This is going to take a long time to get worked out.

By Wolf Richter for WOLF STREET.

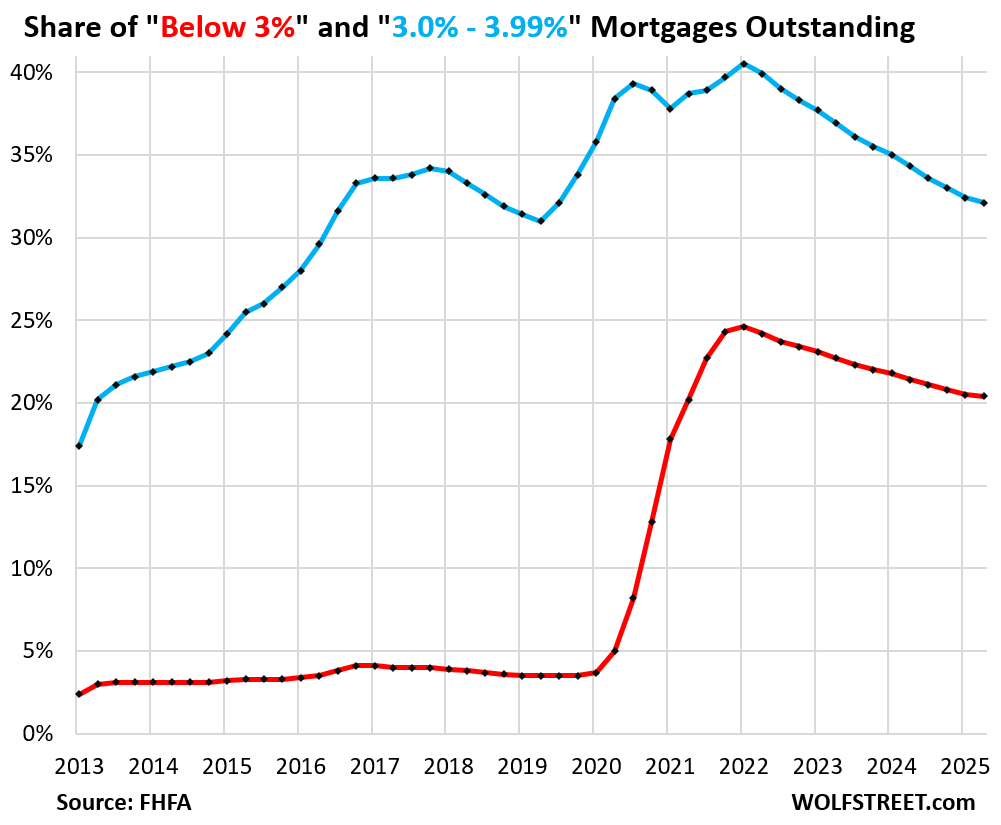

The share of below-3% mortgages outstanding declined in Q2 to 20.4% of all mortgages outstanding, the smallest share since Q2 2021 (red in the chart), according to data by the Federal Housing Finance Agency. The share has been shrinking since the peak in Q1 2022, but the pace has been very slow: Just 4.2 percentage points in three years. The shrinking share of these ultra-low-rate mortgages documents the slow exit of homeowners and investors from the “lock-in effect.”

The share of 3%-3.99% mortgages declined by 30 basis points to 32.1%, the smallest share since Q3 2019 (blue).

When these ultra-low mortgage rates came along in early 2020, they triggered a tsunami of refinancing, and the number of these outstanding low-rate mortgages exploded through Q1 2022, when 65% of all mortgages outstanding had interest rates of 3.99% or below:

All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.

These below 3%-mortgages are free money in real terms because inflation is currently running at about 3% and accelerating, and if borrowing costs run at the rate of inflation or below, it equates to getting free money.

These mortgages were a result of the Fed’s reckless monetary policies that caused home prices to explode in many markets by 50% and much more in just two years, and those too-high home prices and ultra-low mortgage rates have now locked up the housing market for three years.

These homeowners have been altering the course of their lives by avoiding to move, or by not being able to afford to move, which would require losing an ultra-low mortgage and buying the next home at a price that had exploded by 50% or more in a couple of years to an absurd level, and then financing this absurd price at a historically normal rate.

