Pending home sales and applications for mortgages to purchase a home are near historic lows, and lower mortgage rates have not stimulated demand.

By Wolf Richter for WOLF STREET.

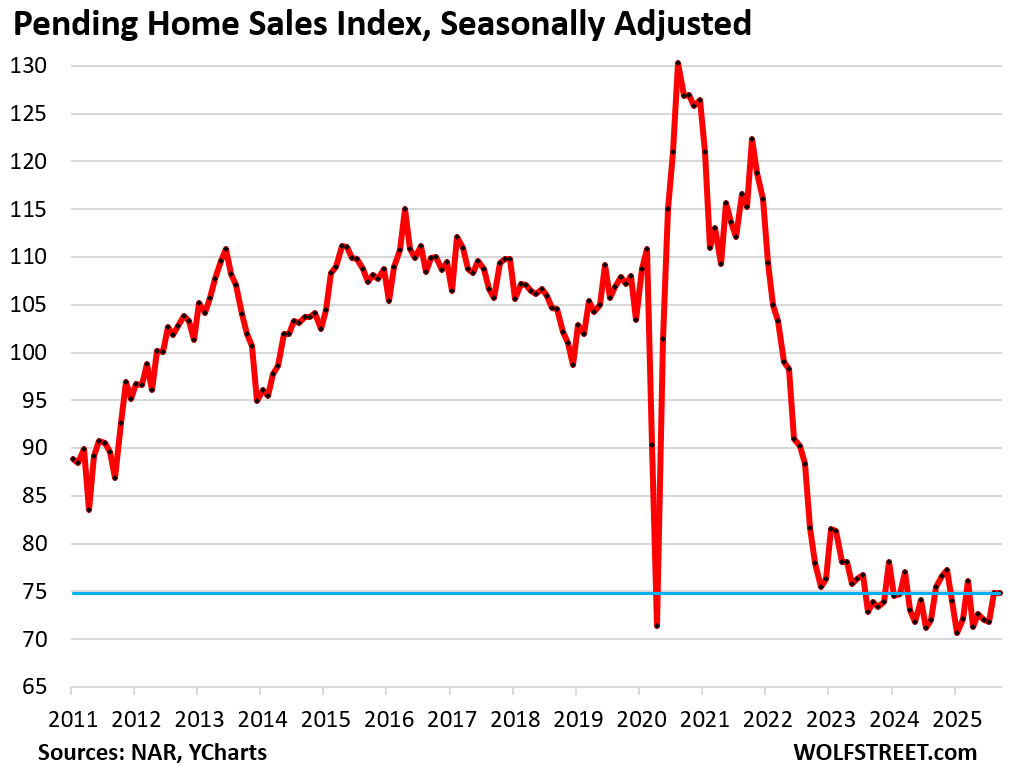

Pending home sales – tracking the number of contracts signed – were unchanged in September from August, and were down 0.9% from the collapsed levels a year ago, seasonally adjusted.

Pending home sales compared to the Septembers in prior years:

- 2024: -0.9%

- 2023: +1.2%

- 2022: -8.3%

- 2021: -35.1%

- 2020: -41.1%

- 2019: -30.7%.

The new normal? This completes the third year in a row that pending sales have zigzagged along record low levels in the data by the National Association of Realtors, which goes back to July 2010. There simply has been no improvement for three years (historic data via YCharts):

Pending sales are based on contract signings and track deals that haven’t closed yet and could still get canceled because buyers cannot afford homeowner’s insurance, or cannot sell their own home, or for other reasons.

