Gold mark-to-market quarterly adjustment: +€158 billion for Q3 on gold’s price spike, largest ever write-up.

By Wolf Richter for WOLF STREET.

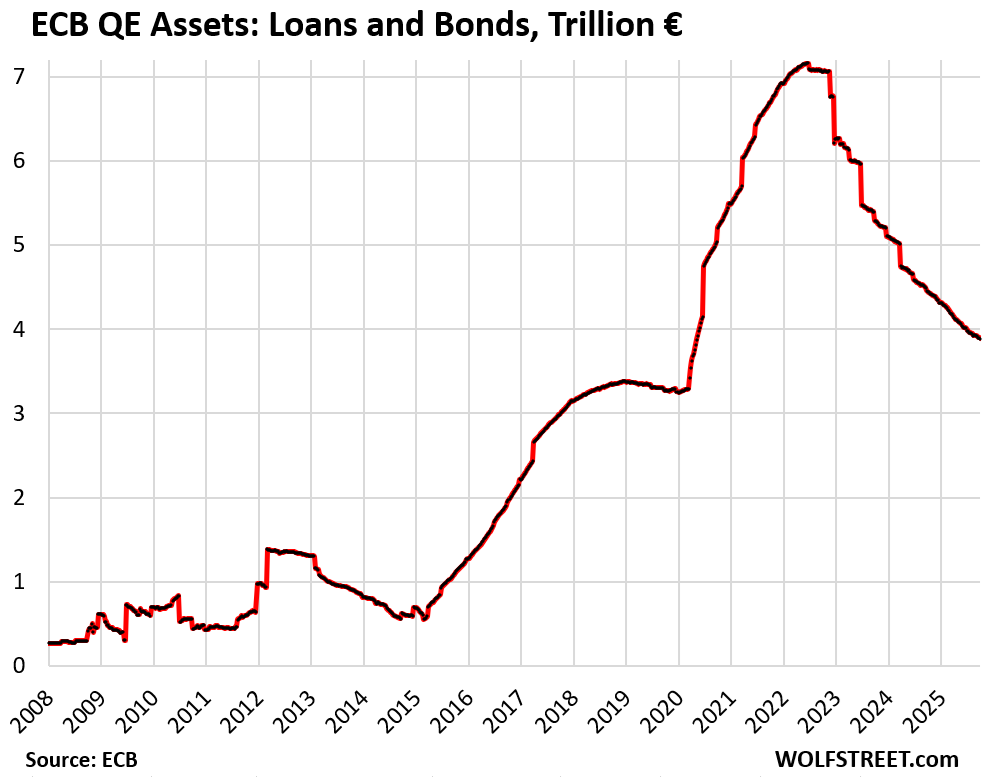

The ECB has now shed €3.28 trillion ($3.81 trillion) of its QE assets, per its balance sheet today – far more, about $1.5 trillion more, than the Fed’s QT of $2.38 trillion – and far more than anyone thought a central bank could ever shed when QT started. And the ECB’s QT continues at the pace that was accelerated for 2025.

The ECB had conducted QE via two methods: Large amounts of loans to the banks for them to plow into whatever; and large amounts of bond purchases, mostly government bonds, but also corporate bonds, mortgage bonds, and asset-backed securities. Between 2015, when its serious QE started, and peak-balance sheet in mid-2022, the ECB’s QE assets (these loans and bonds) had exploded by a factor of nearly 10, from €690 billion in 2015 to €7.16 trillion in mid-2022.

Then, in 2022 as inflation was raging, it flipped to QT, then accelerated QT in phases, accelerating it further for 2025, and now has shed €3.28 trillion, bringing its QE assets down to €3.89 trillion, from €7.16 trillion in June 2022. In other words, it has shed:

- 51% of the entire pile of QE assets added since QE started in 2015.

- 84% of the pile of QE assets added during the pandemic.

