Month-End Liquidity-Palooza: Banks finally used the new & improved SRF the way the Fed has been exhorting them to use it to keep a lid on repo rates.

By Wolf Richter for WOLF STREET.

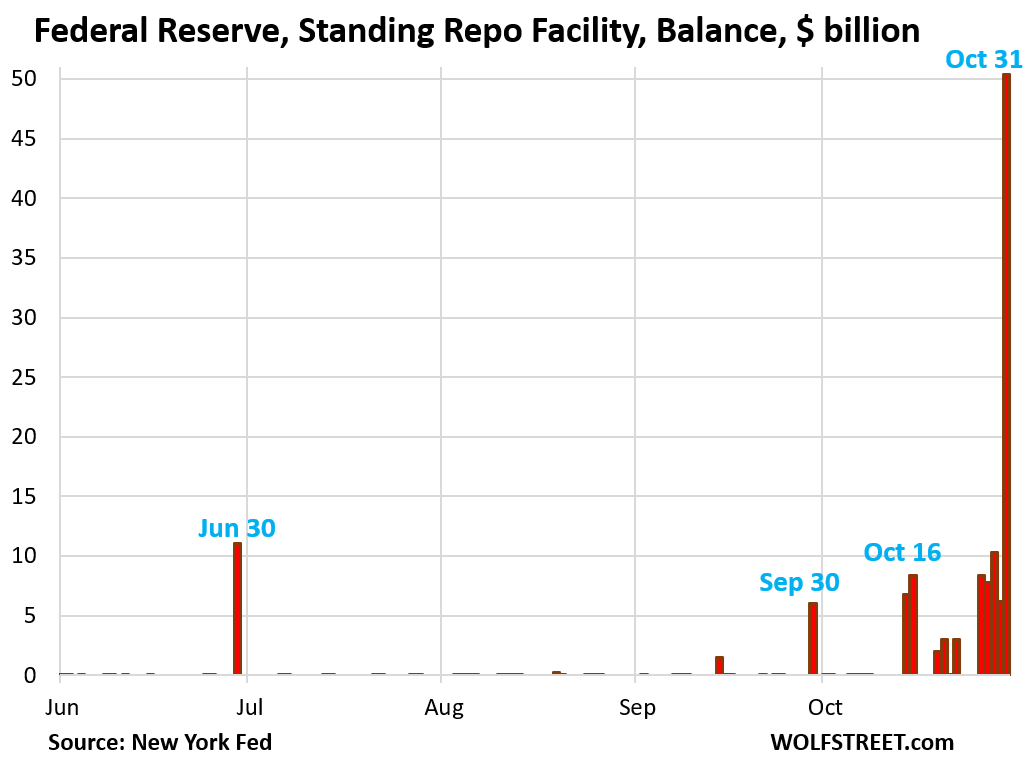

Dallas Fed president Lorie Logan’s speech this morning couldn’t incorporate what happened at the Fed’s new and improved Standing Repo Facility (SRF) at the auction this morning and at the auction this afternoon. But she should be pleased. Usage of the SRF, where banks can borrow from the Fed overnight at 4.0% currently, spiked to $50 billion, the highest since the SRF was established in July 2021.

“I was disappointed to see rates on a large share of tri-party repo transactions exceed the SRF rate at times this week,” she lamented the state of affairs where banks had not borrowed enough at the SRF to lend at higher rates to the repo market to quell the rising rates in the repo market.

“I anticipate that primary dealers will use the facility [the SRF] to obtain repo funding when it is economical to do so. Drawing on the SRF when the rate is economical is a sound way for a primary dealer to serve the [repo] market,” she said in the speech.

And she exhorted “dealers” – the banks that are the approved counterparties at the SRF – to borrow at the SRF and lend to the repo market when the rate spread makes this profitable for the banks because that would keep repo rates near the Fed’s policy rates.

“Dealers may now need to step up their readiness to access the SRF in response to rate moves,” she said.

