Their balances ballooned even as prices of stocks, gold, silver, et al. surged to records. Everything surged. Almost.

By Wolf Richter for WOLF STREET.

Households and even institutional investors continued piling into money market funds (MMFs), and their balances ballooned to new records, despite the Fed’s rate cuts since September 2024, and therefore lower yields on MMFs.

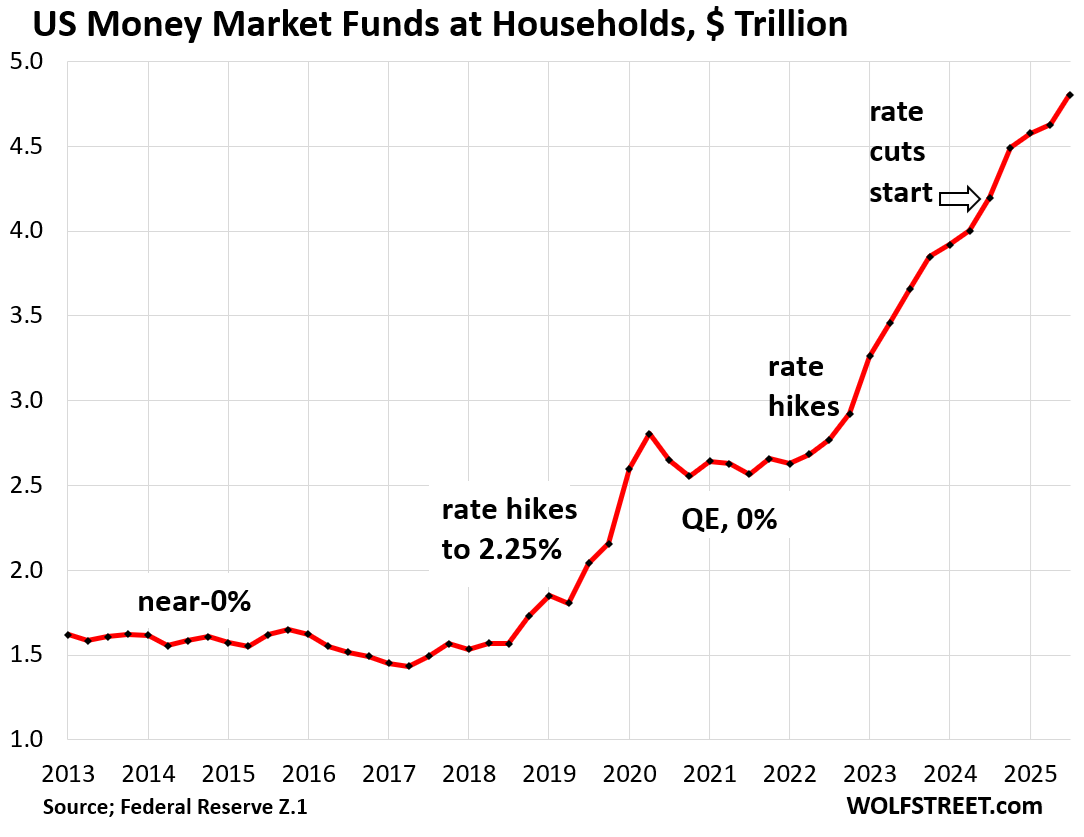

Balances in MMFs held by households jumped by $176 billion in Q3 from Q2, and by $605 billion year-over-year to a record $4.80 trillion, according to the Fed’s quarterly Z1 Financial Accounts on Friday. Since Q1 2022, when the Fed started hiking its policy rates, balances have surged by $2.17 trillion.

These MMF balances include retail MMFs that households have bought directly from their broker or bank, and institutional MMFs that households have bought indirectly through their employers, trustees, and fiduciaries – such as in their 401(k) plans.

