The bond market’s reaction to cocktail of inflation fears, potentially lax Fed, and Mississippi River of new debt flowing into the market.

By Wolf Richter for WOLF STREET.

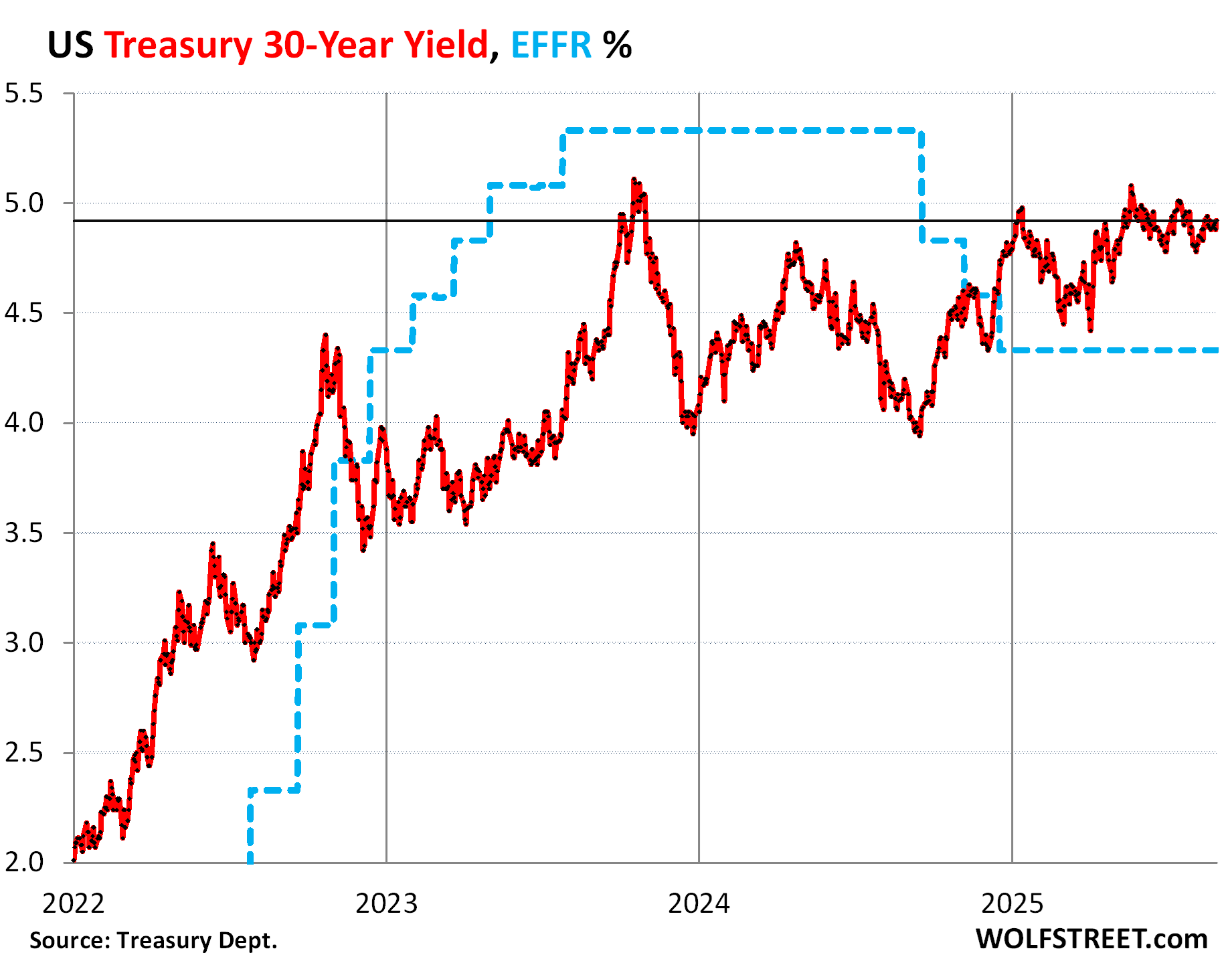

The 30-year Treasury yield rose 5 basis points on Friday and closed at 4.93%. Since the beginning of March, it has risen by roughly 50 basis points, as the bond market reacted nervously to Trump’s enormous pressure on the Fed to cut interest rates amid worsening inflation, driven by inflation in services.

The 30-year Treasury yield is now 60 basis points above the effective federal funds rate (EFFR), which the Fed targets with its monetary policy rates (blue in the chart).

When the Fed cut its policy rates by 100 basis points in 2024 amid rising inflation, the 30-year Treasury yield, in a massive counter-reaction, rose by 100 basis points, and we began musing here about a secret question: How many more rate cuts would it take to drive the 30-year yield to 6%?

Inflation kills the purchasing power of bonds, and investors want to be compensated for the expected loss of purchasing power by being paid a higher yield. So the bond market wants to be reassured by a hawkish Fed that inflation will not be allowed to run wild.

But Trumps efforts of installing a lackadaisical or even reckless Fed even as inflation is accelerating and far above the Fed’s target is making the bond market very nervous – and the 30-year yield shows that.

In addition, investors have to absorb the Mississippi River of new Treasury debt flowing into the bond market – meaning new investors need to be enticed into the market, and that happens with more attractive and therefore higher yields.

