This is going to take a long time to get worked out.

By Wolf Richter for WOLF STREET.

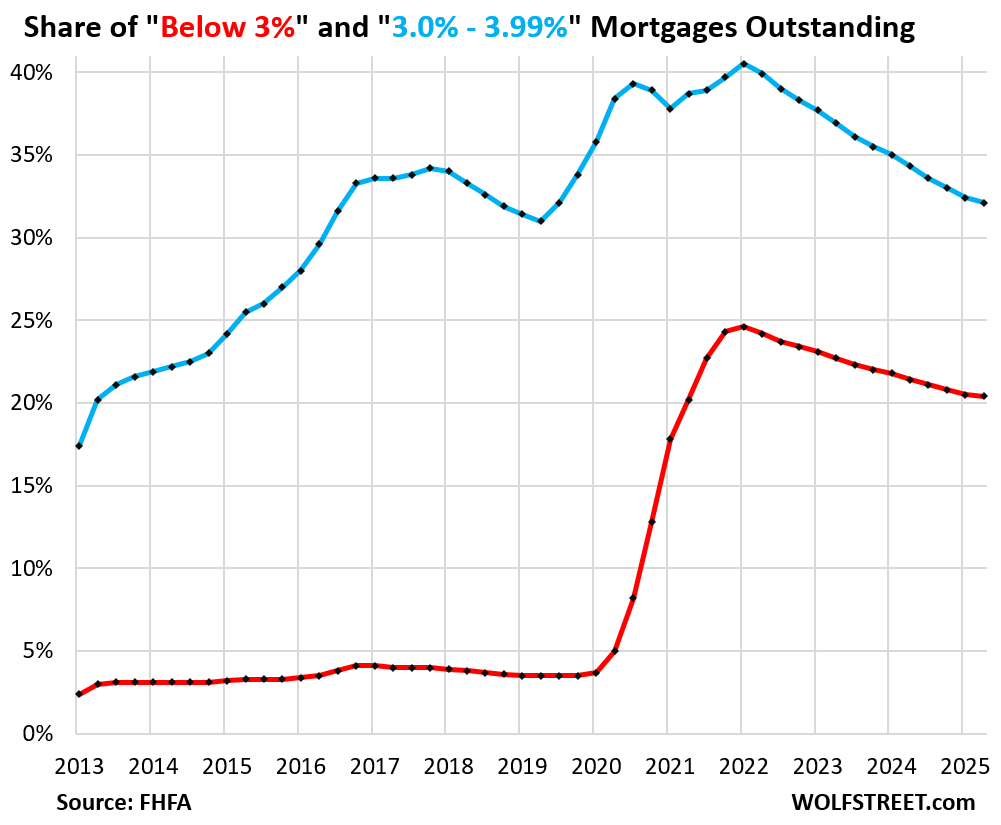

The share of below-3% mortgages outstanding declined in Q2 to 20.4% of all mortgages outstanding, the smallest share since Q2 2021 (red in the chart), according to data by the Federal Housing Finance Agency. The share has been shrinking since the peak in Q1 2022, but the pace has been very slow: Just 4.2 percentage points in three years. The shrinking share of these ultra-low-rate mortgages documents the slow exit of homeowners and investors from the “lock-in effect.”

The share of 3%-3.99% mortgages declined by 30 basis points to 32.1%, the smallest share since Q3 2019 (blue).

When these ultra-low mortgage rates came along in early 2020, they triggered a tsunami of refinancing, and the number of these outstanding low-rate mortgages exploded through Q1 2022, when 65% of all mortgages outstanding had interest rates of 3.99% or below:

All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.

These below 3%-mortgages are free money in real terms because inflation is currently running at about 3% and accelerating, and if borrowing costs run at the rate of inflation or below, it equates to getting free money.

These mortgages were a result of the Fed’s reckless monetary policies that caused home prices to explode in many markets by 50% and much more in just two years, and those too-high home prices and ultra-low mortgage rates have now locked up the housing market for three years.

These homeowners have been altering the course of their lives by avoiding to move, or by not being able to afford to move, which would require losing an ultra-low mortgage and buying the next home at a price that had exploded by 50% or more in a couple of years to an absurd level, and then financing this absurd price at a historically normal rate.

But life happens: career-moves, divorces, deaths, family additions, etc., and so a small number of those mortgages get paid off every quarter anyway, and their share shrinks slowly. It will take years to get this worked out.

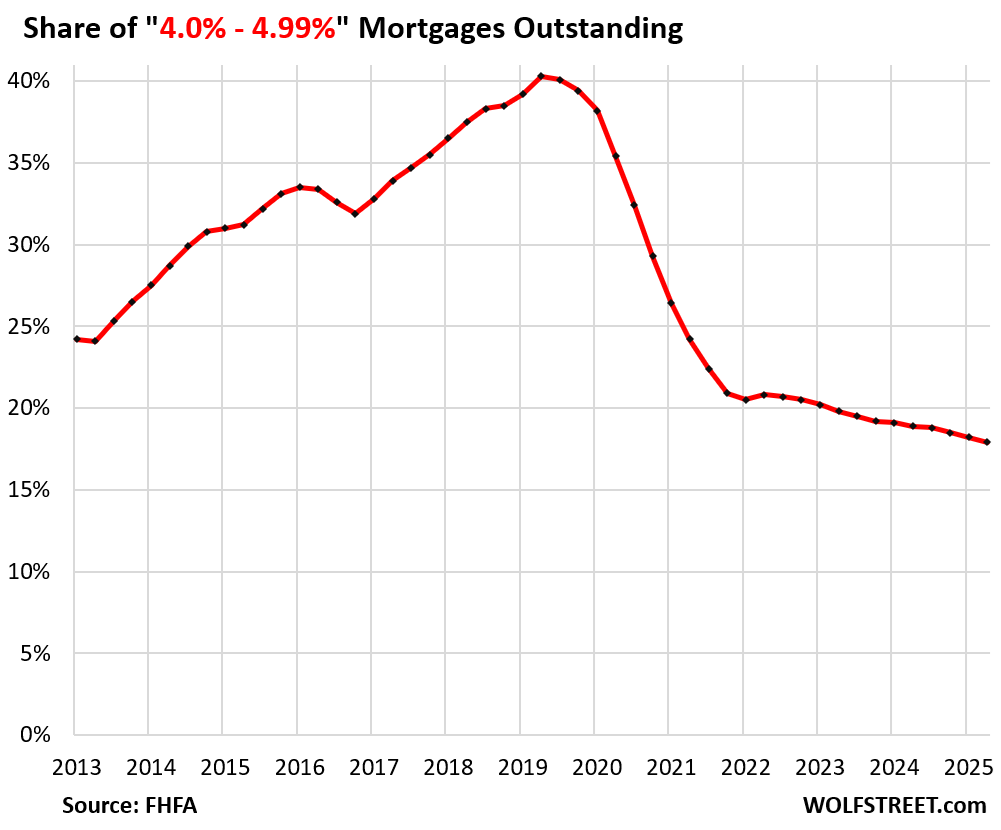

The share of 4.0% to 4.99% mortgages declined to 17.9%, the lowest share in the FHFA’s data going back to 2013, and down from the peak in 2019 of 40%.