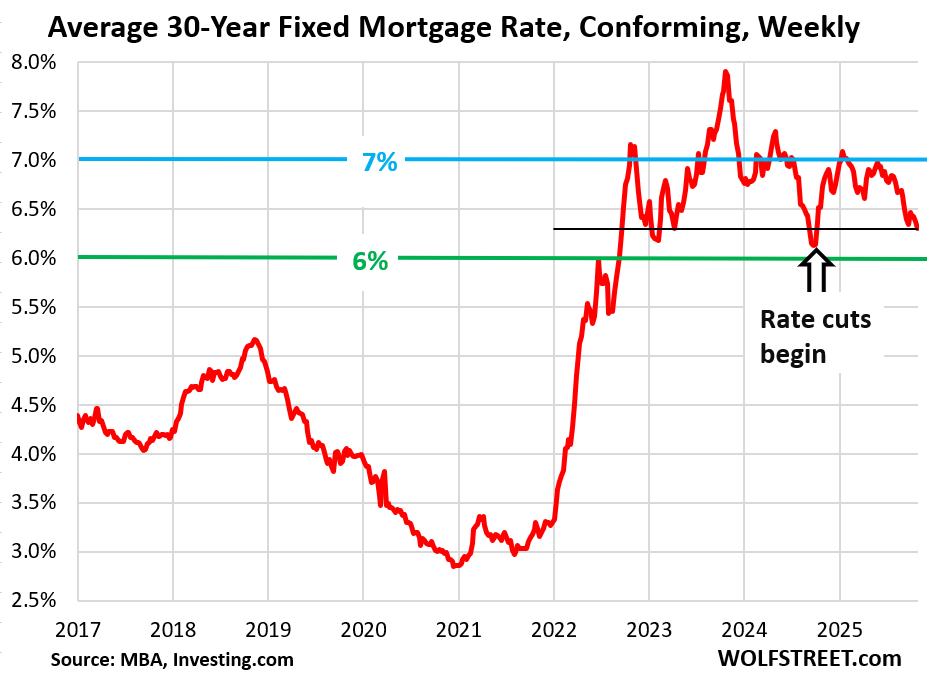

But the average mortgage rate for conforming 30-year fixed mortgages declined by 7 basis points to 6.30% in the latest week, the lowest level in a year, according to the Mortgage Bankers Association today.

Since the end of May, mortgage rates have dropped by 68 basis points (from 6.98%). Yet home sales have continued to zigzag along the record low levels.

Mortgage rates, according to the MBA’s measure, bottomed out in September 2024 at 6.13%, just before the Fed started cutting interest rates.

But this range between 6% and 7% was at the low end of the historic range before 2008 and before QE – including the Fed’s purchases of MBS – which distorted everything.

Applications for mortgages to purchase a home in the latest week ticked up from the drop of the prior week, but not enough to make up for all of the drop, according to data from the MBA today.

These purchase mortgage applications are an indicator of home sales in the near future.

Demand for mortgages to purchase a home began to plunge over three years ago and has been wobbling along these very low levels ever since.

Compared to the same week in 2019, purchase mortgage applications were down by 34%, the new normal – despite the much lower mortgage rates. The immensely hyped theme that lower mortgage rates would unleash waves of demand just hasn’t panned out.