And today, dealers did. She should be pleased. Today, they borrowed $20 billion at the morning auction and $30 billion at the afternoon auction at the SRF, $50 billion in total.

Spiking uptake at the SRF at month-end and quarter-end and on key tax days will become normal.

These repos are “overnight repurchase agreements” that mature the next business day (on Monday), when the Fed gets its $50 billion back and the banks get their collateral back.

If no new repos are taken out on Monday, the balance at the SRF will be zero, and the liquidity that was added on Friday is then backed out of the market. This occurred on the zero-balance days in the chart above, most recently on October 24, 22, 17, 14, 13, 12, etc.

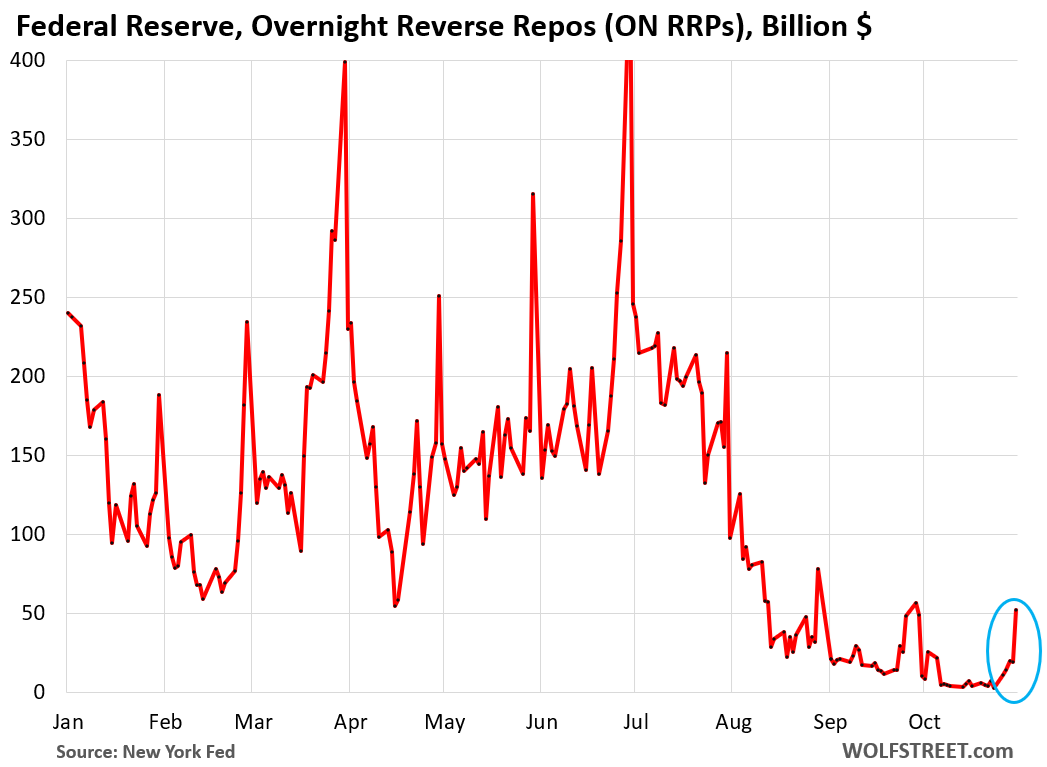

But ON RRPs also spiked to $52 billion: opposite direction.

The Fed’s Overnight Reverse Repo (ON RRP) facility is the opposite of the SRF. ON RRPs represent liquidity deposited at the Fed. The SRF represents liquidity drawn from the Fed.

ON RRPs spiked to $52 billion today. A week ago, it was essentially zero. Spiking ON RRP balances at the end of the month and at the end of the quarter have been normal, and this spike was rather small, compared to the prior spikes.

This $52 billion of ON RRPs counterbalanced the $50 billion drawn on the SRF facility today, and the net liquidity added by the Fed – so SRF balance minus ON RRP balance – was less than zero. In other words, the ON RRP facility effectively withdrew $52 billion in liquidity from the repo market, while banks borrowed $50 billion from the Fed via the SRF to supply liquidity to the market.