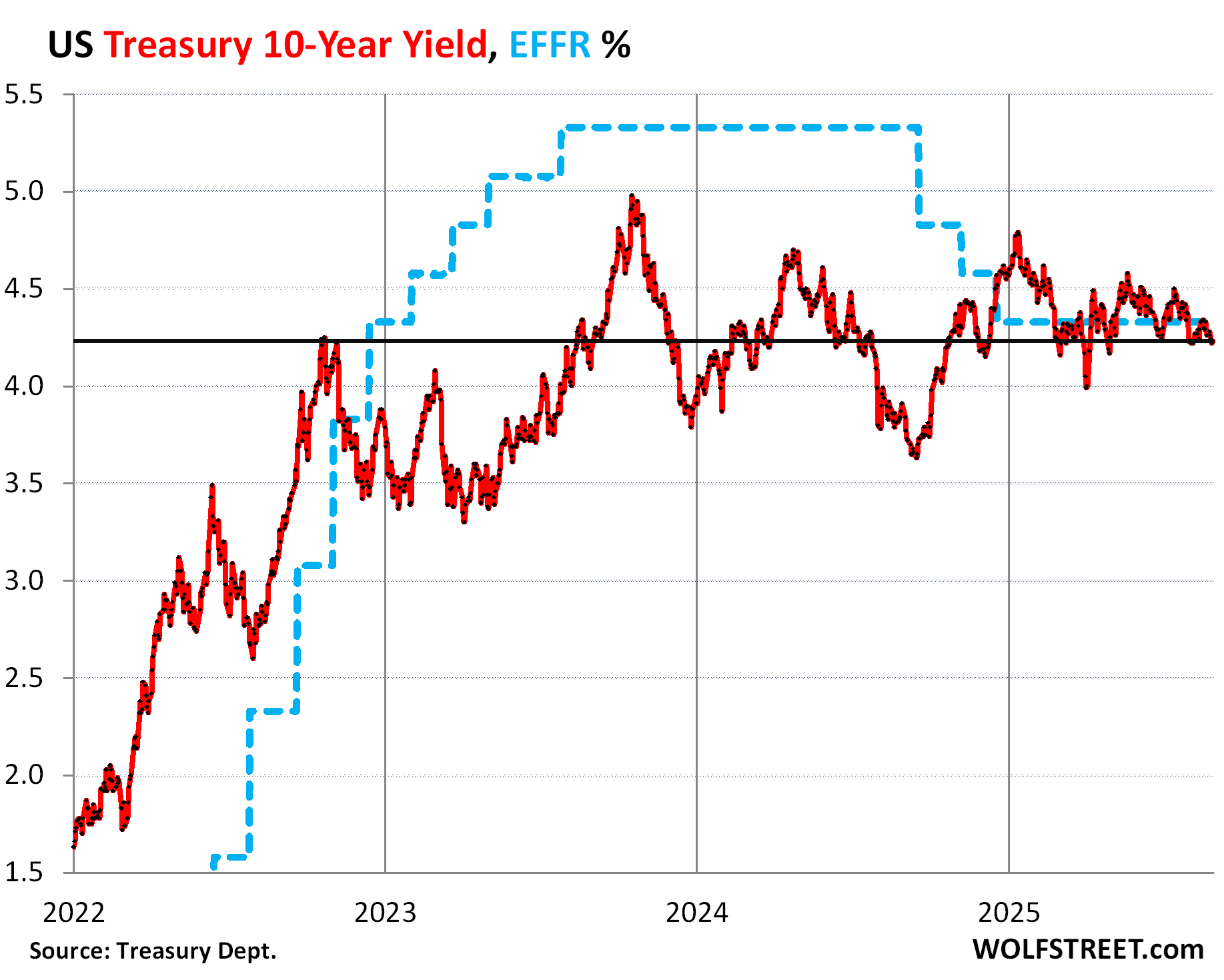

The 10-year Treasury yield has been glued to the EFFR for months, sometimes a little higher, sometimes a little lower.

On Friday, it ticked up two basis points to 4.23%, which is exactly where it was a month ago, and exactly at the end of February, and exactly two years ago at the end of August 2023. It’s up about 80 basis points from just before the Fed cut its policy rates in September last year.