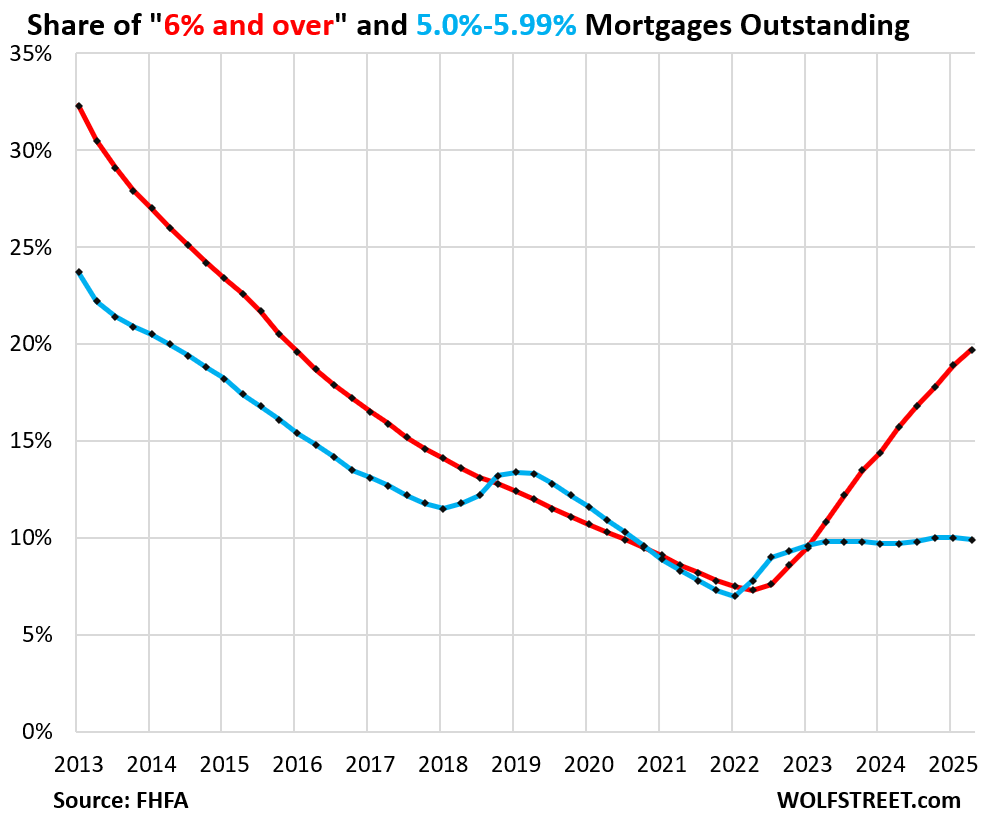

Conversely, the share of 6%-plus mortgages rose 19.7% of all mortgages in Q2, the highest since Q4 2015, up from a share of 7.3% at the low point in Q2 2022 (red in the chart below).

The increase is so slow because home sales have plunged and refinancings have collapsed, and so demand for mortgages has plunged, and a much smaller number of mortgages are being originated.

The share of 5.0% to 5.99% mortgages has remained roughly stable over the past two years, around the 10%-line. In Q2, the share was 9.9% of all mortgages outstanding (blue).

There are currently fixed-rate mortgages offered in this range. For example, the interest rate of the average conforming 15-year mortgage was 5.49% in the latest week, according to Freddie Mac. The Navy Federal Credit Union, for example, quotes 30-year-fixed VA loan rates “as low as” 5.375%.

So new mortgages in that rate bracket are currently being originated at about the same pace as old mortgages are being paid off.

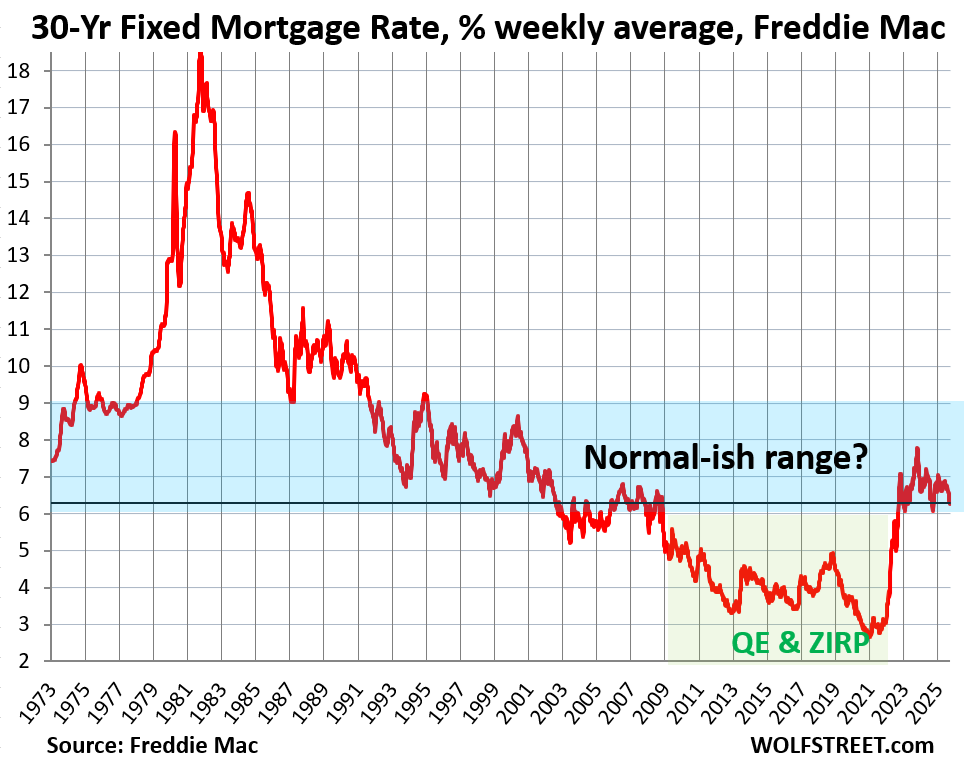

The below-5% average 30-year fixed mortgage was a creature of the Fed’s QE. They didn’t exist until the Fed started buying trillions of dollars of securities, including Mortgage-Backed Securities, starting at the beginning of 2009, and then massively in 2020 through early 2022, which produced the below-3% mortgages.

But since mid-2022, the Fed has been attempting to tamp down on some of the damage – the historic home price explosion and the surge of consumer price inflation – with its QT. By now it has shed $2.36 trillion in assets, and that continues.

The ultra-low-rate mortgages were a brief phenomenon in historical terms – though people now believe that they were normal, and that the current rates are too high. What’s too high are home prices, not mortgage rates.

The data from the FHFA on the share of mortgages by rates goes back to only 2013, and only reflects the era when QE had already repressed mortgage rates.

