GSEs not being delivered. Your article on the subject some months ago was spot on. They couldn’t survive on their own without a guarantee even if the govt privatized them. I think anyone in FNMA or FMCC should cash in their chips and let the true believers have the shares.

Aside from the fact it’s an outlier, why do they duplicate a single data point to fill in missing data? Is that standard practice in someone’s line of work? I’d interpolate.

Amusing (not). Earlier today I was looking at Medigap rate increases recently filed with Arizona Department of Insurance. The filing I was looking at used a 12% per year annual premium increase assumption going forward. It did not seem unrealistic considering that the company increased ACTUAL premiums by an average of 11.5% per year for the last seven years. This was not an outlier, other filings I saw showed similar histories and projections.

Based on what Wolf says in this article, would someone like to venture what the correct YoY CPI-U for December would be (should be)?

Sorry, at the time I wrote this the previous question and reply by Wolf hadn’t been posted yet.

Likely in range of 3.25%…maybe as high as 3.5%

Is it any wonder that our social fabric is fraying (and not at the edges but in the center), when the Federal government gaslights the public at every opportunity? I believe the proper term, as coined by Emile Durkheim, is anomie.

Another proper term, as discussed by a couple guys with impressive beards, would be “class war.”

Only the feds?

Those who expect too much from government deserve to be disappointed.

“So if you want the truth, go to God, go to your gurus, go to yourselves, cuz that’s the only place you’re ever gonna find any real truth.”

-Howard Beale, Network(1976)

This was always going to be the path when they made the choice on bailing themselves out in 2008. The people who run the country are clever, but they aren’t wise. Then again maybe they want all this. They’ve certainly been trying their best to get people at each others throats. When you aren’t evil, its hard to perceive how evil people think. Though we’ve had a master class since the early 2000’s.

“In the physical world, there are constants that serve as dependable benchmarks against which to observe natural phenomena. Examples are the velocity of a falling object, the freezing point of water and the time taken for one rotation of the earth on its axis. In the economic and financial world, this degree of precision is lacking. Instead, we content ourselves with approximations, indices and averages. We pride ourselves in knowing the difference between an inflation rate of 2% per annum and 2.5% per annum. Small deviations of outcomes from expectations can trigger dramatic trading in financial instruments and result in the transfers of billions of dollars between investments. Yet, in the financial realm, can we really be sure of the value of anything?” — From Peter Warburton: The debasement of world currency: It’s inflation but not as we know it

Are you sure?

I thought only the speed of light is constant. Everything else is relative to where the reference grid is planted.

Economics is a “soft science.” Modeling the behavioral decisions of humans doesn’t appear to be susceptible to immutable mathematical laws – especially over the long term.

Economics is not a science at all. There are no immutable laws. “Supply and demand” comes close, but it can be perverted. Demography has an immutable law: in a given area, population growth = births – deaths + net in-migration. But that is more like biology, which is a science.

Oh contraire kimosabe, economics is not a science in the sense of that Chemical Engineering equilibrium has to be measured

Its not as if demography has an immutable law

Yes but each one of those physical metrics should be viewed as temporary rather than absolute

One has too consider that in order for aliens to arrive on earth they obviously can travel much faster than the currently accepted as the physical limit. the speed of light, 186000 miles per second

Retired since 2018. My 2019 Medicare Part B premium was 135.50/mo, my deductible was 185/yr. My Part G supplement health insurance was 110.45/mo. My 2026 Medicare Part B premium is 202.90/mo, my deductible is 283/yr, my Part G supplement health insurance is 165.27/mo.

That makes Part B premium up 49.7% since 2019, deductible up 53%, my Part G supplemental is up 49.6%. Bald face lies by BLS on these health costs, let alone any eye or dentist or drug cost increases. This is getting old fast.

Charlie – Agree…was updating my 2026 monthly financial spreadsheet today… Part G supplemental up, IRMMA up same as you – 202.90 mo, went backwards this year.. Plan to challenge IRMMA when the 2025 tax return is filed…

50% is a good guesstimate for the inflation in healthcare.

50% over 5-6 years would make sense.

All models are wrong, but some are useful. This sounds less useful.

You have great suggestions on how to improve the CPI. They are understandable and each would take lots of time of well trained BLS staff.

I ams sure you are aware that since January 20th much of that staff has been “retired” or fired. Many of the most experienced staff is gone.

Medicare B went up 10% in 2026. Medicare has a committee that decides premiums. Yet as it pointed out, the Medical CPI is quite different. Part B Medicare premiums should be forced to use the Medical CPI. Then Medical CPI will be fixed or Medicare goes broke.

I nominate Wolf Richter for head of BLS. I nominate myself for second in command. We could fix this statistical mess, but I am pretty sure if we were honest about it, we would be arkancided.

No thanks! You take the top job. I don’t want to get indicted if CPI comes out hot.