The $7-trillion money market fund industry is a big lender to the repo market. But money market funds can also put their extra cash on deposit at the Fed and earn 3.75% interest currently.

In early 2023, the ON RRP facility still had a balance of $2.3 trillion that QT has now largely drained from it.

Repo rates have become volatile.

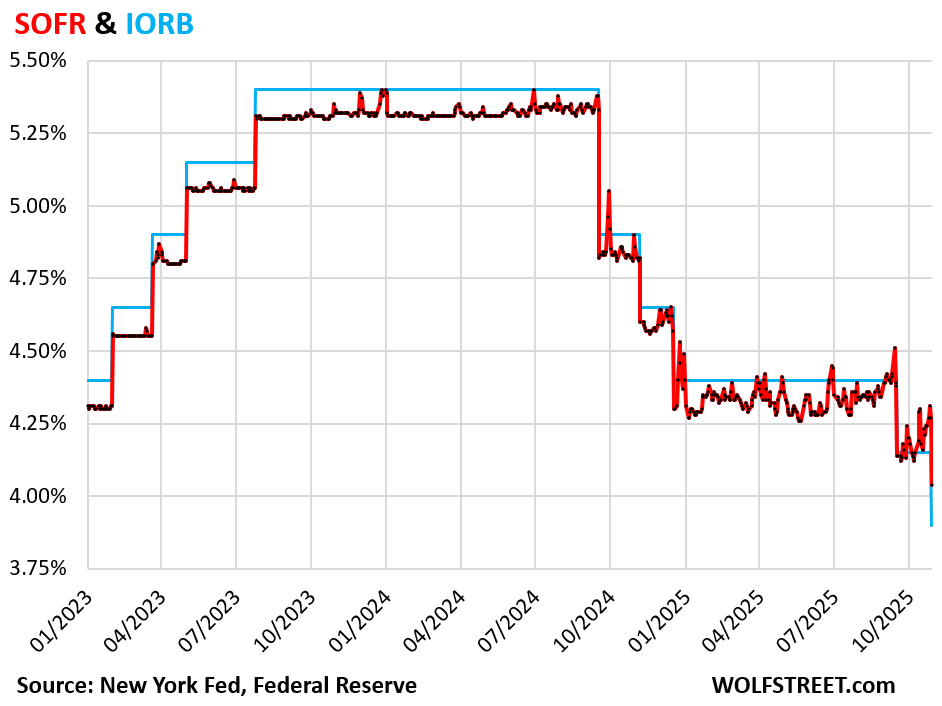

The Secured Overnight Funding Rate (SOFR), which tracks a $3-trillion-a-day segment of the repo market, has become volatile, and has risen above the interest rate that the Fed pays banks on their reserve balances (IORB), and the spread between SOFR and IORB has turned positive.

Normally, at month-end and quarter-end, when massive liquidity flows increase the pressures in the market, SOFR would spike for a day or two above IORB, and then quickly fall below it and remain below it, and the spread between SOFR and IORB would be negative.

SOFR was 4.04% on Thursday (today’s rates will be released on Monday). Intraday, repo rates ranged from 3.95% to 4.27%.

IORB was cut to 3.9% on Thursday as part of the Fed’s rate cuts announced Wednesday afternoon (blue line in the chart below). Normally SOFR (red) would be a few basis points below that. But this is month-end and tighter liquidity, and SOFR was 4.04%, so 14 basis points higher than IORB.

