Subprime is, as always, in trouble, which is why it’s subprime – high-risk-high-profit auto sales & lending that can entail steep losses.

By Wolf Richter for WOLF STREET.

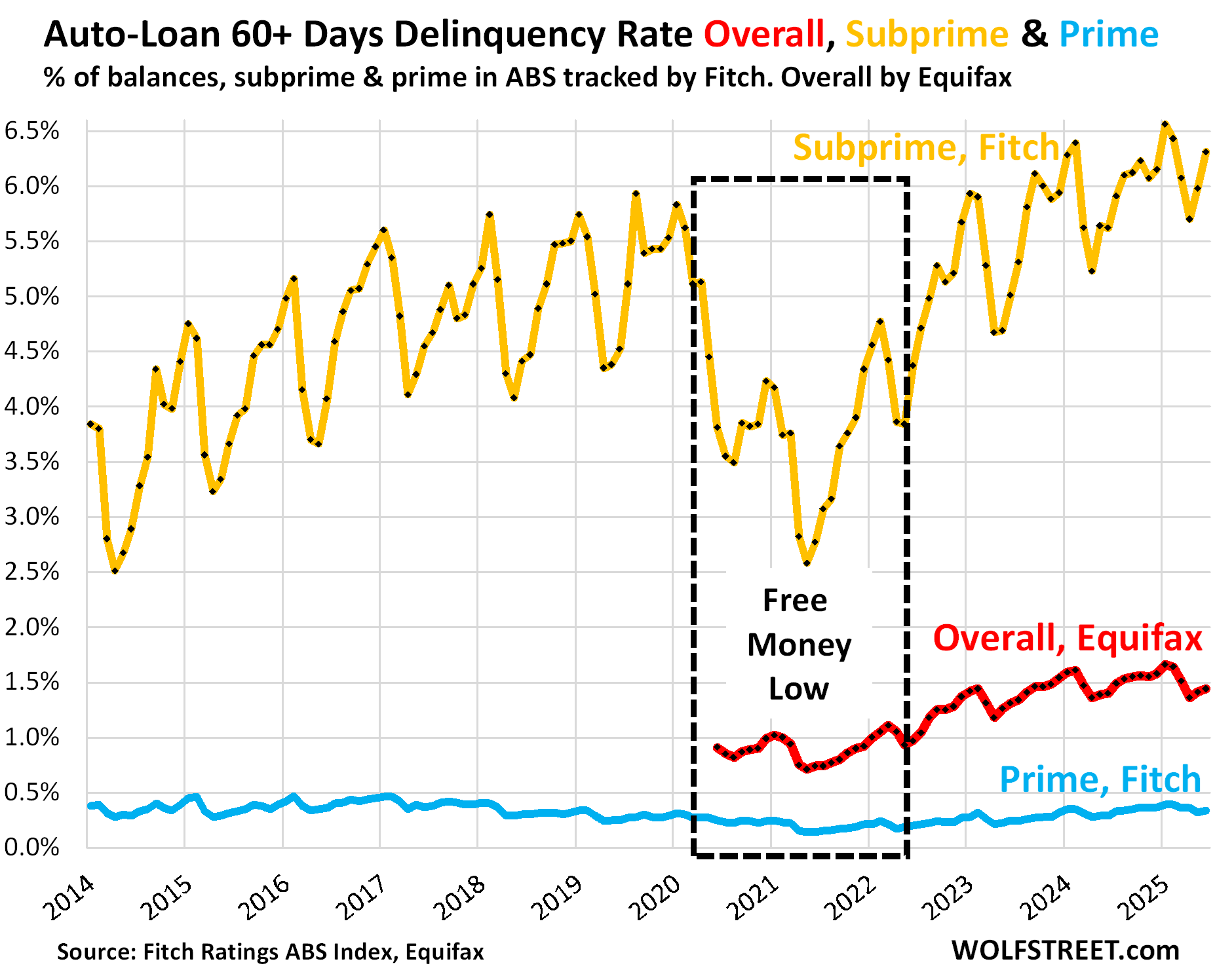

To depict how consumers are handling their auto loans and leases, we look at three delinquency measures: the 60-plus-day delinquency rate for all auto loans and leases, including subprime, reported by Equifax today; the 60-plus-day prime delinquency rate and the 60-plus-day subprime delinquency rate, both reported by Fitch.