But life happens: career-moves, divorces, deaths, family additions, etc., and so a small number of those mortgages get paid off every quarter anyway, and their share shrinks slowly. It will take years to get this worked out.

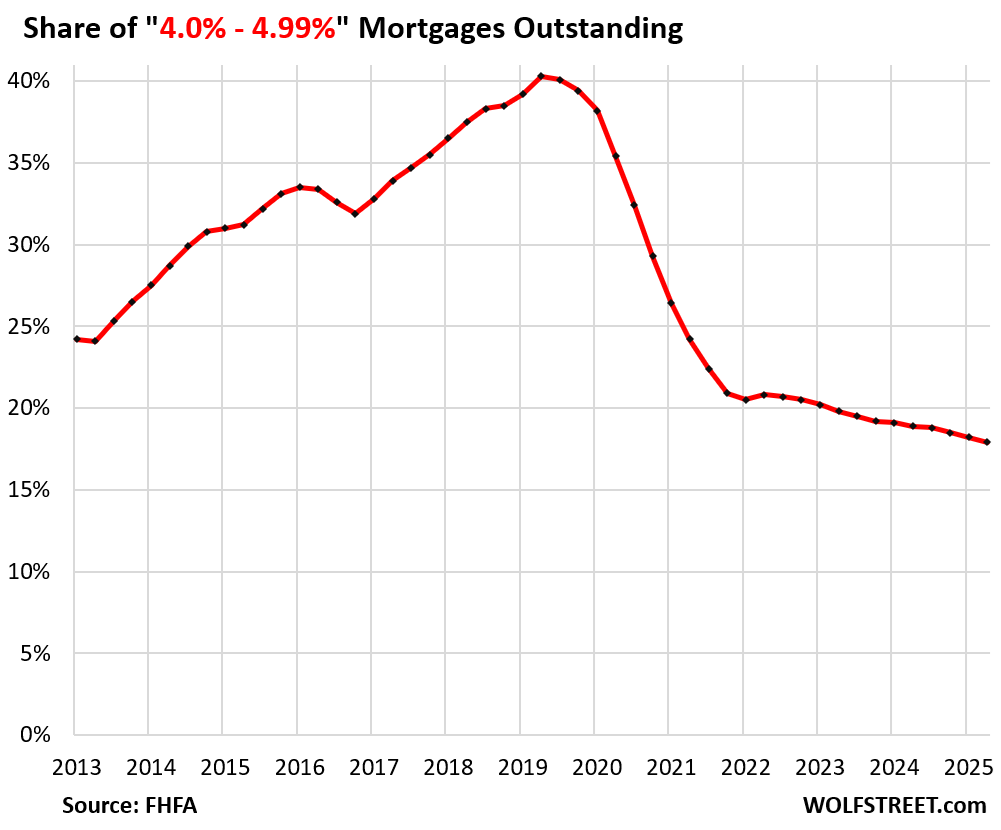

The share of 4.0% to 4.99% mortgages declined to 17.9%, the lowest share in the FHFA’s data going back to 2013, and down from the peak in 2019 of 40%.