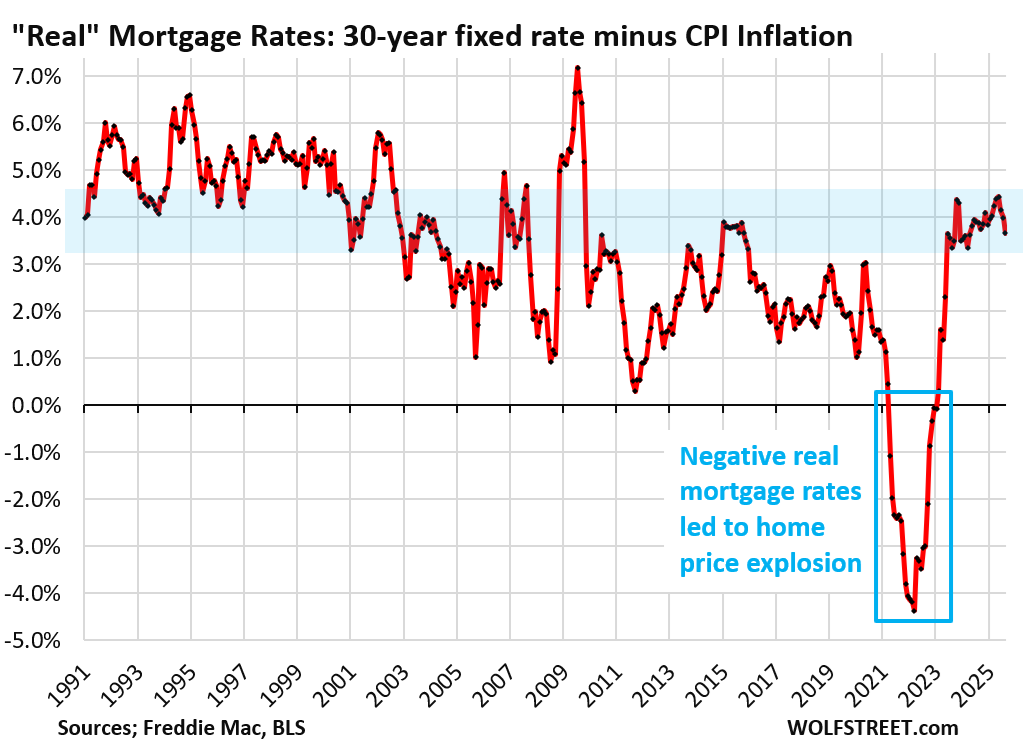

Just how crazy were those ultra-low mortgage rates? Between early 2021 through 2022, the average 30-year fixed mortgage rate was below CPI inflation – meaning negative “real” mortgage rates, better than free money!

At the peak of this craziness, “real” mortgage rates were 4 percentage points below CPI, with mortgage rates below 3% and CPI inflation exceeding 7%. Those were the craziest times ever in the mortgage market, and they wrecked the housing market through a historic home price explosion (now being unwound in many markets) and then the lock-in effect.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The real estate brokers just loved those low rates….

and now the market is broken and they are dead in the water.

People can not move when the have to or want to, people cant sell.

More great work by the Fed, interrupting free markets, skewing reality, then sitting back and pretending they had nothing to do with it.

3rd unmentioned mandate….”moderate long term interest rates”….

and driving down long rates to 4000 yr lows is “immoderate” by any metric. File this with the “stable prices” violation.

So the Fed violates TWO of their three mandates…….and not a word from Congress who allegedly oversees them.

But their friends made out big time.

Yup.

They used to try and hide it but now it is out in the open. It is one big grift for the elite to enrich themselves and everyone else gets to suffer.

my 3.35% 15 will pay itself off in just over 10 years

no hurry

it’ll make good rental soon enough

only owned for 23 years so far

I’m confused by your comment. Are you saying ONLY ELITE, as in top 1%, benefited from low mortgage rates? That everyone else is suffering?? I think MANY people benefited from low mortgage rates, and continue to do so….look at the charts.

I have benefited! I added one small data point to the 3-3.99% in 2016.

I would have been forced to move due to unaffordable rent otherwise.

Since then? I (not so- jokingly) say: I can’t afford to move!

I’m in a position where if I sold, my housing cost would likely go up, for a worse neighborhood (I am “trapped in paradise.”). This was partially true before the price explosion and is absolutely true today.

“These mortgages were a result of the Fed’s reckless monetary policies that caused home prices to explode in many markets by 50% and much more in just two years, and those too-high home prices and ultra-low mortgage rates have now locked up the housing market for three years.”

I agree.

Two ideas to think about. It is my understanding that most countries do not have 30 year fixed rates. U S has them because of Congress legislation to subsidize home ownership via creating Freddie, Fannie, etc. Wonder if Wolf has an opinion on whether societies benefits of 40 year fixed rates exceed the damages thereof in the big picture?

I think an individual homeowner with low rate mortgage could call the mortgage servicing company and negotiate to pay off the mortgage early for a huge discount. The servicer would just run present value calculations to determine mathematically the value, and then adjust for likelihood the homeowner will sell or otherwise trigger the payoff. They would negotiate to fair for both sides and the mortgage goes away. Free up the home and housing market. Keep Congress and the government out of this process. They will screw it up.

Countrybanker – In the ideal world. I have tried that in the past with my mortgage holders. They refuse to adjust a standing loan. So, I’d end up spending the money to refinance at a lower rate a lot of times ending up with the same company.

The middleman needs to be PAID!!!

Many countries also have loans that require a substantial down payment and are no longer than 10 years total. US financials are kept in business by interest payments, and they have incentive to extend the length of the loan to increase the amount of interest paid out, because they expect people to move before the loan is paid off and not pay down the principal.

The problem with longer fixed rates is that it supports price increases. Car loans are a great example. You can afford a more expensive car if you can stretch the payments out for six years. A 30 year fixed product makes sense if you are going to stay in the house, pay it off, and live there in retirement. This isn’t the way the average family lives today, so the 30 year fixed only supports higher prices.

I think a lot of people are getting the “lock-in” thing wrong. People are locked in because of prices, not rates. We’re moving and don’t care that we’re giving up our beloved below 3% rate. What we’re peeved about is that we’re dropping a thousand square feet of house to downsize at nearly the same cost as our larger house. Madness. We’ll rent for a few years while sellers come to accept reality.

Seems like a good idea in theory. But from the lenders standpoint, that proposal turns an unrealized loss into a realized loss. Probably not good for their financial reporting.

If the loan is current, do banks even have to report an unrealized loss on a below-market rate loan. If not, it’s another reason to keep the below market rate loan on the books. Warning, I’m not a bank industry financial accountant.

Countrybanker, Russel: the reason existing mortgages can’t be adjusted is these days mortgages are sold, bundled, traunched and securitized often within 60 days of origination. It really doesn’t even exist as an individual loan at that point. The servicer has no ability to negotiate beyond the original terms.