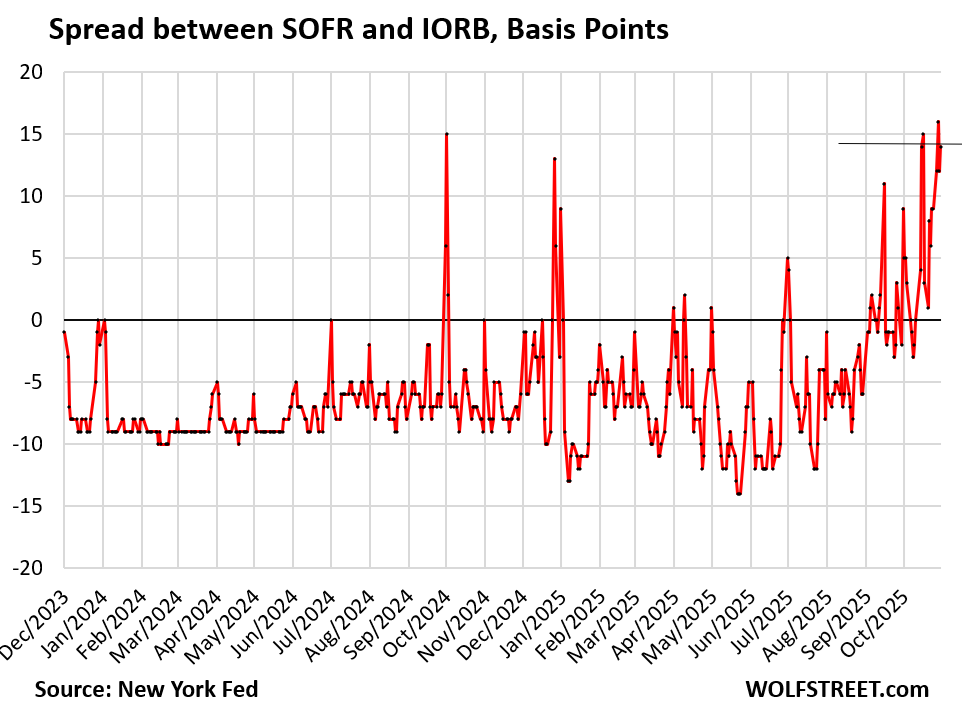

With SOFR at 4.04% and IORB at 3.9% on October 30, the spread between them was 14 basis points. This spread was slightly narrower than on October 28, when it reached 16 basis points.

Banks rich on reserves could lend to the repo market to profit from the spread, which may have been over 20 basis points (high end of SOFR was 4.27% on Thursday).

Banks that don’t want to use their reserves could have borrowed at the SRF at 4.0% and lend to the repo market and still make a nice spread. And they did today!

“With rates averaging higher than they were just a few months ago, the likelihood of the SRF rate becoming economical on some days is higher,” Logan said in her speech. By “economical,” she means, lower than market rates to where banks borrow at the SRF and lend at a higher rate to the repo market and profit from the spread.

And this has been happening, particularly today, when the uptake at the SRF spiked to $50 billion.

Logan cited these repo market rate and liquidity dynamics in support of the FOMC’s decision on Wednesday to end QT as of December 1.

Logan said today that the SRF should be further improved through central clearing:

“In my view, central clearing would further strengthen the facility’s effectiveness. The Fed’s counterparties could net down centrally cleared SRF borrowing against onward lending to other firms. Netting would reduce counterparties’ costs and risks of intermediating SRF funds to the broader market, helping liquidity to flow efficiently through the financial system.”

And she added:

“Streamlined SRF borrowing could be particularly helpful in the event of financial stress. Times of stress are the times when it’s most crucial for the Fed to be able to deliver the liquidity the system needs. Yet times of stress are also exactly when market participants try to de-risk their balance sheets by pulling back from intermediation.”

In her conclusion, she exhorted dealers again to make use of the SRF to lend to the repo market and thereby keep the repo rates in line and reiterated that the new and improved SRF should be further improved: “…dealers may need to increase their readiness to draw on the SRF in an environment where it is in the money more often, and the Fed should also continue to enhance the facility’s usability.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What this latest move in repos and RRPs proves is that the money markets are neither efficient nor continuous. The decision to end QT reflects this reality. Lori may be happy about SRF but maybe also scared about this odd behavior. Who was doing RRPs?

