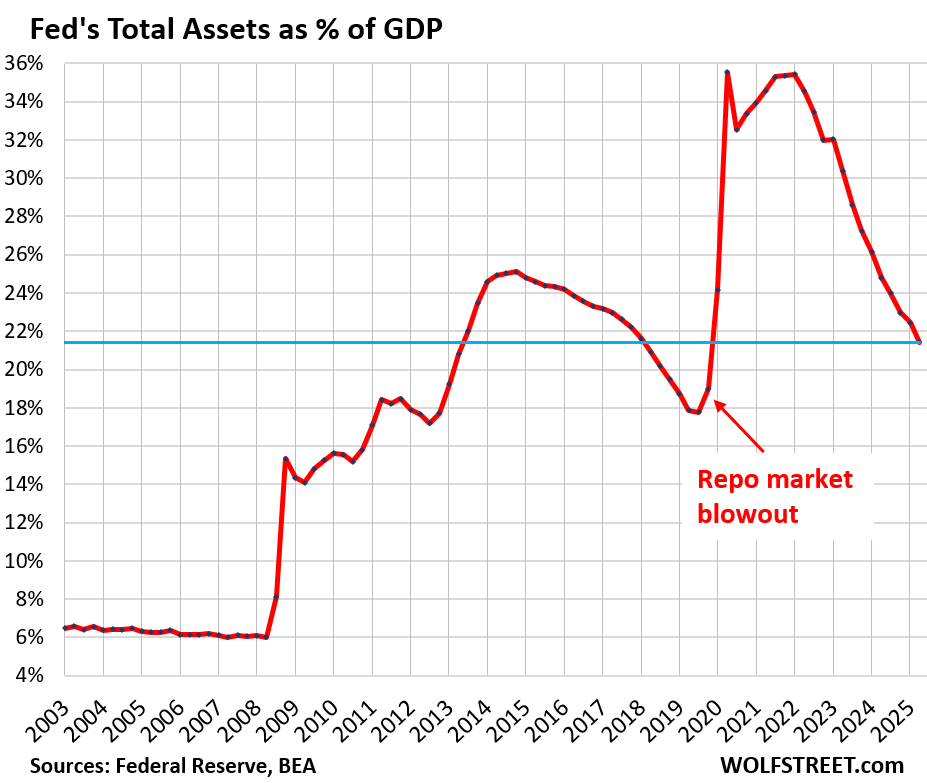

The Fed reverts to pre-2009 balance sheet management where the balance sheet grows with or less than the economy.

By Wolf Richter for WOLF STREET.

In the FOMC statement on Wednesday, the Fed said that it would let the balance sheet grow “as needed to maintain an ample supply of reserves on an ongoing basis.” That supply of reserves has become tight enough, after three years and $2.4 trillion of QT, and lots of inflation, to cause substantial turmoil in the repo market starting in September.

The New York Fed provided additional details about these “Reserve Management Purchases” or “RMPs,” under which the Fed will purchase “shorter-term Treasury securities,” mostly Treasury bills (terms of 1 year or less), and if needed Treasury securities with remaining maturities of 3 years or less.

The amounts of RMPs will vary. The NY Fed’s operating policy note on Wednesday said that the RMPs “will be elevated for a few months” – $40 billion the first month, starting December 12 – “to offset expected large increases in non-reserve liabilities in April” [due to tax payments, more in a moment].

And then, the RMPs “will likely be significantly reduced in line with expected seasonal patterns in Federal Reserve liabilities.”

“Purchase amounts will be adjusted as appropriate based on the outlook for reserve supply and market conditions,” the note said.

MBS that will continue to run off at a pace of about $15-20 billion a month via passthrough principal payments will be replaced by T-bills, as per the FOMC statement of the October meeting, and confirmed in the FOMC’s Implementation Notes today.