The 60-plus-day delinquency rate for all auto loans and leases ticked up along seasonal lines to 1.44% in June, from 1.41% in May, and from 1.40% in June a year ago, and was well below the seasonal highs over the winter that had topped out at 1.66% in January, per Equifax data today.

During the Free-Money era of the pandemic, delinquency rates had dropped below 1%. But the monthly Equifax data that is available doesn’t go back further than the low point of the Free-Money era and therefore lacks the comparison to the pre-pandemic normal years (red in the chart below).

Prime-rated auto loans are nearly always in pristine condition. The 60-plus day delinquency rate of loans that had been rated prime at the time when they were originated ticked up to 0.34% in June from 0.32% in May, and from 0.29% a year ago, and were well below the winter high of 0.39% in January, according to Fitch, which rates asset-backed securities (ABS) backed by auto loans. Even during the Great Recession, the prime delinquency rate maxed out at only 0.9% (blue in the chart).

Subprime is always in trouble which is why it’s “subprime.” Fitch’s subprime 60-day-plus delinquency rate rose to 6.31% in June along seasonal patterns. The seasonal peak was in January at 6.56%, an all-time high. Compared to a year ago, the delinquency rate was 69 basis points higher (gold in the chart).

Subprime means “bad credit” – a history of being late in paying obligations, or not paying them at all. It does not mean “low income.”

And subprime is just a small specialized part of auto lending: Of all auto loans and leases outstanding, only about 14% were rated subprime and deep-subprime at origination, according to Experian data.

Subprime lending has its own ecosystem. Nearly all subprime auto loans financed the purchase of used vehicles, mostly older used vehicles sold by specialized subprime dealer-lender chains, or financed by specialized subprime lenders. Subprime deals come with very high interest rates and very high prices on their vehicles. It’s a specialized high-risk-high-profit part of auto lending.

Lenders package these subprime auto loans into ABS and sell the bonds to pension funds and other institutional investors that buy them for their higher yield. The lowest-rated slices of the bonds take the first losses, but also offer the highest yield. When things go wrong, they can get wiped out quickly. Their job is to protect the highest-rated slices of these bonds. So when losses occur, they’re spread across investors that got paid to take those losses, not banks.

PE firms got into this subprime dealer-lender business, and a few of those chains collapsed when interest rate rose. Publicly traded America’s Car-Mart [CRMT] got hit too, and its shares have plunged by over 70% and joined our imploded stocks. So subprime is not for squeamish investors.