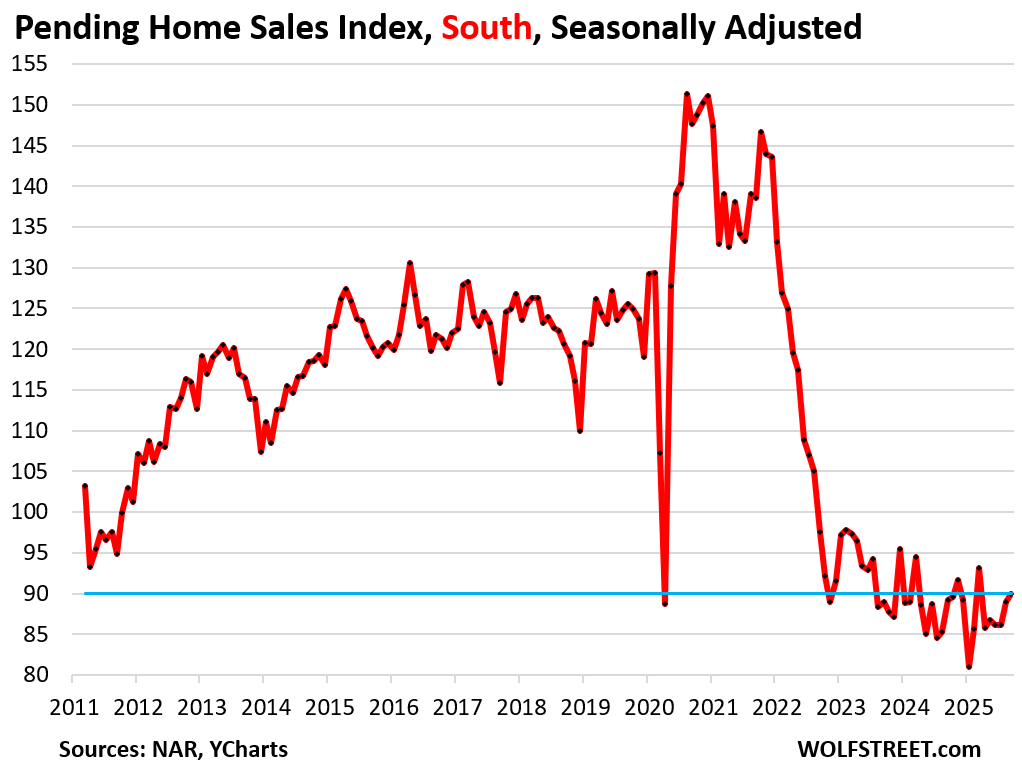

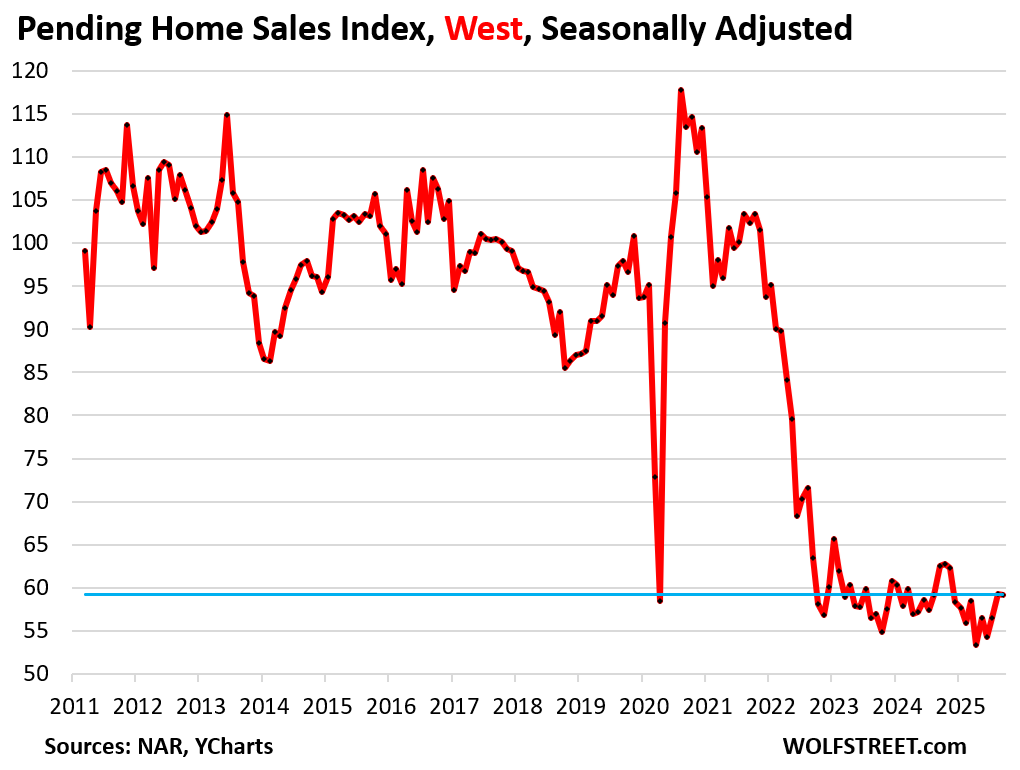

Pending home sales by region.

A map of the four Census Regions is posted in the comments below.

In the South, pending sales ticked up 1.1% in September from August, and by 0.9% year-over-year, seasonally adjusted, according to the NAR today.

Compared to the Augusts of prior years:

- 2024: +0.9%

- 2023: +1.1%

- 2021: -35.0%

- 2020: -39.1%

- 2019: -28.3%.

In the West, pending sales dipped by 0.2% in September from August, and were down 5.3% year-over-year.

Compared to the Septembers of prior years:

- 2024: -5.3%

- 2023: +3.9%

- 2021: -42.1%

- 2020: -47.8%

- 2019: -39.5%.