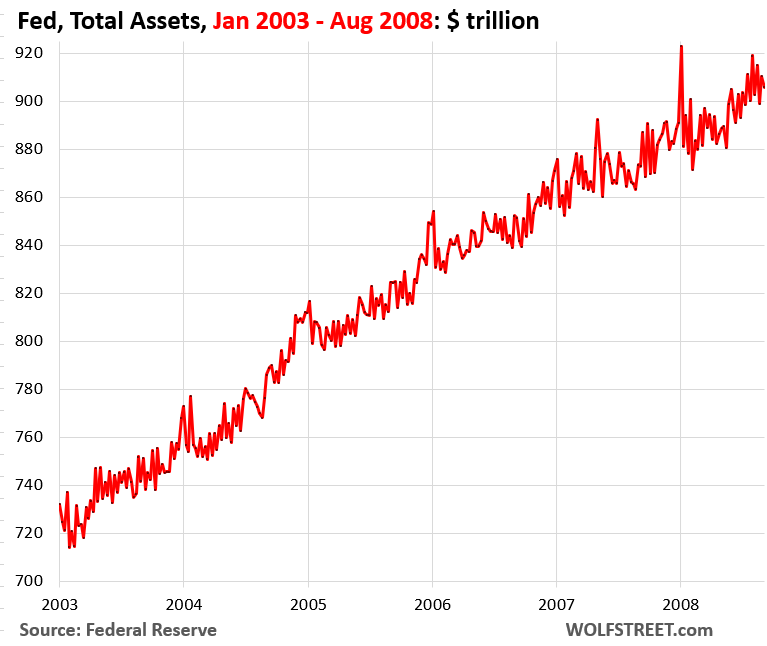

Before 2009 and QE, the Fed’s balance sheet always grew with the banking system and with the economy, driven by demand for the Fed’s liabilities; the largest liability at the time was currency in circulation (paper dollars). The chart shows the balance sheet growth from 2003 to 2008, before QE started. At the time, the Fed held mostly T-bills and repos. The ups and downs were caused by the repos with which the Fed attempted on a daily basis to bracket short-term interest rates:

With today’s policy shift, the Fed reverts to pre-2009 balance sheet management, where the balance sheet grows with or less than the economy; total assets were for years above 6% of nominal GDP, eventually on a slightly downward slope (see chart below).

In 2009 and after, QE inflated the ratio. But keeping the balance sheet flat in 2014 through 2017 deflated the ratio, though not as fast as QT-1 and QT-2.

How much in purchases to keep the Total-Assets-to-GDP ratio flat or on a slightly declining trajectory, as it had done before 2009? Nominal GDP grew by $1.34 trillion over the 12-month period through Q2 (last GDP data available). If nominal GDP continues to grow at that pace, the Fed’s initial suggestions in this sparse preliminary announcement of the RMP amounts would keep the Total-Assets-to-GDP ratio roughly flat.

During periods of QE, the ratio rose: QE-1, QE-2, QE-3, and pandemic QE. During periods of not-QE and QT, the ratio fell: before 2009, after QE-2, after QE-3, after pandemic QE. The announced asset purchases are small enough for the ratio to continue to fall, but at a slower pace.

The monthly amounts will be announced around the 9th business day of each month, along with a schedule of tentative purchase operations for the following 30 days.

This is all about dealing with the demand for the Fed’s liabilities (liquidity that others have deposited at the Fed). On the current balance sheet, the largest liabilities are:

- Reserve balances: $2.86 trillion (liquidity banks deposited at the Fed)

- Currency in circulation: $2.43 trillion (liquidity people, entities, drug dealers, etc. around the world exchanged for Federal Reserve Notes (paper dollars)

- TGA: $900 billion (government cash on deposit at the Fed)

- Reverse repurchase agreements: overnight reverse repos: down to near $0; reverse repo with “foreign official accounts” (USD cash from other central banks): $330 billion.

Large tax payments around Tax Day in April shift liquidity from bank accounts, and therefore from reserve balances, to the government’s checking account, the TGA, and drain reserve balances substantially and rapidly. This also happened but to a lesser extent around September 15 when estimated corporate tax payments drained reserves and flowed into the TGA and started causing the ripples in the repo market that were then made worse by the shutdown when the government didn’t disburse some of the funds in the TGA, and therefore didn’t move them back to the reserves.

Both, reserve balances and the TGA are liabilities on the Fed’s balance sheet, and funds shift between them, which could quickly and problematically drain reserves around Tax Day in April. So the Fed is trying to prevent another repo market blowout.

We also know that the RMPs are not QE from the way they were introduced. When the Fed kicks off QE, it makes a big deal out of it, with big upfront numbers, with Powell standing there and touting them in front of the world – remember March 2020? – to obtain the “announcement effect,” which may be the most powerful aspect of QE. By contrast, the RMPs were a low-key add-on to the FOMC statement, with plenty of discussions about it beforehand that explained what those RMPs are and why they’re needed for liquidity purposes.