She also said that banks, after years of having endless liquidity, and getting above-market rates for their reserves, have lost their ability to manage their reserves properly because they haven’t had to do it in so long, and now banks need higher reserve levels to operate than they did before mega QE because they can’t manage them properly, and the Fed responds to that need with even more reserves — and this triggers, as she calls it, the “ratchet effect.”

Logan in her speech:

“Many banks have adapted their business models to an environment with more-than-ample reserves and market rates consistently below interest on reserves. These adaptations likely increased the aggregate demand for reserves compared with the prepandemic level. There’s a ratchet effect: To meet banks’ reserve demand in the short run, the Fed now must supply more reserves than it would have previously.

Since late summer, market rates have risen significantly relative to IORB. The rise in market rates relative to IORB will likely make many banks want to cut back on reserve holdings. There is only so much a bank can do, though, to reduce its reserve needs from one day or week to the next. It takes time to shed unwanted deposits or to adjust the composition of assets and liabilities so the bank needs less immediate liquidity. By sustaining a period of money market rates averaging close to IORB, including some modest, temporary swings higher, the FOMC can give banks the incentive to make longer-term adjustments. In turn, those adjustments will undo the ratchet effect, allowing the FOMC to meet banks’ long-run demand for reserves, rather than the temporarily higher short-run demand. This will let the Fed operate with a smaller, more efficient balance sheet over time while continuing to foster safe and efficient liquidity for the banking system.”

” have lost their ability to manage their reserves properly because they haven’t had to do it in so long”

Just wondering. Can you give an example of this? I’m certainly not questioning your reasoning, but how do banks “forget” how to manage reserves? That seems very odd. Do they have fewer options of where to place these monies? Why is it harder now specifically? I can’t imagine it’s just due to lack of remembering.

I just told you what Dallas Fed president Logan said in her speech. In her prior job, she was the head of the NY Fed’s trading activities and securities portfolio (SOMA) and knows the technical and market aspects inside and out. I linked the speech in the article. You should read it. it’s good.

The banks will need to closely watch their cashflows and, with predictability, time their depositors withdrawals and match them with their electronic deposits. Obviously, banks that intermittently come up short on liquidity will need to have sufficient collateral such as treasuries etc. to use for repo purposes. So, if banks will get less yield on IOER or IORB they could move into treasuries for collateral and use the SRF etc. There is a $1 million dollar minimum to participate in the Repo market and there are smaller institutions that don’t regularly have that much liquidity on hand. They usually have to borrow at a higher cost.

Quote from Mr. Wolf text: “…banks had not borrowed enough at the SRF to lend at higher rates to the repo market to quell the rising rates in the repo market.”

Sounds to me like this would be a profit center for a bank. Who wouldn’t take that cash and profit off the spread, assuming the money can be obtained at the same time a repo borrower is lined up. Sounds like the Federal Reserve should create a repo borrower “window.”

The SRF is the “repo borrower window,” as you call it.

Logan addressed an issue in her speech. The text I quoted in my comment above, in reply to RC Whalen, alludes to that: banks have gotten out of practice of managing reserves and liquidity and need to get back into it, after years of everything being flooded with liquidity.

Or the serial grifters are about to lose their shirt on a leveraged bet about to go wrong. Executive action is required.

Just like the last time, the public pays for it with an astonishingly profound lack of vigor that hasn’t been seen since the collapse of the Roman Empire which is still a work in process.

Normally, banks borrow from each other for overnight needs. The Fed discount window usually charged 25 basis points over the overnight rate. So, since the Great Financial Crisis, banks were reluctant to loan to each other. I think you know what that implies. The Fed became the lender of last resort and now, more than 17 years ago, the Fed is trying to get back to “normal”.

50 billion is a rounding error in a trillion economy. Each morning is reinforced by an increase the stock market share price.

