Consumer spending growth accelerated from low levels. Federal government spending drops for second quarter in a row.

By Wolf Richter for WOLF STREET.

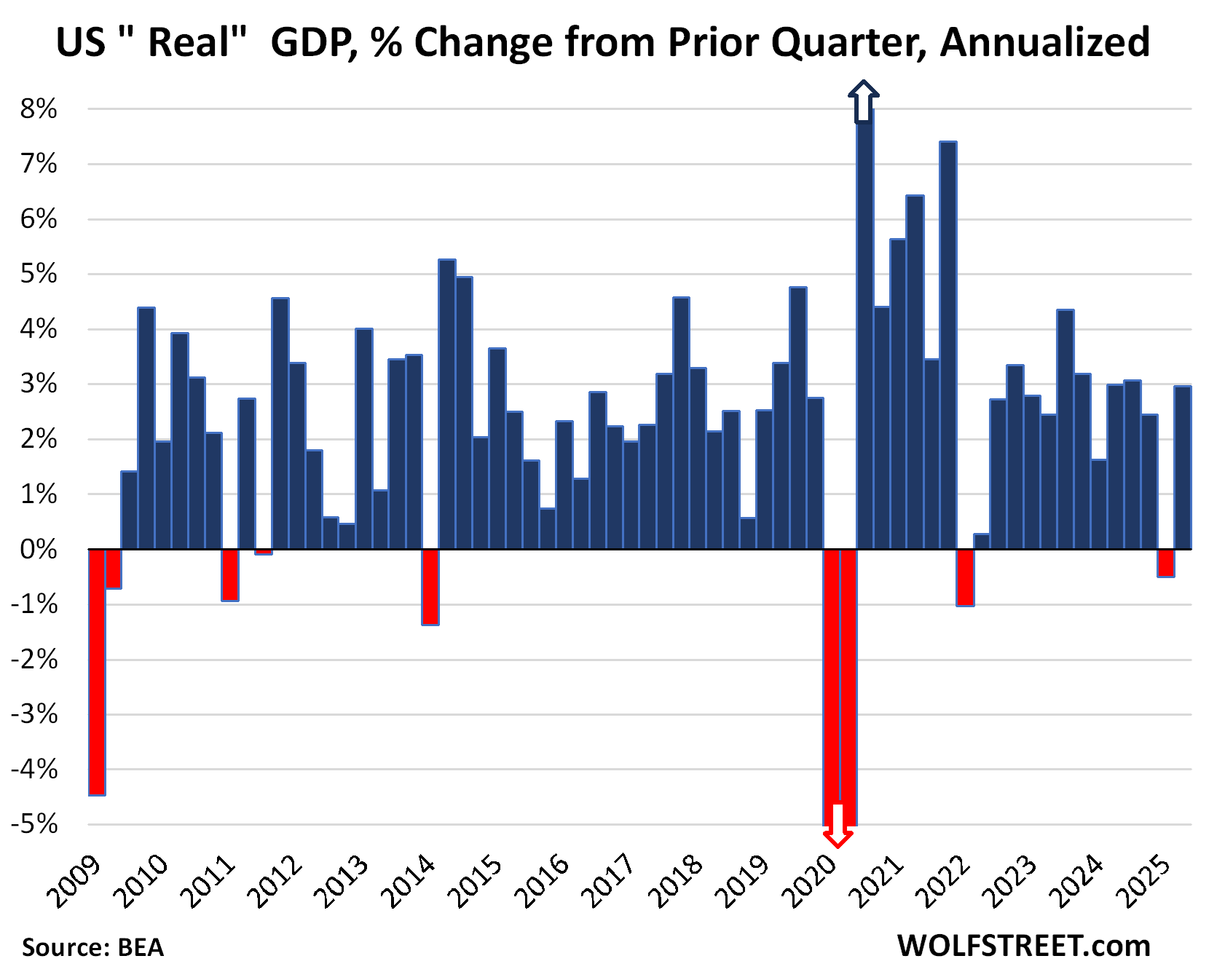

Gross Domestic Product, the broadest measure of the economy, grew by an annual rate of 3.0% in Q2, adjusted for inflation (called “real GDP”), according to the Bureau of Economic Analysis today. This growth more than undid the 0.5% decline in Q1 that had been driven by a record spike in imports on tariff front-running.