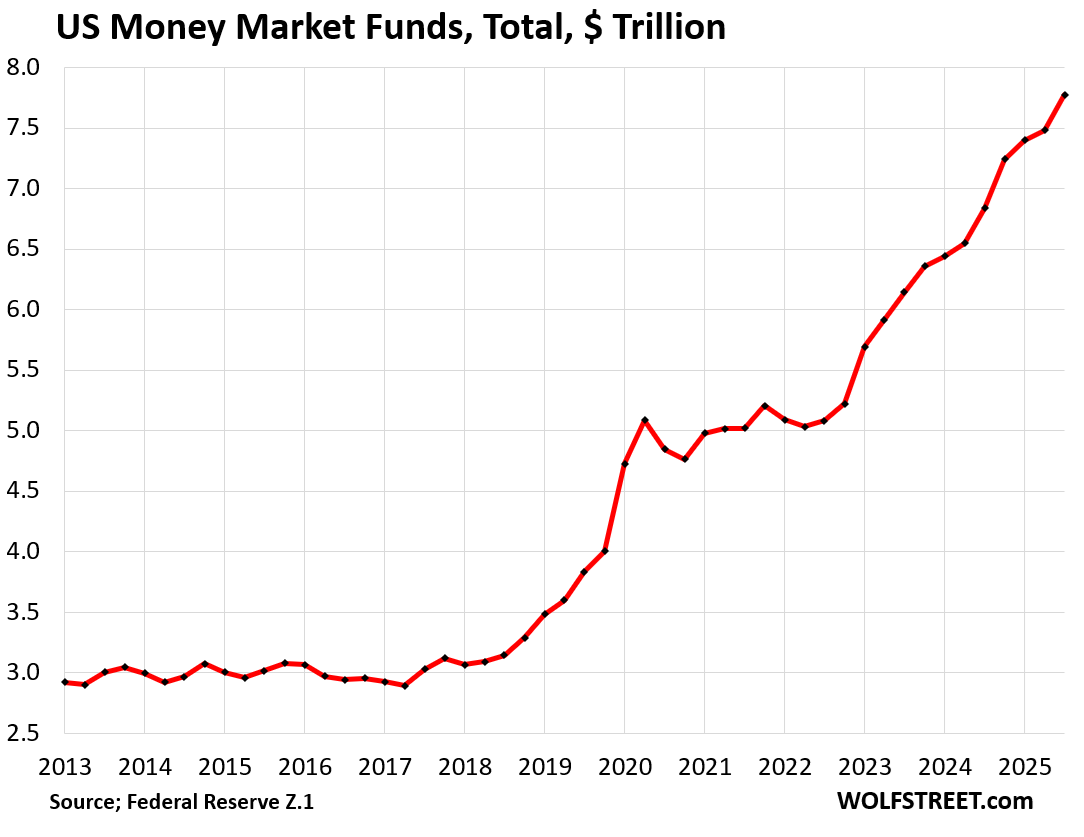

Total MMFs held by households and institutions jumped by $293 billion in Q3 from Q2, and by $935 billion year-over-year, to a record $7.77 trillion. Since Q1 2022, balances have ballooned by $2.68 trillion.

MMF yields roughly track the Fed’s five policy rates which are designed to form a floor and ceiling for short-term market yields, such as the gigantic repo market, to which MMFs are big lenders.

Prime MMF yields, at around 3.5% to 3.7%, are still above the rate of CPI inflation, around 3.0%, so they still have positive “real” yields. Municipal MMFs, though they offer major tax advantages, yield in the range of 1% to 2%.

But it’s not “cash on the sidelines” of the stock market. Buying money market mutual funds is an investment choice. It’s an alternative to buying stock mutual funds, ETFs, stocks themselves, or gold or silver or long-term bonds or real estate or cryptos. Crypto is not “cash on the sidelines” either. They’re all investment choices.

Buying MMFs is an investment in a mix of short-term low-risk securities, such as Treasuries with less than one year to maturity, high-grade corporate short-term commercial paper, and high-grade asset-backed commercial paper, and in repurchase agreements (lending to the repo market against collateral), and overnight reverse repos (ON RRPs) at the Fed – though ON RRP balances are now down to near-zero, as yields are higher elsewhere.

Any investor can sell one category of investments and buy another category of investments, and they do it all the time, and thereby that one investor can take money out of the stock market or put money into the stock market.

But other investors have to be on the other side of the trade with the exact same amounts. If one investor buys stocks, other investors have to sell those stocks dollar for dollar. So one investor can take money out of the stock market, but other investors must by definition put the exact same amount into the stock market.

When investors in MMFs sell their shares back to the fund, the fund will eventually have to unwind that amount in Treasuries, commercial paper, repos, etc., and other investors have to step into the place of the MMFs with the exact same amounts. That cash is not on the sidelines. It just flows from one investor to another as assets change hands.

