This buyers’ strike, which started in mid-2022, completes its third year.

By Wolf Richter for WOLF STREET.

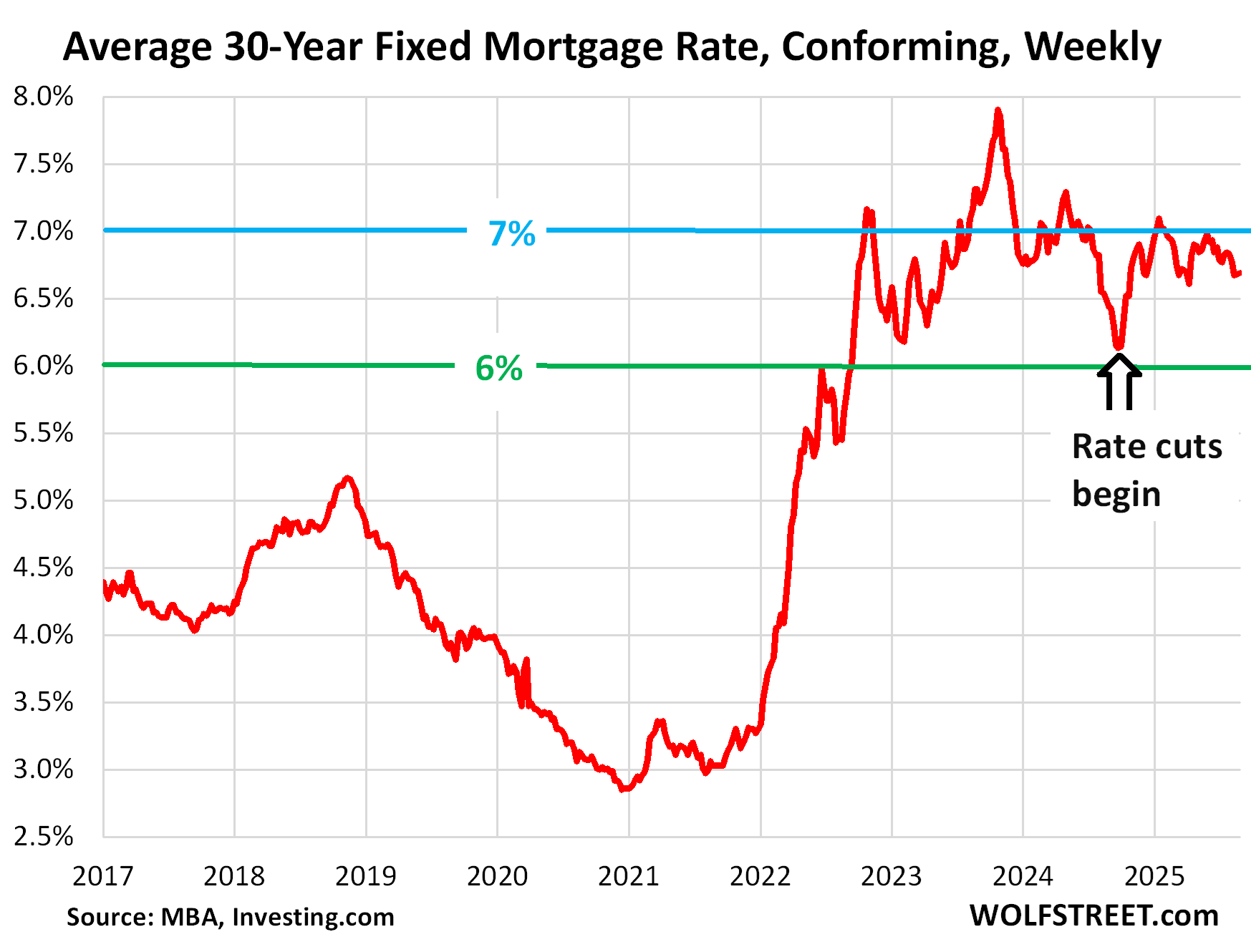

Mortgage rates ticked up a hair for the second week in a row to 6.69%, and have been in this range between 6.6% and 7.1% since October last year, with the average conforming 30-year fixed mortgage rate at 6.69% in the latest week, according to the Mortgage Bankers Association today.