Imports deduct from GDP; exports add to GDP. The unwind in Q2 of that tariff-frontrunning import spike in Q1 pushed up GDP growth. But the resulting drop in inventories in Q2 pushed down GDP.

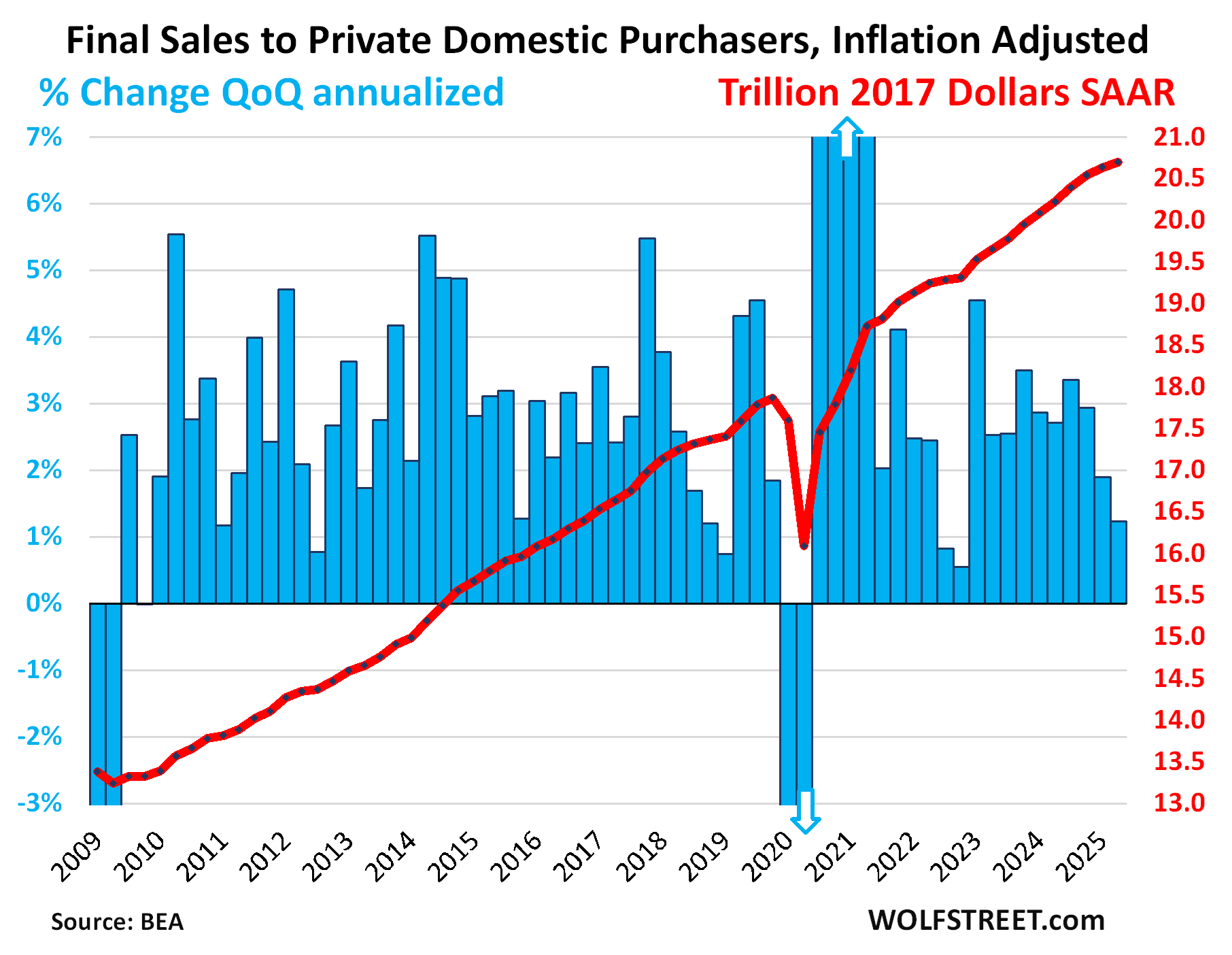

So this is a little confusing. At the bottom of this article, we’ll get to the GDP measure, “Final sales to private domestic purchasers,” that excludes these factors, along with government spending, to get a clearer picture of private demand in the economy. It showed less than spectacular growth, adjusted for inflation, of 1.2%.