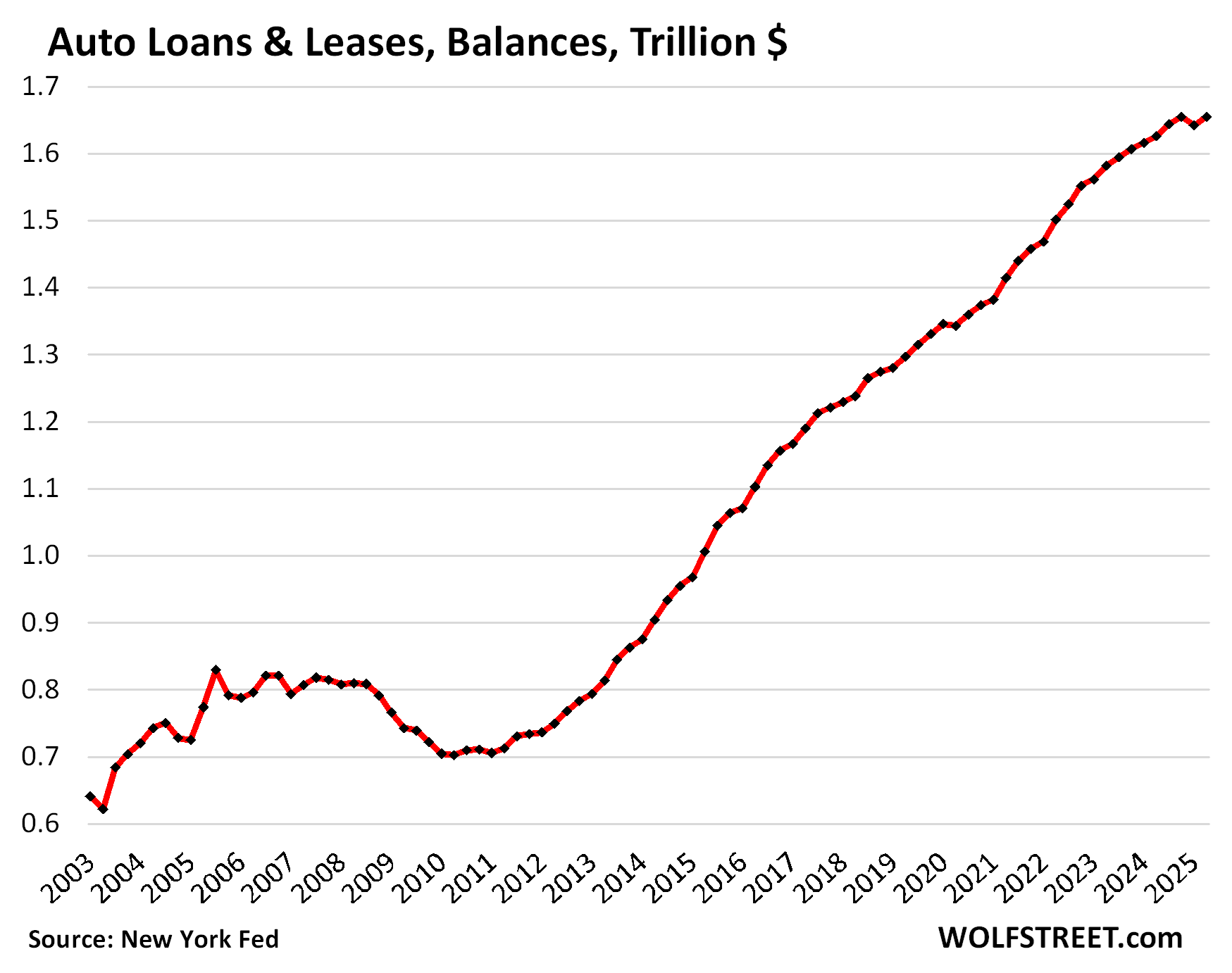

Total balances of auto loans and leases for new and used vehicles rose by $13 billion in Q2, after falling by $13 billion in Q1, and is back where they’d been in Q4, according to the New York Fed’s report on consumer credit.

The reason auto loan balances rose 25% since 2019 is because prices spiked from 2019 through mid-2022, not because more people are borrowing to finance purchases – they’re not.

The CPI for new vehicles has surged by 21% and the CPI for used vehicles by 34% over the same period. Those price increases caused balances to rise since 2019.

But the number of accounts of loans and leases peaked in 2019 at over 90 million accounts and then began to decline, in part due to the plunge in new vehicle sales amid the shortages in 2021 and 2022. It bottomed out in 2022 and has since then inched higher.

In June, the number of accounts remained at 87.1 million accounts, up a hair year-over-year, but still down from the peak in 2019, according to Equifax data today.