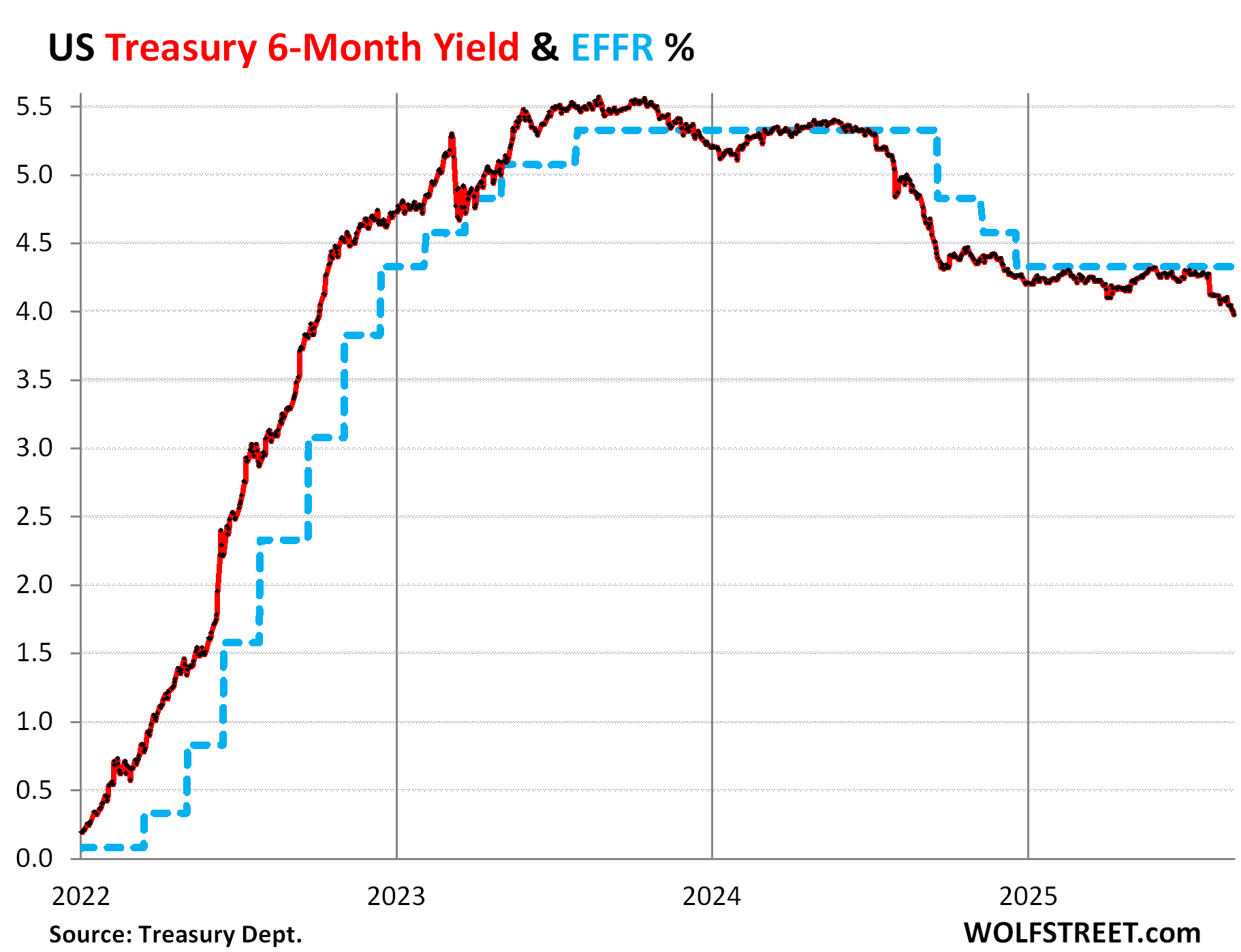

But the six-month Treasury yield dropped further on Friday, to 3.98%, the first time below 4% since October 2022 when the Fed was still hiking rates in large increments.

It is now pricing in nearly two rate cuts in its window of about 2-3 months, so one cut at the September 17 meeting, and it’s getting closer to pricing in a cut at the October meeting.

The Fed is under enormous pressure to cut. Before the FOMC’s September 17 meeting, there will be a number of data releases, including crucially, one more nonfarm jobs report and one more CPI report.

But the Fed is under such enormous pressure from Trump that it will likely cut by 25 basis points, even if the jobs report turns out to be rock-solid and CPI comes out red-hot.

There may be dissents by FOMC voters, maybe in both directions, for a bigger cut and for no cut, and the majority voting for the 25-basis-point cut may be slim. But the Fed is under such pressure that a 25-basis point cut will give it some breathing room.

If inflation accelerates further in the fall, while the labor market is solid, Fed officials will have more ammo to defend not cutting again this year.

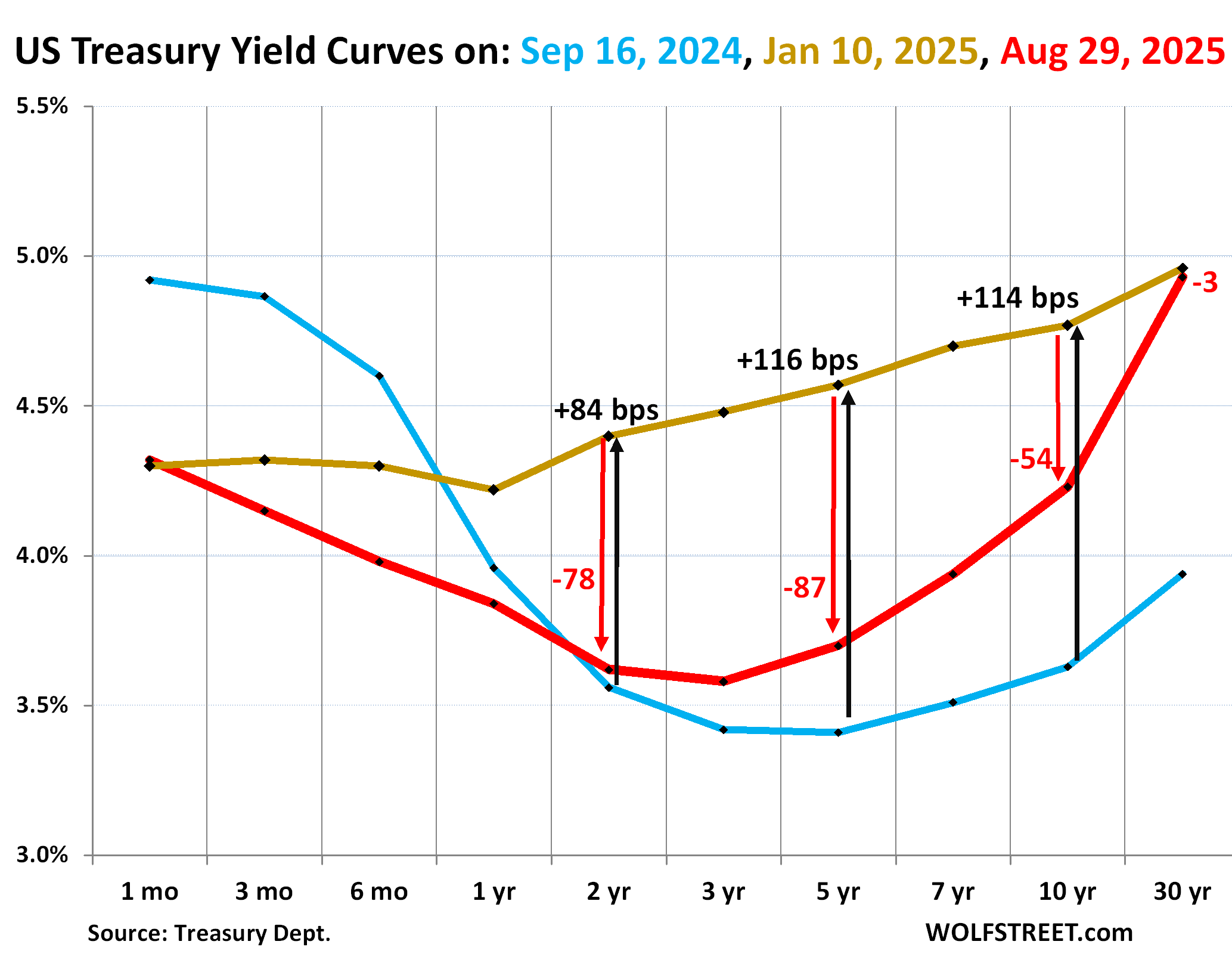

The yield curve steepened a lot at the long end. The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Red: Friday, August 29, 2025.

- Gold: January 10, 2025, just before the Fed officially pivoted to wait-and-see.

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

The 1-month yield is boxed in by the Fed’s five policy rates (from 4.25% to 4.50%) and closely tracks the EFFR. So the 1-month yield hasn’t changed much since the last rate cut in December.

But rate-cut expectations have pushed down the shorter end of the yield curve, while fears of inflation, fears of a lax Fed, and fears of the Mississippi River of new Treasury issuance have tied the 30-year yield close to the 5% mark.