“Currently the weight of the health insurance CPI in overall CPI is less than 1%”. At least this means the misrepresentation of the cost of insurance isn’t having a material impact on the inflation data that the market is fixated on.

Our CPI has turned into something you’d see in North Korea. Why not just get rid of CPI altogether? This is why gold and silver are shooting the moon. Naranja Jesus wants to turn the US dollar into toilet paper by faking CPI and hammering rates back to zero. Viva platano republica! The US is finished.

Gold and silver are experiencing a severe manic speculation episode which will not end well at all and which is decimating the jewelry industry.

Let’s decimate the data center/AI/crypto bubble instead. This sham can’t end soon enough. It is the biggest waste of natural resources in the history of mankind.

Depth Charge Gold and Silver shooting to the moon

More money is flowing into equities than both precious metals and bonds combined.

US Finished?

Economy is booming, jobs strong, people spending, companies making money, inflation is stable, interest rates heading righ direction

Typical Voter: “But the price of gasoline is only $2.25/gallon. They have my vote.”

The CPI only sees spending, oblivious of the increase in debt required to sustain the spending extravaganza

Many components of CPI are very good. Even rent CPI is very good (except for those two no-data months), and nothing in the private sector comes even close. The new and used vehicle CPIs are excellent (they buy that data from JD Power). But OER is bad conceptually; and the health insurance CPI is bad structurally — those two are my long-term pet peeves.

They just need to fix that stuff that isn’t working; and they need to not mess up like they did over those three months.

CPI reports reality better than the spin around it.

CPI has never been a perfect measure of real-life inflation — it’s a benchmark, not a truth machine, and consistency over time matters more than precision.

CPI works because it is flawed — but consistently so.

When you replace that with “improved” methods, you get MORE uncertainty masked as precision that adds more politics, and talking points just to blab about on cable news.

Health insurance is a perfect example of an impossible tweak — tens of thousands of moving parts – individual, group, catastrophic, and HDHP plans, paid through employers, individuals, HSAs, or trust funds – And good luck getting full cooperation from the insurers themselves, from massive carriers to tiny brokers — no one could manage it all and who would pay them for their “help”.

ACA — UGH -massive problem: since inception, billions in federal subsidies have distorted the ENTIRE health insurance market, creating incentives for higher premiums and care costs across the board. Since inception the system hasn’t been a free market, and CPI can’t capture the noise it creates.

That Trojan horse needs to be put out to pasture with Barack and Sleepy Joe – Now that would shape up CPI.

Breaking News: Democrat Government Shutdown 2.0 coming soon — say goodbye to reliable data, AGAIN.

With CPI now at 2.7% and increasing it is time for the Federal Reserve FOMC to start seriously considering increasing their interest rates.

This is gross malpractice by design. The CPI number must be on a downward trajectory to serve the king’s interest in getting interest rates as close to 0% as possible. If you fire all of the serious people, this is the result.

As an aside, here in Mexico, where private health insurance premiums haven’t yet reached the absurd levels of U.S. policies, they account for about 7% of my household’s annual spending. I think a reasonable case could be made for it being 2x that level in the total CPI calculation.

Wolf makes two solid and very specific points.

But overall, did anyone else notice that up until the September report, the inflation trend was going straight up. The BLS commissioner was fired in August for the crime of reporting data contrary to the political narrative and presumably replaced by more optimistic leadership. Lo and behold, the November and December inflation numbers are heading down! The timing is suspicious.

Here are just a few reasons to think the economy is overheating and inflation is a lot higher than we think it is, even after adjusting for errors in OER and insurance:

-Very low Initial and Continuing Claims

-Very low National Financial Conditions Index

-Hourly Wages increasing at a 3.8% annual rate (although also BLS numbers)

-All Transactions House Price Index up 3.8% annualized in Q3.

-Historically high Durable Goods Orders.

-M2 growth at +4.2%, M2 Velocity rose sharply in Q3.

-GDPNow is crunching these numbers and outputting a +5.1% GDP growth rate, which would be a historical anomaly.

-The Federal Deficit hit $602B in the first 3 months of FY2026. Utter money printing.

-Finally, did foreign export companies really absorb almost all of the additional cost of the tariffs, contrary to the expectations of virtually all economists? Were their margins so fat that absorbing a 25% to 30% tariff didn’t even persuade them to raise prices? And margins that high didn’t attract competition in all these years?

Basically, every other metric or gauge is saying the economy is overheating, and we’re expected to believe core CPI is rising at +0.2% per month? Buy commodities, especially OILK.

90+ silver.

I am not sure whether as a stacker to celebrate or get ready to bunker down,guess both a good option.

The super economists at Wells Fargo loved it, they just glanced at the numbers and said bullish! You seem to be the only one looking between the lines.

I wanna buy this health insurance, who is the company?????????

Month to month: -1.1% (-13.8% annualized)

Over the 3 months since September: -3.9% in (-14.8% annualized).