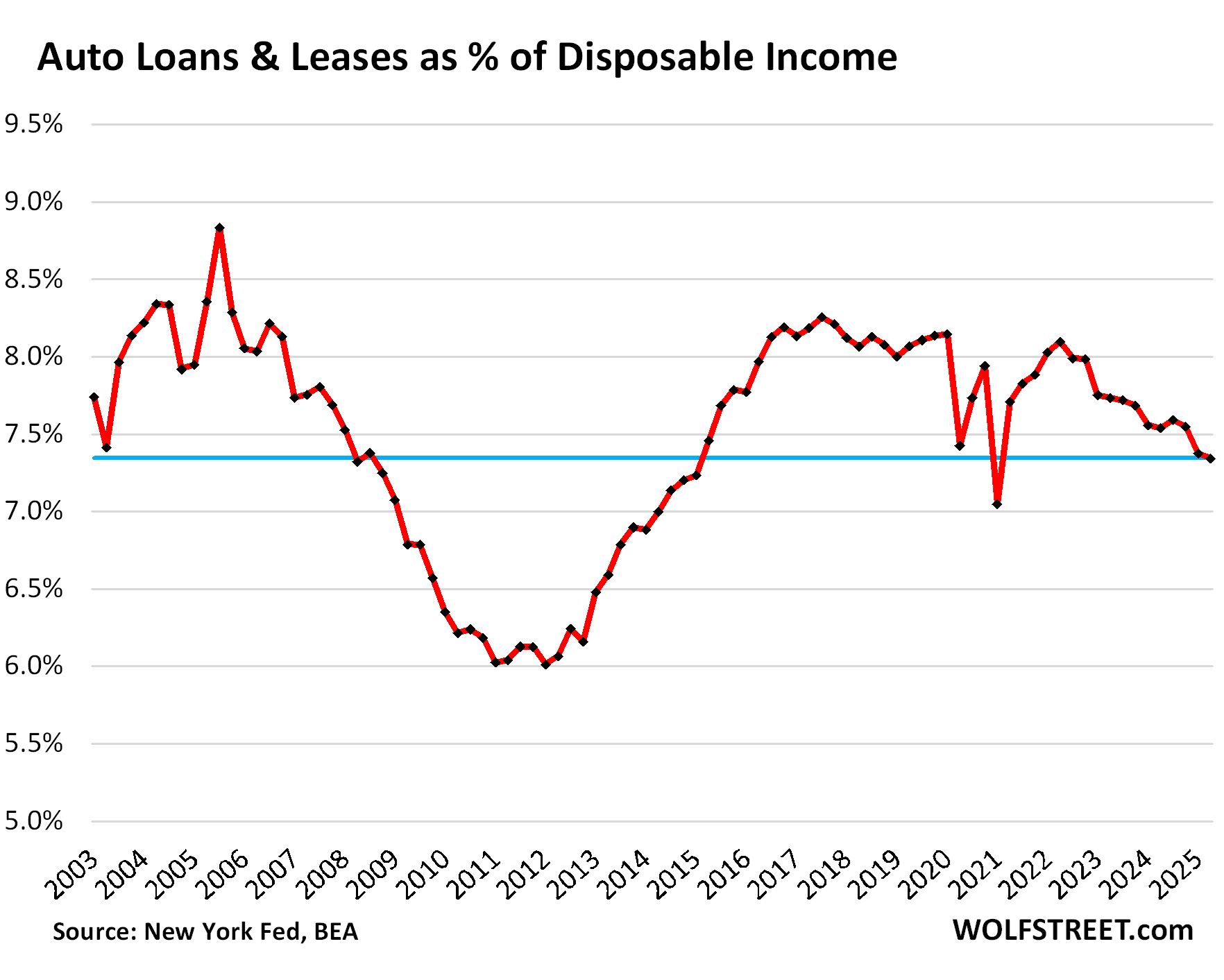

The burden of auto loans and leases. Debt-to-cash-flow ratios are classic measures of borrowers’ ability to deal with the burden of their debt. With households, a metric of cash flow is “disposable income,” which represents the cash households have available to spend after payroll taxes.

Disposable income excludes capital gains. It’s income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

Disposable income rises with higher incomes at individual households and with more people working and making money (population/job growth):

- QoQ: disposable income +1.25%, auto debt: +0.8%.