In case you missed it, the theory and charts of the reserve management purchases here: The Fed Will Talk a lot about “Reserve Balances” and “Reserve Management Purchases” at its FOMC Meetings

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Where will the Fed buy the T-bills – at auction or the secondary market? The extra demand from the Fed will push up prices in the secondary market and reduce the yield attached to T-bills at auction – thus reducing the cost to the government? Is that how it works?

The Fed can only roll over existing debt at the auction. Under the law, it is required to buy new securities in the secondary market. But that’s almost the same thing because the “secondary market” for the Fed is its primary dealers, and they buy at auction and hand that stuff to the Fed.

This piece specifically (and presciently) addressed the initial question that came to mind after the Fed announcement yesterday: whether (or not) these newly planned reserve management purchases might effectively be just another name for some form of QE. I much appreciate Wolf explicitly covering and explaining this. Meanwhile, it’s interesting that the Fed seems to be keeping its hands off of the longer end of the yield curve. Are the powers that be really OK with how all of this might drive up long-term yields, like what happened about a year ago with treasury bonds?

Thank you for replying to my questions Bro!

Seeking Cassandra,

“Meanwhile, it’s interesting that the Fed seems to be keeping its hands off of the longer end of the yield curve.”

That really disappointed the army of YYC mongers out there. And worse for them: The Fed is unloading long-term MBS and is replacing them with T-bills at a rate of about $15-20 billion a month. That’s the opposite of YCC.

On that note, what I don’t understand is why the 10 year is continuing to drop.

Does the bond market believe the nonsense about disinflation in services?

The bond market WANTS to believe in it. The bond market loves falling yields = rising bond prices = because it then can sell the bonds at a profit. There is an entire industry hyping the bond market to push yields down and prices up.

Most Koreans, Korean broadcasters and YouTubers also think that the Fed has resumed quantitative easing again. As a result, we are expecting a surge in asset prices. I’m a Korean, but Wolf’s writing is always interesting and a great reference for my investment. I can’t find a place in Korea that tells you this truthful, honest, and data-based.. Thank you always!

https://wolfstreet.com/how-to-donate-to-wolf-street/

“As a result, we are expecting a surge in asset prices.”

As well you should. That’s the entire goal of the FED.

Well I always take the opportunity to suggest that inflation should be the mirror image of deflation.

One feared, deflation, the decline in asset prices. The other, inflation, measured as the rise in cost to support the increase in prices.

Thanks Wolf for a factual perspective that surrounds us.

Increasing the balance to sheet to grow with the economy makes sense, but only if you assume that the current balance sheet is the appropriate frame of reference.

If he does, it says to me that they believe all of the printed money from March of 2020 through May of 2020 is now structural, and the economy cannot survive without it.

Note that they’re still running off the longer-term part of the balance sheet. The purchases are all short term, and limited to the amounts required to keep financial markets operating smoothly.

My guess is that they’ll consider tackling the structural overhang (market dependency on too much printed money) under the next Fed Chair.

Powell wouldn’t want to start that and then leave it mid-flight as a mess for his successor next year. (His successor may already face plenty of messes…)

Perhaps someone can take the rate of growth from say 1950 until 2008 and use that as a guide to where prior history says it should be in 2025, so we have an idea of how out of whack its been since they decided to bail themselves out.

If they were to keep it at the average from 1980 until the GFC (around 5%) then the balance sheet should be like 2 trillion based on current GDP figures. So they’re still about four trillion above that.

But the balance sheet has changed structurally, including by the TGA ($900 billion) that wasn’t at the Fed but a commercial banks before 2009. So take that $900 billion off today’s figure. Also reserves have changed a lot in how they’re used, part of it through regulations. And the foreign official reverse repos are now $330 billion. I don’t know if they even existed back then. So you can take that $330 billion off too. Then there is currency in circulation, that’s demand based, those bank notes must come out of the ATM when bank customers want them… that’s over $2.4 trillion now…

I agree with your conjecture, “but only if you assume that the current balance sheet is the appropriate frame of reference.” My problem is I do not agree with what the Federal Reserve thinks they should be doing.

Which appears to be to support asset prices to avoid deflation.

There it is. The illogic that justifies man’s journey.

I’m unclear, is the Fed going to roll off the longer than 3 year bonds that it currently holds?

Or does that only apply for these new purchases?