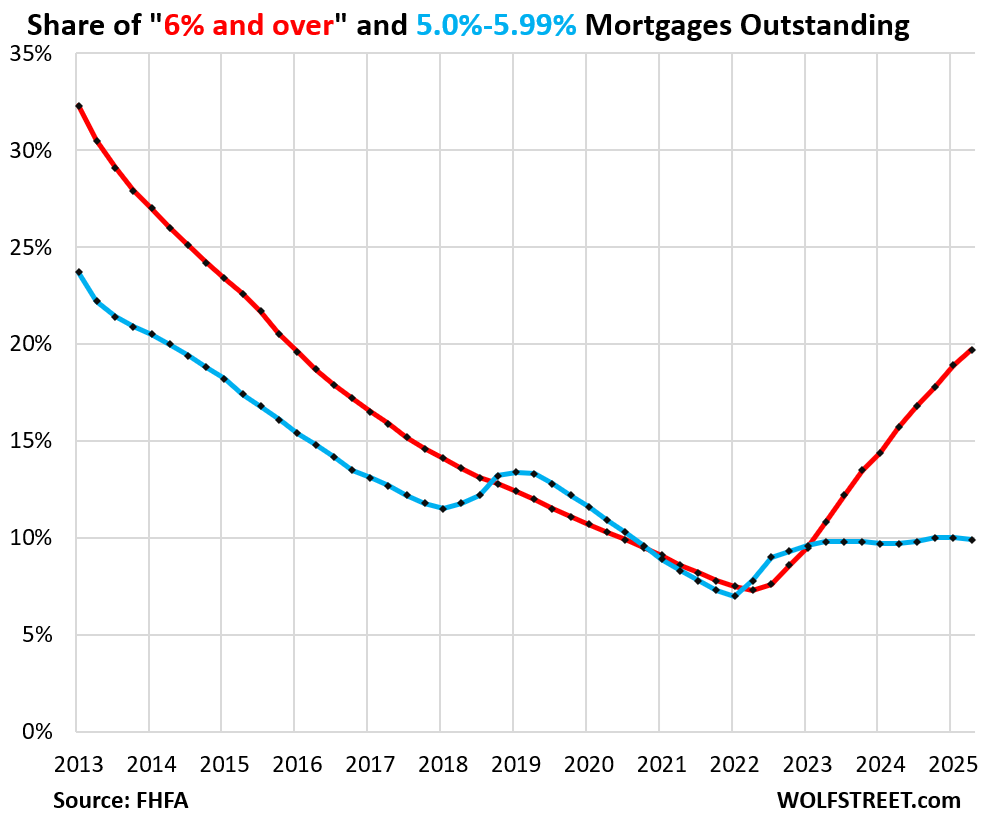

Conversely, the share of 6%-plus mortgages rose 19.7% of all mortgages in Q2, the highest since Q4 2015, up from a share of 7.3% at the low point in Q2 2022 (red in the chart below).

The increase is so slow because home sales have plunged and refinancings have collapsed, and so demand for mortgages has plunged, and a much smaller number of mortgages are being originated.

The share of 5.0% to 5.99% mortgages has remained roughly stable over the past two years, around the 10%-line. In Q2, the share was 9.9% of all mortgages outstanding (blue).

There are currently fixed-rate mortgages offered in this range. For example, the interest rate of the average conforming 15-year mortgage was 5.49% in the latest week, according to Freddie Mac. The Navy Federal Credit Union, for example, quotes 30-year-fixed VA loan rates “as low as” 5.375%.

So new mortgages in that rate bracket are currently being originated at about the same pace as old mortgages are being paid off.