According to my models, this might be a good time to do do what I did last week was to sell grossly overpriced equities and

She also said that banks, after years of having endless liquidity, and getting above-market rates for their reserves, have lost their ability to manage their reserves properly because they haven’t had to do it in so long, and now banks need higher reserve levels to operate than they did before mega QE because they can’t manage them properly, and the Fed responds to that need with even more reserves — and this triggers, as she calls it, the “ratchet effect.”

excellent synopsis of the larceny that we every day mugs navigate,

How long will it be before banks hand this money management over to AI & then layoff tons of people? That seems quite plausible.

Does this activity suggest rates are at unrealistic levels (too low)?

Spiking up and through the Fed’s policy rates (3.75 to 4)?

Just seems like the Fed is trying to hold the beach ball under water.

Wolf:

Please share again which large banks or dealers are most likely borrowing from FED using SRF facility and what they are pledging. Then please again share who is borrowing,doing a repo with such banks and what type of collateral are they using. I assume those entities borrowing from the banks do not have direct access to the FED?

“what type of collateral are they using”

They can only use Treasury securities and government-backed agency MBS as collateral.

“who is borrowing, doing a repo with such banks”

You mean after the bank borrows from the SRF and then lends the proceeds to the repo market, who are the entities that the bank lends to via new repos? So there are different parts of the repo market, but much of it is like the stock market: when you buy a stock, you don’t know who the seller of that stock is. You’re just buying from the market through a third party.

“which large banks or dealers are most likely borrowing from FED using SRF”

It is not disclosed which individual bank uses the SRF. But they have to be approved counterparties, and there are only 40 of them for now, listed below which include the big broker-dealers plus some regional ones, some US entities of foreign banks, and a big credit union:

Ally Bank

Bank of America, National Association

Banco Popular de Puerto Rico

Barclays Bank PLC, New York Branch

BMO Bank N.A.

Canadian Imperial Bank of Commerce, New York Branch

Capital One, National Association

Charles Schwab Bank, SSB

Charles Schwab Premier Bank, SSB

Charles Schwab Trust Bank

Citibank, N.A.

Citizens Bank, N.A.

Credit Agricole Corporate and Investment Bank

East West Bank

Fifth Third Bank, National Association

First-Citizens Bank & Trust Company

Goldman Sachs Bank USA

HSBC Bank USA, N.A.

JPMorgan Chase Bank, N.A.

KeyBank National Association

Manufacturers & Traders Trust Company

Mizuho Bank, Ltd., New York Branch

Morgan Stanley Bank, N.A.

Morgan Stanley Private Bank, National Association

MUFG Bank, Ltd., New York Branch

Natixis New York Branch

Navy Federal Credit Union

PNC Bank, National Association

Regions Bank

Royal Bank of Canada, Three World Financial Center Branch

State Street Bank and Trust Company

Sumitomo Mitsui Banking Corporation, NY Branch

The Bank of New York Mellon

The Huntington National Bank

The Norinchukin Bank, New York Branch

Truist Bank

USAA Federal Savings Bank

U.S. Bank National Association

Wells Fargo Bank, N.A.

Zions Bancorporation NA

Wolf:

When does temporary, short term liquidity to make sure market transactions clear and timely and to support orderly markets…..become a proverbial punchbowl and put option to those participants that are overextended and that someday need liquidated?

The SRF is NOT a punchbowl. It costs 4.0% to borrow at it, and borrowers have to pledge good collateral. 4% may sound low to you, but it’s high for banks. Banks borrow at close to 0% from most of their depositors, though they’re paying more on CDs, and their average cost of funding (from all deposits and all other forms of borrowing) is around 2% now. So the SRF is TWICE AS EXPENSIVE. That is why it is used so little, and the Discount Window, also 4%, is used even less.

SRF is a blowoff value to accommodate upside pressures in the money market. Pegging interest rates is getting more complex. What is R * now?

The corresponding uptake in O/N RRPs seems to be counterintuitive. It must be the result of nonbanks redistributing IBDDs?

So it was Oct 31. The month-end uptake of ON RRPs was small compared to prior month-end uptakes.

By Wednesday, ON RRP and SRF balances will likely be very low or zero.