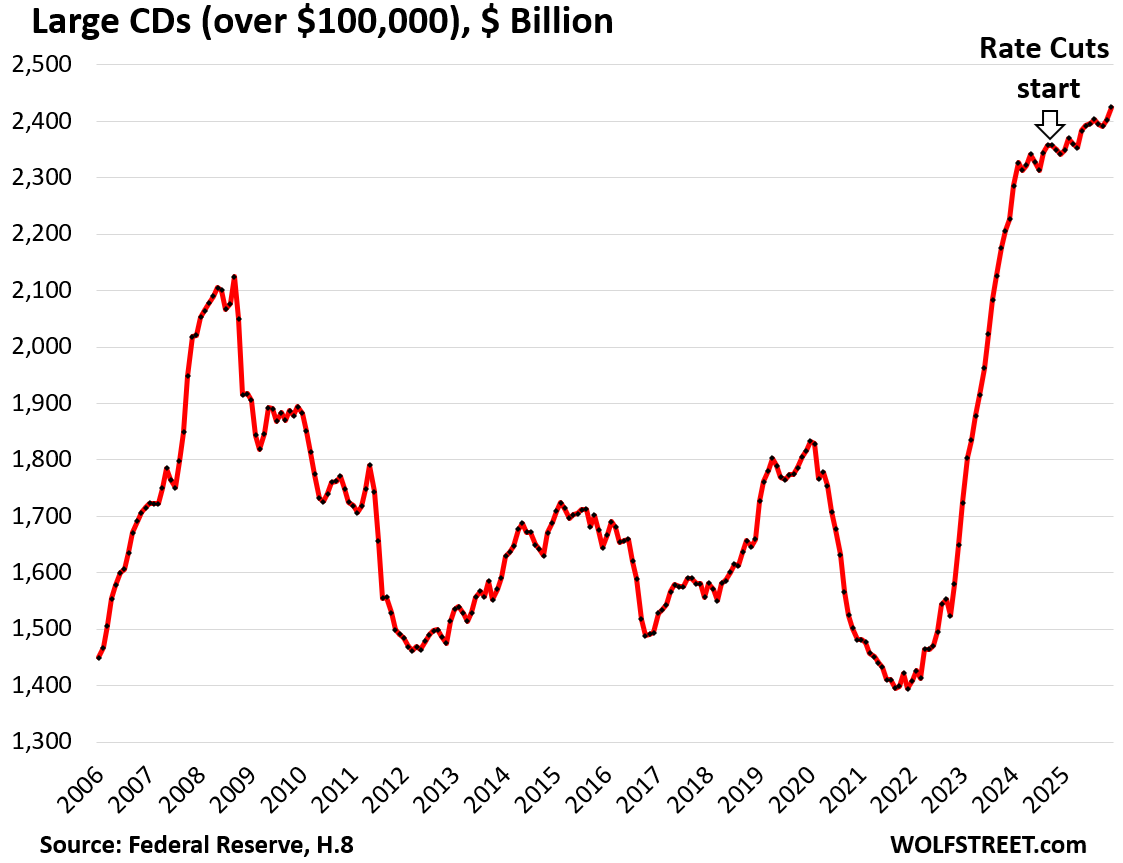

Large Time-Deposits (CDs of $100,000 or more) rose to a record $2.42 trillion in December, up by $83 billion year-over-year, as per the Federal Reserve’s monthly report on bank balance sheets (H.8), also released on Friday.

Since March 2022, when the rate hikes began and then even as the rate cuts began, large time-deposits have surged by $1.01 trillion.

The FDIC insures CDs up to $250,000. And it seems those CDs are still popular, despite their yields having come down.

Not cash on the sidelines either but an investment choice with a maturity date, like bonds, but they’re investments whose principal is guaranteed by the FDIC if within the FDIC limits.