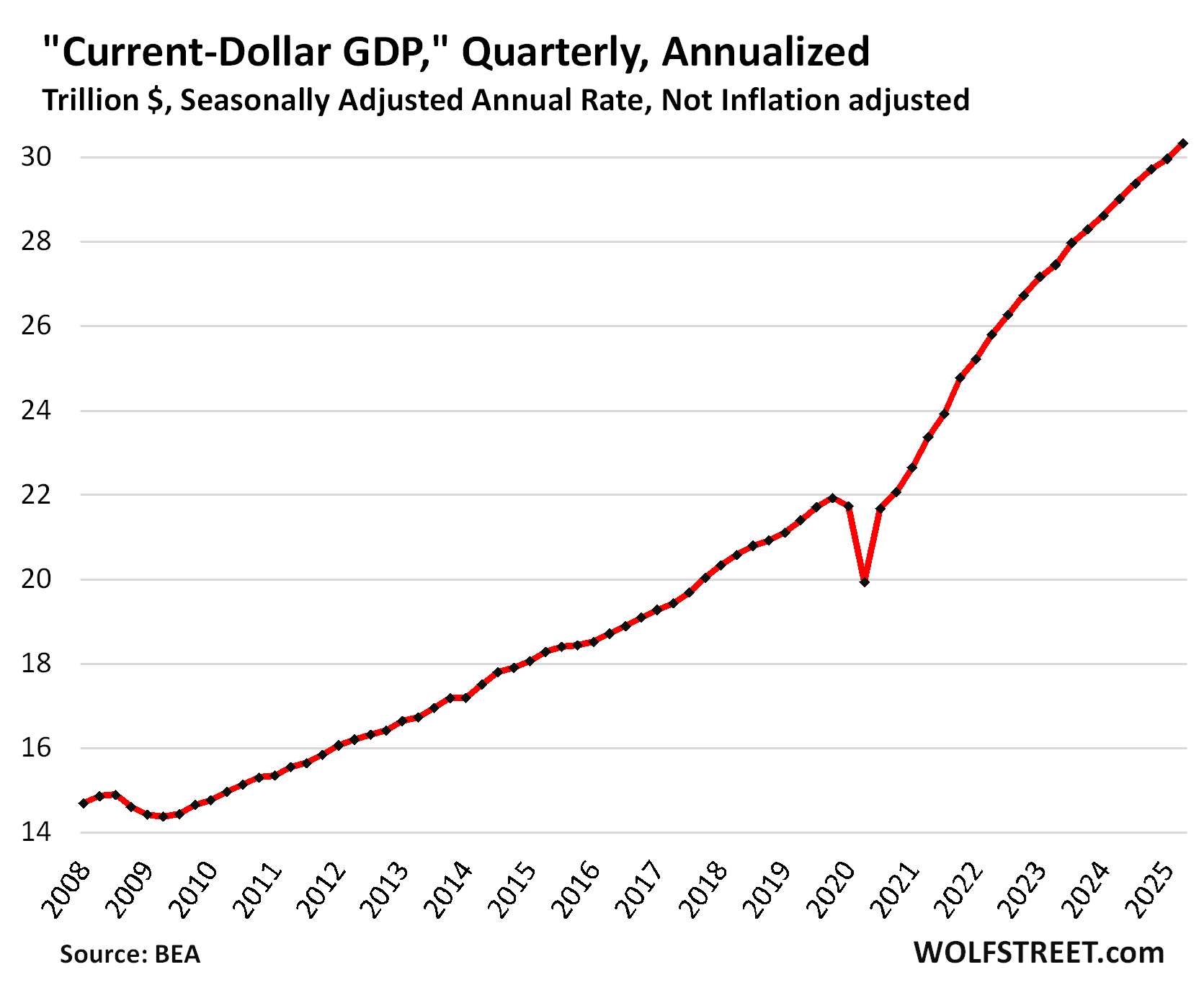

Not adjusted for inflation, “current-dollar GDP” grew by an annual rate of 5.0% to $30.3 trillion.

Also called “nominal GDP,” it represents the actual size of the US economy in today’s dollars and forms the basis for the Debt-to-GDP ratio and similar GDP-based ratios.

