American consumers are doing OK on their auto loans.

By Wolf Richter for WOLF STREET.

Every time a specialized privately-owned subprime auto dealer-lender implodes – which happens periodically in this high-risk-high-profit business – the headlines are full with, Oh Deary, the American Consumer is cracking, tapped out, stressed out, and in free-fall, or whatever. Some even put into the headlines some nonsense about surging delinquency rates. And the latest collapse of an auto dealer-lender, that of Tricolor Holdings, is no exception.

The debris of Tricolor, a privately owned AI-powered fintech used-vehicle-dealer-lender with 60 stores, is now being picked through in a Texas bankruptcy court, amid a mushroom cloud of fraud allegations by lenders from all directions, after they’d closed their eyes for years in order to not see what they should have seen but didn’t want to see because they were lusting after the high interest rates and fees. So now, part of that money has vanished.

But don’t cry for the lenders. They knew that Tricolor largely lent recklessly to illegal immigrants with no driver’s license and no credit rating (so they weren’t even subprime), which Tricolor marketed as “social lending.”

Social lending has been promoted for over two decades by the federal government through the Community Reinvestment Act (CRA) and the Community Development Financial Institutions (CDFI) Act. In 2019, the Treasury Department certified Tricolor as a CDFI, granting it a federal endorsement as a “socially responsible” lender.

It’s hard to imagine a more intensely reeking cesspool than Tricolor – a bankruptcy trustee said that the initial reports “indicated potentially systemic levels of fraud” – and it’s hard to imagine more reckless banks, lenders, and investors who eagerly closed their eyes to these shenanigans because they were chasing yield and they didn’t want reality to get in the way – typical behavior at the peak of a credit bubble. But it has zero to do with the cracking or whatever American consumer.

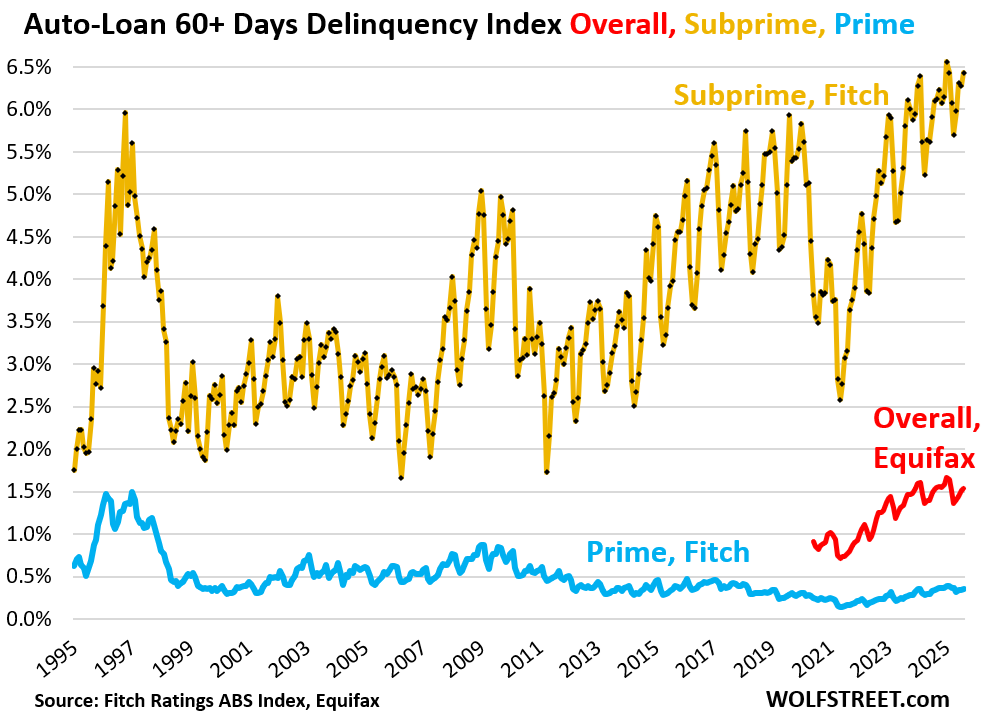

Consumers and their auto loans are doing OK.

All auto loans and leases, including subprime, had a 60-plus-day delinquency rate of 1.54% in August, about the same as a year ago, according to Equifax. The seasonal high was in January at 1.66%. Available monthly data from Equifax only goes back to July 2020, the absolute low of the free money era and lacks the pre-pandemic normal years (red in the chart below).