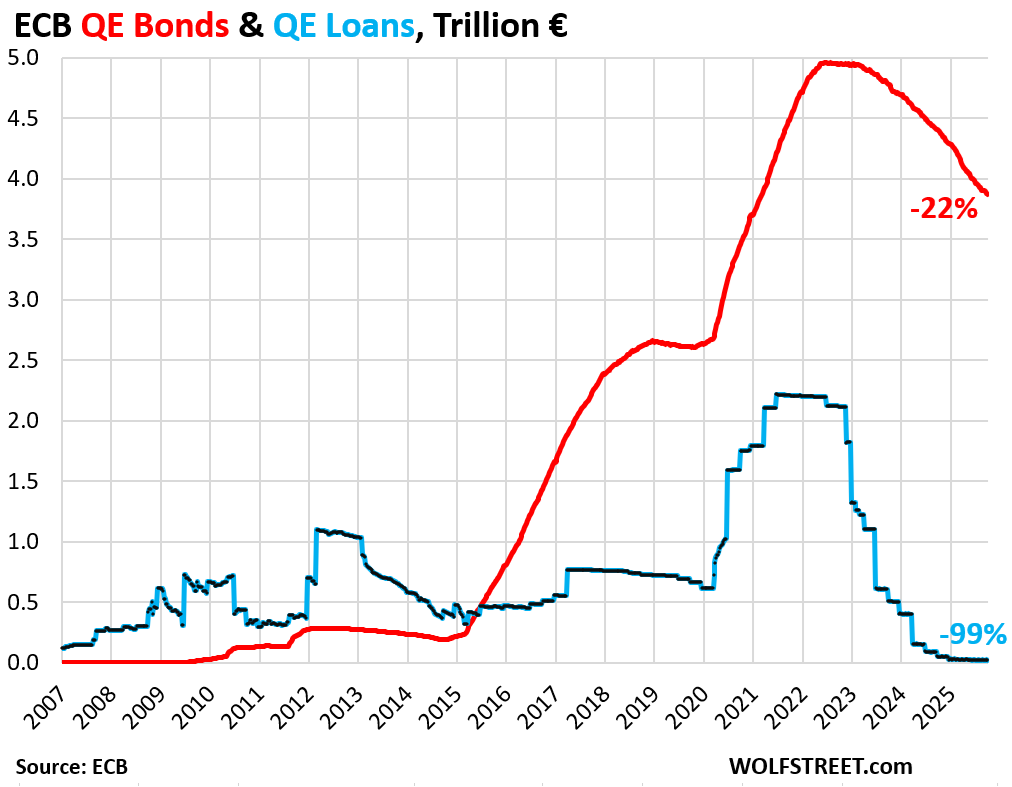

The two QE assets: Loans and bonds.

Loans to banks: nearly gone, -99%, to less than €20 billion, the lowest in the ECB’s data going back to 1999. The ECB started changing the terms of the loans in 2022, thereby making them less attractive, and the banks paid them back (blue in the chart below).

Bonds: -$37 billion in September, to €3.87 trillion.

Bonds come off the balance sheet as they mature. During the early phases of QT, the bond roll-off was limited by preset “caps.” The amount that matured above the caps was replaced with new purchases. But the last cap was removed effective at the start of this year. In some months, more bonds mature, in other months fewer bonds mature, but whatever matures comes off the balance sheet, and nothing is replaced.

In September, $37 billion in bonds matured and came off the balance sheet. On average, €47 billion a month matured and came off the balance sheet in 2025. Bond holdings have declined by 22% from the peak, to €3.87 trillion (red in the chart below).