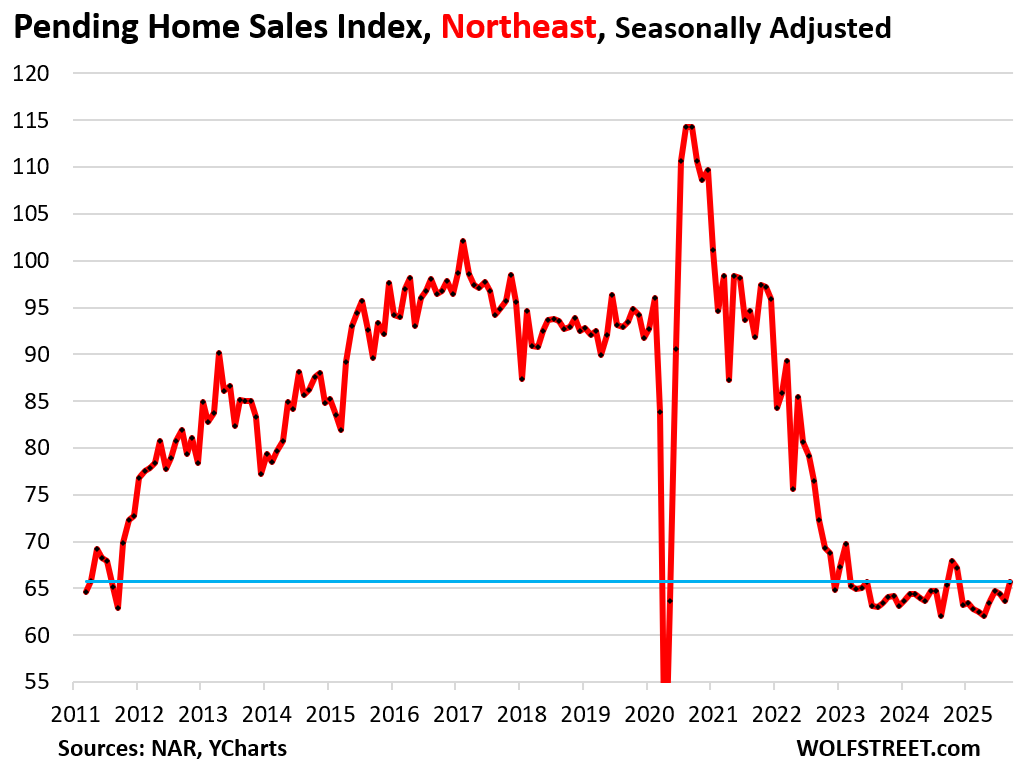

In the Northeast, pending sales rose by 3.1% month-to-month, and were a hair higher than a year ago, seasonally adjusted.

Compared to the Septembers of prior years:

- 2024: +0.5%

- 2023: +3.5%

- 2021: -28.5%

- 2020: -42.5%

- 2019: -29.7%.