The chart shows current dollar GDP, expressed in seasonally adjusted annual rates – what GDP would be if it continues to grow at the pace of Q2 for an entire year.

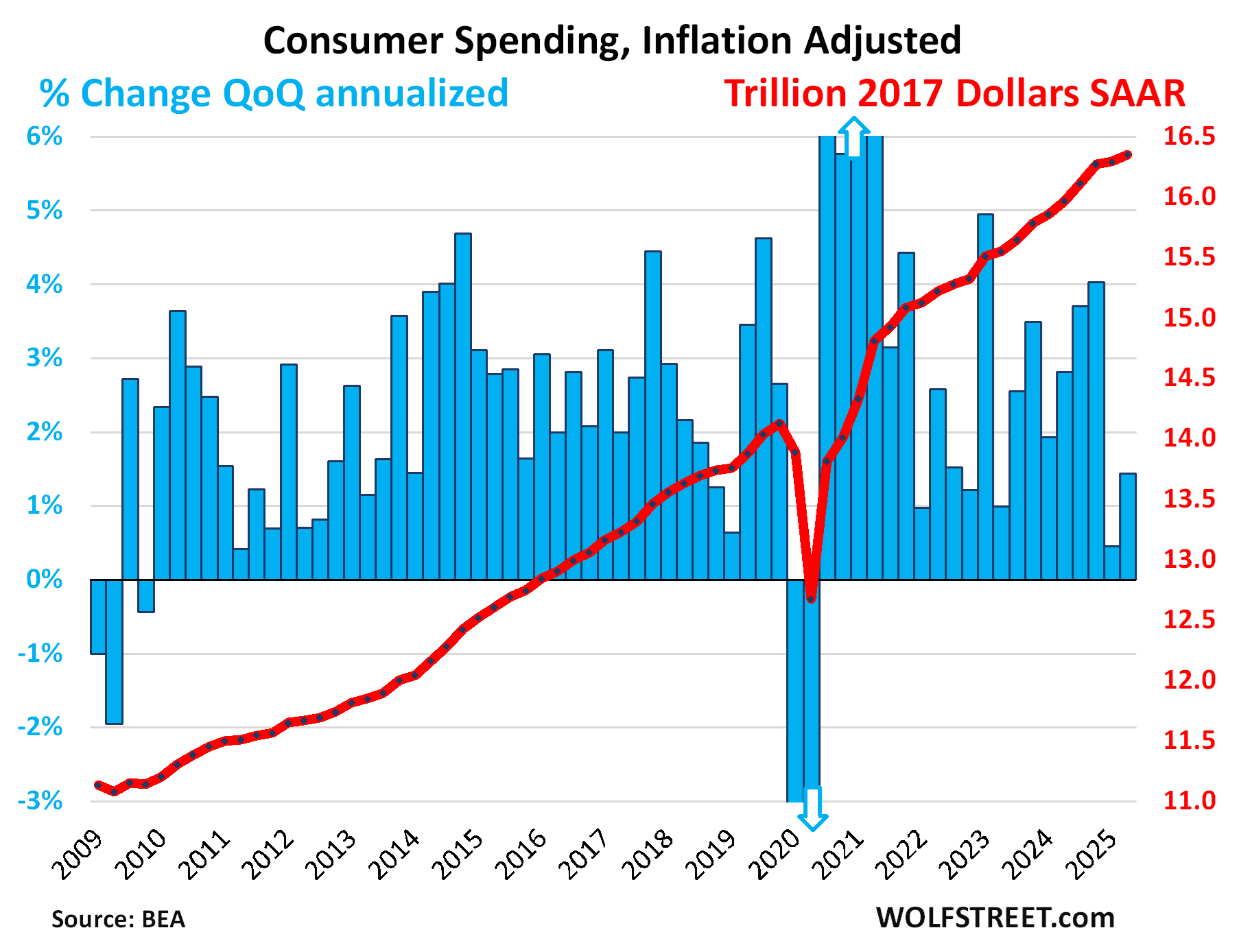

Consumer spending rose by an annual rate of 1.4% in Q2, adjusted for inflation, to $16.4 trillion, accounting for 69% of total GDP.

- Services: +1.1%.

- Durable goods: +3.7%

- Nondurable goods: +1.3%.