Mortgage rates re-spiked by about 100 basis points from mid-September 2024 into January 2025, following with long-term Treasury yields, while the Fed cut by 100 basis points, despite inflation re-accelerating. This dovish move by the Fed in 2024, in face of accelerating inflation, spooked the long-term bond market, and thereby the mortgage market. The bond market is not to be trifled with.

As this 100-basis-point spike was unfolding, the Fed started talking tough on inflation at the December meeting, indicating that this was its last rate cut for a while. The purpose was to stop long-term yields and mortgage rates from spiking further. The tough talk grew into 2025, and there were no more rate cuts, and it worked in soothing the rattled nerves of the bond market, and mortgage rates stabilized.

But the bond market has remained on edge, leerily watching the Trump administration’s all-out determination to impose its will on the Fed to cut rates by a lot, despite accelerating inflation.

There are two more inflation measures to be released before the Fed’s September meeting. And they’re not going to be pretty. But the Fed, under enormous pressure to knuckle under, may cut anyway, regardless of what inflation does.

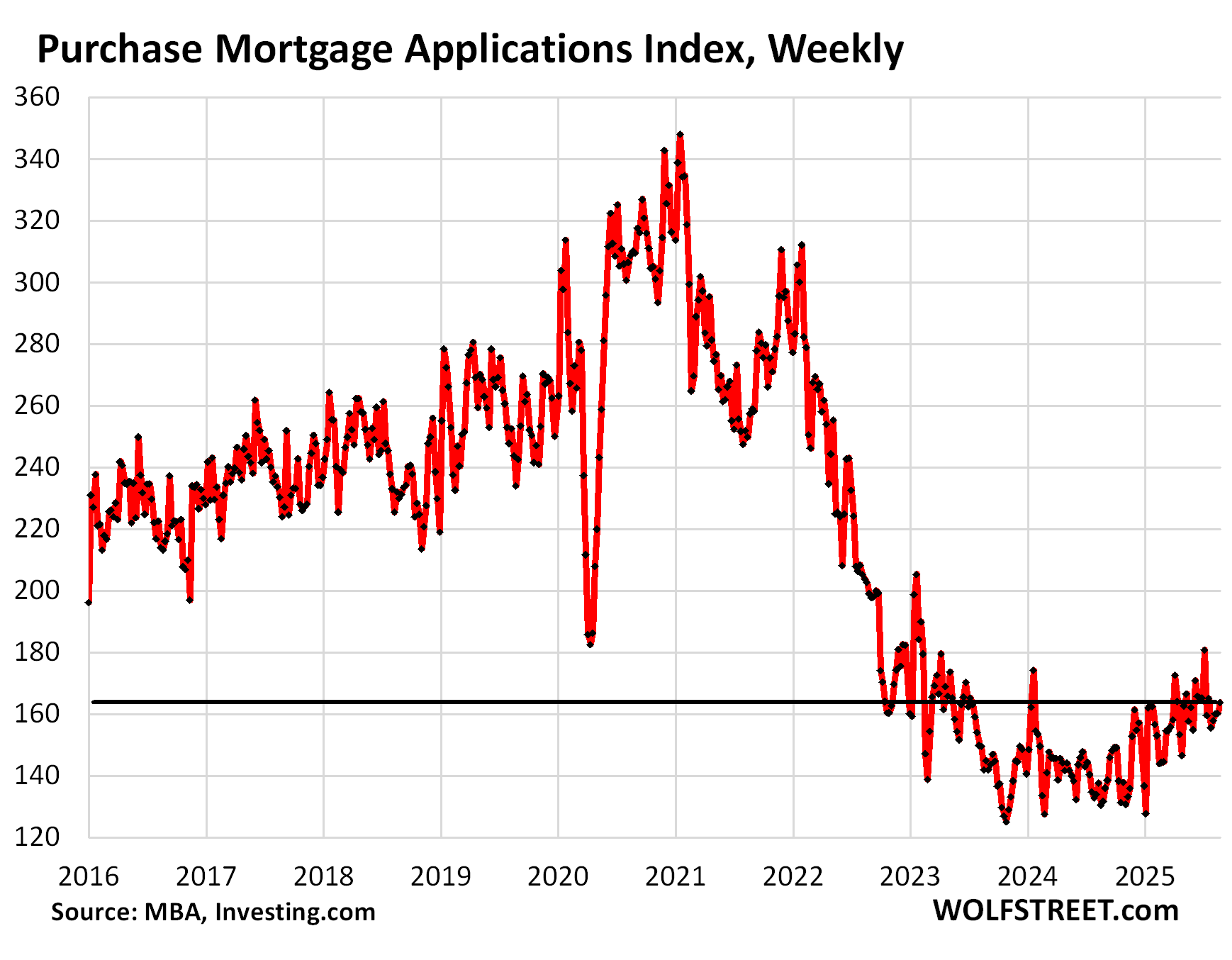

Mortgage demand remains in the deep freeze.