- YoY: disposable income +4.5%, auto debt: +1.8%.

With auto debt rising more slowly quarter-over-quarter and year-over-year than disposable income, the debt-to-income ratio declined (improved) to 7.3%:

Turns out, the vast majority of our Drunken Sailors, as we’ve come to call them lovingly and facetiously, is managing their auto loans and leases just fine. And subprime is, as always, in trouble, which is why it’s subprime.

In case you missed the earlier parts of the debts of our Drunken Sailors:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Nice charts.

“Automotive Credit Corporation (ACC), a 33-year-old regional auto lender specializing in subprime, has abruptly halted all new loan originations “indefinitely” effective immediately, citing “internal and external financial conditions” and strategic changes, according to an internal memo shared with CDG News.”

Yes, subprime dealer-lenders are tumbling, as mentioned. High profit, high risk.

Thank you, Wolf. No doubt we’re going to see some MSM articles this week touting a “spike in serious delinquencies”, as usual…without any context whatsoever.

The sky is always falling…..thanks for reminding everyone that the situation is still normal.

Situation normal, AFU

”It was the best of times, It was the worst of times.” appears to always have been and continues to be for some folx on either of those extremes,,, apparently now also.

While Wolf and I only disagree on the need for the Federal Reserve Bank as a ”GUVMINT” or at least partially government entity, as opposed to entirely private, as the FRB so clearly serves only the banksters.

I ”like totally dudes and dudettes” support him in his continuing work to bring the very best reporting of all available information to us…

Ha, ha, ha, your observation that the “situation is still normal” recalls the age old “SNAFU” that may or may not accurately describe the more or less constant subprime situation :-))

…well, at least it isn’t FUBAR’d yet…

may we all find a better day.

That Auto loan lease balance chart is really mind blowing. Coming out of the GFC in 2011 it has been more or less a straight line upwards. Nearly $1.7 trillion now?? Another 15 years of this and US auto loans will be bigger than most national economies.

I was in the service side of a Toyota dealership back in the 1990s when the “Peace dividend” temporarily knocked a lot of us out of the defense biz. Back then a Toyota or Honda could go 200k with regular maintenance. Chevy and Fords were done around 150 except for a few of the truck motors. Dodge electronics were shot after ten years no matter what the mileage. In any case, new cars might be financed for a maximum of 60 months, used maybe 36 tops. After that, cash in hand.

Are new cars meant to last a lot longer now and hold some “financiable” collateral value? It seems that the same iron is going to be financed several times by the first few owners – maybe finally free and clear to someone after fifteen or more years of payments?? The first owner takes an 84 month loan, the second a 60, and finally the last guy buys it with 150k on the clock and pays for three more years? Finally in 2040 that vehicle is paid off and gets traded around for cash like we did in the old days?

Love to see the first chart going back to 1995 or know the delinquency rates during the GFC, after all the GFC is what all else is measured.

I’ve posted this many times. The old stuff never changes; what changes is the new stuff, but in long-term charts, it’s hard to see the new stuff.

@Wolf Thanks for the long term chart, I’ve noticed that as the amount people owe gets bigger things “seem” worst to many people my age. When you are in your 60’s and your first car payment was $200 and your rent was $500 40 years ago it is hard to believe that a “kid today” will be able to afford a $800 car payment and $2,000 rent, but as the prime chart shows almost everyone (~99.5% gats a car loan they can afford).

Can’t they foresee this stuff?

Maybe don’t hand the keys over to these risky folks.

It’s like kite surfing in high shark season while bleeding. Not smart!

Unrelated, but the financial media is reporting on the “light” inflation report. The 10 year treasury is up a few bps, so the bond market clearly doesn’t agree.

The stock market and crypto are in a mania with no signs of relenting.

DC:

Doesn’t strike me that way.

What is absurd (not that that term has deep economic meaning) is the enormous market capitalization of the Mag 7.

Because mania.

Agree with you. In this case, it’s retail investors. They truly believe they can’t lose.