Prime-rated auto loans had a 60-day delinquency rate of 0.35% in August, roughly the same as a year ago, a little higher than in the free-money era, a hair lower than in 2017 and 2018, according to data from Fitch which rates auto-loan ABS. During the Great Recession, it peaked at 0.9%. In the mid-1990s, when auto-loan securitization was still new and was handled by cowboys, it peaked at 1.5% (blue in the chart).

Subprime means bad credit – a history of being late in paying obligations and not paying them at all. It does not mean low income. The young dentist in over his head is a classic example of higher-income subprime. They’ll get it worked out eventually. Low-income people often cannot borrow at all, and if they can borrow, the amounts are small.

But an outfit like Tricolor – and other specialized subprime dealer-lender chains that have collapsed, such as two in 2023 that I covered here – can lend recklessly, and these securitized auto loans blow up and drive the subprime delinquency rate.

Subprime auto lending is a small part of auto lending, done mostly by specialized lenders and specialized dealer-lenders, and is limited mostly to older used vehicles.

Fitch’s subprime 60-day-plus delinquency rate rose to 6.43% in August along seasonal patterns. The seasonal peak was in January at 6.56%, an all-time high. Compared to August a year ago, the delinquency rate was 33 basis points higher (gold in the chart).

Tricolor was a AI fintech star in Texas.

In 2023, the Dallas tech media still gushed:

“Tricolor, the largest used vehicle retailer to the Hispanic market in the US, has secured a new patent for its innovative AI tool called Automás. The tool lets customers self-select and finance vehicles, generating offers for different models and financing terms with machine learning. A unique feature of Automás is that it empowers customers to customize their own financing terms within the parameters of the system-generated offer.

“Tricolor said the new tool, U.S. Patent No. 11,574,362, leverages data across the company’s integrated platform to give historically marginalized consumers the power of self-selection when choosing and financing a vehicle from Tricolor.”

The funding for these deals.

Big used-vehicle-dealer-lenders obtain financing for the inventory of vehicles and for the auto loans they originate in three phases:

Floorplan line of credit, under which each vehicle, identified by its VIN, serves as collateral for a portion of the loan. The purchase of the vehicle is funded through the floorplan, and when the vehicle is sold, that portion of the loan is paid off.

Warehouse line of credit, under which the auto loans extended to vehicle buyers are temporarily funded by banks. In other words, funds from the warehouse line of credit are used to pay off the floorplan when the vehicle is sold. The collateral is each loan, collateralized by that vehicle.

Securitization, through which auto loans that had been temporarily funded through a warehouse line of credit are packaged into Asset-Backed Securities (ABS) and sold to institutional investors around the globe. The proceeds from the sale of the securities pay off the warehouse line of credit for those vehicles. These ABS are backed by auto loans that are collateralized by the vehicles.

And they’re all now alleging all kinds of sordid stuff. These three types of lenders to Tricolor, and a federal government investigation, have formed a mushroom cloud of fraud allegations. Tricolor allegedly pledged the same vehicles as collateral for multiple loans from multiple lenders, misrepresented the credit quality of the borrowers, understated the risks of the loans, etc., etc., and money has vanished.

But the last securitization occurred in June, $217 million, three months before Tricolor’s collapse, when everyone involved was still trying to close their eyes as hard as they could. A unit of Tricolor was also the servicer of the securitization; borrowers are supposed to send their payments to this unit of Tricolor, which is then supposed to forward the passthrough principal payments and interest to the ABS holders.

S&P Global rated the six slices of the $217 million Tricolor Auto Securitization Trust 2025-2. The four top-rated slices were all “investment grade” and amounted to $189 million, or 87%, of that securitization (my cheat sheet for corporate bond credit ratings by ratings agency):

- ‘AA’: $131 million

- ‘A’: $27 million

- ‘A-‘: $14 million

- ‘BBB’: $17 million.

The four slices were rated “investment grade” on the theory that the two lower-rated slices, representing 13% of the securitization, would eat the first losses, after the credit support measures built into the offering were used up, and that this would be enough to protect the investment-grade slices from losses when the borrowers – mostly illegal immigrants – failed to make their payments and failed to return the vehicle.