Year-over-year, and adjusted for inflation, “real” consumer spending rose by 2.4%.

In Q1, consumer spending along with business activities had gotten “disrupted” by the wildfires in Los Angeles County (nearly 10 million population), and the disruptions showed up in the GDP data, but the BEA said at the time, “it is not possible to estimate the overall impact of the California wildfires on first-quarter GDP.” In Q2, consumer spending growth began to recover.

The blue columns show the growth rates (left axis), the red line shows the dollars (right axis), all in seasonally adjusted annual rates (SAAR):

Massive whiplash from changes in inventory: Gross private domestic investment plunged by 15.6% after the 23.8% spike in Q1. Both quarters were distorted by the massive change in “private inventory investment,” as tariff-frontrunning caused inventories to spike in Q1, and the drawdown of those inventories in Q2 caused inventories to drop sharply.

The plunge in inventory investment deducted 3.17 percentage points from GDP growth in Q2, which is huge.

But in Q1, it had added 2.59 percentage points to GDP growth. These distortions were caused entirely by tariff front-running and have nothing to do with demand in the economy.

The plunge in gross private domestic investment, driven by the plunge in inventories, deducted 3.09 percentage points from GDP growth.

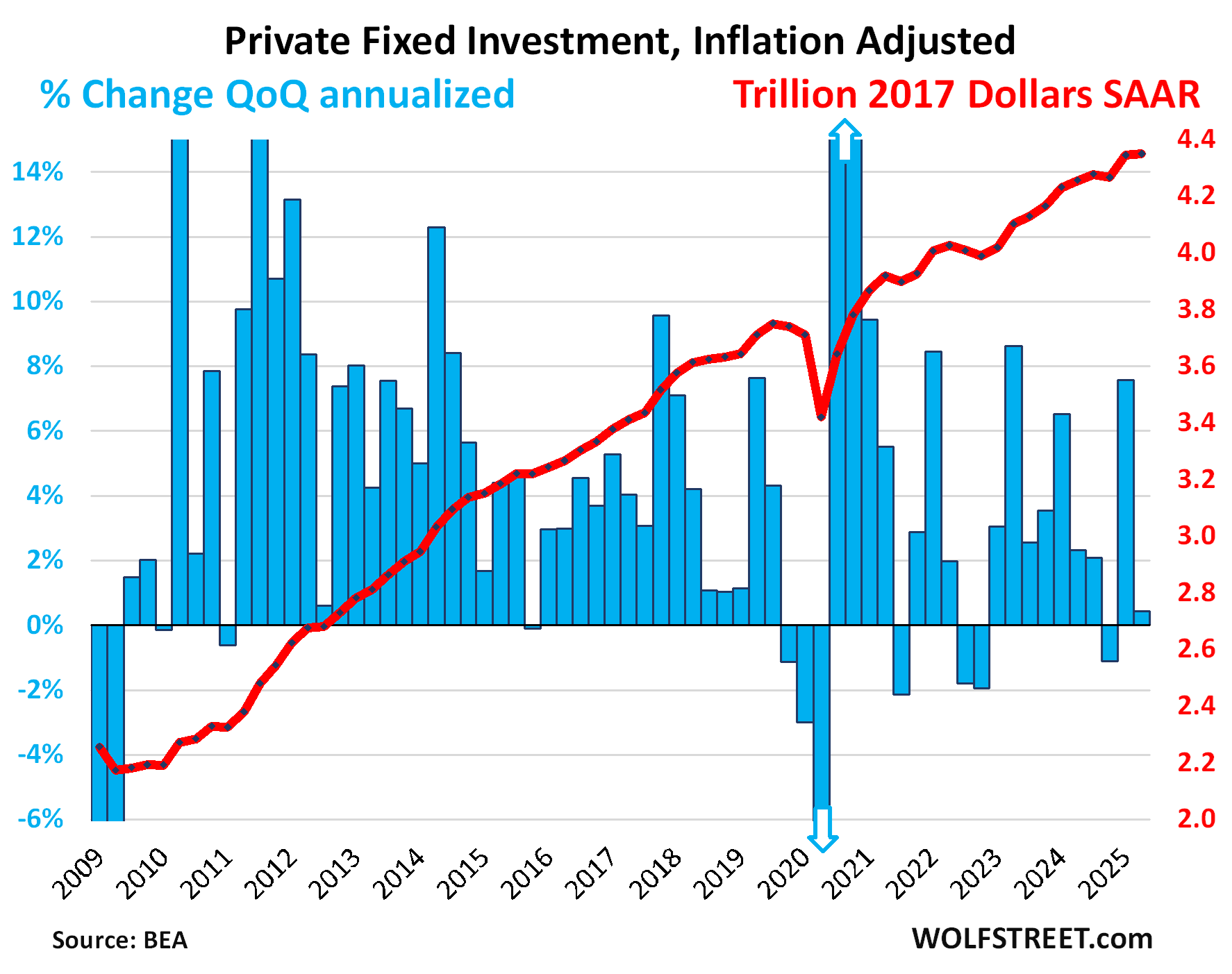

Private fixed investment, which excludes changes in inventory, rose by 0.4% annualized and adjusted for inflation, on top of the 7.6% spike in the prior quarter. Of which:

- Nonresidential fixed investments: +1.9%:

- Structures: -10.3%

- Equipment: +4.8%.

- Intellectual property products (software, movies, etc.): +6.4%.

- Residential fixed investment: -4.6%.

Private fixed investment accounts for 18% of GDP.