I keep hearing people say to invest everything you can into diverse index funds. Nobody seems to care that valuations are the highest since the dot com bubble burst. Everything thinks there is no risk.

That is true, until it’s not.

I wouldn’t say it’s a mania.

But if it fell 25% for 9 months I’d be a very happy camper.

The Shiller PE is very high.

I keep trying to get the new edition of stocks for the long run but I’m not paying more than $5 for a book.

The drunken sailors are about to go down with the ship. The reality is this – if the drunk sailors ran into a massive rock and made a hole in the ship, they could take EVERYBODY down with them. Run (swim) for your lives!

The stock market can still stay elevated for awhile this year. 2026 is going to be the big bust, which may start later in 2025. Lots of chickens will be coming home to roost in a mighty unpleasant synergy, oh oh.

I will be really curious to see what happens to crypto in this coming stock market downdraft. I’ve always thought it a scam, but when things get propped up artificially by the powers that be and even by the latest edition of our federal government (to call it that), it seems less predictable. It would be normal to expect crypto to collapse too when the music stops, but these days I’m not sure there is a normal anymore. The delusions of the masses is a potent thing, at least for awhile.

It’s entirely possible that we are entering into a period like Japan’s late ’80s bubble, when asset prices went totally insane. Depending on the metric, P/E ratio of the market was at least 50x, up to nearly 100 on the CAPE/Shiller index.

Perhaps due to bonds funds having performed so poorly due to the Fed’s switch from QE/ZIRP near-zero rates to the 5% region, 401k flows are now heavily weighted towards stock ETFs, especially S&P500 ETFs, but also leveraged-long ETFs like QLD. Since the S&P500 is capitalization-weighted, the higher the Mag7 go, the more of them the ETFs must buy — if they’re 34% of the S&P, 34% of the 401k inflows to those ETFs must go into them, kiting them ever higher — a virtuous or vicious circle depending on your viewpoint. Ironically, the higher they go, the less good they are as long-term retirement fund investments, because they pay essentially no dividends — the only way to get cash from them to pay retirement living expenses is to sell shares, and as more and more 401k holders retire, and their living expenses are driven up by inflation, there will come a point at which the outflows exceed the inflows, selling pressure will begin to start share prices falling, and the more they fall the more the retirees will need to sell shares to pay expenses.

When will we reach that point?

I should have made explicit that if the U.S. stock market follow the Japanese bubbly course, the average P/E could easily double before the ultimate crash.

And also should have noted that in the U.S. we’re only in the mid-stage of the financial games that were played by Japanese companies with, for example, convertible bond issuance. The parallel is in crypto currency plays such as MSTR, and the copycats rushing in.

Japan manipulated their currency to horrible effect.

To give the yen more value. They burned out all their candles too fast.

@Shamus I have been reading a post like yours almost every day for the past 30 years (since I first got an AOL account in the mid 90’s). Almost everybody knows that the overall stock market and overall real estate market is “overvalued” but other than a small number of people who need every penny in the stock market to live and the small number of people who bought real estate with maximum leverage at the top of the market and need to sell few will “go down with the ship” (or even really notice a 25% market correction).

The day is likely to come when the number of retired people who need every penny in the stock market to live will rise to the point where their 401k drawdowns will outweigh the inflows from the employed, especially as AI and off-shoring decimate the middle-manager and professional class.

I have several retired friends whose real estate taxes on their multiple residences total more than $50k/year, and more whose RE taxes must be around $20k or more. On top of that comes rising home insurance bills as a consequence of global-warming-accelerated climate disasters.

Oh so those are the SALT morons.

Subprime lenders have a special place in hell in my book. Lend at 20 plus % interest knowing there is a high likelihood the borrower will default. Repossess, do it again. I’m glad I never have been a position to buy from one of them.

I’m looking for a subprime lender who will loan me money to buy my next bicycle. 🥲 😬☹️

P H P,

Perhaps your comment is sarcasm?