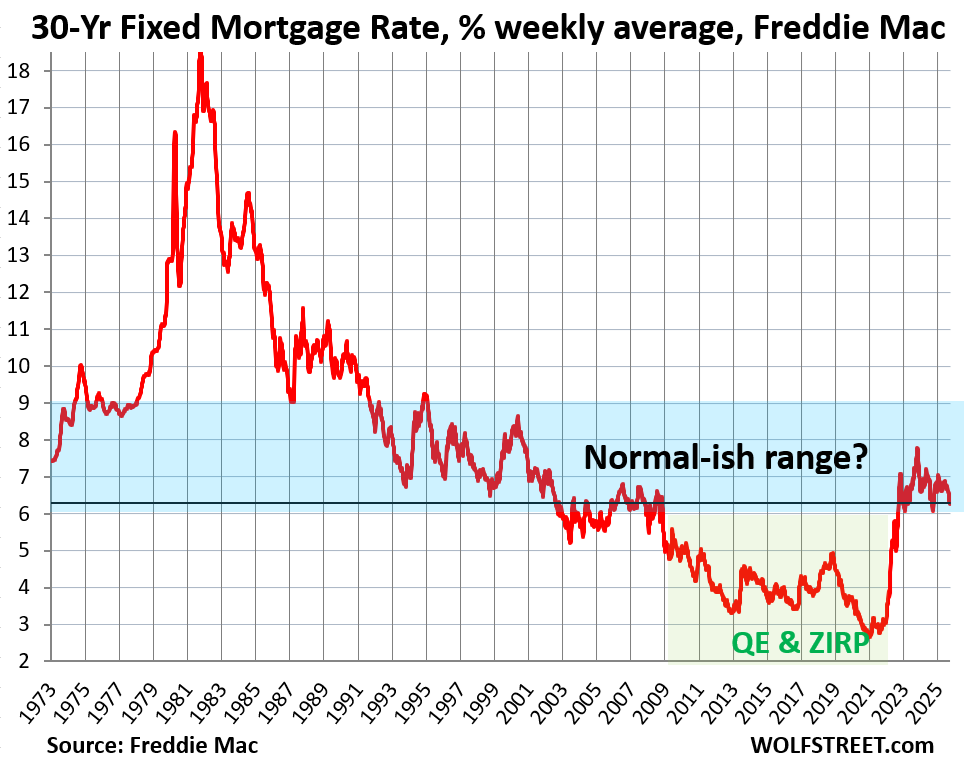

The below-5% average 30-year fixed mortgage was a creature of the Fed’s QE. They didn’t exist until the Fed started buying trillions of dollars of securities, including Mortgage-Backed Securities, starting at the beginning of 2009, and then massively in 2020 through early 2022, which produced the below-3% mortgages.

But since mid-2022, the Fed has been attempting to tamp down on some of the damage – the historic home price explosion and the surge of consumer price inflation – with its QT. By now it has shed $2.36 trillion in assets, and that continues.

The ultra-low-rate mortgages were a brief phenomenon in historical terms – though people now believe that they were normal, and that the current rates are too high. What’s too high are home prices, not mortgage rates.

The data from the FHFA on the share of mortgages by rates goes back to only 2013, and only reflects the era when QE had already repressed mortgage rates.

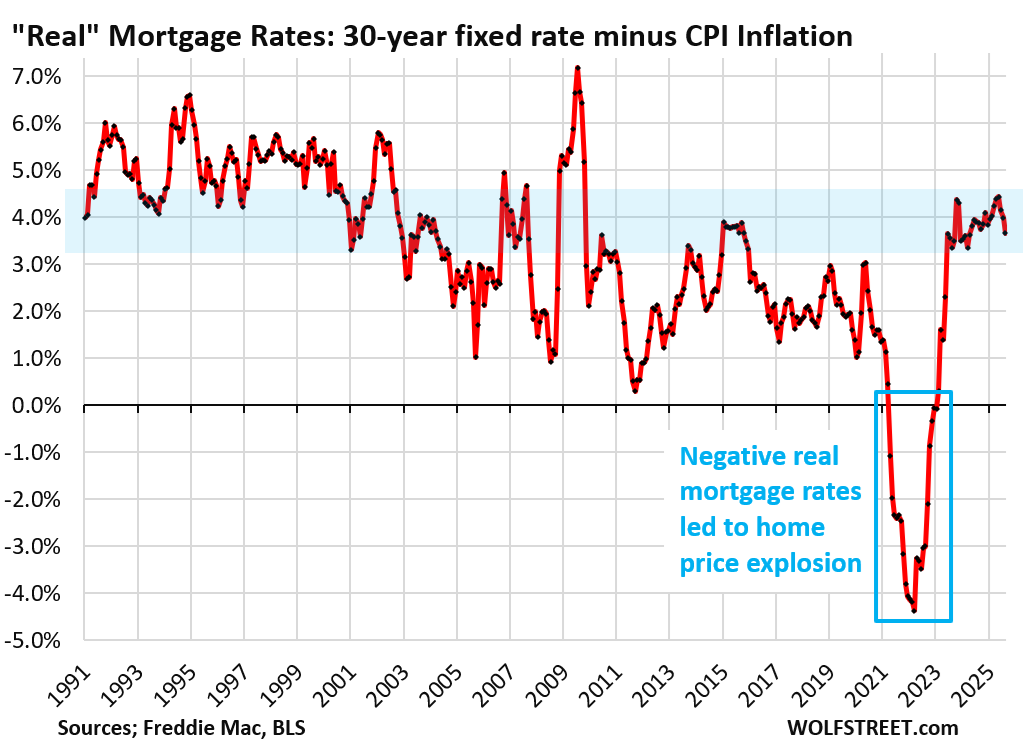

Just how crazy were those ultra-low mortgage rates? Between early 2021 through 2022, the average 30-year fixed mortgage rate was below CPI inflation – meaning negative “real” mortgage rates, better than free money!