With the 2-year yield falling to 3.62%, and the 30-year yield at 4.93%, the spread between them has widened to 131 basis points on Friday, the widest since November 2021. That part of the yield curve, from the 2-year yield to the 30-year yield has steepened a lot this year.

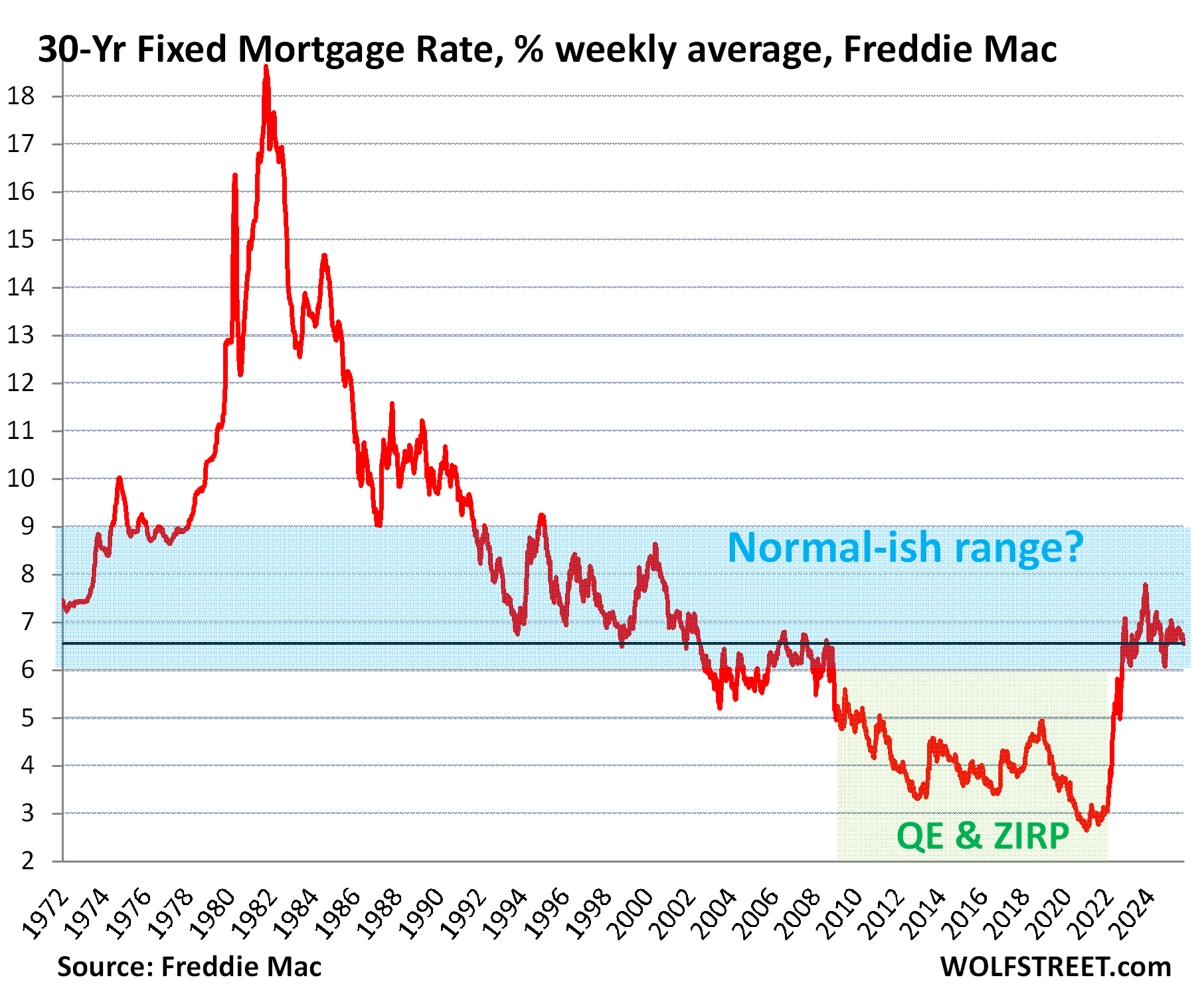

Mortgage rates track the 10-year yield, and the 10-year yield is stuck. The average 30-year fixed mortgage rate in the most recent reporting week (from Thursday last week through Wednesday this week) edged down to 6.56%, according to Freddie Mac data on Thursday. It has been above 6% since September 2022.

On the eve of the rate cuts last September, this measure of mortgage rates had dropped to 6.09%. But then the bond market freaked out over a lax Fed amid rising inflation.

Further rate cuts, if inflation continues to accelerate, may not be good for mortgage rates.

Mortgage rates didn’t drop to 5% until the Fed started QE, including buying trillions of dollars of MBS, from early 2009 on, which was designed to push down mortgage rates.