Mortgage applications to purchase a home were still down by 30% from the same week in 2019, and have been in the same range all year. In the latest week, they ticked up a hair, but were lower than they’d been a month ago and two months ago, according to MBA data today.

Mortgage applications have been wobbling along very low levels, showing that demand for mortgages along with demand for homes remain in the deep freeze, after prices exploded between early 2020 and mid-2022.

These too-high prices triggered demand destruction on a historic scale, a fundamental economic principle. And that demand destruction is now showing up in prices in many markets:

- 21 bigger cities where condo prices dropped 12-26%

- 12 bigger cities where single-family home prices dropped 10-23%.

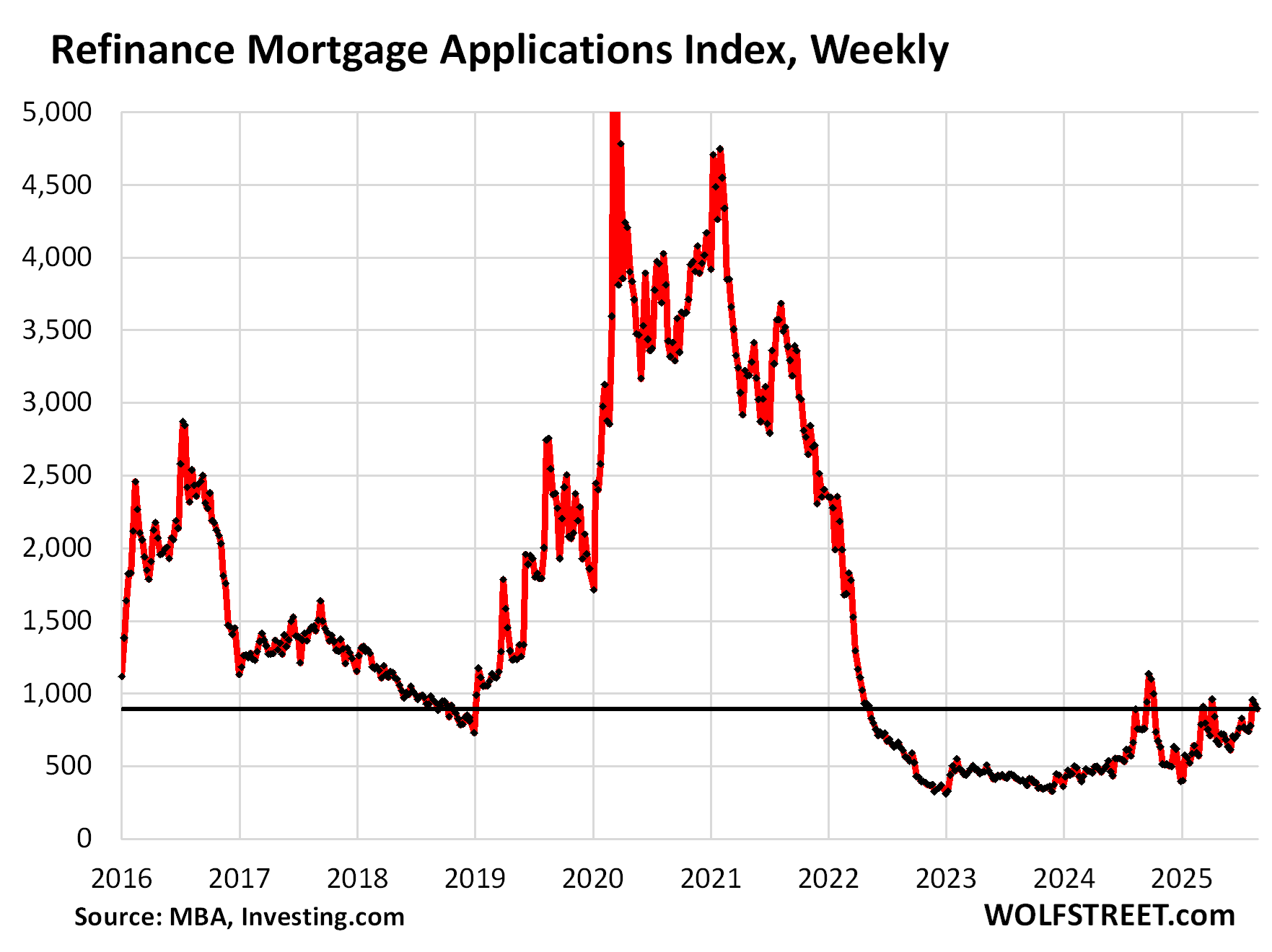

Mortgage applications to refinance a home dipped a hair for the second week and were down by 65% from the same week in 2019. They also have been hobbling along very low levels since early 2022.

But homeowners still want to refinance mortgages for various reasons, and so some refinancings are still happening despite the higher mortgage rates.

Many homebuyers remain on strike.

This buyers’ strike, which started in mid-2022, has now completed its third year. They’re waiting for prices to come down, they’re waiting for their household incomes to rise, and they’re waiting for rates to come down.

Some of them are already homeowners, so they don’t put their homes on the market either.

And others are renters, and in most markets, it’s now far cheaper on a monthly basis to rent a single-family home than to buy an equivalent single-family home – another distortion coming out of the price explosion between early 2020 and mid-2022.