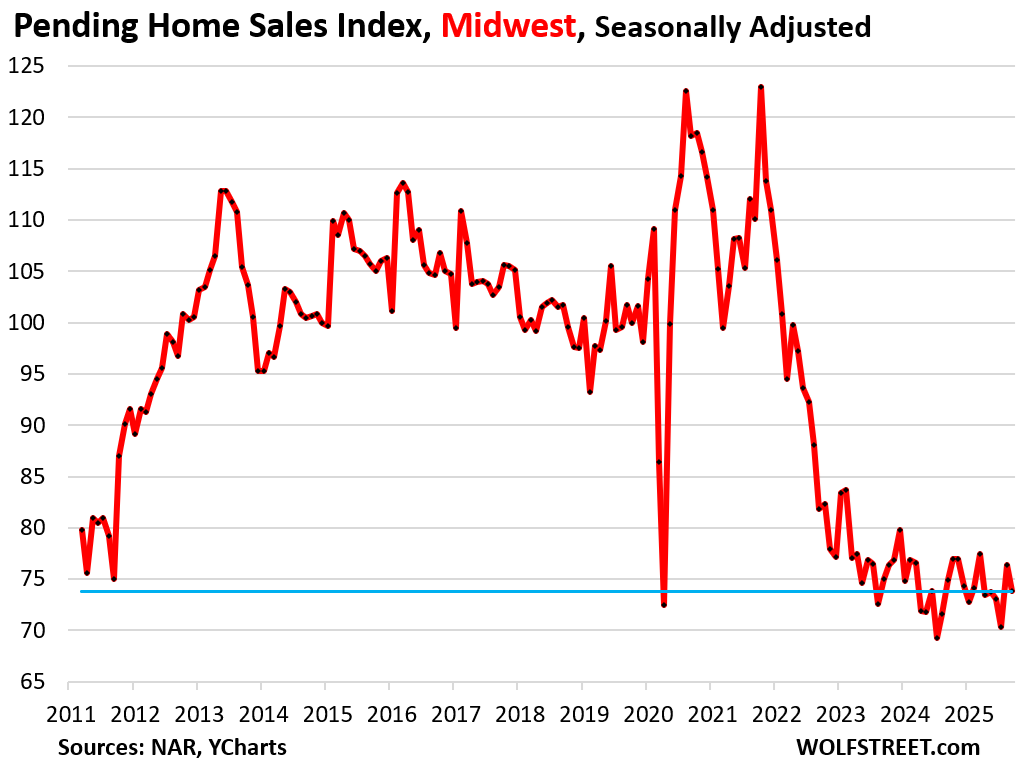

In the Midwest, pending sales fell by 3.4% in September from August and by 1.5% year-over-year.

Compared to the Septembers of prior years:

- 2024: -1.5%

- 2023: -1.6%

- 2021: -33.0%

- 2020: -37.6%

- 2019: -27.4%.

Clearly, the market is not thawing. Prices are still too high after they exploded by 40%, 50% or even 70% in specific markets over the course of 2-3 years.

They’d exploded because the Fed had forced mortgage rates down via massive purchases of Treasury securities and MBS, to where mortgage rates dropped below 3% while inflation was spiking toward 9%, and borrowing at 3% with inflation at 5%, 6%, 7%, and then higher was free money, better than free money, and when money is free, prices don’t matter, and home prices exploded.

But those prices don’t make economic sense, they’re too high, they’ve destroyed demand. And in some markets, they have started to come down fairly hard:

The 23 Bigger Cities where Condo Prices Dropped by 12% to 28% through September

The Cities Where Condo Prices Are Now Below their Housing Bubble Peaks 20 Years Ago

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The four Census Regions of the US:

Wolf has been an information lifeline for most here. It appears the audience here is old guys trying to understand what is happening.

Wolf is savvy about Homes and Autos which are the giant economic drivers in our economy. The money velocity resulting from these two sectors along with all associated with these sectors are the best (and only) real way that the old guard (us) can assess and attempt to use for comprehension of what is to come and what is to do….

In short, imagine how it is to deal with Google… No customer service like we all want. Instead, it is one-way, top down, do it yes or no. Binary is tech which is yes/no. No grey area to speak of…. That sums it up and it means something ten times more impactful in every subject especially warfare.

In short, what seems to be the case is to manage your resources to protect what you have and in terms of income producing assets you will have to look for the many “wolves” of which AI are the equivalent of a pack of wolves moving fast so you never see them.

I am glad to be 70…. It has been a good run… Thanks to Wolf for the info to help me see our demographic in relation to the big picture now unfolding. I am a perennial student. I may end my life with a Phd in something worthwhile like agriculture. Dirty hands/Honest money.

See you on the other side =)

It’s not all old. I’m young and have been reading him for many years. Wolf is extraordinarily generous with his limited advertising and detailed analysis. Few people can match the integrity here.

Ungrateful peasants

The lower mortgage rates will eventually help, BUT at much lower levels than where they are now. I still want to buy a home before I die, but hard to argue at $500 rent.

Where do you live that you manage to get a $500 rent? And how did you find this oasis of sanity?

I review the national metro apt rent surveys pretty frequently and $500 seems unachievable in even smaller metros – at best, the Wichitas and Akrons of the world might bottom out at $700-$750 nowadays.

And there are maybe only 20 metros out of the top 100 where the the listed one bedroom median rates are below $1000 (far worse than pre-pandemic, pre-open-border insanity).