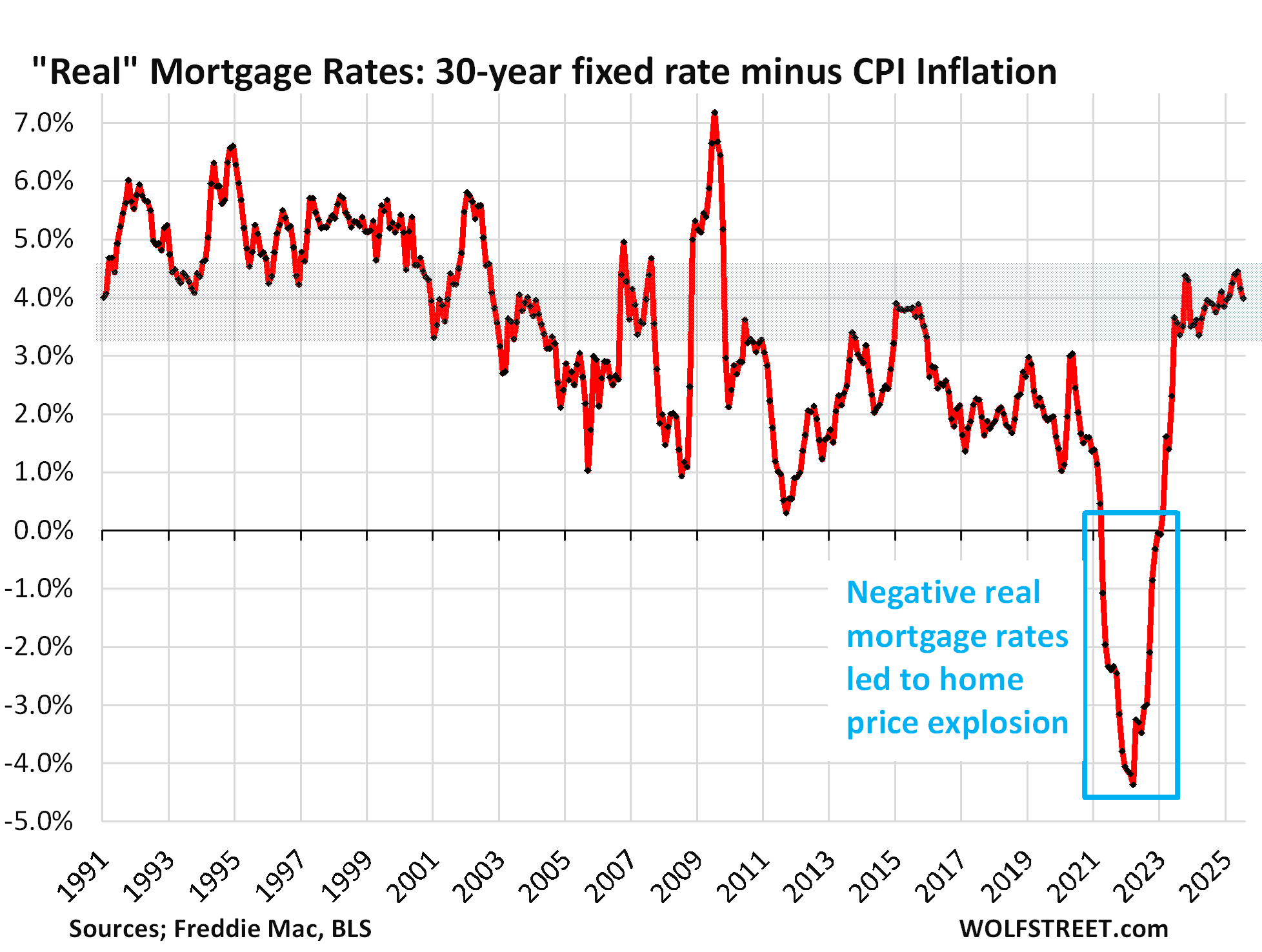

Under the force of the Fed’s mega-QE of 2020-2021, mortgage rates dropped below 3%, even as consumer price inflation broke out in late 2020 and then spiked in 2021, creating the most negative “real” mortgage rates (mortgage rates minus CPI) ever. And money was suddenly free.

And when money is free, price no longer matters, and home prices exploded far beyond where they make economic sense when money is not free.

With these policies, the Fed broke the entire housing market. The housing market has now been frozen for three years. These too-high prices have started coming down in many markets, faster for condos than for single-family homes, but it’s a slow process. It’s unlikely the Fed will do that ever again.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The seller will eventually crack as the cash buyer wins through patience/attrition .

Have a fantastic weekend W.R. and posters ! 🍻

Most of us are not cash buyers! Its pushed first time home buyers out of the market.

The whole thing is insane , could be fixed thru less greed, common sense and stop trying you predict and just let things fall into place naturally. A rate between 4 and 5.50 seems doable for most folks. 6 or higher is just greed.

A 30-50% price decline in home prices will make homes affordable again. Yes, less greed = lower prices. Lower rates = more greed and higher prices.

A lot of homeowners who recently bought a home in the last three years would be really hurting with negative equity if home prices declined 30% or more. I suppose some would just walk away from their home/mortgages similar to what happened in 2009. The current Fed Chairman seems to always be fighting the previous Fed Chairman’s errors. Although this current FOMC set themselves up creating their own problems with the 2024 100 basis point cut. It’s a moving target with many variables and you do need to lead a moving target. The question is by how much…

Wes,

Most homeowners don’t walk away from an underwater mortgage:

1. They only can do so in the 12 non-recourse states. In all other states, they’re liable for the deficiency that remains after the foreclosure sale, and the lender will obtain a deficiency judgement and go after them personally.

2. Homeowners normally continue to make their payments if they can and just ignore the Zillow value of their home.

3. During the mortgage crisis, the biggest culprits were mom-and-pop landlords that walked away from their rentals.

4. Only a relatively small portion of homeowners bought homes in 2021-2023. And a 30-50% rollback will mostly hit those, so it will be nothing like the mortgage crisis where a big portion of homeowners were underwater.

It is not greed. If I sell my home here and pay taxes on the sale, move, etc., I can not afford to move because the cost of the downsized home is more than what I sold my home for, and it is half the size. If my gains were adjusted for inflation, as Trump is proposing, no problem, lower taxes would allow me to downsize and move. After all, why should the US government profit from inflation. That really is the 64 dollar question, now isn’t it?

Andrew pepper

LOL, adjust capital gains for inflation? What kind of inflation? Home price inflation? then capital gains would always be zero. Capital gains are capital gains. Excluding some capital gains from taxation is a taxpayer subsidy for holders of that capital.

Even technically underwater homeowners may not walk away from a 3% mortgage, as there is value in the cheap loan…

Correct. But the people that bought in since 2022 don’t have 3% mortgages. But as we said, that’s a relatively small number.

You have to remember ther has been ALOT of inflation of the dollar. Also the bottom of where home prices are has moved up from say 2018.

We’re all in price discovery mode atm.

Sellers are figuring it out, buyers are figuring it out and the maket is also.

Exactly. There’s been too much inflation to send house prices down 30-50%.

That won’t happen when everything else in the country has doubled – nor do you want it to.

Homes out paced inflation by a large margin. Homes will return to median affordability. It will happen by some combination of time, wages, and home price corrections.

President Trump will lower interest rates and the economy will take off like a rocket.

If that happens, long term yields will take off and shut down the housing market and long-term financing (corporate bonds, etc.).

The article explains that principle, and how it played out in 2024 when the Fed cut 100 basis points upon which long-term yields jumped 100 basis points.

Could a “toadie” Fed also manipulate long-term rates to lower them as well? That can do more than change the overnight rate.