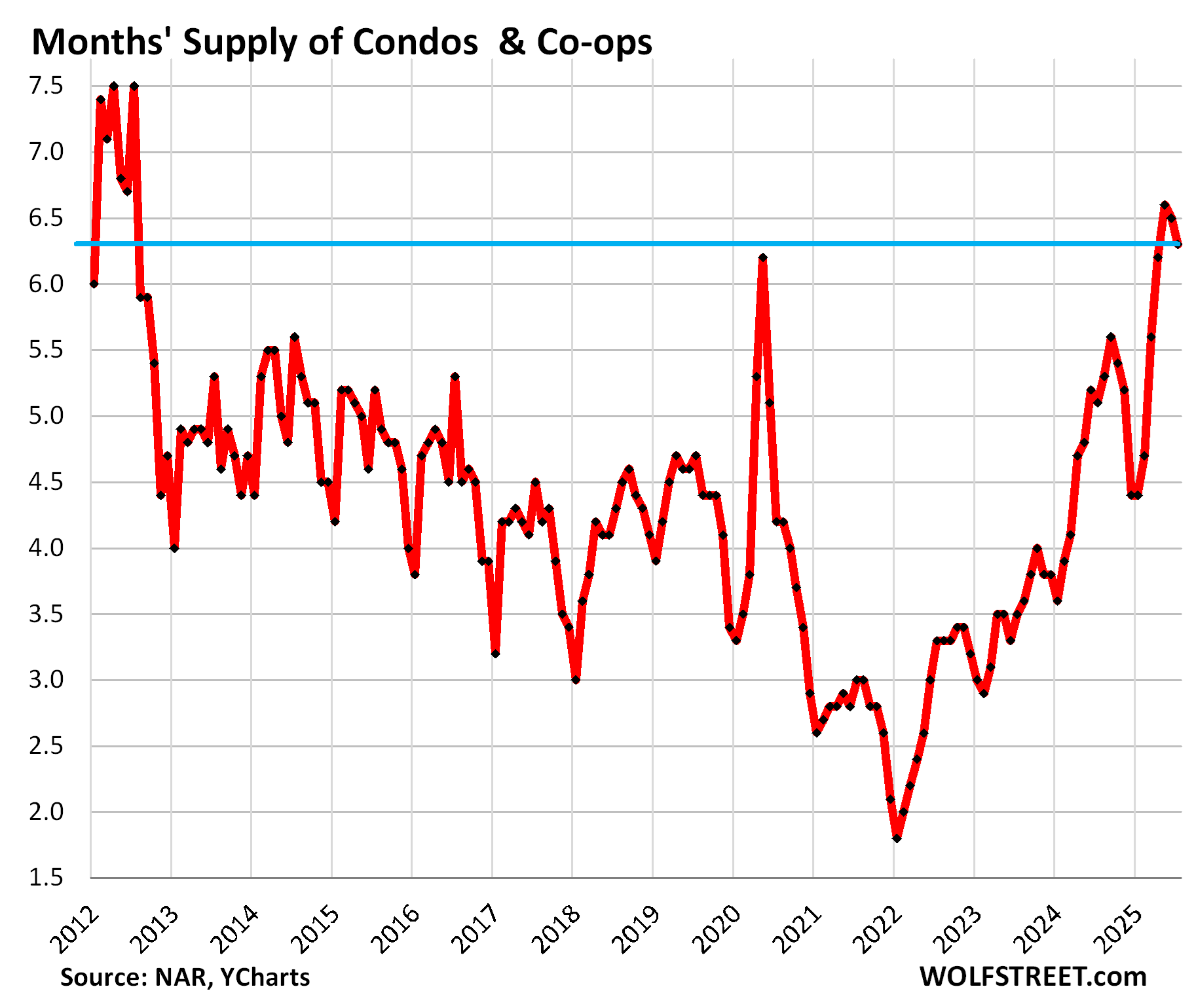