How “unhealthy” of a correction is this? I understand that the price/rate equation was totally out of whack during the free money era, but it now feels like we’re returning to a more reasonable place, historically.

Are we unwinding, or is this just the eye of the storm?

It’s a twist to what they say about the economy …

“It’s the price stupid!”

Anyone, especially agents trying to tell you otherwise is either stupid, manipulative or naive, perhaps elements of all 3 at once. Especially for folks in HCOL area, no $1M crapshack in sketchy hood is not the new norm

“the average mortgage rate for conforming 30-year fixed mortgages declined by 7 basis points to 6.30% in the latest week, the lowest level in a year.”

The hopium is on full blast: ATH indexes and languishing yields.

Trade agreements and rate cuts are purported to usher in the golden-est of this golden age!

Reality may show that market rates have already bottomed, and will turn upward after this cut.

Mortgage applications may stay low, and transactions may be dominated by cash buyers?

The price drops are abundant and the lack of price history on most of the popular RE sites suggests people are again doing their homework before buying?

I don’t think your average buyer thinks about historical rates but rates and mortgages their friends and family have. Doesn’t mean it will happen and reality won’t hit but I am sure many are seeing where things are at in the Spring.

You may be right but with multiple bubbles since 2000, people are slowly getting smarter about home market insanity. The current bubble seems to only maybe be about 50%-60% of the pre-2008 bubble (likely because potential buyers learned fear – proper fear).

And that’s including the truly insane pandemic Bubble – prices exploded, but the actual number of transactions did not parallel them – which really matters on the way down, since fewer people will be welded at the hip to pandemic peak prices.

Hopefully this will continue on for a decade or more. It would be good for generations to grow up believing house prices can only go down, and real estate, at least in the form of single family housing, is a terrible investment.

This. A prolonged contraction to strangle the idea that a house is an investment. A house is a lifestyle and liability, you can do just as well in index funds and your money is liquid and not tied up in a house.

Of course index funds might also go down if the everything bubble bursts…

Excellent point – S&P 500 PE ratios are in excess of 30 with 15 being the historical norm – meaning a 50% drop would only return things to historic norms.

Based on my earlier counts of today (can’t vouch for my free data source, but my sense it that it is likely broadly right at a minimum) shows that a freakin’ incredible 170 companies of the SP 500 have PEs in excess of 30, 330 companies have PEs in excess of 20.

These are the biggest companies there are – and rational calculations tie PE ratios to expected growth rates.

There is no way in hell that 170 of the largest companies on earth are going to grow at rates double that of the period from say 1900 to 2000 – unless a duplicate earth (equally wealthy) is discovered to do trade with.

The only way this insanity has been grown and propped up has been through essentially 20 years of ZIRP (2002-2022) and magic-adjacent expectations in things like the Metaverse (RIP) and AI (RIPending).

Cas127: Apparently, super business man Zuck, stated this recently:

Zuckerberg said the company is “aggressively” preemptively building up capacity to prepare for the arrival of superintelligence, where Meta will be “ideally positioned for a generational paradigm shift in many large opportunities.”

My message is be prepared for what’s coming (many large opportunities)! /s

Bingo. Destroying the expectation that owning a hone is the key to building “generational wealth” is necessary to restoring long term sanity to the housing market.

Sufficient additional housing *supply* would also massively help…but that would puncture the “wealth effect” bubble that 20 years of Fed ZIRP created.

So I suspect that the Fed and local home permitting authorities are going to be slow-walking/actively hostile to much faster supply additions.

The volume of new housing has greatly increased in the last 2 or so years…but that is off a mediocre base following an extended period of crater-dwelling in terms of new supply.

If local home permitting authorities (what a concept in a free country) allow it, new home supply could likely match 2024 levels for 3 or 4 more years and bring more pricing sanity to the housing market.

But that ain’t the policy history of 2002-2022.

Wolf, this is unrelated. I think it breaks one of your rules. I’m too impatient to wait for your next article on the subject. But can you bring back “The Most Reckless Fed Ever” headline with a twist after today’s rate cut:

“Still a Fairly Reckless Fed”?

We’re a long ways from that. But I will if the Fed will.

Houston, we have a problem; house prices are too darned high.

“Clearly, the market is not thawing. Prices are still too high after they exploded by 40%, 50% or even 70% in specific markets over the course of 2-3 years.”