What it means when it buys “if needed Treasury securities with remaining maturities of 3 years or less” is that occasionally it will buy some securities, such as a 10 year not that was issued years ago and matures in less than three years.

The Treasury notes and bonds that is holds now will be replaced when they mature.

So if the Fed buys 3 bonds, each with 3 years to maturity, one 5-year, one 10 and one 30, then in 3 years, it’ll buy a 5, a 10 and a 30 year treasury? If doing the Operation Reverse Twist, it still kind of matters what duration bonds it buys, even if they all have a 3 year remaining maturity, right?

1. no, it doesn’t matter. A 30-year bond with exactly 3 years of remaining maturity trades like a new 3-year note. A 10-year treasury with 90 days left before maturity trades like a new 3-month T-bill.

But the calculations are complicated and require maturity dates (time to maturity). There are bond price calculators that figure out the price you have to pay for $1,000 of 30-year bonds with 415 days left to run, and with a coupon of 5%.

The thing you want to know is the yield to maturity, which includes the interest payments you will receive, the timing of those interest payments, the principal payment you will receive at maturity, and time to maturity.

2. The composition of the Fed’s holdings will shift under this new plan, with lots more T-bill holdings and fewer long-term notes and bonds. The Fed is now loaded up with long-term notes and bonds, including 15-year and 30-year MBS. It will replace all its MBS with T-bills, and it will bring the share of its long-term bond holdings down to the national level of all Treasuries outstanding. That’s the plan now. But it’s a very slow process and will take years.

Until Sept 2008 the Fed only controlled the front end. After Oct 2008 the Fed controlled both the front end and the long duration. It’s assets grew until 2014. In the next 6Y, until Jan 2020, Fed’s notes expired and faded. The Fed was weak again. In Mar 2020, when interest rates were zero, the banks parked in the Fed for safety. The Fed raided people’s bank accounts to save the comatose econ. Thereafter, RRP sucked liquidity a year before raising rates. Bills provide a good collateral in the O/N market, but they don’t enhance the Fed power to control of the long duration. In recessions banks and the private sector invest in notes and bonds, sending rates down. The Fed can keep rates low for years, while the econ is booming, to ease debt payments, as long as inflation isn’t too hot. Negative rates, a smaller gov, tariffs.. will fill gov coffer. GDP to $40T/$50T, gov debt down to $25T/ $30T. Can it happen: yes !

I’m confused by the 4th to last paragraph. If individuals and corporations need money to pay taxes in April, and take the money out of their bank accounts (which the banks in turn have at the Fed, in reserve balances) and make the payments to the Treasury, which will go into the SGA, the Fed’s liabilities should stay the same, no? One for one trade. Why would the assets (other side of the balance sheet) need to change if the liabilities have not?

Yes, the total liabilities stay the same but reserves plunge, and stay down until the government disburses that money again over the next few months. Reserves are liquidity that flows everywhere. The TGA is liquidity for the government, but it’s locked up in the TGA and doesn’t flow anywhere until it gets disbursed.

Ahh, got it, so it’s a situation where every dollar of liabilities are not created equal.

I guess it’s sort of like “currency in circulation” to the extent that that currency is hoarded under a proverbial mattress overseas. It’s not actually doing anything.

“Overall U.S. commercial banks: About ~3.3% (for Q3/September 2025). This is based on FDIC-reported data showing net interest margin at roughly 3.309% most recently.”

“Interest it pays the banks on reserve balances (IORB): 3.65%.”

So, there’s still not a lot of incentive for DFIs to buy securities or make loans.

The effect of current open market operations on interest rates is indirect, varies widely over time, and in magnitude. What the net expansion of money will be, as a consequence of a given change in policy rates, nobody knows until long after the fact. The consequence is a delayed, remote, and approximate control over the lending and money-creating capacity of the banking system.

It sounded funny a few months ago when they were starting the “buyback” program ostensibly just to provide liquidity in thinly traded issues that they were going to swap for bills. Now they are buying bills. So if I buy a long-dated T bond, sell a T bill, and then buy a Tbill….what does that equal?

BS. You don’t even know the difference between the US Treasury Dept and the Fed.

“They” = US Treasury Dept bought back tiny amounts of notes and bonds. And since the US Treasury cannot print money, they had to issue more debt (borrow money) to fund the buybacks.

“They” = the Fed is replacing MBS with T-bills and is adding some T-bills to keep reserves from plunging further.