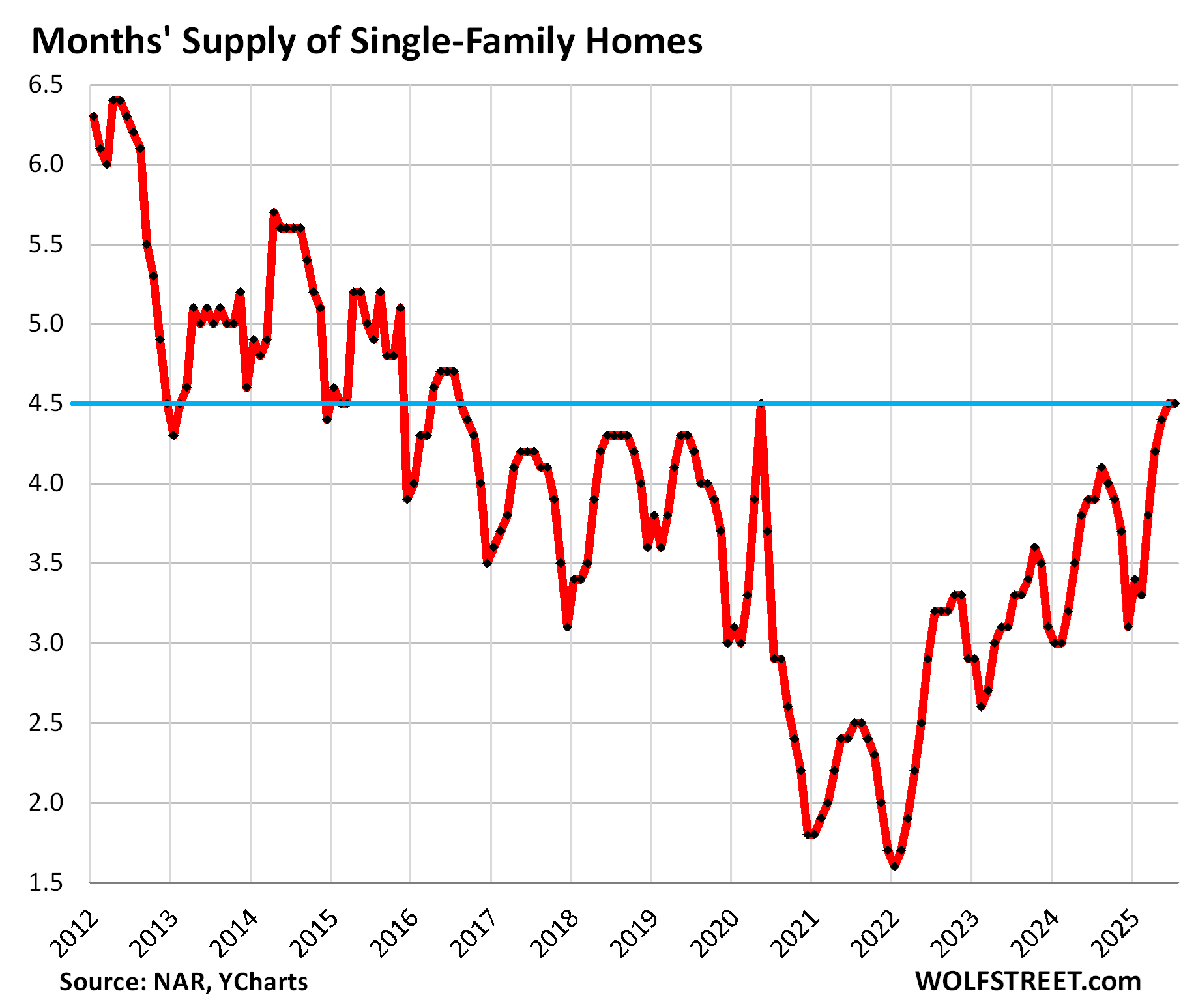

But supply has surged.