Yes, through high levels of QE, or even yield curve control. Of course, those have massive ramifications.

I don’t see how long term rates fall anywhere meaningful otherwise.

1.) US debt burden is insane as it is with interest expenses ballooning and no signs of showing down.

2.) The refinancing wave is coming, who is going to absorb all of this debt?

3.) The continued deficit burden which structurally just increases from the social security borrowing and inability to keep it positive finally coming to roost (and interest expenses). The amount of debt we will accumulate from these 2 required expenses alone will be insane.

4.) Trade wars causing investment uncertainty and likely dragging down economic growth. While tariffs provide a temporary deficit reduction through increased revenues, some of this is offset by the decrease in tax receipts which is going to occur no matter what. Either from US businesses or US consumers, or both, this will drag down economic growth and there is no indications in the data the exporters are eating the tariffs.

5.) The continued “gamification” of the US debt maturity portfolio by switching long term debt for more short term debt, and even doing things like requiring stablecoins to be backed by dollars or treasuries (to increase demand for treasuries ).

These are all pretty structural by nature, and don’t even involve speculation or politicization. To me, it gets significantly worse when you start factoring these in.

Fiscal dominance is among us. How long does it take to get out of control is anyones guess.

The president can remove the Fed chairman, but only for cause, such as misconduct or neglect of duty, not simply for policy disagreements. This process is governed by the Federal Reserve Act, which aims to protect the Fed’s independence.

What the heck? Why is the Fed under such “pressure” from Trump, when Trump or any president for that matter, can’t remove the Fed Chair simply for policy disagreements, which is what’s going on with Trump and his rate cut demands.

Powell ought to raise his middle finger to Trump and leave it at that.

“Powell ought to raise his middle finger to Trump and leave it at that.”

Powell’s record:

Three Fed governors resigned after getting caught front running Fed decisions(during Pres. Biden)

Powell lowers rates to goose the economy 2 months before the last election(favoring the D Party)

Biden appointee Lisa Cook is caught in blatant mortgage fraud for three properties. Powell sidesteps.

I’d say Powell has been giving Trump the middle finger with both hands.

There was no ‘mortgage fraud’ whatsoever with Lisa Cook and claims of such as such blatant disinformation attempts by Bill Pulte (yes, of Pulte Homes) to get a cut in Federal Reserve interest rates which he doesn’t even comprehend will cause mortgage interest rates to rise just as last time the Federal Reserve did that.

Another superbly detailed exposition of one of my favorite topics that Wolf regularly covers, and I’ll admit that I’m one of the readers here who’s been fantasizing about loading up on 6% long-term treasuries if the opportunity arises. But now I’m going to show my naïveté of the broader topic with this question…

I can see the Fed succumbing to pressure to lower short-term yields and simply declaring one (or more) rate cuts, and how this can subsequently bring out a new generation of bond vigilantes demanding higher long-term yields that would further steepen the yield curve. However, looking ahead toward how the “powers that be” might also try to additionally push down the long-term treasury yields, can they not simply shift even more of the upcoming federal debt into short-term treasury issues in order to keep the long-term treasury supply at a minimum, and simultaneously push for the Fed to again restart the QE machine with the Fed purchasing long-term treasuries? Is it possible that this is someone’s planned thinking for ultimately controlling interest rates across the board over the next few years?

Bond market participants are not stupid, they are not going blindly continue to buy and hold treasuries at top dollar in a long term inflationary environment no matter how many QE programs the fed tries to shove down their throat.

The Federal Reserve is doing QT (Quantatative Tightening) and hasn’t done any QE for many years. That has been covered quite extensively year over the past few years.

What else would these bond investors invest in, in the case of a return to QE? Remember TINA?

It took 9% inflation and 45% long bond losses for the Fed to finally throw bondholders some bones in 2022/2023.

Overseas bonds, stocks, real estate, anything else.

TSonder305,

Are those really good alternatives? Safe overseas bonds generally pay less interest than US bonds. Stock prices are 2-3 standard deviations above historical norms. Residential RE prices are also at record levels relative to income.

Bond investors generally hate downside risk. They’ll gladly take a manageable annual loss to inflation before exposing themselves to a quick 20-50% loss in other markets.

I still think rate repression will be very tempting next time economic troubles hit.

Seeking Cassandra,

Shifting the number of long-dated bonds to short-term bills will certainly reduce pressure on long term rates. Despite the reduced number of long term issues, those most interested in long dated bonds such as insurance companies are going to require higher yields based upon their perception of monetary and fiscal policies. Otherwise they are buying an asset they expect to lose money on. Restarting QE would set rates on fire. Markets are a psychological phenomenon more than anything else, at least until fundamentals re-assert themselves.

Enjoy your Labor Day Weekend!

“those most interested in long dated bonds such as insurance companies are going to require higher yields based upon their perception of monetary and fiscal policies.”

why didn’t they stage a rebellion 3 years ago?

Apparently, these “smart” investors couldn’t fathom that $4-5T of money printing (a helicopter drop) would lead to inflation. The Fed couldn’t fathom it either.

“How many more rate cuts would it take to drive the 30-year yield to 6%?” Actually, I wouldn’t pose that musingly afterall.

These interest rates are ridiculously low. The 30 year should be at 10%. Mortgage rates should be at least 12%. The US is now the Titanic in the North Atlantic. The question is not whether it’s going to hit an iceberg, it’s when. It’s inevitable.

Yeah, but with Fannie Mae and Freddie Mac backing all those MBS with tax payer dollars, it keeps the rate artificially low.

Wolf, the chart showing change in yield curve between Sep 16, Jan 10 and Aug 29 is elegant in its simplicity, but conveys a lot of visual information. Nice work.

I ask these tongue in cheek, but are those the Bond Vigilantes holding up the long end of the curve? And what name will the captured Trump FOMC use for YCC when the time comes? They can’t call it yield curve control, so they’ll obfuscate with jargon as they do.

YCC is just QE with a specific rate goal, such as a 10-year yield of X%, while the Fed’s QE had the same goal of pushing down long-term yields, but without a target.

Even Japan had to give up YCC when inflation took off. For the past 18 months, the BOJ has been doing QT to deal with inflation.

None of this stuff can be done in an inflationary environment. See Argentina.