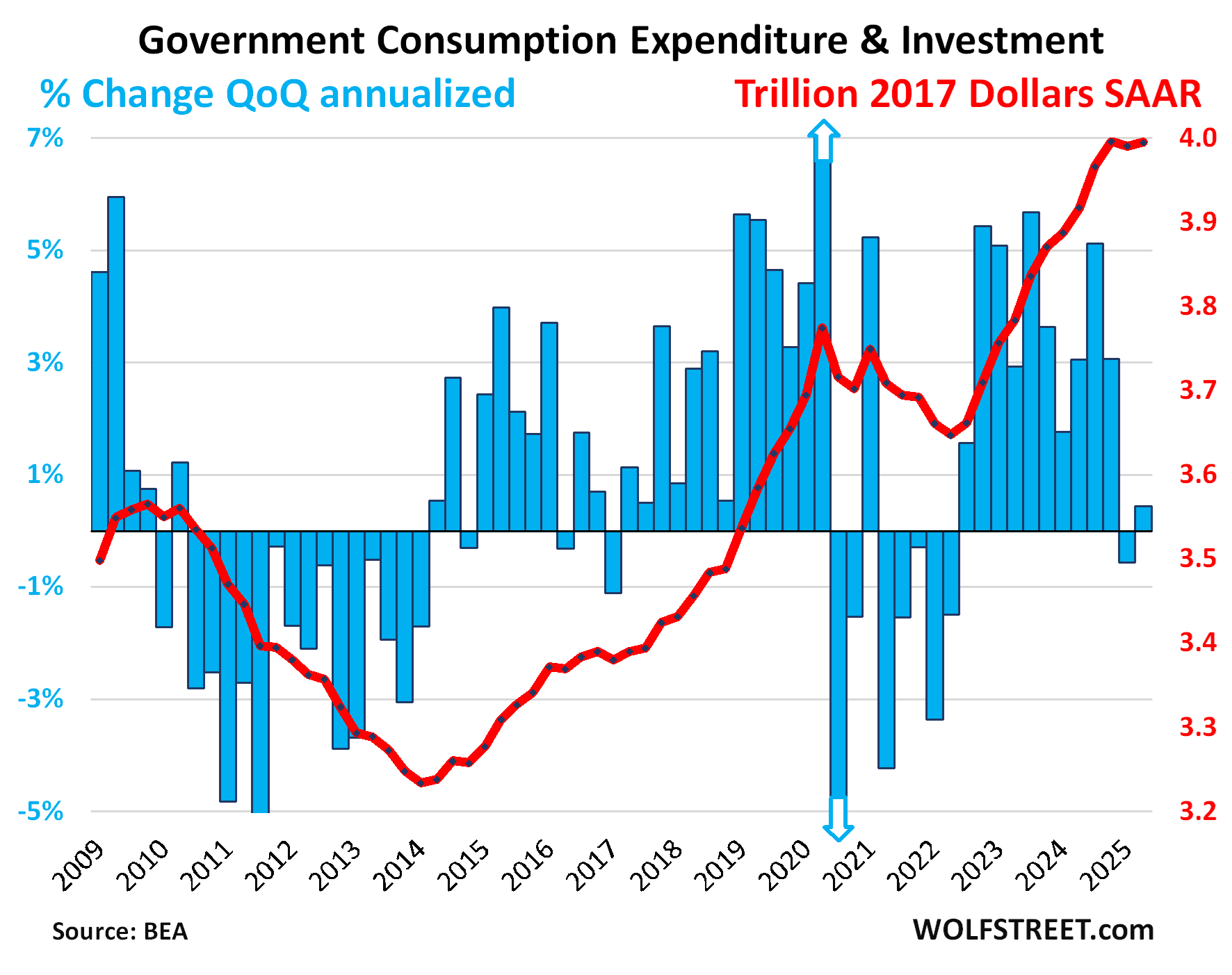

Government consumption expenditures and gross investment rose by 0.4% annualized and adjusted for inflation, after a decline in the prior quarter.

Federal government spending dropped by 3.7% annualized, the second quarter in a row of declines, on a plunge in nondefense spending.

- National defense: +2.2%

- Nondefense: -11.2%

The drop in federal government spending deducted 0.24 percentage points from GDP growth.

This does not include interest payments, and it does not include transfer payments directly to consumers (the biggest part of which are Social Security payments), which are counted in GDP when consumers and businesses spend these funds or invest them in fixed investments.

State and local government spending rose by 3.0%.

Combined, federal, state, and local government consumption and investment accounts for 17% of GDP.

State and local governments account for 61% of total government spending. The federal government accounts for 39% of total government spending.

The explosion of imports unwound.

Imports plunged by 30.3% in Q2 to $3.65 trillion annualized, more than undoing the entire historic tariff-frontrunning spike in Q1. Imports are a negative in GDP.

- Imports of goods: -35.3%

- Imports of services: -5.4%.

Exports declined by 1.8% in Q2 to $2.63 trillion. Exports are a positive in GDP.

- Exports of goods: -5.0%

- Exports of services: +4.4%.

“Net exports” (exports minus imports) improved from the historic all-time worst in Q1, to a negative $1.03 trillion, the least terrible since Q1 2024.

“Final sales to private domestic purchasers,” included in the GDP report, is a measure of the private US economy. It excludes exports, imports, government consumption expenditures, government gross investment, and changes in inventories. It covers about 87% of GDP and presents the core of the private US economy.