Who or what caused the problem?

“They’d [prices] exploded because the Fed had forced mortgage rates down via massive purchases of Treasury securities and MBS, to where mortgage rates dropped below 3% while inflation was spiking toward 9%,…”

This is the Fed’s “wealth effect;” increased paper wealth for asset holders. Both houses and stocks were targeted way back in 2010 to reinflate these asset bubbles after the GFC collapse in 2008-2009. There are no more free markets. This is central planning; a command and control economy. The results are predictable and devastating to the bottom 90% of the economy.

The U.S. housing market is FUBAR. The only workable solution going forward is much lower housing prices. Just back out all of the price gains since 2019. Absent further (misguided) Fed policy, that will happen, but will likely take years.

It’s a direct result of massive market interventions by .gov and the Fed. This was intentional. This was policy. The Fed could and should be replaced with the U.S. 2 yr. Note yield. See former USSR for recent example of a failed Socialist State. Let’s not be USSA.

Both U.S. housing and stocks are (each) in another asset bubble. Think dot com + housing bubble 1.0. Together, since it wasn’t bad enough each time when they were separate, so let’s combine them. That should be fun!

Based on the historical record, asset bubbles always burst and prices mean revert. An inconvenient truth. Enjoyed the boom? Now enjoy the bust.

The lack of new mortgages created clearly will affect the supply/creation of MBS. Does this lack of supply increase demand?

Many new mortgages fund house purchases that mostly pay off old mortgages so it is not certain that there will be any effect on supply…

As a builder I can’t tell you how many HUNDREDS of people have told me they are waiting for RATES to come down. Not PRICES, RATES. The Fed is purposely strangling the building industry to death.

Those that are telling you that are the ones that the effing RE industry has successfully brainwashed with bullshit, such as that home prices never drop…

https://wolfstreet.com/2025/10/26/the-cities-where-condo-prices-are-now-below-their-housing-bubble-peaks-20-years-ago/

“such as that home prices never drop…”

Not enough truth telling chart porn here…show him 20 metro SFH price charts from 2002-2012 (The long night of ZIRP 1.0).

In the era of the Internet, there is no more reason for “Big Lies” like “real estate can never go down” to survive unchallenged.

The public (kinda) picking up on this likely caused Bubble 2.0 sales volumes to maybe only reach 60% of bubble 1.0 levels – which while still pretty sh*tty at least provides hope that the arc of history bends towards less sh*ttiness.

Most people only care about the monthly payment amount. Anybody focused on rates has just been listening to the industry trying to push their narrative to preserve their margins (builders included) and sell out their neighborhoods before people start seeing the same home they just bought sell for less next door. Price influences taxes, insurance, and other things that add to the monthly expense of owning a home so anybody rational wants those to drop more than rates, but at the end of the day it’s the monthly payment that drives purchases.

Look at all of the major builders, they’ve been using rate buy downs and other tricks to try and preserve the prices because they know once that bottle (pricing) is opened, there is no closing it back up. Hopefully you’ve been saving the massive amounts of cash you should have been making over the last few years.

The fed doesn’t set mortgage rates though- the free market does.

And don’t kid yourself: everyone knows your potential buyers would snap up your houses, even at today’s rates, if you ffered a 25% price cut.

So, this is now PROOF in the pudding that Humpty Dumpty is broken beyond repair. Can’t be fixed. Shattered. No hope.

Send rates to ZERO – same result – BROKEN!

It was one Big Beautiful Bubble. it made some people rich. It made a lot of people feel rich. It made a lot of people happy. It made business deals happen. What happens to those bubbles you blow with liquid soap? Oh yeah – they pop!.

A lot like jumping out of an airplane with a wingsuit on but no parachute – it’s one heck of a ride on the way down, but it ends in disaster.

Financial bubbles always end in disaster. 🫧

Yes, the flurry of mergers and circular tech deals could indicate we’re finally nearing the end of the cycle. They said the AOL-Time Warner tie up was going to be the greatest thing since sliced bread and it ended in tears. Now Paramount wants to buy Warner-Discovery after it just completed a merger. Anyone remember Lucent? People said it would never go south because they made physical goods (of the future!) unlike all the dotcoms with zero revenue. If it could happen to Lucent it could happen to nvidia

Prices are too high.