Totally agree!

So, there has been practically no change whatsoever in interest rates of any during in the US this year.

Thanks Wolf. Awesome work.

Given that nominal rates should reflect a combination of, inflation plus taxes plus risk, and central banks are not buying, I too am surprised rates are so low. Especially a 30year treasury that could become a debt trap. Maybe it is already? If for example pensions are compelled to buy treasuries. Or if banks are complicit with goverment in the pass trough to the retail market. Or?

Also, if rates are lowered, by say 300 points, from political manipulations, then the cheering beneficiaries are likely: politicians (more extend and pretend room; carry on with increasing deficits and debt), overly indebted underwater commercial real estate sector, and billionaire class who would access. But likely not anyone else who source retail loans. Then comes the follow up on inflation and who is buying? Federal Reserve compelled? Pension funds compelled?

France’s recent debt woobles come to mind. So does the Greek debt crisis, (years ago), too.

So: inflation + taxes + risk

These are great charts. A picture is worth a thousand words. The greatest risk to the economy is an explosion in the 30 year bond rate. The Fed does not control this rate. If it goes any higher say to 5.5% then you can kiss the real estate market goodby. Any move by the Fed to lower rates on the short end could trigger this rise in long term rates. Trump will then own the resulting recession. He’s walking into a trap by harping on the Fed to lower rates. The economy is overheated right now and doesn’t need a cut in rates. I was out and about town today here in the Swamp and observed massive traffic jams, stores with lines at the cash registers and full of drunken sailors spending like there was no tomorrow.

Why do you say they are spending like drunken sailors? Maybe they have money in the bank, their investments are doing well, etc… Not everyone is broke.

I went to the shopping mall today and could not find parking. This economy is doing very well.

Well, it is labor day weekend, which is a pretty big weekend in general but also back to school and so on.

Sounds like full employment and increasing wages. Hopefully it shows up in the jobs report next week.

I was just helping a realtor friend today that wanted to lower their lease payment. I think they are struggling. They said “when the Fed lowers the rate then buyers will come out again and prices will go up”. In order not to lose the sale I just laughed in my head, not out loud.

The Federal Reserve FOMC members seem to care more about maintaining their jobs (aka positons of “power”, although the Emperor Wears No Clothes if they are merely marionettes) rather than maintaining their reputations or the fate of the US main street economy. The whole economy could just as well collapse in an inflationary spiral, so far as they seem to be concerned.

So ~$9.2T in short-term debt had to be replaced this year. The Treasury appears to be committed to purchasing mostly short-term debt as they take various steps in the coming months to push down short-term rates.

Okay, so let’s say they keep this up for the next few years, and our deficits remain at least $2T. So by the time Trump leaves office, there’s a real chance the debt will be pushing towards $45T

Okay, so how much short-term debt do we think we’ll need to roll over in FY 2028?

$12T, $13T, maybe $15T? At what point does the non-Fed investors get tapped out?

“The Treasury appears to be committed to purchasing mostly short-term debt”

1. Not “purchasing” but “selling”

2. No, what they’re doing is replacing ALL the notes and bonds (2-30 years) when they mature with the same types of notes and bonds, but a bunch more.

3. A larger portion of the new debt to fund the new deficits is getting financed with T-bills so that will cause the proportion of T-bills to grow. It was at 16% in July ($6 trillion of $37 trillion) and will likely grow to maybe over 20% later this year. You see this when you watch the auctions of notes and bonds: they’re huge, much huger than the maturing issue, but roughly the same as last year. What’s getting bigger are the T-bill auctions.

I couple of days ago, I gave you this example:

https://wolfstreet.com/2025/08/28/us-governments-fiscal-mess-interest-payments-on-the-treasury-debt-interest-rates-tax-receipts-and-debt-to-gdp-ratio-q2-2025/

For instance, the 10-year Treasury notes, issued in May 2015 at a yield of 2.24%, matured in May this year and were replaced at the auction on April 30 with 10-year notes that sold at a yield of 4.34%.

In addition, the size of the 10-year note auction nearly doubled, from $24 billion in 2015 to $42 billion in May. So instead of paying 2.24% on $24 billion on the old notes, the government is now paying 4.34% on $42 billion of new notes, which then starts pushing up the interest expense.

4. rolling over short-term debt is a well-oiled machine. For investors, this happens automatically and seamlessly if they choose so. If feels like a savings account. You can do it in a brokerage account or directly at TreasuryDirect.gov So that part is not really an issue. But there are other issues with that, for example, if inflation takes off, and rates are hiked, much more of the US debt gets more expensive within a very short time, and so the interest expense shoots up much more quickly. That’s the tradeoff.

Be careful about automatic reinvestments in Treasury Direct. Bills will be reinvested with the same maturity as the old instrument but notes and bonds may be reinvested with a different term: https://treasurydirect.fiscal.treasury.gov/marketable-securities/reinvesting-a-marketable-security/#id-will-i-always-get-the-same-type-and-term–588958

I had a 2-year replaced by a 5-year once (the rate was the same) and now I always do a new purchase not a reinvestment.

Yes, but I was talking about rolling over T-bills (not notes and bonds) in response to the point about the ever lager T-bill auctions.

A heads up. At Schwab, if you choose auto-rollover of Treasury bills, you will lose a week of interest each time you do an auto-rollover. So a rolled over 13 week bill actually pays you (12/13)*interest rate. 13 week T-bill rates are now around 4.20%. If you do a Schwab auto-rollover, you are only getting 3.88%. Schwab is paying you their cash rate (close to 0%) for a week and thus making more money off of you. I do all my purchases manually so that my new bill is purchased on the exact date the old one matures. I don’t know how auto-rollovers work at other places.

I see a few things getting back to normal over time but in general feels like the roaring 20s right now with little awareness of real headwinds. Admittedly there are some solid actions that could be taken by our leaders of unified in purpose but that isn’t exactly our system. Seems like maybe just turning the running of the government over to AI might not be a bad thing. It actually provide some very common sense answers to most of the problems we face today

Unless managing others money Glen, most of us are managing our own money or looking for insight while others manage our money. And it boils down to chasing yield. If it is the 1920’s what do you do? Not chase? What about when conditions deteriorate? All that time is spent dodging and weaving to avoid the contraction, while everyone from companies down to your local government suck up what cash is flowing. As for AI. Insert clown face.