Over the past three months, highest supply of condos since the end of the Housing Bust in 2012 (data via National Association of Realtors):

Highest supply of single-family homes since Lockdown May 2020 and before then since mid-2016.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

LOL….So much for date the rate but marry the house…what if your data turns out to be more horrible every time and the one you married is wayyyy overpriced?

No doubt, still plenty of desperate RE agents will tell the less informed potential buyers to squeeze into a house now and point to the upcoming short-term Sept rate cuts to proudly predict mortgage will cut real soon…fool me once….

Thanks for this. In Canada, the local taxes have skyrocketed and I’m now paying monthly for local taxes what I used to pay for a mortgage 20 years ago. Although they are claiming it’s only a 4% increase, math suggests with all of the add-on levies it’s more like 12%.

Insurance has also gone way up

Not sure if America has the same issue but it maybe useful to consider mortgage rates plus city taxes plus insurance to consider affordability compared to wages.

Feeling so badly for my kids who will likely never own a home.

I completely understand that frustration. What you’re describing with the ‘4% increase’ feeling more like a 12% jump is happening here, too. The way property taxes are calculated can make it feel deceptive. It’s not just the advertised tax rate that matters, but also the increase in your property’s assessed value.

In the US, as home values have gone up significantly, even a flat or slightly increased tax rate can result in a much higher bill. On top of that, new local taxes or “add-on levies” you mentioned are a thing here as well. They can be for things like new school construction, road repairs, or other municipal projects, and they get added to your annual property tax bill, making the true increase in your total cost much higher than the simple percentage the local government might be advertising.

There has been destruction of demand, but there also must have been destruction of supply given prices haven’t dropped much yet. Today’s elevated supply statistics aren’t that meaningful if sellers are willing to let an overpriced house sit on the market for long periods without serious buyer interest.

There are lots of potential sellers, but are they motivated yet? It might take a recession to tip prices.

A recession? We need a full fledged depression with gigantic unemployment in order to flush this turd away. We need to have everyone’s hopes and dreams shattered beyond repair. Hopelessness and despair is the only thing that will fix this mess.

True but it’s be so sad. Powell really screwed the housing market for all.

As much as I dislike central bankers and Powell in particular they don’t have as much control as people like to think. This is (was) a good old fashioned speculative mania. Fed stimulus only works when the market willingly goes along for the ride.

Anon is right…but historically the Fed’s job was to take the (LSD-laced) punchbowl away, not prostitute currency stability in order to facilitate perpetual fiscal deficits.

55 years of fiscal failure (perpetual deficits) have more or less put the Fed into a nightmare box…but many, many, many times during those 55 years, the Fed could have short-circuited DC’s perpetual debt machine.

@Anon:

“As much as I dislike central bankers and Powell in particular they don’t have as much control as people like to think.”

I don’t agree with you. There was no need for Powell to buy trillions in MBS when housing market was on fire with bidding wars and crazy price appreciation.

This is all the doing for Central Banks.

You’re missing my point. Powell should not have bought MBS because it stoked a psychological mania but the bond market clearly thought that it was a non issue and bond buyers were willing to accept low yields even in light of everything that was going on.

What Powell can not do is suppress a revolt in the bond market. If the bond market decides they don’t like QE, because it’s inflationary, or for any other reason, bonds will sell off and it won’t work. In the same way that the 2024 rate cut actually increased mortgage rates.

The central bank can not overrule the market, they can try to flip their little switches here and there but ultimately they are not in control. To think that some stupid bureaucrat like Powell really could trick the entire world into paying more for treasuries than they would have otherwise is kind of laughable if you think about it.

And it will come to pass as a result of President Trump’s policies.

A slow, relentless multi year downward grind is also possible…

Bobber

“must have been destruction of supply given prices haven’t dropped much yet”

The last two charts are supply. Have a look.