The new leader of bank of international settlements, BIS recently said this “ these channels stems from hedge funds’ leveraged trading strategies, which are facilitated by the availability of repo financing on very favourable terms. In recent years, hedge funds have been able to borrow amounts equal to or higher than the market value of the collateral provided – that is, without any discount, or haircut, protecting the cash lender from market risk. Around 70% of bilateral repos taken out by hedge funds in US dollars and 50% in bilateral repos in euros are offered at zero haircut, meaning that creditors are not imposing any constraint on leverage using government bonds. Larger hedge funds – those relative value funds typically involved in the basis trade – are especially prone to receive such favourable terms from their dealers relative to their smaller peers.”~ Wolf how does the Fed recent decisions that you discussed today effect what the chairmen of the BIS was referring too? Does it provide NBFI with more liquidity? Or is it neutral liquidity to the leverage crowd?

The basis trade is a concern because it’s so huge, and so opaque, and for other reasons, and the Fed has pointed that out, and is worried about it. When markets are calm, the basis trade provides liquidity in the Treasury market, and that’s a good thing. But when there is a crisis (last one was in March 2020), the basis trade locks up the Treasury market and causes huge problems.

The current set of decisions is unrelated to the basis trade. No one knows how to deal with the basis trade.

Right now, there is a lot of yield-chasing going on everywhere, which explains the no-haircut terms in the repo market. Lending to the repo market is essentially a low risk, highly liquid investment that pays a yield recently close to or over 4%, and money markets do a lot of that. Because it’s a pretty good deal for those lending to the repo market, they relax their terms a little, which is classic yield-chasing.

Not only ”classic yield chasing” Wolf,,, but far damn shore classic corruption including what used to be called ”insider trading”…

When, and if, WE, the workers and savers of USA and the entire global work force WE, come to understand the HOSING WE have received and continue to receive from earlier, much more likely these days due to Wolf’s Wonder and the incredible increase of information now available on web,,

those folx who considered us their serfs or slaves,,, WE will ABSOLUTELY first request and then some level of DEMAND that the balance, SO far greatly out of balance, be corrected to clearly reflect our work.

Until that happens, the entire ”financialization” of every product and process will be on shaky or worse base,,, and, to be sure, the laws of physics and other ”HARD” such processes, absolutely manifest that will be true SOONER OR LATER…

”Hedge Accordingly” seen on WS. is exactly correct…

It doesn’t matter what we call it. Any balance sheet expansion is inappropriate if the purpose is to provide adequate liquidity to support an asset price and deficit spending bubble.

When bubbles are in play, liquidity will naturally tighten as speculators and excess risk takers lever up their investments. That’s not a reason to increase liquidity. It’s a reason for the private market to decrease leverage.

For example. Look at the aggressiveness if Open AI’s s liquidity strategy.

That’s not how it works — in terms of your first paragraph.

Before QE, before 2009, the Fed always provided liquidity through its repo facility — and a lot of it on some days — as you can see in the jagged line of the first chart. All central banks do that.

In addition, at that time, banks were lending their scarce reserves to each other on a daily basis in the at the time huge unsecured interbank lending market (the federal funds market). This connected banks to each other in a wide web of unsecured lending, and it was this interbank lending by which contagion spread across the banks during the Financial Crisis. And that was not a good thing.

Now unsecured interbank lending is almost nil, and that’s a good thing. Banks have enough reserves. And if they’re a little short on specific days, or see opportunities to make some money in the repo market, they can borrow at the SRF.

But Powell’s “ample reserves regime” means that banks don’t need to borrow at the SRF all the time and a lot. So that’s the choice: tighter reserves would cause the SRF to be used a lot much more. This is the case at the Bank of Canada and at the Bank of England: both their repo facilities run big balances.

Repos and T-bills are both assets on the balance sheet. But repos are demand-based liquidity management – when banks want more liquidity, they can get it there. Whereas T-bill purchases are supply-based liquidity management.

So instead of running up its repo balances, the Fed is increasing its holdings of T-bills. It doesn’t make a big difference.

The Fed holds very small amounts of T-bills now ($195 billion). The rest is longer-term notes and bonds. Before QE, most of its holdings were T-bills and repos. Now the Fed wants to gradually return to a balance sheet where T-bills are a much bigger component and long-term bonds are a much smaller component. For example, it’s swapping out its long-term MBS holdings for T-bills.