On September 12, two days after Tricolor had filed for liquidation in bankruptcy court, S&P Global put the bonds on “CreditWatch with negative implications.”

Tricolor was a creature of alleged fraud, taking advantage of willfully blind lenders and investors in the midst of a huge credit bubble when greed had turned their brains to mush. And it has nothing to do with American consumers and their auto loans.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is a dynamite piece, Wolf. I’m a corporate bankruptcy professional focused on CRE; the tide is washing out and providing a good view of random trash and dead bodies. It’s getting exciting! ZIRP and Covid Era Stimulus Squared fostered spectacularly profligate lending. (Good thing rates would never go up. 🙄). Of course, it’s always other people’s money getting thrown to the dogs. Some lender might lose his bonus or his job and get nasty things said about him in court. Big deal. The money is somebody’s ephemeral pension.

Are you a lawyer or do you work for a special services?

FYI: BlackRock put $90mn behind Tricolor in 2021, touting it as one of the asset manager’s first commitments in its “impact opportunities” strategy and for its use of artificial intelligence.

I’m betting a box of milk bones, that BlackRock was behind the patent process from the beginning , and they’ll probably mysteriously end up with that super valuable asset — that provided to be so critical in stealing cash ….

See also:

Creditors of PrimaLend, which provides financing to auto dealerships that cater to subprime borrowers, are weighing pushing the firm into bankruptcy after going unpaid for months, and as the industry reels from the recent downfall of Tricolor Holdings. Holders of the company’s $75 million bond due in 2028 are working with lawyers…

When money changes hands, signatures are required. Time for signatories to assume debts or occupy the cell. Until people are actually jailed – nothing will change.

Perfect

yea dont hold your breath. Animal spirits and all.

I wonder where all the money went from multiple financing of the same assets?

Yes, lots of people are wondering about that. It went somewhere.

Wolf, what’s up with your website. The add bar is operating like nefarious code.

Are you talking about the Cboe ad at the bottom of the page? Does it do something funny?

They better start warming up the printing presses for the next $10 Trillion bailout of all the AAA investments out there in the wild. Just Sam Altman’s shenanigans are going to need a trilly or two.

What about Carmax ?

They’re not a dealer-lender, and they don’t target subprime.

But Car-Mart targets subprime and is a dealer-lender. They’re publicly traded [CRMT], and their stock today hit a new 10-year low.

I wrote about it back when they ran into trouble in December 2023, and it has become part of my Imploded Stocks.

https://wolfstreet.com/2023/12/06/subprime-comes-home-to-roost-for-specialized-auto-dealers-lenders-their-investors-car-mart-was-next-to-confess/

Back in late July/ early August of 2007, the very first two subprime mortgage hedge funds blew up, both with Bear Stearns.

This event occurred < 2 weeks from my closing the sale of my business. I had been glued to the housing insanity for almost two years by then, and was well aware it was going to blow and take the economy either way it. I was practically praying every day my buyers did not disappear. (They did not).

I like to remind a few friends that “eventually and imminently are not the same words”.

I’ve long believed we could not turn a blind eye to housing, as I’ve long believed we could not turn a blind eye to the excesses and euphoria of our present markets.

While the reported numbers still look good, beneath the surface there are lots of troubles in housing, employment, commercial real estate, etc. But… the credit has kept flowing to paper everything over.

I’m personally of the belief you cannot have a strong economy with a lackluster housing market. Too many jobs both within housing and beyond (manufactures of housing related goods) are dependent upon it. And we all know housing is not doing every well.

My belief is that eventually this is all going to blow up spectacularly, just as we had in 08/09. Is it imminent? That part I don’t know.

Those two Bear Stearns funds were the first warning shots. I’m treating this current episode of Tricolor, First Brands, AND the “spill over” into Jeffries, regional banks, and others with the same sense of caution.

There is nothing systemic about specialized subprime auto dealers. They’re only a minuscule part of total auto sales. Regular dealers don’t do that. I have covered imploding subprime dealer-lenders since at least 2018, and the world hasn’t ended yet. They just do that. It’s a regular occurrence. It’s a slimy risky business, and these dealers implode, often overnight.

It’s nonsense to compare this to the mortgage crisis.

And in terms of mortgages, most of them now guaranteed by the government, and low-down-payment subprime mortgages are insured by the FHA. Banks have nothing to do with that. So you can forget that too.