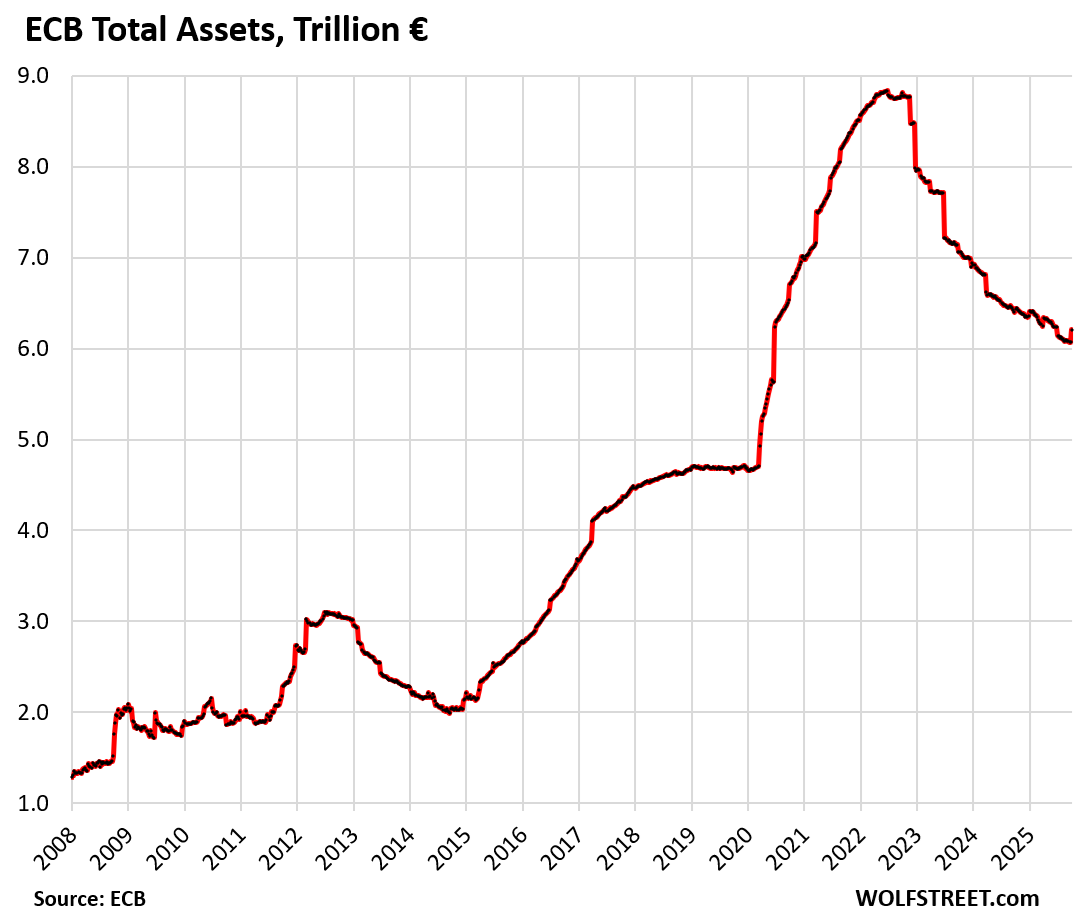

The ECB’s total assets.