Ross – You still end up with a single promissory note between a single borrower and a single carrying entity. Whether their policy prevents the occurrence or banking laws, there is nothing preventing the two groups from agreeing on a rate that is more acceptable to both parties without the need to refinance.

In this case, the 2020-22 vintage sub 3.5% mortgages, the lender is the Federal Reserve.

Borrowers must deal with the servicing “bank” who has less than zero incentive to see the loan paid off. They are paid a service fee.

“Fed’s reckless monetary policies ”

Your being much too kind.

The Federal Reserve is a pyromanaic burning down our economy for the benefit of a small group on Wall street.

The youth can’t afford a house, a car, a vacation, babies, marriage, or groceries.

I fear for my kids future.

I agree with you. But what’s missing in the whole discussion: Who is responsible for this? Yes, everyone says it’s the FED, but it’s not the FED, it’s politics. At some point, someone decided that there has to be an institution like this, the FED. And this institution has existed for almost 100 years now. The discussion should be: Do we need the FED? And I say, we don’t need a central bank. Let the market sort it out.

I think you should do a bit of research into the history of the fed and why it came to be. The market created a very dangerous situation that resulted in the formation of the fed, not the other way around. Those who refuse to learn from history are doomed to repeat it.

In the US, the central bank was created, because after a bust cycle (Panic of 1907), John P. Morgan had to bail out many banks, so that a single private banker could dictate the terms of other banks’ survival. Many Americans and politicians were left sickened by the power of one man. This showed the advantage of an independent central bank – the 3rd one in the US. The US had to learn this mistake 3 times and still you hear demagogues saying there is no need of a central bank. It’s just unfortunate the errors the Fed have committed since 2008 as this article illustrates

“More great work by the Fed, interrupting free markets, skewing reality, then sitting back and pretending they had nothing to do with it.”

Well that sums it up quite nicely . Thanks to JustAsking !

This is true.

Live in a neighborhood of twenty homes where say 50 to 60% likely have 3% loans ( I am a 3.34%).

Given inflation these people wont move unless forced. People here have been for 5 to 40 years wit last two forced sales in 2022.

Of course the lucky ones that pay cash have one huge hurdle avoided that the everyday people have too navigate. Without being aware of their loving aura.

The real estate market is moribund because no one can afford the payment at 6 % asking price set at the low of the mortgage rates.

I agree with you on your statement that “What’s too high are home prices, not mortgage rates”. Before the Updraft for homes, there was a reasonable market for New entry for first time buyers, Moving up for the second time buyer, and let’s go wild and get a 97.5% mortgage because Daddy or Mommy got a raise. Now there is No Entry Level Scale, those that were thinking of remodeling or moving up have pulled the plug on their plans. And those that went kind of nutty overbidding everyone for the fancy new homestead are selling all of their toys. Like Travel Trailers, Off Road Racers, Lavish get away vacations, and still can’t meet their obligations for HOA fees for the Condo, or HO Insurance with an ever increasing deductible because they need all the little savings that they can find. And the Credit Card debt keeps pilling up. But what amazes me is seeing a family of 4 eating in a restaurant that is going to cost at least $40.00 a person. I am on a Retirement Income that is basically fixed. So I do a lot of cooking at home. But they pack the restaurants every night.

A family of four at a restaurant is nearing the prime of its earning potential and can afford it. If you’re retired, as you are, the days of splurging are over. The prime earning years are from 38 to 50, when we’re most productive. Our young families have grown into adolescents by then. They demand the most social investments as they mature into working adults of their own. It is a bonding experience to go out to a restaurant with your relatives and something at least a little special. We should not begrudge them this.

You are going to have to scrape these sub 3% mortgage holders off the walls to get them to unload these homes. Even after they pass, look for their next of kin to keep the homes in their newly created family estate forever. I heard that estate attorneys are doing a record amount of conversions to family estates to preserve this low financing. They will just rent it out if they have to and live like a king somewhere else. This is one of J Powell’s legacies that he left us with for the next 25 years or more. Thanks but NO thanks!

Prop 19 in California will prevent this at least in that state (even if in a trust) unless one of the heirs actually lives there as their primary residence. Otherwise the house value and taxes are reassessed at market rates, and the property taxes will swamp any mortgage savings.

Correct. Primary residences cannot be turned into rental properties without losing the tax benefits of them being primary residences.

I was able to retire because of and during the free money orgy by cashing out and I see the youtube demographers claiming that ten thousand people per day are now exiting that system. While not all boomers own mortgages, this activity will exacerbate the housing glut ( if you have been gaslighted into the housing shortage beliefs, please disregard this comment) that is now set to pop the housing bubble. I’ve been staying in empty houses (there are now likely tens of millions) every year when in the USA for the past 3 years and notice AI increasing access to this stock as the retail rental industry continues to operate in the extend and pretend mode. The question is how long extend and pretend can continue as virulent populism takes over the political system. If they extend the free money orgy, another year or two inflation will spike out of control, largely resorting to a wartime economy of supply disruptions which have been rather unpleasant and diminished the quality of life in the USA since 2020. China is a few years ahead in the cycle and might provide a glimpse of our future. Japan is a decade or two ahead and has cultural characteristics that allows for very long term extend and pretend tactics. No country with western dynamism or a strong averse reaction to authoritarian regimes can tolerate this very long. It seems to be widely understood now that free money orgies only ever concentrate wealth in the top one percent while taxing the bottom seventy percent heavily through inflation. If the economy does go into a deflationary cycle will the federal government start destroying collateral? One can see that china and Japan will probably need to do this in the near future and war is not what it once was, but is now largely automated. It’s funny how language alone allows this system of overproduction to perpetuate. If we started calling houses collateral, and honestly examine the cost of four decades (1982-2020) of free money while honestly measuring inflation, we would be able to see the fake economy for what it is.

Invest in gold.

Plan on lots of folks moving their primary residence to mom and dad’s house. Property tax bite on write up is even worse than mortgage rate. Look for CA to find a way to change the law to allow higher tax rate on death – they love to legislate higher cost levels to smaller segments of the population.

You can have my 2.7% mortgage over my dead body…

There is a music video about this very phenomenon. Look up “Remy, cold dead hands” on YouTube.

Same here @ 2.25% on 10 year note

Every time we’ve gotten a mortgage, I would tell my wife,we’ll never see rates this low again.

First home

2005: 30 year at 5.625%

2011: 15 year at 4.125% (Refi)

Second home

2012: 30 year at 3.375%

2021: 15 year at 2.125%

So I’ve been wrong every time which she found hilarious.

Frankenstein’s monster was actually named Three Percent Mortgage. What few friends he had called him “TPM”, or sometimes “TP” for short. He had a difficult life and a bad ending.

Wonder if Congress might eventually force these low mortgage rates to be re-adjusted to market rates (~7%) or the mortgages won’t be guaranteed by the government.

That would force change in a hurry.

What? As in existing mortgages going up?

Yes, like every other country ever.

Mortgages used to be 5 year terms, half down, with floating rates, when it was a free market.

We should return to that.

This is the dumbest fucking thing I’ve read in the internet today so congrats on that.