AI isn’t even close to being able to handle that and let’s pray it never does. Pretty sure it would find that we are the problem.

Artificial = FAKE

So let’s call it FI….and see how that sounds to the investing public

As long as the value of their portfolios keeps increasing, they won’t care what you call it. You could call it EI (Epstein’s Island) and they wouldn’t even flinch.

Glen – your AI generated comment is well received.

Please try harder next time…

Nice try clanker.

In my mind there is no doubt a free market on its own would drive long rates to 6%+ from here. The only thing holding rates below 5% is the threat of QE. It’s an obvious consideration if/when deflationary risks present, like 2009 and 2020.

As we’ve seen, economic outlooks can reverse on a dime.

We are seeing continued QT from the Federal Reserve without a single hint of QE and that will continue to be the course from the Federal Reserve.

Talk to Mike Tyson about the credibility of your plan.

Who? Do you not look at the Federal Reserve balance sheet and/or listing to their policy statements?

That’s my concern with the housing market. If unemployment goes up and foreclosures start, it the government is ultimately on the hook for the defaults anyway, why not just create endless forbearance programs under the guise of “keeping American families in their homes?”

Anly chance there is a “failed auction” coming?

The mistreatment of the dollar is remarkable and bothersome.

Why do we have a leader that is enamored with Cryptos which are nothing more than a substitute for the dollar?

Interest rates never went high enough to shut off the spending in Washington….and to lower rates is to further subsidize the recklessness.

Predictions are for bad employment numbers coming which will give the Fed an excuse to cut. But not too long ago, under 5% unemployment was considered “normal”…..so now 4.4% will be prompt an emergency cut?

And not too long ago, “stable prices” was the mandate, and now 2.6% inflation is considered “ok”.

They move the goal posts all in the direction of justifying low interest rates, and thus the currency demise. Idiocy and political games.

The average monthly Fed funds rate 1954 to 2025 is 4.61%, median 4.33%. Current rates are slightly below normal.

Wolf: A lot of damage is created by FED. A small group of people should not set the price of any product or service, especially the price of short term money. The fact that they can is what creates the political pressure and the citizen populist pressure. Over 90% of citizens do not understand all the interrelated consequences of a FED policy action.

My question is this. Would letting the market set long, medium and short rates result in more stability in rates, slower and more gradual changes that investors in every sector of the economy good more easily rely upon to prevent so much malinvestment?

My second question is it even possible for the FED to achieve there dual mandate?

If you started with a clean slate, what would you do (regarding FED and congressional attempts to stimulate and slow down the economy with monetary policy)?

“Since the beginning of March, it has risen by roughly 50 basis points, as the bond market reacted nervously to Trump’s enormous pressure on the Fed to cut interest rates amid worsening inflation, driven by inflation in services.”

“But the Fed is under such enormous pressure from Trump that it will likely cut by 25 basis points, even if the jobs report turns out to be rock-solid and CPI comes out red-hot.”

Is there evidence of the referenced “enormous pressure” by the POTUS? Or is it just him saying outrageous stuff and posting even more crazy claims online, e.g. I see at one point he was calling for a full 1% cut? Or is there any actual rational economic policy, plan, and actions by his administration that are applying the pressure (beyond the POTUS just yacking)? The POTUS says a lot, on a 24/7/365 basis, so much that it is hard to tell what is real, i.e. could have actual effect, other than him personally just trying to stay at the top of the news cycle. I would think that the bond market would ignore him, unless there is substance to the “enormous pressure” which must extend beyond his just seeking attention. Do we understand how the pressure is being applied (if in fact this is the main factor in the bond market driving 30-year yields higher)?

My understanding is that we really need a policy of higher taxes, and government austerity (both deflationary) combined with stimulative (inflationary) moves by the Fed, to gradually reduce the debt. So perhaps the Fed making rate cuts would make sense, but only in response to deflationary moves by Congress to reduce the debt. It would seem that the Trump administration is totally ignoring the reason for the strong economy is the “free money” that was debt-financed, and now that debt needs to be drawn down systematically.

I’m 71 and 100% fixed income and MM funds in a small portfolio. My accountant and financial planner recommended last week that I lock in all treasury ladders in IRAs out to 2036 and fill in all taxable ladders to 2030, with all purchases locking in a minimum of 4.2%. I did it. Now my entire portfolio is making a minimum of 4.2% out to 2036, when I will be 82. With coupon payments, funds should last until age 86-90. It feels stupid and smart at the same time, but I won’t know until hindsight. I’m not at all money savvy, but I know I have extreme jitters about this administration and interest rates, and since I am all fixed income, this seemed like a decent solution. If longer-duration rates go up to 5% and beyond, I will be a sad old lady, but much sadder if rates fall below 4% at all, ever. Help, help me, Rhonda.

To repeat, the average monthly Fed funds rate 1954 to 2025 is 4.61%, median 4.33%. Current rates are slightly below normal. A guaranteed 4.2% minimum with no risk, if I read your comment correctly, is not bad. I buy three month Treasuries. If the Fed cuts another one, which I am pretty sure it will, I am sniffing at 20 year Treasury bonds, which would likely rise to above 5% after the cut. All bets are off if inflation numbers come in really low, which I doubt.

Thanks, thurd2. I have recency bias, because I could have locked in 4.8-5% if I hadn’t procrastinated forever in building out my ladders, so 4.2 will always feel low to me, but I do feel good about no risk and guaranteed minimum, and also it’s going to be such a relief to stop looking at the interest rates and CME FedWatch every day (ok, maybe more than once a day) for a ridiculously long time (years). If I were younger, I would definitely grab some 20-year and 30-year. I feel sick when I think about the 1980s when my young family could barely afford our rent and oil, but interest rates were 15%! Good luck with your purchases!

I guess it won’t get posted with a link but there are vanishingly few periods in US history with both increasing mortgage rates and declining home prices.

It’s irrelevant because there was NEVER a period in US history when the national median home price spiked by 50% in two years, and by a lot more in a lot of markets, as it did from June 2020 through June 2022. That has never happened before. So it’s likely that what comes afterwards also never happened before. Whatever that may be. So you can throw your history out the window.