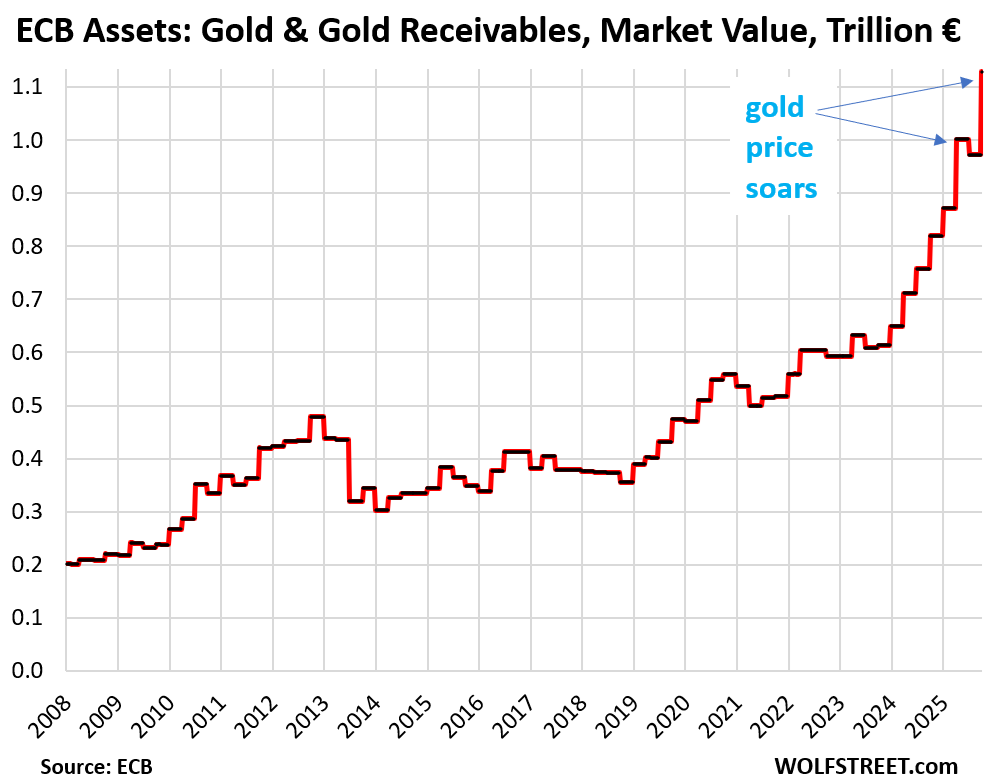

The ECB has other assets on its balance sheet, including over $1.1 trillion of gold valued at market value.

Gold holdings mark-to-market: +€156 billion in Q3, or +16%, to €1.128 trillion.

The ECB values its holdings of “gold and gold receivables” at market prices in euros. Every quarter, it adjusts its holdings to market value in euro terms. The balance sheet released today includes the quarterly mark-to-market adjustment of gold, and the price of gold spiked in Q3!

The ECB marked up its gold holdings by €156 billion on this balance sheet, to €1.128 trillion, the biggest mark-to-market increase ever, bigger even than in Q1. In Q2, the ECB had marked down its gold holdings.

Mark-to-market adjustments of its gold holdings are paper adjustments at the end of the quarter and do not involve purchases or sales of gold, or money printing, or QE or QT or whatever.

From mid-2019 through Q3 2025, the ECB wrote up its gold holdings by €726 billion (+180%), reflecting the surge of the price of gold in euros.

Total assets: This €156 billion quarterly mark-to-market adjustment of gold on the current balance sheet caused total assets to jump by €138 billion this week, to €6.21 trillion. That little hook at the end:

And in case you missed it: The ECB is way ahead of the Fed, which has shed $2.38 trillion under its QT program. But even the big straggler, Bank of Japan has accelerated its QT this year.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So which CB is doing it right? Is the US Fed a laggard, or is the ECB going too fast?

The ECB is doing fine.

The Fed slowed the Treasury QT down but didn’t slow down the MBS QT.

The Fed’s actual cap is $40 billion a month. But they would have to sell outright $15-20 billion a month in MBS to get there. They’ve been talking about it casually. $40 billion a month would be a decent pace.

Hey Wolf!

So why are the ECB and BOJ accelerating and the fed slowing down to an average trickle of 22 billion a month? Even the Bank of Canada just lets everything roll off once it matures with no cap. Are they afraid of something? Cheers

The BOC has stopped QT last year, after shedding a whole big pile fairly quickly.

I don’t think the Fed needed to slow down like this, especially since they have the Standing Repo Facility now that they didn’t have in Sep 2019 when issues in the repo market got out of hand.

The Fed’s actual cap is $40 billion a month. But they would have to sell outright $15-20 billion a month in MBS to get there. They’ve been talking about it casually. $40 billion a month would be a decent pace.

But I can kind of see why they slowed the Treasury QT down (they didn’t slow down the MBS QT):

Given the dollar’s global role, the Fed has a global responsibility. Withdrawing large amounts of liquidity fast is risky. And the Fed doesn’t want a liquidity problem somewhere à la Sep 2019 to get out of hand. So they decided to go slowly.

It was a little easier for the ECB to shed its loans; all it had to do was make them less attractive, and banks paid them back when they were ready. It was up to the banks to deal with liquidity issues. And that’s what banks do in the normal course of their daily operations. Now the ECB is shedding bonds at a good clip. But it too has repo facilities to deal with liquidity issues if they crop up.

Covid was the greatest global looting and plundering operation since the great depression, it only took the money masters 16 years to cause the great depression…9,000 banks failed…millions wiped out, their cronies did very well…these cretins never go away, recycle their tired scripts…the world deserved better…everyone takes their dirty money….

Hi Wolf, thanks for these articles. Are you able to do the same for the RBA (Australia)?

Michael

I haven’t even tried. I can do and used to do the BOC and the BOE but stopped because relatively few people read those articles. So I just look at them on my own.

The ECB is doing great but there is still a lot of money in the system. Real estate prices in many countries have fallen but are still far from a reasonable decline to affordable levels.

In Central and Eastern Europe, prices are only going up