At the peak of this craziness, “real” mortgage rates were 4 percentage points below CPI, with mortgage rates below 3% and CPI inflation exceeding 7%. Those were the craziest times ever in the mortgage market, and they wrecked the housing market through a historic home price explosion (now being unwound in many markets) and then the lock-in effect.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The real estate brokers just loved those low rates….

and now the market is broken and they are dead in the water.

People can not move when the have to or want to, people cant sell.

More great work by the Fed, interrupting free markets, skewing reality, then sitting back and pretending they had nothing to do with it.

3rd unmentioned mandate….”moderate long term interest rates”….

and driving down long rates to 4000 yr lows is “immoderate” by any metric. File this with the “stable prices” violation.

So the Fed violates TWO of their three mandates…….and not a word from Congress who allegedly oversees them.

But their friends made out big time.

Yup.

They used to try and hide it but now it is out in the open. It is one big grift for the elite to enrich themselves and everyone else gets to suffer.

“These mortgages were a result of the Fed’s reckless monetary policies that caused home prices to explode in many markets by 50% and much more in just two years, and those too-high home prices and ultra-low mortgage rates have now locked up the housing market for three years.”

I agree.

This is true.

Live in a neighborhood of twenty homes where say 50 to 60% likely have 3% loans ( I am a 3.34%).

Given inflation these people wont move unless forced. People here have been for 5 to 40 years wit last two forced sales in 2022.

Of course the lucky ones that pay cash have one huge hurdle avoided that the everyday people have too navigate. Without being aware of their loving aura.

The real estate market is moribund because no one can afford the payment at 6 % asking price set at the low of the mortgage rates.

I agree with you on your statement that “What’s too high are home prices, not mortgage rates”. Before the Updraft for homes, there was a reasonable market for New entry for first time buyers, Moving up for the second time buyer, and let’s go wild and get a 97.5% mortgage because Daddy or Mommy got a raise. Now there is No Entry Level Scale, those that were thinking of remodeling or moving up have pulled the plug on their plans. And those that went kind of nutty overbidding everyone for the fancy new homestead are selling all of their toys. Like Travel Trailers, Off Road Racers, Lavish get away vacations, and still can’t meet their obligations for HOA fees for the Condo, or HO Insurance with an ever increasing deductible because they need all the little savings that they can find. And the Credit Card debt keeps pilling up. But what amazes me is seeing a family of 4 eating in a restaurant that is going to cost at least $40.00 a person. I am on a Retirement Income that is basically fixed. So I do a lot of cooking at home. But they pack the restaurants every night.

You are going to have to scrape these sub 3% mortgage holders off the walls to get them to unload these homes. Even after they pass, look for their next of kin to keep the homes in their newly created family estate forever. I heard that estate attorneys are doing a record amount of conversions to family estates to preserve this low financing. They will just rent it out if they have to and live like a king somewhere else. This is one of J Powell’s legacies that he left us with for the next 25 years or more. Thanks but NO thanks!

Prop 19 in California will prevent this at least in that state (even if in a trust) unless one of the heirs actually lives there as their primary residence. Otherwise the house value and taxes are reassessed at market rates, and the property taxes will swamp any mortgage savings.

Frankenstein’s monster was actually named Three Percent Mortgage. What few friends he had called him “TPM”, or sometimes “TP” for short. He had a difficult life and a bad ending.

Wonder if Congress might eventually force these low mortgage rates to be re-adjusted to market rates (~7%) or the mortgages won’t be guaranteed by the government.

That would force change in a hurry.

What? As in existing mortgages going up?

No. The markets will do that over time.

What Congress should do is allow current home owners to buy back the underlying “bond” held against their mortgage. Your mortgage exists as a repackaged security others can buy and sell. And guess what, this security has greatly dropped in price as it yields 6.5 percent now instead of 2.5 percent.

This allows u to close out your mortgage for a much lower sum than the balance printed on your statement.

This process would make manifest the “free money” aspect of these mortgages and allow owners to book the profits of their current low rate mortgage in the present, rather than over years, and move to a different house if they choose.

Crazy? No. This is how bonds, which your mortgage essentially is, work.

Sure, if they wanted to guarantee losing their next election, this is a surefire way to do that.