Congress has no authority to change my mortgage rate. You are advocating for the government to get even more involved in the market. It is a horrible idea.

Like every other country: each of which is grappling with their own brands of housing un-affordability!

This is an issue that forces instability. When I have a housing payment that can jump every 5 years and a family, it makes it difficult.

Canada is like this (UK, many others) and the Toronto area has also seen prices explode.

I have only ever had one mortgage. I was, and am still, grateful for my 30-year fixed.

My wife was talked into more house than she needed with an ARM back in 2006-7 era. A surprise repair and general life circumstances got her out of it, largely unscathed (but close to taking a big bath otherwise).

No. The markets will do that over time.

Markets for housing are already pretty much nonexistent because of mortgage guarantee and other government policies.

Why not interfere more in a way that saves the government money?

They may well be forced to regardless but that’s another issue.

Why not just eliminate all private property while we are it?

What Congress should do is allow current home owners to buy back the underlying “bond” held against their mortgage. Your mortgage exists as a repackaged security others can buy and sell. And guess what, this security has greatly dropped in price as it yields 6.5 percent now instead of 2.5 percent.

This allows u to close out your mortgage for a much lower sum than the balance printed on your statement.

This process would make manifest the “free money” aspect of these mortgages and allow owners to book the profits of their current low rate mortgage in the present, rather than over years, and move to a different house if they choose.

Crazy? No. This is how bonds, which your mortgage essentially is, work.

Exactly. What’s the mark2market value of my 2.7% mortgage now that rates are higher 🤔

If I bought the 10y note five years ago and now want a higher coupon, I’m going to take a big hit on the principal value…

This is the ideal long-term solution, but I don’t think anybody has the stomach for the short-term pain. It would lower home values, which is what needs to happen to stabilize the market. Over-indebted homeowners and lenders would be screwed. A homeowner who buys their loan for a discount is in a position to sell their home at a lower price. This is the only sensible way to lower prices. This approach requires common sense among incumbent institutions. I had this exact conversation with my servicing company about my 2.25% 20-year fixed-rate mortgage. They didn’t get it. The problem is that institutional investors, who ultimately hold mortgage-backed securities, must mark their assets to their current value which blows up their derivative trades. Financing would seize up, leading to lower home values, and the financial and housing markets would crumble. It’s not just consumers who have too much debt; companies and the government are both swimming in debt. What’s the solution? Let the market sort it out without government intervention. We’d end up in a better place than we are now, but consumers, politicians, and businesses would have to accept the short-term challenges. Fat chance of that happening.

Austerity can’t happen if political operatives need to get reelected. It can happen in authoritarian countries. Argentina is a test case we can watch while the current USA federal regime wants to have it both ways, authoritarianism and money printing for their own cartel.

If the MBS were sold then they would have to recognize the losses of lending at such a ridiculous rate, which nobody wants to do. They would rather pretend.

Sure, if they wanted to guarantee losing their next election, this is a surefire way to do that.

They may be forced to.

Do you really think that the federal government has the fiscal capacity to bail out America’s mortgages?

I don’t think so.

Waiona, I am not saying there should be no vacation rental units. I am saying they should be taxed and regulated like hotels motels because that is what they are, and they should obey zoning laws like everybody else, or pay fines or go to prison.

Try putting a tax on unrealized capital gains. A lot of property would go on the market at very low prices. Sounds very Democratic, doesn’t it.

We live in a post-democracy country. Try to keep up ;)

There would a real revolution. Taxing unrealized gains is a holdup.

This is already what property taxes are.

The tax is based on the “assessed value” of your home, today (on the day of assessment).

This already has been bunching up the panties in my neighborhood. To the point where a self proclaimed real estate expert is complaining about her property taxes (in a letter to the editor about a municipal bond issue), not understanding the difference between a mill-levy, property tax or a loan repayment (which wouldn’t come from a tax increase)….

I digress: the game is SO rigged that the “top players” are losing ways to cheat the rules.

What a lovely progressive liberal concept. Akin to communism.

“The shrinking share of these ultra-low-rate mortgages documents the slow exit of homeowners and investors from the “lock-in effect.” In this Great Housing Abomination, there is a lock-in-effect, which is akin to a seat belt, intended to have some safety benefit. When this GHB bursts, the number of homeowners pulling the ejection lever will be frightening. It’s more of a lifesaving/ crash-imminent measure.

In response to that very last graph -Negative real mortgage rates lead to home price explosion” – HOT JAMBALAYA! Here we are. How’d we get here?!

Lastly – “These below 3%-mortgages are free money in real terms because inflation is currently running at about 3% and accelerating, and if borrowing costs run at the rate of inflation or below, it equates to getting free money.”

So, when I deposit money into a money market at 3% or more, the BANK is the LUCKY ONE getting the FREE MONEY.

I’ve finally got that conundrum figured out.

This part is interesting:

“All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.”

Some of the negative slope of the 3.99% and below chart lines are presumably the 5/1 ARM borrowers timing out of their lottery-winning rates after they, well, “adjust”. That’s probably not a big number (why would you only take free money for 5 years instead of 30?) but it’s not zero.

The question in my mind is what proportion of the huge up-slope around 2021 in the sub-3% mortgages were 5/1 ARMs. Because those people are about to have a very interesting 2026.

Never mind. It doesn’t look like there’s going to be ARM pain in 2026.

perplexity.ai: “Produce time-series data year by year between 2009 and 2025 of proportion of new U.S. mortgages that were five-year ARMs.”

Year | Estimated % of New Mortgages (5/1 ARMs)

——+—————————————–

2009 | ~8%

2010 | ~8%

2011 | ~6%

2012 | ~6%

2013 | ~7%

2014 | ~7%

2015 | ~6%

2016 | ~6%

2017 | ~5%

2018 | ~7%

2019 | ~5%

2020 | ~5%

2021 | ~4%

2022 | ~9%

2023 | ~10–14%

2024 | ~6–7%

2025 | ~6%

But 2027 is looking to take out a chunk of the spike in four-percenters from 2022.

perplexity.ai: “Produce time-series data year by year between 2015 and 2025 of the average rate for a 5/1 ARM.”

Year | Average Rate (%)

——+——————

2015 | 2.98

2016 | 2.92

2017 | 3.09

2018 | 3.81

2019 | 3.45

2020 | 3.27

2021 | 2.61

2022 | 4.09

2023 | 6.18

2024 | 6.80

2025 | 7.11

Good analysis. Multifamily landlords have bridge debt pain. Functioned essentially like an ARM. Rates were based on SOFR plus a spread. Once SOFR skyrocketed then the rates did.

I have a 7 yr arm

2.5

caps at 6.5

right now at 4% the fed is paying my mortgage. At EOY 7 my payoff is 130k+ from what I borrowed because of principal pay down

So someone lent me $$$ and the Fed gov’t paid me over $130,000 to stay 7 years in the mortgage….that’s based on the 2 mo bill staying above 3.75%. I’ll take over 20k a year tax free to add to my retirement.