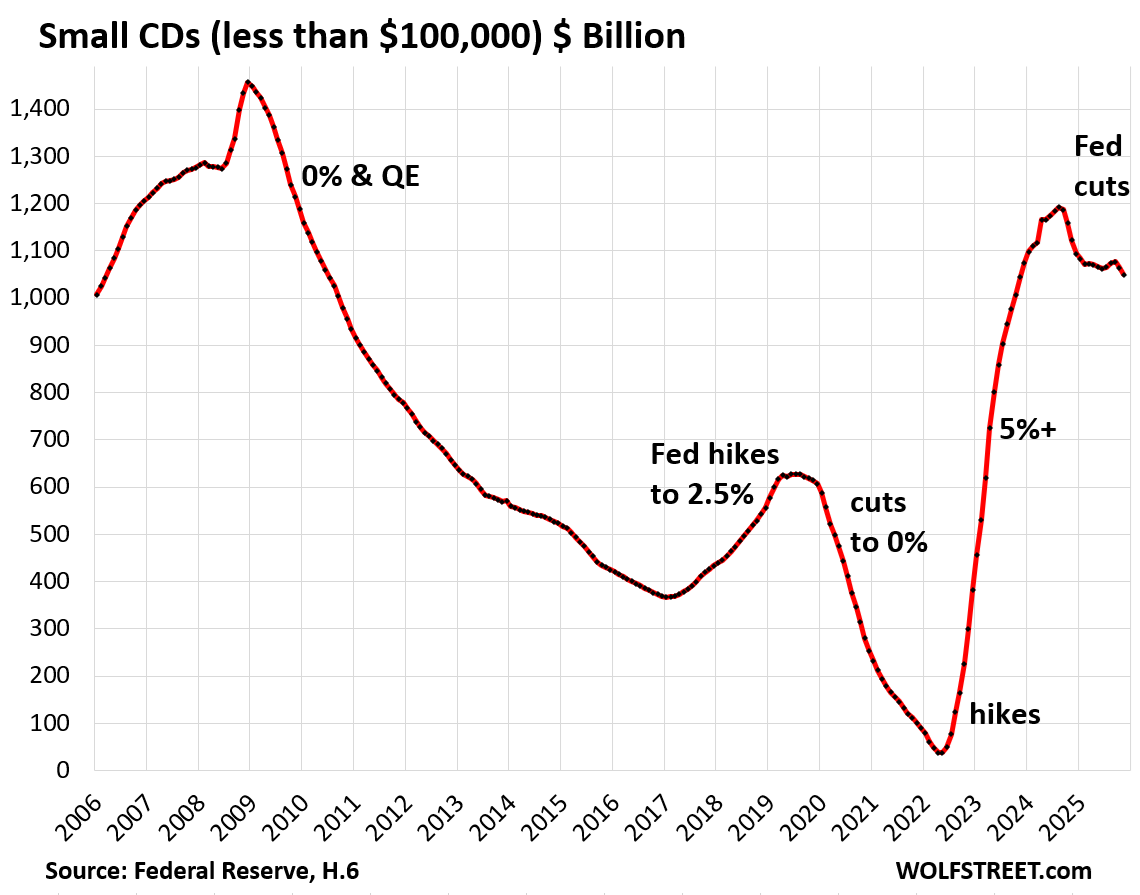

But small Time-Deposits (CDs of less than $100,000) fell to $1.05 trillion in November, down by $73 billion from a year earlier, per the Federal Reserve’s data on money stock (H.6), released in December.

Smalls CDs react fairly quickly and strongly to interest rates offered by banks. They’re not “sticky” at all. Investors shift into them and out of them depending on yields that banks offer.

All asset classes ballooned during the everything bubble. Money market funds are not the only ones that reached all-time highs. Stock market indices, gold, and silver rose to new all-time highs today. Bitcoin and other cryptos had risen to all-time highs in October 2025 and have sagged since then. Home prices had soared to all-time highs across the US until mid-2022, when the market began to split, with prices falling in many markets, but still rising in others. None of these movements had anything to do with “cash on the sidelines,” but with the general mania of the Everything Bubble.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanx for the update Wolf.

Ok, makes sense NOT to view MMF amounts as “cash on the sidelines”, but why should we care at all what MMF trends are doing? Is it as a measure of liquidity for the economy?

Also, when looking at the trends over anything more than a few months, is it useful to look at them adjusted for inflation?

Thanks

1. Do you only care about stocks and gold and zero-nada-else matters to you? This site is full of mostly other stuff.

2. The S&P 500, gold, silver, etc., reported every minute of every day, are not adjusted for inflation either because NO ONE pays inflation adjusted prices. They’re figment of your imagination. Thanks.

And there was me thinking that it was the nominal price that was other-worldly and the inflation-adjusted price that was real.

Well written and thought through.

E.g. My youngest chose to put $40K in a Credit Union GIC at something like 3%.

He knows I invest but wants the security of the basically sure bet (certainly an asteroid could take out Canada or some unforeseen event which bankrupt all of our insurances and the Central Bank but…..).

The Credit Union will not be putting that money in the equities markets (they lend it out at a higher rate for mortgages or small business loans).

For some of your readers for whom 3% is just a good day trading this might seem crazy but for many people – especially those without large amounts of capital – they prefer it.

Mr. Wolf writes: “But other investors have to be on the other side of the trade with the exact same amounts. If one investor buys stocks, other investors have to sell those stocks dollar for dollar.”

“Market Makers” do this. Interestingly their trade is always against the investor by definition.

No, market makers are only a transit point. They have to buy and sell, and make a spread.

How does the surges in MMF balances during these rate-decline periods compare to MMF flows in other such periods?

Yeah I hate the “cash on the sidelines” meme.