“The shrinking share of these ultra-low-rate mortgages documents the slow exit of homeowners and investors from the “lock-in effect.” In this Great Housing Abomination, there is a lock-in-effect, which is akin to a seat belt, intended to have some safety benefit. When this GHB bursts, the number of homeowners pulling the ejection lever will be frightening. It’s more of a lifesaving/ crash-imminent measure.

In response to that very last graph -Negative real mortgage rates lead to home price explosion” – HOT JAMBALAYA! Here we are. How’d we get here?!

Lastly – “These below 3%-mortgages are free money in real terms because inflation is currently running at about 3% and accelerating, and if borrowing costs run at the rate of inflation or below, it equates to getting free money.”

So, when I deposit money into a money market at 3% or more, the BANK is the LUCKY ONE getting the FREE MONEY.

I’ve finally got that conundrum figured out.

This part is interesting:

“All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.”

Some of the negative slope of the 3.99% and below chart lines are presumably the 5/1 ARM borrowers timing out of their lottery-winning rates after they, well, “adjust”. That’s probably not a big number (why would you only take free money for 5 years instead of 30?) but it’s not zero.

The question in my mind is what proportion of the huge up-slope around 2021 in the sub-3% mortgages were 5/1 ARMs. Because those people are about to have a very interesting 2026.

Never mind. It doesn’t look like there’s going to be ARM pain in 2026.

perplexity.ai: “Produce time-series data year by year between 2009 and 2025 of proportion of new U.S. mortgages that were five-year ARMs.”

Year | Estimated % of New Mortgages (5/1 ARMs)

——+—————————————–

2009 | ~8%

2010 | ~8%

2011 | ~6%

2012 | ~6%

2013 | ~7%

2014 | ~7%

2015 | ~6%

2016 | ~6%

2017 | ~5%

2018 | ~7%

2019 | ~5%

2020 | ~5%

2021 | ~4%

2022 | ~9%

2023 | ~10–14%

2024 | ~6–7%

2025 | ~6%

But 2027 is looking to take out a chunk of the spike in four-percenters from 2022.

perplexity.ai: “Produce time-series data year by year between 2015 and 2025 of the average rate for a 5/1 ARM.”

Year | Average Rate (%)

——+——————

2015 | 2.98

2016 | 2.92

2017 | 3.09

2018 | 3.81

2019 | 3.45

2020 | 3.27

2021 | 2.61

2022 | 4.09

2023 | 6.18

2024 | 6.80

2025 | 7.11

I have a 7 yr arm

2.5

caps at 6.5

right now at 4% the fed is paying my mortgage. At EOY 7 my payoff is 130k+ from what I borrowed because of principal pay down

So someone lent me $$$ and the Fed gov’t paid me over $130,000 to stay 7 years in the mortgage….that’s based on the 2 mo bill staying above 3.75%. I’ll take over 20k a year tax free to add to my retirement.

If bills rise sharply then I’ll let it ride

Howdy Folks. WOW, that sure is STILL a large number of prisoners….

Terrific analysis as always, Wolf.

My very limited anecdotal evidence strongly supports the thesis that the homeowners with these ultra low rates will do absolutely everything they can to keep them. I wonder if, given the scale, this increases the fragility of the housing market.

I know a handful of Gen Xers who did cash out refis to under 3%, then took that massive cash pile and plowed it into Airbnbs. They have been living well, not many worries.

The US needs to delete all subsidies.

Just take all the hundreds of thousands of pages of laws designed to distort markets for some social objective and hit the delete key.

My Google friend says: Home refinancing during the “mid-2020 to mid-2022” period involved a significant amount of money, with estimates suggesting around $5.4 trillion in first-lien refinance originations during this timeframe, driven by historically low interest rates following the pandemic’s onset.

If my friend is totally wrong, I’m sorry — I was just curious about what kinds cash traded hands, which might explain something…

Refinancing a mortgage, unless it’s a cash-out refi, is zero-sum. The homeowner ends up with the same amount of debt, but a different lower-interest rate mortgage. Lenders of the original mortgage get the remaining principal back, paid for by the lenders of the new mortgage. And a lot of times, those lenders were the same. So the aggregate mortgage balance remains the same, but the average rate is lower.

Only cash-out refis add to the aggregate mortgage balance.

Well, and of course, fees are being extracted everywhere along the way, and some of those fees get rolled into the new mortgage as points that the homeowner pays.