If bills rise sharply then I’ll let it ride

Howdy Folks. WOW, that sure is STILL a large number of prisoners….

Terrific analysis as always, Wolf.

My very limited anecdotal evidence strongly supports the thesis that the homeowners with these ultra low rates will do absolutely everything they can to keep them. I wonder if, given the scale, this increases the fragility of the housing market.

Howdy Tight Purse. YEP, I ‘ ll bet divorced couples get remarried and everyone still lives in the same house. Dogs and cats living together too.

Maybe not remarried and living in the same house. But staying divorced and parking an Airstream to live on the same land. A recent WSJ article says that’s a thing now. Because low rate.

I know a handful of Gen Xers who did cash out refis to under 3%, then took that massive cash pile and plowed it into Airbnbs. They have been living well, not many worries.

All Airbnb owners should be treated as motel/hotel owners (because that is what they are), and should be subject to all regulations, fees, licenses, and taxes paid by motels/hotels.

Oops, I forgot to mention. Airbnb owners should also be subject to the same zoning laws that motels/hotels deal with.

Ah yes lets crank up the zoning restrictions and make the lot & build affordable for only the top tier.

Throw a HOA in for good measure.

Tom, that’s stupid.

Zoning restrictions to prevent building new housing is not even close to equivalent to zoning restrictions to prevent people from running unlicensed hotels that TAKE HOUSING AWAY.

@TSonder305 are you aware that we have had furnished vacation rentals in vacation areas of the US and furnished executive rentals in big cities for the last 100 years? AirBnB and other online platform have inceased the numbers of short term rentals in most markets, but just by a small percentage. The number of furnished cabins in Tahoe that are rented and the number of furnished apartments in SF did not double after AirBnB started.

The County of Hawaii paid for a study(conducted by the same company that the Hotel industry uses) and it concluded ridding the County of transient vacation rentals will not bring prices down or increase rental stock. Only 1 in 25 vacation rental owners said they would consider long term rental if the TVR’s were legislated away.

There are many reasons for this. #1 being places like Calif and HI that have a lot of TVR’s also have draconian renter protection laws. Anti-TVR is a Hotel industry campaign designed to eliminate competition.

Waiono, I don’t believe those numbers.

If you only are talking about people who use these properties as vacation homes, and rent them out during spare weekends for some extra money, then I can possibly believe that only 4% would do a long-term rental if short-term were banned.

If you’re talking about people who bought the properties solely to use them as short-term rentals (and in some markets, there are a lot of these), I don’t believe for a second that they would leave them empty if they couldn’t STR them. They’d either sell them or rent them out the traditional way.

@TSonder305 If you “don’t believe the numbers” Do the math on any home or condo in Hawaii (or Tahoe where I have a cabin) and you will see that even with a 50% cash down payment you won’t have positive cash flow from any property rented as an AirBnB (if you don’t do all the management, maintenence and cleaning yourself). We have a paid off cabin with low property taxes (thanks to Prop 13) and we gross over $100K a year but it costs more than that to keep the place running paying 30% off the top to our manager.

Those would be just rental income properties subject to all of the issues and problems and costs associated with rental real estate. Air is just a rental service and does not own properties.

As documented by our host, the houses they bought to be Airbnbs have likely declined in value since closing. If they have mortgages on them then they might have lost all their equity or even be under water, despite the benefit of still being cash flow positive for now.

That’s not many worries, only one. But it’s also not a little one.

That is likely true of most of those who are holding on to their 3% mortgage for any reason.

They are losing money every day in terms of reduced equity but don’t feel it so they don’t do anything about it.

Primary residence owners are slowly leaking wealth to keep a roof over their heads. Airbnb owners are slowly leaking wealth to keep a roof over somebody else’s heads. Opinions can vary about which is more painful.

@Reticent Herd Animal only a samll percentage of AirBnBs are pure “investment” properies. The majority of them are people renting a room or a room above the garage in their personal home for extra cash or people with vacation or seasonal homes and condos making some extra cash when they are not using the property.

That’s not the subset Depth Charge called out to start this thread.

In many markets, that is not the case.

Many AirBnb hosts are quitting the platform, as AirBnb has become difficult for hosts (supposedly). Buying a piece of real estate where the economics only work with one particular service is not wise, in my opinion.

Booking,com and VRBO….Bigtime competitors.

The US needs to delete all subsidies.

Just take all the hundreds of thousands of pages of laws designed to distort markets for some social objective and hit the delete key.

While I agree with the sentiment, the largest subsidies are for agriculture, energy and transportation.

I like the easy availability of these things.

Others include tech: data centers and other things that I use, but could also ctrl-alt-DELETE and keep smiling.

My Google friend says: Home refinancing during the “mid-2020 to mid-2022” period involved a significant amount of money, with estimates suggesting around $5.4 trillion in first-lien refinance originations during this timeframe, driven by historically low interest rates following the pandemic’s onset.

If my friend is totally wrong, I’m sorry — I was just curious about what kinds cash traded hands, which might explain something…

Refinancing a mortgage, unless it’s a cash-out refi, is zero-sum. The homeowner ends up with the same amount of debt, but a different lower-interest rate mortgage. Lenders of the original mortgage get the remaining principal back, paid for by the lenders of the new mortgage. And a lot of times, those lenders were the same. So the aggregate mortgage balance remains the same, but the average rate is lower.

Only cash-out refis add to the aggregate mortgage balance.

Well, and of course, fees are being extracted everywhere along the way, and some of those fees get rolled into the new mortgage as points that the homeowner pays.

The amortization schedule principle / interest parts of payments is reset.

Yup, I am sure this is the part most, if not all RE agents will not be too up eager to advertise when leveraging their marry the house, date the rate talking point. Not to mention the added closing cost to the overall cost as well.

Then againwe live in a society where people only want to focus on the number they pay each month and not the total cost/benefit ratio.

I agree, Many just look at the monthly payment and not the big picture over the life of the loan.

There were quite a few mortgage brokers who were either naive or con men.

For example, I had refi’d 3 years before back around 2015 and the avalanche of mortgage brokers started calling me.

I would listen to them to find out the current rates. The first thing they asked was what was my monthly payment.

This broker said he could lower my payments by over $100/month with a 30 year refi.

1. Their fees and points to do this were excessive.

2) The new term would have been another 30 years when I had already paid over 3 years on my current loan.

But he kept saying your monthly payment will be lower. He didn’t get it but it must have worked on many people.

I always refi’d when rates dropped over a point and fees/points were minimal.

I don’t get why people are refiing now when rates have dropped less than a half point. I guess the payments are less over the next 30 years.

Trump planning – 1. a fed that will massively cut short rates 2. immigration enforcement including legal immigration that will reduce employments 3. AI improving efficiency and fuelling deflation 4. AI cutting white collar employment 5. International trade inefficiencies with tariff leading to massive investments further bolstered by short rates and tax writeoffs 6. SALT reducing effective interest rates for blue states

I see a mixed signal here – with depopulation we will have empty houses at the same time inflation in other areas will prop up pushing up gold and stocks. US30Y may stay flat as people buy US30Y,even with higher inflation – due to artificially pushed down short rates and counterbalancing QT.