And prices are coming down hard in quite a few markets:

The 12 Bigger Cities with the Biggest Price Declines of Single-Family Homes (-10% to -23%) through July

Condo Prices Already Dropped by 12%-26% in 21 Bigger Cities through July. Condo Bust Takes Shape

Sellers are still delusional and think they should be compensated for the hard work of sitting on their asses with double digit appreciation. They will accept the reality eventually, recession or not. A recession would be a nice bonus though.

Delusional and entitled, and with the nature of how slow housing market typically moves, it just further emboldens them to take the position much longer.

“They will accept the reality eventually, recession or not. A recession would be a nice bonus, though.” I have my doubts if this will be the equalizer that will get the market right with a huge correction or crash. I am not naive enough to think this admin or FED wouldn’t try to pull out every trick under the sun and maybe some tricks not so conventional to ensure home prices won’t correct down too much… Time will tell, and I would be more than happy to be wrong about this one; a 30% to 40% correction in SoCal would be refreshing to withness.

A lot of places have already corrected more than 20% and FED did nothing to prop these markets.

I see home prices going down in general for the society.

All the essentials of lives have been financialized due to FED’s financial repression. The common people is suffering because of this.

That sounds about right Bobber, I think supply is definitely up but sellers are willing to delist rather than sell at lower prices, so effectively lowering supply rather than lowering price. Clearly demand is lacking, and if it doesn’t pickup with the help of lower mortgage rates, prices will continue to be pressured down. If a recession hits, more sellers will need to sell rather than delist, demand would drop even further, and we could finally see an accelerated decline in prices. I still believe the housing market has potential for another run up in prices, but that would only happen if mortgage rates drop and we avoid a recession.

What a bold homebuyers gets under these conditions is “location and choice”. When rates drop you get bidding wars on less desirable properties. A bold person can re-finance.

That’s precisely what brokers have said for three years, and rates haven’t dropped enough to refinance, and so people that followed that advice are stuck with their high mortgage payments and with their high price. They married the high price and they married the high mortgage rate, while they thought they were just dating.

Yep, and I don’t think the power of cycles is given enough run. There was a long period of time, and I’m talking around 25 years, where rates were low. This was, “The low interest rate period,” before the 80’s, which was a, “High interest rate period of time.” The next, “Low interest rate period,” just wrapped up as inflation said, “Here I am,” in 2021, 2022, and 2023.

Any thoughts of anything close to 3% mortgages again any time soon, (certainly not in the next 6-8 years), is folly. This is not according to me, it’s according to the cycle.

For those of us that have difficulty discerning sarcasm from “Realtor®️ speak” it would be helpful to add a /s or [SARC] tag, and/or maybe a /r or [REALTOR] tag after you write stuff like this.

I can’t tell is I’m supposed to be laughing at your joke, or rolling my eyes. I’ll boldly do both for you — RMEL (rolling my eyes laughing)

Melanias meme coin went from a high of 12 dollars to 12 cents…Trumpets from 65 to 8 dollars and his golden clown shoes are currently sold out…what an empire but taxes have to go up eventually and when the AI bubble pops, the retail folks won’t understand that all bubbles pop, reality included. Buying your own debt is like incense, never ends well but the elites did it anyway for power….

😲😲😲

Your city, Wolf – that lovely (?) place called San Francisco just made it to # 4 of the MOST EXPENSIVE cities in the world, according to

Visual Capitalist. Wow.

It’s surprising, in a way, how many cities from Switzerland made the top 15 list.

Enjoy your expensive lifestyle, whether you mean for it to be that way or not.

Did you just wake up to this? 🤣

What’s expensive is housing. But incomes are very high too: minimum wage of $19/hr, median household income for married couples is $200K (Census Bureau).

Housing is very expense but 16% less expensive than it was at the peak:

What I fear is that the Fed will try to “engineer” a way out of the housing bubble they helped create.

Some new form of QE possibly? Some games with Fannie and Freddie?

You know they always have “to fix it “, because they think they can.

Fed hubris knows no bounds but I don’t think another round of QE will play all that well considering the disaster that was the last one. The bondholders are not going to sit there and wait to get rug pulled again. That’s the kind of thing you can only do once.

I absolutely would not put it past the federal government however to just make it illegal to foreclose on anyone or bail out bagholders in some other way. It’s a pretty safe bet actually. Especially with this admin. Trump thinks if he yells enough we will get 1% rates and it will unleash a boom.