The big news is that DXY has fallen. That will propel commodities upward.

dXY or $usd will experience a golden cross on the daily charts Monday or Tuesday. Up sloping 50DMA is crossing above the down sloping 200dma. Don’t bet against the dollar yet. Googl will dictate the AI bubble direction. The market has rallied 4 Fridays in a row, let’s see what happens tomorrow if rocket ship friday continue with the front loaded 8b t bill purchase.

Well trading the dollar index takes a certain level of sophistication that most of us have never been privy.

There is one technology that I am familiar with these past 20 years. That is company I established 20 years ago that failed using machine learning algorithms to categorize the character of a product on an 8 ft conveyor belt

AI, the fools paradise

I think the confusion is in the amounts. I read somewhere that QE was about $40B per month and whatever they are doing now is also $40B per month. That may or may not be true, but I think they also said it on CNBC leading people to just call it QE. If it’s the same amount, then there’s no real difference.

Why are Precious Metals Prices up today?

What does the Market know that we do not?

I don’t Trust the Banks and Life Insurance Companies.

They are market makers hiding a lot of insolvent borrowers, “too big to fail” scheme with the Fed, “extend and pretend”, from which one could deduce they believe it will be all ok or worthwhile due guarantee of later money printing and corresponding inflation saving the day (another under reported stat.)

“Why are Precious Metals Prices up today?”

Gold has been surging since 2018, when it was $1,200 per ounce. By 2020, it was $2,000. Now it’s $4,300. But it had plunged by 50% starting in late 2011 to 2018.

Yes, and it’s been like this for 2,000+ years. Despite that, it remains the preferred collateral of all central banks and the only universally accepted money, although silver may be as well…

HJC is correct but they forgot “mark to fantasy”

“Why are Precious Metals Prices up today?”

Because inflation is surging and the FED is cutting. Inflation = dollar devaluation. Precious metals are an inflation hedge – a store of value while the central bank turns the dollar into toilet paper. Jerome Powell is a Weimar Boy.

Silver is Quickly Escalating

As well it should. The FED is destroying the dollar.

Well, they are not referred too as precious metals for no reason. Each of the precious metals have their special properties like gold which enjoys the advantage of being rare, is inert to most oxidation agents including nitric acid, centuries of environmental exposure

Not to even mention platinum

So the FED started buying Treas Bills and people are calling it QE and hence the market keeps going up as FED started “QE”.

The perception matters not the reality.

Yes this is best time to cut rates when the all asset markets are at around ATH.

Thank You FED as I am almost fully invested keeping faith in you.

S&P 500 rose 0.21% today, Nasdaq fell 0.25%. This market has been rallying for years. The S&P 500 is up something like 40% since the low in April. You think +0.21% for the S&P500 and -0.25% for the Nasdaq say ANYTHING about monetary policy? You’ve got to be kidding.

“Why the Fed’s “Reserve Management Purchases” Are Not QE”

OK That’s what you said back some time around 2019.

I’m going to go with, if it looks like a duck and quacks like a duck, it’s probably a duck.

But it doesn’t look like a duck and it doesn’t quack at all. It meows.

The article tells you what it looks like and how it meows. All you have to do is read it.

The DOW is up 3,000 in a few weeks. This stuff is scary stupid. Cartoonish. And people think it’s normal.

Depth…

There is a greed out there that is brand new, powerful, and in control

Your concerns and observations are correct and valid.

Widely dispersed costs (inflation) concentrated to the benefit (asset appreciation) of a concentrated group.

How do these UST purchases work ?

Does the FED buy UST off banks etc ?

Then what do banks do with that newly printed magic money ? Do the banks then use that cash to lend, invest in stocks or keep it in the bank ? If they will lend or invest soon, then can’t that show up in inflation somewhere ?

Thanks !

The Fed buys these T-bills from its primary dealers, which buy them at the auction or in the market, and they hold a lot of them also. Every T-bill they sell to the Fed they have to buy first and pay the seller, either the USG or a private entity, and that cash begins to circulate so they can’t use that cash for other stuff. But they make a small profit.

Allowing the MBS’s to roll off without replacement and purchasing short term instruments will have the effect of allowing mortgage rates to increase while pushing down on short term rates. Am I looking at this correctly or am I missing something?

What does this mean for inflation? Can the Federal Reserve still mange price stability While trying to fight a liquidity crisis in the banking system? I mean in retrospect if liquidity is becoming an issue now, shouldn’t we already in theory have stable prices?