Next govt may prop up tax rates and cut tariffs – to reduce deificits. all in all a VERY TOUGH period for people who buy houses instead of gold and stocks.

The dark horse is AI bubble, if it crashes, we have massive AI model improvements as costs of AI come down and massive reduction in AI high paid workforce – this will kill Bay area prices.

Will the FED actually lower rates to effect a 5% mortgage interest rate?

The economy does not seem to be as good as some say. When people with low mortgages stay put that is a big obstacle to any serious uptick in the economy. Without motion no much will happen. If things remain like they are now NOT GOOD!

My strategy is to stay put and see if things get going. If not, there is still the significant reduction of expenses by leaving California in a smaller town outside Nashville, TN like a university town (cookville TN) and taking less on my home here would be easier to give up.

How many times do we have to discredit the same tired old tropes about the Fed lowering mortgage rates? The Fed only lowers the short-term borrowing rate, also called the fed funds rate.

Mortgages are tied to the 10 year treasury and trade on the open market.

Unless we have a nasty recession such that people want 10 year treasuries at 2.5%, or unless the Fed starts QE again, 5% mortgage rates are not happening anytime soon.

I think Trump is the most business minded president we have had in my lifetime with Reagan in second place in terms of pro business. It is my hope that the economy will quickly rise the tides for all boats to get things going.

Living in California has lost any advantage for great deal of its population.

Most younger people cannot even fathom buying a home. And, who would want to given the ancillary costs now going through the roof?

Keep in mind that these ultra-low mortgage interest rates started under Trump and he’s pushing for them again.

The unwind will come quickly in areas where H1Bs or deportees are concentrated. In Austin, H1Bs were overpaying for homes because they could and prices were only going up. Now that many will have to go back, and the jobs are not that plentiful, the unwind will be brutal and swift. I know it is already happening.

The other part of this is property taxes. The taxing districts are fat and greedy and the payers are unemployed, underemployed, and maxed out. Eventually, they will have to walk away no matter how low the mortgage rate. I just read Austin is increasing property taxes by 9% and they are already a high tax area, with a downtown drowning in unsold condos. Maybe Musk will buy them all.

In terms of the H-1b situation, there is a possibility that it may shake out in a different way than you describe: Demand for H-1b and related visas has for years exceeded by a wide margin the caps and the lottery. What the $100k fee will do is cut down on the lower-wage tech workers brought in to replace American workers. But it makes room for companies to bring in high-wage workers since the lottery will be less competitive. So the caps and the lottery maximum could still be reached, and the number of H-1b workers coming in might therefore not decline, but their average quality will shift to higher-end tech workers. There are a lot of tech companies that like the new system for that reason because they have a better chance of bringing in higher-end tech workers. So I’m not sure how all that will wash out for the housing market.

That was my first reaction. H1B are being used for low quality workers thanks to the insane decision to make the lottery random.

Hostile though the US currently is to foreigners, I think there’ll still be enough demand to fill the cap. And it’s pretty easy to underpay by 40k+ a year, recoup the fee, and still get the application accepted when you’re talking about a 200k value worker, so companies will still be interested.

I always respond with wonderment when I hear people say that the US has become hostile to foreigners.

It’s as if people are unaware that the US is, does, and has for a long time been the nation with the largest annual in-migration population in the world. By a LARGE margin. Annual US legal immigration is around 1 million. Second place is Germany and they’re not even close with something around 300k.

I understand that US “hostility” has become a popular talking point among left-wing pundits, but what I’m hearing from regular folks on the right is that they want two things: stop ILLEGAL immigration, and make sure that our importing of skilled (and unskilled) labor isn’t needlessly supplanting domestic supply, thereby disadvantaging our own civilians in favor of foreign workers who may be willing to work for less or in worse conditions.

If people being concerned about breaking our immigration laws is tantamount to feeling “hostility” then I’d say it’s long overdue. Following immigration laws isn’t actually that hard. I’ve traveled countless times to many countries, including some hostile to the US. I’ve never once violated an immigration law. Not on purpose and not on accident.

“I just read Austin is increasing property taxes by 9% and they are already a high tax area…”

I have a front row seat to this. Your point is a little off target. The city isn’t imposing a 9% increase, they put it on the ballot in November (Proposition Q). So we, the residents of Austin, get to choose the level of our collective pain. If we vote Prop Q down then city taxes only go up about 3.5%, the state law cap for un-voted tax increases. Democracy in action.

I’m not sure why everyone is negative towards people with low mortgage rates. Sometimes you just get lucky. I currently have a 2.5 percent mortgage. I wasn’t paying attention to the mortgage market. We had a great mortgage broker who called and let me know rates had dropped. So, I went from a 20 year fixed at 3.5 to a 2.5 fixed at 15 with no fees. Like I said, sometimes you just get lucky.

Speaking for myself, I don’t hold any negativity to people with low mortgage rates. What I dislike are those who bought in 2016, refinanced in 2021 to a 3% mortgage, and now think they’re brilliant real estate investors, as opposed to people who were just in the right place at the right time.

@TSonder305 Did you buy in 2016 and refinance in 2021? Anyone could have bought in 2016 and refinanced in 2021 not just the “people who were just in the right place at the right time”. Last year I was told that a 14 unit apartment I “didn’t” buy (I was too busy at the time) for just over $100K/unit in 2013 sold for just over $300K/unit. You have to be in the righ tplace at the right time and “actually take action” (I bet a dozen people hung hung on the cold calling mortgage broker before Yukon Cornholio took his call and decided to refinance)…

“Anyone could have bought in 2016 and refinanced in 2021”

2016 was 9 years ago. Millions of people have become adults, graduated college, and started careers since that time and would not have been able to buy a house in 2016.

What idiocy. What about people who were 20, a junior in college, in 2016? They’re now 29, and are finding home affordability among the worst it’s ever been.

What about someone who spent 5 years overseas in the military, and returned to the current housing market?

This level of arrogance is exactly what I’m talking about.

For the record, I bought my home in 2013.

Yes, free money at 3%, just imagine if you or your business could borrow directly from the Fed for ZIRP…

“Full FAITH and Credit”…

Interesting times.

Any sign that realtors commissions are falling? 6% is crazy. Paid 1.2% in UK. Sellers could accept a lower price if realtors were paid what was reasonable.

This doesn’t answer your question, but it does illustrate a level of flexibility among realtors that most of us would not have expected. I did my last housing purchase for flat $1,000 all in. It’s a rental in a city 100 miles away but my network up there is solid and it’s pushing 12% EBITA this year. Cash transaction with fees et al <0.5% on the nut.

I'm not particularly smart, but I've always paid it forward and this time it worked out. I recently facilitated a car deal for this same realtor that saved her 2x what she would have made on my purchase at 6% (on a car that cost almost as much as the house I bought – strange times).

The last chart is just stunning. It’s quite obvious that the Fed should have been moving on raising rates no later than the start of 2021 probably by 50 BP.