But a good bicycle is not inexpensive. My 2020 Bianchi road bike was $12.4k new; five years ago. Fifteen grand for a top-end bike is to be expected.

Yes, some of the bike shops in the Twin Cities will sell to customers who qualify on credit, with payment plans. This is straight from a shop’s website (where I bought my OTSO gravel bike four years ago):

“Ride Now. Pay Over Time.

Thanks to our special financing* offers, a fantastic new bicycle is within your reach. Increase your buying power, and take home a new bike as well as cycling apparel and equipment today! We offer 6 and 12 month special financing* plans, allowing you to ride now and pay over time.

Applying online is quick, convenient, and secure. Qualified buyers can be approved in minutes! You can also visit us and apply in-store; please bring a valid ID, credit card, and your social security number. As soon as you’re approved, you can start enjoying all of the benefits of special financing.

*Subject to credit approval. Some restrictions apply. Ask for details.”

So, P H P, if you don’t qualify at the bike shop, I’d suggest finding a loan shark who’ll help you out, eh? Or check out some garage sales, you know.

And no, my comment is not sarcasm. That’s how it is these days.

A “good bicycle” isn’t $15,000. Not everyone should be purchasing brand new 911 GT3RSs, either. Your bike shop is no better than these subprime lenders: “Increase your buying power” for a depreciating asset with minimal value over something 3x less expensive; there are plenty of new $5000 or less bicycles that will be 95% as nice as your $15k example when it comes to getting you somewhere; maybe a few watts difference in efficiency.

Trade a few more watts and you’re in the $2000 range, and still more than sufficient as transportation and exercise. Used and you’re saving even more, and still getting a very nice bicycle. Not everyone needs to pay a premium to have the “best” in everything. This mentality + the availability of subprime lending/other sources of living beyond your means is the nasty trick that keeps people captured in the orbit of financial insolvency. For those who have the spare money, by all means, buy whatever you want, but pretending a $15k bicycle is the norm non-sarcastically is silly.

David,

I do not pretend that a $15k bicycle is the norm. That’s why I referred to one at that price as a top-end bike.

But the St. Paul bike shop where I purchased my $5k gravel bike from, which is from a Minnesota company, Wolf Tooth Components, by the way, is not catering to only expensive bikes. They are trying to capture, through financing, the $5,000 bike buyers, and the lower priced entry level bike buyer too.

This is a fairly new trend in bicycle retail. Buying on finance from the shop – just like buying on finance from a Ford dealer. That was the point I was trying to make.

And among my friends, who are mostly ex-racers like myself, yes it is the norm to have a few high-end bikes in your stable. The bike shop in St. Paul where I do all my business, other than buying the OTSO, which is a brand they don’t carry, sells and services bikes in the mid-level to high-end. For this shop. $10k on up is their bread and butter. You’d be surprised at the volume and pricing they do. People have and spend money on things they’re into.

David, you are right though. Most people are happy with a Toyota Camry, and they are good cars, for sure. A Camry will get you from point A to point B just like a 911 GT3RS will.

I have a couple of older “base model 911s” that I ride in bad weather. And in the winter with road salt and slush, my gravel bike is perfect.

Maybe I am silly? I’m in my early 60’s, I ride nearly every day, and I put on over 10,000 km riding on the road last year. And hell yeah, after working all my life, I feel blessed that I can afford a 911 GT3RS (both car & bike versions. I drive an older M4 car though).

With the Bianchi, my daily ride of 35 km takes me about 62 minutes. On one of my “base model 911s”, which are indeed 95% as nice to ride as my Bianchi, it only takes a minute or two longer for the same ride. But why go slower than you have to?

Life is short. Enjoy it while you can!

Dude just think about going to the Auto Loan Association. Conference every year, 2003 was a dull affair with cupcakes, 2011, sorta ok, you know they got a karaoke machine.

2025 they have helicopters and models! lol

Good analysis! Do you know where to find delinquency rate of recreation vehicle and luxury vehicle? And the price index of such vehicles?