Adjusted for inflation, final sales to private domestic purchasers rose by an annual rate of 1.2% in Q2, to $20.7 trillion. So somewhat decent but not exactly spectacular growth.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I love the idea of getting 500 billion in tariff tax receipts on the imports. If they decline, it will be replaced by domestic production which will increase other taxes and keep the production in the US and employing Americans who can invest or spend in their local area. It’s a roll back of the unfettered free trade of the past 30 years.

Doubtful a lot of new jobs will be employing most high tech domestic manufacturing. Probably a whole lot more employed in construction to get that manufacturing going. Just challenging as building out manufactured or finished assembly is one thing but building out the entire supply chain is the unlikely part and of course where China excels. So I think some positive for sure but also need realistic expectations. This won’t be a return to the manufacturing of old, not in a declining(without immigration) and aging population would it be desired.

Tariff tax receipts could decline without an increase in domestic production, if sellers choose other markets and domestic production remains economically, technologically, or culturally expensive.

In that case, tariffs cause the US consumer to lose power in the global economy.

I don’t understand how the “debt out the wazoo” can be increasing at record rates while government spending is down for two quarters. Does that mean that it is interest costs and transfer payments that are growing so rapidly? Or that government spending (excluding interest and transfer payments) is so enormous that two quarters decline in spending does nothing to slow the debt growth?

over 30% of tax receipts now goes into interest payments. It’s a biggie. But it doesn’t go into GDP at all.

WTH!?! Copper just dropped 17%.

OK, found out why. Trump instituted a 50% tariff on copper imports. sucked the wind out of those sails.

Not exactly. Trump stated US would impose a 50% copper import tariff – futures contracts shot up. He then announced an exemption for refined copper. Copper futures dropped bigly.

I lost a bunch of dineros on the drop. CU prices are edging back up again. Commodities follow an asymmetric plot – long-run bet.