I can’t post the link, but there is a hilarious (and spot on) video called “My Cold Dead Hands” by a fellow named Remy about people holding on to their sub 3% mortgages “until the day they die”.

Well worth a watch (it’s only 2 minutes).

The FED’s purchase of agency MBS was perversely an allocation of credit, an action which it was originally supposed to restrict and not favor.

It is the mortgage holders who are locked in. They are stuck with loans paying lower than current market rate for longer than they expected when the loans were made.

Sometimes I think the Fed were geniuses this time compared to Housing Bubble I.

Back in 2008, people had slightly lower rates but with higher house prices and a job loss recession, they were stretched much thinner and many had to sell at a loss or foreclose. Once the foreclosure avalanche started, it caused a panic as prices spiraled down.

This time, people are so proud of their low rates and 50% appreciation buffer, that their mortgage will have to be pried from their cold dead fingers.. if a recession does occur, it will take a HUGE drop in prices for panic to ensue.

Many probably could take a break from working and flip burgers at $20/hour for awhile down the street rather being forced to sell. This time it is better for current mortgage holders but bad for anyone trying to buy. Thanks to wage inflation and ultra-low rates, there may not be a panic like last time. Unless we have deflation in wages and house prices. The FED hates deflation.so that isn’t likely.

“Thanks to wage inflation and ultra-low rates, there may not be a panic like last time. ”

I don’t see wage inflation ( i.e. wage catching up with inflation in real world ) and of course rates are not as low it was few years back ( although historically rates are normal).

Everyday, people are slowly but surely selling for multitude of reasons and once hot markets like Austin and SFO has already seen 22% plus decline from their peak price and still going down despite hot economy.

People have some life change (not always financial reason for moving) on average every six or seven years. The notion of locking one’s life up in a geographic place for financial reasons is a boomers idea that may not survive in the yolo modern economy and the panic selling (equity disappearing rapidly) has begun in the bubbliest boomtowns of 2020-22.

You also have to factor in the availability of insurance, which is a huge grey swan at this point. It’ll be interesting to see what happens when the immovable object (people living in houses with 3% mortgages) meets the irresistible force (sea level, etc.)

Matt the oceans are not rising significantly to cause any sort of problem in our lifetime. Neither are the temperatures for that matter. Building in high risk areas where there are hurricanes and fires is another story.

I live near an area where you can’t get insurance due to fire hazards.

It would be difficult to sell your house when every mortgage requires insurance.

The cash buyers will likely come out with lowball offers that will drive down prices.

A lowball sale should drive down property taxes for these areas.

“A lowball sale should drive down property taxes for these areas.”

If these lowball sales (the clearing price) whittle down overall prices in that area over the years, making those homes less expensive to insure, then insurance might show again eventually.

As Wolf has stated many times, it is essentially a zero-sum game. If those clutching low rate mortgages are not selling, the other side of the coin is that they are not buying either.

In my area chart, active inventory has been rising, sales and prices have been flat. Seems reasonable to predict that if listings continue to rise, prices will come down to get to a deal (absent significant decline in mortgage rates). This will play out over years.

I’m calling BS on the lock in effect. If you have a sub 4% interest rate, your home’s value has increased massively. You’ve also been able to save up money with these lower payments. If you haven’t, you’re not good with money. This lock in narrative is essentially saying you can’t afford another home because your current one didn’t appreciate in value and you weren’t able to save money.

OK, lets do some mortgage math here.

Assume you bought in 2021 a $400,000 house, zero down, with a 3% mortgage. Your payment = $2,015/month.

You want to sell it in 2025 for $500,000, so you get $100,000 in gains + $35,000 in principal payments – $30,000 (in 6% fees and costs) = $105,000 in cash after paying off the remainder of the mortgage.

You buy another $500,000 house, put that $105,000 down, and finance $395,000 at 6.3%. Your monthly payment = $2,745.

So your payment is $730 a month higher, if you sell your house for $500,000 and buy a house for $500,000.

Given the higher purchase price, insurance and property taxes may also be higher.

This is a great example of mortgage math! I will use it as a reference with my co-workers.

I’d like to add that many of my Millennial co-workers (born 1981-1990) bought when they were in their late 20’s and early thirties if they had a job. This was around 2010-2016 when houses were at the bottom from HB 1. After rock bottom prices, by 2021, they only had about 200K left on their mortgages when rates hit 3% and they were in their late 30’s and early 40’s. With a 3% 30 year refi mortgage, their payments are now $1K/month. In some states/cities, minimum wage is $15+/hour or $31K+/year. Their mortgage payment is about 1/3 of minimum wage.

My points are:

1) if you bought a house from 2010-2016, (or before 2003) you can likely survive and keep the house with a minimum wage job if all heck breaks loose in the economy. Peace of mind is keeping these owners in place. This was not true during HB 1 so many unemployed lost their houses. Low end wage inflation helps this for HB 2.

2) I could be truly happy and secure in my house with a Walmart greeter job.

3) Contrary what was being said 10-15 years ago, Millennials and Gen X are the luckiest generations ever. Even more lucky than Boomers who had to deal with 18% mortgages during their prime home buying ages.

4) Every generation seems to get their chance. It looks dark for Gen Z at this point but who knows what will happen on this great roller coaster? Millennial and Gen-X whining paid off with a little patience.

Boomers are aging out of ownership (and this widely understood to be a marketing phrase in the era of mortgages) and younger generations are less interested in subsidizing wall street than prior generations.

I just sold my home because I got a contingent offer accepted. Buying our dream home for $1.4M and giving up a 4.5% rate and doing a 5/1 ARM giving me a 5.5% rate on the new place. It was the best I could find and I’m better rates will dip below 5.5% at some point in the next 5 years. I’ll refinance to a 30 yr fixed when that does happen. People with rates 3% or lower will never sell unless they are old or moving halfway across the country.

“Forced sales” will remain a tiny share of home sales. After 2009, lending standards are such that there will be no wave of foreclosure forced sales.

I would bet a lot of those mortgages are to 40-60 year olds who are at the least propensity to move for any reason as they have kids in school etc etc.

I normally like Wolf’s chart type selections, but on this one I think a stacked area for the mortgage rate distribution trends would be easier to digest than multiple charts.

Not a complaint, just an observation.

No it wouldn’t be, because it looks like artificially dyed spaghetti without sauce. And that’s literally not easy to digest.

Judging by the source of the information, I’m assuming this does not include Jumbo mortgages that cannot be bought from the banks. Just verifying for reference. If that is correct, do we have any data on Jumbo mortgages or at least know what percentage of mortgage balances outstanding fall under that umbrella?

“I’m assuming this does not include Jumbo mortgages that cannot be bought from the banks”

This is not correct. The data is a sample of 5% of all mortgages in the US, based on three components:

(1) the National Mortgage Database (NMDB);

(2) the National Survey of Mortgage Originations (NSMO); and

(3) the American Survey of Mortgage Borrowers (ASMB).

https://www.fhfa.gov/document/national-mortgage-database-technical-documentation