Year-over-year: -0.5%

Since September 2022: -32%

0% health insurance inflation since February 2019

And I thought ( and still do) Hedonics suppressed the Inflation data.

This takes the cake.

Why do I not read this in the WSJ or other business journals???

Thanks for your insight Wolf.

Watching broader events unfold over the past year, in tandem with the new “top down” approach to all this, I was afraid shenanigans like this might be forthcoming. My key question is, where is the new generation of bond vigilantes? Considering current treasury yields, will the bond market really be willing to tolerate this nonsense?

The ten year is pinned at a rate that is unlikely to be a bond that one would look to purchase because based on the decent into the morass of QE, LTD lost nearly half of it’s value for those unfortunate souls who thought that buying the 30 year at 1 pct

“When it becomes serious, you have to lie”

Wolf,

Same liars, different uniforms.

Hmm…no health insurance inflation for nearly six years? Then how come Medicare premiums rose by 9.7% for 2026? Medicare premiums are now up 93% in the past ten years. No retained earnings to measure here.

The current swindle involves the need for AI to require a database of protected information while recording each and every one of us.

An AI model requires time to learn a path not supported by the central limit theorem but with the same rationale of minimizing the sum of the squared error between the model prediction and a target variable

The difference for a number of reasons is important in seeing the evil application of big tech adapting military enemy identification technology on the civilian population.

And in response to my outrage as an average American suffering the consequences of manipulated data by a self-enriching government, I’m going to re-elect all my congressman and senators as if they’re doing a great job so that nothing changes.

I would look foolish if I disagreed

On the other hand I would look foolish not pointing out Thomas Paine’s opinion as expressed in his tome ” the Pamphlet

Words that clearly demonstrate in the long run, America has always been a Social Democracy, the secret too our success

Simple CPI: The CPI is simpler than the Bureau of Labor Statistics (BLS) scratching their heads on how much cat food to substitute for hamburger when using an old expired box of hamburger helper. Using official US Government data on costs Labor, vehicles, whatever for a huge operation; i.e., the US Postal Service. Found a stash of USPS flag self stick stamps, thought they were forever stamps, but they were 39 cents, so ok 2 on each letter for 78 cents and I lost half my money. The stamps didn’t look old, so how long ago, looking them up 2006 or 20 years ago. That works out to 3.5% annual compounded. So the real CPI is 3.5% a year no matter what some central banker says.

It’s getting hot in here! This would have been a great opportunity for MSM to call out the administration’s touting of lower than expected inflation. But they mostly didn’t. They are probably too embarrassed to admit their interests for lower interest rates align. That kind of thing can get you cancelled nowadays.

I was just watching Trump’s speech talking about Powell and interest rates and he said “I want the market to go up.” This guy’s fascination with destroying the country for the stock market is disturbing.

“This guy’s fascination with destroying the country for the stock market is disturbing.”

Not really, debt is where their power comes from. Why would you ever liquidate your own power base? They’ve all been doing Dem or Repub for my entire adult life time. It is why recessions are essentially outlawed now. Wait until the next crisis, when they treat people talking about economics like they treated people talking about it which shall not be named.

They defaulted on pensions in the 70’s and 80’s, then made the stock market the new retirement account. Why would you be surprised if they defaulted on that?

Nothing to see, move along don’t question the official data,, believe what they tell us.

Maybe as high as 3.6% if they use real data? Right or wrong? It’s accumulative correction maybe as high 3.7% annualized.

$vix just needs to close above 18.52. Than boom. It’s like the sodium potassium pump moving muscles. Short yen Short $vix spoof the algo into buying risk. Once the $vix breaks out tail risk will be everywhere. SCOTUS decision tomorrow, I think so.

I’m not understanding something.

Why is the OER inflation for December 2025 impacted by readings in Sept-Nov for purposes of YOY inflation computations. I expect they would just compare Dec 2024 values to Dec 2025 to determine YOY inflation, and that would effectively true up any mistakes in prior months.

“… and that would effectively true up any mistakes in prior months.”

I think I understand what you’re thinking: that if you measure the distance between two endpoints of a 2×4, for example, you get the correct result even if you mis-measured some of the 12 increments that you measured in between.

But the CPI index is not a fixed 2×4. It is built month by month. One segment is added every month. If you add three segments that are too short, the whole 2×4 is going to be too short, and your measurement between the two endpoints (year-over-year) is going to show that and will be too short.

Below are the OER index values. The value for October is the mean of Sep and Nov for illustration purposes. In each month, one segment was added. If three segments (Sep, Oct, Nov) were too low, the year-over-year distance will be too low by that amount:

12/1/2024: 419.7

1/1/2025: 421.0

2/1/2025: 422.2

3/1/2025: 423.9

4/1/2025: 425.4

5/1/2025: 426.6

6/1/2025: 427.9

7/1/2025: 429.1

8/1/2025: 430.7

9/1/2025: 431.3

10/1/2025: 431.9

11/1/2025: 432.4

12/1/2025: 433.8