Wolf. It would be nice if your charts went back to 2003 so ” Half Empty ” guys like me can see what could happen in the future.

Look at the charts, they include the Financial Crisis. So you can see how that turned out. But nothing bad happened between 2003 and 2007, so you can skip that part. In return, you get better details for the current period. That’s always the tradeoff.

Thank You. If it was back to say 2005 it would show how violent it was. I am so grateful to live through it and experience the turmoil. Young people just don’t know the fear and uncertainty going on then but on the other hand if you didn’t glue yourself to the news you may have not felt a thing. lots of pockets of the country just didn’t see much change, similar to the great depression.

John, don’t worry. Everything will be just fine going forward as our leaders have it under control. I’m old enough to remember black and white tv, Buster Brown shoes and roll up car windows. So I have seen it all and live through it./s

GDP hopefully will start to accelerate in the second half of 2025 after the front running of Tariffs in Q1.

Year 2026 with some of the spend for new manufacturing may start to show up in GDP spend. Overall I am optimistic for USA economy especially vehicle manufacturing.

Yes, would love to see a BYD factory here in the US. Encouraging production here for American jobs is definitely a positive.

.

Wolf,

Great work, thank you.

can you explain more the specifics of imports —–> investment ——> consumption? and it having no effect (apparently on GDP)

i can’t wrap my head around GDP was strong because imports went down… while that is strictly true via the GDP equation, i am trying to think of this logically…. massively increased or decreased imports is generally offset by a big opposite move in investment/inventory…

but the offset is nowhere near 1 to 1.. is it possible to reconcile it all?

i do understand the general concept of subtracting imports.. mostly, consumption that is import is not positive GDP. so you have positive and negative offset.

An import is a sale in the US where the US-cash paid by the importer gets sucked out of the country permanently. Instead of circulating in the US, this US-cash is circulating in China. And that’s permanent.

Changes in inventory — the issue I made a big deal out of in the article — are just a flow measured at a point in time. So it increases in one quarter and as this inventory moves on, it decreases in the next quarter. It’s not permanent and on net will wash out. But imports are a permanent cash suck, all the time every time.

If the U.S. were to target a lower trade deficit, it would slow the permanent outflow of dollars — and in the case of a trade surplus, even result in a net inflow. With more US dollars remaining in the domestic US economy and the US government maintaining higher deficits, could this be more inflationary than be currently think? Or is this dynamic counteracted by increasing tariff revenue effectively “taking out” US dollars from the economy at the same time? Would the U.S. then be able to rely more on domestic buyers, rather than foreign buyers to finance its government debt? Conversely, would a decline in dollar (out)flows to countries like China — whose local demand and growth depends on dollar earnings from trade surpluses — lead to deflationary pressures abroad? – so, maybe a defacto divergence in inflationary cycles between consumption led and export-growth orianted economies?

Wolf – I’ll tell you a secret, but you can’t tell anyone. The reason our GDP grew 3%. Shh, no telling! It’s a little trick called INFLATION.

I sell you ten cookies for $10. You like them.

Next month I sell you ten cookies for $12, being the greedy person that I am, or maybe my costs really did go up.

Was there really an increase in economic output?

It’s PhD level economics. Maybe we should call in the experts to help figure this one out.

🤣🤣🤣 RTGDFA. The 3.0% GDP growth is adjusted for inflation, you goofball. Aren’t you glad you just whispered this into my ear so no one could hear how big of a goofball you are?

Not adjusted for inflation (see second chart), GDP grew by 5.0% to $30.3 trillion annual rate.

you’re hilarious 🤣🤣🤣

FRED just released the tariff revenues collected. The chart looks like a meme stock, lol

https://fred.stlouisfed.org/series/NA000324Q

That FRED chart is quarterly. Q2 = April + May + June. Those were the three months when tariffs took off.

WOLF STREET has been releasing the monthly data for three months, including June almost a month ago, on July 1. My July chart will be released in a few days. FRED is way behind. This is the WOLF STREET monthly chart through June, released by WOLF STREET on July 1:

https://wolfstreet.com/2025/07/01/tariff-cash-is-rolling-in-junes-record-take-spikes-by-20-5-billion-year-over-year/

Hey Wolf! Can you try to speculate on Q3? What could we potentially see in Q3 data based on all this stuff?