Homeowners insurance is getting hard to get and if you do the price is very high.

Property taxes due to high prices are high.

It’s more than just the mortgage rate now.

San Diego county I am still seeing homes list for double what they paid in 2022. Ridiculous!!! Still seeing some properties sell over asking. Ridiculous!!! Seeing most inventory sit. The market needs to bust to get back to normal.

We scream prices are to high all day, but apparently homeowners are happy (or at least have the capacity) to sit on the sidelines. An interesting phenomenon that even with the pressures of increasing insurance and property taxes, homeowners for the most part are in no hurry to sell. With lowering rents, renters in no hurry to buy. Buyers and sellers are inconvenienced, but the ones really being hurt are those who live off sales: realtors, mortgage brokers, etc….

I like your comment, however no one is happy to sit on the sidelines. Having hundreds of thousands or millions of people sitting on the sidelines is a symptom of a BROKEN MARKET.

“but the ones really being hurt are those who live off sales: realtors, mortgage brokers, etc….”

Hmmmm….,more reason then ever to remain on buyers strike…..,kidding,I think.

Recently our DOJ confiscated about $150B of bitcoins from one of the largest ponzi scam in the recorded history. The center of this crime is in Cambodia 🇰🇭. It is said that real estate especially in locations such as SoCal has become the venues for money laundering. Many who participated in helping & selling (buying really) these properties will face justice. Wonder how much this will affect the market & bring down the price to the level that is supported & sustained by disposable income of law biding citizens. I so look forward to what is about to be revealed.

Before all the folks declaring a collapse in home prices I always look to months of inventory as that key indicator. Right now nation wide it is still at 4.9 months. It needs to get over that key 6 months mark to be declared a full sellers market.

A key note as real estate is local – FL is at 5.3 for homes and 9.7 months for condos, hence why prices are melting down more quickly there.

It’s over 6 months where prices are dropping, and days on the market have soared in those markets too, including Florida, as you pointed out, but also in many other markets. But inventory is tight in other markets where prices are not dropping, such as Chicago, New York, and Philadelphia. I have a series of articles with supply and days on the market, by major market that you can check out. Here are some examples:

Days on the market by market:

https://wolfstreet.com/2025/10/03/it-took-the-longest-time-to-sell-a-home-since-at-least-2016-if-it-sold-at-all-in-many-markets/

Prices AND inventories of 33 big metros — you’ll see the relationship between inventory and prices:

https://wolfstreet.com/2025/09/16/the-most-splendid-housing-bubbles-in-america-aug-2025-price-drops-gains-in-33-large-expensive-metros-us-home-prices-fell-yoy/

Days on the market in California’s metros:

https://wolfstreet.com/2025/09/09/in-california-the-time-a-home-sat-on-the-market-in-august-before-it-was-sold-or-delisted-soars-to-highest-in-at-least-a-decade/

Inventories in that corner of the US:

https://wolfstreet.com/2025/08/13/inventory-of-homes-for-sale-in-new-york-philadelphia-chicago-boston-nashville-atlanta-washington-dc-columbus-detroit-minneapolis/

inventories in the biggest cities in Texas:

https://wolfstreet.com/2025/08/08/inventory-of-homes-for-sale-balloons-in-texas-and-its-big-metros-dallas-fort-worth-houston-austin-san-antonio/

days on the market in Florida:

https://wolfstreet.com/2025/08/07/days-on-the-market-blow-out-in-floridas-big-metros-as-homes-for-sale-dont-sell-and-pile-up/

inventories in these cities:

https://wolfstreet.com/2025/08/04/inventories-of-homes-for-sale-surge-in-denver-seattle-phoenix-tucson-portland-las-vegas-salt-lake-city-albuquerque-boise/

etc. etc.

As morbid as this sounds, I think about the great the wealth transfer when all of the boomers start moving to care facilities or even passing away and their houses get listed. I believe we are starting to see this happen in some areas and this will continue to add more houses to the market. Over the next several years, generational change will be a major factor in the economy.

It’s the post-pandemic price-stabilizing contraction, for which artificial intelligence will take the fall. Vent your rage into the chat box.